Accounting for Inventory

In This Chapter

![]()

- What inventory is and why we care about accounting for it

- Different types of inventory items

- Methods of valuing inventory

- Counting your physical inventory

- Inventory reporting

Businesses come in all shapes and sizes and offer a variety of products and services for sale. When a business creates and sells a physical product, it generally keeps a stock of that product on hand as inventory. A business also might house a supply of raw materials for creating finished inventory. You might resell products you don’t physically stock on-site, or you might need to standardize prices and descriptions for service items. The inventory feature in your accounting software can track all this and more.

In this chapter, we discuss some of the risks and benefits of maintaining inventory. We also offer a breakdown of the various types of inventory items you might be tracking in your business, how the tracking generally works, and how this might impact your financial statements. From there, we move on to the various methods you can use to value your inventory and discuss when and how to perform a physical count of inventory and report on it. And along the way, we explain how your accounting software gives you a huge hand in managing inventory.

The Importance of Tracking and Valuing Inventory

Physical inventory often poses a high degree of risk for small businesses. Let’s say you sell chicken feed to farmers. You have to forecast the amount of feed you need to stock so you don’t run out and lose sales. When the feed arrives, you have to store it someplace dry, clean, and secure from rodents and other pests. You have to be sure to sell your oldest bags of feed first so you don’t get stuck with spoiled product. And you must stay aware of your competitors’ pricing practices so they don’t undercut your prices and leave you with inventory you can’t sell.

Depending on your business, you also might have the stress of borrowing money to fund your inventory. For instance, new car dealers often don’t actually own all the cars on their lot. Rather, they use a mechanism called floor plan financing to borrow money to keep a certain number of cars at the dealership. The longer a new car stays on the lot, the more interest the dealer has to pay on that car. This added cost raises the stakes of maintaining certain types of inventory.

Physical inventory clearly has special requirements: items must be stored, counted, valued, and sometimes financed. Your inventory might be perishable or have an extraordinarily long shelf life, such as metal parts for earthmoving equipment. You might have high-value items you need to track by serial number, or your inventory could be less specific, like piles of cypress mulch you’ll measure imprecisely.

Your inventory might consist of physical items never directly in your possession. In effect, you’re able to leverage someone else’s warehousing and inventory system to offer products to your customers. This approach is often referred to as drop-shipping. Paradoxically, inventory also can serve as an effective means to sell and track services.

Even if your business sells intangible services, the inventory feature in your accounting software can help you streamline accounting tasks. Later in the chapter, we describe how service-based businesses can use a special type of inventory item to simplify data entry and also track sales.

BOTTOM LINE

Knowing how much inventory to keep can be tricky. You want to have enough to fulfill customer requests and maintain an on-hand stock in your showroom so potential buyers can see what you offer. But you don’t want to keep excess inventory that can spoil, nor do you want to spend a lot of money on slow-moving products. The physical inventory counts we discuss later in the chapter enable you to keep tabs on how much inventory is in stock. Over time, your experience can guide you on how much inventory you can afford and how to keep it turning at an appropriate pace.

Inventory Item Types and Setup

If your accounting software offers inventory tracking, you might have a large number of item-type options to choose from when identifying your inventory. The level of control and flexibility you have with regard to tracking your inventory items varies based on your software. In this section, we look at the most common types of inventory-related software issues you’ll encounter along with a summary of other related software features. (We cover how to purchase and sell inventory items in Chapter 6.)

Unfortunately, we can’t provide specific guidance on where to start adding inventory items within your accounting software because almost every program seems to take a different approach. With that said, desktop-based accounting programs often have a Lists or Maintain menu across the top in which you can find Inventory commands. Within cloud-based accounting programs, you might have to look for a Settings command (sometimes represented by a gear-shape icon). Once you find the inventory section of your software, actually adding new items should be intuitive from there.

Stock Items

Stock items are physical goods you keep on hand for sale to customers. Depending on your industry, these could be cans of green beans you take out of the case and put on a shelf or manufactured goods you assemble from raw materials. Your customers might purchase items from a retail location you own, or you might ship everything to your customers. Whatever your product, you’ll need to keep track of the physical count of these items and very likely take certain items off your books occasionally due to shrinkage. The wording your accounting software uses can vary; for instance, Xero uses the term tracked items, while QuickBooks Online allows you to track the quantity on hand.

DEFINITION

Ideally, you’ll sell 100 percent of the inventory items you purchase. However, sometimes unfortunate things happen to inventory. Items break, get stolen or misplaced, or any of a number of things. The term shrinkage refers to these events and the reduction of your stock.

Your accounting software keeps track of the number of stock items you have on hand and notifies you if you try to sell beyond the quantity you have.

Nonstock Items

Nonstock items are the physical goods you sell that are typically never in your possession, or perhaps you house them only temporarily. Often referred to as drop-shipments, you place an order for these items through your supplier who then ships the products directly to your customer.

Your accounting software won’t keep track of any quantities on hand for nonstock items. You can run reports that track the amount of these items you’ve sold, but they won’t affect the Inventory account on your balance sheet because you never actually take possession of the physical goods. Your Inventory account only reflects items you keep on hand or store elsewhere but maintain ownership of.

For instance, you might sell bottles of rare wine that a distributor ships on your behalf. This contrasts with bottles of wine you purchase and cellar in a special facility. The latter would be considered stock items you carry on your balance sheet.

Let’s say you purchase a bottle of wine for $10 and sell it to your customer for $25. You’ll invoice your customer for $25, pay your vendor $10, and pocket a profit of $15, and the vendor will ship the wine directly to your customer (assuming customer’s state permits sales of alcohol by mail).

Assemblies

Assemblies are best thought of as a collection of goods and/or services that go together to make one inventory item that’s sold as a unit. For example, a manufactured product might be comprised of four individual parts and two labor processes to put together those parts. When you create an assembly, you assign a name to the item and then assemble a list of two or more other inventory items (the individual parts for the assembly, which you previously purchased and added into inventory in your accounting software).

In turn, when you sell the assembly, your accounting software takes the individual items out of stock and records the cost of both the parts and labor. One sales price applies to the entire package that comprises the assembly.

Assemblies are typically considered an advanced feature within accounting software, so you might need to choose a desktop-based program to use this feature. The following figure shows an assembly screen from Sage 50. Notice that the active tab is referred to as the Bill of Materials.

Assemblies enable you to sell combinations of inventory items and/or services as a single item.

Assemblies allow you to sell multiple items at once. However, when you create the assembly items, you might need to carry out a “build” step in your accounting software. Building an assembly lowers the on-hand quantity of the individual stock items so you don’t inadvertently try to sell them twice. Physical inventory, which we discuss later in this chapter, can be trickier if certain items on your shelves are earmarked for assemblies you haven’t sold yet. Depending on your business and your software, you also might have the option to “unbuild” assemblies, which restores the on-hand quantities for the individual items that were formerly part of the assembly.

Service Items

Within the context of an accounting program, service items represent services you provide to others. There’s nothing physical to keep count of, but service items can provide a helpful tracking mechanism if you offer two or more types of services. For example, as writers, we offer multiple services at different price points. In our accounting software, we might have service items ranging from Consulting Services, to Freelance Writing, to Technical Editing, all with different prices and descriptions.

Service items help ensure you price services consistently and provide consistent descriptions on your invoices. The following example shows the window in QuickBooks Online you’d use to establish a service.

Service items simplify the invoicing process by enabling you to use consistent descriptions on invoices.

Some accounting programs use the inventory feature for more than just tracking products. For instance, in the desktop versions of QuickBooks, you can add a variety of items, as shown in the following figure. Each of these allows you to streamline some aspect of your invoicing process. In this example, Other Charge allows you to add an ad hoc charge to an invoice. The Discount item lets you calculate discounts on an invoice.

The desktop versions of QuickBooks offer the capability to establish other charges, discounts, subtotals, and special-use items.

ACCOUNTING HACK

You might want to be able to offer special pricing to specific customers. Instead of keeping this information in your head to recall when you create an invoice, your accounting software might allow you to establish price levels. These let you provide automatic discounts to customers when you record invoices. Price levels are typically set at a global level, meaning you’ll establish discounts of, say, 10 percent, 15 percent, 20 percent, etc. and then assign the respective price levels to specific customers.

Physical Inventory Valuation Methods

When you purchase inventory, you exchange one asset, cash, for another asset, inventory, which you hope to convert to cash again by ideally selling at a higher price than what you paid.

The inventory items or assemblies you sell could rise or fall in value. For instance, if you sell sand and gravel, the price most likely won’t change very often. If you sell freshly baked bread, the value of your inventory can drop to 0 within a day or two as the bread becomes stale. A jeweler buying gold for necklaces can pay a different price for an ounce of gold every day—and sometimes even within a given day. Multiply these complexities by dozens, hundreds, or thousands of products, and you can see how critical accounting software can be for tracking your inventory.

You’ll need to keep track of not only how many items you have on hand, but also the current value of the items. Further, when you sell an item from your inventory, the portion of your inventory cost relating to the item you sell is recorded as an expense on your books. When you first purchase inventory, the cost is recorded as an asset, but as you sell items, the cost of the items sold appears as an expense on your profit and loss or income statement. As you might expect, there can be some nuance involved in determining exactly how much to treat as an expense when you’ve bought various items at different times and at different prices. In accounting terms, these nuances are referred to as costing methods.

DEFINITION

Costing methods are used in your accounting software to determine the amount you should record as an expense when you sell an item. You don’t have to use the same costing method for every item in your inventory, but you might find your inventory reports confusing or misleading if you mix and match costing methods for the same type of inventory items.

Depending on which accounting software you use, you might be able to choose from up to four different inventory valuation methods. When you purchase inventory, it stays on your books at the price you paid for it. By “on your books,” we mean the amount you see on your balance sheet in your Inventory account. The amount in the Inventory account reflects the sum of your total current inventory on hand. Your accounting software enables you to run inventory valuation reports that reflect the underlying detail on an item-by-item basis.

You shouldn’t take inventory costing methods lightly, as your choice of method can not only affect the bottom line of your income statement, but also impact the amount of income taxes you pay. With that said, you should follow the matching principle when making this determination, as it affects an expense on your income statement known as cost of goods sold (COGS). Your accounting software typically allows you to mix and match costing methods item by item, but the Internal Revenue Service (IRS) expects you to choose one costing method and use it across the board. Exceptions to this rule are permitted on a case-by-case basis if you’re able to document a valid business purpose.

The matching principle of accounting strives to match revenues and expenses. So when you report the sales price of an item you sell, you also should report the price you paid, to the extent possible. Both the sales price and the commensurate price you paid should flow through your profit and loss statement. The price you paid for inventory is known as cost of goods sold (COGS). When you sell an item from your inventory, your accounting software reduces the cost value inventory on your balance sheet and records an expense in the Cost of Goods Sold section of your income statement.

In the following sections, we look at four costing methods you can choose from and share information to help you decide which one applies best to your inventory situation. Be sure to make your selection of a valuation method and note it in your accounting software before inputting your actual inventory amounts.

Average Cost

As you might have already gathered, the concept of tracking costs for inventory items can be confusing. Many accounting programs try to simplify this by only offering a single inventory valuation method known as average cost. When you sell an item, the software looks at the average cost of all the items you’ve purchased and uses that as the cost of goods sold. This eliminates fluctuations in your cost of goods sold because each item you sell is expensed at roughly the same amount.

If your inventory items were all purchased at approximately the same price, the average cost method represents a reasonably fair value for your inventory items. If the prices fluctuated significantly, this method wouldn’t be very accurate.

First in, First Out

If your accounting software permits it, first in, first out (FIFO) often gives the best representation of your cost of goods sold. In this case, the price for the oldest items in your inventory is applied to sales of inventory items first. You sometimes goof up your local grocer’s definition of FIFO when you grab a gallon of milk from the back that has a later expiration date instead of taking a gallon from the front.

FIFO is particularly well suited to perishable goods. You want to sell the items you purchased first—for example, a gallon of milk—before you sell anything you’ve purchased more recently.

Last in, first out (LIFO) is often used in industries where prices are typically fluctuating upward, so your cost of goods sold reflects the current cost of items being sold. LIFO is also sometimes used for bulk items where a new load is dumped on top of whatever is still in the bin. In these cases, you’re actually selling the last items first, so LIFO is appropriate.

The following figure provides a table of example inventory purchases and shows how the average, FIFO, and LIFO costing methods vary based on the example purchase data. In particular, this example illustrates how LIFO results in the highest inventory cost.

The amount applied to cost of goods sold can vary widely based on your choice of costing method.

Specific Identification

When you sell an item using specific costing, your accounting software uses the actual cost you paid for that specific item as the cost of goods sold. Specific identification also is used for items for which you track individual serial numbers.

The higher the cost you pay for an item, the more important it is to ensure the cost is directly associated with the sale, per the matching principle discussed earlier. Charging the wrong cost of goods sold to a high-value item can unnecessarily fluctuate your cost of goods sold and result in misstatements within your financial reports.

For this reason, most accounting software geared at small businesses doesn’t offer this costing method as an option. It’s usually only used for selling high-value items, such as expensive watches or jewelry.

RED FLAG

As soon as you click Save to add a new inventory item to your accounting software, you can’t change its costing method. If you need to change it, you have to create a new item, transfer the balances by way of inventory adjustments, and potentially create fictional transactions to provide the proper costing history. If you decide to change your inventory valuation method, you need to notify and get permission from the IRS by filing form 3115, Application for Change in Accounting Method, after the first day of the year you’re making the change. Most inventory valuation change requests are approved, but special rules apply if you use LIFO. Work with a tax adviser if you use LIFO.

Keeping Count

There’s definitely an art to effectively managing inventory. You don’t want your inventory level to be too large or too small, but rather just right. Keeping your inventory too low can save money on inventory costs, but it could result in lost sales. Buying too much inventory not only drives up costs, but also can result in items you can’t sell due to changes in the marketplace, spoiled inventory, damage, or myriad other problems.

Reordering

Rather than manage inventory based on gut feelings, use your accounting software to make inventory purchasing decisions based on actual sales data. Your software might enable you to specify a minimum stock level, so, ideally, you can keep a certain number of items on hand at all times and never miss sales opportunities because you were out of stock.

As we discuss in the reporting section of this chapter, you also might be able to run a report that lets you know which items you’re getting low on and should consider ordering. For example, your accounting software might offer a report like the Inventory Stock Status report from the desktop versions of QuickBooks shown in the following figure.

Although most of the accounting programs we discuss in this book don’t offer inventory optimization features, you might be able to purchase or subscribe to an inventory management program that can fill the gap. For instance, TradeGecko (tradegecko.com) connects with QuickBooks Online, Xero, and other cloud-based programs. On the desktop front, QuickBooks users who need enhanced inventory tracking and analytics often turn to Fishbowl (fishbowlinventory.com).

Your accounting software might offer reports that notify you when it’s time to reorder stock.

Taxes, Accounting, and Inventory

The physical inventory count we describe in the next section is used to back up the amount of inventory you report on your year-end financial statements and the amount of inventory you report on your income tax return. Your accounting software can maintain a perpetual count of the inventory you started with minus the items you’ve sold, but it can’t determine spoilage, obsolescence, or shrinkage–only your physical count can do that. To ensure accuracy in your financial reporting, it’s necessary to perform periodic inventory counts.

Physical Inventory Count

Occasionally you need to perform a count of the physical items you have in stock. Your accounting software maintains a perpetual inventory count as it tracks the items you buy and sell so you can keep a general sense of what you have. But you still need to verify that what your accounting software reports actually matches what physical inventory you have.

As you’ll see in the upcoming inventory reporting section of this chapter, your accounting software enables you to print a report or worksheet that lists all your inventory item types, with blanks for filling in the physical count. This report shouldn’t contain the quantities on hand, because knowing how much of something you should have can sometimes inadvertently prejudice the person performing the inventory count.

Here are the two types of inventory counts:

Periodic inventory count: During a periodic inventory count, you perform a physical count of every item you have on hand so you can reconcile what’s in your warehouse with what your accounting software reports in. Depending on the nature of the items and their value, you might perform this inventory annually or even daily.

Cycle count: For some businesses, it might be cost-prohibitive or too disruptive to do a physical count of all inventory items at once. In such situations, businesses often rely on a method called cycle counting, wherein a rotating subset of the inventory on hand is counted.

Inventory Adjustments

You’ll sometimes need to make adjustments to your inventory due to situations such as loss, spoilage, or obsolescence. For example, you might find that you only have 8 purple propeller hats instead of the 10 you thought you had. You can use an inventory adjustment command to change the quantity of items on hand.

Although most of the accounting programs we discuss in this book don’t offer inventory optimization features, you might be able to purchase or subscribe to an inventory management program that can fill the gap. TradeGecko (tradegecko.com) connects with QuickBooks Online, Xero, and other cloud-based programs. On the desktop front, QuickBooks users who need enhanced inventory tracking and analytics often turn to Fishbowl (fishbowlinventory.com).

When changing the quantity of items on hand, use your software’s inventory adjustment feature.

You also might be able to record changes in value, should you find that the price of an item has changed substantially since you first purchased it.

If you consistently make large adjustments to your inventory, it’s a good idea to research the reasons why. You might find indications of employee theft, more spoilage than you anticipated, or even evidence of unrecorded sales.

Reporting

Your accounting software enables you to generate a surprising number of reports that allow you to analyze your inventory activities. In this section, we review which reports to look for and how to use them.

Inventory Valuation Report

A key report you’ll want to view frequently is the Inventory Valuation report. The actual name of the report might vary based on the accounting software you use, but the purpose of this report is to document the detail of the Inventory account balance on your balance sheet.

The total asset value calculated at the bottom of the Inventory Valuation report should always match the Inventory amount that appears on your balance sheet.

This report details the sales quantities for each particular item. It shows sales of all your inventory items, not just stock items, so it’s a great way to track the popularity of the various products and services you sell. You can use this information to set minimum stock levels so you don’t inadvertently run out of popular items. You also can use this report to determine which items aren’t selling so you can jump-start sales through promotions or perhaps price cuts.

Items Sold to Customers

This report details the products and services each customer has purchased. You might find this report useful for identifying customers who haven’t purchased recently or helpful in suggesting to current customers other, complementary products you offer. You can run this report for two or more separate periods to try to identify customer purchasing trends.

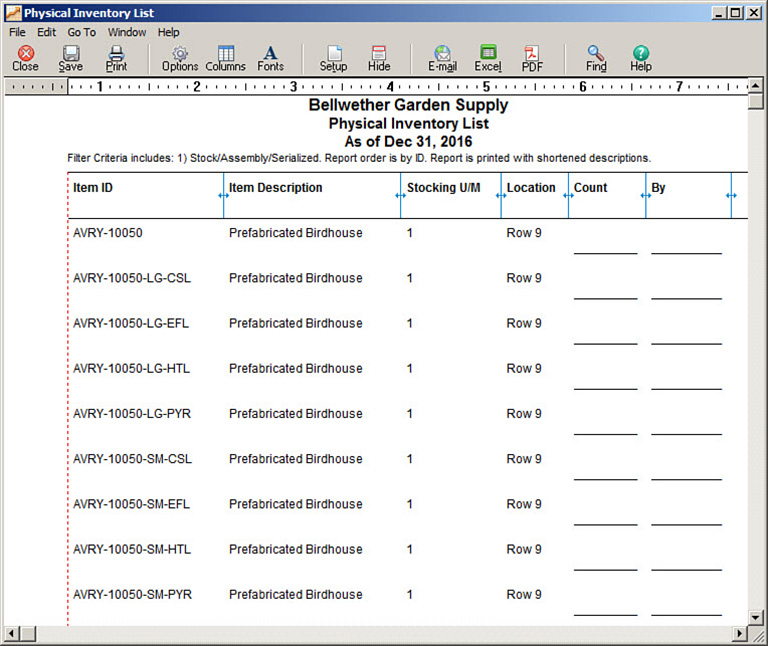

Physical Inventory List Report

Print the Physical Inventory List report before a physical inventory count, and use it as the worksheet for recording the count. It provides a list of your inventory items with space for recording the quantity of each item on hand.

The Physical Inventory List report omits the quantity on hand to eliminate bias during the counting process.

Be sure to keep copies of completed inventory reports as documentation for the IRS. It pays special attention to inventories because some taxpayers try to defer or evade income taxes by manipulating inventory values. Clean and accurate count sheets with initials are your best defense from an IRS query about your inventory.

The Least You Need to Know

- The stock of the items you sell represent your inventory, and the value of your inventory appears on your balance sheet.

- Accounting software aides you in keeping track of how much inventory you have on hand by adjusting your inventory balances with every sale you make.

- Inventory can be classified as stock items, nonstock items, assemblies, service items, and special-use items.

- The method you use for valuing your inventory plays a role in how your inventory appears on your balance sheet as well as how your cost of sales is calculated. Methods include average cost, FIFO, LIFO, and specific identification.

- You might lose inventory through damage and other issues, so it’s important to physically count inventory periodically and make inventory adjustments in your accounting software.

- Inventory reports in your accounting software can show your inventory value, sales by item, and sales by customer, as well as provide a handy worksheet for a physical inventory count.