Tracking Receivables and Payables

In This Chapter

![]()

- Setting payment terms for customers

- Using the Aged Accounts Receivable report

- Making refunds for overpayments

- Writing off bad debts

- Tracking payables with an Aged Accounts Payable report

Unless you’re the type of business that’s able to get paid immediately when products are delivered or services are rendered, and you can pay all your vendors and service providers in the same fashion, you’ll likely have accounts receivable. You’ll have accounts payable to track as well, either within your accounting software or by keeping an eye on a stack of unpaid bills in both your physical and virtual inboxes.

Your accounts receivable is comprised of unpaid invoices you’ve sent to customers, while within your accounting software, your accounts payable includes bills for amounts you owe to vendors you’ve entered into your books but haven’t paid yet.

If you opt to enter bills into your books at the time you write the payment checks, you may not carry any accounts payable on your books. However, whenever you have bills you plan to pay at some point in the future instead of immediately, it’s always best to enter a bill in your accounting software, as we discuss in Chapter 6.

If the nature of your business is such that you handwrite invoices to customers for work performed in the field, always be sure to record the invoices in your accounting software as soon as possible so you don’t lose track of the money due to you.

This chapter introduces you to all the best practices for tracking receivables and payables.

Payment Terms

Each business has the flexibility to set its own policies on how quickly payment is expected from its customers. You’ve likely received bills that say “payable upon receipt,” but a more standard convention is referred to as “net 30 terms.” This is how accountants signify that payment for the entire bill is expected within 30 days.

You also might encounter situations when a bill shows payment terms of “2%/10 net 30.” In this case, the vendor is saying you can pay 98 percent of the bill within 10 days (a 2 percent discount) or 100 percent of the bill within 30 days.

In your books, you’ll record the entire expense in the usual fashion and add a line item for the discount that has a negative amount posted to an Other Revenue account called Discounts Taken.

If you choose to offer such terms to your customers with the hope of speeding up your cash flow, you’ll record the early payment discount in much the same fashion as the credit card transaction fees we discuss in Chapter 6.

Your accounting software enables you to set payment terms for customers on a global basis, but you can always override this global setting for specific customers.

Customer payment terms are typically set at a company level within your accounting software.

Aged Accounts Receivable Report

Your Aged Accounts Receivable report provides a detailed accounting of all the money owed to you by customers, as well as any credits you’ve issued to customers that have not yet been applied against an invoice or refunded. If you maintain your books on the accrual basis, the amount of this report should match the balance of the Accounts Receivable account on your balance sheet and General Ledger. If you use cash basis accounting for your books, you won’t have an Accounts Receivable account because invoices you issue don’t truly affect your books until your customer pays you.

The following figure shows a typical aging report. The standard configuration, which you might be able to change to suit your needs, is as follows:

- Customer name and/or customer ID

- Invoice date

- Invoice number

- Aging bracket columns typically in 30-day segments, such as 1 to 30 days, 31 to 60 days, 61 to 90 days, and 91 days and older

- Total due by invoice

The report then reflects a subtotal of the amounts due by customer along with grand totals for each column at the very bottom.

The Aged Accounts Receivable report gives you an overview of how much money each customer owes you as of the report date.

Some accounting programs, notably the desktop versions of QuickBooks, use the number of days past the due date to age invoices and bills. In effect, the report shows you the number of days past due a transaction is, as opposed to the number of days old. So a transaction that’s due within 30 days of the invoice date but is 15 days past due would appear in the 1–30 Past Due column based on this convention. If you set your accounting software to age based on the transaction date, this amount will appear in the 31–60 Past Due column. Be cognizant as to which approach your software uses so you don’t misjudge the age of unpaid bills and invoices.

As noted in Chapter 17, many accounting reports have a drill-down feature that allows you to easily dig deeper into the source of amounts shown in your accounting records. In the case of an Aged Receivables Report, you can click on an invoice amount to see the supporting detail of the amount. Depending on your software, you’ll see either the unpaid invoice or a new version of the aging report that shows all unpaid invoices for that customer. You might have to click one more time to display the actual unpaid invoice.

Once the invoice is on your screen, you can print another copy if you want to send a reminder by mail, or you can email a copy of the invoice from within the software. Some accounting programs add the word DUPLICATE prominently to invoices you print or email more than once so customers don’t inadvertently pay the same invoice twice.

Customer Statements

An alternative to sending additional copies of invoices to your customers is to use the Customer Statement feature if its offered by your software.

You can typically run statements two different ways:

Open transactions: This type of statement allows you to generate a list of open invoices and credit memos for your customers. This format is helpful for reminding customers they might have missed one or more invoices, or to give them a quick overview of their account.

Customer activity: This type of statement reports all activity on a customer’s account for a given period of time, including their payments. In effect, it’s a mini general ledger just for that customer for a specific period of time. This is helpful in eliminating discrepancies that arise when you post a payment from a customer in a different fashion than they expected. For example, you might have applied a customer payment to a different invoice than the one the customer intended the payment for.

This excerpt from a customer statement shows only unpaid invoices and unapplied credit memos, if any.

This excerpt from a customer statement displays all activity that occurred on your books for a given period.

Although your accounting software might enable you to send a statement to every customer, every month, it’s usually best to reserve customer statements to an as-needed basis. Some customers might want you to submit a statement periodically, and don’t be surprised if some customers only pay from a statement rather than individual invoices.

Keep in mind that only customer invoices, credit memos, sales receipts, and invoice payments appear on a statement. Estimates, quotes, and sales orders don’t affect your general ledger and, therefore, won’t appear on an aging report.

BOTTOM LINE

Statements provide documentation of what your records show for a given customer as of a certain point in time. Statements serve as a useful collections tool for you, as well as a research aid for your customers when their records differ from yours. Keep this type of document in mind should you encounter discrepancies on what you think you owe to a vendor. Most likely their accounting software enables them to prepare a statement on your behalf so you can quickly see how your payments to them have been applied.

Collectability Risk

Always keep an eye on your Aged Accounts Receivable report. There’s a distinctly inverse relationship between the age of an invoice and its collectability. In other words, the farther to the right the amount moves on your aging report, the odds of the customer paying it drop precipitously.

Some companies take excessively long periods to pay their bills. This is often referred to as vendor financing, as by exceeding the agreed-upon payment terms, your customer is using your business as a de facto lender. It could be that the invoice got lost by the U.S. Postal Service if sent by mail. Keep in mind that, occasionally, emailed invoices don’t make it to their intended inbox. Or your customer could be continually promising, “the check is in the mail” when it’s actually not. The person making the promise likely has the best intentions but either can’t pay the invoice due to financial constraints or they simply don’t have authorization to do so.

As invoices age beyond the 30-day past due column, it might be time to consider your options.

Unfortunately, the saying “nice guys finish last” is often true when you allow customers too much leeway. Be proactive but polite when pursuing what’s due to you. Do give the benefit of the doubt when first following up on invoices. If you email invoices electronically, you’ve likely noticed that most, but not all, of your electronic correspondence gets to its intended destination. As for paper mail, you’ve likely seen news stories trumpeting a letter finally delivered after lingering in the postal system for sometimes decades.

The reasons why invoices are paid late are legion, but sometimes the late payment occurs because the person who needs to approve the invoice is on vacation, traveling, or simply swamped with work. A gentle “just making sure you saw this” follow-up by email within a couple days of an invoice exceeding your payment terms could prevent many collection issues. Being proactive also helps you temper your frustrations, because most customers can and want to pay their invoices timely.

Be prepared to gently ratchet up the pressure as needed if an invoice payment continues to slip into the future.

Finance Charges

Your accounting software might allow you to assess finance charges on unpaid balances. It’s doubtful that a customer who consistently pays invoices late will honor a request for finance charges, but some will, and by assessing extra charges, you’ll then have that fee on record should you need to send the customer to collection.

Your software won’t automatically charge interest on unpaid invoices, and not every program offers this capability. If this feature is available, you’ll be able to choose which customers you want to charge in this fashion.

Your accounting software might allow you to specify which customers you want to assess finance charges.

Keep in mind that states set usury limits on the amount of interest you can charge. These caps on past due invoices vary by state, and businesses may be subject to different rules than consumers. States periodically change their maximum permitted interest rates, and some make a distinction between simple interest and compound interest. Check your state’s regulations to determine whether late fees in lieu of or in addition to interest are permitted.

DEFINITION

Usury interest rates are generally exorbitant or excessive. Simple interest means you can only charge interest on the original amount due, while compound interest means you can charge interest on unpaid interest amounts as well.

The penalty for violating usury statutes typically entails some amount of monetary forfeiture and could include criminal penalties as well. Tread carefully when applying finance charges so you don’t inadvertently run afoul of the law.

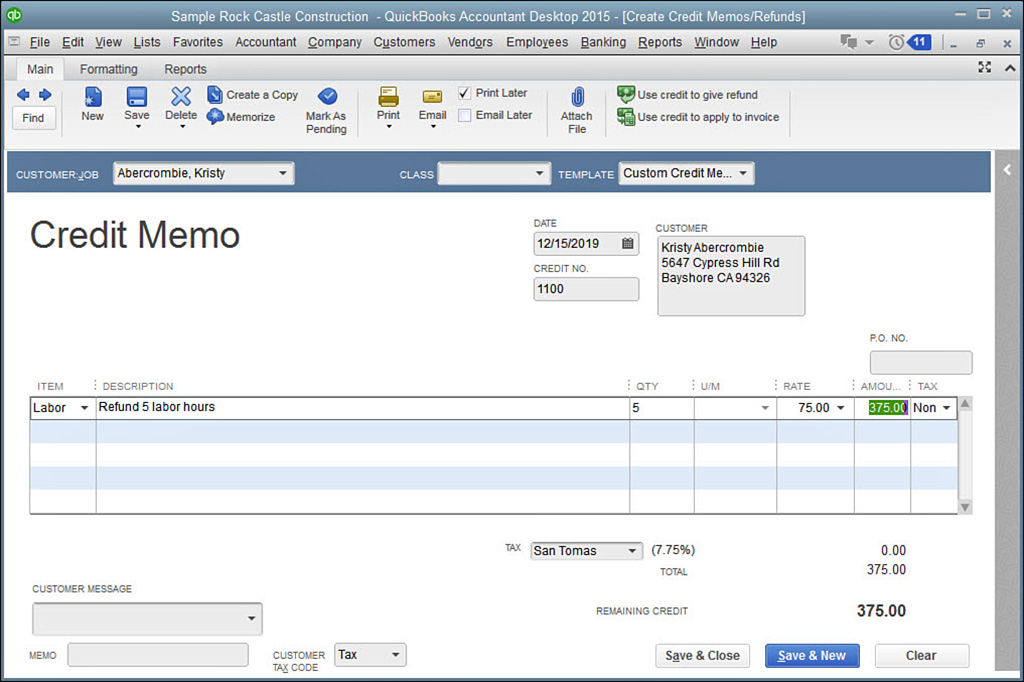

Refunding Credit Balances

From time to time, a customer might inadvertently pay an invoice more than once, and you might cash the check before realizing it’s a duplicate payment. For instance, many banks offer lockbox services where customers mail payments directly to a post office box controlled by the bank. The bank opens the envelopes, creates an electronic copy of the checks and any supporting documents, and provides you with electronic documentation of the deposit made. If a bill is paid twice accidently using this system, your customer must issue a stop payment notice when they realize their error.

If it’s too late, you can post a credit memo to your books on behalf of the customer to be applied against future services. Or you could issue the customer a refund. Your accounting software might offer two different ways to issue refunds.

The screen you use to pay bills might allow you to choose a customer instead of a vendor. In such cases, you should have the option to select the invoices and/or credit memos you’re applying the refund against. Keep in mind that accounting programs sometimes make a distinction between paying bills and writing checks. A “write checks” window likely won’t allow you to choose a customer, so check the bill payments window if necessary. In some cases, you might be refunding a remaining balance; in others, you might need to first apply the credit against one or more unpaid invoices and then refund the difference. If you issue a check without applying it against open invoices and/or credit memos, the open balance remains on your books even though you’ll have given the customer their money back.

In some software, the screen you use to issue credit memos may offer a “Use Credit to Issue Refund” button. If available, this approach helps you avoid leaving an open accounts receivable balance on your books.

RED FLAG

Use care when recording payment transactions that involve your customers. If you write a check to a customer for an amount other than a credit balance due, your accounting software might try to be helpful and set up a receivable balance for the amount you paid. For instance, you might need to purchase products or services from your customer. To avoid such situations, set up your customer in your accounting software as a vendor as well so you don’t inadvertently record receivable balances for purchases you make to the vendor.

Some accounting programs make it easy to issue refunds to credits; you have to do some legwork in others.

Writing Off Bad Debts

Unfortunately, you might reach the inevitable point that you determine one or more invoices are simply uncollectible. The one saving grace about a bad debt is that if you’re an accrual basis taxpayer and already recorded the revenue on your books, you’ll receive an income tax deduction in the amount of the foregone revenue. In that regard, it’s important to keep your books up-to-date so at least you’re not unnecessarily paying income taxes on money you’ll never see (even though you will recoup the tax amount paid at the point you write off the debt).

Accrual basis companies that maintain an Accounts Receivable account are allowed to create a contra-asset called Allowance for Bad Debts. In particular, if you have a history of a certain percentage of your receivables being uncollectible, the IRS encourages you to set up this offsetting asset so your Accounts Receivable, net of the Allowance for Bad Debts, reflects a realistic total of what you actually expect to collect.

You’ll use your past history as a guide for how much to aggregate in the Allowance for Bad Debts account. When you record the initial amount and update the allowance account periodically with a journal entry, the offsetting entry goes to a bad debt expense. This expense reduces your revenue for tax purposes so you’re not paying taxes on amounts you don’t plan to collect.

If you maintain your books on the cash basis, you aren’t entitled to an income tax deduction for bad debt because you were never taxed on the revenue. As we discuss in Chapter 2, cash basis accounting recognizes revenue upon receipt from the customer, while accrual basis books recognize revenue when earned.

Managing Credit Risk

You often can minimize the risk of lost revenue by doing some homework in advance. As shown in the following figure, Microsoft Word offers a free business credit application template. An internet search using the term “business credit application” can unearth other alternatives.

Your word processing program might offer a built-in business credit application template you can modify to suit your needs.

You also might be able to purchase the equivalent of a consumer credit report for many, but not all, businesses from Dun & Bradstreet (dnb.com). Indeed, you may have seen customers make reference to their D-U-N-S number, a program offered by Dun & Brandstreet to make it easy for businesses to share their credit profile with prospective vendors.

Your accounting software likely enables you to establish credit limits for your customers. These can often be set globally, such as a $5,000 maximum for every customer, although you can also permit larger or smaller thresholds as needed. When utilizing this feature, you might have the following options:

- View a notification prompt that the invoice you’re entering will cause a customer to exceed their credit limit, with the option to override the credit limit.

- Prevent a user from posting the invoice they entered because the credit limit would be exceeded.

Some accounting programs show the current balance for a customer when you add a new invoice. In other cases, you might not realize the credit limit conflict until you go to save the invoice, which can cause a frustrating loss of your work.

Aged Accounts Payable Report

Just as the Aged Accounts Receivable report shows what’s owed to you, your Aged Accounts Payable report displays what you owe to others.

Every accounting program offers such a report, but if you don’t record your vendor bills until you’re ready to pay them, there won’t be any items listed on this report and you won’t have a need for it. As discussed in Chapter 6, you have the option to enter vendor bills into your accounting software in advance of paying them, or you can streamline the process by writing checks when payment is due and skip the bill-entry step.

You might be able to get away with bills initially being added to your books when you write the payment check, but as your business grows, you’ll likely gravitate toward entering bills as they’re received. The vendor bills you enter will appear on the Aged Accounts Payable report.

Among other things, the Aged Accounts Payable report can help you keep track of bills you’re purposely not paying, such as a bill you’re holding due to a delayed completion date or goods damaged in shipment.

Eliminating Zero Balances on Aging Reports

From time to time, you might encounter situations in which a customer or vendor shows an amount due of, for example, $100 alongside a credit balance of $100. You’ll need to purposefully match these transactions to clean up your aging reports.

Within your accounting software, go to the screen where you apply customer payments or pay vendors, respectively. Depending on the software you use, you might be able to simply select both the amount due and the corresponding credit to create a 0 balance transaction you’ll post. Or you might have to click a Credits button to instruct the software that you want to apply a pending credit against the invoice. This, too, generates a 0 balance transaction that will clean up your aging report.

- Payment terms vary from one business to the next. Check any bills you receive to determine if any early payment discounts are available.

- Your Aged Accounts Receivable report shows how much is owed to you at a particular point in time and how long those accounts have been lingering on your books.

- Use the Aged Accounts Payable report if you enter vendor bills when you receive them, and you’ll always know how much you owe and to whom.