The primary audience for this book is students in MBA and Executive Education programmes. For this reason, much of the book is directed at issues of management, both within steel companies and more broadly. How do steel companies operate, what motivates executives in charge of them, and how do they manage and coordinate their huge and complicated global operations?

Classic steel companies were operated like huge centrally controlled machines. They had their own iron ore and coal mines, railroads, furnaces, rolling mills, and distribution centers. With this scale and throughput they produced steel products, which in their standard grades, cost less than the price of chicken at the local grocery store. Price pressures from low-cost minimills and foreign imports, along with financial pressure to maximize shareholder value, caused the integrated steel companies to change how they operated in the 1980s and 1990s. They closed or sold off most “noncore” assets such as mines, transportation, and distribution facilities. Instead of internally regulated functions, these became arms-length contractual relationships. In retrospect, the timing could not have been worse. The steel companies had become extremely vulnerable to escalating input cost pressures as the price of raw materials surged, driven by the emergence of Chinese steel demand. It caused a quadrupling and more in commodity prices, plus a level of volatility that was unprecedented that destabilized existing steel company operations. Managing dispersed supply chains instead of in-house operations became the new norm for steel companies. They joined other manufacturers in coordinating a level of complexity that was a qualitative change from the industrial organizations and culture of previous company operations. Steel companies are now immersed in the global system of networked manufacturing. This raises the question of what the steel company of the future will look like. Some commentators suggest that they will take on the role of systems integrators as have other advanced manufacturing companies. Maybe, maybe not.

The chapter begins with the current situation, who the new steel companies are, and brief profiles of the major players. It then turns to the history and culture of steel companies in the past century in order to outline the challenges older corporate structures and cultures present for the new generation of global steel management. We then return to the present and look at the objectives of steel company executives and how they measure results through benchmarking of local operations. Finally, we look at steel company operations as coordinated global supply chains, taking a closer look at the example of metallurgical coal. The chapter concludes with some suggestions of what the steel company of the future might look like.

Global Consolidation of Steel Companies

We now have global steel companies in an entirely new way than what there was in the past. While international steel trade has been around for a long time, the unprecedented trade pressures and disputes of the 1980s (Chapter 7) led to a major change and formation of joint ventures with foreign producers. This made for a somewhat disjointed and transitional stage for the industry. It was followed over the past decade by the complete international reorganization of the industry through mergers and acquisitions, along with many exiting companies. The new global steel companies are still very much a work in progress and will continue to evolve. For example, as discussed later in this chapter, the physical boundaries of the firm are an issue, both at the raw materials end and at the distribution end of the business.

The industry has seen a huge consolidation of steel companies driven by bankruptcies, mergers, and acquisitions. The list of companies itself tells the story. The most dramatic changes were within North American operations.

• Algoma Steel (assets bought by Essar Steel, India in April 2007)

• Arbed (merged with Aceralia and Usinor 2002 forming Arcelor)

• Arcelor (merged with Mittal forming ArcelorMittal)

• Bethlehem Steel Corporation (assets bought by ISG in 2003. ISG merged with Mittal, now ArcelorMittal)

• British Steel (merged with Koninklijke Hoogovens (NL) in 1999 to form Corus, now Tata Steel)

• Carnegie Steel Company sold to U.S. Steel

• Cockerill-Sambre (acquired by Usinor in 1998, which became part of Arcelor in 2002, now ArcelorMittal)

• Corus Group (acquired by Tata Steel in 2007)

• Dofasco in Hamilton, Ontario (acquired by Arcelor, now ArcelorMittal)

• Hoesch Stahl AG (acquired by ThyssenKrupp)

• Inland Steel Company (acquired by Ispat International, became Mittal, now ArcelorMittal)

• International Steel Group (merged with Mittal, now ArcelorMittal)

• Jones and Laughlin Steel Company (acquired by Ling-Temco-Vought, renamed LTV Steel, acquired by ISG)

• Koninklijke Hoogovens (merged with British Steel (UK) in 1999 to form Corus, now Tata Steel)

• Krupp (merged with Thyssen to form ThyssenKrupp in 1999)

• Lackawanna Steel Company (acquired by Bethlehem Steel in 1922, plants closed in 1982)

• Laiwu Steel (merged into Shandong Iron and Steel Group)

• Lone Star Steel Company (acquired by U.S. Steel in 2007)

• Mittal Steel Company (merged with Arcelor, forming ArcelorMittal)

• National Steel Corporation (acquired by U.S. Steel in 2003)

• Northwestern Steel and Wire closed in 2001. Later partially reopened by Leggett and Platt, as Sterling Steel Company LLC

• Republic Steel (merged into LTV Steel, acquired by ISG, merged with Mittal, now ArcelorMittal)

• Rouge Steel (formerly owned by Ford Motor Corporation) acquired by Severstal in 2004

• Steel Company of Wales (absorbed into British Steel in 1967)

• Stelco (acquired by U.S. Steel in 2007)

• Thyssen (merged with Krupp to form ThyssenKrupp in 1999)

• Weirton Steel (acquired by ISG, which merged with Mittal, now ArcelorMittal)

• Youngstown Sheet and Tube (acquired by ISG, which merged with Mittal, now ArcelorMittal)

Source: Wikipedia.

The result of the wave of consolidation was to establish huge international steel companies. The following is the list of the top 12 steel-producing companies in the world by capacity as of 2010. As can be seen it is heavily weighted toward Asian countries.

|

Rank (2010) |

Capacity (Mtns) |

Company |

Headquarters |

|

1 |

98.2 |

ArcelorMittal |

Luxembourg |

|

2 |

52.9 |

Hebei Iron & Steel |

China |

|

3 |

37.0 |

Boasteel |

China |

|

4 |

36.6 |

Wuhan Iron & Steel |

China |

|

5 |

35.4 |

POSCO |

South Korea |

|

6 |

35.0 |

Nippon Steel |

Japan |

|

7 |

31.1 |

JFE |

Japan |

|

8 |

30.1 |

Jiangsu Shagang |

China |

|

9 |

25.8 |

Shougang |

China |

|

10 |

23.5 |

Tata Steel |

India |

|

11 |

23.2 |

Shangdong Iron & Steel |

China |

|

12 |

22.3 |

U.S. Steel |

USA |

Source: World Steel Association.

Of the top 12, all but two are in Asia. There is one European, ArcelorMittal and one North American company, U.S. Steel. They are also all integrated steel producers. The implication is clear; the future of the steel industry will be led by a relatively small number of integrated producers with a dominant presence in regional markets. This suggests a different outcome than the minimill-led steel innovation story that has dominated the steel news of the past 20 years.

However, looking at it from the perspective of the past 5 years, the trajectory of that development may be greatly impacted by forces largely outside of steel companies’ control, that is, the trajectory of raw materials prices and development. As shown in the following table, even with this level of consolidation, globally, the level of concentration in the steel industry is dwarfed both by those in the industries upstream where it sources its raw material inputs and by its key downstream consuming industries such as automotive.

Steel, Auto, and Raw Materials: Levels of Concentration (%)

|

Industry |

Percentage output of top 10 producers (%) |

|

Steel |

23 |

|

Iron Ore |

96 |

|

Metallurgical Coal |

85 |

|

Automotive |

80 |

So, while steel is big, it is severely constrained when it comes to upstream and downstream pricing power. It is this that has made the dramatic and volatile prices changes in the price of raw materials so destabilizing for steel producers.

Who Are Some of the Key New Global Steel Companies?

In concentrated industries, it may make sense to work outward from the lead firms.

Who are some of the key new players?

U.S. Steel

U.S. Steel was the leading steel producer in the first half of the 20th century. It dominated the US market and was looked to around the world as the model of what a steel company should be. With the difficulties in the industry in the 1980s, the company diversified into other fields including energy and transportation. More recently, it restructured and regained its focus in steel, expanding into Eastern Europe and into Canada as part of the global consolidation in steel. It supplies the automotive and energy sectors. It is now organized around U.S. Steel operations for North America and U.S. Steel Europe. The company manufactures a wide range of value-added steel sheet and tubular products for the automotive, appliance, container, industrial machinery, construction, and oil and gas industries. U.S. Steel is a leader in both process and product technology. The company has three research and development facilities.

Nucor

Nucor, originally the Nuclear Corporation of America, appointed Ken Iverson as president in 1965 and he changed the industry with the new electric arc furnace (EAF) technology, a staunch antiunion policy, and introduction of the first minimill to produce flat rolled products in 1987. Nucor is headquartered in Raleigh with major production operations across the United States and in Canada. It is a global player because it has been for 30 years the reference case for minimill technology developments. Because EAF steelmakers produce almost entirely for regional markets, all of its operations are in the NAFTA region. Through acquisitions and joint ventures, the company eventually grew to become the second largest American steel producer. Because of the nature of the electrical furnace technology, Nucor has adapted to fluctuations in the market more by reducing volumes in downturns rather than by reducing prices. In addition to its head start on the technology side, much of its success is the result of a highly motivated, team-based workforce with high profitability bonus compensation.

ArcelorMittal

ArcelorMittal is the world’s largest steel company, headquartered in London and Luxembourg, with operations in more than 60 countries. It is present in all major global steel markets, including automotive, construction, household appliances, and packaging. ArcelorMittal is a leader in R&D and technology development. The company has its own supplies of raw materials accounting for about 60% of requirements and has its own distribution networks. ArcelorMittal was formed in 2006 by the merger of Arcelor of Luxemburg and Mittal. The latter was originally from India but later consolidated Central and Eastern European operations, and then took over a series of distressed North American steel companies. ArcelorMittal continues its strategic policy of horizontal consolidation. More recently, it has been seeking to expand operations in China and India. Construction and infrastructure are the leading steel sectors in emerging market countries and the company’s product market and facilities configuration have been similarly focused.

Posco

Posco is headquartered in Seoul, Korea. It was incorporated in 1968 with close ties to the government who had the objective of making the country self-sufficient in iron and steel. It has expanded and formed joint ventures in China, India, Vietnam, Mexico, and Brazil. Most observers regard it as the most technically advanced steelmaker in the world. It has major expansion plans in Asia and in Brazil based on its indigenous technology advantage. It also has an announced policy of displacing the Steel Service Centers in order to get closer to the knowledge base of its customers. It has developed the Finex process for iron-making, which may eventually replace the traditional blast furnace with significant reductions in production costs and fewer environmental impacts.

Gerdau

Gerdau Group is headquartered in Brazil. It is the world’s 14th largest steelmaker and the largest producer of long products in the Americas. Gerdau Ameristeel is the fourth largest overall steel company and the second largest minimill steel producer in North America. The company’s products are used in a variety of industries, including construction, automotive, mining and electrical transmission. It has a vertically integrated network of minimills, scrap recycling, and downstream facilities. Its products are generally sold to steel service centers and fabricators and a minor share going to original equipment manufacturers.

ThyssenKrupp AG

ThyssenKrupp is the largest European steelmaker. It is a result of a merger between other leading German steel companies. The company is a technical leader in metallurgical engineering, process technology, and new application development in the automotive, construction, and energy industries. It is a global leader in advanced steel product development with engineering applications especially supporting the German auto industry, which leads the world in automotive design and tooling.

Tenaris

Tenaris is headquartered in Buenos Aries, Argentina. It is a leading supplier of tubular products and related services for the world’s energy industry. The company’s principal products include casing, tubing, line pipe, and mechanical and structural pipes. It produces seamless products for high-pressure, high-stress applications, and welded pipe for more standard environments. Tenaris expanded in the past decade into the United States principally through the acquisition of Maverick Steel and Hydril. It operates Tenaris University, which gathers and codifies the knowledge and best practices within the company’s operations for both salaried and hourly employees.

Baosteel

Baosteel is the one of largest steel company in China. It is state owned and is headquartered in Shanghai. With the economic reforms in 1978, the government decided it needed a major steel capability located close to Shanghai. It incorporated the latest technology then available, principally from Japan. As other Chinese mills came on stream, Baosteel decided to diversify into exports. Baosteel also absorbed several other money-losing state-owned steel companies. It later formed a joint venture with Thyssen Krupp of Germany. It is rightly regarded as the symbol of the rise of Chinese steel. It has been expanding through co-ventures in Brazilian iron ore developments.

Tata Steel

Tata Steel is the largest private sector steel company in India. It is part of the Tata Group comprising a broadly based enterprise with interests from financial services to chemicals to automobiles. It recently acquired Corus Steel of the UK and has announced the intention to expand to 100 million tons of capacity, half by building greenfield facilities and half by acquisitions. It exemplifies the rise of India as a global steel power. India has plans to add more steel capacity in the coming decade than does China.

How Steel Companies Used to Operate:

The U.S. Steel Model

As indicated, steel companies used to be highly integrated vertical hierarchies managing the process from iron ore in the ground to delivery of a steel coil to a stamper’s loading dock. They were present at the birth of the modern business corporation. The first billion dollar corporation ever formed was U.S. Steel in 1901. Given the scale of capital and operations, vertical integration was seen to be absolutely necessary, both to reduce transaction costs and to control production flows.

Steel companies were a huge story in the economy. The steel industry had the largest stock of plant and equipment in the US economy in the 1950s and from 1929 to 1958 accounted for the largest single component of GDP of any domestic industry. Even later, in most years it retained its place in the top three contributors to GDP till the mid-1970s.

From 1900 to 1960, the U.S. steel industry had an entrenched oligopolistic structure. Prices were based on a mark up over costs1 and market demand was closely coordinated with industry production capability. The large integrated steel producers competed for market share to maximize internal utilization rates.

However, steel companies lagged other industries in modernizing their organizational structures and cultures. In 1962, the great business historian Alfred Chandler observed that the steel industry was virtually alone in staying with the centralized, hierarchical form of organization when all other major industries by the 1940s had moved to some version of the multidivisional corporation pioneered by GM and Dupont.2 The GM model not only allowed it to produce different cars for different market segments—Chevrolet, Pontiac, Oldsmobile, Cadillac—it also made for a more diversified and innovative company.3

The steel industry was not alone in resisting the new multidivisional structure. The traditional approach was also kept in other metal and materials industries. Copper and nickel companies paid the least attention to the new management philosophy. Steel companies devoted more thought to the lines of authority and communication, in almost every case, bringing increasing centralization.

Steel had a long history of integrated activity, from refining of ores, converting iron to steel, and the fabrication of semifinished products all being done in the same plant. They produced a standardized set of products for a large number of customers, often accumulating large volumes of inventory in advance of orders. The higher volume of goods, large number of customers, and integrated production have made scheduling of operations and coordination functions much more complicated than the copper industry for instance. The production of standardized items in high volume ahead of orders also created more of a need to forecast and analyze future market trends in order to integrate the various parts of the enterprise.

After its initial consolidation, in its first operating period, U.S. Steel functioned as a somewhat loose federation of units with a small holding company office in New York. The major reorganization came between 1929 and 1937 under President Myron Taylor. It included building a large general staff, including a centralized Production Planning Department. The functioning departments were left in Pittsburgh including operations, sales, industrial relations, research and metallurgy, and traffic, each with its own vice-president. This was a step toward a multidivisional organization, but in 1950 U.S. Steel reverted to a renewed centralism. Central Operations took over all steelmaking. All activities under it were departmentalized along functional lines. In Chandler’s view, U.S. Steel after 1950 became more like that of DuPont prior to 1921. Other steel companies followed the U.S. Steel pattern over the 1950s.

As stated, U.S. Steel in the mid-1960s had a culture replicated by most the big steel companies. Production men ran the company. Their only management metric was tonnage of steel produced. Quality and customer service were secondary. The organization was inbred, centralized, and autocratic. The main focus was not on products or markets.

It was 50 years later that steel companies began to experiment with multidivisional organization—separate operating companies for steel production facilities, distribution, transportation, and raw material inputs. Meanwhile, the world had moved on to matrix-style organizations that were much more flexible and emphasized cross-functional coordination and work teams.

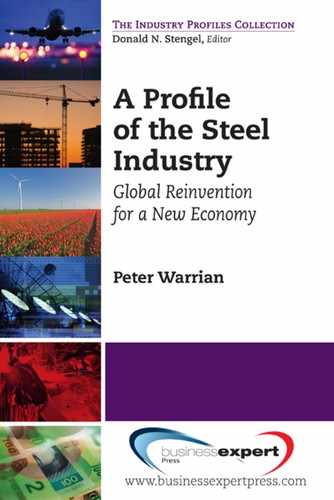

There was a major North American exception to this direction, the Canadian steel producer Dofasco, which in the 1990s would become the most profitable integrated steelmaker in North America. When it became a fully integrated steel company under its founder Frank Sherman in the mid-1950s, he consciously decided not to go the route of U.S. Steel and the established form of organizational development. Instead, he developed an early form of the matrix organization. The pioneers in this area were ITT in the US and Panasonic in Japan. Dofasco’s success in innovation in the 1990s flowed in no small measure from this different trajectory of organizational development taken 40 years earlier. It was also nonunion and built an inclusive workplace culture. The latter was ultimately probably more important in the long run than whether or not it had a union. It allowed the company to operate in a fundamentally different way.

However, across the industry, the narrow organizational form dominated. As Chandler stated:

…the production and marketing facilities for ore and semi-finished and even finished products cannot be easily transferred to the production and marketing of new and different products. Therefore, the strategy of diversification with its inevitable increasing long range decision-making has not been a tempting one in the expansion of the steel industry. (337)

Chandler’s theory of the modern corporation was based on a linkage between skills and organizational structure. He identified steel companies as typifying the functionally departmentalized organization as examples of early 20th-century capitalism. It divided the organizations along discrete tasks, that is, manufacturing, sales, finance, and centralized decision making. He argued that for the future, the multidivisional form was the most efficient organizational response to the increased complexity of expanded administration. Decision-making authority would be re-distributed to various functional operating units. Middle management would coordinate product flow from production through distribution, while top management defined and allocates unit responsibilities, monitored and controlled their activities, and plans and allocates corporate resources for future activities.

Chandler had identified what he thought to be the “logic of managerial enterprise,” the dynamic of growth and competition of modern industrial capitalism. Such large, oligopolistic industries would be efficient because competition for market share and profits sharpened the skills of senior management. The key was the scale and scope of the modern industrial enterprise.4 Scale refers to the cost advantages of large plants; scope meant the use of many of the same raw materials to make a variety of different products. Steel companies therefore stood at the head waters of managing operations in the modern industrial enterprise.

Such exemplary, focused corporate headquarters skills, however, did not spare U.S. Steel from making perhaps the biggest strategic error in business history in the mid-1950s when it invested backward instead of forward in steel technology. This also happened at the exact time the corporation was recentralizing.

In the 1950s, the American industry was the preeminent leader in the world. U.S. Steel alone had more capacity than Britain, Germany, and Japan combined. But by that time, the capacity built up during World War II had to be renewed and new capacity had to be built to meet the demands of the postwar consumer economy. U.S. Steel and the industry was awash in cash. Unfortunately, the company, followed by its fellow American steel companies, decided to re-invest backward in the old technology of the open hearth furnace, notwithstanding that the new technology of the basic oxygen furnace and the continuous caster were already installed in other parts of the world.

The drivers of the decision were the traditional culture of integrated steel companies, the tax code, and the regulatory environment.

The U.S. Steel executives were in part the victims of accounting rules. As depreciation is normally spread over 20 years, 1955 investments could not be fully recouped till 1975. Retirement of production facilities early would eliminate millions in tax deductions and undermine operating profits. Similarly, for raw material assets, they did not invest in new higher quality iron ore and coal resources because they would have to write off earlier investments in existing mines.5

The executives who made the decision were also constrained by their personal histories. Almost all of the top executives were former open hearth engineers.6 It was the only production technology that they knew. What it meant, however, was that their personal pasts compromised their company’s future. By the 1960s and 1970s, the US producers were fundamentally uncompetitive with Japanese and European producers using the new technologies. The following 30-year slide in the US industry would really only end with the merger and acquisition movement of the past decade.

In the early 1980s, U.S. Steel produced a ton of raw steel in 11 man hours per ton. By the mid-1990s it produced a ton of raw steel in 4 man hours. The massive downsizing of U.S. Steel in the 1980s resulted in a company that was basically an exclusive producer of flat-rolled steel products. Legendary U.S. Steel mills were closed—Homestead, Duquesne Works, and McKeesport. U.S. Steel was frog marched into catching up with the revolution in continuous casting that the Japanese steel industry had led in the 1970s. Capacity and employment were cut in half. The number of mills was reduced from 15 to 5.

In the end, U.S. Steel, or USX as it had come to be called, was focused and profitable. It retained a physical advantage within the high end of the flat-rolled market over its new minimill rivals. Complex processes in the melt chemistry produce an irreducible surface quality advantage for sheet made from iron ore over similar products made from scrap that have inevitable impurities. The physical properties required for ultralow carbon steel, mainly formability, cannot be matched by scrap-based production. This became the last and most highly valued market niche for the integrated producers, of which U.S. Steel was the clear leader in the United States.

Managing Steel Companies in the New Global Environment

What is the impact of globalization on management of steel operations and what are the likely future directions?

The most immediate, practical impact has been significant cost savings, reportedly in the 10–15% range, through global benchmarking of best practices within the new global steel management system. These range from technical operating, engineering and procurement practices, to human resource policies. It has also been accompanied by circulation of technical talent both inward and outward bound between domestic and international operations. This has now become embedded in standard management practices and procedures, including regular monthly and quarterly meetings and conference calls, along with formal annual reporting and quantitative measurement. Management practices have become much more systematic.

The second and more important long-term factor is the change in access to capital and technology. Private sector steel companies have always been capital constrained. Access to capital has significantly increased and decision making on capital expenditures has been significantly speeded up say managers who worked under the old system as well as the new.

The following are variations on the same theme from several different steel companies:

There is greater access to capital but it is competitive. Things like environmental regulations are a factor. Best practices have reduced overheads. There is more leverage with suppliers. We have become a more sophisticated company.

Capital access is much better. We have dramatically improved our scrap business, a new reheat furnace, new cold bar sphere, other upgrades. This started with the previous ownership but accelerated with the new owners. But there is competition within the organization. We have to get the benchmark returns.

Steel Executives

Technology transfer has also improved under globalization. The industry in the previous 20 years had become increasingly reliant on international technology licensing and transfer to try and stay abreast of the latest and greatest in steel technology and applications. However, those who worked with technology licensing are of the view that the vendors never provided the absolute best-of-breed solutions.

We only ever got about 2/3 of the knowledge. We never got the best talent and latest stuff. We would get 590 but meanwhile the other companies had moved on to 780. We never got what we contracted and paid for.

There is fuller access now.

Steel Executive

As indicated in the quotes, under licensing, the local managers were always trying to catch up and never believed that they were getting all that they paid for. Now they believe that they get full access to the complete range of leading-edge technology from around the world.

However, this improved and expanded access to capital and technology comes at a price. The managements of operations are in an intense competition with other facilities trying to get their projects accepted and funded by head offices.

Steel Executives Objectives

Recent research by the author indicates that CEOs of steel companies currently identify five long-term operational and business objectives:7

1. Zero accidents in an inherently dangerous production environment.

2. Zero defects in the face of relentless pressure from quality-conscious customers.

3. 100% reliability for on-time delivery into lean production environments.

4. Ongoing productivity gains through continuous improvement.

5. Penetrating new markets with innovative products, while at the same time achieving constant cost reductions.

This agenda of challenges for managers frames the larger issues discussed in this book. To understand steel management, we have to begin with the global context. New global steel companies manage differently from their classic steel company predecessors.

New Global Steel Benchmarking

A major impact of the globalization of ownership in the steel industry has been the new and rigorous application of international benchmarking norms. Benchmarking applies to all aspects of production and management, including human resources management performance. For local management, achieving benchmarks is critical to compensation as well as attracting new investment and new technology. In the long run, achieving benchmarks is essential to the continued viability of a production facility. They have also become a key driver of innovation at the plant level, including organizational development strategies.

Traditional Steel Industry Performance Benchmarking

Traditional steel industry performance metrics were fairly simple. At the operations level, performance was measured by tonnage volume and capacity utilization. By the 1970s, additional economic metrics were added, utilizing costing expressed as Man Hours Per Ton (MHPT) at the raw steel, hot-rolled, and cold-rolled stages of steel production. The latter became common measures for productivity comparisons between national steel industries. An example comparison table is given on the previous page.

Traditional Comparative Data for Steel Industry Production Costs

Such metrics are still used; however, a new set of measures and practices have been developed for management of multiple operations across nations and regions.

Reference Mill Labor Productivity Benchmarking

The new companies have developed different sets of metrics for multinational operations based on reference mills. How they individually implement this varies considerably by company. In the following discussion, Ameristeel is a US-based steel company with operations in North America and Europe. Eurofer is a large European-based steel producer with multiple steelmaking operations across all product markets in North America and around the world. Metallos is a South American-based steel maker primarily focused on the energy industry in all major markets.

Ameristeel Case

Ameristeel bases its mill metrics on a single reference mill, a key flat-rolled steel facility in the United States. All other facilities, in America and in Europe are based on this one reference point. It is a labor time metric based on the full time, direct labor costs expressed in terms of the number of employees per production department and at each stage of the production process. It is basically a head count metric.

The facility work force is segmented into Active employees, Laid-Off, Active Retirement-Eligible, and Collective Agreement-based. The labor productivity cost is calculated based on the Active Employee totals and number of employees by Department. The units are numbers of Employees. For reasons of confidentiality, only the categories not the actual figures are included.

|

Departments |

Primary steelmaking operations only (No. of employees) |

Hot-rolled coils (primary and zinc line operations) (No. of employees) |

Cold-rolled (primary and cold rolled operations) (No. of employees) |

Total (No. of employees) |

|

Operating |

||||

|

Coke |

||||

|

By-products |

||||

|

Blast Furnace |

||||

|

Raw Materials |

||||

|

Steelmaking |

||||

|

Conditioning |

||||

|

Pickle Line |

||||

|

Ops Services |

||||

|

Bloom & Bar |

||||

|

Total |

||||

|

Maintenance |

||||

|

CO/BF |

||||

|

Steel Making Maintenance |

||||

|

CRC/HRC Maintenance |

||||

|

Ops Services Maintenance |

||||

|

B&B |

||||

|

Plant 24/7 Maintenance |

||||

|

Total Maintenance |

The labor cost-based productivity comparisons are then used to benchmark domestic and international plants in comparison to the Reference Plant on a monthly basis. The results are then aggregated into the relevant product line, in this case flat-rolled steel products.

|

Facility |

4Q09 (No. of employees) |

1Q10 (No. of employees) |

2Q10 (No. of employees) |

|

Reference Mill |

|||

|

Mill1 |

|||

|

Mill2 |

|||

|

Mill3 |

|||

|

Flat-Rolled Total |

Eurofer Case

Eurofer has a much more ambitious set of performance benchmarks. They operate in many countries and identify three reference mills for flat-rolled steel, one each in Europe, North America, and South America. The performance and practices of these three provide the template for the others in the group.

The Eurofer Benchmarking Program Objectives include: Health & Safety, Organizational Effectiveness, Repair, Maintenance & Capex, Energy and Other Costs, Quality, Environment Improvement Programs.

Major contributors to differentiation between facilities include asset configuration: size, age, volume of facilities; operating practices: sinter versus pellets, etc.; and, local plant factors: wage levels, labor standards, and raw material logistics. Among the measurement challenges for these reference mills are ever-changing exchange rates, product mix, and employment practices, which can cause significant shifts in the ranking as shown in the examples below.

Benchmarking Metrics

|

Mill 1 |

Mill 2 |

Mill 3 |

|

|

Total #FTE (own, contracting, overtime) |

No. of |

No. of |

No. of |

|

Ratio own FTE/total FTE |

% ratio |

% ratio |

% ratio |

|

TCOE |

$ per year |

$ per year |

$ per year |

|

Total contractor cost |

$ per year |

$ per year |

$ per year |

|

% cost employees in total contractor cost |

% ratio |

% ratio |

% ratio |

|

Compare avg cost own FTE |

% ratio |

% ratio |

% ratio |

|

Avg cost contractor/cost own fte |

% ratio |

% ratio |

% ratio |

|

# own blue collars/total # fte |

% ratio |

% ratio |

% ratio |

A surprising finding is that contracting out is often more expensive than in-house costs. Contracting out is historically cheaper in South America but exchange rate changes are rapidly eroding this advantage. The cost metrics are then used to rank relative performance of the Reference Mills across global operations. As can be seen below, places in the ranking tables shift at various times between the different regional mills.

|

Comparative Mill Productivity Metrics 1: Ranking Shipments/FTE own + overtime + contractors |

||

|

2008 |

2009 |

2010 |

|

Mill 1 |

Mill 2 |

Mill 2 |

|

Mill 2 |

Mill 1 |

Mill 1 |

|

Mill 3 |

Mill 3 |

Mill 3 |

|

Comparative Mill Productivity Metrics 2: Ranking HRC/FTE own + overtime + contractors |

||

|

2008 |

2009 |

2010 |

|

Mill 1 |

Mill 1 |

Mill 1 |

|

Mill 3 |

Mill 2 |

Mill 2 |

|

Mill 2 |

Mill 3 |

Mill 3 |

|

Comparative Mill Productivity Metrics 3: Ranking Employment cost/tons shipped |

||

|

2008 |

2009 |

2010 |

|

Mill 1 |

Mill 1, Mill 3 |

Mill 1 |

|

Mill 3 |

Mill 3 |

|

|

Mill 2 |

Mill 2 |

Mill 2 |

|

Productivity Metrics 4: Comparative Mill Employment cost/HRC: Ranking |

||

|

2008 |

2009 |

2010 |

|

Mill 2 |

Mill 3 |

Mill 2 |

|

Mill 3 |

Mill 2, Mill 1 |

Mill 3 |

|

Mill 1 |

Mill 1 |

|

To add complexity and give more granularity to management metrics, Eurofer is moving to asset-based measurements. Within the reference mill set, the facilities have been disaggregated into asset groupings by department and function.

Productivity Mill Metrics: Asset-based: No. of Employees

|

Asset area |

Mill 1 No. of employees |

Mill 2 No. of employees |

Mill 3 No. of employees |

|

Primary |

|||

|

Finishing |

|||

|

Maintenance |

|||

|

Executive Team |

|||

|

HR |

|||

|

Health & Safety |

|||

|

Infrastructure |

|||

|

Support Services |

|||

|

Metallurgy & Quality |

|||

|

Continuous |

|||

|

Engineering |

|||

|

Environment |

|||

|

Process Automation & Modeling |

|||

|

IS/IT |

|||

|

Purchasing |

|||

|

Warehouse Operations |

|||

|

Customer Service |

|||

|

Order Fulfillment/Production Planning |

|||

|

Finance/Controller |

|||

|

Central Warehouse/Plant Stores |

|||

|

Utilities |

|||

|

Sales |

|||

|

Total |

No. of Employees |

No. of Employees |

No. of Employees |

Eurofer also uses their three reference mills to do on-going experiments. For instance, Mill 1 is used to benchmark Maintenance practices. Mill 2 is the reference for Contracting Out practices. Mill 3 is being used for Knowledge Management practices for the production work force. Within this again, there are developing metrics for Human Resource functions and organizational effectiveness and innovation.

Steel Benchmarking and Time Metrics

In addition to these labor-based productivity metrics, benchmarking is also being applied to time utilization in new and finely grained ways. Steel, like all continuous, capital-intensive operations have always used the language of Up Time and Down Time, because profitability only really begins at about 80–83% of capacity utilization. More recently, with the incredible pressures of cost and delivery, things have been taken to a new level. Stoppages are the variable factors.

Metallos Case

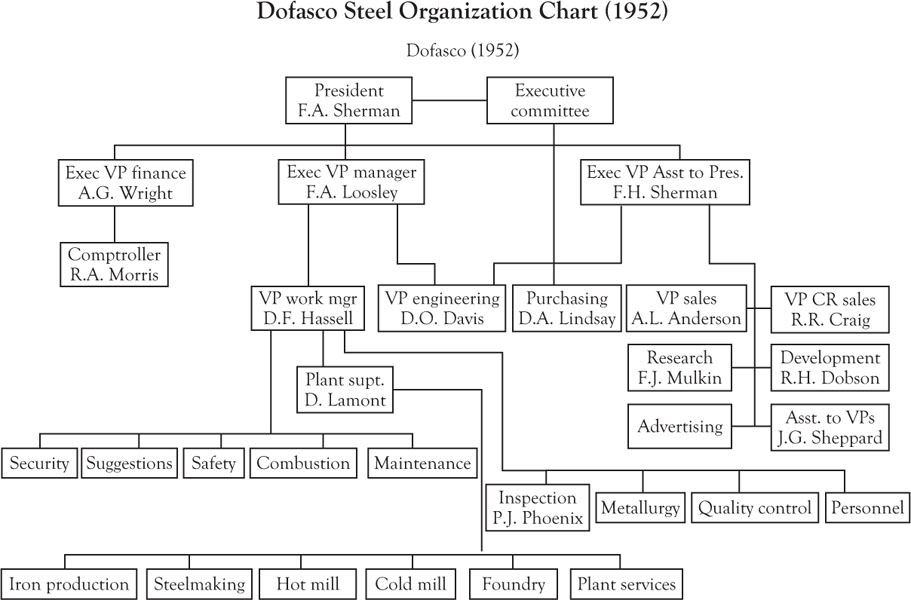

Metallos has what appears to be the most top-down engineering-driven metrics for capacity utilization and “up time.” Because the company produces products for the global energy industry with central supply contracts, their objective is a single industrial system standardized across operations around the world, to guarantee product technical specifications and quality. It is particularly directed to issues of time metrics for continuous production.

Metallos’ methodology uses Calendar Time, Possible Time, Available Time, and Effective Time to generate a new set of ratios. Calendar Time is the time included in the period under analysis, for example, 24 days, 744 h per 31 day month, 365 day years. Structural Stoppages are times when the line does not have the crew to operate for structural reasons: holidays, union activities, rest periods, nonscheduled shifts, production suspensions, unscheduled maintenance, and vacations. Possible Time is the time the line is fully prepared to operate. Stoppages include scheduled repairs, change overs, peak energy periods, previous stoppages and subsequent startups, lack of demand, lack of energy, new technology installations, raw material shortages, logistics interruptions, weather, and preventive work. Available Time is Possible Time minus Stoppages. Effective Time is the time the line is actually running.

These definitions give rise to the following calculations:

These ratios are then applied to benchmarking matrices within and between facilities as shown in the following table.

Time-Based Productivity Metrics

|

Actual (No. of hours) |

Objective (No. of hours) |

Var vs. obj % ratio |

|

|

Calendar Time |

|||

|

Possible Time |

|||

|

Available Time |

|||

|

Operations Delays |

|||

|

Nonoperations Delays |

|||

|

Total Delays |

|||

|

Calculations |

% Ratio |

% Ratio |

% Ratio |

|

Utilization (Effec/Avail) |

|||

|

Utilization (Effec/Poss) |

|||

|

Utilization (Effec/Calendar) |

|||

|

Efficiency (Perf/Util) |

|||

|

Productivity (tons/effect hr) |

|||

|

Productivity (SRM pcs/ effect hr) |

Taken together, these new and sophisticated labor productivity and time metrics are being integrated with the conventional financial metrics in assessing steel company operations. They directly impact executive compensation and capital allocation decisions. This is an entirely new way of managing steel operations from the simple internal hierarchies of the past.

Global Supply Chains and the Reverticalization of Steel

About 70% of steel company costs are related to raw material inputs. Therefore, how a steel company manages its raw material supply chains is critical to its survival. To illustrate, we will look at the case of metallurgical or “met” coal. Met coal stands at the most upstream of all of these production activities. Even the seams of coal in the ground at the mine have critical properties for the whole downstream processing and product development.

Coal is seen by many as the ultimate industrial commodity. It is black, dirty, and bulky. Much like steel itself, it is a classic of the old, industrial economy. However, coal is now in transition as a value-added resource input to advanced steel manufacturing. In academic language, this has meant a classic shift from commodity production to its full integration into the value chains of the new steel industry.

The seams of coal at the mine have critical chemical and physical properties. Once the coal is out of the ground its properties cannot be changed. It can only be blended with other grades. The extracted coal is separated and managed in terms of these elemental properties. At the mine operations level, these coals are blended into standard mixes and are labeled “components” for the subsequent processes. In global steel, reliance on seaborne coal is the new standard practice. The coal is moved in unit trains to terminals on the coast. It is there that the components are combined into “products” to match the specific grades steel-producing customers have specified as the “recipes” they need for steelmaking downstream. This takes place literally as the coal is loaded on to the vessels. Products may even be segregated within specific holds on the bulk carriers. A typical coal producer may produce eight to ten components, which are later blended into 20 different products.

The most desirable product in global metallurgical coal is HCC (Hard Carbon Coal) preferably with medium volatility. The prime grade HCC coals are scarce and much desired because they ultimately have major impacts on the efficiency of the steelmaking units in the mills and thereby affect productivity, profitability, and product quality for the steel companies. The highest grade HCC is critical in the Blast Furnace because of its chemical properties and also because it is strong enough to keep the sides of the furnace from caving in. This is most important with the newest generation of large-diameter blast furnaces developed originally by the Japanese, then extended by the Koreans and now being installed in the new mills in China and India.

There are only three established sources of this HCC with premium qualities: Australia, Western Canada, and the USA. The latter’s sources are rapidly dwindling, leaving Australia and Canada as the lead competitors. The former have about 65% of the market and the latter about 35%. This is the heart of the HCC seaborne market. There are potential new sources in Mongolia and Mozambique, but significant political risks and infrastructure development challenges constrain their early entry into the international market place.

For coal companies, transportation and distribution costs are their highest fixed costs. National, country-specific railway freight rate determination by public agencies has become wild cards for price and development decisions. The Regulator is more concerned with system maintenance costs than optimization of the specific supply chains that undergird the whole of the system. In addition, there are coordination and access issues around the terminals and access in general at the ports. Getting the coal shipped has become as complicated as its extraction and grade determination.

The actors and regulators of the supply chain should step back and take a breath while they reconsider the interrelationships and long-term interests of the met coal producers and the optimization of the supply chain. To take one example: if unit costs of transportation can be reduced by optimizing performance through use of larger trains, better traffic coordination and more effective access to ports and terminals, then this feeds back directly into economics of mine operations. Reduced fixed costs for transportation will allow the mine operators to literally go deeper in their seam cuts, utilize larger mines with longer ore body life, improved economics for all levels of extraction, make the mines more productive, and employ more people for longer. It should probably result in higher not lower revenues for system operators, railways, and terminals in the long run.

Virtually, all industry observers give optimistic outlooks for metallurgical coal for the next 10–20 years. The fundamental driver is Chinese steel demand to support huge steel-intensive infrastructure projects. Demand especially for high-quality HCC coal will exceed supply for the foreseeable future.

Prices movements may be a different issue. Mining conferences and business publications have been filled with excessive exuberance about a China-led super cycle in metal prices that is expected to run for decades. Financial markets seem to have bought into the story. However, there are good reasons to be skeptical about such a one-way economic forecast. There is an important debate going on in resource economics about this theory, especially in the light of the setbacks in 2008–2009.

In summary, the counter-argument is that there is not a one-way up escalator in metal prices. Steel in particular has always been a cyclical market and that factor is still with us. Demand from China is a huge story but locational factors may account for at least another one-third of the movement in prices. The other issue is historical supply problems. We are still reaping the downside of inadequate investment in mine development from the 1990s. All these factors should be considered both with respect to coal and metal price forecasts in general as well as mine and supply chain performance if the potential of the industry in future years is to be realized.

Implementing supply chain management successfully leads to a new kind of competition on the global market where competition is no longer of one company versus another company but rather it takes on the form of one supply chain versus another supply chain.

A value chain is a chain of activities for a firm operating in a specific industry.8 Products pass through all activities of the chain in order, and at each activity the product gains some value. The chain of activities gives the products more added value than the sum of added values of all activities.

Value chains are networks, and the academic literature9 distinguishes three basic types: modular, relational, and captive.

The Coal Chain is clearly not modular like the electronic and auto chains with closely specified OEM–supplier linkages, where the lead firms design platforms with tight material and performance requirements, which are then turned over to the suppliers to design, produce, and validate. Coal is not a widget. Even though coal producers have adopted the language of “components” they are not modular components, like parts and subassemblies are in the auto industry for instance. A coal company is not a Tier 1 auto parts supplier.

Coal, like iron ore, was once a predominantly captive supplier. Steel companies owned their own mines. As discussed above, the pressures on steel companies in the 1980s and 1990s, particularly in North America, to cut costs and revive profits, led them to largely divest of their iron ore and coal holdings. This was followed in the 1990s and aggressively in the 2000s by consolidation of coal producers into their own separate globally integrated companies. Buyer power, which was traditionally held by the steel companies, has now been replaced by Supplier power, most dramatically in iron ore and less so but importantly in coal.

However, this has to be qualified by understanding how the actual transactions take place. As described above, coal right from the seam is specified according to the product strategy and even the physical configuration of furnace facilities at individual steel companies and even specific mills within those companies. Hence, the all-important role of specification of the “recipes” needed for coal within the production parameters of the different mills. For this reason, the best characterization of the Coal Chain is that it is relational. Coal is not simply sold on an open market where price is the only factor. Much more information is required as the basis of the interchange between coal producer and steel producer. This inherently makes the transaction relational.

While there is much current discussion and speculation about whether steel companies will revert to direct ownership of mines, there are good reasons to believe that the story will play out differently between iron ore and coal. Many observers and commentators equate iron ore and coal but there are critical differences. Iron ore mining is much more concentrated and there is no alternative for integrated steel producers. Coal mining is less concentrated and there are other options: pulverized coal injection (PCI), natural gas, directly reduce iron (DRI), etc.

For this reason, while there may well be ownership changes in coal, including steel companies buying interests or shared ownership, the fundamental character of the Coal Chain will by its nature remain relational.

These issues of raw material supply in steel raise important questions in current industrial economic theory. Value chains capture the process of sequential transformation from inputs through stages of transformation to outputs and through to distribution and final consumption. It is related to transactional cost economics and based on three criteria: complexity of transactions, ability to codify transactions, and capabilities of the supply base. The increased complexity of global supply chains is changing our perspective on steel company economics.

There has been a major change in restructuring and locational decisions for steel facilities and capabilities.

The fulcrum of global steel development is raw materials and energy. It rises and falls on the cost structure. This follows the other metals groups like globalization in aluminum.

The key is Brazil. It has this incredible base in low cost, high purity iron ore.

Steel Consultant

The major restructuring of the industry in the 1990s saw steel companies looking to disaggregate their operations horizontally (i.e., focus on what you are good at). Now the industry has been challenged to reverticalize. As mentioned, the trigger was the impact on steel prices and the cost of raw materials accompanying China’s emergence as the leading steel power in the world. The story is told by a group of international steel engineering consultants.

Twenty years ago the companies disaggregated (do what you are good at) then with the rise of China and shortages/rising prices for raw materials, there was a wholesale re-aggregation and consolidation in the industry. It has turned around 180 degrees.

Steel Consultant

Ownership of iron ore and control of costs became strategic. Companies have leveraged back to the iron ore stage. It is the big competitive advantage. It is where Brazil has such an advantage. It has the cost advantage in iron ore and plays it through to the slab stage.

Steel Consultant

The key variable in accessing the lowest possible raw material costs has raised Brazil’s profile for investment decisions. As suggested, Brazil may actually be a more important steel company restructuring in the coming decade than China. Companies have focused new capacity investment on Brazil at least for raw material processing up to the slab stage.

China may not be such a big story because it has to import everything and has such bad infrastructure.

Steel Consultant

Company operations will be impacted by decisions to locate basic production facilities close to the cheapest raw material inputs. Finishing capacities can then be located wherever the end-user markets are located.

There is a New Steel Paradigm

The old view was that raw materials were ore and coal.

The new view is that raw materials include right up to the slab and even hot band stage.

The end user only comes in at the finishing stage. You locate that close to the market.

Brazil is positioned to play this strategically but isn’t there yet.

Steel Consultant

The big guys with ownership and control of resources will be able to choose where their intermediate products are positioned.

Value added will be assessed at each step in the chain of manufacturing and assessed in terms of the capital required.

Steel Consultant

There are two significant implications of this shift. In the past, raw materials simply meant commodity grade iron ore and coal, but now steel companies regard raw materials as including everything up to the slab stage and perhaps even the hot-band stage. This may have dramatic implications for the nature and scale of North American steel facilities in the coming decade. The test case of this is being played out in the new Thyssen facility in Alabama where all the raw materials up to the slab stage will be imported then the finishing will be specialized to feed the local auto plants. The international location of raw materials versus domestic processing capacity can fundamentally change how steel companies operate in the future.

The Steel Company of the Future

Where does one find a model for the steel company of the future?

Boeing may be as a good an industrial corporation reference point as any for operations of the new networked manufacturer. It was and is one of the premium manufacturing companies in the world. Its past was anchored in a deep aeronautical engineering and machining culture with strong social ties to Puget Sound. In the 1990s, it faced persistent dissatisfaction from investors and financial markets for its inability to generate consistent strong earnings, even when orders were buoyant. In response, it acquired McDonnell Douglas. In retrospect, this was a tipping point for changing the culture of the company.10

Modularization has been an important feature of Boeing’s production system ever since the divestiture decision in the 1950s forced it to spin off its engine division into what would become Pratt & Whitney.

However, with the development of the 787 Dreamliner, Boeing took on the new role of system integrator. Traditionally, it pursued a rigorous system of boundaries on key information in which its Tier 1 and Tier 2 suppliers had a directive to simply “build to print,” that is, build a component to specifications as provided. In general, Tier 1 suppliers are the upperend producers of subassemblies, while Tier 2 producers supply the former with individual parts. Tier 3 producers such as stampers are the furthest upstream the supply chain.

Two factors caused the system to move in a new direction. The sheer costs to developing a new plane exceeded what even Boeing could afford. Therefore, it looked to its suppliers to co-fund development with the inevitable consequence that they acquired a greater share of production knowledge and the levers for incremental improvement. Also, as Boeing pursued foreign sales, particularly in Asian markets, it conceded more production control and related knowledge to foreign operations. For example, Mitsubishi is close to Boeing in terms of its proportion of the final manufacturing content and share of value added for the air frames “made” in Seattle.

In the past How to Build a Commercial Airplane was the proprietary bible for Boeing engineers, incorporating 50 years of learning. With the 787 Boeing “opened” the Book and provided suppliers with performance specifications for parts and components and collaboratively worked with them in the design and manufacturing of major components such as the wing, fuselage section, and wing box. With assemblers sharing more of the “secret sauce” with suppliers, incremental technology improvements are increasingly likely to be replicated across multiple aircraft platforms. This becomes a strategy of sustaining innovations by migrating value from assemblers to Tier 1 suppliers.

More than 90% of the 787 is outsourced to a global multitiered supplier network. Boeing has sought to commoditize most components manufacturing while retaining strategic assembly expertise and proprietary processes for manufacturing selected key items. The objective at the Boeing end is that value migrates to and stays with the systems integrator.

There are tensions and competing interests in even the most advanced supply chains. For instance, in the value-added of a car, about one-third of the cost is logistics. It is premature to assume that the mere presence of time–space shrinking technologies in transportation and communications have eliminated these problems. The problems of actually moving materials, components, and final products still confront the increased complexity and geographic extension of production networks.

The Boeing Systems Integrator model for global manufacturing is still facing growing pains. The company has changed its self definition from manufacturer to designer and assembler. Famously, the 787 Dreamliner has been designed and coordinated through a distributed computer system with final assembly in Seattle being reduced from 30–40 days to 3 days. Even the holiest of holies, the manufacturing of the wings, is now done by Mitsubishi in Japan. While the concept and digital architecture may be leading edge, the implementation and administration of the new systems is incredibly complicated and uncertain. The time delays and associated penalties on the Dreamliner are reported to be in excess of $10 billion.

Arcelor may be the closest analog in steel to Boeing, seeking to use financial and performance metrics to coordinate a new kind of global steel company: the systems integrator. Another reference point is the ambitious attempt, being led by Thyssen Krupp, to have a control room in Rotterdam doing real-time coordination of shipments of iron ore and slab production in Brazil to producing plants in Europe and America within detailed specs and just-in-time schedules of lean production manufacturing customers. It is reported that there are continuing operational issues in its implementation.

Systems Integrator is an appealing concept as the organizing principle for the steel company of the future. However, getting there will be even more challenging than it has been for Boeing. The complexity of upstream supply chains and the fact that the steel company is not the final user makes the situation both more complicated and riskier. Alternatively, steel companies may not move forward to system integration. They could move one step back and limit themselves to reintegration of steelmaking and raw materials production in house.

In summary, supply chains are contested economic terrain. At the end of the day, a steel company may not have the power position of an automotive or aircraft OEM to play the full system integrator role in the future.