A prom without dancing, like a courtship without romancing, is steeped in illusion and mired in confusion, its failure a foregone conclusion.

—© 2013 Sage Sayings™

Introduction to Financing Your Firm’s Growth

Some things are wanted but not essential. A major essential for each business is the financing of the enterprise. Business owners generally are more focused on product or service quality, production, marketing, and management. Financing is usually an afterthought. That being the dominant situation, an overview of both the sources of financing, and the process of obtaining financing specific to the needs and stage of your firm is absolutely essential; since, as your firm grows, your need for financing expands substantially. To achieve this growth, you must be prepared to respond effectively to several challenging questions in the area of financing: (1) What are the various sources and types of financing that are available? (2) Who are the providers of this financing? (3) What do the providers of this financing look for in making their decision of whether or not to provide financing to your firm? (4) What do you need to do to meet the specific requirements of funding providers?

This chapter provides an overview of both the sources and types of financing available to small businesses, as well as a review of the processes associated with obtaining such financing. It is designed to assist you in understanding and finding the various sources of financing that you might need for the specific stage(s) of your business as well as the costs of such financing, and what you can do to obtain that financing. You are encouraged to be proactive in searching for sources that might be specific to your individual circumstances.1 For example, there are sources set aside for minority-owned firms, firms operating in the inner cities, women-owned firms, and firms owned and operated by military veterans. These sources might be made available by various levels of government (local, state, federal) as well as foundations, in various forms—including loans and grants. As your business grows, new sources will be needed; it is imperative that you familiarize yourself with the various sources available, and anticipate when you will need these. You should also strive to formulate a set of financial statements that will allow for easy access to funds. Table 3.1 provides a list of sources that will be covered in this chapter.

Table 3.1 Sources of financing

|

Self-Financing Personal Savings Mortgages and Home Equity Loans Pension Funds Whole- and Universal-life Insurance Policies Credit Cards Friends, Family, and Associates State and Local Government Community Development Corporations U.S. Small Business Administration Liability-Based Financing Accounts Payable Accruals: Wages and Salaries Asset-Based Financing Inventory Accounts Receivable Specialized Assets: Sale and Leaseback Real Estate Patents, Copyrights, etc. Profit from Operations Finance Companies Commercial Banks Credit Unions Angel Networks Venture Capital Crowd Financing Initial Public Offerings |

Each of these sources of financing will be reviewed in detail. As Table 3.1 shows, in addition to yourself, friends, family, and associates (FFA), financing providers include community development banks and credit unions, state and local government programs, the U.S. government’s Small Business Administration (SBA), finance companies, commercial banks, venture capital firms, and angel networks—individuals with a strong interest in achieving the types of objectives your company epitomizes. Each provider has different criteria and different expectations. Some, like FFA and angel investors, are more strongly interested in the type of product or service that your firm provides, with profitability playing a secondary role (for these people, the service is most important). Others, such as finance companies and commercial banks, are more interested in your past and future financial and profitability performance, with a particular interest in your ability to pay both the principal and interest on your loans. Governmental providers are specifically interested in your ability to add to the growth, employment, and development of the community in which your business operates; thus, various agencies provide such things as direct grants, incentives (e.g., reduced taxes), and loans with lower requirements. Providers such as the SBA offer a number of venues of support for your business, the most important for our purposes here being the provision of backing your commercial bank loan up to 70% in some cases. This typically results in a lower interest rate for your loan, due to the substantial reduction in the probability of a loss by the bank if your firm fails to repay.

A major question that will be answered for each type of financing is what you need to do to meet the requirements of your source. For many of the sympathetic sources, your business model itself answers that question. However, for finance companies, banks, venture capitalists, and equity investors, the answer is embedded in your financial statements and financial performance, both historically and in the future. The assessment includes the effectiveness and quality of your management team, the ability of your company to pay its debt, your ability to control costs, the strength of your market, and the quality of your marketing strategy. Commercial banks and finance companies will require you to create a strong loan package. Later in this chapter, there will be a review of the major financial ratios that these lenders examine, as well as the most important factors lenders consider in the loan package that you submit. The review will also include a list of the top qualities that most bankers and investors find important in making loan decisions.

Overview of Sources and Types of Financing

Over the years, in the course of interviewing and training entrepreneurs, the authors of this book have seen that, typically, in the beginning stages of a business the primary financing sources tended to be from personal savings, second mortgages on a home, home equity loans, and systems of revolving credit cards. While these sources can often work temporarily, as the business grows, more funding is needed than these sources can provide. The next set of sources tapped is relatives and friends. These sources are often quite sympathetic to the efforts and concept of your business, and are generally very supportive and often happy to provide such assistance. Indeed, it is for this reason that funds secured from FFA are often referred to as love money. You might, actually, find many friends through modern social networks such as Facebook. However, at a certain point in the growth of your firm, these sources also are exhausted. It is important to note here that the major sources of financing listed in Table 3.1 are in an approximate order of alignment with the general growth stages of your firm. That is, in the early start-up stage, you will tend to draw from self-financing, family or friends, and possibly angel investors. At the middle stage of growth, you will need to shift to finance companies, then commercial banks. At some point, you might then decide to access external equity investors, through such mechanisms as crowd financing, venture capital firms, and initial public offerings (IPO’s). In addition, the external sources (those beyond self-financing and friends) tend to progress from debt to equity.

Self-Financing: Using Your Own Resources

In the early stages of an enterprise, financing from outside sources such as banks and finance companies is difficult to obtain, since these sources usually require a three-to-five-year financial performance history. Therefore, most of your initial financing must come from your own sources, such as personal savings, real estate, pension funds, whole-life and universal-life insurance, and credit cards.

Mortgages and Home Equity Loans

A natural first place to raise financing is through real estate that you already own, such as a home. If you already have a mortgage on your property and the market value of the property is substantially greater than what you owe on the existing mortgage, you might be able to obtain a home equity loan, a second mortgage, or if mortgage rates are low you might consider refinancing your existing mortgage. Indeed, in recent years, low mortgage interest rates have provided a great opportunity for this type of financing, especially if the market value of your property substantially exceeds the balance on the existing mortgage. In terms of prioritizing, generally, refinancing—that is, paying off your old mortgage completely with a new mortgage—is the most preferred method since first mortgages have fewer restrictions and penalties. Of course, the downside of using mortgages and home equity loans is that, if your business fails and you go into bankruptcy, you will lose your home. Also, if you used a home equity loan, it is a recourse loan, and therefore, even if you sell your house at a loss, the lender will have recourse to the full value of the loan.2

Pension Funds

If you have a defined contribution pension fund, such as a 401(k) or 403(b) plan in which you are currently vested, you may be able to draw or borrow from it. Most other pension plans such as Individual Retirement Accounts (IRA’s), Simplified Employee Pension Plans (SEPP’s), and so forth, do not allow you to borrow. Moreover, if you are age 59.5 or older, you are also able to withdraw funds from your pension fund without penalty. Generally, if you have 401(k) or 403(b) accounts and are younger than 59.5, you will be allowed to borrow up to 50% of the amount vested. However, plans do have different rules, and you should check your specific plan for the details.

In the case of borrowing, you will be charged an interest rate and will be given a time period in which to restore the amount borrowed. Also, you may face a 10% penalty from the Internal Revenue Service if you fail to restore the amount borrowed. In the case of a withdrawal, you should be aware of the fact that the plan will distribute to you the after-tax amount. Thus, if you need $20,000, you should request a higher pretax amount. For example, if your tax rate is 20% you would need to request approximately $25,000 in order to receive $20,000 after taxes.

Whole- or Universal-Life Insurance Policy

Another option for borrowing is your whole-life or universal-life insurance policy. In most cases, you should be able to borrow against the full cash value of your whole-life insurance policy. Fundamentally, you are obtaining a loan from your insurance company, which is holding your cash value as collateral. Again, this type of borrowing may come with several charges. For one, you will usually sacrifice any dividend payments that would have been earned on the cash value of your policy; in addition, you will usually be charged an interest rate on the amount borrowed. In general, there is usually no set repayment schedule. The interest rate is usually a fixed rate, and may be as high as 7%. However, this 7% plus the lost dividend payment can add up—especially over time. Furthermore, the interest charges will be accumulated in the loan balance. Universal-life loans differ from whole-life loans in that the loan balance on a Universal-life loan is usually placed in a guaranteed fund which earns a much lower interest rate than your policy. Thus, the total interest cost to you is the interest charged plus the difference between what you would have earned on the universal policy and what you earn on the guaranteed fund. Borrowing from your whole-life policy certainly trumps borrowing at high rates from your credit cards, and, it is also tax free. However, it does have the additional downside that, if not paid back, your death benefits will be reduced by the unpaid interest charges and the balance of your loan. Overall, you should discuss this with your life insurance agent or customer representative of your insurance company to obtain the full set of charges that you will incur.

Credit Cards

While not highly recommended, many entrepreneurs have effectively used credit cards as a source of financing. Still, it is a good idea to obtain more credit cards and extend your credit limits while you are employed, if you are thinking of starting a business in the future. Credit cards are easier to obtain than most other financing. On the other hand, the use of credit cards does require continual attention to payment plans and details. You should consider taking advantage of offers such as 0% interest for six months, no fee charges for one year for balances and transfers, and bonus points and rewards such as gift cards for a certain amount of purchases made within three months (say $4,000). However, many credit card companies are aware that consumers take advantage of these promotions and are beginning to charge higher fees.

A major downside of using credit cards is, of course, the high interest rates that must be paid—as much as 19% to 26% or higher. It is imperative that you read every detail of your credit card contract and fully understand all the charges that you may face, such as high late payment fees and jumps in interest charges when late payments occur. Generally, firms that overuse credit cards during the earlier phases of the businesses have a high percentage of failure rates. Personal credit card debt or business credit card debt, if you are not incorporated, will be a debt that needs to be paid by you in the case of bankruptcy. Many business owners have used credit cards to make payroll during emergencies. However, if you do use credit cards, these should not be used for high capital expenditure purchases. High credit card debt and slow payment will also hurt your credit rating and compromise your ability to obtain a bank loan. In addition, missed payments can cause significant jumps in your interest rate—up to 29%+. Nonetheless, there is a positive aspect to using a business credit card and paying on time. Obtaining a good payment record will help to improve your credit rating and provide a credit history that will assist in getting a bank loan.

Credit cards also carry insurance and provide protection against fraudulent suppliers. In essence, a judicious use of credit cards can be helpful, but extraordinary caution must be used to avoid overusing these cards and incurring heavy debt. It is true that 33% to 40% of small business start-ups use credit cards. The key is to use this financing source to enhance your credit rating.

Network Funding: FFA

Depending on the projected size of the business, few people will find personal sources of money to be sufficient to fund the business start-up. This means that, even if the business is initially financed by your own money, your own cash will need to be augmented by other sources of financing. It is at this point that most people will resort to tapping into personal and business networks.

You might consider relatives as a supportive funding source. Many relatives are eager to see another relative succeed in business. Similarly, close friends with whom you have established a good relationship over the years might also be very prone to provide financial support. Earlier, these sources of financing were referred to as love money. In addition, people in your personal or business network, who are not as close to you as your relatives or friends (associates), sometimes will also tend to be quite supportive. One marvelous feature of this is that these are folks who know you well (relatives and friends) or well enough (associates), and have great or sufficient trust in your character, prudence, and integrity, and are generally patient in terms of waiting for a financial return. These people are usually willing to invest at a lower interest or payout rate. Of course, the risk is that, over time, the initial enthusiasm might dissipate, and hard feelings could develop. Nonetheless, for many, this is a good source of funding.

There are, however, two major caveats that you should always consider before resorting to using FFA financing. First, remember that your spouse has an important role in your financial matters, even if not directly involved in your business. This means that you must be cognizant of the fact that, in the unfortunate case of a divorce, community property states can wreak havoc on a business. Secondly, you should not borrow from any single member of your FFA a dollar more than these individuals can afford to lose. In this way, you are able to avoid the painful situation of any one of these supporters losing entire savings or a home due to the losses resulting from having invested in your business.

Exploring Public Funding

Public entities are typically quite interested in promoting the start-up and growth of businesses. The reasons for this are twofold. For one thing, small businesses create anywhere from 67% to 75% of new jobs, depending upon the source consulted. Clearly, all levels of government are very much invested in the notion of ensuring that the population is maximally employed. Another reason for interest in business start-ups and expansion (not totally distinct from the concern about employment) is that such businesses add to the tax base. While the federal government is not mentioned as a direct funding source in the section that immediately follows, it is quite prominently engaged in guaranteeing small business financing through the SBA, which is, thus, included in this section.

Community Development Funds

Throughout the nation, there exist numerous community development institutions. These institutions are provided funding by the Community Development Financial Institutions Fund, backed by the U.S. Treasury Department. Various types of financing are then provided to community development financial institutions, such as banks and credit unions, which, in turn, provide financing for businesses to enhance the development or redevelopment of specific communities. The most recent development in this area has been the CDC/504 plan, which is discussed later in the section regarding SBA programs.

State and Local Government

In anticipation of exhausting self-financing and funding from FFA, you should begin to look to state and local governments for any special financing programs that have been specifically developed for businesses with your profile. There are many programs offered by state and local governments for various areas. For example, at just about every state and local website, you can find lists of sources of loans, tax shelters, as well as other incentives for assisting your business.

SBA Loan Guarantee Programs

The U.S. Small Business Administration (SBA) assists small businesses in a number of areas in terms of obtaining loans. The major programs are the microloan, the 7(a) loan, the CDC/504 loans, as well as a number of other guaranteed loan programs for debt financing. Overall, the SBA programs provide longer terms, lower interest rates, lower down payments, and more flexible payment options. If there is any downside to SBA-secured loans, it is that, for the most part, these loans are only offered by banks and financial institutions at reference rate + a premium (i.e., these are floating rate loans). In a period when interest rates are low but there are inflationary expectations, such loans could become less attractive than a higher fixed rate loan.

Microloan Program. Through the microloan program, the SBA provides short-term funding to nonprofit financial intermediaries that then make short-term loans to small businesses and nonprofit organizations. These funds are usually used to support working capital needs, such as for inventory, supplies, equipment, machinery, furniture, and fixtures. The maximum amount available to a firm is $35,000.

7(a) Loan Program. The 7(a) program is perhaps the oldest loan guarantee program of the SBA. Under this program, the SBA guarantees loans made to small businesses by banks and other financial institutions. The maturity of these loans can be up to 10 years for working capital such as inventory, 15 years for equipment, and 25 years for fixed assets, land, and buildings up to $5,000,000. There are four general classes of the 7(a) guarantee program: Express Loans (maximum $350,000, variable rates, revolving lines of credit or term loans up to 25 years), Export Loans, Special Purpose Loans, and the Rural Loan Advantage Program. For more in-depth information on the details of each of these programs than is found in this chapter, you should visit the SBA website at sba.gov.

Depending on the loan type and amount, the SBA generally guarantees these loans for amounts between 75% and 85%. In addition, loan amounts can range on the high side to amounts between $500,000 and $5,000,000, depending on the type of loan. Again, depending on the term of the loan, the interest rates on these loans usually run between prime+2.25% to prime+2.75% (short-term loans are typically one-month LIBOR +3%). In addition, you will be charged an SBA guarantee fee that varies based upon the size of the loan from 2% for loans of $150,000 to 3.75% for loans above $1,000,000. More specifics on each type of program can be found at sba.gov, and usually terms and rates can be obtained from the websites of lenders that participate in the programs. At this writing, the Wall Street Journal (WSJ) prime rate is 3.5%.3

The 7(a) program provides a source of funding if you need a substantial amount of money. It will provide a maximum of $5,000,000. In sum the SBA guarantee has the benefits of lower interest rates, longer maturities, and a lower down-payment requirement. The standard maturities are 7 years for working capital, 10 years for equipment, and up to 25 years for real estate. The SBA will guarantee up to 75% of the loan (up to a maximum of $3.75 million).

The SBA Express term loan will provide up to a maximum of $350,000. It can also have the same maturities as the regular 7(a) loans, but has the additional benefits of a more rapid process for obtaining the loan, as well as the ability to finance the SBA fees. It also differs from the typical 7(a) loans in that the SBA will guarantee a maximum of 50%.

In addition to the SBA Express, there are two subexpress types of loans. The first is the patriot express for which veterans and family members of veterans may be eligible. The Patriot Express Loans are for up to $500,000 for the purpose of starting a business and are guaranteed up to 85% by the SBA. The second type of express loan is the Export Express Loans, which may also be up to $500,000 and are available for companies that export goods and want to expand or need working capital to enter a new overseas market. There is also an Export Trade Funding Program for longer terms which provides up to $5,000,000.

Guaranteed Loan Program for Debt Financing. There are two basic SBA programs for line of credit financing: the SBA Line of Credit Express and the CAPline. The SBA Express will provide a line of credit for short-term cash management by providing a revolving line of credit for up to three years. In addition, the SBA fees may also be financed. The Express has an accelerated process and the SBA guarantees up to 50%.

The CAPline is designed to fund short-term cyclical working capital. Terms for this line are set by the lender. The lender can provide, for example, a line of credit for $350,000 to $5,000,000 for a term up to 24 months that is renewable for 12 months at a time, thereafter. The SBA guarantees up to 75%.

CDC/504 Loan Program. Community development companies (CDC’s) are charged with assisting the development of their local communities. The SBA CDC/504 Loan Program differs from the other programs in a number of ways. There is generally no maximum loan amount. This is due to the fact that both the private lender and the business owner can put up as much as each desires. However, the SBA will fund up to 40% of the loan or $5,000,000 ($5,500,000 for a manufacturing firm), whichever is lower. In addition, the business receiving the loan must generate one job for every $65,000 of the loan amount (or one job for every $100,000 of the loan amount for a manufacturing firm). CDC/504 loans are quite recent and are a result of the Jumpstart Our Business Startups (JOBS) Act. These loans are long-term loans made by CDC’s and are provided to small businesses that enhance the economic development of the community.

The CDC/504 loans have basically three additional features. First, the loan from the private-sector lender is secured with a senior lien covering up to 50% of the project cost. Second, a CDC loan which is backed by a 100% SBA-guaranteed debenture (bond) is also secured with a junior lien covering up to 40% of the project cost. Third, the borrower must contribute at least 10% of the financing in the form of equity. This program is designed for projects that range in cost from $100,000 to $12,000,000.

Looking Within the Firm for Financing

Sometimes, the answers to your funding problems can be as close as your own business’s financial position. Knowing the details of your firm’s financial position can be of great help in leading you to viable options for gaining the funds that you need. Many of the alternatives are explained further in this section.

Using Your Firm’s Liabilities and Assets

All businesses have things that the company owns (assets) and things that are owed to others (liabilities). What is useful for you to consider is that both assets and liabilities represent channels for you to achieve the financing that you need. We will now discuss the various ways that this may be done.

Using Firm Liabilities. You might be surprised to learn that you can manage some of your business debts in ways that translate these into quasi-funding sources; but, it is, indeed, possible. This section of the chapter explores how this can be done.

Accounts Payable. Often, in the early periods of a business, the entrepreneur needs to cover periods where the inflow of cash from sales is slow, or the timing of the cash inflows does not match the timing of payments that are due to suppliers. To overcome this temporary mismatch, you might be tempted to stretch the accounts payables, that is, to pay late. One way to avoid this situation is to try to negotiate with your supplier to modify your payment terms so that payments match your cash inflows from your customers. For example, if your customers tend to pay at the end of the month, then try to negotiate end of the month payment terms with your suppliers.

Stretching accounts payables can be costly, however. Suppose your supplier allows you to pay 2/10 net 30, that is, you will receive a 2% discount if you pay in 10 days; otherwise, you must pay the full amount in 30 days. Not taking this discount can be costly. In fact, if you miss the discount consistently for a whole year you will effectively be paying 37.2% more for your supplies! Moreover, if you do not make the payment by day 30, you risk lowering your credit rating, and losing the ability to receive a discount in the future, or you might even be required to pay immediately upon the receipt of supplies. Some finance companies will realize this and will pay your suppliers on time, but they will also charge you a substantial interest rate and other fees for doing so. Overall, stretching accounts payable, or not paying on time is not recommended if it can be avoided.

Accruals: Wages and Salaries. The largest and most easily used accruals are employee wages and salaries. The key aspect of dealing with these is in the structuring of the payments to employees. To optimize savings on these accounts, you should examine whether to pay weekly, biweekly, or monthly. Obviously, more is saved by paying monthly, or biweekly, rather than weekly. Paying wages and salaries monthly will allow more flexibility in your cash management and will also allow more interest to be earned on cash invested in bank accounts.

Using Your Firm’s Assets. Remember that assets are those things that your company owns or possesses. These things can include anything from the tangible items shown on a balance sheet (cash, inventory, accounts receivable, marketable securities, and fixed assets) to intangibles, such as goodwill. When you understand how to convert these assets to relieve your financial burdens, you will have gone a long way toward increasing your ability to make all aspects of your company work to your optimal advantage. Here, coverage will extend to consideration of a number of ways that your company’s assets may be used for this purpose.

Finance Company Loans—What You Need to Know

Finance companies provide a chief source of asset-backed funding. However, funding from finance companies is not inexpensive. You will be charged higher interest rates and other costs, and there may be significant penalties for late payments. Finance companies provide funding predominately by using the firm’s various assets as collateral—most commonly, inventory and accounts receivable.

Using Inventory as Collateral. For many businesses which carry high levels of inventory, such as auto dealers, and so forth, finance companies will provide loans which use inventory as collateral. Such loans allow firms to have expensive inventory on hand and readily available. As the borrower makes payments on the loan, the lender releases inventory for use by the borrower.

There are four types of inventory loans: field warehouses, terminal warehouses, trust receipts, and floating lien loans, each designed to serve particular, specialized needs of the business. Field warehouses set up a warehouse on the business’s plant or store premises, and inventory is not released from the warehouse until the lender provides permission. As inventory is sold, the lender is paid for the inventory, and the borrower retains any profit on the sale.

A second form of inventory loan is a terminal warehouse, which is a central warehouse that is set up reasonably close to the business of the borrower and is used for inventory that is easily and inexpensively transported. This gives the lender more control over the releasing of the inventory.

A trust receipt loan, also called a floor planning loan, is typically used for businesses such as auto dealers. For these loans, the borrower retains physical possession, which means the auto dealer keeps the automobiles on the business’s lot. Once an automobile is sold, the dealer reimburses the finance company for that portion of the loan, and retains the profit.

The final type of inventory loan is the floating lien loan. A floating lien loan is also known as a blanket loan, and covers all types of inventory of a firm. The loan is usually made for a percentage of the book value of the inventory (e.g., 40%). Floating lien loans are usually made at a high interest rate. Consider a situation where you need a loan for $100,000 for the next 45 days. Suppose the finance company offers you a floating lien loan for prime + 6% (say prime is 3%); thus, your interest rate would be 9%.4 Let us further assume that the finance company will advance you 40% of the book value of your inventory. In this case, you would need to put up collateral of $250,000 (or $100,000/0.4). The cost of your loan will be ($100,000 × 0.09 × 1.5/12) or $1,125. Note that the 9% has been annualized for the 45-day loan period (0.09 × 1.5/12).

Clearly, using inventory as collateral can assist the firm through early years. However, like most asset-based financing, it is ultimately more expensive than a bank loan, and in all cases the finance company usually only provides a loan for a percentage of the value of the inventory, and imposes a substantial interest charge.

Accounts Receivable. Accounts receivable represent an asset which may be used for raising funds, either through a process known as pledging or another process known as factoring.

In the pledging process, a lender selects the accounts that it wishes to purchase, usually the accounts receivables of your customers who have the best credit history. The lender will first adjust the accounts receivables for any potential returns or discounts. For example, if the face value of the receivables is $1,000, the lender will adjust the amount to, say, $950. The lender will also apply an aging schedule to your receivables and only accept those that are not well past the normal payment date. Next, the amount the lender would loan you for the $950 pledge will be reduced to, say, 85% of the $950, or $727. The collection of the receivables may be on either a non-notification basis or a notification basis. The non-notification basis means that you will collect the receivables from your customers and then pay the lender yourself. The notification basis means that your customers will be notified that they are to pay the lender directly. Clearly, the non-notification basis is preferred, since some customers might be fearful of the fact that you are using a lender and, therefore, might be concerned that your financial viability is at risk. This could, in turn, cause them to turn to another supplier.

An alternative to pledging is factoring. Factors look for stability and sustainability in your business, customers with excellent credit ratings, and a customer base that is reasonably large with high average size of receivables.

Factors will purchase your accounts receivables at a discount and then proceed to collect the debts. A factor will also select the best accounts receivables, that is, the ones for which there is a high probability of being paid. Factors will also examine the aging schedule of your receivables and, similar to pledging, will only accept those that are not beyond a reasonable payment period. Generally, the factor will collect the accounts receivables directly from the customers. Factoring can be done either on a recourse or nonrecourse basis. The recourse basis provides the factor with the right to demand payment from you if your customer fails to pay. You will be paid when the factor collects the account, or on the last day of the net credit period, whichever comes first. You may receive advance payments prior to the due date of the receivables, and the factor, of course, will impose an interest charge on any advances. However, in the case where surpluses occur and you do not draw on the advance payments, you may also earn interest.

Typically, the factor will keep a reserve of 5% to 10% for protection against any returns or cash discounts. Factors generally will earn a commission of 2% to 4% of the face value of the accounts receivables to cover their administrative costs. In addition, the interest on advances is usually 2% to 5% above the prime rate.5 Also, the interest rates paid on surpluses are generally much lower, most likely equivalent to the rate on commercial bank savings accounts.

Both pledging and factoring have two positive aspects. First of all, as your sales grow, they provide you with greater flexibility in financing your business. Secondly, they provide some assistance in your decisions regarding whether to extend credit to a given customer. Pledging provides you with an analysis of the relative strength of each of your customers, while a factor will make all credit decisions on each customer for you. In some cases, factoring may eliminate the need for an entire credit department, since the factor makes all the decisions on whether or not a customer obtains the ability to purchase on credit. Furthermore, the factor shoulders all of the costs of the collection process.

The two major negatives of pledging and factoring are that customers and potential customers may view the use of either of these as a weakness. Additionally, both pledging and factoring can be very costly—ranging from effective rates of 18% to 30%.

Sale and Leaseback of Real Estate and Specialized Assets. In addition to financing assets such as receivables and inventory, some firms may have some very specialized assets such as the real estate used for the business, very expensive technological equipment that is used by biotech firms, or patents and copyrights. Each of these may have a significant value that can be used to raise financing through the process of sale and leaseback.

Fundamentally, the finance company will buy these items from you and then lease them to you at a monthly fee. Each of these types of financing has the positive aspect of allowing the firm to raise some capital for current use. Often, after the leasing period is over the firm has the right to repurchase the asset that it has been leasing. The sale and leaseback provides the entrepreneur with immediate cash, which can then be reinvested in the business to fund growth. The downside of this type of funding is that it is usually at high interest rates, and the leasing period may extend beyond the true useful life of the assets.

Using Your Firm’s Profit from Operations

When your firm begins to generate profits, it is imperative to reinvest as much of those profits as possible back into the business. Reinvesting profits provides savings in terms of interest costs on other types of financing, and also provides future lenders with a positive view of your performance and ability to pay debt. Indeed, reinvesting profits also sends a positive signal to potential lenders and investors, since it further demonstrates that you have strong confidence in your company’s business model and future performance.

Clearly, lenders and future investors look very carefully at the percentage of profit that goes to owners; a high percentage can be a significant negative insofar as obtaining financing is concerned. Reinvesting profits also assists in maintaining ownership and control. However, in many cases, profit is the only source of remuneration for the owner so it might be difficult to maintain a prudent level of restraint with respect to forgoing some things that profits could allow you to afford on a personal level. Nonetheless, you must remember that such restraint is crucial to the growth and solvency of your business—especially in its early stages.

Finally, profit goes into the retained earnings account, and lenders look very carefully at this account. Negative retained earnings imply bankruptcy. Retained earnings represent the cumulative reinvestment of profits over the life of the firm, and are counted as part of equity. Higher retained earnings imply a lower debt to equity ratio.

External Sources of Funds

In the previous section, we looked at utilizing your company’s assets and liabilities to find needed financing. In this section, we look outside the firm to find sources of funding that may be secured as either debt or equity. In this discussion, we also seek to provide you with an understanding of the criteria that are typically used by the various sources, so that you can make an intelligent assessment of what sources are more suited to your company’s financial performance profile and funding needs.

Debt Financing

This form of financing provides funds to you, based upon a promise that you will repay the funds, usually with interest and within a specified period of time. Coverage in this section will include nonpersonal loans and other forms of debt financing. First, however, it is very important that you gain an understanding of how your credit impacts on a lender’s decisions, as well as what lenders and investors generally consider when making decisions about extending loans to small business owners.

Bank Loans—What You Need to Know: The 5 C’s of Credit

Traditionally, bank loan officers talk about the five C’s of credit. These are capacity, collateral, credit, capital, and character. The fifth C, character, may be a key factor especially for local small-town banks, as well as credit unions. Character refers to the reputation that you and your family hold in the community. Are you known as a person of honor and integrity? Capacity refers to your firm’s financial ability to pay back your loan and make your interest payments. It refers to the profitability of your firm. Is your firm generating sufficient profit to make required payments? Collateral refers to the level of assets that you have to support your loan in the event of bankruptcy. Collateral can be assets in your firm, or personal assets such as real estate that has no other encumbrances. Credit refers to your history regarding paying your suppliers and other lenders on time. This is reflected in your Duns PAYDEX6 number. Capital refers to the equity base you have invested in your business; in particular, your retained earnings and equity. The key element of all of these factors is your ability to pay both the interest and the face value of the loan. Others might add a sixth C—economic conditions: Are the general economic outlook for your particular industry and the local market conditions suitable for the sustainability of your company?

What Is a Ratio and Why Is It Important?

Ratio analysis is a critical determining factor used by banks, as well as finance companies, and other lenders and investors in measuring your ability to pay. These ratios fall into four basic categories: liquidity, asset utilization, debt, and profitability. The two ratios that interest lenders most are liquidity ratios (which indicate the ability of your firm to make short-term payments) and debt ratios (which measure the ability of the firm to take on more debt financing). Key liquidity ratios are the current ratio (current assets divided by current liabilities) and the quick ratio (current assets less inventory and less aged receivables divided by current liabilities). Again, the current ratio represents your ability to make your short-term payments. Generally, a bank looks for a current ratio of at least two times and quick ratio of at least one time. Other important ratios are the earnings before interest and taxes divided by your interest charges—called the times interest earned; and, finally, total debt to total capitalization ratio, as well as the total debt to equity ratio. All ratio measures are compared against the industry median for firms of your size (as measured by sales or assets). Some industries might have both a current and quick ratio that is lower than the ones just suggested, while others might have a higher requirement. The key question is how your ratios stack up against the median ratios for your industry. One way for you to check this is to look at the RMA ratios for your specific industry.7 Your business’s financial ratios should be at or slightly better than the median ratios for companies in your industry with asset and sales levels similar to yours.

Banks might also impose covenants, both positive and negative. Covenants often take the form of requiring that your business maintains certain levels of specific financial ratios, such as a liquidity or debt ratio, as well as paying on time, and usually, also impose restrictions on taking out any other loans.

The Lender’s Perspective

Bank loan officers and investors in general ask specific questions in determining whether or not to make a loan. Usually, the first question in the minds of bankers is the quality of the management. Does the business have high quality, reputable managers of high ability and integrity running it? Secondly, bankers and investors want to know whether the business has an effective business model that will be sustainable in the long run. In addition, other central questions include: Can the firm adequately service the debt (i.e., repay the funds) that it is seeking? Does the firm have a good credit history? Does it have a good collateral position? Does the firm have a good marketing plan and a strong sustainable position in its market? Does the firm have good cost control? Is the firm’s risk exposure limited? Is the owner risking a substantial amount of his or her own capital? Finally, are the firm’s financial projections reasonable and accurate?

The previously asked questions are central to all investors. Indeed, from the most recognized investor such as Warren Buffet, to the smallest local bank, the same questions are asked, and all should have the positive answer of “yes.” Table 3.2 provides a listing of the primary factors considered by investors.

Table 3.2 Major factors that bankers and investors consider

|

• Strong and Ethical Management • An Effective Business Model • Strong Ability to Service Debt • Solid Equity Position • Good Collateral Position • Good Cost Control • Owner Risking Own Capital • Limited Risk Exposure—Especially for Banks • Good Credit History • Good Marketing Plan and Strong Market • Company Has Secure Position in Market • Solid and Accurate Financial Projections |

Banks as Sources of Business Loans. Banks provide three basic forms of financing: a revolving credit agreement, line of credit, and term loans, the latter being made available for approximately one to seven years. In a revolving credit agreement, the bank guarantees the availability of a certain amount of funds in exchange for a commitment fee (to be paid on the unused amount of the credit line). The interest rate charged would be floating and usually tied to the prime rate. The borrower is allowed to draw down on the credit line and then repay. Revolving credit lines assist the business in bridging cash flow gaps (gaps between receipt of payments from customers and payments due to suppliers), and also can provide a needed cushion during cyclical or seasonal fluctuations.

A line of credit is somewhat different from a revolving credit line. Banks would authorize but not guarantee loans up to a certain amount during the year (e.g., $100,000 to $500,000+). Interest rates vary usually with the prime rate. You can expect to pay an annual fee, as well as the interest charge in most cases. Historically, banks also required that the firm maintain a compensating balance with the bank, but few banks still have this requirement.

Both revolving lines of credit and lines of credit may be either secured (i.e., you must put up some collateral) or unsecured (no collateral is required). The interest rate spread between a secured line of credit and an unsecured line of credit can be significant. For example, a secured line of credit might have a rate of 10%, while an unsecured line of credit might have a rate as high as 23%. Generally, when you use either the revolving line of credit or a line of credit, you will be billed monthly, at which time you pay both interest and at least a partial payment on the amount used.

Credit Unions as Business Loan Providers. Generally, credit unions have not been a large provider of business loans. Indeed, credit unions provide a small percentage of business loans, approximately 1.3% of business loans compared to banks which have provided over 90.2% of business loans.8

Historically, credit unions have operated under a number of regulatory rules that have limited their ability to be a large provider of business loans to members. These constraints include the fact that a credit union’s member business loans (MBL’s) above $50,000 cannot exceed 1.75% of net worth or 12.25% of the credit union’s total assets, whichever is lower.

Secondly, borrowers must be within the credit union’s geographic area, and cannot include CEO’s or Directors, or family members, and borrowers must provide personal liability and guarantee of principal. These last two conditions are legal terms which in essence mean that if there is any default on the loan the lender can automatically garnishee the wages of the borrower, as well as take any personal assets, such as personal bank accounts and real estate not associated with the business, to collect what is owed. Moreover, the loan-to-value ratio of any loan cannot exceed 80%. Banks do not operate under any of these restrictions. Moreover, while credit unions might be a good source of financing during periods when bank lending is tight, credit unions generally have higher interest rates than banks.

Recently, there has been a modest push for congressional legislation to relax the credit union restrictions, such as increasing the 12.25% of total assets restrictions to allow member business loans up to 27.5% of total credit union assets. In part, this legislation has been motivated by the fact that, during the tight loan period subsequent to the 2007 crash, credit unions were one of the few sources that small businesses could turn to for loan financing. However, banks strongly oppose these regulatory changes. As banks began to offer more funding in 2013, the motivation for such regulatory changes has become weaker.

Crowd Financing. Crowd funding is expected to be a huge source of financing in the future. A large number of portals, at this writing, are setting up for the purpose of providing crowd funding. This process is expanding exponentially, not only for crowd funding in the United States, but globally.

In 2012, the passage of the Jumpstart Our Business Startups (JOBS) Act introduced a potentially less costly, more effective, and efficient way for entrepreneurs to raise equity capital. The JOBS Act provides firms with less than $1 billion in sales the ability to go public much more readily than in the past. The Act allows firms to secure up to $50 million in equity funding. A major component of the Act is the provision for the allowance of broad advertising of public securities. The goal is to provide an easier, faster, and less costly method for small firms to raise equity. A second significant component of the Act allows smaller investors to invest in the company. Anyone can invest a minimum of $2,000 in the IPO or 5% of the investor’s annual income, whichever is higher. In addition, individuals with an income of $100,000 may invest up to 10% of annual income. This is a major change since previously only accredited investors could invest (accredited investors are defined as those with net worth in excess of $1 million, or individuals who have earned an income of $200,000 per year for the last two years).

At the time of this writing, the Act has yet to be fully implemented. Once the U.S. Securities and Exchange Commission (SEC) institutes the operational rules relaxing financial reporting and accounting standards, the process will be less cumbersome for small businesses. Firms will be able to broadly advertise their equity offerings through social media sites such as Facebook, Twitter, and other websites. The goal is for the entrepreneur to reach investors who are especially attracted to the type of service or product that the firm is offering.

In anticipation of the Act’s full implementation, a number of groups and websites or portals are already preparing. However, some key issues that still must be resolved are cyber security and whether there will be a sufficient number of firms that will be willing to use this IPO method. Additionally, there is the question of whether there will be a sufficient number of interested investors. There is also the possibility that the SEC rules might still be so restrictive as to make it almost impossible for a small firm to raise funds in this manner. Finally, all investors need to be aware that there is a high failure rate among start-ups. Indeed, recently the rule of thumb is that only one out of every 15 to 20 start-ups succeeds. This causes pause for many who believe that few small investors will have a solid grasp on the riskiness of investing through the crowd funding process.

Angel Investors. Angel investors usually are involved at the seed or even preseed stage of your firm. These investors also look for the same features as a venture capitalist. Angel firms try to seek out specific high-wealth individuals who would have a strong interest in the product or service that a firm offers. Thus, if your product is a medical service, the angel firm would look for wealthy physicians who would be interested in investing. On the other hand, if your firm had something to do with sports or athletics, the angel firm would look to successful professional athletes as potential investors. However, by current laws, they can only seek out qualified or accredited investors.9 A firm owner who seeks out angel investors must sit down with each qualified investor, one at a time, to find the right funding. However, the concept of crowd funding, discussed previously, seeks to expand this opportunity so that many investors who have an attraction and passion for your type of product may be reached and allowed to invest.

Equity Financing

Of course, equity financing provides some share of ownership of your company in exchange for receipt of funds or other valued resources. Quite often, aspiring entrepreneurs are very leery about giving up any of the ownership of the company, fearing a loss of control. However, it is useful to consider the reality that 100% of nothing is nothing. Sometimes, in order to move your company to where you want it to be, you will need to consider trading a portion of the ownership for funds that you need to help the company grow. Keep in mind that, as long as you own 51% of the shares in your company, you are still in control.

Using Convertibles. Convertibles come in a variety of forms (bonds, preferred stocks, and stocks with warrants and options, etc.). What distinguishes convertibles is that, as compared with standard instruments, these are developed with provisions for repurchase or resale at specified prices within certain time periods.

Convertible Bonds. In the early stages of your business, investors such as venture funds may be interested in investing with convertible securities. In many cases, these types of convertibles charge low interest and have long, delayed principal repayment periods.

Convertibles usually have a specific conversion ratio and, therefore, a conversion price. The conversion ratio indicates how many shares of stock the bond may be converted into, if desired (e.g., 50 shares of stock per bond). Thus, for a $1,000 face value bond, the conversion price is $1,000/50 shares = $20 per share. Hence, if the stock goes above $20 per share, the bondholder will find it beneficial to convert it into equity. The main reason that investors like convertibles is that, in the event that the business becomes quite successful, the ability to share in that success can be achieved by converting the convertible security into equity.

Convertible Preferred Stock. Preferred stocks usually have a fixed dividend rate, and normally dividend payments for preferred stock are cumulative, so that, if the firm is unable to pay a dividend in one period, it must pay the cumulative amount when it does pay. Preferred stocks are termed as such because these stockholders must be paid their dividends before any dividend payments are made to owners of common stock. These stocks are like convertible bonds, except that convertible preferred stock prices do move with the market. An example of a convertible preferred stock would be a share of preferred stock that can be converted into four shares of common stock any time after a period of two years.

Common Stock with Warrants & Options. Warrants give the investor the right but not the obligation to purchase a prespecified number of shares of common stock at a certain price, by a certain time. The main difference between a warrant and an option such as a call option is that warrants are usually detachable and may be traded or sold separately from the stock or bond. Call options associated with either common stock or bonds are not detachable and also usually have a shorter exercise period than a warrant.

Venture Capital and Private Equity. Venture capitalists as well as private equity firms look for very specific opportunities. The first and perhaps most important thing they look for is the uniqueness of the product or the business model. In concert with uniqueness, a key factor is the size of the market. Does the product or service represent the potential of having a huge market both in terms of the U.S. market and globally? There is also major attention directed toward whether the product carries with it a strong competitive advantage. Furthermore, the huge market potential must be able to be achieved quickly. One aspect of the competitive advantage is whether the product can be brought to the market at a highly accelerated speed. Another aspect can include a unique patent or a copyright. An advantage that cannot be quickly replicated is essential.

In addition, like most other investors, venture capital firms also look for a high-quality management team. However, as a business owner, you should be aware of one important fact: If you do not have a powerful vision for your product or the future of your business, investors perceive you as impeding the growth of your firm. This means that, although you founded the firm, you might be replaced at some point. A readily available example of this fate was Steve Jobs, to whom this very thing occurred (remember this and other examples from the introductory chapter of this book). Venture capital firms as well as private equity firms invest in a number of new potential start-ups with the hope that at least one or two will have a significant payoff.

Venture capital generally has four stages of investment after the angel stage: seed or start-up, early development, expansion and growth, and exit. The initial hope is always that your firm will be a successful national or global company in the end. At the seed stage, the venture capitalist will want a position on your board, and the ability to hire or bring on a more seasoned management team. In addition, venture capitalists at seed stage will want a solid equity (ownership) position in your firm. As your firm grows, the initial venture capitalist firm will assist you in getting further investment funds from other venture capitalists.

In seeking to understand how venture capitalists operate, you should be aware of the fact that each venture capitalist firm tends to be focused and have expertise in specific stages of a business’s growth. Some will only invest in your industry at the seed stage; while others focus on providing investment for the early development stage, and still others only invest in the expansion and growth stage. With the addition of a venture capitalist firm at each stage, you will be giving up more equity, and you will be receiving greater expertise for operating in each specific stage. It is the goal that the value of the equity holding is increased substantially at each stage.

While you likely view your business with some degree of emotional attachment, you should know that venture capitalists enter business investment arrangements with a plan for exit. A venture capitalist or private equity firm always has an IPO as the firm’s final exit goal. Nonetheless, it should also be noted that, even in the event of a desired IPO, venture capital firms will not be able to exit for a period of one or two years, due to SEC regulations.

Despite working toward an IPO, in many cases, other exits will be more beneficial. These exit options include the sale of your firm to another firm, the sale to another venture capitalist or private equity firm, the sale back to you, or the options might even include bankruptcy (the latter is, of course, not an intended or preferred goal).

Exploring Small Business Investment Company (SBIC) Funding.

The SBA also sponsors the SBIC’s—small business investment companies. These companies specialize in providing venture capital-like funds to small businesses (small being currently defined by net worth of $18.0 million or less, with average after-tax net income for the prior two years not exceeding $6.0 million—inclusive of all affiliated enterprises of your company). The SBIC’s provide both convertible debt and equity financing. In addition, each SBIC is set up to specialize in a particular industry. Historically, SBIC’s have funded such companies as Microsoft and Apple, Inc. SBIC’s are licensed and regulated by the SBA and there are over 300 SBIC’s operating today. SBIC’s use their own capital, but their funds have an SBA guarantee. You can find more information on SBIC’s located in your state at the sba.gov website.

Engaging in Private Placements. As your firm continues to grow beyond funding from, say, venture capital and private equity, the next step for funding might be private placement of debt or equity. This type of funding is usually done through an investment bank, which will find a single or a few accredited investor(s) willing to purchase bonds or stock in your business. These investors are usually insurance companies, pension funds, and mutual funds. Since these are all highly qualified investors, private placements do not require all of the stipulations and rules of a public offering as required by the SEC. Private offerings are done under the SEC rules (which include Regulation D) and do not require the same financial reporting as a public placement. There are also savings in terms of commissions, since not many intermediaries such as brokerage firms are involved.

In addition (similar to angel investors), with private placements, you have an opportunity to select the types of investors you wish. This generally makes private placements a less costly financing option relative to public offerings. However, private placements can only be made to accredited investors.10 As a consequence, it is possible that there might not be many sympathetic investors with sufficient wealth to fully fund your needs. Alternatively, there might not be as many sympathetic accredited investors who are interested in your business. Moreover, private placements have the additional potential downside that the pricing of your securities is usually lower since you are facing sophisticated investors who will bargain for much lower prices.

The IPO. If your enterprise achieves a substantial national market and has the opportunity to grow even further, both nationally and perhaps internationally, it will become a candidate for an IPO. At this point, you would need the services of an investment bank. The rules of an IPO are very cumbersome and require the assistance of attorneys, accountants, investment bankers, and others to be certain that you are in compliance with all SEC regulations. SEC requires the preparation of financial statements such as 10K’s and 10Q’s, and the preparation of a prospectus which meets all legal requirements. The process also requires a network of investment banks to market your securities. An IPO is a large undertaking, and requires tremendous detail which is beyond the scope of this chapter. Few enterprises reach this level, but those that do will need the assistance of a cadre of experts.

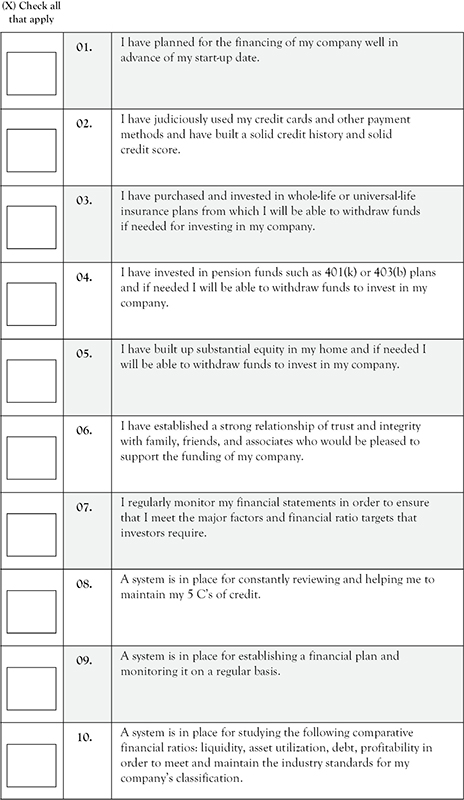

Chapter Summary Checklist