A man had a dollar and spent a quarter and gave fifty cents to his daughter; he gave another quarter to his friend, and then had nothing left to spend.

—© 2013 Sage Sayings™

Introduction to Successfully Managing Your Cash

In business, as in life, learning how to manage your cash is essential for long-term survival. In fact, one of the most critical problems facing small businesses today is managing cash flow. Cash is king for the successful business! The reality is that cash is the critical fuel that allows the business to continue its operations and grow. Without this essential fuel, too many of today’s small businesses experience great difficulty trying to keep afloat. Businesses that receive too little fuel will sputter and never have an opportunity to grow. Ironically, businesses that have too much of this fuel will also have problems maximizing development and growth. In a nutshell: cash management is extremely important to small business growth and success.

Conventional wisdom states that the biggest challenge for small businesses today is access to capital. However, the author’s own surveys of small business owners have revealed a challenge to conventional wisdom. When asked “What is your greatest financial obstacle?” responses from a small group of business owners were as follows:

• Uneven cash flow (35%)

• Payroll (17%)

• Taxes (17%)

• Raising capital (12%)

• High rent (5%)

• Other (14%)

Thirty-five percent of the respondents cited “uneven cash flow” as the greatest financial obstacle, followed by payroll and taxes. At a distant fourth place, only 12% of the surveyed business owners cited “raising capital” as the greatest financial obstacle. Further review of these results suggests that the business owners’s concerns regarding payroll and taxes are related to concerns about cash flow. When these results are combined, the implication is that uneven cash flow was the concern of 69% of the respondents. The survey results glaringly point to the importance of managing cash flow for the success of business growth and development.

This chapter explores the cash management strategy of projecting cash flow, understanding the importance of financial statements, and safeguarding your cash. Additional topics of discussion will be: cash flow and decision making, cash management and banking, and using technology in cash management strategies.

Cash Management Strategies and Systems

Effective cash management strategy can be succinctly described in two simple steps:

1. Get your cash as quickly as possible.

2. Hold onto your cash as long as you can.

Although this is a simple formula for effective cash management, it is very difficult to implement and typically requires a lot of attention from the small business owner, along with the devising and implementing of complementary or ancillary cash management strategies.

In the process of managing cash flow strategy, there are a number of roles that you must ensure are executed. These include the following:

1. Cash finder—investing and borrowing cash

2. Cash planner—deciding how cash will be used now and in the future

3. Cash distributor—determining how cash will be provided to the critical elements of the business

4. Cash collector—ensuring that cash is being collected in an effective manner

5. Cash guardian—monitoring, protecting, and safeguarding cash

These roles are very important and many times require you, the business owner, to be able to ensure simultaneous execution. Although business owners often delegate these roles to employees, the importance of each role requires that you never become detached but continue to be involved in these cash management roles.

In addition to the judicious demonstration of the earlier roles, an effective cash management system requires the implementation of six important strategies:

1. Accelerating cash receipts

2. Planning, managing, and controlling cash

3. Forecasting inflows and outflows of cash

4. Investing surplus cash

5. Monitoring cash flow

6. Understanding and effectively using financial statements

Cash Management Strategy 1—Accelerating Cash Receipts

In selling products or services, or both, many companies extend customer credit in the form of accounts receivable and later seek to collect on these receivables. Credit sales have become an important part of doing business in today’s marketplace and these sales have increased significantly as a portion of the total sales of most businesses. The key element for business success is to reduce the amount of time that sales remain in accounts receivables. Therefore, you must employ tactics that will turn receivables into cash as quickly as possible.

Methods that may be used to accelerate cash receipts include the following:

• Collecting and depositing cash in your bank as soon as possible

• Using bank funds transfers

• Billing customers as soon as possible

• Using effective and appropriate customer credit terms

• Utilizing post office boxes and lockboxes

• Using your bank effectively

• Developing a system for monitoring cash management

Cash Management Strategy 2—Planning, Managing, and Controlling Cash

It is highly unlikely that any effort needs to be expended to convince you that planning, managing, and controlling cash—your most precious business resource—is extremely important. This strategy principally focuses on the second element of the simple cash management strategy: holding onto your cash as long as you can. To execute this strategy, you must implement processes that will allow you to hold onto cash as long as possible. In addition, you must effectively plan how the cash will be used now and into the future. This strategy requires that your business strategically delay payments without incurring late fees or damaging supplier and vendor relationships. The strategy requires a “just-in-time” approach to delaying payment of obligations so that you can hold onto cash. You must make sure that the business has the correct amount of cash available when needed—not only to address present needs but also future needs. Therefore, this strategy requires that the focus should not be on the bank balance or net profit but on the ability to predict cash flow in the future.

Planning cash requires that you never pay any bill or obligation a day sooner than necessary. It is also important to employ tactics to delay or extend the payment date to increase the amount of time the business holds onto its cash. Some planning or delaying tactics that could be employed include the following:

• Mailing payments on Friday

• Centralizing the accounts payable function and developing an overall strategy for evaluating creditors (all creditors are not equal in importance and credit terms)

• Employing a bill paying priority system

• Utilizing control distribution accounts with your bank

• Employing the use of credit cards in your bill paying strategy

• Scheduling cash disbursements only twice a month

• Negotiating and renegotiating with suppliers and vendors

Each one of these tactics will improve your ability to hold onto your cash. However, utilizing all of these tactics will allow you to pay as late as possible.

Cash Management Strategy 3—Forecasting Inflows and Outflows of Cash

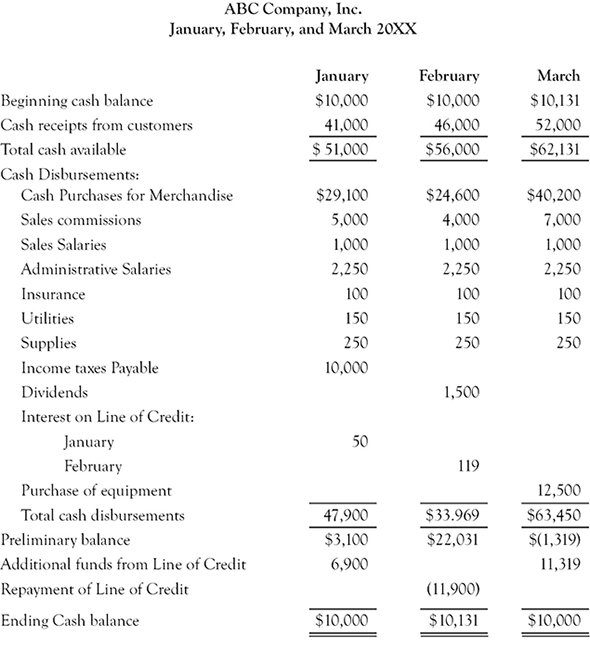

Forecasting cash inflows and outflows is an extremely important function. This activity must be engaged in at least once a month and should be centered on predicting how much cash is expected to flow in for the month and how much cash will flow out during that same timeframe. This process is critical, because it allows you to effectively budget for cash inflows and outflows and plan for the cash necessary for growth and expansion. The use of a cash budget is a critical part of this strategy. Figure 5.1 shows an example of a cash budget for a small business.

Figure 5.1 Cash budget

The basic steps in preparing a cash budget include the following:

1. Determine the required minimum cash balance.

2. Forecast sales and other revenue items.

3. Forecast cash receipts.

4. Forecast cash disbursements.

5. Determine the end of the month cash balance needed for business operations.

Cash Management Strategy 4—Investing Surplus Cash

In effective utilization of a cash budget system, you will determine if the business will have surplus cash and the amount of idle cash that remains in the business on a monthly basis. It is important to find methods to reemploy idle cash or surplus cash to earn additional dollars. It is advised that you discuss the strategies for investing short-term cash balances with your banker, accountant, or investment advisor.

Cash Management Strategy 5—Monitoring Cash Flow

The monitoring of cash flow requires you, the business owner, to determine, on a daily basis, the amount of cash that is available and compare that with what is needed: (1) for reinvestment in your business; and, (2) for payment of pending obligations. Monitoring cash on a daily basis aids in determining if and when there is a shortage of cash and when to deploy your business’s bank lines of credit. The monitoring process also aids in determining whether there is too much or excess cash on hand that needs to be invested.

Cash Management Strategy 6—Understanding and Effectively Using Financial Statements

Understanding and effectively using the information contained in your business’s financial statements are critical to the effective management of cash flow. The three essential financial statements for any business include the statement of financial position or balance sheet, the income statement or profit and loss statement, and the statement of cash flows. Each of these will be discussed further.

Statement of Financial Position or Balance Sheet

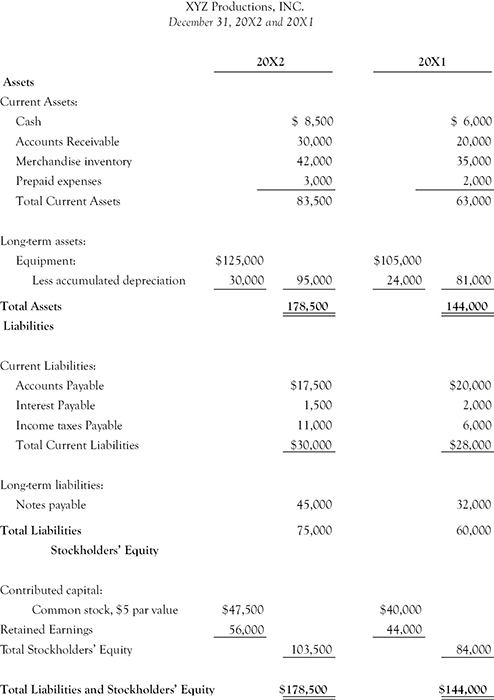

This statement reveals the assets of your business and the claims against those assets (see Figure 5.2). Assets are defined as tangible and intangible valuable resources owned by the business. Assets include equipment, inventory, securities, receivables, property, land, patents, and of course, cash. Assets are on the left side of the statement of financial position or balance sheet.

Figure 5.2 Balance sheet

The claims against assets are in two basic forms. The forms include liabilities (what the company owes to creditors), and the claims of the owners (referred to as owners’ equity or stockholders’ equity). Liabilities or the obligations of the business include accounts and notes payable, loans, tax liabilities, and mortgages and long-term debt. Liabilities are on the right side of the statement of financial position or balance sheet.

The claims of the owners of the assets of the business are known as owners’ equity or stockholders’ equity. There are two sources of equity—capital and retained earnings. Capital includes the direct investments of the owner(s) or stockholders in the business. Retained earnings are the amount of profits or earnings held by or reinvested in the business. The claims of the owners or stockholders are on the right side of the statement of financial position or balance sheet. The sum total of the liabilities and equity (right side) equals the total of the assets (left side).

The statement of financial position or balance sheet shows the financial health of a company or business at one point in time. This statement is typically prepared quarterly or annually.

Income Statement or Profit and Loss Statement

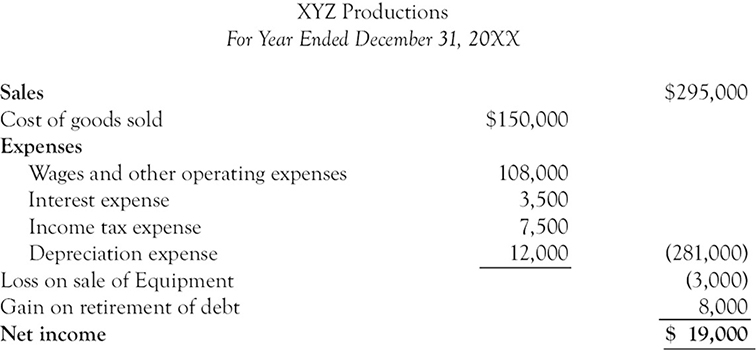

This statement provides information on the profitability of your firm or business. It explains how income is derived and how expenses are incurred in generating revenue. Figure 5.3 is an illustration of an income statement.

Figure 5.3 Income statement

The basic income statement equation is revenues or sales or services minus expenses equal net income or net profit. Revenues or sales are the amount of products, goods, or services sold or delivered to customers during a certain period of time. Gross profit or gross margin is generally derived by taking total revenue or sales and subtracting the cost of sales or the cost of inventory items sold.

The second major item on the income statement or profit and loss statement is expenses, generally operating expenses. These are the costs that are incurred during the period to generate the sales or revenues that have been recorded. Operating expenses would include salaries, rent, insurance, supplies, and other expenses that are necessary for the enterprise to continue to operate and generate revenue.

The third major item on the income statement is net income, net profit, or net loss. This is the indicator of whether your business’s revenues or sales are greater than expenses or vice versa. It is important to know that the net income or net loss reflected on the income statement does not, by itself, indicate cash inflows or cash outflows.

Statement of Cash Flows

The statement of cash flows is perhaps the most important financial statement for operating a small business or enterprise. It outlines the sources and uses of cash for a specific period of time. This critical information is vital to you in managing your small business and managing cash flow. You must know your business’s sources of cash, how it is being used, and the additional cash needs or surplus of cash that your business has. Profit or net income is not cash and cash is not profit or net income.

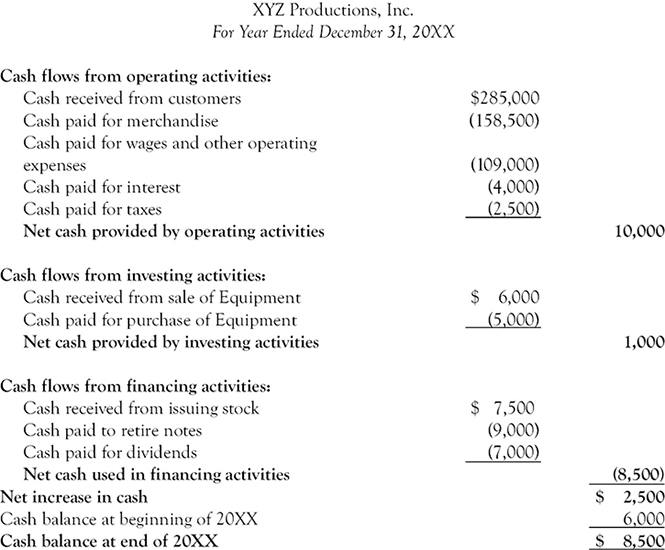

The statement of cash flows is organized into three categories for the sources and uses of cash. These are: operating activities, investing activities, and financing activities (see Figure 5.4 for an example of a statement of cash flows).

Figure 5.4 Statement of cash flows (direct method)

Operating activities are all transactions associated with cash from the normal operations of the business (the central function of the business). Cash inflows from operating activities include sales or service revenue, and cash outflows from operating activities include payment of salaries and wages, payments to suppliers, interest, rent, and taxes. Changes in accounts receivable and inventory are also included in operating activities.

Cash outflows from investing activities include purchase of long-life assets, such as land, plant, equipment, and purchase of nonmarketable securities. Cash inflows from investing activities include the opposite of those types of transactions: sale of land, plant, equipment, and nonmarketable securities. Investing activities also include the collection of noncurrent loans.

Cash inflows from financing activities include borrowing of cash and issuance of common or preferred stock. Cash outflows from financing activities include repayment of loans, repurchase of stock, and dividend payments to stockholders or investors.

Preparing the Statement of Cash Flows

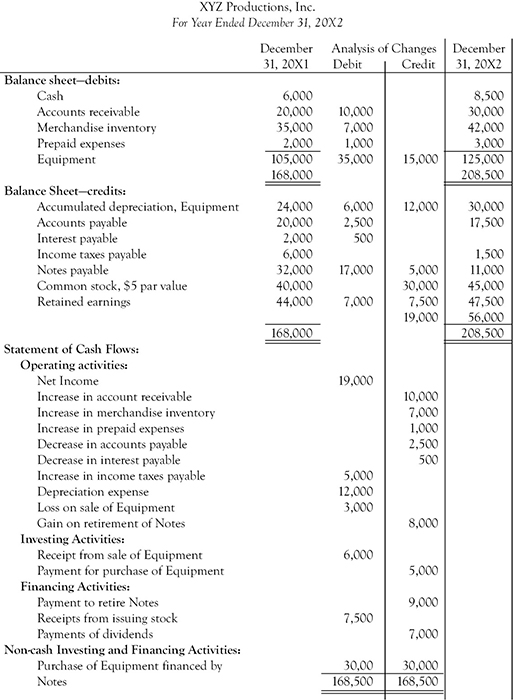

To prepare a statement of cash flows, you will need the current year’s income statement and the current and immediately past year’s balance sheets, along with a worksheet to record your calculations. See Figure 5.5 for an example of such a worksheet. Adjustments to net income are necessary because most businesses use a method of accounting (accrual accounting) that records revenues at the time of sale, without regard to whether the sales are for cash or are made on credit. Adjustments to account for this must be made when converting income statement information to the statement of cash flows.

Figure 5.5 Worksheet for statement of cash flows (indirect method)

Operating Activities

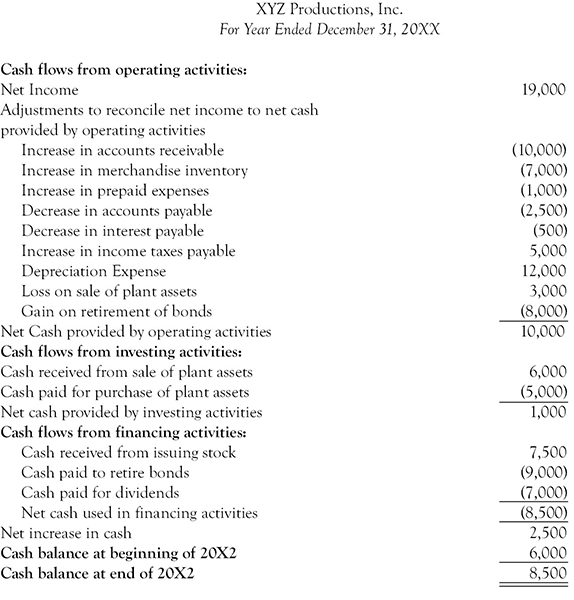

As stated, the statement of cash flows begins with the operating activities section. There are two methods of calculating cash flow from operations: the direct method and the indirect method. The direct method1 identifies the operating activities that generate cash inflows and outflows. The indirect method2 adjusts net income for accruals, deferrals, and noncash expenditures. The two methods yield the same cash flow result. Compare the final results in Figure 5.4, which was prepared using the direct method, with those shown in Figure 5.6, which employed the indirect method.

Figure 5.6 Statement of cash flows (indirect method)

Next, the cash increase or decrease for the period is determined by comparing the beginning cash balance with the ending cash balance. Refer again to Figure 5.2, which shows balance sheets of XYZ Productions, Inc. for years 20X1 and 20X2. The income statement of XYZ Productions, Inc. is shown in Figure 5.3, and Figure 5.4 is the corresponding cash flow worksheet, which shows the changes in the balance sheet accounts from one year to the next.

After determining each account’s increase or decrease for the year, it must be further determined if the changes resulted in cash inflows or outflows. Beginning with the operating activities section of the statement of cash flows (Figure 5.4), the information on the worksheet aids in adjusting the net income amount to a cash basis. The chart shows the impact of increases and decreases in certain accounts on cash flows from operations. Changes in accounts receivable, inventory, and prepaid expenses impact cash flows from operations. The accounts receivable balance relates to credit extended to customers in selling goods and services. The accounts payable balance reflects the amount that has been used to buy inventory to sell; and, changes in the inventory balance are related to the main operation of the business—selling goods.

Investing Activities

This section of the statement of cash flows records the increases and decreases in noncurrent assets, such as equipment, buildings, land, and investments. The sale of equipment, for example, will generate cash inflows, while the acquisition of additional equipment will result in cash outflows. Thus, cash inflows and outflows from investing activities are, respectively, determined by adding the proceeds from the sale of noncurrent assets and subtracting the purchases of noncurrent assets during the period.

Financing Activities

The third and final section of the statement of cash flows focuses on financing activities. This section records the increases and decreases in the two areas of investing—noncurrent liabilities and owners’ or stockholders’ equity. Increases in noncurrent liabilities such as long-term debt result in increased cash, while decreases in noncurrent liabilities will decrease cash because liabilities are being paid with cash. Furthermore, the financing section is impacted by increases and decreases—not from operations (i.e., net income or net loss), but in owners’ or stockholders’ equity. An increase in the capital account is an additional investment in the business and will provide additional cash to finance business activities, while a decrease (e.g., owners’ or stockholders’ withdrawal) will reduce cash available for financing operations and result in cash outflows.

The following information is a guide to preparing the financing section of the statement of cash flows: Cash inflows or outflows from financing activities; + increases in noncurrent liabilities – repayment of noncurrent debt – dividends paid + increases in capital stock or – decrease in capital stock.

Following the guidance provided earlier for each section will facilitate completion of a credible statement of cash flows. Refer again to Figure 5.4, which shows such a statement.

Analyzing the Statement of Cash Flows

The statement of cash flows shows the business owner(s), stockholders, decision makers, or all, where cash was generated and how it was utilized. In analyzing the statement of cash flows, you will need to review all three sections: the operating activities section, the investing section, and the financing section.

Operating Activities Section

You should begin your analysis with the operating activities section. This section reveals the amount of cash generated or lost from the business’s main activity. In reviewing this section, you will discover whether sales and expenses met or exceeded plans. Collection of customer accounts and increases or decreases in short-term debt (accounts payable) are also shown. Increases in accounts receivable may require a review of customer credit terms or the collection process. Increases in accounts payable may require a review of inventory for nonmoving items and purchase prices and quantities. If cash flow from operations met or exceeded plans, there might be no need for adjusting the business plan or business operations. If, on the other hand, cash flow from operations did not meet plans, a readjustment of the business plan or review of sales and expenses could be warranted. In the long term, the cash flow from operations should sustain the business. Over the long term, insufficient positive cash flow will result in your business being unable to pay its employees, creditors, taxes, and owners or stockholders—that is, business failure.

Investing Activities Section

The investing section of the statement of cash flows reveals (during the period of operations) whether the business reinvested in its assets and operations or sold its assets to fund current operations. A lack of reinvestment in noncurrent assets might reveal lack of growth or serious cash flow problems.

Financing Activities Section

The financing section of the statement of cash flows reveals the payments of or increases in long-term debt, capital infusion, or withdrawals of capital, and payment of dividends to stockholders. This will reveal the business’s methods of financing long-term operations as well as payments of obligations and payments to investors.

The overall analysis of the statement of cash flows shows where cash is being generated in the business and allows you to analyze whether operations are going according to plans. The analysis also provides information for making changes to meet plans. Looking at past cash flow statements will provide trends upon which important decisions can be made, such as whether to increase long-term investments or to increase the investment returns to business owners or stockholders. Long-term positive cash flow indicates a growing business, while negative or sporadic cash flow can indicate serious problems and need for business adjustments. The statement of cash flows provides the critical information needed for making important decisions about the long-range success and viability of your business.

Banking Relationships

It is important that you have a dependable relationship with your banker. A good banking relationship can make the difference between a business’s survival and its failure. You should strive to develop a relationship with a supportive and reliable bank that will address the needs of your business as it grows over the next three to five years. In order to determine banking needs, your task as the business owner is to assess and evaluate the current and future financial needs of your business. Will those needs include a checking account, overdraft protection, lines of credit, small business loans, short-term or long-term investing, and so forth?

After effectively assessing and evaluating your financial needs, you should shop around and find the right bank: one that can aid and assist the growing needs of your business. When attempting to choose the right bank, many people find that size does matter. Generally, small businesses develop a better relationship and receive better services (including small business loans, overdraft protection, and lines of credit) from small community or regional banks. It is important, on at least an annual basis, that you review your relationship with your bank and consider the products and services of your bank’s competitors.

Finally, the bank plays a crucial role in managing your cash flows, from the way receipts are recorded to access to lines of credit, and the like. It is essential for you to understand your relationship with your bank and use it effectively to manage your cash flows. Chapter 3 of this book provides some helpful information that you can use to better prepare yourself to meet the expectations of banks as you attempt to carve out the best relationship for your business.

Safeguarding Your Cash

Cash management and managing your cash flows are major challenges for any small business and business owner. The necessity to safeguard and protect cash and resources adds another formidable challenge to your list of key owner or manager responsibilities. If you have not yet experienced it, you need to be aware that fraud should be one of your key concerns. Fraud continues to be a growing menace to the health and viability of all businesses—including small businesses. Your job is to know how to counteract it (preferably, before it happens).

There are several conditions that allow fraud to occur, including: poor internal controls; collusion on the part of employees and third parties; management override of internal controls; and, having high cash transactions and activities. Accompanying these conditions are several preconditions that must be present for fraud to occur. These preconditions include the following:

1. Need—which exists when a person, such as an employee, has a perceived urgent financial requirement such as overdue bills, mounting debt, or personal desires not supported by personal financial means.

2. Access—which is possible when a person has a position working with cash or desirable business assets.

3. Opportunity—which arises when a business with poor or a lack of internal controls provides great potential for fraud to occur.

4. Rationalization—which can easily occur when, for a variety of possible reasons, a person is convinced that committing fraud is justified (e.g., a person holding a grudge over additional pay or other compensation believed to be due—even if this source of dissatisfaction is not known to you).

Following is a list of the means of discovery of fraud, in order of discovery frequency:

1. Internal controls

2. Notification by an employee

3. Internal audit review

4. Management investigation

5. Notification by customer

6. By accident

7. External auditor review

Please pay special attention to the fact that fraud discovery by external auditor review has the lowest discovery frequency. Therefore, seeing to it that your business maintains good internal controls is essential for discouraging and detecting fraudulent activities. For some very helpful examples of specific methods of internal control that can help you in this regard, see the theft and fraud section of Chapter 6 of this book.

Using Technology in Managing Cash Flows

Effectively managing cash flows requires the use and regular review of cash flow reports, and technology can play a significant role in that regard. The reports that show entire inflows and outflows of cash in your business can be created in a number of ways. Begin with your accounting software programs, which are designed to: (1) assist in managing small business accounting functions; and, (2) have built-in report generation functions. For example, QuickBooks accounting software has an excellent cash flow management tool that is straightforward and effective. You should also look to your accountant to develop the kinds of reports that are needed, including keeping track of the critical timing of the reports needed to effectively manage cash flows. There are also free templates that are available to generate cash flow reports. Many of these are available at local small business development centers (SBDC’s), and the U.S. Small Business Administration. Also, in today’s environment, what would you do without cellphone applications (apps)? Yes, cash flow apps are available, many of which are free; although, some may require a monthly subscription. Pulse is a great app and it costs a nominal amount each month. Another popular app for small business is Enloop, which is free and assists in creating financial forecasts, as well as in writing a business plan.

Summary

Managing cash flows is vital to the success of your small business. You play critical roles in managing the cash of your business. Implementing cash management strategies ensures effective use of your business’s most important asset. Use of a cash budget further assists you in forecasting and predicting cash inflows and outflows. Finally, understanding and analyzing the statement of cash flows and its components will give you information for the critical decision making that is required for small business growth and profitability.

Chapter Summary Checklist