1

A RICH DECISION: MAKE THE CHOICE TO

UNDERSTAND YOUR MONEY

Decision is the ultimate power.

—Tony Robbins

If you want to find out the meaning of life, go to New York City.

When I was twenty-eight years old, I had a life-changing moment that would alter the trajectory of my life. Some would call it an epiphany, others a financial wake-up call. I call it a financial awakening.

In the fall of 2014, I was living in New York and enjoying every minute. My career was taking off, I was making lifelong friendships, and I was continuously learning. Life was perfect.

New York taught me about life, the minimum viable space for an apartment, the art of navigating crowded subways, how to hail a taxi, and the value of work. With a city that eats up most of a young professional's budget with rent, it also taught me how to survive on a small amount of discretionary income. Allocating my spending was crucial to survival, and as a result, savings was always a second thought, if a thought at all.

But one evening everything came crashing down. For some reason, I decided that I wanted to start saving more—well, really, just save at all. I was getting sick of just getting by every month. Something inside me was saying there was more to life than living paycheck to paycheck. So I sat down at my desk in my fifth-floor walk-up apartment, overlooking Brooklyn, and put together my first real budget.

That is when the clouds parted.

As a newly minted certified public accountant (CPA), I lived in Excel most of my days and nights. Creating financial projections for existing businesses, models for business plans, and slicing through mounds of data were routine projects. But modeling out my own future and thinking about the business of “me” always seemed to fall to the bottom of the to-do list. I decided to change that by sitting down to figure out exactly where I stood.

The result was not pretty. My financial life was in shambles. If I was going to save myself, I knew that I needed to do something quick and drastic. At that moment, I decided to change. I decided to change my relationship with money forever and turn professional with my finances. That is when my money makeover began.

Something tells me you are looking to do the same.

That evening is seared into my mind as one of the most transformational moments of my life. It was a moment of full decision. I was going to stop. I was going to stop living on the edge. I was going to stop unnecessarily spending on clothes, trips, and going out with friends. And I was going to stop living in New York, the city I loved. My financial life was a wreck, and the only way to fix it was with a complete money makeover.

This will happen to you too. Perhaps it already has. There will come a time when you realize you are losing control of your finances and everything isn't quite working out. You will become tired of the routine—fighting through the Sunday Scaries, hating Mondays, living for the weekend, and haphazardly spending money. When you finally become fatigued by it all, you will know it is time for a change.

Perhaps that is why you picked up this book?

I changed my life during my late twenties, but only after I dusted off the haze of the previous years. If I remained entrenched in my old routine, I realized my long-term financial outlook was bleak. If, on the other hand, I wanted the financial freedom that I had always dreamed of, then I was going to have to make major changes in my life. The dormant need to take control of my life was beginning to wake up. It was time for a money makeover.

When we first start our careers, all we know about money is that we do not have enough of it. And far too often, we are naive to the fact that creating a solid financial base in our twenties and thirties will pave the way to lifelong financial success. Our distraction is not without merit. As young professionals, we are perpetually engrossed with the mythology of the success sequence: trying to find the right job, the right spouse, and just generally working things out.

We tend to become overwhelmed with life's expenses, and as a result, we are always stressed about money. The comforting news is that you are not alone. Nearly 70 percent of Millennials report feeling financially stressed.1 Making the choice today to get your finances in order can alleviate this burdensome stress and increase your happiness.

If you are merely starting to think about paying off your debt, saving, or developing a financial plan, this book will guide you on your way to financial success. This book will help you set up the financial ecosystem to create lasting change. You will finally be on your way to financial freedom.

Sounds great, right? Well, there is one catch. The steps in this book will present the agenda for success. But as it is with most difficult decisions in life, change can only begin with you taking action. Picking up the phone to call your credit card companies, setting up your savings account, opening retirement accounts, and automating your finances will all have to be done on your time and by the work of your own hands.

Turning Professional

Let this moment be one that you remember. Realize that this is a unique opportunity. You have the chance for a complete transformation—to escape debt, build up savings, create a career that matters, and live life on your own terms.

Take the time today to consciously decide that you are going to turn professional in your finances. This will be one of the most important decisions you will ever make. Commit to leading an exceptional life in which you can buy your dream car and purchase that perfect house.

“I could divide my life into two parts: before turning pro and after.

After is better.”

—Steven Pressfield, Turning Pro

The concept of living a financially healthy lifestyle is not novel. It is, however, a very hard thing to accomplish in today's society. We live in a world in which we are perpetually inundated with marketing campaigns designed to pull us away from being financially prudent. The competing messages are everywhere: Buy this fancy new purse. Don't you need that new shirt? Do you have the latest iPhone? We are constantly reminded of our inferiority if we do not have the appropriate stuff Ignore those voices and listen to the one in your head (that would be me right now). You do not need excess, and you do not need more. Look around you; you barely use what you already own (more on this in Chapter 3).

A money makeover starts with the realization that you are an incredibly important person. Mastering your money is worth every minute of your time. You need to recognize that only you control your financial destiny.

This book is here to help as a financial tool. As humans, we are hardwired to use the tools around us to construct our environment. Use this tool to better your life. In this book, you have the insights and perspectives of those who have gone before you. They are adamantly showing you the path to success. Live a debt-free life. Invest when everyone else is spending. Create the income to last a lifetime. When you start to get uncomfortable, that is when you know you are beginning to get close. Launch yourself, and your finances, forward.

It is the few who end up on the path to success, but there is always time to change the road you are on.

Turn professional today.

Building Your Confidence

Stop deferring action to the future. Do I need to pay that bill today? Can I just make the minimum payment? Should I make my student loan payment this month? One reason why people procrastinate when it comes to making hard choices is fear. Fear that they will have to change. Fear that they may be socially excluded from the tribe. Fear that they will be wrong. This fear causes paralysis and fuels the status quo.

Fear is public enemy number one.

“Skill and confidence are an unconquered army.”

—George Herbert

The good news is that fear can be beaten. Fear ushers in negative thoughts, which lead to negative actions or inaction. The best way to beat fear is by confidence-building. By replacing your negative thoughts with positive and confidence-building thoughts, the cycle of fear can be broken. Our brains are remarkably powerful, and if you train your brain to harness the power of positive thinking, remarkable changes begin to unfold.

One of the secrets of the rich life is: Confidence is a commodity. Confidence can be developed, mined, and acquired over time. By practicing confidence-building techniques, you can produce confidence to be used at your convenience. This confidence will permeate all aspects of your life, including your career, personal relationships, and money management.

The following list displays fears people face when failing to realize their financial potential. Read the fears and their associated confidence-building responses out loud. You can download a spreadsheet with blank responses at MillennialMoneyMakeover.com

Do you feel that? That is confidence beginning to flow through your veins.

A history of poor financial decisions can lead someone to think they cannot master their finances. You do not lack ability, only knowledge that you will acquire shortly. But fear is a nasty little emotion that feeds on itself. The fear that is developed through constant debt and living a financially poor life is proliferated by a lack of three major aspects to success: autonomy, mastery, and purpose.

Popularized by Daniel Pink in his bestselling book Drive, these three aspects of success harness the power to gain fulfillment in most of life's endeavors.2 Attain these three qualities in your financial life, and you will regain control of your future. Let's take a look at each one.

Autonomy

Financial autonomy, or the freedom from external control, gives you the ability to break free from dependence upon your next paycheck. If you decide that you want to quit living what I call the “just in time” paycheck lifestyle, then you need to change your relationship with money. That starts by keeping money around instead of giving it away.

What constitutes financial autonomy? When you have no debts to repay, that is financial autonomy. When you have enough savings to take a year off that is financial autonomy. When your investments produce a secondary income stream, that is financial autonomy. Financial autonomy gives you the freedom to choose what you want to do in life. It liberates you. Maybe you finally want to start traveling or explore a new career. Whatever your reason, autonomy gives you the freedom to make choices. But you have to choose financial autonomy first.

Mastery

Mastery produces a kind of pride and passion. Lack of mastery, however, makes us nervous and fearful. When it comes to mastering money, most people run in the opposite direction.

There seems to be an infinite number of choices about what to do with your money. Confusion about what to do induces financial paralysis. Amid the cacophony of advice, we have been erroneously conditioned to think we need to know everything about money. The steps and principles in this book will give you all that you need to know.

Mastering your money is a necessary part of your self-education. Luckily, it only requires middle school–level math skills and an appetite for change. During your flight into financial fluency, keep the words of the Stoic philosopher Epictetus in mind: “Only the educated are free.”3

Purpose

Developing yourself, and your finances, allows you to pursue your purpose in life. You are called to do something wonderful. For some this means teaching, starting a new business, or founding a charity.

Purpose is the deep urge you feel toward your life's work. It means finding your passion and pursuing it relentlessly. But purpose needs room to germinate. Whether your passion is philanthropy, art, writing, or business, financial stability lets you do more of what you love. Financial stability lets you find your purpose.

![]()

Confidence-building is a decision that we make every day. You will have to remind yourself of that continuously because the financial system is designed to decrease your confidence. But there are no recurring fees to be made on the financially intelligent. Understand that there is a lot of useless information about money and finances out there. By aiming to achieve financial autonomy, mastery, and purpose, you can hone your financial acumen. You can learn to surgically remove the useless information and decipher what is important. This process is the key to confidence-building.

The Path of Least Resistance

In recent years, technology has democratized access to information, and the former gatekeepers are slowly fading away. The market for financial advice is now saturated with opinions and overwhelming amounts of information. With the age of information asymmetry officially behind us, no one has stopped to ask if that is a good thing. It turns out, this new onslaught of information overload can actually begin to work against you.

There seems to be an infinite amount of choices about what to do with your money: options, stocks, warrants, investment properties, bonds, high-yield investments, and dividends. The terms and options seem endless. The information overload begins working against you, and you get stuck. There are just too many choices. Instead of making a decision, you simply do nothing, but find yourself yearning for a path to follow. That lack of financial action comes from an internal conundrum called the paradox of choice.

Marc Cuban, billionaire investor and outspoken owner of the Dallas Mavericks, has mastered this concept. Cuban has had tremendous success in business, and one of Cuban's core mantras, although initially counterintuitive, is that businesses should offer fewer options to customers, not more. Offering the path of least resistance to customers, which means fewer options, he says, “is a lesson in basic business.”

In his 2011 book How to Win at the Sport of Business, Cuban details the debate between two schools of thought in the advertising and television universe in the early 2000s: Is it better to offer unlimited channels or suggestive programing to customers?

Others seem to think that unlimited choice is the holy grail of TV. It's not. The reason it's not is that it's too much work to page through an unlimited number of options. It's too much work to have to think of what it is we might like to watch. We are afraid we might miss something that we really want to watch. . . . The smart on-demand providers will present their programming guide more like Amazon.com and Netflix.com, both of which do a great job of “suggestive programming.”4

This phenomenon of suggestive programming harnesses the power of the paradox of choice or the concept that customers may choose nothing when confronted with too many options. So reducing choice can significantly reduce anxiety for customers. As it turns out, this has a profound effect on how customers feel when they shop. For big business, limiting choices can mean increasing the bottom line. The same is true for you.

Aside from Cuban's business instinct, the paradox of choice is also grounded in social psychology and behavioral economics. Columbia University's Cheena Iyengar and Stanford University's Mark Lepper set out to examine how potential customers would react to varying degrees of choice. To do this, they set up booths outside an upscale grocery store in northern California and tried selling jam.

During the first week of the experiment, the researchers offered prospective customers a display of twenty-four varieties of jams. Then, a week later they set up shop again, but this time they only offered customers six varieties of jams. As you might have guessed, more people stopped by the first booth with the greater number of options than the second booth with fewer options. But when researchers examined the sales data, they found a peculiar occurrence: Only 3 percent of customers made a purchase from the booth containing twenty-four varieties of jam. This contrasted with the 30 percent who bought jam from the booth containing only six varieties of jam.5

This proved a valuable lesson: Less was more.

With all of the noise in our daily lives—work, Instagram, family—getting people to stop and concentrate on one task is becoming increasingly difficult. In our attention-driven economy, giving people the best options quickly can be the difference between success and failure. That is precisely what you will get throughout this book.

The money makeover is designed to walk you through exactly what you need to create a healthy financial ecosystem. Think of this program as the path of least resistance, or your suggestive financial programming. Ignore the advice of pundits or talking heads when it comes to finance. They generally offer horrible advice (unless, of course, they are recommending this book).

Money is easy to master, and I am going to show you exactly how to master it. You will be able to slice your way through the noise and finally achieve your financial goals. The path is here for anyone to take.

It May Get Harder Before It Gets Easier

The suggested course you are now on (reading this book) is the path less traveled. You are trying to do something that most people never accomplish in life. This will require learning the language of money, good financial behaviors, and confidence-mining techniques.

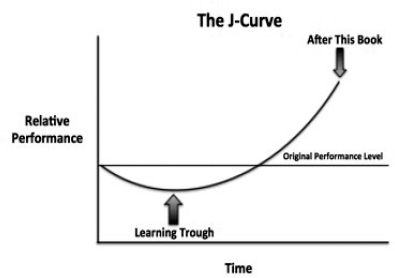

As with absorbing anything new, there will be a period of time where your skills may become worse than when you first started. Then, over time, your skills will gradually improve, and you start the ascent up the learning curve and go on to achieve mastery (remember Daniel Pink). According to Seth Godin, marketing expert and author of The Dip, rewards flow disproportionately to those who achieve mastery.6 So why not reap the rewards?

In economics, this concept is known as the “J-Curve.” Its application can be seen across some of the most sophisticated industries including private investment, global trade, biotechnology, and personal finance.

The initial outlay of time and energy is followed by a dip into the learning trough. This type of downward learning is what Josh Waitzkin, world champion chess player and author of The Art of Learning, calls “investment in loss.”7 This early investment is a necessary step to internalize the fundamentals of whatever skill you are trying to acquire. In your case, you are trying to master money. Internalize all of the concepts in the next several chapters, and before you know it, you will be on your way up the learning curve.

Many people descend into the learning trough never to resurface. Don't let that be you. The people who devote themselves to the process and embrace the learning eventually begin to absorb the concepts they are studying. Model yourself after Waitzkin, who used this concept to become a National Master in chess and a world champion in Tai Chi push hands, conquering wildly different skills.

Learning successful financial habits will help you build the life you want. While in the throes of learning, you may be tempted to abandon your commitment to sound personal finance. Remember, it may take losing in the beginning to learn the lessons of success. This is your tuition into the university of knowledge. And if you find yourself getting frustrated, remember the J-curve. If it is hard now, easy is just around the corner.

Why Talking to Yourself Is Okay (for Now)

Shay Carl talks to himself. And he laughs at himself in the mirror too. For the thirty-something YouTube extraordinaire, this was a necessary part of his routine.

In an interview with angel investor and author Tim Ferris, Carl reveals that he used to intentionally laugh at himself in the mirror to increase his happiness. He was trying to harness the power of positive psychology and make himself feel physically better before beginning his YouTube videos. Carl had this crazy idea that if he could make himself feel happier, it would translate to his YouTube audience. And translate it did. Carl turned himself into a YouTube celebrity, and his channel has more than two billion views.8

Carl began his YouTube career in the midst of a midlife crisis. On the verge of a mental breakdown and sick of working his day labor job, Carl decided to change his life. As a means of coping with his newfound anxiety, Carl filmed himself, and sometimes his family, every single day for 365 days until fame came his way. He literally laughed his way to success.

For that transformative year, Shay Carl showed up every day. You need to show up every day too. The numbing routine of daily life keeps most people from achieving success. But you are not most people.

Talk to yourself in a positive light and laugh your way to success, just like Shay Carl. Use the proven positive psychological benefits of interrogative self-talk, which is a method of asking yourself pointed questions that force you to search inward. For example, a great way to kick off your day when confronted with a challenge might be, “Can I do this?” Remarkably, when you begin asking yourself questions out loud, your mind turns inward for answers, and they are always there.

Ask yourself the right question, and you just might find you already have the answer. Getting your debts paid off, building savings, and learning how to optimize your finances will take a dedicated focus.

Do you have what it takes?

Breaking the Habit Loop

In everyday life, people make huge financial decisions without giving them much thought. Sometimes, if we think the decision—what college to attend, how to pay for graduate school, or buying a home—is significant enough, we consult with family and friends. The problem is that our family and friends enthusiastically support what they think we want to hear, not what we need to hear.

This is especially true when it comes to money.

In many households, discussions about finances and money remain taboo. Discussing real-world financial topics, such as student loans, financing a new car, or securing your first mortgage, can bring to light hard economic truths about your situation. We never seek objective advice; instead, we rely on family and friends who are invested in our personal story to tell us what we want to hear. We look for affirmation, which they gladly provide. As a result, many people make horrible financial choices very early in life because they do not receive proper counsel. Well, not anymore. Consider the old paradigm broken.

“Make good habits and they will make you.”

—Parks Cousins

The lack of communication around critical and expensive decisions creates a cycle of bad behavior. This cycle leads to a repetition of crucial financial errors made early in life by millions of Millennials. Our lack of communication is a bad habit that society needs to break.

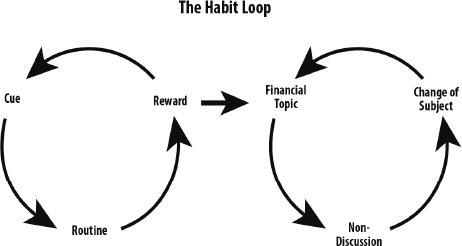

In his groundbreaking book The Power of Habit, author Charles Duhigg discusses how habits work and describes them through the “habit loop.”

The habit loop consists of a cue, followed by a routine, and finally a reward.9 Let's take a look at our society and the current habit loop associated with discussing money. The habit loop begins with the cue to discuss some particular personal finance matter, which is demonstrated in the following example.

Jenny is a recent college graduate and has started her marketing career as a junior account executive. Earning a salary of $50,000, Jenny decides she wants to buy her dream car, a BMW. Jenny believes this car will show her family and friends she is responsible, successful, and ready to take this whole “adulting” thing seriously. But before Jenny heads to the local BMW dealership, she decides to ask her parents for some advice about her new purchase.

Jenny: Mom and Dad, I want this new 2018 BMW 328i. I am so excited to get it (Jenny pulls out her phone to show her parents pictures of the car). Doesn't it look awesome?

Mom: Wow, that is cool. But buying a new car is a big decision, Jenny.

Dad: Jenny, I love BMWs. That's why I have the X5. BMWs are pretty expensive though. Good for you.

That is typically where the conversation ends. Jenny's general inquiry, the cue, is met with a routine of nondiscussion. This avoidance of difficult topics is often accompanied by deflecting phrases such as:

- “That is a big decision!”

- “You should talk to a financial advisor about that!”

- “Are you sure you can afford it?”

These indifferent statements do not help anybody and are intended to spur the habit loop to its final phase, reward. In this case, the reward is moving on to another topic of conversation or perhaps washing the dishes or doing the laundry. It seems people will do anything to avoid hard discussions. Why is this? The reason is because everyone around you is invested in your success.

No one wants to tell Jenny that buying a new BMW right out of college is a horrible financial decision (see Chapter 4). Instead, they want her to be “happy.” The outcomes of hard discussions can be a bitter pill to swallow and are often deferred to someone outside the family and friends circle—typically, the student loan-lending officer, the mortgage broker, or the financial advisor. The problem is that these people don't have a real responsibility to help you.

That's where this book comes in. I am not invested in your “happiness.” Instead, I am invested in your financial success. I want you to be able to pay off your credit cards, get rid of your student loans, buy your first car, invest in income-generating assets, save for retirement, and eventually buy your first house. I want all of that for you. But we are here to have that awkward conversation of what makes good financial sense. We will have a conversation of substance about your financial fitness.

The power of habit can be deceptively strong. So, first things first, we are going to break the old habit loop. Instead of not talking about finances, we are going to discuss all the major financial decisions you will make. We are going to dive into how much to invest, when to pay off your credit cards, and how to build a financial future that will make you proud.

The key to getting on the right track is to create new and productive habits. This means a complete makeover to your current way of thinking and acting. Adding in positive habits and subtracting negatives habits will help you navigate the daily churn of distractions. The formula might take a moment to get used to, but once you adopt this new process, talking about money will become fun. You will have created an entirely new and healthy financial habit.

Why Setting Goals Makes You Win

Getting started, or unstuck, is often the biggest hurdle to success. But once you start to generate momentum, creating and achieving goals is fantastically important for sustained success. Goalsetting fertilizes the seed to your success because it bridges where you are today with where you want to be in the future. Goals give you a tangible and measurable path to follow.

Let's turn to an iconic Olympic champion, Michael Phelps. Throughout the course of his star-studded fifteen-year career, Phelps won twenty-three gold medals, three silver medals, and two bronze medals. His twenty-eight Olympic medals make Phelps the most decorated Olympian of all time.10

How did Phelps achieve such greatness? He set goals for himself very early in his career and remained adamant about meeting them. In fact, at the mature age of fifteen, Phelps already wanted to compete in the Olympics. He set that as a long-term goal and made it a reality. When asked how he approaches his goals, Phelps says “day-by-day.” That should be your approach too.11

“He that would have fruit must climb the tree.”

—Thomas Fuller

As you can see, setting goals is extremely important because it gives you a clear path on the road to success. Whether it is waking up at 5:00 a.m. to head to the pool for a workout or posting a daily YouTube video, achieving small wins will propel you toward your larger goals.

When you set goals, you unleash one of the human mind's most powerful tools, the subconscious. Even when you are unaware, your subconscious mind will begin to internalize your goals and build a deep current of thought that pulls you toward ultimately achieving your goals.

Setting goals can take you on a wild ride to success, but it all starts with laying the foundation of mapping out where you want to go. As humans, we are engineered to achieve. Sit down right now and think about your short-term and long-term goals. These could range anywhere from paying off a student loan or saving up for a down payment on your dream house. Spend time formulating a strategy for your future and develop a winning plan. Take a look at the following chart to gain inspiration for your own desired accomplishments. Go to MillennialMoneyMakeover.com to download your own goal-setting spreadsheet.

Be honest with yourself as your look at your answers. Are you aiming for what you want? Greatness is never achieved through small goals. Set high standards for yourself and begin the climb.

The Professional

At some moment (hopefully today), you will decide to change the direction of your life. When you realize that being in debt sucks, a lack of savings breeds anxiety, and that your future is purely in your hands, action is required. Deciding to turn professional is never easy, but once you taste success, you will find yourself looking back and wondering why you didn't act sooner.

As a professional you will:

- Increase your confidence

- Change the direction of your life

- Grasp the concept of the J-curve

- Work on creating good financial habits

- Develop short- and long-term goals

- Internalize sound financial judgment

As you will see in the next chapter, the second major step in the money makeover is to eliminate all of your debt quickly. There will be moments when it seems hard, but ride through the dip of the J-curve and remember that success is on the horizon. Encourage yourself with positive self-talk and reinforce your successes. When the going gets tough, remember that you have someone here who cares about your success and wants you to change the road you are on.

Welcome to the professional life.

![]()

Action Items

The money makeover is all about momentum. With inertia on your side, you can start to make positive change in your financial life. Throughout this book, you will incrementally build upon the ideas presented in this chapter. While absorbing and implementing this new skill set, remember the following steps:

- Decide to turn professional with your money.

- Build up confidence in yourself and your abilities.

- Break bad habits and learn now to create new ones.

- Set short- and long-term goals.

- Decide to go all in on your money makeover.

Accelerate your money makeover by internalizing everything that is laid out in the following chapters; they are here to change your life.