5

MINTING MOMENTUM: SAVING, INVESTING,

AND CONSTRUCTING YOUR RETIREMENT

Wealth that stayeth to give enjoyment and satisfaction

to its owner comes gradually, because it is a child born

of knowledge and persistent purpose.

—George Clason, The Richest Man in Babylon

If you are an average Millennial, saving for the future has not been a top priority. However, if you have read this far, you already accomplished what most never will. You have turned professional with your money. You have paid off your debts. Your budget is humming on autopilot. You are optimizing all your large purchases. Now it is time for the fun part: getting rich.

Building wealth is a habit. In this chapter, you will learn how to reinforce that habit by building an emergency fund and reaching slush-fund status, as well as learn to invest and save for retirement.

The rich life is quickly approaching. Now is the perfect time to welcome it with open arms and lay a remarkable foundation.

Humans Aren't Wired for Saving

The state of Millennial savings needs a drastic makeover.

Most Millennial simply have not saved enough cash for unexpected expenses, true emergencies, or retirement. It seems the more conceptual the event, the more ill-equipped Millennials are to save. According to the Federal Reserve's 2013 Survey of Consumer Finances by economists from the Economic Policy Institute, “Nearly half of working-age families have nothing saved in retirement accounts, and the median working-age family had only $5,000 saved in 2013.”1

Clearly, we have some work to do.

This chapter is about answering a fundamental question: Are you saving enough? Depending on where you are in life, it is one of those questions that can elicit extraordinarily different responses. The answers typically go something like this:

- Twentysomething: Saving? Isn't that something only wealthy people do? I plan on saving more in the future, but right now I am just trying to survive.

- Thirtysomething: Saving? Well, I have a 401(k). Does that count? I would save more, but my kids and house are much more expensive than I anticipated!

- Fortysomething: Saving? Of course I am saving. But have you seen college tuition recently? My financial advisor tells me it is going to cost me a quarter of a million dollars to send my kids to college!

- Fiftysomething: Saving? I can tell you one thing: Working every day is getting old. I feel like I need to start putting more money toward retirement so that it will finally get there someday.

The data is clear; most people are not living the money makeover lifestyle. As a result, their approach to savings is haphazard, and this leads to dangerously low savings. But how have these abysmal savings habits come to pass? How has the “Do It Yourself” retirement system failed so many people? One reason could be that humans aren't wired for saving.

Like any machine or software, we are only as good as our operating system. One part of our developed brains, which makes us uniquely human and sets us apart from other animals, is our frontal lobe. This more recent evolutionary development allows humans to imagine the future and develop a more robust understanding of the world. Our frontal lobe gives us the capacity to plan for the future, which can be wonderfully advantageous. However, it can also produce anxiety surrounding the anticipation of how that future will unfold.

From a financial perspective, modern man relies on the frontal lobe to see the need to save for retirement. It turns out, with all of the frontal lobe's amazing benefits, it does have some faults. When we think about deferring savings, we tend to enjoy the thought of reaching the savings goal more than actually doing the saving.

Humans enjoy visualizing the completed product. As Harvard psychology professor Daniel Gilbert emphasizes in his book Stumbling on Happiness, one problem with dreaming into the future is, “people find it easy to imagine an event, and they overestimate the likelihood that it will actually occur.”2 In other words, there is a gap between where we are now and the future we imagine. Our imagination bridges that disconnect. That imaginary bridge holds us back from actually saving as much as we should, unless we convert the imaginary into tangible and actionable steps. This process is critical to long-term financial success and overriding our core operating system.

Another caveat with the frontal lobe is how it works. Although we can imagine ourselves in the future, we default to imagining the current version of ourselves. When it comes to successfully saving, the version of ourselves we see in the future can have a profound effect on how we save.

To demonstrate this, Hall Hershfield, a social psychologist at New York University, conducted an experiment. Participants were asked to wear virtual reality headsets, and Hall divided the participants into two groups. The first group saw a digital representation of themselves in their current state for a brief time span. The second group also saw a visual representation of themselves, but this time, a software program aged the participants' images to seventy years old. After using the virtual reality headset, both groups of participants were asked a series of questions. One of the questions regarded money allocation: What would you do with $1,000?

The group who saw themselves at their current age said they would save $80 for retirement. The group who saw the older version of themselves allocated $173—more than twice the first group—for retirement.3

According to the researchers, thinking about yourself in the future as your current version is equivalent to thinking about a stranger (no wonder you only gave up $80).4 But when you harness the power of technology and virtually age yourself, the stranger becomes much more familiar. The stranger becomes, well, you. This visualization process can have a tremendous impact on how much you save during the course of your life.

When we are reminded that growing old will happen whether we like it or not, an internal change takes place. Visualizing the aged version of yourself can be the difference between saving 8 percent or 16 percent for retirement. Throughout the course of a career, that can produce 401(k) millionaires (more on this shortly).

Savings Makes You Look Younger

“Not only do I feel better, but I just don't have to worry about things as much,” said one of my blog readers. The positive psychological benefits of having a financial buffer are amazing. Your outlook on life becomes positive and forward-thinking because you don't worry about meeting the present.

The mind is a wonderfully complex machine, and when it knows that it has room to breathe, it thanks the body. Knowing that losing your job, damaging a car, or paying an unexpected medical bill won't leave you broke can create space in your life. This space can be used to concentrate on other tasks. Instead of slogging through the day-to-day struggle, you can focus on doing things you enjoy and start looking younger during the process.

Stress ages people, and financial stress is no exception. A recent study on financial stress showed that worrying about money can make you appear older. According to Margie Lachman, a psychology professor at Brandeis University and one of the study's authors, surprised researchers discovered, “financial stress was related just to how old you looked to others. It was not related to how old one feels or how old one thinks they look. So it showed up to others in one's appearance, but not in terms of one's own subjective views or perceptions of their age.”5

Researchers speculated as to why participants would appear older to others when they were financially stressed, but the question is still unanswered.

Perhaps people who don't have to worry about money can:

- Spend more time working out

- Take the time to care for their appearance

- Afford more nutritional meals and snacks

- Buy higher-quality clothing and beauty products

- Spend less time frowning

The point is: Erasing financial stress can have a massively positive impact on your life. By removing the weight of poor finances, you can distance yourself from the paycheck-to-paycheck lifestyle. This allows you to do more of the things you love. Let's learn how to create that space in a specific sequence, which begins with building up a cash cushion and ends with FU money.

How to Reach FU Status

Financial peace of mind equals cash accumulation. But the vast majority of people just don't have enough cash saved. Paying off reoccurring debt, trying to strike it rich with the next hot investment, or spending on the sparkle of a new purchase distracts even seasoned finance aficionados from savings. The following steps are critical to generating enough savings to eliminate financial stress and begin looking younger immediately.

Step 1. Start an Emergency Fund

Virtually every financial advisor (human or machine) has one rule: Make sure you have an emergency fund. This is especially true for people who are starting to get their finances together for the first time. An emergency cushion, as it is so aptly named, is a preventative measure to stop you from dipping into your savings in the event of unforeseen unemployment, unexpected medical bills, or a random accident.

For those who don't have savings set aside for emergencies, there is a temptation to pay for unexpected bills with credit. This can begin, or even perpetuate, a credit card debt cycle. The financially fit prepare for the inevitable emergency.

Personal finance personalities such as Dave Ramsey and Clark Howard popularized the concept of the emergency fund. On Ramsey's award-winning talk radio show, The Dave Ramsey Show, he argues that you should have at least $1,000 set aside in your emergency fund. And he was right—twenty years ago. For the modern Millennial, you need at least $3,000 set aside for an emergency fund.

The necessity of establishing an emergency fund in your money makeover is a critical part of distancing yourself from the breakeven lifestyle. Most people ignore this advice and continuously dip into their savings account, inhibiting their financial progression. A lack of an emergency cushion removes a protective layer, which could stifle your money makeover.

Your future can change in an instant. A perfect budget can be smashed to pieces by a million variables. Preparing for that eventuality today will soften the blow tomorrow. By establishing a safety net, you will build up your confidence and alleviate the stress of the marginal escape. Save $3,000 for your emergency fund and start protecting yourself now.

Step 2. Build Up a Slush Fund

Once you have $3,000 in your emergency fund, you will be well on your way to gaining financial peace of mind. The next step is to build on your momentum and increase your financial health. In finance, there are a million ratios for determining financial health. The lion's shares of ratios are irrelevant, but one stands out as my favorite: the monthly living expenses covered ratio (covered ratio), or the amount of savings you have accumulated divided by your monthly living expenses.

The covered ratio is a beautiful barometer of financial health. This ratio shows how long you could last without any income. Take a look at your budget from Chapter 3. Your monthly living expenses includes expenses such as rent, food, transportation, and utilities. The rule is: The higher your covered ratio, the greater your financial health. Calculate your covered ratio. How long could you last? One month? Two months? A year?

A good rule of thumb is to have a covered ratio between 3 and 6, which would allow you to live off of your savings for three to six months. This is important because it typically takes ninety days to find new employment, thereby providing a fantastic hedge against any unforeseen, or voluntary, unemployment. It is important to point out that your covered ratio does not include your emergency fund. When calculating your covered ratio, only use the amount above your emergency fund balance.

The following chart contains a list of financial health categories based on your covered ratio.

| Covered Ratio | Financial Health Status |

|---|---|

| Less than one month | Breakeven |

| 1–3 months | Padding |

| 3–6 months | Slush fund |

| 6–12 months | Options |

| 1–5 years | Bright future |

| More than 5 years | FU money |

Don't get overwhelmed if you are not where you want to be right now. This is simply a snapshot in time. Now that you know your covered ratio, and what it will take to build up your slush fund, you can pursue it aggressively and increase your financial health.

The covered ratio democratizes the appraisal of financial health. If you decrease monthly living expenses and increase savings, you can rapidly improve your financial health. Once you start to climb the ladder of economic health and reach slush-fund status, then it is time to press the accelerator.

Step 3. Reach FU Status

For those readers who want real freedom, you should aim to accelerate your savings and reduce your consumption to accumulate more than six months of living expenses. Once you accomplish this, you can focus on amassing more than a year's worth of living expenses. That is when financial freedom begins to set in and you start absorbing the positive psychological benefits of having money.

The rich life shows itself to those who are persistent and form good financial habits. The magic of the rich life is that it opens up the doors to so much more in life. Instead of focusing on barely getting by, you can focus on becoming a more refined version of yourself.

Reaching FU money status allows you to pursue opportunities as they come across your desk without the cloud of financial considerations. You will have already done your work up front, and now you can reap the rewards of flexibility. Maybe you can finally pursue your passion project full time, tell your bosses to shove it, or take time off to build a new business. In the end, a more substantial covered ratio facilitates more options, peace of mind, and newfound freedom.

Invest Your Ass Off

I can't write a personal finance book without talking about investing. In this section, I am going to cover the basics. As you start to generate momentum with your emergency fund and slush fund, you encroach on a point of critical mass. Once you have your slush fund built with cash, anything after that point should be put to work.

That takes place in the world of investing. The idea of investing is simple: You allow other people to use your money, and you defer consumption. In turn, you accept a rate of return, which varies among different types of investments, and you watch your money grow. It is worth noting that all investing involves some level of risk, so performing your due diligence, weighing your risk tolerance, and understanding your desired rate of return are all vital aspects to successful investing. Although investing involves risk, it is the single greatest way to accumulate wealth over the long run. Investing is how most millionaires become millionaires. It is how the rich remain rich.

To get you started, let's look at some common terms you need to know:

- Time value of money: This fundamental investing principle states that money available today (present value), is worth more than the same amount of money in the future (future value) because of its potential earnings capacity.

- Interest: This is the charge that a borrower pays to a lender for the privilege of borrowing money. Interest is meant to compensate the lender for their delayed consumption. Usually expressed as a percentage, interest can vary depending upon expected inflation, length of loan, riskiness of borrower, and more.

- Compound interest: This is interest paid on the initial principal of a loan plus accumulated interest on the loan. The rate at which compound interest accrues depends upon the number of compounding periods in the loan. For example, a 5 percent semi-annual loan accrues faster than a 10 percent annual loan due to the additional compounding period in the loan.

- Equity: Companies are allowed to issue equity, or ownership, in a company to raise capital. Companies do this for all types of reasons—to purchase equipment, invest in research and development, or expand operations. When companies do this, they issue shares of stock for investors to buy.

- Stock: The shares of stock a company issues are typically called “common stock” (there are many forms of stock, but for purposes of this book, let's focus on common stock). These fractional pieces of ownership in the company allow investors to receive dividends, participate in company elections, and have an overall say in company operations. Individual investors (you), can buy stocks on exchanges, such as the NYSE, NASDAQ, and LSE. Once you purchase shares of a company, you become what is called a “shareholder.”

- Debt: If you completed Chapter 2, then you are all too familiar with debt on a personal level. When companies are looking to raise capital (for the same reasons they were in the equity section), they can issue equity or raise debt. Corporate debt is much like personal debt in the way it works, except that when a company is seeking to raise a lot of money in the form of IOUs, they issue what are called “bonds.”

- Bonds: A bond is a debt security that corporations sell to investors. They are essentially small IOUs, which the company promises to pay back to investors in addition to an interest rate, or reward for lending the money.

- Certificate of deposit: A certificate of deposit, or a CD, is a promissory note, typically issued by a bank. These promissory notes are time deposits that limit investor's access to cash for a specified period, or the CD's maturity. CDs range in maturity from only a couple of months to several years. The idea is that you give the bank access to your funds for a certain period of time, during which you cannot use the money. After the CD's maturity has passed, the bank pays you back your principal plus interest.

- Mutual funds: A mutual fund is a pool of money aggregated by investors who hire a fund manager to take their cash and make investments on behalf of the fund. There are many different types of funds with different investment objectives: equity funds, bond funds, or money market funds. Investors can buy into a mutual fund at the end of each trading day.

- Exchange traded funds: Exchange traded funds, or ETFs, are pools of money that track a group of assets, bonds, or equities. They are like common stock on a stock exchange and can be bought and sold throughout the investing day. They are popular for their low fees and broad diversification.

- Target date fund: A target date fund, or a TDF, is a collective investment approach (like ETFs and mutual funds) where the investments chosen by the fund are designed to become more conservative as the “target date” approaches. They are often used to track retirement dates. For example, a TDF 2055 would be a fund allocation mix for a Millennial set to retire by the year 2055.

When it comes to investing the amount of information can be overwhelming, even to seasoned investors. Don't get caught in the vortex of the paradox of choice (Chapter 1). The good news is: Because you are investing, you are winning. Investing allows you to grow your hard-earned capital by leveraging the time value of money and enjoy the bounties of compounding interest. This can grow your wealth at an exponential rate and puts you on the fast track to the rich life.

As a young investor, time is on your side. During your twenties and thirties, you have the added benefit of starting your retirement savings early enough to learn from mistakes and make investing a lifelong habit, which is the greatest predictor of becoming rich. Let's learn how to take your investment knowledge and put it to use for the future you (virtually aged to seventy years old).

Beginning the Retirement Journey

Most Millennials are indifferent to the idea of retirement. Our limited commitments compound our laissez-faire outlook on life. But when life starts to heat up, and responsibilities begin to accumulate, the idea of retirement suddenly starts to creep back into our peripheral vision.

In the money makeover, we look forward to retirement. Instead of staring up at the peak of retirement in awe, we move out of base camp to begin the journey as soon as possible. We embrace the hike. But Millennials have some catching up to do.

“The man who moves a mountain begins by

carrying away small stones.”

—Confucius

A survey conducted by GoBankingRates concluded that 72 percent of Millennials have less than $10,000 in retirement savings.7 There are a variety of factors that steer people away from retirement saving, but the number-one killer of savings is fear. People often use statements such as, “I don't know how to invest” or “The stock market seems too risky.” Fear feeds on itself, so the best way to combat fear is to cut it off early at the pass. Start investing now, and your level of comfort with the concept will skyrocket.

A fundamental principle of investing is: It is not how much you start investing but that you start investing. In the world of compounding interest, saving as much as $100 or $200 a month can grow into substantial investing over time.

Starting a retirement account is the first step. If you accomplish this step during your twenties or thirties, then you are on the road to success. After that, you can focus on increasing your contributions. According to Cameron Huddleston, a Life+Money columnist for GoBankingRates, “The earlier you start saving, the easier it is—really. Thanks to the power of compounding, if you start regularly setting aside even small amounts as soon as you start working, you could easily have enough for a comfortable retirement.”8

By investing early, you will not fall behind like the majority of people. Can you imagine the daily anxiety if you were in your fifties and behind on your retirement savings? Well, the problem is more systemic than people realize. Roughly 78 percent of Americans over fifty years old are behind on their retirement savings. Don't get behind on one of the most important long-term decisions of your life.

Planning for retirement when you are a young professional is the best time to make the conscious decision to save as much as you can. This will alleviate the stress of feeling behind, and it will pave the way for exploration throughout the remainder of your life. Instead of scrambling to stash enough money for retirement in your forties and fifties, you can go on vacations, make memories, and enjoy your peak earning years.

Your relationship with money is incredibly personal. This relationship can define you in more ways than you can imagine. Money orates the tale of who you are, where you come from, and why you are here.

Make your life a great story.

The New Retirement

Googling the phrase “retirement” might make you depressed. According to the first several definitions, which is where most Millennials stop, retirement is “the action or fact of leaving one's job and ceasing to work” How old-fashioned.

Although our economy changed dramatically during the technological revolution of the 2000s, the traditional view of retirement wasn't rebooted. However, Millennials are starting to change that. Most Millennial expect to retire by sixty-two years old, and 40 percent want to semi retire by fifty-seven years old.9

Retirement needs a makeover. Instead of sitting around doing nothing during retirement years, Millennials want to pursue passion projects, explore hobbies, engage in activist opportunities, and monetize their skills. They want to fund their desired lifestyles rather than view retirement as a singular stopping point. With this new view, retirement in general needs to be rebranded; it needs life injected into it. This new definition of retirement is already marinating in the minds of Millennials, so you might want to define what your future looks like too. This begins with forecasting the future.

What do you want retirement to look like? For some, it may mean part-time consulting, writing, advising, or simply spending time with family. Either way, you should develop clearly stated goals. Saving to save is not an optimal strategy (and really boring). You need intention behind your savings to reinforce the retirement habit loop.

There is no better way to formalize a goal than writing it down. Think about your top five goals and write them out. The following spreadsheet is a great example of goals for your retirement. What are yours? Go to MillennialMoneyMakeover.com for a blank spreadsheet of your own.

| Retirement Goals | |

|---|---|

| Goal 1 | Work only three days a week starting at fifty years old. |

| Goal 2 | Travel abroad to different countries at least once a year. |

| Goal 3 | Create a mentor program to stay connected and help my profession. |

| Goal 4 | Own a country home for peace and quiet and a condominium in the city for fun. |

| Goal 5 | Be able to live off of my passive income streams. |

Take a look at what you wrote down. Be honest with yourself. Are those your goals for retirement, or are those goals embodying what other people say should define retirement? If they are not your actual goals, take another shot at writing them down.

The next step is to reverse engineer your path to success. For example, if you wrote down that you wanted to take a European vacation each year, then the travel costs of that annual trip need to be baked into your retirement budget. During this process, it can be easy to feel overwhelmed. Ignore that sensation.

The fact that you are taking the time now to think about where you want to be in thirty to forty years sets you apart from other Millennials. Retirement as a concept needs a makeover. Setting up your goals now gives it the facelift it so desperately needs. Your commitment, your drive, and your dedication to reaching your vision of retirement will help reinvent what retirement means.

Building Your Retirement Accounts

Now that you know the basics of investing, defined retirement goals, and understand the importance of investing early, you need to know what types of accounts to invest in for retirement planning. There are different types of retirement accounts, but like you have been doing throughout the money makeover, you will concentrate on a few to produce maximum results. The following choices describe several different types of retirement accounts, each with pros and cons, which can set you up for long-term wealth and the retirement you deserve.

Roth Individual Retirement Account

For younger investors, beginning a conversation about retirement savings with the Roth individual retirement account (IRA) only seems fitting. If you are looking for a trusted and advantageous retirement account to get your feet wet in retirement investing, then this is the account for you. The Roth IRA receives a tremendous amount of praise for being the go-to account for younger investors because it offers wonderful long-term advantages.

For the tax year 2018, the IRS allows individuals to contribute up to $5,500 of post tax money into a Roth IRA. As you save for retirement, these contributions have the opportunity to grow tax-free. Better yet, you can invest your contributions in a wide variety of investment vehicles, such as stocks, bonds, ETFs, mutual funds, and more. This flexibility gives new investors the control to invest their money in a wide range of opportunities. Most young investors enjoy this freedom because they are just beginning to determine their risk tolerance.

Another advantage of the Roth IRA is that you are able to pull money out of your account (given certain criteria) without paying a penalty on the withdrawal. But I recommend never doing this. Your retirement accounts should not be used as a crutch for poor financial planning. That is why it is essential to establish an emergency fund and slush fund first—to protect yourself from the temptation to dip into your retirement accounts.

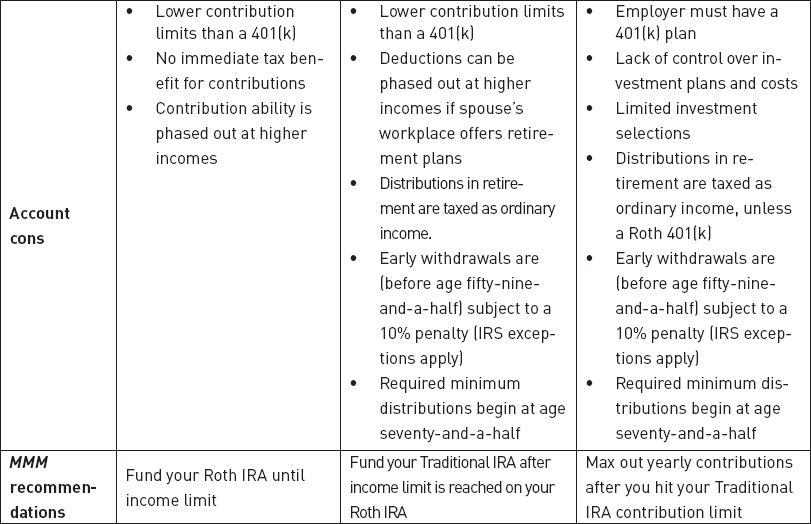

With all of its advantages, the Roth IRA does have some downsides. Once your income exceeds certain IRS limits, you are no longer allowed to contribute to this account. Another disadvantage is that your contributions are limited to $5,500 regardless of how much you want to defer to this account, which caps your capacity for growth. Finally, there is no immediate tax benefit for your contributions.

For retirement planning, you should continue to contribute to your Roth IRA as long as you are not phased out by the IRS income limits. Once you are no longer eligible to contribute to your Roth IRA, then you can move on to the second rung of individual retirement accounts, the Traditional IRA.

Traditional Individual Retirement Account

A conversation about retirement that disregards the Traditional IRA is not a conversation worth continuing. The Traditional IRA is one of the hardest working retirement accounts around. Among retirement aficionados, it is known for its long-term loyalty and continual devotion.

An amazing benefit of the Traditional IRA is the fact that your contributions to this account are never limited by your income or employment. An individual can set up this retirement account and start making contributions immediately.

As of 2018, the Traditional IRA has a contribution limit of $5,500 too. These contributions are also highly flexible and can be invested in a wide range of investment options, similar to the Roth IRA, which is a major advantage to many savers.

However, a major difference between the two retirement accounts is that the money contributed into your Traditional IRA is tax deductible. This means that there is an immediate tax advantage to contributing to this account.

The Traditional IRA does come with some strings attached. Not only do you face the annual contribution limit of $5,500, but you also could face an early withdrawal penalty if you take money out before you are fifty-nine-and-a-half years old. Once you reach retirement age and begin taking distributions, these distributions are taxed as ordinary income. Although you can enjoy the bounties of compounding interest, you are required to make minimum distributions beginning at seventy-and-a-half years old. Luckily, that is a long way off.

An important element to highlight is that the annual contribution limit of $5,500 is split between both of your individual retirement accounts, Roth and Traditional. That means if you contribute $5,500 to one, you cannot contribute to the other.

Once you have maxed out either of your individual retirement accounts, then it is time to move on to your workplace retirement accounts.

Traditional 401(k)

The Traditional 401(k) is my favorite retirement account, bar none.

If you are able to contribute to this account, then do so. The workplace retirement account is a terrific way to supplement your individual retirement accounts. Let's walk through some of the major advantages and disadvantages of the Traditional 401(k).

As the name implies, you can only contribute to a Traditional 401(k) plan if your employer offers this tax-advantaged option to retirement savings. As an added workplace benefit, some employers offer an employer-matching program, meaning that the employer will incentivize employees to save for their retirement by giving those savers matching contributions. The details of the program vary from company to company, but the matching program can act as a catalyst to your retirement savings.

If your employer does not offer a 401(k), I suggest consulting with the head of human resources. It is worth having the conversation to see what the company's plans are for the future. And if your employer is not going to offer a 401(k), then you should continue contributing to your individual retirement account until your employer does provide a 401(k).

Assuming your company has a 401(k) plan, one of the first items of business is determining how much of your income you want to allocate to your account. For the tax year 2018, the annual contribution limit for employees was $18,500.

The Traditional 401(k) is ideal for long-term savers because the account imposes a 10 percent penalty for withdrawing money from your 401(k) accounts before you are fifty-nine-and-a-half years old. This forces deferred consumption. Additionally, you are not required to take minimum distributions until you reach seventy-and-a-half years old. A disadvantage of this account is that because your employer creates the account, investment options are typically preselected, thereby limiting your options.

Regardless, you should do everything in your power to maximize your contributions and harness the power of compounding interest. You will also feel the benefits of the tax-deductible contributions once tax season rolls around. That means more money in your pocket!

After you have determined how much to save for retirement, automate the process because it will increase your yields. Just by setting up your accounts and maximizing your contributions you have beaten 99 percent of your peers. The rich life is on its way.

The bottom line is: By contributing to your individual and workplace retirement accounts, you are adopting a rich outlook. As a young investor, time is on your side in this process. You have the added advantage of watching your money grow for decades, which only expands good financial habits. Visualize your feet in the sand and the palm trees waving. Smile, because retirement is going to be a breeze.

Employer Match and Free Money

If your employer offers a 401(k) plan, then you are at a good company. If they offer a company match program, you are at a great company. Employer matching programs work when employees put aside a certain percentage of their income, say 5 percent, and the employer will make contributions to your 401(k) in the same amount. My favorite way to help people visualize this is by imagining your boss stopping by your desk every month and handing you a pile of cash simply because you put money into your 401(k) account. The match is a reward for saving and it offers a terrific return on investment.

With a little math, you can see that if you put in 5 percent, and your employer matches you dollar for dollar, you effectively save a total of 10 percent!

“Diligence is the mother of good fortune.”

—Miguel de Cervantes, Don Quixote

If you have reservations about saving with a 401(k), you should contribute up to your employer's match at a minimum. Otherwise, you are leaving free money on the table.

To effectively capture the unbelievable power of compounding interest, saving early, the employer match, and long-term planning, let's examine two saving scenarios.

Scenario 1: Compounding Colin works for Matching Monsters Inc., a factory for children's toys, earning a salary of $75,000. As part of a management training program, he has the option to contribute to a 401(k) plan with a 5 percent dollar-for-dollar match. Compounding Colin decides to contribute the annual IRS contribution limit of $18,500 and also enjoy the benefits of the company's matching program.

Scenario 2: Lazy Larry, Compounding Colin's manager, does quite well for himself and earns a six-figure salary of $150,000. He lives large and is not that concerned about retirement. As a result, he only contributes up to the company's matching percentage.

Let's see how the two savers perform after thirty years on the job in the chart on page 181.

Both savers have captured the power of compounding interest. However, Compounding Colin has dedicated himself to maxing out his 401(k) contributions, whereas Lazy Larry only took advantage of the company match. With time, the chasm between the two savers is gigantic. Although Lazy Larry may have been Compounding Colin's boss, it is safe to say that Compounding Colin saved like a boss.

Savings Gives You Freedom and Purpose

Mastering your finances will lead you to your true calling. Defeating debt has a tremendous effect on the psyche. Saving an emergency fund seems to numb the worries of daily financial issues. Building up a substantial retirement savings makes the future transparent. This mental peace grants you the ability to focus on your purpose in life.

Being financially fit will allow you to excel in your career. This fitness makes the risks of starting your own business or venture seem less daunting. Perhaps you already love what you do, and gunning for that promotion or making that next sales pitch seems a little easier when the risk of financial failure is removed from the picture.

Creating a life in which you don't have to worry about tomorrow allows you to seize new opportunities. This life allows you to accept projects or opportunities you previously could not afford.

Money points to tangible progress. Although you shouldn't be focused on money alone, recognizing that having money creates opportunity is key to financial progression. Allow yourself the security of no debt, cash savings, investments, and retirement savings, and suddenly chasing after your passions seems like a matter of necessity.

![]()

Action Items

Hopefully, this chapter has taught you at least two critical pieces of valuable information: Investing means you are winning, and time is on your side. The future is full of retirement millionaires; the question is whether you are going to be one of them. Investing early and often is the surest path to financial freedom.

When you are starting to accumulate your cash and investments, remember to follow these steps to grow your riches quickly.

- Understand that you are your own worst enemy.

- Build up your emergency and slush funds.

- Start investing early and let your seeds grow.

- Set your retirement goals and create your bridge to reach them.

- Allocate as much as you can to build the retirement you deserve.

Now that you have a clear vision of how to put your financial house in order, it is time to learn how to use technology to increase your chances of success. In the next chapter, you will learn about the rise of robo-advisors and why you should use them, develop an automated financial ecosystem that will optimize your financial growth, find the right money management approach, and understand the essential elements of the rich life.

When it comes to your money makeover, it is important to highlight that what you are investing in is less important than starting the process altogether. As Burton Malkiel, author of A Random Walk Down Wall Street, says, “Put time on your side. Start investing early and save regularly. Live modestly and don't touch the money that's been set aside.”11 Above all, have fun with picking your investments, and focus on long-term capital appreciation.

Technology is about to make this exponentially better.