On January 3, 1842, Charles Dickens and his wife, Catherine, left Liverpool on a 19-day Atlantic crossing to America. After a very cold and stormy winter steamship journey, at the Boston docking, Dickens was just two weeks shy of his 30th birthday. Dickens had already achieved fame and literary success with the 1836 serial publication of The Pickwick Papers, the 19th-century version of a 21st-century Internet streaming event. A ChristmasCarol was soon to be published in 1843.

The six-month American itinerary began with visits to Lowell MA, New York, and Philadelphia, followed by a journey to more than a dozen eastern-American cities, as far south as Richmond, as far west as St. Louis, and as far north as Quebec. Dickens provided a colorful, detailed travel-log of the six months in American Notes for General Circulation (Dickens1842).

A one-day train excursion to Lowell had been prearranged with business leaders of Lowell’s factory community. The city of Lowell had been founded a century earlier by Francis Cabot Lowell who sought a blank slate on which to build an entirely new approach to textile manufacturing. Lowell and his business partners had achieved success with the first American integrated textile mill in Waltham, MA. But with the integrated model’s success, prices were falling and demand increasing at a faster pace than could be satisfied. Scale was desperately needed. A large undeveloped site was soon discovered at the confluence of the Merrimack and Concord Rivers which was, conveniently, two miles down-river from the 36-foot drop of the Pawtucket Falls.

The geography was perfect for the construction of an elaborate array of canals, which, by the power of gravity, were fed from above the falls and which emptied below the falls. The costless water power, eliminated the dirt and soot of coal power, which had taken on increased importance as an energy source in England. Dickens wrote:

The very river that moves the machinery in the mills (for they are all worked by water power), seems to acquire a new character from the fresh buildings of bright red brick and painted wood among which it takes its course; and to be as light-headed, thoughtless, and brisk a young river, in its murmurings and tumblings, as one would desire to see. (Dicken 1842, Chapter 4)

With the construction of the canal network, massive financial capital was raised. Investors were intrigued with the entirely new manufacturing approach. The construction of a widespread complex of textile manufacturing facilities soon appeared, all while the technology of textile manufacturing, itself, was rapidly advancing.

While Dickens was clearly impressed by the young city’s “quaintness and oddity of character,” the massive manufacturing facilities, and the leading-edge technology, he was much more impressed with the novel use of human resources—“the mill girls.”

Dickens was very much aware of the hard work endured by the young women. With 12-hour days and 6-day weeks, the work was not easy. However, the mills provided, according to Dickens, a clean, comfortable environment with “much fresh air,” “conveniences for washing,” and windows with green plants to reduce the sun’s warming, greenhouse effect. Dickens described the young women as well-dressed, carrying themselves with pride and self-respect.

The living arrangements were also of interest to Dickens. The women lived in boarding houses provided by the business leaders. Dickens described the living arrangement and security as if a nineteenth century #me-too movement already protected the young women from threat and assault. Health care was provided in a novel arrangement with a hospital located some distance from the mills and boarding houses.

However, what was perhaps most intriguing to Dickens was the artistic and literary life of women factory workers. Dickens wrote:

I am now going to state three facts, which will startle a large class of readers on this [British] side of the Atlantic, very much. Firstly, there is a joint-stock piano in a great many of the boarding-houses. Secondly, nearly all these young ladies subscribe to circulating libraries. Thirdly, they have got up among themselves a periodical called The Lowell Offering, “A repository of original articles, written exclusively by females actively employed in the mills,”—which is duly printed, published, and sold; and whereof I brought away from Lowell four hundred good solid pages, which I have read from beginning to end. (Dickens 1842, Chapter 4)

After that thorough, careful reading, Dickens concluded: “putting entirely out of sight the fact of the articles having been written by these girls after the arduous labours of the day, that it will compare advantageously with a great many English Annuals” (Dickens 1842, Chapter 4).

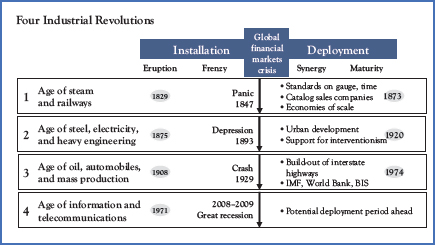

The story of Dickens’ journey to America and his one-day visit to Lowell highlights several important elements that have had enduring importance across each industrial revolution. The advances in technology and massive tangible capital investment requirements are apparent in the Lowell story and each industrial revolution. The story also highlights the role of falling prices, the appearance of rapidly increasing demand, the need for scale, the benefit of business model innovation, and the opportunity for new energy sources. However, Dickens’s writing also points to the critical role of human resources. The innovative notion of attracting bright, intelligent, young women to work in textile manufacturing, for a time at least, helped to meet the demand for labor. The truly creative aspect of the arrangement was to offer an arrangement that deeply engaged the women in their work, secured their living arrangement, and promoted their leisure. Worker engagement, good or bad, is an important element of each industrial revolution.

However, what a one-day visit misses is the dynamics of change as the technology matures, capital investment accumulates, and demand is satisfied. The story of industrial revolution is ultimately about the pressures and dislocation necessary to force migration from one era to another (see Table 3.1).

Table 3.1 Industrial revolutions eras

Source: Perez (2002), 78.

This chapter provides an overview of each industrial revolution from an economist’s perspective. Notwithstanding long-standing debates among economic historians about the nature of industrial revolutions, the aim here is to provide an economists’ view on what has been largely an economic historians’ discussion on whether these are “revolutions” or “evolutions” and what the necessary preconditions are.

The First Industrial Revolution: Creating the Factory System

As the First Industrial Revolution began, a series of inventions resulted in the appearance of the British factory system (Landes 1969). After a string of innovations, the factory system fundamentally altered business and work. Machines were substituted for human skill and effort. A new, more efficient energy source—steam—were created. And, new and abundant raw materials—wool, cotton, and iron ore—appeared. By the early 19th century, the installation period of the First Industrial Revolution had taken hold. Economic activity and knowledge were growing fast enough to create and support the needed capital investment and technological innovation.

While the first revolution began in England, it soon spread to Scotland, Wales, and Ireland, as well as North America, most notably New England. Per capita incomes were rising and the technology provided a means to substantially lower prices of goods for which there was elastic demand. As new technology and innovative business processes resulted in lower prices, the number of units sold grew more than proportionately. Revenue grew rapidly. Massive capital investments materialized in both Britain and New England. Light woolen and cotton textiles were provided to meet, first, domestic demand and soon global demand. The notion of workers and families having access to an expanding wardrobe, beyond everyday work clothes, was at the leading edge of technological change.

While water power was sufficient for early textile manufacturing, a more powerful and efficient source was required for the development of a productive iron industry, producing at scale. With abundant coal deposits in both England and North America, coal became the preferred energy source. After 20 years of development, from 1830 to 1850, the steam engine with coal as the energy source, provided sufficient power for a highly efficient iron industry. The coal–steam combination permitted, but did not cause, the development and diffusion of the First Industrial Revolution.

Like success of the coal–steam combination, the advent of the rail network in England and across Europe and North America further aided the development and diffusion of the first revolution. With prices of goods falling and access to larger rail-provided markets, economies of scale in production improved the economics of production for a much broader array of businesses, employing a much larger labor force. The rail network also altered the competitive landscape as entrepreneurs had a wider choice of locations from which to operate and sell product.

However, as the installation period of the First Industrial Revolution progressed, business leaders and workers resisted. Despite the benefits of the new technology and the growth in demand for their products, resistance was strong. As Landes writes, “only the strongest incentives could have persuaded entrepreneurs to undertake and accept these changes; and only major advantages could have overcome the dogged resistance of labor to the very principle of mechanization” (Landes 1969, 43). However, entrepreneurs soon discovered that with rising demand, marginal costs were rising as well. The inadequacy of the legacy technology created pressure for improvement. It didn’t take long for entrepreneurs to learn that the reduction in cost resulting from the new system would sufficiently cover the expense of the needed investment in the new capital and technology. Despite the powerful business case of growth and expansion, entrepreneurs now faced a new risk environment. Where previously, manufacturing costs consisted primarily of labor and materials, financed from current period cash flow, now fixed costs in the form of capital investment appeared. Fixed costs were a new source of entrepreneurial risk. With new long-term debt necessary, judgments were required about business profitability years in advance.

For workers, the new business model—the factory system—meant a separation of work from the means of production. The worker no longer had to be both entrepreneur and worker. The small, artisanal enterprise could be replaced, should the worker choose, with a week’s work with defined hours, pay, and responsibilities. The worker could leave the pressures of building and managing a business to someone else. The trade-off was that the factory system imposed a new form of discipline under the watchful eye of the factory overseer (See Crafts and Mills 2002a and 2002b).

While data are limited, Landes estimates that by 1830 there were “hundreds of thousands of men, women, and children employed” in the British factory system (Landes 1969, 114). Importantly, factory production created new tasks and new opportunities for workers and businesses that had not previously existed. Machine building and maintenance were newly and frequently subcontracted to those with specialized skills. Completely new occupations were created. Increased capital investment, employment growth, and the appearance of new tasks and new businesses, all contributed to substantial macroeconomic benefits as income and wealth grew rapidly.

As we saw in the previous chapter, the need for massive capital investment for both the factory system and the railroads not only led to the attraction of massive financial capital but soon to a frenzy in the financial markets. The prospects of future profits became, for the first time, an opportunity for third-party investors who hoped for substantial capital gains and income growth.1 Not surprisingly, enterprise values became disconnected from reality. However, after the 1857 London financial markets correction, battered investors were more informed and better prepared to fund activities by entrepreneurs with a shared view of future opportunities. With financial capital available and resistance to change and transformation overcome, the now GPT was available to support creative destruction in the decades ahead.

Thus, the deployment period of the First Industrial Revolution, from 1850 to 1873, was a period of unprecedented growth with incomes across the United Kingdom, United States, and Europe rising rapidly. As would be expected in a deployment period, these were also years of technological maturity. The technologies first developed in Britain, and later in the United States, spread across Europe and North America. The third quarter of the 19th century was a period of sustained creativity and important innovation.

Institutional change was especially important. With knowledge diffusion and the absorptive capacity of those receiving the newly emerging technological expertise increasingly important, easier conditions for company formation was a critical change in the rules of business governance and management. Britain was the first nation to permit the right to limited liability formation by simple registration (Landes 1969, 198). Despite an initial fear of unlimited speculation, concerns were soon overcome and the true limited liability partnership become available across much of Europe. Other changes such as the end of the prohibition of usury, the creation of transactions executed by bank check, the easing of penalties for debt and bankruptcy, and the amendment of patent laws to allow for trademarks and other intangible forms for business property, all eased the adoption of the new technology and new business models. As is characteristic of deployment periods, not only did the mature technology spread widely and tangible and intangible capital investment accelerate but also the rules of the game changed among businesses, governments, and families.

Importantly, the first revolution’s deployment period brought improvements in transportation, increased availability of new energy sources and raw materials, and increased access to financial capital. The deployment period also brought a creative entrepreneurial response to the long-run opportunity and to the short-run improved facilitation of business creation, knowledge diffusion, and tangible and intangible capital investment.

Unlike the installation period when British firms dominated markets and technology, in the deployment period, a much broader set of competitors emerged—both across Europe and the United States. Not surprisingly, across Europe, barriers to international trade fell with riverway levies lower, exchange rates simplified, and a series of treaties between nations signed. The United States was endowed with abundant land and natural resources, which caused labor scarcity but resulted in capital complementary (see Habakkuk 1962 and Broadberry 1997). By the 1870s, all nations saw their exports grow. With the added competition, home industries did not collapse but grew stronger as marginally inefficient firms disappeared with business reallocated to more efficient firms.

By 1870, Landes observes, “British industry had exhausted the gains implicit in the original cluster of innovations that had constituted the Industrial Revolution … Not until a series of major advances opened new areas of investment around the turn of the [twentieth] century was this deceleration reversed” (Landes 1969, 234–235). Importantly, demand failed to keep up with very rapidly growing industry capacity. Excess capacity substantially reduced the need for further capital investment. With a growing array of suppliers, demand was easily met. New customers with unmet needs were much harder to find. Landes writes:

There were customers for those who knew how to find them; but one had to look for them in new places and woo them in new ways. And the task was not so easy as it had been for the pioneer industrialists of the first half of the century. (Landes 1969, p. 237)

The First Industrial Revolution had exhausted its opportunity and its deployment period was coming to an end.

The Second Industrial Revolution: Electric Power Creates Expansion

As the Second Industrial Revolution began, the legacy of the First Industrial Revolution hung over it. The success of the preceding period had put in place what was, by the last quarter of the 19th century, an aging technology embedded in an aging and excessive capital stock governed by business rules and practices from the earlier era. However, the deployment period of the previous era had also created great wealth. The resulting golden age has been called La Belle Époque when Europe achieved its greatest power in global politics, and exerted its maximum global influence.2 The epic coincided with the installation period of the Second Industrial Revolution. Not surprisingly, income and wealth protection became important motivators in resisting change.

Slower growth in capital investment along with continued income growth and wealth accumulation is characteristic of the installation period. The stock of capital put in place in the prior era is sufficiently large that it continues to generate income and wealth even as growth is slowing. Despite the capital investment slowdown, as the name implies, the installation period is one in which new technology is installed, initially on an experimental basis with immature applications. The development of the new technology is setting the stage for the possibility of growth in a future period.

Advances realized in the early adoption of electricity were at the heart of the installation period of the Second Industrial Revolution. The advent of electric power permitted the birth of electric motors, organic chemistry and synthetics, the internal-combustion engine, automotive equipment, precision manufacturing, and assembly (Landes 1969, 235). These advances made possible an entirely new set of consumer goods—the sewing machine, inexpensive clocks, the bicycle, electric lighting, and electric appliances. Robert Gordon describes, at length, the impact that these innovations had on consumers and families. Gordon explores the increase in living standards and welfare as a result of water and sewer service, indoor bathrooms, central heating, lighting, and early appliances (Gordon 2016, Chapter 4).

The new technology, and the products it spawned, altered the demand for capital investment significantly. Where the First Industrial Revolution was one in which investment surged primarily for capital goods, most notably for textile equipment, metals production, and railways, the Second Industrial Revolution created demand for capital investment for consumer goods. The demand shift and the new technology suggests that as the installation period of the Second Industrial Revolution progressed, and consumer goods production at scale was possible, the existing capital infrastructure was antiquated and poorly suited for the decades ahead. Entering the installation period of the Second Industrial Revolution, capital infrastructure would have to be renewed to meet the needs of the new consumer.

The technological innovation of the Second Industrial Revolution has been well documented by Paul David, including the “war of the currents” between Thomas Edison and George Westinghouse in establishing alternating current as the industry standard, building the electrical power network, and setting global standards (see David 1990 and 1998). In addition, Nordhaus (1997) details, in a well-known paper, lighting innovations over millennia. Among the many innovations that have reduced the price of lighting by many orders of magnitude, the development of electric power and the carbon-filament lamp were among the most important.

By the third quarter of the 19th century, the new technologies were beginning to have a broader social, as well as economic, impact. While it was very beneficial to workers and families to have the access to an expanded and affordable wardrobe that inexpensive textiles provided in the First Industrial Revolution, electric power technology had a much broader and more consequential impact.

The broad social and economic benefits that the advent of electric power brought can be seen in the Swiss experience. In recent work, Brey (2021) has provided new insight at the outset of the installation period of the Second Industrial Revolution.3

Switzerland was early to adopt electric power in the late 19th century. Because the generation of electric power relied exclusively on locally available waterpower, the initial ability to adopt electricity depended on unique geographic features, randomly distributed across the nation. In addition, waterpower was unexploitable with earlier power technologies. In effect, waterpower suddenly appeared and was spread randomly across Swiss regions for a 20-year period. Thus, a natural experiment was created.

Brey finds that industries associated with the provision of electricity provided a meaningful boost to industrialization in the 1860–1880 period, as well as a positive effect on economic development over the long run. The reason for stronger economic performance, Brey finds, is that the early electric power exposure triggered the accumulation of human capital and further innovation, leading to persistent divergence in economic development. Local schoolchildren immediately experienced an improvement in educational outcomes with (1) the student population expanding more rapidly in areas adopting electricity earlier, (2) employers and local governments providing apprenticeships and technical schools, and (3) increased support in national referendums for education investment. Those early adopting areas today remain innovative with a higher patenting rate.

As the Swiss deployment of electric power suggests, deep business and social innovation followed the Second Industrial Revolution’s technological innovation. One important innovation, as documented by Alfred Chandler is the creation of the modern industrial enterprise in the deployment period of the Second Industrial Revolution. As expected, the 1893–1920 deployment period is a time in which the power of creative destruction fundamentally altered the organization of business and work. Chandler finds that those business leaders who were able to fully exploit the potential of the then-new electric power technology made investments large enough to develop “competitive capabilities that permitted their enterprises and their nations’ industries to dominate markets abroad as well as at home” (Chandler 1998, 432).4 Chandler argues that exploitation of the new technology resulted in the creation of the modern industrial enterprise, citing investment in (1) production large enough to generate economies of scale and scope that the new technology had potential to deliver, (2) marketing and distribution capabilities large enough to sell products in the volume produced, and (3) managerial skill and structure to manage, coordinate, and allocate resources for future production and distribution.

Not only did such enterprises appear suddenly in the last quarter of the 19th century, Chandler writes, but they also clustered in industries with common characteristics. These industry-leading enterprises were found in food, chemicals, oil, primary metals, electrical machinery, and transportation equipment. They were produced in volume and in a capital-intensive environment. And, they were located principally in Britain, Germany, and the United States. Notable clusters appeared in cigarettes, tires, newsprint, plate and flat glass, razor blades, and mass-produced cameras. In today’s lexicon, such enterprises are called “superstar firms” (see Autor et al. 2020). Chandler observes that high-volume electric power generation in the 1880s resulted in massive capital investment and created needs and opportunities for technological and organization innovation across many industries.

Beyond the “superstar firms,” described by Chandler, the very slowly changing behavior of the nonsuperstar firms—those with lagging innovation, diminished competitiveness, and lack of technological intensity—arose from deeply rooted cultural barriers. Lazonick (1998) argues that after the deployment of the electric power network, some British industrialists were challenged to develop the organizational capabilities that Chandler had observed elsewhere. These British business leaders, like craft workers, jealously guarded the status quo.

In addition to the absence of adaptive British leadership skills, Lazonick highlights barriers that proved difficult to overcome—the durability of then-existing plant and equipment, the immobility of workers, a lack of understanding of the new science and technology, the embedded class structure making it difficult for senior leaders to gain commitment and coordination of technical specialists, and the failure to restructure the education system to marry science and technology.

For previously successful business leaders of the earlier period, Lazonick asserts, “the strategy of living off his industrial capital was rational.” The required dramatic transformation of the social determinants of technological progress was beyond the lived experience. As the Second Industrial Revolution began, fixed costs—and thus risk—were limited, inputs were readily available, outputs were sold in a known marketplace, and competition was nearby and well understood.

With success as an individual business, not as a “modern industrial corporation” with the beginnings of global reach, Lazonick (1998) and Landes (1969) point to a changed strategic and operating model. Lazonick writes the British business leaders’ “estimates of returns were conservative because [their] organized competitors had the power to shape their economic environment in ways that [the British leader], as an individual proprietor, could not.”

In contrast to the British experience, as the Second Industrial Revolution began, Germany was well positioned to prosper. During the first three-quarters of the 19th century, Germany addressed transportation, communication, and political barriers across a collection of independent and sovereign territories, allowing for commercial and financial success and a strengthening of institutional rules and practices. In addition, Tilly and Kopsidis find that increased literacy, school enrollment, and patent activity contributed to Germany’s “take-off.” In addition, they observe that the high literacy rates also contributed to the spread of new technical knowledge and high numbers of skilled craftsmen (Tilly and Kopsidis, 2020, 142–143).5 By the last quarter of the 19th century, Germany emerged as an industrial power (Tilly and Kopsidis, 2020, 165). The railway boom created important points of linkage between heavy industry and mechanical engineering allowing for information exchange and knowledge spillover as the new technology was adopted. Aided by the abundant supply of literate and skilled workers, the close relationship between science and industry resulted in substantial research and development activity in pigments and dyestuff, forming an important link in the chain of chemical processes for textiles, leather, plastic, paper, packaging, printing inks, paints and polymers, and so on. As a result, over the Second Industrial Revolution’s deployment period, production of pharmaceuticals, synthetic fertilizers, and other heavy chemical products expanded rapidly. In addition, building on the newly available electric power technology, industry giants such as Siemens and AEG emerged in the nascent electrical engineering industry (Tilly and Kopsidis, 2020, 175).

Consequently, a regime shift occurred with American, Swiss, and German businesses taking the lead. Landes asserts that “the rapid industrial expansion of a unified Germany was the most important development of the half century that preceded the First World War” (Landes 1969, 326). The new innovative and competitive landscape included global competition, the power of corporate enterprises, research and development of new productive resources, the interaction of organization and technology, the required human resources, and the commitment of financial resources. British business leaders were challenged to adapt. As industrial leadership passed from Britain to Germany in the closing decades of the 19th century, Germany’s gains, according to Landes, were social and institutional. Britain, Landes writes, “basked complacently in the sunset of economic hegemony.” Family firm ownership was passed down to generations with less skill, knowledge, and interest. Reflecting amateurism and complacency, corporate enterprises recruited inexperienced leaders and promoted leaders out of production roles ill prepared for larger challenges. German entrepreneurs, by contrast, were trained in science and the new technology, worked hard, and were astute financial managers. While older British enterprises were complacent, younger firms failed to appear in larger enough numbers in the new industries of electrical engineering and organic chemistry (Landes 1969, 336–338).

The early decades of the 20th century, as expected in the deployment phase, brought broad advances that indicated approaching maturity. Basic innovations spread from small groups of “superstar firms” to the balance of the business sector with electric power used widely. While new uses and less expensive power promoted capital formation, the importance of intangible capital cannot be overemphasized. Scientific knowledge, technical skill, and high standards of performance weighted heavily. Nonetheless, aggressive capital investment in both Britain and Germany eventually resulted in capacity outstripping demand. With the technology maturing, capacity in surplus, and the world at war, the Second Industrial Revolution came to an end.

The Third Industrial Revolution: War and Depression Ignites Growth

As the Third Industrial Revolution began, the global economy faced unprecedented problems and challenges. The 20th century had already brought a world war and a simultaneous global pandemic, both resulting in extraordinary death and destruction. The installation period of the Third Industrial Revolution has become more commonly known as the interwar years, as it was bookended by a world war and a pandemic juxtaposed to a second world war and a global depression. As the era began, early in the 20th century, the United States was assuming global economic leadership after a period of strong growth and success in the Second Industrial Revolution.

The First World War hastened the dissolution of the international economic order of the prior revolutionary period. Britain ended free and open trade with the institution of a 33⅓ percent tariff on trading partners, except those in the empire; the monetary stability of the prior century disappeared; and global inflation resulted from emergency conditions, market quotas, and rationing. After the war, German inflation was especially severe with the Allied nations imposing burdens of reconstruction that were extracted a very high price (Landes 1969, 357–364).

With the hangover from the preceding deployment era and consequences of the global financial impact of the war’s conclusion, the Third Industrial Revolution’s installation period not only suffered from global inflation but also weak employment growth. In today’s language, it was a period of stagflation. Despite constraints imposed on European nations with the liquidation of financial assets held abroad to pay for the war, opportunities in the energy and automotive industries began to appear with mass production emerging as an entirely new production model. German and U.S. capital investment was growing rapidly.

By the early 20th century, as series of automotive design and mechanical improvements created a more useful and usable vehicle, opening the possibility of mass production. Steering improved; engines were larger; and spark plugs, carburetors, transmissions, and starters all made automobiles more reliable and convenient. These innovations expanded the market with greater consumer interest in an easier-to-use vehicle. Consequently, production at scale became an important opportunity. Henry Ford and others soon began the development of the internal-combustion engine and the mass production of automobiles. Other industries also adopted the same assembly and production model (Gordon 2016, 150). As a means of travel, auto travel began to replace walking, mass transit, and horse-drawn wagons. Aircraft manufacturing and airplane travel also gained traction as the installment period progressed. While remaining very immature, initial attempts were made to make air travel economic.

Not only did transportation begin to improve but communications became more widely available. By 1919, rotary dial telephones and automatic switches were introduced into service (Gordon 2016, 183). Radio technology also gained, in part as a result of the war and in part as a result of the invention of the vacuum tube. The tube’s innovation made possible not only the radio but also radar, recording devices, the computer, automated control systems, and television (Landes 1969, 425).

Consumers also benefited as families were no longer limited to purchasing from small local stores. The A&P grocery chain began its period of most rapid expansion in 1912. The Kroger and Grand Union chains soon followed. Volume purchases by the chains allowed them to pass on lower prices to consumers, creating a meaningful threat to small independent merchants. Urban, general merchandise department stores soon followed (Gordon 2016, 78–90).

In the Third Industrial Revolution’s installation period, as expected, new technology—internal-combustion engine, telephone systems, vacuum tubes—appeared but with slow adoption, outdated business models, and technologically lagging enterprises. Landes summarizes the pressures to transform as the installment period progressed:

It was the more progressive, more innovative branches that grew fastest and drew redundant labour from lagging sectors. For another, this movement of workers conduced to higher wages for those who remained, so that it paid to substitute capital for labor. The result was a stimulus to technological improvement in these lagging sectors, which in turn hastened the purge of inefficient enterprises and the process of reallocation. Prosperity may be the best friend of progress, only because new investment usually entails new and better ways of doing things. (Landes 1969, 420–421)

The coming of the new technology spawned rapid investment in UK, Germany, and U.S. tangible and intangible capital. Along with a massive flow of funds into the equity shares, frantic speculation on share exchanges was the eventual result. By late 1928 and early 1929, American banks began calling their European loans. When the net export of capital plunged, European banks came under great pressure. A rapid fall in the price of industrial equity shares, quickly set off market reaction with equity values crashing. In the scramble for cash, loans and debts were recalled. The lack of capital quickly resulted in a business collapse and rising unemployment. The Great Recession had begun and the installation period of the Third Industrial Revolution came to an end.

The Great Depression, as is well known, was a global event. However, Germany was affected as much or more than any national economy. With high inflation and onerous war retribution payments extracted by the allied nations, depressed business conditions, and massive unemployment created polarization between an extreme left and an extreme right. With the coming of the National Socialist party, irrational beliefs and rise of Hitler’s government, by 1939–1940, preparation for war was complete.

The death and destruction resulting from the second world war created an enormous hole in Europe’s private and public physical capital infrastructure. In the United States, the impact of the war was very different. No measurable military action occurred on the U.S. mainland and no capital was destroyed. Instead, the U.S. economy was converted to a war-time footing and economic activity and business processes were widely employed to produce military output. As a result, when the war concluded, U.S. and European businesses were left with a decision to return to the prewar technology and business processes or to replace their military production with the then more modern, current technology. Similarly, the workforce was fundamentally transformed as well. Those serving in the military learned new skills and a new way of life while those not joining military service—most often women—joined the workforce for the first time and also gained new skills and experience.

The shock of the Great Depression cleansed nonperforming assets—both equity and debt—from investor’s balance sheets and freed capital for more productive use. The reallocation of labor and capital from inefficient and lagging firms, the business sector dislocation created by the Second World War, and the transformation of the workforce as a result of military and wartime activity, all combined to set the stage for very strong economic growth and more equally distributed incomes in the period immediately ahead. A very painful 15 years, experienced worldwide, was about to pay-off with 30 years of prosperity.

In understanding the means by which the benefits of the deployment period of the Third Industrial Revolution appeared, Landes cites four “prime moves” and enduring factors: an increase in technical and scientific knowledge, a new spirit of international cooperation, an increase in economic knowledge (by which he seems to mean improved business leadership and more skilled public policy making), and a postwar commitment to change and growth (Landes 1969, 536).

Growing out of innovation of the technology initially employed in radio, television, and radar devices, computing machines became a reality. Despite their initially primitive nature and lack of electronic componentry, basic business functions were eventually performed at scale by early computers. In the later portion of the deployment period electronic components became a reality, setting the stage for the GPT of the Fourth Industrial Revolution.

Similarly, the chemical industry built on its advances of the installation period created artificial fibers, leather substitutes, plastics, protective coatings, new drugs, and nylon, the first all-synthetic fiber. Other industries brought products to market such as in optics, photography, xerography, light metals, and nuclear power (Landes 1969, 514–517).

Consequently, a question subject to debate for many years surrounds the possible link between the cognitive acceleration in the Third Industrial Revolution’s installation period and economic growth experienced in the deployment period. While Landes’s work occurred too early in the era to expect an answer, with the benefit of 50 additional years of data, Gordon follows Landes in exploring the same question. In Gordon’s view, there are several elements that explain the strong growth in the 1950s and 1960s:

• The Second World War created an “economic rescue” along every conceivable dimension from education and the GI Bill to the deficit-financed mountain of household saving that gave a new middle class the ability to purchase the consumer durables that had been unavailable during the war.

• On the supply side, the U.S. government paid for vast expansion of the capital stock for new factories and equipment that were then operated by private firms to create aircraft, ships, and weapons.

• The surge in infrastructure investment in the 1930s and 1940s, related to depression recovery programs and the Second World War, provided for more efficient movement of people, goods, and power. These projects included, for example, building the nation’s highway system, the Golden Gate Bridge, the Bay Bridge, the Tennessee Valley Authority, and the Hoover Dam.

• Finally, another supply channel Gordon cites is “learning by doing.” As a result of supply constraints imposed by the war effort in 1942 to 1945, each firm found it necessary to devise new techniques to boost output while constrained by limited capital and labor resources (Gordon 2016, 535–565).

Landes writes that the greatest change of all was a “revolution in expectations and values.” The revolution created a return to “the high hopes of the dawn of industrialization, to the buoyant optimism of those first generations of English innovators” (Landes 1969, 536).

The strong growth of the 1950s and 1960s eventually gave way to the 1970s slower growth, bringing the Third Industrial Revolution to an end. By the late 1960s, demand exceeded available capacity with U.S. imports growing rapidly, demand that domestic producers were unable to address. When combined with a series of policy errors by the Nixon Administration and the Federal Reserve, historically high inflation resulted with slower growth following.

Perhaps the best illustration of the early 1970s inflection point is the 1971 pressure on the Nixon Administration to the address of the value of the dollar, exchange rates, and the gold standard. After the protectionism of the 1930s, the world’s finance leaders agreed at the 1944 Bretton Woods conference to fix the value of one ounce of gold at $35. Other currencies were fixed to the dollar within a trading band. Any government or central bank could redeem their dollars by going to the gold window at the U.S. Treasury. For 25 years, the dollar stood at the center of an institutional arrangement that was an important contributor to robust U.S. economic growth and the astounding recovery in Europe and Japan. However, the arrangement was under severe pressure as the Third Industrial Revolution was about to come to an end. Indeed, by 1971 the U.S. Treasury was short of gold, putting at risk the role of the dollar.6 With the dollar, as the world’s global currency and the need for much of the world to hold dollars, the United States benefited with lower interest rates and ready access to capital for financing government spending. Jeffery Garten tells the story of this policy inflection point in some detail (Garten 2021).

While most crises seem to appear out of nowhere, rapidly rising inflation and a growing trade deficit—both at least partially linked to the overexpansion of capital investment—had created a series of currency crises leading up to 1971. A stable dollar was at risk. Despite a series of global finance leader summits convened to save the post-World War II currency arrangement, by mid-1972, floating exchange rates had become the norm. Each industrial revolution gets to define its own set of rules, practices, and arrangements. The next and Fourth Industrial Revolution was about to get its chance.

Beyond the high and rising inflation, capacity limitations, and the crumpling institutional arrangements, the era’s technology developed in the 1920s and 1930s reached maturity, having been fully exploited for nearly five decades. The result was a need to turn the page. Like earlier revolutionary periods, the move to a new era, initially, had to come to grips with the legacy of the concluding era and, at the same time, find new technologies to support future growth.

The Fourth Industrial Revolution: Resistance and Computing

The beginning of the Fourth Industrial Revolution coincided with the invention of the microprocessor. In 1974, Intel introduced the 8080, called a “computer on a chip.” However, it was more than 20 years before Intel and others achieved sufficient scale for the microprocessor to have a measurable impact on growth.

The legacy of the Third Industrial Revolution’s deployment period hung over the installation period of the Fourth Industrial Revolution for a considerable period. The inflation of the late 1960s and early 1970s continued and worsened throughout the entire decade of the 1970s. As is well known, it was not until Paul Volcker was appointed as Chair of the Federal Reserve Board in 1979, that monetary policy succeeded in addressing the worsening inflation problem. Under Volcker’s leadership, the Fed fundamentally transformed the execution of monetary policy, and imposed extremely tight financial conditions on global financial markets that inflation began to lessen. Nearly six years was required to achieve the Fed’s inflation goals. Ironically, in creating the new monetary policy arrangement, it was also Paul Volcker who, a decade earlier, had played a critical analytical and support role as the Nixon Administration came to grips with the collapsing global institutional currency arrangement.

The increased use of fossil fuels, and oil in particular, was also a legacy of the Third Industrial Revolution. Consequently, the installation period of the Fourth Industrial Revolution was a period of extreme oil price volatility as demand surged and energy investment responded to changing price signals. The West Texas Intermediate (WTI) oil price rose from $22.39 in June 1973 to $134.22 in May 1980, a more than six-time increase in just nine months, before wiping out the enter gain, falling back over 18 years to $20.44 in December 1998. The WTI price rose again, over 20 years, to $177.80 in June 2008 but fell to $48.07 in February 2020, nearly 12 years later. Much of the world, of course, was very dependent on the Middle Eastern nations, Russia, and other oil-producing nations for their energy supply. The dependency heavily influenced geopolitical, diplomatic, and military considerations, resulting in significant armed conflict and strained global relationships. However, by the period’s end, energy exploration and production capabilities had advanced sufficiently, with the help of considerable advancement in electronics technology, that fracking methods allowed the United States to achieve energy independence and lessen oil supplies as a source of global tensions.

While the legacy of Third Industrial Revolution was hanging over the 1970s and 1980s, the technology of the Fourth Industrial Revolution began to take off. Initially, led by IBM, Digital Equipment Corporation, and others, large computing systems became increasingly powerful and were used to automate basic business tasks, such as finance, human resources, and inventory management. However, with Intel’s microprocessor, the personal computer became a reality with Apple and IBM at the forefront. As Nordhaus (2021) has shown, the cost of computing continued to fall rapidly.

It turned out that microprocessors also permitted advances in other computer hardware, such as servers, expanding the range of software functionality to databases, mail, printing, web services, and games. With computing costs falling and functionality growing, by the late 1980s and early 1990s, tasks were partitioned among various servers. And by the early 1990s, Intel had learned how to move its technology from generation-to-generation, using pricing to make each generation attractive to users, and profitable for Intel, while holding competitors at bay. By the late 1990s, the combined impact of the technology and the market strategy was effective enough to see measurable productivity gains in the economic statistics.7

While Intel’s success on the supply side was making semiconductor technology and its business model viable, advances in optical networking, and client–server as well as the design of the World Wide Web and the creation of the web browser made the Internet a viable platform for business activity. As would be expected in an industrial revolution, a frenzy emerged—the dot.com bubble—in which an uncountable number of businesses were launched attempting to deploy the novel technology. However, in the absence of new, innovative business models, most failed to exploit the new technology with significant financial capital destroyed. The 2001 recession and equity market collapse were required to clean up the mess.

It was not until the 2007 launch of Apple’s iPhone combined with the creation of Google, Facebook, and Amazon, along with Microsoft’s focus on the Internet browser, that the required technology and business models began to align. With many other entrepreneurs learning from these early, successful ventures, both e-commerce and advertising-supported services grew rapidly with mobile devices and Internet service providing a convenient and workable infrastructure. With investors seeking to protect wealth and grow income, a wide array of complex financial instruments, most notable in the housing and mortgage lending sector, were created in the first half of the 2000s decade. However, the widespread failure of such instruments and the subsequent 2008–2009 financial market crash cleansed balance sheets and prepared investors for the technology-driven growth that has followed.

While it’s much too soon in the course of economic history to make a definitive declaration, the 1990s dot.com bubble and the 2008–2009 Great Recession appears to have marked the end of the Fourth Industrial Revolution’s installation period and the possible beginning of the deployment period. However, the weak, disappointing, and stuttering growth during the decade between the Great Recession and the global pandemic demonstrates the difficulty in launching more rapid growth. With robust economic growth, productivity growth, and capital investment spending having failed to emerge, uncertainty remains. But the increasing adoption of the new technology, by consumers, workers, businesses, and governments, and the increasing digital intensity of economic activity generally suggests a corner might have been turned.

Four Industrial Revolutions: Parallels, But No Repetition

As the story of Charles Dickens visit to America suggests, there are parallels across each period. Harberger’s “mushrooms” appear in each era’s early period when a wide range of technological applications spring forth. While the legacy of the prior era hangs heavily over the early years, even decades, resistance to change is substantial and protection of income and wealth by those who were the prior eras’ winners is strong. Time is required for the previous eras’ capital to age and depreciate when the prior era’s technology is exhausted. Failure is also necessary as entrepreneurs learn, from trial and error, and the process of creative destruction reveals which new business models will succeed.

After a global recession and financial market crash cleans up the mess that’s been created, Harberger’s “yeast” appears. The new technology and new business models begin to slowly take hold. But overcoming the resistance to change is critical and, as history suggests, is never easy. Creative destruction requires knowledge diffusion and the ability of lagging firms to absorb the new technology with new business models by deeply transforming their businesses. Likewise, governments and households need to transform their activities. If successful, tangible and intangible investment becomes more robust, as new capital replaces old capital. With the combined new technology and new business models, the result is massive transformation of how work gets done and lives are lived. With new capital investment, economic and productivity growth strengthens. But the issue is what causes businesses, households, and governments to take the risk and discard old ways and adopt new ones.

1 Landes describes the widening available of bank credit and services as well as the rise of joint-stock commercial banks. See Landes (1969), pp. 206–210.

2 (See Wikipedia: Belle Époque https://en.wikipedia.org/wiki/Belle_%C3%89 poque).

3 Brey finds persistent differences across the Swiss regions with early access to electric power, not because of the manner in which electricity is used but as a result of increased human capital accumulation and innovation. Brey had access to Swiss data covering the period from 1860 to 2011, so is able to consider both the installation of the technology in the late 1800s and the long-run consequences. Importantly, the installation of electric power generation was unique in Switzerland and had the effect of creating a random control experiment from which Brey can draw conclusions about causality.

4 Harberger (1998) developed the notion of “yeasty” growth during the same period Chandler (1998) was documenting the “modern industrial enterprise.” Both captured the essence of the deployment period. Chandler provided an empirical view of an important new turn-of-the-century business model, while Harberger articulated a theoretical notion of more rapid deployment period growth following innovation and transformation.

5 Similarly, Gordon finds that by the last quarter of the 19th century education practices in the United States were comparable to those of the “major relatively rich European nations.” Gordon writes: “Native-born Americans were largely literate by 1870, and the remaining cases of illiteracy involved immigrants to the northern states or former black slaves in the south” (Gordon 2016, p. 58).

6 By 1971, gold had been draining from the U.S. Treasury for many years. In 1955, the United States had $2.7 billion of gold at $35 per ounce to cover the $13.5 billion of liabilities to other governments and central banks, 60 percent more than required. By mid-1971, the U.S. stock of gold had increased to $10.2 billion with official dollar holdings by foreign governments exploding to $40 billion. To make good on its commitment to exchange gold for dollars, the United States had only 25 percent of what would be needed (Garten 2021, p. 9–10).

7 Notwithstanding the technology advances of the 1990 to 2022 period, Strauss and Howe (1997) provided a prescient view of the challenges to be encountered in the generation ahead.