Like anything in life, to gain an appreciation of how we got to where we are, it's helpful to understand the background and history of how it all started. To some people, blockchains and cryptocurrency are just a technology fad, but to the dedicated few, this is a movement of epic proportions, centered around trust and the decentralization of it.

Understanding some of the fundamental concepts of this technology will help to enable all of us to see the potential revolution that blockchains, the wider concept of distributed ledger technologies, smart contracts, and tokens will bring.

In this chapter, we will go back in time and look at:

- Bitcoin: In the beginning

- Altcoins: The alternative to bitcoin

- Blockchains: The immutable database

- Smart contracts: Are they that smart?

- ICOs: The peak of ICOs in 2017

Since bitcoin appeared on the scene in 2009, it has had its fair share of drama. It has become the "crypto gold standard" that everything is measured against, but very quickly, alternative coins were created to copy bitcoin's success. Next came the blockchain era, where everything was being placed on the blockchain.

Smart contracts then became the "in" thing a few years later and that allowed software programs to be created and live on the blockchain. A year later, smart contracts spawned an era of decentralized applications, also known as dApps, on a popular platform called Ethereum. In amongst all of this, tokens were created and a new age of funding was born. Let's dig a little deeper into this by starting at the beginning.

Money has not had a major innovative disruption in at least several decades, but there have been many attempts in the past, such as DigiCash (Chaum, 1989), e-gold (Jackson and Downey, 1996), B-money (Dai, 1997), bit gold (Szabo, 1998), and Liberty Dollar (von NotHaus, 1998). It wasn't until the invention of bitcoin that a disruption really started to show, but why did these previous attempts fail?

One of the biggest challenges in creating a cryptocurrency is the double-spend problem. This is where the same digital currency is spent twice because it can be easily copied in the digital realm. In fact, it can be spent many times over.

In 1982, David Chaum, an American computer scientist and cryptographer, published a paper on his idea of Blind Signatures for Untraceable Payments (http://www.hit.bme.hu/~buttyan/courses/BMEVIHIM219/2009/Chaum.BlindSigForPayment.1982.PDF). Then, in 1988, he co-authored a paper on Untraceable Electronic Cash (http://blog.koehntopp.de/uploads/chaum_fiat_naor_ecash.pdf). The concept here was a method of solving the double-spend problem by revealing or exposing the double spender's identity.

In 1989, he took his idea and commercialized it, forming a company called DigiCash. The actual system was called eCash, while the money in the system was called CyberBucks (https://bitcoinmagazine.com/articles/genesis-files-how-david-chaums-ecash-spawned-cypherpunk-dream/). There was significant interest from major banks and other corporations, but for some reason, DigiCash failed to close the deals that would allow the company to realize its full potential.

DigiCash ended up failing due to the lack of adoption because it didn't support peer-to-peer transactions very effectively, and it was very much ahead of its time. This is 1990 we're talking about. The other challenge was that DigiCash required a server to be run by a central authority and for everyone to trust that organization. Chaum eventually exited the company in 1996, DigiCash filed for bankruptcy in 1998, and the company was sold in 2002.

E-gold was founded by oncologist Douglas Jackson and attorney Barry Downey in 1996. It had grown to over five million users by 2009, when transfers were suspended due to legal issues. At its peak, in 2008, e-gold was processing more than $2 billion USD worth of precious metals transactions per year.

However, e-gold was indicted (formally accused of or charged with a crime) for money laundering and illegal money transmission, and in July 2008, the directors pleaded guilty to these charges (https://www.justice.gov/archive/opa/pr/2008/July/08-crm-635.html).

B-money was an idea created by Wei Dai, a computer engineer and cypherpunk, in 1997, that outlined two concepts. The first concept was that every participant maintains a separate database of how much money belongs to each other (http://www.weidai.com/bmoney.txt), and the second concept was the accounts of who has how much money are kept by a subset of the participants. These were just concepts, though, without actual implementations, primarily because the first concept was impractical, as admitted by Wei Dai:

I will actually describe two protocols. The first one is impractical.

Shortly after the B-money concept was released publicly, Nick Szabo launched a very similar project known as bit gold in 1998. The key concept here was the move away from centralized authorities. It described concepts such as proof of work and digital signatures, similar to bitcoin, but bit gold was never implemented.

Figure 1: Nick Szabo on Twitter comparing his bit gold design to that of bitcoin (https://twitter.com/nickszabo4/status/846116902833303552)

The Liberty Dollar was an alternate currency created by Bernard von NotHaus, in 1998, for the purpose of combating inflation. Liberty Dollars were backed originally by silver, then later other precious metals, such as gold, copper, and platinum. Von NotHaus introduces himself on his website:

"Hi. My name is Bernard von NotHaus. I was so concerned about what was happening to our country's "money" that I created the Liberty Dollar. For 25 years, I was the Mintmaster at the Royal Hawaiian Mint and devoted those years to the study of money, why it is valuable, and how we use it to fulfill our dreams. I wanted to create a totally new inflation proof currency based on precious metals. That quest was completed on October 1, 1998 when the Liberty Dollar was first issued."

However, FBI agents raided the office of Liberty Dollar in Indiana in November 2007, and confiscated all of its property and equipment. In March 2011, von NotHaus was convicted of making, possessing, and selling his own coins.

DigiCash failed because it was centralized. E-gold and Liberty Dollar failed because they broke the law, as well as being centralized. B-money was never implemented because it was impractical, and bit gold was never implemented at all. Therefore, the secret was to create something that was decentralized, leaderless, and practical. Having a decentralized network meant that it could not be taken down, stopped, or disrupted, and not having a leader meant that no government, however powerful, could raid, sue, coerce, or blackmail the company. Being practical meant that the network could be built, demonstrated, and eventually used and adopted by everyone.

The key problem that bitcoin solved that all the previous attempts couldn't, was to prevent double spending in a decentralized manner. The brilliance was that the system was designed to come to an agreement on everyone's bitcoin balance without a central leader, and it even works in the presence of hostile adversaries, so long as they are outnumbered by honest participants. Then bitcoin gained momentum with branding, network effects, popularity, first-mover advantage, investment, exchanges, and applications.

Bitcoin came from humble beginnings. A message appeared on a crypto forum mailing list, called metzdowd.com, from Satoshi Nakamoto, detailing a new electronic cash system called bitcoin in October 2008.

Figure 2: Nakamoto announcing the bitcoin idea on a crypto mailing list called metzdowd (https://archive.is/20121228025845/http://article.gmane.org/gmane.comp.encryption.general/12588/)

The bitcoin white paper detailed a new electronic cash system that claimed to solve the double-spend problem, as mentioned earlier. For the first time, a network was to replace trusted third parties. Many were skeptical and it wasn't until January 3, 2009, when the first bitcoin was created, that many got to see bitcoin in action.

Nakamoto outlined the problem:

"The root problem with conventional currency is all the trust that's required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts" (http://p2pfoundation.ning.com/forum/topics/bitcoin-open-source).

Nakamoto then outlined the solution:

"Before strong encryption, users had to rely on password protection to secure their files, placing trust in the system administrator to keep their information private... Then strong encryption became available to the masses, and trust was no longer required.... It's time we had the same thing for money. With e-currency based on cryptographic proof, without the need to trust a third-party middleman, money can be secure, and transactions effortless."

This leads us to the first fundamental concept: trust. Users would trust the network instead of third-party centralized intermediaries. Trusting the network provides certain advantages. The network does not discriminate, it is neutral, it is not limited by borders, and it is open to participation by anyone and everyone.

There is also a common misconception that blockchains eliminate trust or allow parties to transact without trust. The truth is that trust is merely converted from one form to another, similar to energy. Instead of trusting banks to verify transactions, with blockchains we trust the technology and the mathematics behind it.

The second fundamental concept is just as important as the first. It is decentralization. If we remove the need to trust centralized intermediaries, then who do we trust? We trust a network that is decentralized and participated in by everyone, yet owned by no one.

Decentralization, at first glance, seems very strange. It goes against the popular belief that something has to be owned by someone or at least someone needs to be responsible (or more accurately, held accountable) when something goes wrong. However, in this new world of bitcoin and everything that has stemmed from it, this long-held belief is being tipped on its head.

A third fundamental concept is transparency, and there is no better example than the open-source nature of the bitcoin software code. Anyone can view the code, understand the rules of game, and choose to participate by their own free will.

These fundamentals are important to keep in mind as we continue along our ICO journey. ICOs that do not earn the users' and community's trust, are centralized in nature, or are not transparent will find themselves not as successful as they could be.

Understanding bitcoin and blockchains can be an endless rabbit hole that involves learning more and more technical concepts, such as hash functions, merkle trees, public key cryptography, and the ever-important digital signatures. To the average user, though, all that they need to know is that the underlying mathematics works and when a bitcoin is sent, another copy cannot be created. This is very much like users not needing to understand how the internet works to use the internet.

Having said this, there is one other fundamental concept that is very important to understand: consensus. In a decentralized system with a group of machines, how do the machines agree on something, especially the order of the transactions in a cryptocurrency?

In the case of bitcoin, the whole point is to order a bunch of transactions and the way it works is that anyone in the world can propose a list of transactions to be put into the official list or "chain." If everyone's proposed list was accepted, chaos would ensue. Therefore, a puzzle was invented called proof of work, where the first computer to solve this difficult puzzle would have their version of the list accepted on the official list. Of course, prior to the list being accepted, it would be checked, so if, for example, Alice sent Bob one bitcoin and also sent Charlie the same one bitcoin, only one would be accepted and generally it's the first transaction. Therefore, consensus is very important to understand in blockchain technologies, but there is more than one way to arrive at a consensus. Having a race to solve a mathematical puzzle is only one way.

Another simple way to achieve consensus is for everyone to have a turn at being the leader and having the leader's list of transactions accepted. The problem here is that the leader can be attacked by other computers and prevent consensus from being achieved, stalling the network. If the leader changes, this new leader can be attacked in a follow-the-new-leader scenario. It is also not fair, as the leader has sole discretion on the order of transactions. This is why leader-based consensus is not generally used.

Proof of stake is another consensus algorithm where computers on the network essentially put coins in escrow (staking) and propose a list of transactions. Choosing the winning list can be done in several ways, such as random selection and its variants, or coin age-based selection. Nxt and Blackcoin use random selection and Peercoin uses coin age-based selection.

To the technical purist, a bitcoin is not really a coin and it is not owned by anyone per se. A bitcoin represents the digital right to transfer ownership of an unspent output of a previous bitcoin transaction, to create an input for the next bitcoin transaction. If that last sentence didn't make sense, don't worry, as it's not critical to understanding bitcoin.

A more common definition of bitcoin is that it is a cryptocurrency that can be used as a form of payment in exchange for goods or services.

Another interesting definition is by Peter Van Valkenburgh, the director of research at Coin Center: "Bitcoin is software running across a network of peers that creates and maintains a shared ledger accounting for holdings of a scarce token."

The unique aspect about bitcoin is that no centralized organization owns it nor has any centralized organization created it. This leads to the question: what is a coin?

In the crypto world, a coin can be thought of as the native digital asset of a blockchain. For example, a bitcoin is the native digital asset of the bitcoin blockchain, but people usually refer to bitcoin just as a cryptocurrency or a digital currency.

Another way to look at it is that when a network is created and becomes live, the native digital asset or coin is available immediately. Understanding this is important when considering the concept of mining coins.

Mining is the process of bringing coins into existence over time, usually based on an issuance rate determined by some mathematical formula. In bitcoin, the design was to mimic the discovery or mining of gold, where energy and resources are required to find it and there is a limited supply. This plays to the fact that some people call bitcoin "digital gold."

Tip

Mining: The process of using a computer to verify transactions and having them added to the bitcoin blockchain, and bringing more bitcoins into existence.

Bitcoins are rewarded to incentivize people to participate in verifying transactions, and a puzzle is required to be solved to determine who wins this reward because there are many computers attempting to verify transactions.

The formula is quite simple and goes like this: 50 bitcoins are minted on average every 10 minutes and after every four years (approximately), this number halves. When the total supply reaches 21 million, no more bitcoins will be created. Currently, the reward is 12.5 bitcoins before the next halving, at around May 2020.

Learning about bitcoin often leads newcomers to ask the simple question: what is money? While this is an entirely different subject, it is important to note what the functions of money are and how bitcoin compares to money.

Money has three generally-agreed-upon functions: it is a Unit of Account (UoA), a Medium of Exchange (MoE), and a Store of Value (SoV). Nakamoto envisioned bitcoin as operating or functioning as money, as detailed in the bitcoin white paper. However, a bitcoin is not currently a unit of account. We know this because currently, hardly any merchants price their products or services in bitcoin. Merchants may accept bitcoins as a payment option, but prefer to use fiat currencies, such as USD.

In the early days, bitcoin was primarily used as a medium of (decentralized) exchange, making media headlines for being used to buy drugs on the now-defunct Silk Road website or being used on gambling sites, such as Satoshi Dice. As bitcoin's adoption grew, the value also grew with it, which led many to perceive bitcoins as a store of value. Why spend them today if I believe that they will be worth more tomorrow?

The point here is that bitcoin is constantly evolving and changing. The ultimate goal is to one day visit your local supermarket or grocery store and see bitcoin price tags on the shelves.

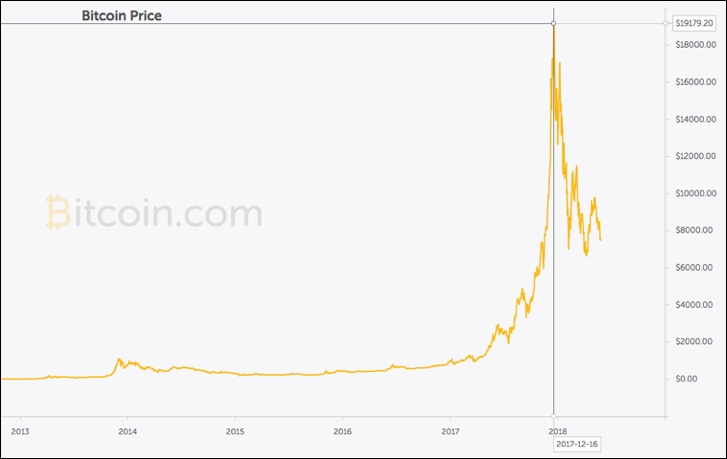

Figure 3: Bitcoin price charts started around mid-2010, peaking in December 2017

Now, because bitcoin was built with transparency in mind, the code was open source. This means that the creator or copyright holder provided the rights to study, change, or freely distribute the software to anyone and for any purpose (Understanding Open Source and Free Software Licensing, St. Laurent, Andrew M., O'Reilly Media, 2008). One advantage of open-source software is that it is generally more secure, due to a large community of developers vetting the code and improving it. It is also open to constant attack, as vulnerabilities can be more easily identified if access to the code is available. This is a positive, however, as vulnerabilities typically can be fixed faster than with closed-sourced software.

The bitcoin source code was originally hosted on sourceforge.net (http://www.metzdowd.com/pipermail/cryptography/2009-January/014994.html), and available for anyone to download and test, and was migrated over to GitHub, where the first commit occurred in August 2009 (https://github.com/bitcoin/bitcoin/tree/4405b78d6059e536c36974088a8ed4d9f0f29898). There are currently 548 contributors from around the world, including some of the best and brightest minds.