Whether or not you believe that history repeats itself, there is no denying that there are patterns. Patterns affect other patterns (like a kaleidoscope), patterns are found within patterns (fractals), or are hidden (the value of pi). Much of what we see today, in this new world of cryptocurrencies, blockchain technologies, and the new token economy, can and has been compared to various historic events of the past.

In this chapter, we will take a look at the potential of Initial Coin Offerings (ICOs) by taking a step back in time, before zooming into the future by looking at the following topics:

- What is an ICO?

- The difference between coins and tokens

- The dot-com versus dot-coin bubble

- Risk in ICOs

- A new era of ICO innovation

We will start by explaining what an ICO is and all the associated terminology, before interpreting the days of the dot-com bubble back in the late 1990s/early 2000s and comparing them to what many now call the "dot-coin bubble," where many cryptocurrencies and ICOs are overvalued. So, was the December 2017 crash an actual crash similar to 2000 or are we still at the foothills of the mountains? If it was the bust, shouldn't we start seeing the new era of ICO innovation?

An ICO, is a fundraising mechanism where new projects sell an underlying crypto token in exchange for capital. In the early days, the capital was in the form of bitcoin, but over time this increased to other forms of cryptocurrencies, in particular ether. Now that the industry has developed, regular fiat currency is being accepted under certain conditions as well. Accepting fiat currency means the ICO can reach more people.

The term "ICO" was created and popularized to allow comparisons to the term Initial Public Offering, otherwise known as an IPO. Similar to an IPO, where shares are sold to investors for equity in a company to fund operations, an ICO is where "coins" are created and sold to investors to fund the operations of a company or project.

There are some subtle, but important, differences between an ICO and an IPO. The lack of current regulations and oversight in the ICO space has been seen as an advantage to helping avoid the costly and expensive process of raising capital using traditional methods. Another subtle difference, more relevant in the early days, is that while IPOs deal with investors, ICOs deal with supporters who believe in the cause of the project and are keen to invest, much like a crowdfunding event. The main difference, though, is that these coins do not provide the investor with ownership rights to the company. In other words, they do not represent equity.

To the technical purest amongst us, in an ICO, the coins that investors receive are actually digital tokens, which is why sometimes they are called an Initial Token Offering. However, ICO is currently the accepted mainstream terminology.

ICO is an unfortunate acronym because, as mentioned in the preceding paragraph, it is actually an Initial Token Offering or ITO. Another term used was Token Generation Event or TGE. This is actually a much more accurate description of what exactly is occurring. An event, that usually lasts an average of 30 days, is created where cryptocurrencies or regular currencies are received, after which tokens are generated and then distributed to those who contributed. This is remarkably different to an ICO, simply because there are no coins and they are arguably not offered. What is interesting is that not many white papers reference the term ICO and the terminology used varies a lot. In fact, the term ICO has been popularized by the media and the wider public.

|

Date |

Company name |

Terminology used |

|

Aug 2016 |

ICONOMI |

Initial Coin Offering |

|

Sep 2016 |

FirstBlood |

Crowdsale |

|

Nov 2016 |

Golem |

Crowdfunding |

|

Apr 2017 |

Humaniq |

Initial Coin Offering |

|

Apr 2017 |

Gnosis |

Token Launch |

|

May 2017 |

Basic Attention Token |

Token Launch |

|

May 2017 |

Monaco |

Token Creation Event |

|

Jun 2017 |

Civic |

Token Sale |

|

Jun 2017 |

OmiseGo |

Token Sales |

|

Jun 2017 |

TenX |

Initial Token Sale |

|

Jul 2017 |

Tezo |

Fundraiser |

|

Oct 2017 |

Horizon State |

Initial Coin Offering |

Figure 1: Many companies didn't actually use the word ICO in their white paper

TenX uses the term Initial Token Sale in its TenX white paper:

"An Initial Token Sale (ITS) is an event in which a new cryptocurrency project sells part of its cryptocurrency tokens to early adopters and enthusiasts in exchange for funding. For the party offering the tokens for sale, this has become a well-documented and well-respected way to raise funds to upscale an existing product or service."

The fact that the word "ICO" is similar to "IPO", which has been around for a long time, provides comfort due to familiarity and we'll continue using the word "ICO" throughout the book for simplicity and brevity. However, we must acknowledge that things change very quickly in the world of crypto and, in fact, new terms such as Security Coin Offering (SCO) or Security Token Offering (STO) are increasing in popularity. With this said, let's explore the concept and definition of a token in more detail.

Oxford Dictionaries defines a token as:

"A voucher that can be exchanged for goods or services, typically one given as a gift, forming part of a promotional offer, a metal, or plastic disc used to operate a machine or in exchange for particular goods or services."

David Siegel, CEO of Pillar Project and a vocal thought leader in this space, defines a token as follows:

"Fundamentally, a token is an IOU. It is a contract. It represents rights and obligations… with the properties of having an issuer, a substrate (carrier), a system it is meaningful in, a value to someone, and some way to use them." (https://hackernoon.com/the-token-handbook-a80244a6aacb).

William Mougayar, another vocal thought leader introduced in Chapter 1, Once Upon a Token defines a token, in the context of this industry and in a more abstract way, as:

"A unit of value that an organization creates to self govern its business model and empower its users to interact with its product, while facilitating the distribution and sharing of rewards and benefits to all its stakeholders."(https://www.slideshare.net/wmougayar/state-of-tokens-by-william-mougayar-april-2018).

Let's start with traditional physical tokens, as we introduced in Chapter 1, Once Upon a Token. Examples include milk tokens, which were used back in the good old days when milk was delivered to your doorstep in glass bottles, or arcade tokens that you would have to buy to play your favorite game, such as Donkey Kong, or Street Fighter, at your local arcade hang out.

Taking the concept of an IOU from above, that arcade token is an IOU for access to a game and the milk token is an IOU for a bottle of milk. If we analyze these physical tokens further, what we see is that we have a company that issues the token and we have the perceived value to the holder of the token, due to the promise that the token can be redeemed based on certain terms and conditions. A token in this context is an in-house representation of some amount of real money that now only has some utility value.

Fast-forward in time and let's compare this to frequent flyer miles or "airpoints", which are given by almost every airline in the world. As previously mentioned, these frequent flyer miles are just another form of token. There is an issuer and there is perceived value to the holder, due to a promise that they can be redeemed based on certain terms and conditions.

Then we start moving into the numerous loyalty cards, including the Starbucks loyalty card. The card and the stamp represent the token and ensure that if 10 stamps are collected, the next coffee is free. Note that the stamp alone is not worth anything because if you stamp it on any random piece of paper, my bet is that Starbucks won't be giving you that 10th coffee for free.

This brings us to an interesting point where tokens quickly evolved to inherit anti-counterfeiting technologies. The level of investment made into anti-counterfeiting measures generally reflects the value being protected. There is no point in producing holographic tamper-resistant Starbucks cards where the reward is an extra coffee worth $4.50. A $100 USD bill, though, is an entirely different story.

In the blockchain world, tokens can be considered as the non-native digital asset of a blockchain. They are non-native because tokens can be created on any blockchain technology. These tokens can then be programmed to have meaning. In a sense, they can be considered smart tokens that are powered by smart contracts.

Recapping the definition of a coin from the previous chapter, the following table shows the difference between coins and tokens. As of June 2018, CoinMarketCap lists 839 coins and 795 tokens:

|

Coins |

Tokens |

|

Native digital asset of a blockchain. |

Non-native digital asset of a blockchain. |

|

Coins are digital currencies in which mathematics is used to regulate the generation of the currency and verify the transfer of funds. Coins belong to and move within decentralized, cryptographically protected blockchains. |

Tokens are a representation of a particular asset or utility that usually resides on top of another blockchain. Tokens can represent basically any assets that are fungible and tradable, from commodities to loyalty points, to even other cryptocurrencies! |

|

Examples include Bitcoin, Dash, Litecoin, and Monero. |

Examples include OmiseGo, TenX, Augur, and Humaniq. |

Figure 2: The difference between a coin and a token

Currently, there is no global unified classification of tokens. However, there are attempts being made by various regulatory bodies around the world. The US Securities and Exchange Commission (SEC) and the Swiss Financial Market Supervisory Authority (FINMA) have divided tokens into three broad categories, which we will return to in Chapter 6, Playing by the Rules.

These coins or tokens are intended to provide similar functions to currencies, such as the US dollar, euro, or Japanese yen, but they do not have the backing of a government. Bitcoin, Bitcoin Cash, and litecoin are examples of cryptocurrencies whose function is purely to operate as a means of payment.

These are the most popular types of tokens being promoted, rightly or wrongly, in an ICO and they represent future access to a company's product or service for a customer. Sometimes they are referred to as "user tokens", "appCoins", or "appTokens" (application coins/tokens). The most important feature of a utility token is that it is not issued as an investment asset, which exempts it from having to comply with the relevant regulations.

These are "digital assets" that represent or are backed by "physical underlyings, companies, or earnings streams, or an entitlement to dividends or interest payments. In terms of their economic function, the tokens are analogous to equities, bonds, or derivatives, (https://www.finma.ch/en/news/2018/02/20180216-mm-ico-wegleitung/)" as defined by the FINMA (https://www.finma.ch/en/news/2018/02/20180216-mm-ico-wegleitung/).

Sometimes referred to as "equity tokens", they can provide investors with some amount of ownership and rights to the profit generated by the company, much like traditional stocks. The main point here is that these tokens are subjected to security laws and regulations in the relevant jurisdiction. For example, the tokens for the ICO for tZERO, which is a portfolio company of Overstock Inc, promise to provide quarterly dividends derived from the profits of the tZERO platform to its investors.

LAToken aims to connect cryptocurrencies to the real economy, by allowing crypto holders to diversify their portfolios with access to tokens linked to the price of real assets. The company launched a trading platform for hard assets, such as real estate and gold. LAToken trades in assets, such as shares of blue chips (Apple, Tesla, and so on), and commodities (oil and gold). This classification is not exhaustive, and ICO token types can change over time.

With the rise in popularity of the crypto space, there has been an increase in new terms or terms that were once only popular within a small community. Here are some common terms associated with tokens:

- Airdrop: A strategy to facilitate the wide distribution and use of project tokens. Project creators give away tokens, sometimes randomly, but mostly to avid supporters or potential supporters of the project.

- ATH (All Time High): This refers to the price of cryptocurrencies or tokens that reach their highest historical price.

- Bounties: Incentivized reward mechanisms offered by companies to individuals. Many companies incorporate a bounty program as part of their ICO campaign. The reward is usually in the form of cryptocurrency or, more commonly, the ICO tokens themselves. Popular bounties include bug reporting bounties and translation bounties in particular for white papers.

- Burning: Removing tokens from the total supply by deleting them, if the smart contract allows it, or making the tokens permanently un-spendable by sending them to an address with no known private key. This is usually done when not all tokens are sold in an ICO. The effect is to reduce supply.

- FUD: Fear, uncertainty, and doubt. A strategy of spreading negative, dubious, or false information to influence perception.

- Locking/freezing: Preventing the tokens from being used for a set period of time. Early investors' tokens are often locked at specific time intervals to prevent them from selling all their tokens immediately and negatively affecting the price. Pillar Project didn't burn but locked up its unsold tokens and froze them for 10 years.

- Meta coin: Similar to coloring a coin, where extra meaning is given to a coin to increase the function and hence the purpose. This term has been superseded by the term "token."

- Shilling: Tricking as many people as possible to invest in a coin or token that may be valuable in the future but in 99% of cases won't be. A shill attempts to spread excitement by endorsing the product or service in public forums with the pretense of sincerity, when actually they are being paid for their services.

- White paper: Very loosely, it is essentially a prospectus that outlines the technical aspects of the product, the problems it intends to solve, how it is going to address them, a description of the team, and a description of the token generation and distribution strategy (more on this in Chapter 8, White Paper, Website, and Team).

ERC20 deserves a special mention because most of the ICO tokens are classified as ERC20 tokens. ERC stands for Ethereum Request for Comment and is used for creating standardized smart contracts.

It was proposed in November 2015 by Fabian Vogelsteller and defines a set of rules, or, more specifically, functions that Ethereum tokens should contain (https://github.com/ethereum/eips/issues/20). The six functions are totalSupply, balanceOf(), transfer(), transferFrom(), approve(), and allowance(), along with two events: Transfer() and Approval(). The ERC20 standard has simplified the process of the creation of tokens and as of June 2018, there are 91,247 ERC20 token contracts listed on etherscan.io.

As a side note, an ERC is actually a subtype of EIP, which stands for Ethereum Improvement Proposal. An ERC is the original proposal, although perhaps not complete, and with further input it is refined to something most participants will agree is useful, that then becomes an EIP. Therefore, ERC20 should really be referred to as "EIP20" but with widespread use of "ERC20", both terms tend to mean the same thing.

So why is there so much excitement about blockchains and ICOs? The answer is that the promise made is game-changing. The promise is to create, or design, a system, or a platform, that will disrupt the disruptors. The promise is made to decentralize centralized organizations and remove intermediaries that clip the ticket but provide no extra value whatsoever. The promise is made to revolutionize how data is owned and value is stored. There have been attempts in the past to do something similar, but nothing on the scale we are seeing currently. These goals all involve utilizing the disruptive blockchain technology, and ICOs lend a hand by disrupting the funding mechanism. The catch is, ICOs also utilize blockchain technologies.

Some of these promises touch and appeal to our humanitarian emotions, such as helping displaced refugees with aid by tracking donations on the blockchain, or providing a means of personal identification on the blockchain so that no single entity can accidently, or with willful intent, change.

Others see a way of doing old things better. Uber challenged the existing taxi conglomerates by providing a more streamlined and efficient approach to personal transportation. Why not decentralize Uber? With autonomous or driverless cars coming to a town near you within the next decade, there is a paradigm shift coming, involving not just peer-to-peer electronic payments, but peer-to-peer decentralized autonomous transportation. It is these promises, and more, that have the growing community of tech geeks excited.

As the ICO craze caught on, there was a mad rush to buy these tokens in order to participate. This was a contributing factor leading to the increase in demand for bitcoin and ether, which helped to fuel the incredible gains observed in the past few years. These gains have led to what many have called a "speculative bubble."

Next, we look at whether we are indeed in a speculative bubble. Are cryptocurrencies and tokens overvalued? Is this the digital version of Tulip mania or the South Sea Bubble?

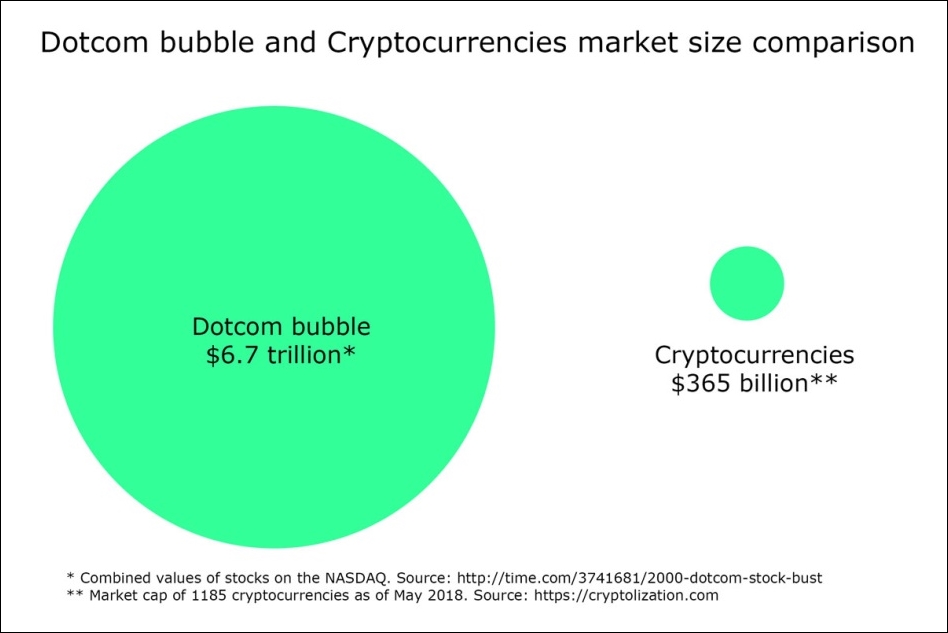

The most common comparison to what is happening now in the cryptocurrency world is made with the dot-com bubble, where between approximately 1997 and 2001, a period of excessive speculation and exuberance, coupled with a significant growth in the usage and adoption of the internet, fueled a frenetic feeding frenzy. Investors and venture capitalists poured money into companies, many of which operated at a net loss, to harness the network efforts and to build market share. The network effort was a great sell because the more something was used, the more value it had due to the users on the network. Any company with a domain name ending in .com, or with the promise of eCommerce, was having money thrown at it, even if the business model was flaky, sketchy, or even nonsensical.

Compare this to early 2014 to 2016, where companies only had to mention the word "blockchain" in their pitch deck to have investors throwing cash at them. Existing companies would pivot from traditional software companies to becoming blockchain companies and overnight, hundreds of self-titled "blockchain experts" or "blockchain consultants" appeared on LinkedIn. As for the network effect, what better story to sell than the more people using a cryptocurrency or a token, the more value it has?

According to the New York-based securities data firm Commscan, web companies raised a total of $1 billion USD in 34 IPOs in 1997, rising to $2 billion USD in 45 deals in 1998, and then exploding to $24.1 billion USD in 292 IPOs in 1999 (http://money.cnn.com/2000/11/09/technology/overview/).

The market value of Nasdaq technology companies peaked at $6.7 trillion USD in March 2000 (http://articles.latimes.com/2006/jul/16/business/fi-overheat16). The market capitalization of the current cryptocurrency market fluctuates greatly between $200 to 600 billion USD. A common way to show the value of these two markets is as circles drawn side by side in a crude attempt to not just compare, but also to somewhat indicate the potential room for growth of the cryptocurrency and token, or ICO, markets.

Figure 3: Comparison of the dot-com bubble and the current cryptocurrency market size

This graphic needs to be taken with a grain of salt, though. The market capitalization or "market cap" of cryptocurrencies is taken as the circulating supply of a cryptocurrency, or token, multiplied by the current market price, and this can be deceiving.

Traditionally, market capitalization measures the equity value of a business or what investors are willing to pay for its future profits. Visa, for instance, has a market cap of $300 billion USD as of May 2018. (https://ycharts.com/companies/V/market_cap). Bitcoin had a market cap of $300 billion USD at its peak in December 2017 and currently sits at around $136 billion USD as of May 2018. However, bitcoin isn't a business and has no profits. In some ways, we are not comparing apples with apples. Perhaps we should be comparing total assets or perhaps transactions per day. In this case, bitcoin has around 200,000 (https://blockchain.info/) per day versus approximately 345 million on Visa (https://www.reddit.com/r/nanocurrency/comments/82438o/visa_is_capable_of_performing_24000_transactions/). Using this comparison, compared to the global financial institutions, bitcoin is still very insignificant.

Now, because the software code of nearly all cryptocurrencies is open source, anyone can create their own cryptocurrency, such as MyCoin, or their own token, such as My Unique Token (MUT) in a matter of hours.

Let's imagine that MUT has an arbitrary supply of one billion tokens that somehow managed to increase in price to $1. All of a sudden, the market cap has increased to a billion dollars, all from an idea, a white paper, and a website. Take this example and multiply it by 1,000 coins and we get to the magic market cap of $1 trillion USD out of nowhere. Unfortunately, until there is a better way, the market cap seems to be the easy figure to quote to indicate the potential of the ICO market, however inaccurate it may be.

If we compare the early internet days circa 1994 to the current progress of blockchain and ICO developments, and believe the far-reaching technological impact they could have, it is obvious that there is a lot of potential ahead. A common understanding in the crypto industry is that bitcoin is just the first application utilizing the blockchain technology and there are many more exciting applications yet to be invented. Some argue that the current "killer application" is these tokens, which have just started to revolutionize the funding industry.

This is similar, though, to how email was the first, and for a long time the only, "killer application" of the internet. Email was invented in 1972 by Ray Tomlinson and it wasn't until the mid-1980s, some 20 years later, that commercial use grew (http://www.nethistory.info/History%20of%20the%20Internet/email.html). In the mid-to-late-1990s, email really started to take off. To get to that point, the technology had to be stable and have features that were valuable to users. User interfaces had to be developed, so it wasn't just a black window full of text (engineers refer to this as a Command-Line Interface (CLI)) and a user base had to grow over time, referring to the network effect mentioned earlier.

The same comparison can be made with bitcoin. It was very much for computer geeks and engineering hobbyists in the early days, but now more and more features, services, and products are being developed in and around the crypto space. What needs to be taken into account, when comparing bitcoin's adoption rate with the adoption rate of email and the internet, is that with the current technology suite, adoption times are now compressed.

Instead of taking 20 years for the commercial adoption of email, bitcoin or cryptocurrency will take less. Payment gateways and merchant services appeared very early on. Some websites provided bitcoin addresses for payment to be made or the same address, but represented as a QR code:

Figure 4: A bitcoin address represented as a QR code

When celebrities, such as socialite Paris Hilton, boxer Floyd Mayweather, the rapper The Game, and DJ Khaled, start endorsing ICO projects, you know we are in the midst of a potential bubble. With many projects promoting similar ideas, having celebrity endorsements is one way to get attention and large sums of money have been raised in some of these ICOs.

Hilton tweeted, "Looking forward to participating in the new @LydianCoinLtd Token!" The company is claiming users will be able to trade Lydian tokens for the company's data-driven digital marketing services. The irony is that many of these celebrities probably have no clue what cryptocurrencies are.

Figure 5: Hilton's tweet in September 2017, which was deleted shortly afterwards

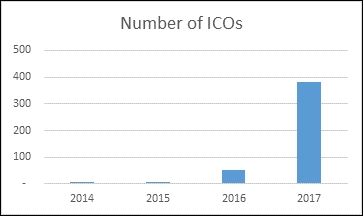

Statistics on the number of ICOs and the total amount raised in each year vary depending on the source but, ignoring outliers, they are all in the same ballpark. There were less than 10 ICOs in 2014 and 2015 and around 40 in 2016. This jumped almost 10 times in 2017, to just under 400, and although the verdict is still out in 2018, it is on track to surpass the 2017 numbers.

|

2014 |

2015 |

2016 |

2017 |

2018* | ||||||

|

# |

$USD |

# |

$USD |

# |

$USD |

# |

$USD |

# |

$USD | |

|

coinschedule.com |

- |

- |

- |

- |

43 |

$95M |

210 |

$3.8B |

420 |

$9.8B |

|

coindesk.com |

7 |

$30M |

7 |

$9M |

43 |

$256M |

343 |

$5.5B |

271 |

$7.0B |

|

icodata.io |

2 |

$16M |

3 |

$6M |

29 |

$90M |

871 |

$6.1B |

846 |

$5.3B |

|

coinist.io |

5 |

- |

4 |

- |

35 |

$284M |

303 |

$5.9B |

- |

$3.3B |

|

Tokendata/Fabric Ventures |

- |

- |

- |

- |

- |

$240M |

435 |

$5.6B |

- |

- |

Figure 6: ICO data from various sources showing the number of ICOs and the amount raised. 2018 figures as of June 2018

The amount raised increased from tens of millions in 2014 and 2015, to hundreds of millions in 2016 and around $6 billion USD in 2017. That is a greater than 10-fold increase each year. One of the reasons for the enormous rise was the ease of creating tokens. As mentioned earlier, it was essentially a cookie-cutter approach where anyone could take some open-source code, replicate the token creation process with very little effort, and then spin up a marketing campaign around it. In fact, the technology was not the challenge: it was all about marketing.

Figure 7: The average number of ICOs from 2014 to 2017

The growth in ICOs came from the emergence of platforms such as Ethereum, Nxt, and Waves. More and more platforms are being created because investors are seeing that the value is not just in the token, but in the platform where tokens can be created from. As these platforms continue to develop, more and more tokens will be invented, spurring on the tokenized economy. When talking about Bitcoin, Ronnie Moas, founder of standpointresearch.com and a prominent stock analyst, has said:

"I don't know how much gold there is in the ground, but I know how much bitcoin there is, and in two years there will be 300 million people in the world trying to get their hands on a few million bitcoin."

Moas claims that currently there is about $230 trillion USD invested in stocks, cash, bonds, and gold and argues that if 2% of that $230 trillion USD finds its way into cryptocurrency, that would be a $4 trillion USD market valuation. Recalling the current $365 billion USD market cap, that would represent 11 times where we are today. The cryptocurrencies Moas talks about include all the ICO tokens as well. So, this is not just about converting frequent flyer miles or supermarket loyalty points into tokens but tokenizing everything from council rubbish bags and Manuka honey, to local sports group membership and Pokémon cards. The potential for tokens in this new economy is tremendous.

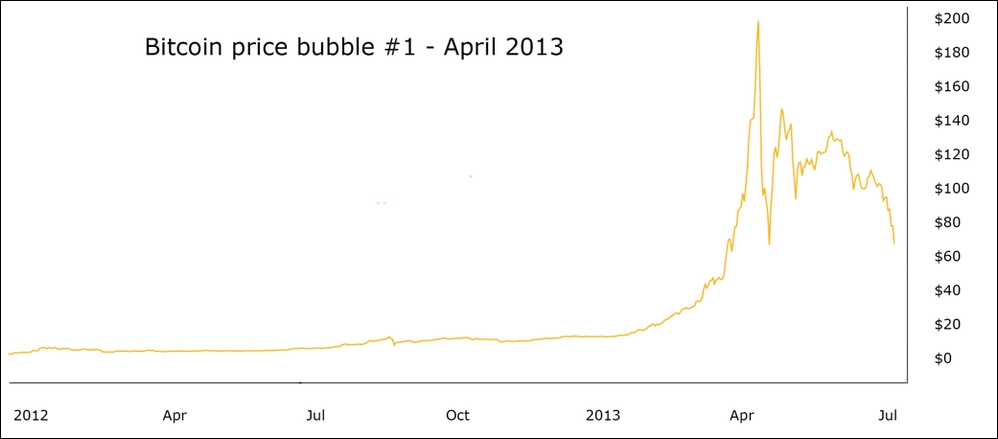

Continuing with bitcoin as an example, back in April 2013, many bitcoin detractors called it a "bubble", citing the meteoric rise in price from $20 USD to $200 USD:

Figure 8: Bitcoin peaked at $200 USD in April 2013

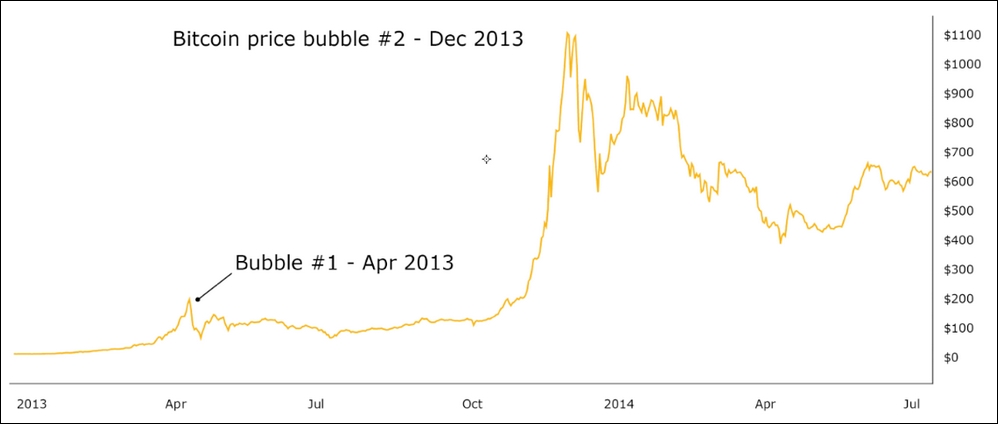

However, during October 2013, just six months later, there was another so-called "bubble." This time, there was a meteoric rise from $200 USD to $1,100 USD, that made the April bubble appear like a small blip in comparison. Again, the detractors cried foul on this, calling it speculative, volatile, and an experiment.

Figure 9: In 2013 to mid-2014, bitcoin peaked at $1100 USD

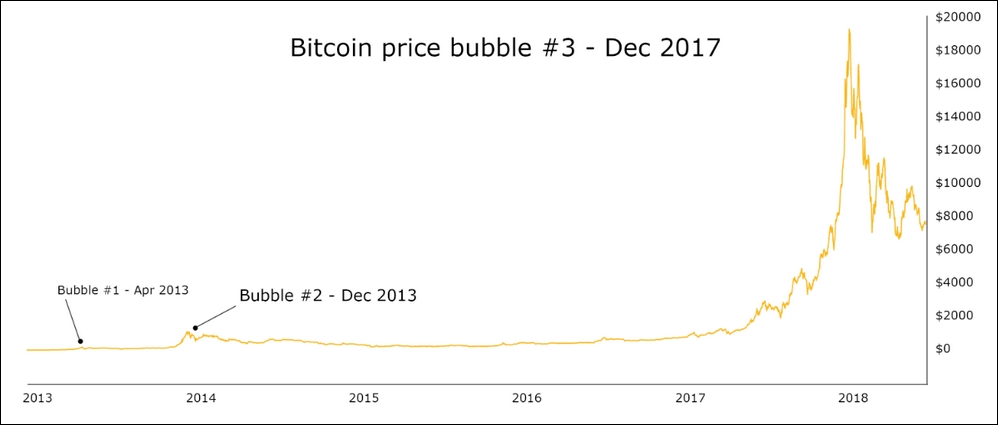

In December 2017, there was yet another bubble, this time rising from $1,100 USD to just under $20,000 USD:

Figure 10: In 2017 to mid-2018, bitcoin peaked at just under $20,000 USD

What we are seeing here is the phenomenon called "scale invariance." In other words, the graph looks similar at different scales, or, more formally, it is any object or function that doesn't change when the scales are multiplied by a common factor.

However, all the other cryptocurrencies and ICO tokens can be observed as following a similar trend. In fact, when bitcoin experiences growth, all other tokens grow along with it. The aphorism "a rising tide lifts all boats" is often seen reverberated in the Twittersphere. Of course, the opposite is true as well.

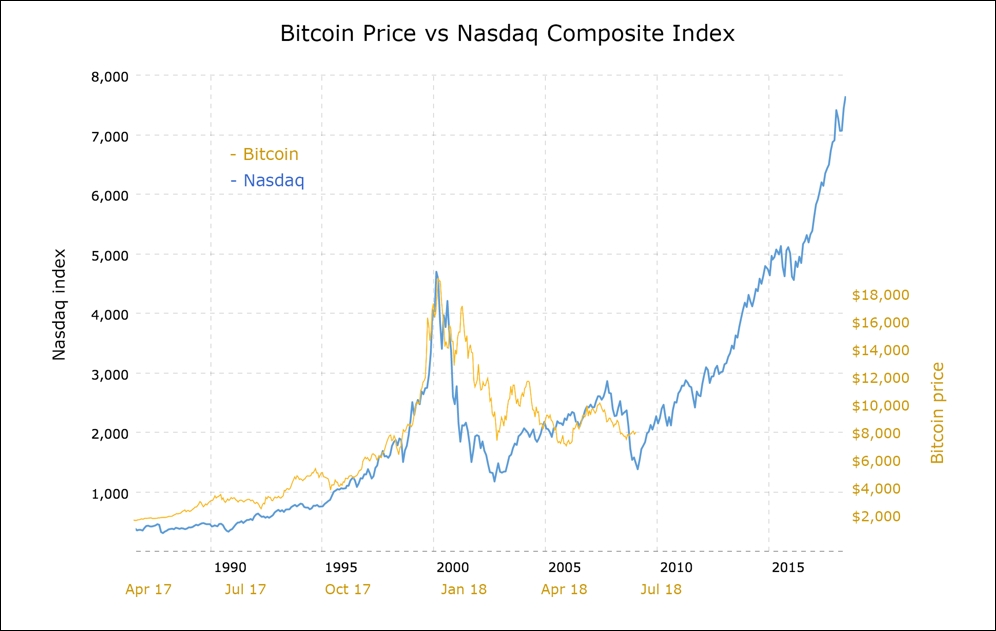

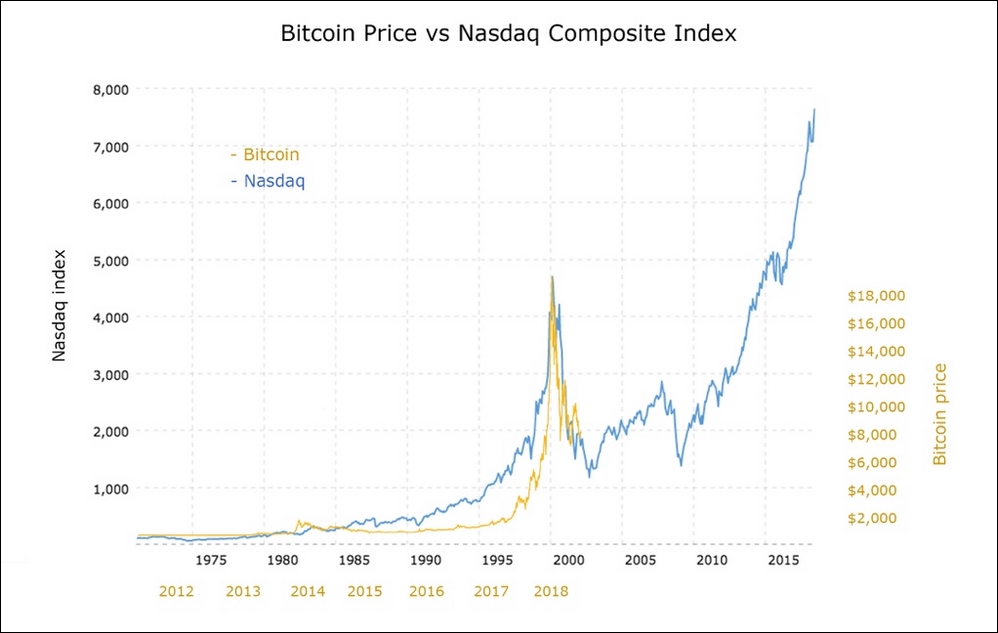

Another popular comparison commonly made between the dot-com and dot-coin boom is the growth of the Nasdaq composite index (http://www.macrotrends.net/1320/nasdaq-historical-chart) in conjunction with the price of bitcoin (https://charts.bitcoin.com/chart/price). Compare the rise from 1990 to 2000 for the Nasdaq against a similar rise for bitcoin, but from only April 2017 to January 2018. The comparison also seems to justify the fall in bitcoin's value.

Figure 11: Comparison of bitcoin price and the Nasdaq index (non-inflation adjusted) showing similarities to the dot-com boom and bust

There are two important points to consider when viewing eye candy such as this. Firstly, the time frame of bitcoin is very small. In this case, it is only nine months. A small time frame is similar to conducting statistical research with a small sample size. Therefore, the results are more susceptible to volatility or outliers. Secondly, when overlaying the charts, depending on the scale or zoom factor, the bitcoin chart can be made to fit almost any time frame. It's almost a case of making the data and evidence fit the hypothesis.

The following chart shows an overlay across a larger number of years, effectively taking a zoomed out view. It actually makes the bitcoin rise more dramatic and makes a stronger case that bitcoin and the crypto space is a bubble (please note that although the Nasdaq period from 2000 to 2018 is presented, it is in no way intended to be an extrapolated view of the potential of the price of bitcoin).

Figure 12: The bitcoin price versus the Nasdaq index over a six-year period

These patterns may or may not be coincidental but combining the knowledge that new blockchain technologies are currently being developed and deployed, and that the awareness of blockchains is growing amongst institutional investors as more and more tokens are created, it is not hard to see the immense potential of blockchains, ICOs, and the new tokenized economy.

"I have not failed. I've just found 10,000 ways that won't work."

- Thomas Alva Edison

To innovate, one must experiment. To experiment, one must continually find new ways of doing things. The catch is that not all of these new ways of doing things will succeed, as Thomas Edison found out. The sensible conclusion to draw is that out of all the thousands of ICOs created so far, most of them will fail. In fact, many have. White papers and GitHub source code repositories have been deleted and any remnant of LinkedIn profiles for the ICOs removed, that is, if they were real in the first place.

The rise of speculators and opportunists is of no surprise to those in the industry and it shouldn't be a surprise to anyone else. It happened in the dot-com bubble, the housing bubble, and even the various gold rush eras throughout the world. However, as the clampdown begins in 2018, from regulators and governments, and closer scrutiny is placed on ICOs, we will start to see a wave of new ICOs that work a lot closer with these regulatory bodies (more on this in Chapter 6, Playing by the Rules).

The irony is that these regulators will need to learn and understand this technology in the first place. They often try to wrap it up in a neat and tidy box to categorize it in the existing system of laws and frameworks. This is where the problem lies. Cryptocurrencies and tokens created through ICOs don't fall neatly into any existing categories. New definitions need to be created and new boxes need to be made for cryptocurrencies and tokens.

The dot-com crash resulted from the inflated share prices of technology companies losing significant value over a short period of time, when startups promised the world but all they could deliver was a simple web interface and a credit card form that required manual processing in the back-end. Does this sound familiar?

In the ICO world, we have seen very creative and innovative propositions, such as Augur/Gnosis, a decentralized prediction market; Basic Attention Tokens (BAT), where attention span becomes the traded commodity and Civic, a digital blockchain-based secure identity ecosystem. We may not see it, or even agree with it, but they are the equivalent of the HTML web page of the late 1990s. There is no doubt that digital identities will be a necessity as we all become digital citizens, but there are many questions yet to be asked and so many answers yet to be discovered.

One issue with many of these ICOs is that the tokens are purchased by supporters, users, and investors before the platform is even launched. If the platform has not been launched yet, how are tokens valued? How is this different to someone selling the vision of an unknown product for a certain amount of money, hoping that it will be worth something in the future?

Tremendous faith is put into the team to deliver something potentially six-to-18 months away, where anything could happen, such as the infighting between the Tezos (a blockchain with in-built governance) founders and the foundation it created.

The industry is slowly changing to become a place where many companies build proof of concepts, test their business model and, with more understanding of what tokens are and how they work, offer better and more innovative ideas towards solving real-world problems.

Infrastructure was a problem for the internet back in the 1990s because you couldn't launch a high-speed video streaming service when the majority of users were still on dial-up modem. The difference now, though, is that the internet infrastructure is there and the users are there also. In a global, interconnected world, where the best minds can work collaboratively with the power of the internet, this blockchain infrastructure can be built much faster. This is what continues to support the potential of blockchain technology and the tokenized economy.

There are several things holding blockchain technology back, though. First of all, scalability is a constant challenge. Although the basic infrastructure, such as access to the internet and computers, and powerful mobile devices, is there, the infrastructure of the blockchain technology itself is still immature. The internet infrastructure of Facebook may be able to support one billion plus Facebook users, but blockchains cannot yet support a billion users on a decentralized version of Facebook. The bitcoin blockchain is said to process only around seven transactions per second. This is a very crude estimate but is reflective of the scalability issue. However, these issues will be solved. The internet didn't manage to support a billion Facebook users overnight and blockchains won't either.

Next comes the complexity problem. It should come as no surprise that humans have evolved into creatures seeking instant gratification: wanting things now and wanting things simple. We have a magic button to cook dinner in four minutes, a magic pill to lose weight in four weeks and, of course, with one click of the mouse we can have our favorite pair of shoes delivered to our doorstep.

In this new crypto world, where we become our own bank and there are no third parties, intermediaries or toll-free customer support lines to call upon, we need to learn and understand how this stuff all works. We cannot shift responsibility to someone else because there is no someone else. Understanding basic concepts, such as public and private keys, and the fact that if you lose your private key you lose all your cryptocurrencies, sounds scary at first, but it is no different to losing your wallet in the back seat of a taxi after a night out in town. Complexity is relative to the amount of effort spent learning and understanding this new and innovative technology. The potential for blockchains and the tokenized economy carries with it the enormous potential for learning.

All ICO projects have a road map. It is almost a mandatory requirement to show not only the potential of the project, but the timeline as well. There is no point in designing flying cars if the delivery date is a hundred years out. What we are slowly starting to see is projects that did an ICO in early 2017 beginning to miss or delay milestones six-to-nine months later. Smaller ICOs have simply faded away, but bigger ICOs will face intense scrutiny.

The key is that it takes a couple of years for investments into ICOs to see significant tangible results. This follows the trend of investment into blockchain technologies, such as the Lightning Network and Segregated Witness (both introduced in Chapter 2, A Bit of Coin Theory) back in 2014, which saw tangible outputs several years later and eventual promotion to production in 2017. Therefore, while many ICOs are still in the honeymoon phase of how to spend the millions that has just been raised, some road maps look very optimistic.

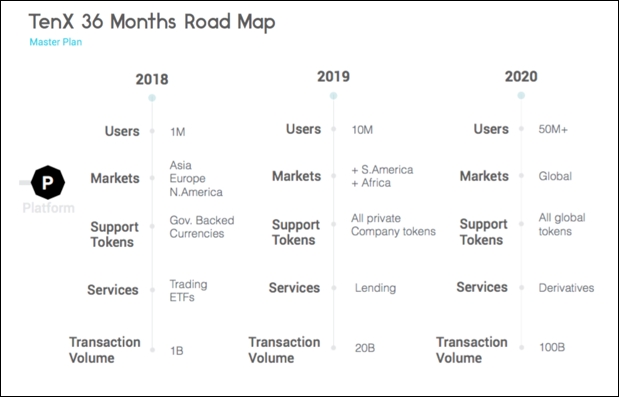

TenX, for example, gets full credit for providing a 12-month and a 36-month road map in its white paper, but looking at the projected growth rate of users, from one million in 2018 to 10 million 12 months later, and then 50 million in 2020, that is some projection. TenX raised $80 million USD and seems to have significant resources to execute its plan, but it doesn't take a rocket scientist to appreciate that out of all the many ICOs that make similar predictions, not all of them can come true, simply because not all projects can achieve 50 million users within three years.

Figure 13: TenX's ambitious 36-month roadmap

Essentially, it comes down to being able to deliver a conceptual idea within a timeline. This is not new. These ICOs are software projects with road maps, milestones, resource requirements, and a budget. What is new is the technology being deployed and in some cases the software language being used.

Speak to any software developer at the coalface of developing blockchain technologies, or smart contracts, and you will understand their frustration. An example includes removing certain functions and then delaying the updating of the documentation (https://github.com/ethereum/go-ethereum/issues/3793). This can set back even the best project with the best developers. New ICOs have caught onto this and designed platforms that use existing programming languages and technologies, making them interlocking in an effort to combat the yet-to-mature frameworks out there.

If software projects weren't already difficult to build, in the blockchain world they are made more challenging with the additional concept of economic incentive schemes, in the form of tokens, to incorporate into their design. In the future, programmers may need economics degrees to write software code, just like how lawyers may need to learn programming code to interpret smart contracts.

Logic would tell us that there are only so many loyalty tokens, so many provenance tracking systems tokens or so many personal identity tokens that the market can tolerate before saturation. The smart ones will pivot before saturation hits. The clever ones have already pivoted.

They have pivoted away from just providing a loyalty token, to providing a loyalty platform where loyalty tokens can be created in a very simple, non-technical drag-and-drop manner on the blockchain. However, even most of these will fail too. The reason being that the real innovation is yet to happen, as Mougayar succinctly summarizes:

"Tokens 1.0: copying what we see. Tokens 2.0: inventing what we don't see."

Take, for example, personal identity on the blockchain. How many personal identities will one have or need? The most logical answer is one. If there is more than one, say per country, then we may end up in a situation similar to that of instant messaging systems. WhatsApp, Skype, WeChat, Viber, Signal, Telegram, Messenger, Slack, LinkedIn Chat, and Google Chat are just a few of the chat services available. We are spoilt for choice and end up saturating our phones and scattering our time. At the moment, all we are doing is building and tokenizing existing systems as it is far easier to copy than to create. If these competing applications don't consume each other, the next big "killer app" that everyone is waiting for will.

Application saturation is not the only reason that many of the ICOs will fail. Communities are being saturated with marketing activities attempting to grow groups of supporters, programmers, and influencers. Large marketing budgets are typically set aside with bounties, which pay people to become supporters or to raise awareness. The company gets everyone excited about using its product on its blockchain. What tends to happen is that the fundamental technology seems to get lost in the noise and hype that is generated.

National or international "community managers" spend the marketing budget that was raised in the ICO to spread the good word in an evangelical manner, explaining why their blockchain platform is better. The fight for this territory will become fiercer because the space is becoming overcrowded.

The general concept of this theory is that there's always someone, an even greater fool, that will overpay for something, in this case ICO tokens, that are already overpriced. This can often be seen in a heated or overheated bull market.

Applying this to ICOs, many investors are blinded to the fundamentals and real value that an ICO provides by the marketing hype around how it will change the world. Everyone jumps on the ICO train with the belief not that the value of the technology will increase, but that the price of the token will increase based on media-announced partnerships. It has become a game that has shifted away from how the technology can change the trust relationship, to one of finding another buyer who will pay a higher price for the same token.

What lies in waiting is a bust, as highlighted earlier: a digital graveyard of broken promises, dormant or abandoned Twitter accounts, 404 page not found websites, and the remnants of chat logs in now-empty Telegram groups or Slack channels. Images of empty towns from old Wild West movies, with digital tumbleweed rolling by, come to mind.

In many ways, a clean out will be healthy in the ICO world. There is currently so much noise that it is hard to distinguish between the legitimate ones and the unscrupulous ones. The key to success, though, hasn't changed just because a new three-letter acronym has arrived in town. Business models need to be sound, continuous research, and innovation is required and having a solid team of people is, and always has been, key to any company's success.

ICOs may be a relatively new and complex phenomenon but with all the talk of doom and gloom, this hasn't prevented ICOs from continuing to innovate. There will be diamonds in the rough. There are two levels of innovation: firstly, the ICO mechanism itself and secondly, the blockchain-based technology where innovative products and services are created, with almost always a token in tow.

In fact, if you cast your mind back to March 2006, when Twitter first appeared on the scene, or even back to February 2004 if you are a Facebook fan, it wasn't until around three-to-four years later that these companies really found their groove and user adoption started. Now, Twitter and Facebook are household names worldwide.

Facebook and Twitter didn't have all the answers when they first started and neither do all these companies trying to tokenize everything in their path. However, the potential for a handful of companies somewhere out there to discover real applications is exciting. Whether it is through decentralized digital identity, the tokenization of all human interaction in a virtualized world or just the realization of Satoshi Nakamoto's original goal of a peer-to-peer electronic cash system, the future is there to be created.

ICOs, in the early days, only accepted bitcoins. Examples included Omni, Counterparty, Ethereum, and Factom. When ICOs started to be built on the Ethereum platform, it was only natural for ether to be included as a payment option.

Then there was a brief period where a multitude of cryptocurrencies were accepted, such as the TenX ICO where bitcoin, ether, litecoin, and dash were accepted. It quickly became a lot of work managing multiple cryptocurrency wallets, along with potential fluctuations in price. So, startups tended to generally opt for payments in ether in 2017. The price of bitcoin also saw large increases, which made people hold Bitcoins rather than spend them.

In the latter half of 2017, it became almost a game of who would take out top gong and raise the most money. Bancor raised the bar to $153 million USD in June, Tezos raised $233 million USD in July, and Filecoin took the cake for 2017 and raised $253 million USD in August. These ICOs will be analyzed in more detail in the next chapter.

For the Filecoin ICO, around $52 million USD was sold to private investors including Sequoia Capital, Andreessen Horowitz, and Union Square Ventures. Then, the next round was only to accredited investors. An accredited investor was deemed to have a net worth exceeding $1 million USD and/or the ability to demonstrate an annual income of over $200,000.

It then became evident that to raise hundreds of millions of dollars in an ICO, the ICO would have to be bolstered by some form of private money. This private pre-sale provided the added advantage that if well-known investors backed the ICO early, this was a positive signal for public investors.

This was particularly evident with Vitalik Buterin, where ICO projects would scramble to have his name associated with their projects. Only a handful succeeded, such as OmiseGo and Fenbushi Capital. OmiseGo also has a lot of other high-profile names endorsing it, such as Gavin Wood, the co-founder of Ethereum, and Joseph Poon, Plasma, and Lightning Network's co-author. Fenbushi Capital, on the other hand, invested in blockchain companies such as Bloq (enterprise grade blockchains), Filament (a decentralized Internet of Things platform), and Tierion (data verification on the blockchain).

Along with getting big names on board as advisors, and large upfront investments to signal the positive potential of the project, ICO smart contracts incorporated discounted token rates for investors. For example, participating in the pre-ICO would attract a 10% token bonus. Creativity was also extended to the price discovery method of determining a fair price of an ICO. A modified reverse Dutch auction was used by Gnosis (predictions market).

Some ICOs took on the challenge of doing a second round ICO, which currently is not standard practice. Storj (decentralized file storage) and Synereo (a blockchain-enabled attention economy solution) attempted this with interesting effects. Generally, ICOs should only perform an ICO once. The reason is that there is a common understanding that an ICO's token supply is known and that it is fixed. The belief is that with a limited supply, the value will increase over time.

Whether it is 100 million or one billion tokens, there will be no more. There are various ways around this however, such as creating a family or suite of products, and having an ICO for each of these, or creating a secondary token with a variable exchange rate to convert between the two tokens. Centrality had such a large demand that it provided a further announcement to its investors:

"After completely selling out our token in record time, we know that there are investors who missed out. We're now encouraging those with funds remaining in the Blockhaus sales app to leave them there, as the announcement of our next big token sale is only weeks away."

Although creativity, innovation, and a marketing story were required to increase the success of an ICO, the purpose of the ICO itself was where the real innovation took place. Many of these ICOs were presenting ideas that were very bold and grand, and this was observed across many different industries.

What is interesting to note, also, is that many of these concepts arose several years earlier when blockchain was the buzz. For example, Genomecoin, Healthcoins, Learncoin, Journalcoin, and Campuscoin are only a few mentioned in book Blockchain: Blueprint for a New Economy, Melanie Swan, first published in February 2015. While it may seem that the only thing that has changed is the word "coin" moving to "token", there is a lot more awareness of this industry, which has brought in a lot more ideas.

No matter where you are in the world, there is a constant battle to aggregate and integrate personal health data between all sorts of different health providers, so that there is a single view of patient information that is accurate, up to date, and reliable.

This means that information from your physiotherapist, your general practitioner, your hospital, and even your chiropractor can be stored on the blockchain, encrypted of course, and you are the only person that can access and allow access to that information.

Blockchain technology is the touted savior where this health information can be stored on a distributed and decentralized network. The difference now is that there is not a generic Healthcoin or even health token, but there are many tokens that have become very specific.

Patientory uses the blockchain along with its own specific token to secure medical records along with Medicalchain, Medibloc, and Solve.Care. There's Dentacoin, a blockchain solution for the global dental industry, MediShares for health insurance, and Nursetoken to apparently solve global nurse shortages. These are just a few random examples of the hundreds out there. This naturally leads to the question of digital identity.

There are ICOs that purport to be working on providing digital identity on the blockchain. This is where cryptography is used to create a super-secret password that only you know and then your personal data is attested by a third party.

A simple example would be your local birth, death, and marriage government department that would attest to your date of birth. In fact, one could foresee a future where the obstetricians or nurses could digitally attest the date and time of the delivery, along with even GPS coordinates, with their mobile device minutes after the actual delivery. This information could then be combined with your super-secret password and placed on the blockchain.

You would then control this data, deciding where, when, and who to release it to. To prove that you are over the minimum age to vote or to drive, you could show evidence by having a recognized third party attest that you meet the criteria, without having to reveal your date of birth.

A similar scenario can be walked through using your name. The difference with a name is that it can be changed at any point in time. This change can be recorded on the blockchain and because it is an update-only database, a record or digital paper trail will be available for audit purposes.

Digital identity can be taken a step further when combined with genomics, the science around the function, evolution, and mapping of genomes. Instead of a doctor stating the claim that your eyes are brown, blue, or green, this can be inferred directly from your genes. In fact, your genome, that is your complete set of genetic material that represents who you are, can be stored on a distributed and decentralized database where, again, you are the only person that can access the information or allow others to access it.

TheKey, Authorian, and KYC.Legal are again a random selection of the many companies out there that have a token that is required to be purchased to be used in their identity verification system.

There are also many examples of ICOs attempting to solve the "supply chain and provenance of food" problem on the blockchain. Many ask the questions: do you know where that piece of beef you had for dinner last night came from, or was the fish you bought sustainably caught? Existing systems can record this information, but are they trustworthy? Who is to know if the data was corrupted or, worse, doctored?

ShipChain, WaltonChain, SmartContainers, Ambrosus, and Sweetbridge are all building the so-called next evolution of logistics enabling privacy, scalability and security for the supply chain, unlocking the value trapped in assets, and payment delays, helping countries and individuals to find a better way to trade and innovate. Enterprises can eliminate traditional supply chain barriers and integrate actors big and small into an efficient, transparent, and secure global network.

The preceding description was a sentence taken from each of the above supply chain ICOs to highlight how many companies are working on very similar ideas in slightly different ways. This is a huge positive as long as there is collaboration and sharing involved. Let's hope that happens.

Energy is another large area where companies such as SolarCoin, Power Ledger, Grid+, and Global Grid are attempting to disrupt the energy market in energy trading, generation, transmission, and retail. Each ICO has its own token that will be used in its network to represent energy of some form, such as a watt (a unit of power) or even down to the electrons generated from a solar panel or wind farm. These tokens can then be used to represent the amount of energy generated and sold either directly to a consumer on a local micro-community grid or on a decentralized marketplace.

The energy concept can be taken a step further where electric vehicles can plug into a charging station and have tokens automatically transferred from their smart wallet to the wallet of the charging station provider. In fact, with induction charging of mobile phones, the kind where the phone charges simply by being placed on top of a surface, electric cars could be recharged while remaining stationary through a car wash. Tokens can be used as a form of payment, automatically, seamlessly, and even to the nearest minute.

It all seems very futuristic and like science fiction, but there is a prevailing pattern here. The potential of ICOs is tremendous because the tenet of the technology is to decentralize centralized systems and to provide a tokenized medium of exchange. The tokens can be used for anything valuable and exchangeable, therefore, no industry can hide from this innovative disruption. These ICOs are raising capital by creating tokens in a tokenized economy to build the next generation of "entities", that are vastly different to what we are used to.

The ICO phenomenon has sparked a creative and innovative flair in those young and old. The young are jumping in with naïve, but unlimited, energy and disrupting everything in their path, and the old are radiating caution and timing.

In this chapter, we learned what an ICO is and explained the concept of a token, along with some associated terminology. Several bitcoin bubbles were highlighted, only to discover that subsequent bubbles rendered the previous bubbles insignificant in comparison.

Several challenges were highlighted, such as the need for the development of infrastructure and increased education.

Finally, we learned about the new era of ICO innovation and what the future could bring.

Now that we have an insight into the potential of ICOs and blockchain technologies, we next look at the various token varieties and ICOs that have occurred over the past four years, starting with the very first one: Omni.