Nowadays, there are tokens everywhere, purporting to do everything from replicating loyalty programs and gaming credits, all the way to acting as payment systems within messaging apps and even using token platforms to create more tokens. There are a dizzying number of tokens available at present, all claiming to provide exceptional world-changing utility and value.

The question is: do these tokens really offer what they claim? In this chapter, we'll take a closer look at tokens, particularly:

- Tokens on the bitcoin blockchain (Omni/Counterparty)

- Tokens on custom blockchains (Nxt/Waves)

- Tokens on the Ethereum blockchain (Augur/ICONOMI)

- Tokens on non-blockchain technologies (IOTA/Hashgraph)

We'll take a step back in time to see how ICOs were done back in the good old days, on the good old original bitcoin blockchain, then on other blockchains such as Nxt and Waves, before jumping into the ever-popular Ethereum blockchain. We will also round off by introducing relatively new, non-blockchain technologies, such as IOTA and Hashgraph.

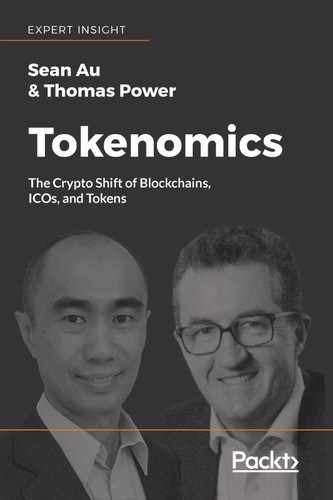

Before Ethereum existed, and ERC20 tokens were the buzzword, ICOs were known as crowdsales or fundraising events. Platforms based on the bitcoin blockchain were invented to enable the creation of tokens linked to a bitcoin address, much like how ERC20 tokens are linked to an Ethereum address. Omni (formerly known as MasterCoin) was such a platform. Counterparty was another and so was Factom.

Figure 1: Omni, Counterparty, and Factom were the early adopters that built on top of the bitcoin technology

These platforms also included rules or "protocols" on how other tokens could be created and are generally referred to as "protocols" for this reason.

Omni is an open-source, fully-decentralized asset platform on the bitcoin blockchain and was created by J.R. Willet when he published a paper in mid-2012 infamously titled The Second Bitcoin Whitepaper (https://github.com/OmniLayer/spec#development-mastercoins-dev-msc). Omni claimed in its white paper that the existing bitcoin network can be used as a protocol layer, on top of which new currency layers with new rules can be built without changing the foundation.

What this meant was that other currencies could be created using the Omni protocol that ran on the bitcoin blockchain. For example, to create a new currency, Omni stated that, The user must decide on the ticker symbol, a short name, a long name, a short URL pointing to more information about the currency along with various parameters governing the currency's behavior.

The goal of the fundraiser was stated in the Omni white paper: Initial distribution of MasterCoins will essentially be a fundraiser to provide money to pay developers to write the software which fully implements the protocol (https://e33ec872-a-62cb3a1a-s-sites.googlegroups.com/site/2ndbtcwpaper/MasterCoin%20Specification%201.1.pdf).

In July 2013, the fundraiser ended up collecting 5122 bitcoins, or the equivalent of $500K USD at the time, at the bitcoin exodus address 1EXoDusjGwvnjZUyKkxZ4UHEf77z6A5S4P. The exodus address was a play on the bitcoin genesis block terminology.

Tip

In ancient times, books were written on scrolls and were a standard size. Five of these scrolls were used to record the Torah, which is the basis of the Jewish religion and faith. The word genesis is the English translation of the title of the first scroll, meaning beginning. Exodus is the title of the second scroll, meaning leaving (in reference to the Jewish people leaving Egypt where they were slaves.

The initial 2012 white paper covered a stable coin concept, where a coin would be split into two components: a stable component and a volatile component. It also talked about conditional transfers and distributed exchanges. Interestingly, these concepts rose to popularity several years later, and now many companies are researching and experimenting with stable tokens, and more and more decentralized exchanges are coming to the market.

There was a section in the white paper titled The Trusted Entity that was about controlling the initial distribution of MasterCoins and the development of the software. It was later removed from the white paper but its presence can be seen in today's ICOs, as they are all governed by a trusted entity, whether they are companies, startups, or not-for-profit foundations.

The terms of the sale were that one bitcoin would obtain 100 MasterCoins. There was also a pre-sales bonus explained in the white paper:

"Early buyers get additional MasterCoins. In order to encourage adoption momentum, buyers will get an additional 10% bonus MasterCoins if they make their purchase a week before the deadline, 20% extra if they purchase two weeks early, and so on, including partial weeks. Thus, if I send 100 bitcoins to the exodus address 1.5 weeks before August 31st, the protocol recognizes my bitcoin address as owning 11,500 MasterCoins (10000 + 15% bonus)."

What made this a currency instead of a token, where all the supply was created at once, was that for every 10 MasterCoins sold, one additional Development MasterCoin called a Dev MSC was created. This would then be released into the system using the formula:

y represents the years since the sale of MasterCoins. This translates to 50% of the Dev MSC released into the supply after year one, 75% in year two and so on. This structure was used as an incentive for developers to continue to maintain, improve, and add features to the protocol and was controlled by the MasterCoin Foundation.

Typically, coins or tokens are created so that they can be used within a platform as a medium of exchange. However, because the MasterCoins idea was a protocol and MasterCoins (the coins) were sold as a means to fund the development of this protocol, you couldn't use MasterCoins (the coins) on the MasterCoin platform because it was a protocol. Confused? Let's explain that again using the new name, Omni.

So, because Omni was a protocol and not a platform, and MasterCoins were sold as a means to fund the development of Omni, you couldn't use MasterCoins anywhere, although they could be traded on an exchange back to USD. This is one of the reasons why Omni is not used anymore because digital assets without features tend to have no value. An interesting experimental proposed feature, though, is to use MasterCoins as an escrow fund to provide price stability for other coins built following the Omni protocol.

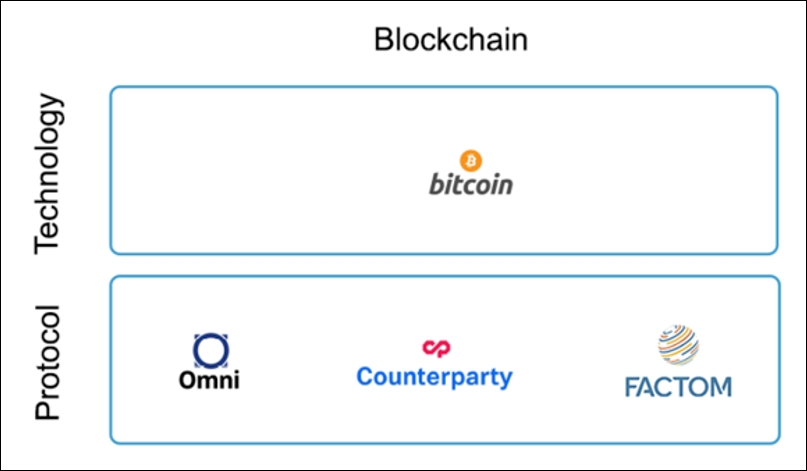

Omni's protocol was highly technical and knowledge of the inner workings of the bitcoin blockchain was required to create applications, that users could use to then create new currencies on. However, when the fundraiser opened a year later, and people actually sent Bitcoins, this was the response from J.R. Willet:

Figure 2: J.R. Willet's reaction when Bitcoins were first sent to his ICO (https://bitcointalk.org/index.php?topic=265488.msg2842681#msg2842681)

Another comment in the bitcointalk forum, one day into the fundraiser, noted:

"Wow you're [sic] funds have just shot up from 35 to 1,257 BTC while writing this so you must be doing something right!!" (https://bitcointalk.org/index.php?topic=265488.msg2847476#msg2847476).

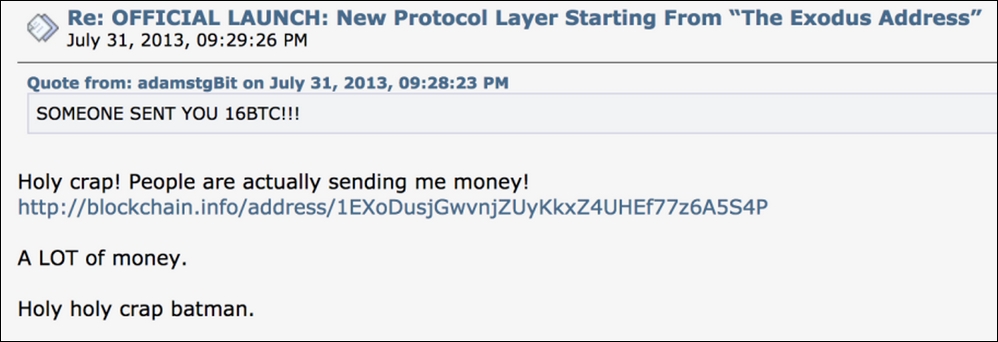

Omni was quite forward thinking at the time, considering that it was still early days in 2013, and a few other companies ended up using the platform to create tokens of their own. One of them was MaidSafe.

Figure 3: Tokens using the Omni platform and protocol

The vision of MaidSafe was to create a cheaper, more efficient, and more secure data-storage infrastructure for the internet. The company was founded in 2006 by Scottish engineer David Irvine and it was an acronym for "Massive Array of Internet Disks, Secure Access for Everyone." The project was ambitious and raising funds with an ICO was great timing because the company had a solid eight-year history, with almost $5 million USD in funding prior to the ICO. (https://metaquestions.me/2014/05/01/surviving-a-crowd-sale/).

The purpose of the Safecoin (SFE) was to access and utilize services on the SAFE network, such as storing data or making VoIP (Voice over Internet Protocol) calls.

The total number of Safecoins that could exist on the SAFE network was 232, or just under 4.3 billion. 5% was allocated to compensate early investors who backed the network over a long period of time, and only 10% was made available in the ICO.

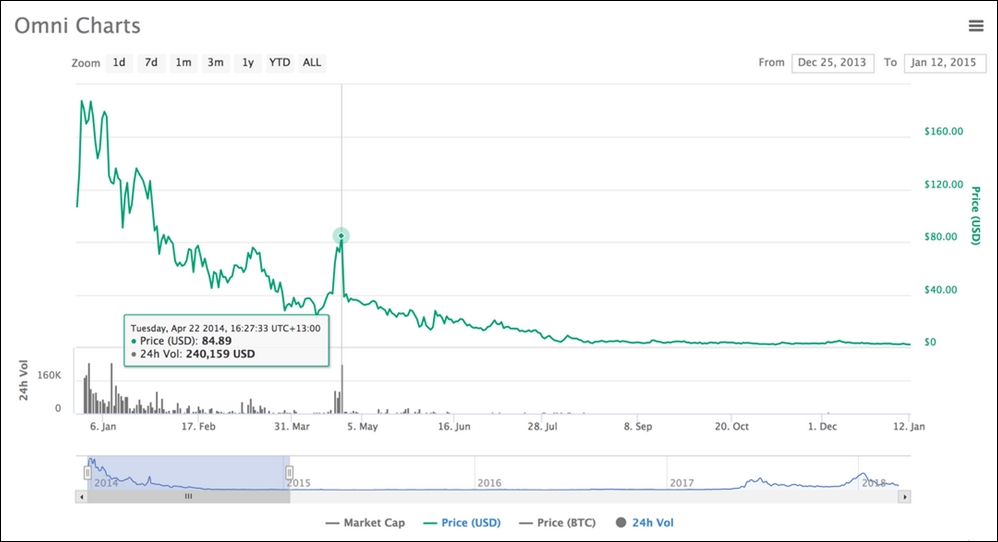

MaidSafe's ICO of Safecoin was launched in April 2014 and ended up raising $6 million USD in five hours, which was huge back in 2014 (https://blog.maidsafe.net/2014/04/23/maidsafe-sells-6-million-of-bitcoin-2-0-software-in-five-hours-press-release/). The MaidSafe team did overlook one small aspect. The original plan was to only accept MasterCoins for 10% of the crowdsale, since there was not much market liquidity for MasterCoins. Bitcoin would then make up the rest of the sale. The allocation of Bitcoins to Safecoins was 1:17,000 and MasterCoins to Safecoins was 1:3,400.

However, what MaidSafe didn't realize was that people could buy far more SafeCoin tokens if they paid with MasterCoins than if they paid with Bitcoins. This resulted in MaidSafe ending up with MasterCoins making up around 50% of the sales. The price of MasterCoins soared in the days leading up to the MaidSafe ICO. As soon as the ICO was over, the major source of demand for MasterCoins was suddenly gone, and the price collapsed.

Figure 4: The price crash of Omni immediately after the ICO [1]

Irvine stated:

"Ok it was over, we had screwed up and screwed all our supporters who were BTC holders. We had bet the business on this sale and spent months working towards it, sacrificing everything to make this happen."

(https://metaquestions.me/2014/05/01/surviving-a-crowd-sale/).

There are some valuable points to learn from the MaidSafe ICO. First of all, from Irvine:

"We knew MSC could be used directly and automatically issue MaidSafeCoins, this was how the protocol worked. This gave us cause for concern, but experts in the field reassured us the MSC part of sale would be minimal. This was comforting, but relied on us using advice and not setting a rule (this was our big mistake)."

(https://metaquestions.me/2014/05/01/surviving-a-crowd-sale/).

Nick Lambert, COO of MaidSafe noted:

"A lot of people questioned why we would use two currencies, and looking back we [should] have used one."

(https://www.coindesk.com/maidsafe-lessons-learned-crowdsale/).

In the end, Irvine said,

"So the oodles of cash, the pile of loot, what happens to that? This part is easy, it is much more equivalent to $3M in today's cash if we were to convert it, so there is a long-term position required. It will keep the MaidSafe staff paid and housed for three years as stated."

(https://metaquestions.me/2014/05/01/surviving-a-crowd-sale/).

MaidSafe ended up with anywhere around $3-6 million USD, according to various reports from its ICO. What the ICO did highlight, as explained on MaidSafe's website, was that things can still go wrong, even for a team of thinkers, inventors, tinkerers, PhDs, engineers, and designers (https://maidsafe.net/company.html).

Accepting two currencies made it more complicated and as noted above, taking advice and not setting a rule, that could have been incorporated into the code, meant that the balance of the two currencies was far from what was expected.

In mid-2014, a few months after MaidSafe's ICO, a company called Tether used the Omni platform to issue tokens. This was not a typical ICO, where one bitcoin could buy a set number of tokens with a goal of say $10 million to bring an idea to the market. It was simply an issue of Tether tokens at a one-to-one ratio for USD. This was called USDT (United States Dollar Tokens) and these US Tether tokens could then be used at various exchanges to purchase other cryptocurrencies.

The way that Tether worked was that instead of depositing USD into an exchange's bank account to buy bitcoin, users would deposit it into Tether's account. Tether would then issue USDT. The user would then send the USDT to the exchange and buy cryptocurrencies.

The exchanges liked this idea because it meant that they did not have to have a bank account. The risk of having a bank account is that there are a lot of regulations and compliance rules that need to be followed, and even if they are adhered to, there is nothing stopping the bank from changing its decision at any point in time, and shutting down the bank account.

Cryptopia, a cryptocurrency exchange based in New Zealand, experienced this first-hand when it was notified that its bank intended to close its New Zealand accounts. Cryptopia made a news announcement:

"Unfortunately, our current bank has notified us that they intend to close our NZDT account on 9 February. Due to this, we are announcing an immediate halt to NZDT deposits from COB today and we are asking all customers to cease sending NZD deposits to our NZDT account." (https://www.cryptopia.co.nz/News).

Tether sounded like a great idea, especially since on the website (www.tether.to) it states:

"Every Tether is always backed 1-to-1, by traditional currency held in our reserves. So 1 USD![]() is always equivalent to 1 USD… our reserve holdings are published daily and subject to frequent professional audits. All Tethers in circulation always match our reserves."

is always equivalent to 1 USD… our reserve holdings are published daily and subject to frequent professional audits. All Tethers in circulation always match our reserves."

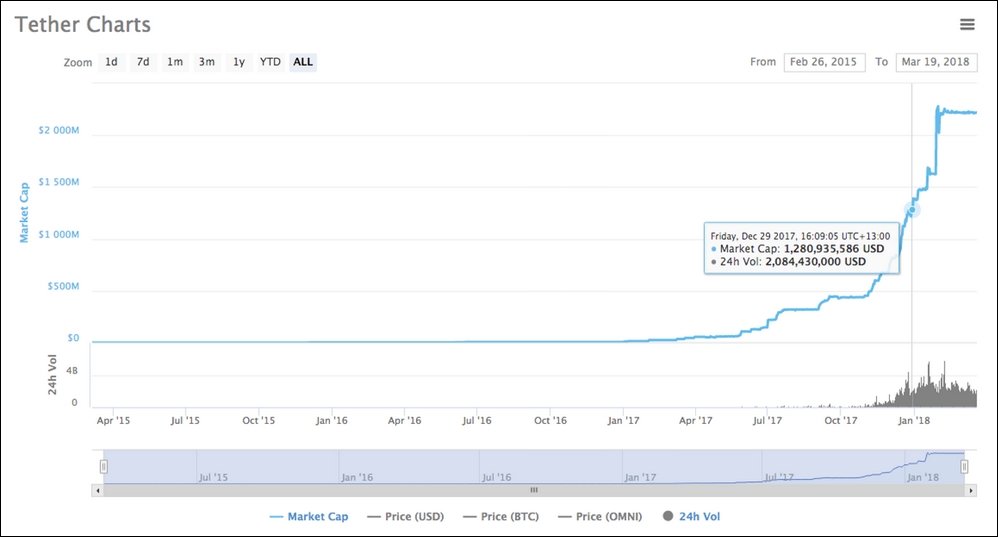

The challenge that Tether has is that the supply of Tether has skyrocketed from 14 million at the start of 2017, to 2.2 billion a year later:

Figure 5: The supply of Tether tokens has drastically increased [2]

In theory, then, Tether should have $2.2 billion in its bank accounts. Some people are questioning this and would like to see an audit to maintain confidence in Tether. Unfortunately, obtaining an audit is not as straightforward as one would think because large auditing firms are understandably cautious and risk adverse when putting their name and reputation on the line to support a cryptocurrency initiative.

There are also a number of other issues that cloud the Tether token. Tether and Bitfinex, one of the world's largest exchanges, appear to be closely associated with common shareholders and potentially the same CEO. Bitfinex and Tether have both been hacked in the past and some banking relationships have soured, for example with Wells Fargo (https://www.coindesk.com/bitfinex-tether-break-silence-go-media-offensive/). Having said this, though, this is not uncommon in the unregulated world of cryptocurrencies.

What Omni did was to provide a platform for innovation, but it wasn't the only one. Counterparty was another company that used the bitcoin blockchain and built a platform for others to create their own tokens.