CHAPTER 27

Human Resources Accounting

CHAPTER OBJECTIVES

After reading this chapter, you should be able to:

- List the objectives of human resource accounting

- Enumerate the methods to evaluate human resources

- Explain the strengths and weaknesses of human resources accounting

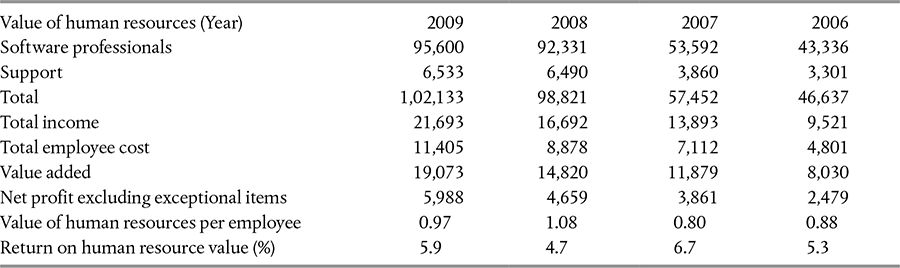

Infosys Technologies has made it a practice to publish the value of its human resources every year as a component of its annual report titled Human Resource Valuation. It introduced human resource accounting in 1995–96 and, thus, became the first software company in India to measure and publicize the value of its human resources. This company uses the Lev and Schwartz model to compute the value of its human resources. Infosys considers the current value of the future earnings of its employees for determining their value to the organization. The following points merit attention: (i) employee remuneration includes both direct and indirect benefits earned in India and abroad; (ii) the incremental earnings were computed on the basis of the age/group of the employees; and (iii) the future earnings of the employees would be converted into the present value with the help of the cost of capital. Based on its human valuation report (see Table 27.1), Infosys prepares unique HR-based ratios like total income/human resource value(ratio), employee cost/human resource value (%), and value added/human resources value (ratio) for making informed decisions. Having seen the importance of calculating the HR value of a company using human resource accounting, we shall now discuss the different aspects of human resource accounting in this chapter.

Introduction

The fundamental aim of human resource accounting is to assist the management in planning and controlling human resources in an effective way. In fact, human resource accounting is a strategic tool available with the management that is used to estimate the cost and value of its aggregate workforce. The role of HR accounting in organizations is to quantify the value of the human resources and is just like assessing the value of physical assets. When human assets are quantified in some form, it helps the organization in understanding the true worth of its human assets. Besides, the value of human resources estimated through human resource accounting becomes an important element of managerial decision making. The primary goals of human resource accounting are estimating the cost of each employee, the value of the total investment in human assets and, most importantly, the returns from human capital investments. Thus, human resource accounting helps the organization in knowing the “expected realizable value” of its employees. The determination of the value of human resources is influenced generally by factors like the compensation payable to the employees, promotability, skills and knowledge, age of retirement, and training opportunities available to the employees to acquire new abilities. As a matter of fact, the human resource accounting information is precious not only for management but also for external stakeholders like shareholders, creditors, and government agencies.1

In recent decades, human resource accounting has been gaining momentum in the business world due to the strong emergence of the service sector in the economy. The growing importance of human resources and the cost of their maintenance in these organizations prompted their managements to think seriously about human resource accounting. Of late, human resource accounting came to be viewed as a strategic tool to manage and control human resources effectively.2 Certainly, employees can also benefit out of human resource accounting because it helps the organizations recognize the skills, talents and knowledge of the employee and decide how to treat them appropriately. Even though human resource accounting is a relatively new concept in the industrial arena, it is capable of providing useful and relevant information required by the organizations to recruit, train, distribute, preserve, utilize, assess and compensate their human resources. In brief, human resource accounting facilitates the management in optimizing its human resources. The preparation of human resource accounting, however, is not statutory in the country and, as such, it is not recognized in the balance sheet of an organization. So far, human resource accounting has not succeeded in meeting the critical norms set by the generally accepted accounting principles (GAAP) to qualify as full-fledged accounting.

Estimating the value of human resources and ensuring their effective utilization are the essence of the definitions of human resource accounting. We shall now see a few of these definitions in Box 27.1.

We may define human resource accounting as a process of estimating the cost benefit of investments on human resources with a view to assessing their value to the organization.

Box 27.1

Definitions

“Human resource accounting is the process of identifying and measuring data about human resources and communicating this information to interested parties.”3

—American Accounting Association

“Human resource accounting is an attempt to identify and report investments made in human resources of an organisation that are presently not accounted for in conventional accounting practice.”4

—R. L. Woodruff Jr

“Operationally defined, (human resource accounting) means measuring the cost, replacement cost, and economic value of people as organizational resources for facilitating human resource management, decision making, and control as well as the reporting of human capital in financial statements.”5

—Michael R. Losey et al.

Objectives of Human Resource Accounting

Human resource accounting is capable of helping the management in various ways. For instance, it can support managerial decisions involving human resources allocation, projection and scheduling in the organization. This is possible because human resource accounting enables the management to assess the value of its human resources realistically. Thus, the general purpose of human resource accounting is to facilitate the managers in planning, supervising and controlling human resources in the most effective manner. In specific terms, human resource accounting aims to

- provide quantitative information about the cost and value of human resources available within the organization

- serve as a basis for decisions concerning the human resources of the organization

- facilitate the preparation of the human cost or budget for performing human resource functions like acquisition, development and compensation of employees

- provide methods and standards for evaluating the worth of people to the organization effectively

- help the management in monitoring the utility of human resources constantly with the purpose of achieving the optimum utilization of labour

- carry out planned and measured changes in the value of the human resources of an organization

- provide an early warning to the management about the impending changes in the value of the human resources. This should enable the organization to act adequately and appropriately to conserve its precious human resources.6

- enable the organization to reward the employees on the basis of the assessment of their values within the organization

- permit all the stakeholders of the business to have a fair knowledge of the value of the existing human resources

- help in the development of managerial principles and practices by clarifying the financial effects of various practices7

- enable the managers to have human resource perspectives in all their decisions by sharing numerical information about human resources8

Approaches to Human Resource Accounting

The traditional accounting practices simply ignored the value of human factors in the organization and preferred to treat it as an expense and expendable factors. This fundamentally lop-sided attitude towards human resources worked against the interest of the employees decisively. For instance, the cost of training incurred to update the skills and knowledge of the employees were treated only as expenses and not as investment.9 Although human resource accounting is still in its infancy as far as its development is concerned, there are a few approaches available to the study of human resource accounting. However, none of these approaches has so far found universal acceptance, because they have in-built contradictions, incompleteness or inability. These approaches have thus far failed to fulfil the basic requirements of traditional accounting concepts and practices like double-entry concept.

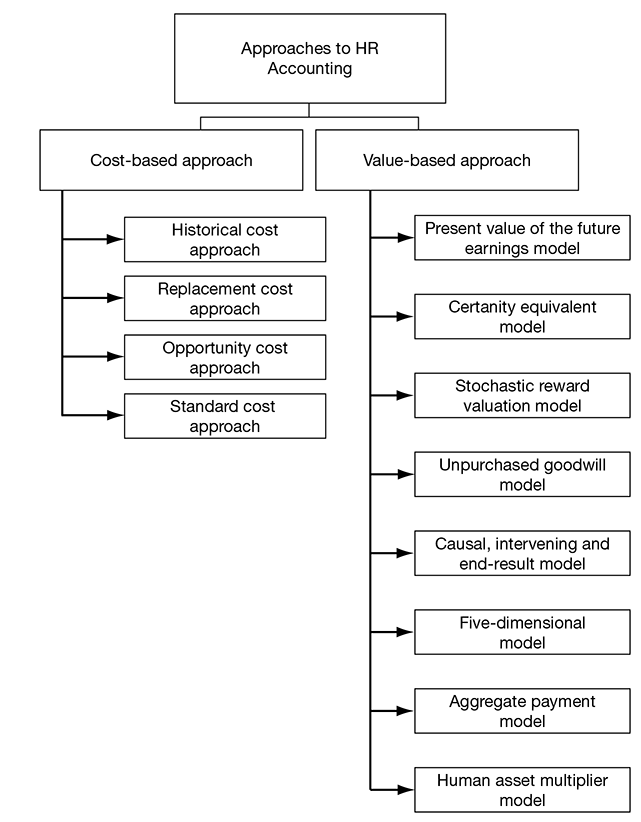

In spite of the inherent weaknesses in the measurement of human resources and in human resource accounting, a few experts have succeeded in developing logically sound and widely accepted approaches to human resource accounting (see Figure 27.1). These approaches are basically classified into cost-based and value-based approaches. The cost-based approach focuses on the cost of procurement of human resources, treating it similar to the historical cost of physical assets. This approach can also include the replacement cost or opportunity cost. On the other hand, the value-based approach to human resource accounting focuses on the income-earning capacity of the human resources. This is normally related to the future earnings of the organization received through human resources. We shall now see these approaches in detail.

Cost-based Approach

This approach is also called human resource cost accounting (HRCA). It operates like a traditional financial accounting system. It assumes that the value of a human asset can be estimated properly through the historical (past) investment or cost incurred. There are four important cost concepts available to measure the cost of human assets: (i) historical cost, (ii) replacement cost, (iii) opportunity cost and (iv) standard cost. We shall now see these cost concepts in detail.

Historical Cost Approach This approach was developed by Lee Brummet, Eric Flamholtz and William C. Pyle.10 According to this approach, the cost incurred for recruiting, training and developing the employees should be capitalized (converting the expenses into capital investment or asset). The total amount capitalized is then amortized (gradually reduced) over the estimated useful life of the human resources. This approach is similar to the accounting treatment of any physical asset in which the cost of an expired portion of an asset is written off from the assets as an expense. Unlike the physical asset, the acquisition cost of human assets is incurred gradually over a period of time and then aggregated to identify the historical cost of that asset. Then, a specific proportion of the historical cost of the human asset is written off every year throughout the life of that person in the organization as an expense against the income earned during that year. We shall now see a simple numerical example with imaginary data for a better understanding of this concept.

Let us assume that the useful life of this employee in the organization is 10 years.

If the capitalized value of the employee is Rs 700, 000 and his estimated life in the organization is 10 years, the annual amortization would be ![]() per year.

per year.

Thus Rs 70,000 per year ought to be deducted from the profit earned by the organization.

In case the employee leaves the organization prematurely, the entire balance amount in the account is treated as an expense and written off completely. The important pre requisite for the historical cost approach is the systematic and objective recording of each cost associated with the procurement and development of human resources.

The merit of this method is that it is simple to understand and easy to operate since it is mostly akin to the traditional accounting treatment of physical assets. However, there are a few major limitations seen in this method. These are: (i) This method is subjective and haphazard since it involves several tough estimations. For instance, it involves the estimation of the life of a human asset in the organization. This is very difficult as human beings can act independent of the organization on matters like their premature exit from the organization for personal or professional reasons. (ii) It ignores the basic characteristic of a human asset. A human asset is the only asset that appreciates over a period of time; all other assets just depreciate. An identical accounting treatment of two contrasting nature of assets cannot be justified. (iii) This method suffers from all the weaknesses of the historical cost method of financial accounting like the non-consideration or non-inclusion of the inflationary cost in the books, the irrelevance of historical cost for future purchases, and so on.

| Historical Cost of an Employee X (all values in Rs) | |

| Cost of recruitment | 200,000 |

| Cost of training | 300,000 |

| Cost of informal training (for example, the loss suffered by the organization due to faulty decisions made by the employee at the initial stage of employment) | 200,000 |

| Capitalized value of the employee | 700,000 |

Replacement Cost Approach The major contributors to this approach are Rensis Likert and Eric G. Flamholtz.11 The aim of this approach is to suggest a more realistic accounting treatment to value the cost of an asset. This approach considers the aggregate cost of recruiting, training and developing persons as suitable replacements for the existing levels of expertise and experience available with the organization. The replacement approach can be classified further into personal and positional replacement.

Personnel replacement— When the cost of replacing an incumbent (job holder) in a specific position of the organization is considered, it is known as a personnel replacement. In this case, the person who acts as a replacement should have all the skills and abilities possessed by the incumbent employee, irrespective of its direct relevance for the present job. This implies that even if the skills and abilities of the present incumbent are more than the job requirement, the replacements ought to possess all those skills and abilities.

Positional replacement— In case of a positional replacement approach, only the exact skills and knowledge required for the job performance is considered. Obviously, this method does not take into account the other skills and abilities possessed by the position holder.

The major merit of the replacement cost approach is that it is surely more practical and logical than the historical replacement cost approach. The limitations of this approach are: (i) It is a vague method since finding a similar replacement for a person or position is very difficult. (ii) The process of cost determination would be arbitrary since it is not possible to fix the future value of human assets objectively.

Opportunity Cost Approach This method was introduced by Hekimian and Jones.12 According to this approach, an opportunity cost exists for all human resources that are in short supply. Basically, any decision that involves a choice from more than one alternative has an opportunity cost. This can be easily understood through a simple example. When an employee decides to resign his present job to pursue higher studies, he should consider not only the expenses (like fees) for the higher studies but also the salary loss due to leaving the present job. Thus, when he makes decision about his future course of action, he must consider both the costs. Clearly, the sacrifices made for choosing a decision are called the opportunity cost. However, there is no opportunity cost for any decision which has no alternatives. In human resource accounting, the opportunity cost arises for an employee when his services are required or bidden for by many divisional heads of a company. Thus, when divisional heads bid for the services of people whose talents are scarce, they may include a bid price for these people in the total investments for the division. Let us see a numerical example for opportunity cost.

A company has invested Rs 4,000,000 in Division X for its operations and it expects the department to achieve a normal return of 16 per cent from its performance. However, the division at present could make a profit of only Rs 600,000 instead of the normal profit of Rs 640,000 (16% of Rs. 4,000,000). Now, the head of the division plans to improve the situation by requisitioning the services of a talented technocrat. The department head estimates a revised profit of Rs 720,000 for the department—an increase of Rs 80,000 more than the normal return. In this situation, the department head can safely conclude that the profit of Rs 80,000 is just due to the capability of the technocrat. As such, the department can fix the HR value of the technocrat at Rs 500,000 (80,000 × 100/16) by capitalizing the excess profit Rs 80,000 at 16 per cent. Finally, the HR value of the technocrat would be included with the investment base of the division.

The merit of this method is that it provides a quantitative approach to the concept of human resource management. It also ensures the optimal allocation of scarce human resources. However, it has a few limitations. These are: (i) This approach is suitable mostly for people at the middle-level management but their services may not be available for auction. (ii) There is no guarantee that a person who performs well in one division or department can repeat the same performance in other departments. (iii) Since this approach discriminates between the employees on the basis of some vague concept, there is a possibility that it can demoralize the other employees and depress their performance. This can eventually neutralize the performance improvements achieved by the expert employees.

Standard Costing Approach This approach was advocated by David Watson. As per this approach, human resource data is used for setting standard costs for various HR functions like hiring and training.13 In fact, standard costing is usually determined every year. In this method, employees of an organization are first classified into different groups/grades based on their hierarchical position. Then, the standard cost is fixed for each grade of employees and their value ascertained. For instance, an organization may decide the standard recruiting cost per grade of employees for a specific year and this may act as a cost guideline for all recruitments in that specific grade. Further, in the subsequent years, the standard cost may be revised depending upon the prevailing conditions. The aggregate standard cost computed for the entire workforce is regarded as the human resources value of the whole organization. This approach is obviously simple to understand and easy to operate. But the major limitation of this method is that it lacks objectivity in estimating the standard costing for human resources. Besides, determining the standard cost for every grade is a complex and time-consuming process.

Value-based Approach

According to the value-based approach, the value of human resources depends primarily on its ability to generate revenues. The major difference between the cost-based and the value-based approach is that the former focuses mainly on the total cost incurred by the organization in hiring and training employees, while the latter does not make much reference to the historic cost but emphasizes more on the future earning capacity of the human assets. Since the valuation approach is based more on the conceptual proposals, it is difficult to practise it in real circumstances due to the complexities involved.14 The important human resources valuation models used for measuring the value of human resources are (i) the present value of future earnings model, (ii) the certainty equivalent model, (iii) the stochastic reward valuation model, (iv) the human asset multiplier model, (v) the unpurchased goodwill model, (vi) the causal, intervening and end-result model, (vii) the five-dimensional model, and (viii) the aggregate payment model. We shall now discuss these HR valuation models.

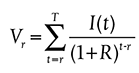

The Present Value of Future Earnings Model This model for measuring the value of human resources was advocated by Brauch Lev and Aba Schwartz 15 According to this model, the value of human resources depends on the present value of the future earnings to be made from a person’s employment. It depends on the economic concept of human capital. Actually, this model aggregates the estimated present value of the future income of an employee from his remaining service after adjusting for the possibility of premature death or permanent disability. Lev and Schwartz suggest the following formula for computing the valuation of human resources.

where Vr = the value of an individual who is r years old

I(t) = the individual’s annual earnings up to his retirement

T = the retirement age

R = the discount rate

r = the present age of the individual

According to this model, the remaining years of service of an employee is critical in determining his value in the organization. However, this model has quite a few limitations. These are: (i) It ignores the role and authority of the organization in deciding how the employee should be used in it. As such, the value of an employee cannot be measured merely by qualities and skills possessed by him but also by the opportunities available to utilize those skills in the organization effectively. (ii) It fails to adequately consider the prospects of employees leaving the organizations early for personal or professional reasons. (iii) It ignores the likelihood of job changes like promotions, and transfers in the career of employees, which may affect their earnings.

Box 27.2 indicates the example of companies that practice human resource accounting.

The Certainty Equivalent Model The proponent of this method is Pekin Ogan.16 The two major components of this method are (a) the net benefit and (b) the certainty factor, which provide the means for determining the net present value of the human resources. According to this model, the net benefit is the difference between the total investment made by the organization in acquiring, training, developing, integrating and maintaining the employees and the total benefits received out of the skills, ability and knowledge of those employees. Net benefit = (the total investment in hiring, training, developing, and maintaining the employees) – (the total benefits received out of their skills, ability and knowledge)

Further, this model views compensation policies, promotion policies, industry averages, labour market conditions and the skill requirements of an organization as the major determinants of the cost of human resources. Similarly, factors like employees’ age and the remaining years of service, their educational levels and their performance levels influence the benefits available from the employees. However, the uniqueness of this model is its certainty equivalent component. Certainty equivalent is classified into two categories—the probability of an employee’s continued employment in the organization and the probability of his physical survival. The probability of continued employment is influenced by his total satisfaction and his attitude towards changes. According to Ogan, the quantified variable of this model can be used to compute the current equivalent of net benefits.

Box 27.2

Human Resource Accounting: Still in its Infancy

Over the years, Indian companies have gradually been transforming their traditionally undervalued human resources into the core assets of their organization. This is due to the growing realization among the top managers that the physical assets hardly make any remarkable differences to the performance and future prospects of modern-day organizations. They also understand that contemporary knowledgeable employees enjoying a high degree of independence and mobility can make or mar the fortune of their business through their attitude and actions. It has thus become a necessity for the success-hungry management to evolve tailor-made and robust HR policies and practices to keep these care-free employees tied to the organization. In fact, the emergence of knowledge industries like IT has further augmented the position of the human resources in the organization. Apparently, the requirements for individual-specific HR policies compelled organizations to identify the value of each employee for their organization so that it manages cost-benefit analysis in its employee retention initiatives. In this regard, quite a few organizations consider human resource accounting as a realistic and strategic tool to assess the real worth of the employees.

Some organizations in India have already begun the practice of human resource valuation and also published reports about the value of their human resources. For instance, BHEL, Infosys, SBI, Reliance industries, Steel Authority of India Limited, Indian Oil Corporation, Cement Corporation of India limited, State Trading Corporation, Southern Petrochemical Industries Corporation Limited (SPIC), Mineral and Metal Trading Corporation of India (MMTC), Oil and Natural Gas Commission (ONGC), National Thermal Power Corporation Limited (NTPC) and Engineers India Limited (EIL) have evaluated their employees and made the results known to the public. Among these companies, BHEL was a pioneering company in introducing the human resources accounting system in India in 1974–75. Interestingly, most of these companies used the Lev and Schwartz model to compute the value of human resources in their organizations.

Adapted from R. K. Malik, Human Resource Accounting and Decision-making (Delhi: Anmol Publications,1993), p.5; and www.indianmba.com/Faculty_Column/FC766/fc766.html.

The Stochastic Reward Valuation Model (SRVM) This model was originally developed by Eric Flamholtz.17 According to this model, the process of fixing the value of an employee depends upon the variability of that person from four different perspectives and potentialities. These are: (i) productivity, (ii) promotability, (iii) transferability, and (iv) retainability.18 This model perceives that the value of an employee depends upon the value of each of these factors or positions connected with that person. However, the chances of the employee being in any of these positions (service states) depend on the law of probability. According to Flamholtz, this reward model can help the organization in deciding (i) an employee’s estimated tenure in the organization, (ii) the mutually exclusive position like productivity and transferability that an employee is likely to occupy, (iii) the value of each position to the organization, and (iv) the probability that the employee would occupy a position at some time in the future.19

This method has several limitations. These are: (i) The organization may find it hard to get specific and reliable data about the value derived by the organization when the employee occupies a specific position in a very uncertain future period. (ii) The performance of an employee as an individual might be different from the performance of the employee as part of a group. This factor is not considered in this model at all.

The Human Asset Multiplier model This method was advocated by W. J. Giles and D. F. Robinson.20 According to this approach, the valuation of human resources is normally made in the same way as other business assets are valued on a “going concern concept” basis. The “going concern concept” assumes that the organization would continue to function for an infinite period of time. In this regard, Giles and Robinson developed a human asset multiplier, which is applied on the gross remuneration of employees. This average multiplier is obtained from a financial formula which is based on the market value of the organization.21 These multipliers are then weighted for different grades of employees. In this regard, employees’ age, experience, qualifications, expertise, commitment, performance and promotion capabilities, replacement scarcity and the remaining period of services are used as weights. The gross value of the human resources of an organization can be computed by just totalling all the individual values calculated separately.

The Unpurchased Goodwill Model The proponent of this method is Roger H. Hermanson.22 According to this method, the organization must ascertain its actual earnings and average it for the past few years. It should then identify the normal rate of return of the industry to which the organization belongs. In the next step, the organization must make a comparison between its actual average earnings and the normal earnings of the industry. In case the actual earnings are more than the normal earnings of the industry, the difference is known as super profit earned by the organization. When this super profit is capitalized with the help of the normal rate of return of the industry, the capitalized amount can be treated as the value of the human resources. This can be explained through a numerical example. Let us say:

The actual capital invested by the organization is Rs 1,000,000. The normal rate of return of the industry is 16 per cent. The actual average earnings of the organization is Rs 280,000.

We shall first find out the normal earnings of the industry.

Step 1: The normal earnings of the industry is 1,000,000 × 16 = Rs. 160,000

Step 2: The super profit (excess profit) of the organization = Rs. 280,000 − Rs. 160,000 = Rs. 120,000

Step 3: Capitalization of super profit = Rs. 120,000 × 100/16 = Rs. 7,50,000

Now the human resource value of the organization is Rs. 750,000.

Thus, the human resource value of the organization—Rs. 750,000—can be added to the existing capital of Rs 1,000,000. Then, the total value of the organization would be Rs. 1,750,000, of which human capital alone constitutes Rs 750,000. The major limitations of this method are: (i) It is based on the historical values which may affect the accuracy of the future predictions. (ii) It assumes that the entire super profit is earned out of the human resources and completely ignores the role of physical assets, which is a fallacy.

The Causal, Intervening, and End-result Model This model was introduced by Rensis Likert and David G. Bowers.23 They advocated the need to develop a participative approach to human resource management. According to them, the development of the participative approach required the introduction of a new organizational structure and style of management behaviour. These are called as causal variables. The result of changes in the organizational structure and style of management behaviour would be an increase in productivity and performance and a decrease in cost and scrap levels. The ultimate outcome of the change would be increased earnings for the organization. These outcomes are called end-result variables. Likert also contends that there are a few critical variables that function in between the causal and end-result variables. These variables are normally called intervening variables. These variables are employees’ attitude, motivation, perceptions, job satisfaction and goals-oriented behaviour. According to Likert and Bowers, any change in causal variables affects the intervening variables and the net effect of these changes would be known through the end-result variables.24 The main limitation of this method is that it is suitable for interactive conditions and not for individual capabilities.

The Five-dimensional Model This model was advocated by Myers and Flowers.25 According to this approach, the five dimensions of workforce determine the value of human resources critically and collectively. These five dimensions of the employees are (i) knowledge, (ii) skills, (iii) health, (iv) availability, and (v) attitudes. These dimensions are factoral (core factors) in nature and not additive. Since the value of human resources is the collective outcome of all these factors, even if one factor is not performing effectively, the other factors would also become proportionately ineffective. This means all aspects of an employee must be taken care of adequately by the organization for enhancing the value of the employees. If an employee is highly skilled but keeps poor health and is frequently absent, then the skills’ levels of the employee can not make the desired impact on the value of the employees unless his health condition improves substantially. Thus, the organization must focus on all the five dimensions to ensure that the employees’ contribution is effective and the value of the human resources is substantial.

Aggregate Payment Model This model was developed by S. K. Chakraborty,26 who suggests that the capital base of an organisation should include the value of human assets. According to this method, the value of human resources is the function of the average salary of the employees and their average employment tenure in the organization. The model suggests that the ideal mode of identifying the value of human resources is group valuation and not individual valuation.

A few steps in this model are: (i) segregation of employees into groups, (ii) ascertaining the average salary of the employees of each group on the basis of the wage structure and/or pay scales, and (iii) measuring the average tenure of the employees based on past experiences. The employee turnover rate and other relevant labour records can be used to estimate the average tenure of the employees in the organization. Now, the average salary is multiplied by the average tenure of the employees to know the gross value of the human resources of the group. Finally, the gross value is discounted at the expected average after the tax return on capital that was employed to know the present value of the human resources.

Uses of Human Resource Accounting

Human resource accounting has formed the basis for the assessment of the efficacy of human resource management. The primary use of human resource accounting is the assignment of a quantitative value to the human resources. It helps the organization in measuring the abilities of employees working at different levels so that it can ascertain the value of its human resources. Though there is no universal recognition for theories and practices associated with human resource accounting, it indeed helps the organization in several ways. We shall now see the important uses of human resource accounting in the field of human resource management.

- Human resource accounting helps the organization in identifying the changes occurring in human resources over a period of time and its impact on the value of those human resources. In fact, the organization can determine the cost of labour turnover through changes in the value of human resources.27

- It facilitates the organization in keeping track of the investment made in its human resources and the likely cost of their replacement in the future.

- It provides useful information to the management for determining HR activities like manpower planning, recruitment planning, training and development planning, and career and succession planning in a cost-effective way.

- It enables the organization to evaluate the returns earned from the investment made on the individual employees. It also enables it to understand the problems of human resource management better.

- It helps the organization allocate the human resources to its various activities properly and thereby ensures the optimum utilization of the available human resources.

- It helps the organization identify and retain the high-value employees by offering them better facilities and emoluments.

- It assists the organization in measuring the worth of the money spent on HR functions like training programmes to decide about continuing them in the future. Indeed, human resource accounting records the improvements in the value of the employees periodically. Any recorded difference can be attributed to skill acquisition by the employee through the training and development programmes.

- Human resource accounting helps the organization proclaim the value of its human resources confidently. When the HR accounts indicate high values for human resources, it obviously implies the existence of excellent HR philosophy, policies and practices in the organization. This may help the organization earn goodwill in the labour market.

- Human resource accounting enables the employees to possess the feeling of self-worth whey they become aware of their value to the organization. Thus, it helps the firm improve employee motivation and morale.

- When the managers are aware of the worth of their subordinates, they would provide due respect and recognition to them. Further, the availability of quantitative data about the employees would enable the managers to have an employee perspective in the decision-making process. They would also change their perception about the employees from being a replaceable expense to an invaluable resource.

- Human resource accounting helps external stakeholders like shareholders, creditors and other agencies make a comprehensive assessment of the worth and performance of the human resources in the organization.

Weaknesses of Human Resource Accounting

In many organizations, the importance of capital shifts gradually from the financial capital to intellectual capital. This has necessitated the development of an accounting system to measure the value of the human resources and distinguish the high-value employees from others. However, the efforts to make a universally acceptable system have not succeeded due to the inherent weaknesses of the existing systems of accounting. Even the generally accepted accounting principles (GAAP), which issue the standard framework of guidelines for financial accounting, does not recognize human capital in the financial books. It continues to treat the expenses on employees as expense only and not as capital. Due to this trend, the organizational expenditure on human resources, like training and develop ment and compensation only pushes up the expenses and brings down the income of the organization proportionately.

So far, the generally accepted accounting principles (GAAP) have declined to treat the expenses on human resources as capital investment for a few solid reasons. These reasons are: (i) violation of conservatism concept, (ii) an uncertainty about the future benefits, and (iii) the absence of initial investment in the acquisition of human assets. We shall now see a few other weaknesses of human resource accounting.

Lack of Real Ownership

Unlike other resources, the human resources can not be owned by the employers physically. When there is no ownership, these cannot be claimed as an asset by the employers.

Lack of Guiding Principles, Concepts, Conventions and a Regulatory Body

Unlike financial accounting, human resources accounting is not regulated by any authority, principles, conventions or concepts. In the absence of concepts and principles, it is difficult to develop a universally acceptable human resource accounting model that complies with the requirement of objectivity, validity and reliability.28 As such, there is no universally accepted method of valuing the available human resources.

Lack of Recognition by the Tax Authorities

So far, the tax authorities have not recognized human resource accounting and its assumption that the money spent on employees is a capital acquisition by an organization. It is still viewed only as expenses.

Possible Opposition from Employees and their Union

Human resource accounting leads to the possibility of discrimination between employees on the basis of their values determined by the management. There is a possibility of employees being exploited by low salary being offered to those who fare poorly in the accounting estimation. Consequently, human resource accounting has been opposed strongly by many trade unions and sections of the employees.

Absence of Adequate Awareness and Research

Since human resource accounting has no direct relevance and immediate necessity, organizations have not devoted adequate attention to developing it as a full-fledged and viable concept. Similarly, organizations have not cared to provide wide publicity to human resource data. Companies take too little initiative to inform their shareholders and the general public about the value of their human resources.29

Summary

- Human resource accounting is the process of estimating the cost benefit of investments on human resources with a view to assessing its value to the organization.

- There are two approaches to the study of human resource accounting: cost-based approach and value-based approach.

- The cost-based approach includes (i) historical cost, (ii) replacement cost, (iii) opportunity cost, and (iv) standard cost.

- As per the historical cost approach, the value of HR is the cumulative cost incurred on recruiting, training and developing the employees.

- As per the replacement cost approach, the value of HR means the aggregate cost of recruiting, training and developing persons as suitable replacements.

- As per the opportunity cost approach, the value of HR calculates the sacrifices made for choosing a decision pertaining to human resources.

- According to the standard costing approach, the value of HR is the standard cost fixed for various HR functions like hiring and training.

- The value-based approach includes (i) the present value of future earnings model, (ii) the certainty equivalent model, (iii) the reward valuation model, (iv) the human asset multiplier model, (v) the unpurchased goodwill model, (vi) the causal, intervening, and end-result model, (vii) the five- dimensional model, and (viii) the aggregate payment model.

- According to the present value of future earnings model, the value of human resources depends on the present value of the future earnings to be made from a person’s employment.

- The certainty equivalent model has two major components: (a) the net benefit and (b) the certainty factor.

- The stochastic reward valuation model perceives that the value of an employee depends upon the variability of that person from four different perspectives and potentialities.

- According to the human asset multiplier approach, the valuation of human resources is normally made in the same way as other business assets are valued on a “going concern concept” basis.

- As per the unpurchased goodwill model, the value of HR is the capitalized value of the difference between the actual average earnings and the normal earnings of the industry.

- As per the causal, intervening, and end-result model, the purpose of human resource accounting is to measure the causal and intervening variables in some way so as to measure the value of the human resources.

- The five dimensions which determine HR value are (i) knowledge, (ii) skills, (iii) health, (iv) availability, and (v) attitude.

- According to the aggregate payment model, the value of human resources is the function of the average salary of the employees and their average employment tenure in the organization.

- The weaknesses of human resource accounting are: lack of real ownership, lack of guiding principles, concepts, conventions and a regulatory body, lack of recognition by tax authorities, possible opposition from employees and their union, and the absence of adequate awareness and research.

Review Questions

Essay-type questions

- Explain the meaning, objectives and importance of human resource accounting critically.

- Discuss the cost-based approaches to human resource accounting using relevant examples.

- Enumerate the value approaches to human resource accounting using suitable examples.

- Describe the strengths and weaknesses of human resource accounting.

- “Human resource accounting system is an inevitable tool for the future.” Discuss.

- Enunciate the role of human resource accounting in Indian industrial organizations.

Skill-development Exercise

Objective – The objective of this exercise is to show you how to plan and choose a human resource accounting model to assess the value of the human resources

Procedure Note – The class is divided into groups. Every group has (1) an HR manager, (2) an external HRA expert, (3) two high-level office-bearers of a trade union and (4) two observers of the interview. The primary role of the observers is to analyse the various aspects of the role-playing session and provide their feedback.

Situation

Windsurf Limited is an automobile company engaged in the production of car accessories and spares. It is a major supplier of auto components to almost all leading car manufacturers of the country. It produces several auto accessories like the car alarm, car glass, wing mirror and power steering.

The board of directors of this company recently approved a major proposal to acquire a rival accessories manufacturer, Gentech Limited, as part of a horizontal integration process. An expert panel appointed by Windsurf Limited to evaluate the acquisition proposal recommended the assessment of the value of human resources of not only the transferor company, Gentech Limited, but also of that of Windsurf Limited. They suggested that both evaluations must be done before the acquisition in order to have a synergy effect upon acquisition. The management of Windsurf Limited accepted the recommendation and instructed its HR department to assess the value of the workforce though an appropriate human resource accounting model. For this purpose, the top management permitted the HR department to requisition the services of the external experts.

Steps in the exercise

There are four steps in the exercise:

Step 1: The HR manager meets the office-bearers of the trade union to ascertain their views on human resource accounting and explain to them the need for fixing values for the employees.

Step 2: He contacts the external expert to discuss and decide about the appropriate human resource accounting model and implementation strategy.

Step 3: He convenes a meeting of his HR team to choose the human resource accounting model after due consideration of the relevant reports and guidelines.

Step 4: The observers analyse the performance of the members in the role-playing session and give their feedback.

Case Study

Genfox Pharmaceutical Company is a fully integrated pharmaceutical company in India. This company is a fast-emerging global pharmaceutical with its production capabilities located in three countries and its markets across nearly 21 countries. Its HR department is headed by Mr Sunil Kumar. Genfox maintains harmonious industrial relations and a labour turnover rate of 4 per cent, which is well within the industry average of 7 per cent. Recently, however, Mr Rajnath Hegde joined as the Vice-President (General) of the company, and the HR department, along with a few other departments, was brought under his control. After joining the company, he conducted a review of the all the departments which came under his jurisdiction. In a subsequent meeting with the general managers, he shared his impressions of their departments. The Vice-President made a critical observation about the prevailing rate of labour turnover. He observed that the labour turnover of 4 per cent could not be considered an indication of good labour practices even if it was nearly half of the industry average. He further observed that a fair conclusion about employee turnover can be made only when the cost of labour turnover is assessed and insisted on the human resource accounting process to assess the value of the employees and also the value of those who had just left the organization. He also dwelt at length on the virtues of human resource accounting and on the need for annual assessment of the employees.

However, the GM (HR) differed with the contention of the vice-president. He insisted that the percentage of employee turnover was a fairly good indicator of the performance of the HR department and claimed that the organization had a consistently positive report regarding labour turnover. But, Hegde overruled the objections of the GM (HR) and instructed the HR department to undertake human resource accounting to know the value of the employees in general and that of the just- resigned employees in particular. He also generally supervised the entire human resource accounting activities. The organization applied the Lev and Schwartz model to determine the worth of the existing and the former employees. The results made startling revelations about the cost of labour turnover. The report showed that though the overall percentage of labour turnover for the organization was low and well within the industry average, several high-value employees had left the organization in recent times. It also found the cost of replacement for these employees to be very high. Mr Hegde discussed the matter with Mr Sunil Kumar and sought his opinion about the developments. He also asked him to explore the options for retaining the high-value employees and the chances of bringing back the employees who exited recently. However, Sunil Kumar remains unconvinced about the reliability, objectivity and validity of the whole exercise. He has made up his mind to raise this issue with the appropriate authority as he felt wronged in the whole episode.

Questions for discussion

- What is your assessment of the whole situation in Genfox?

- Do you justify the actions of the Vice-President, Mr Rajnath Hegde, pertaining to employee turnover? State your reasons clearly.

- If you had been the HR general manager, what would your approach have been from the beginning?

Notes

- Eric G. Flamholtz. Human Resource Accounting, 2nd ed. (New York: John Wiley & Sons, 1985).

- Eric G. Flamholtz. Effective Management Control: Theory and Practice (Boston: Kluwer Academic Publishers, 1996).

- American Accounting Association Committee of Accounting for Human Resources, “Report of the Committee on Human Resource Accounting,” The Accounting Review Supplement to Vol. XLVIII, 1973.

- R. L. Woodruff Jr, referred by Arvindrai N. Desai in Management Strategies and Organizational Behaviour (Delhi: APH Publishing, 1989), p. 150.

- Michael Losey, Sue Meisinger and Dave Ulrich (eds), The Future of Human Resource Management: 64 Thought Leaders Explore the Critical HR Issues of Today and Tomorrow (Alexandria, VA: John Wiley & Sons, 2005), p. 269.

- Eric G. Flamholtz, Human Resource Accounting: Advances in Concepts, Methods, and Applications (New York: Springer, 1999), pp. 17–19.

- Rose Di Carlo, “Human Resource Accounting—A Synthesis,” Cost and Management (July–August 1983): 57–60.

- Rose Di Carlo, “Human Resource Accounting—A Synthesis,” Cost and Management (July–August 1983): 57–60.

- Ben Swanepoel (ed), Barney Erasmus, Marius Van Wyk and Heinz Schenk, South African Human Resource Management: Theory & Practice, 3rd ed. (Cape Town: Juta and Company Limited, 2003), p. 763.

- R. L. Brummet, E. Flamholtz, W. C. Pyle, “Human Resource Management: A Challenge for Accountants,” The Accounting Review, (April 1968): 217–24.

- Eric G. Flamholtz. Human Resource Accounting, 2nd ed. (New York: Wiley, 1985). Also see Eric G. Flamholtz, and George Geis, “The Development and Implementation of a Replacement Cost Model for Measuring Human Capital: A Field Study,” Personnel Review 13, no. 2 (1984): 25–35.

- J. S. Hekimian and C. Jones, “Put People on Your Balance Sheet,” Harvard Business Review 43 no. 2, (1967): 105–113

- R. Lee Brummet, Eric G Flamholtz and William C. Pyle, “Human Resource Management—A Challenge for the Accountant,” The Accounting Review, (April 1968): 218–219.

- William O. Cleverley, Handbook of Health Care Accounting and Finance (Sudbury, MA: Jones & Bartlett Publishers, 1989), p. 173.

- B. Lev and A. Schwartz, “On the Use of the Economic Concept of Human Capital Financial Statements,” The Accounting Review (January 1971): 103–12.

- Pekin Ogan, “A Human Resource Value Model for Professional Service Organizations,” The Accounting Review, (April 1976): 306–20.

- E. G. Flamholtz, “A Model for Human Resource Valuation: A Stochastic Process with Service Rewards,” The Accounting Review, (April 1971):666–78.

- Jac Fitz-Enz, The RoI of Human Capital: Measuring the Economic Value of Employee Performance, 2nd ed. (New York: AMACOM, 2009), p. 134.

- Jac Fitz-Enz, The RoI of Human Capital: Measuring the Economic Value of Employee Performance, 2nd ed. (New York: AMACOM, 2009), p. 135.

- W. J. Giles and D. F. Robinson, Human Asset Accounting (London: IPM and ICMA, 1972).

- Andrew Mayo, The Human Value of the Enterprise: Valuing People as Assets: Monitoring, Measuring, Managing (Naperville, IL: Nicholas Brealey Publishing, 2001), p. 77.

- R. H. Hermanson, “Accounting for Human Assets,” Occasional Paper No. 14., (East Lansing, MI: Bureau of Business and Economic Research, Michigan State University, 1964).

- Rensis Likert and David G. Bowers, “Organizational Theory and Human Resource Accounting,” American Psychologist 24, (June 1969): 585–92. Also, see David G. Bowers’ review of Rensis Likert’s, “Improving the Accuracy of P/L Reports and Estimating the Change in Dollar Value of the Human Organization,” Michigan Business Review, (25 March, 1973).

- Robin Roslender, Sociological Perspectives on Modern Accountancy (London: Routledge, 1992), p. 105.

- M. Scot Myers and Vincent S. Flowers, “A Framework for Measuring Human Assets,” California Management Review, 16, no. 4, (Summer, 1974).

- S. K. Chakraborty, New Perspectives in Management Accounting (New Delhi: McMillan, 1979).

- Raj Kumar Gupta, Human Resource Accounting: Managerial Implications (New Delhi: Anmol Publications, 2003), p. 5.

- Ben Swanepoel (ed), Barney Erasmus, Marius Van Wyk and Heinz Schenk, South African Human Resource Management: Theory & Practice, 3rd ed. (Cape Town: Juta and Company Limited, 2003), p. 766.

- Punita Jasrotia, “The Need for Human Resource Accounting,” IT People, available at http://www.itpeopleindia.com/20021216/cover.shtml.