CHAPTER 15

Incentives and Benefits

CHAPTER OBJECTIVES

After reading this chapter, you should be able to:

- Understand the significance of incentive programmes

- Understand the wage incentive planning process

- List the prerequisites for good incentive schemes

- Enumerate the different types of incentives

- Evaluate wage incentive schemes

- List the objectives of fringe benefits

- List the forms of benefits

The Raymond Group is an India-based textile major operating at the global level. It is one of the largest integrated manufacturers of worsted fabric in the world and contributes to almost 60 per cent of the worsted suiting market in India. The HR objectives of Raymond get reflected in its vision which aims to make “Raymond the most desired workplace for the top talent.”

As far as the fringe benefits are concerned, the company provides educational, housing, recreational and spiritual support systems to its people. The specific fringe benefits available in the company include employee staff quarters, guest houses, Raymond products at concession rates, company bus, and the Singhania School project, which ensures that the employees’ children have the facility to enrol themselves in the schools run by the J. K. Trust at 50 per cent of the fees. In many cases, the children’s education is provided absolutely free. Besides, the company contributes promptly to statutory fringe benefits like Provident Fund and Employees’ State Insurance. It also periodically conducts several fun-filled events to let the employees connect with one another on a regular basis.

For senior managers, the company organizes events like the annual “Raymond Interchange,” an ongoing initiative that harnesses the collective views on business strategy, and the CEO Forum, which is conducted six times a year. It adopts the 360-degree feedback system that provides senior managers with valuable inputs through evaluations from their colleagues, subordinates and customers. The feedback system also facilitates the management in arriving at decisions concerning wage incentives and career plans for individual employees by understanding their real potential, interests and goals.

The success of the Raymond Group proves the important role of wage incentives and fringe benefits in contributing to an organization. Given this context, we shall discuss incentives and benefits from different perspectives in this chapter.

Introduction

Hard work pays is the simple philosophy behind wage-incentive programmes. Employees usually get wage incentives in addition to their base salary in the organization. Wage incentives enable an organization to present challenges and rewards alike to its workforce in order to make the employees enjoy their jobs more. The primary purpose of providing wage incentives is to enhance the organizational performance and employee productivity. Understandably, incentives constitute an important HR tool to achieve the desired performance goals within a reasonable cost. Performance-based incentive programmes enable an organization to keep its employees satisfied without producing any permanent rise in pay and/or benefits. Thus, wage incentive schemes help an organization establish a formal relationship between individual performance and remuneration. Wage incentives also motivate the employees to work harder in their jobs in order to get recognition in monetary and non-monetary terms.

However, when the rewards offered as a part of the incentive programme do not fulfil the exact needs of the employees, they cannot be considered as an incentive at all. The incentive programmes should be such that they should get and keep employees motivated by fulfilling their exact needs. Generally, incentives are provided to employees when their actual performance meets the performance standards set by the organization. Although organizations predominantly offer monetary rewards as a part of performance-related incentives, they may also offer non-monetary rewards to their employees. Finally, an important prerequisite for any effective incentive scheme is the presence of an objective performance evaluation procedure.

Terms like wage incentives, variable pay, pay for performance, incentive plans and contingent pay are used in organizations interchangeably.1 Rewarding employees for reaching the predetermined performance levels is the essence of the definitions of incentives. Box 15.1 lists a few of these definitions.

We may define wage incentives as any form of performance-based financial and/or non-financial rewards payable to attract and retain the best talents without any permanent financial commitment for the organization.

Objectives of Wage Incentives

The primary objective of wage incentive schemes is to attract and retain efficient employees and induce them to work harder in the job. Through these schemes, organizations usually look to achieve the twin aims of getting the best out of their employees and ensuring adequate rewards for employee efforts.6 We shall now discuss the other important objectives of wage incentive schemes.

Box 15.1

Wage incentives are defined as “variable rewards granted according to variations in the achievement of specific results.”2

—Milton L. Rock

“Wage incentive (contingent pay) refers to payment related to individual performance, contribution, competence or skill or team or organizational performance.”3

—Michael Armstrong

“Wage incentive may be defined as the stimulation of efforts and effectiveness by offering monetary inducements or enhanced facilities.”4

—P. C. Tulsian

“Wage incentives are designed to stimulate human effort by rewarding the person, over and above the time-rated remuneration, for improvements in the present or targeted results.”5

—National Commission on Labour

Developing an Ownership Interest

Wage incentive schemes aim at creating a personal interest among the employees in organizational affairs so that this would, in turn, improve the sense of responsibility of these employees.

Enhancing Employee Motivation

Organizations look at wage incentives as a viable option to increase and then sustain employee motivation through monetary and non-monetary rewards.

Improving Employee Retention

Wage incentives aim at controlling the labour turnover arising out of employee dissatisfaction due to the absence of merit recognition and poor pay. Thus, incentive programmes aim at enhancing the employee retention rate.

Facilitating a Greater Role for Employees in Pay Determination

Wage incentive schemes enable the employees to determine their own income by linking their pay with their actual performance. By varying their performance levels, they can earn the required incomes.

Increasing the Performance and Productivity

By establishing a link between the pay and the performance, organizations aim at increasing organizational performance and employee productivity to the desired levels.

Reducing the Labour Cost

Through productivity-linked incentive schemes, organizations seek to avoid a permanent raise in the pay levels of the employees. This is in contrast to the basic pay and other fixed employee benefits, which permanently commit the organization to a fixed labour cost, irrespective of its performance and profitability.

Reducing the Time and Cost of Supervision

Wage incentive schemes aim at reducing the supervisory cost and time by enhancing the sense of responsibility of the employees through linking their performance with pay.

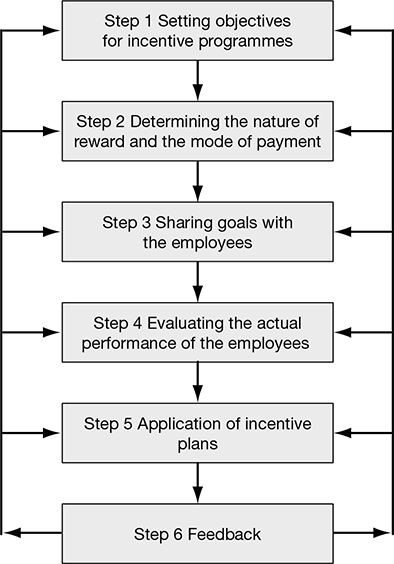

The Wage Incentive Planning Process

Though each organization can have its own style of incentive plans to serve the needs of its employees, the incentive planning process illustrated in Figure 15.1 can be adopted by any organization with necessary modifications. We shall now see the steps in an incentive planning process.

Setting the Objectives

The first step in the process of installing an incentive plan is the determination of goals for such incentive plans. Organizational objectives usually provide the basis for determining the goals of the incentive programmes. An organization must decide the specific goals it wants to accomplish through the incentive schemes and how its employees can contribute to those goals. It is only when the employees believe that the performance goals are attainable that they would put in the additional efforts required to accomplish them.7 Depending upon the requirements, an organization may set individual or group goals as part of the incentive programmes. However, an organization should revise these goals periodically to ensure that there is a continuous improvement in the performance of the employees.

Determining the Nature of Reward and the Mode of Payment

Having formulated the goals to be accomplished through incentive plans, the next step is the determination of the type of incentives and the mode of its payment. An organization should first determine the total compensation payable to the employees for reaching specific performance goals. It should also choose between individual and group incentive plans to achieve the proposed incentive goals. Besides, it should decide between monetary and non-monetary rewards for compensating its employees. It should also weigh up the merits and demerits of different incentive plans before choosing an ideal plan for goal accomplishment.

Sharing the Goals with the Employees

In the next step, the organization should effectively communicate the objectives and nature of the incentive plans to all its employees so that they can understand their role and reward in the incentive plans clearly. All the features of the incentive plans should be explained to them and all their queries clarified. The organization should ensure that the employees believe that the rewards offered to them are worth the efforts put in by them in the job.

Evaluating the Actual Performance

At the end of a specified period, the organization must evaluate the employees’ performance to decide whether they attained the performance standards and also the amount of incentives payable to each one of them. However, organizations do not evaluate the employees’ performances only to determine the wage incentives. Usually, the performance evaluation system keeps incentive fixation as one of its several objectives. Depending upon the requirements, the organization may choose from the evaluation methods like rating scales, ranking method, paired comparison, forced distribution, forced choice, critical incident, essay method, checklist, field review and confidential report (CR) to evaluate the employees’ performance.

Application of Incentive Plans

Once the performance of employees has been evaluated, the next stage is the application of appropriate incentive plans to determine the performance rating and pays of the employees. Typically, the employees at this stage get to know what their reward will be. In fact, the process of an incentive scheme begins with goal setting and ends with reward decisions. Organizations should ensure that the employees’ performances are adequately rewarded and the incentive objectives accomplished.

Feedback

Sometimes, the employees may not be satisfied with the incentive plans, the performance evaluation process or the mode of payment of incentives. In such a situation, the incentive schemes may not only fail to motivate the employees but also dissatisfy them, causing increased labour turnover and absenteeism. To avoid such a situation, it is necessary for the organization to receive periodic feedback from the employees in order to know their views on the incentive schemes. An organization may undertake attitude surveys among the employees to decide the fairness and efficacy of the incentive programmes from their perspectives. Besides, it should have a proper procedure to permit the employees to appeal against the incentive pay in case they have any grievance. Box 15.2 outlines the various incentive practices prevalent in organizations.

Prerequisites for a Good Incentive Scheme

Only an effective incentive scheme can have a desired impact on the productivity and efficiency of the employees. The installation of a good incentive scheme requires meticulous planning and honest execution. Before installing an incentive scheme in an organization, it is necessary to conduct a survey to ensure that the environment is appropriate for its introduction. The organization should also make certain that the incentive schemes proposed to be introduced fulfil the following conditions:

Box 15.2

Incentive Plans at Ranbaxy: A Boost to Performance

Each organization should first ascertain the diverse needs of its employees before developing incentive plans and fringe benefit programmes. It should also consider its organizational objectives seriously as it could provide an overall direction to the HR people about how they should proceed in the compensation planning activities. Last but not the least, it should thoroughly study the HR problems before finalizing any incentive schemes. For instance, if executive attrition is the major issue in the organization, it should develop incentive programmes (like ESOP and deferred profit sharing plan) which retain the executives for long in the organization. On the other hand, when cost reduction is the focal point, it can develop a gain-sharing plan to control the cost of production. Similarly, when the organization is located at a remote place, the transport facilities become a major fringe benefit for the employees. In a nutshell, the needs of the organization and its members drive its incentive plans and fringe benefit schemes. However, there are a few organizations that may offer several incentives and facilities just to keep their workforce happy, efficient and productive. We shall now see the compensation practice of Ranbaxy Laboratories.

Salaries and other benefits in Ranbaxy are comparable with the best in the industry. Its incentive policy is such that it rewards its employees highly if their performance is consistently outstanding. As part of its fringe benefit schemes, it offers group life insurance, medical insurance and pension plans to its employees and their dependents with an adequate financial protection on a long-term basis. Stock ownership is another successful long-term incentive offered by this company to retain the managers and improve their income and investment. It encourages its employees to take up company stock in their early stages of career so that they can gain from the success and growth of the company through capital appreciation.

Adapted from: http://www.ranbaxy.com/career/Lifeatranbaxy.aspx.

Transparency

The foremost requirement for an effective incentive scheme is its transparency. The scheme must be comprehensible to all the employees who are part of this scheme. Even uneducated employees must be able to understand the working of the incentive schemes clearly. As far as possible, highly technical and complex computation procedures must be avoided. This is because simplicity and transparency can greatly improve the employees’ trust in the incentive schemes.

Objectivity

The incentive scheme should keep subjectivity in the performance evaluation and incentive computation to the minimum. The greater the subjectivity in the incentive schemes, the larger the scope for charges of personal bias and prejudice in the determination of rewards for employees. When the employees suspect unfairness in the distribution of monetary rewards, they might remain indifferent to or even oppose the scheme. Thus, an effective incentive scheme must be equitable, objective and fair to all the employees.

Measurability

The next important prerequisite for an effective incentive scheme is that the scheme be quantifiable. The incentive scheme must be readily measurable. It should be based on rational and scientific work measurements. Organizations should not attempt to keep abstract terms like attention, required concentration and stress levels as the basis for determining the incentives. They should keep measurable terms alone as the basis for fixing the incentives for the employees.

Attainability

The performance goals fixed by an organization for computing the incentives should be practical and achievable. If they are too tough to be achieved by the employees, the latter may not be keen on accomplishing these goals. Eventually, the employees may develop an indifferent attitude towards the incentive schemes of the organization. By involving the employees adequately in the preparation of the incentive schemes, organizations can ensure that the goals and incentive schemes are attainable and practicable. Thus, a participatory and inclusive approach in the designing of incentive schemes would be a prerequisite for effective schemes.

Flexibility

An effective incentive scheme should be flexible enough to adapt itself to the changes in the internal and external environment. The organization must be able to effect changes in the scheme without too much delay. The administrators of the scheme should review its performance periodically and make necessary changes, as and when required. However, flexibility in an incentive scheme does not mean that the scheme or reward can be revoked at will. In fact, once the rewards have been computed and officially declared, they must be paid by the organization at all costs.

Comprehensiveness

An effective incentive scheme should have something to offer for all the employees of the organization. All the sections of the employees—from foremen and supervisors to helpers—must be covered under the scheme. The total cooperation of the workers, managers and unions must be obtained for the scheme. Covering only some employees under the scheme and rewarding only a few of them could prove detrimental to their unity and team spirit. Thus, a good incentive scheme should be comprehensive and inclusive in nature.

Cost-effectiveness

A good incentive scheme should not only be efficient but also economical in achieving the goals of the incentive programme. The purpose of linking pay with performance is to achieve cost-effectiveness in the management of the incentive scheme. In contrast, if the cost of maintenance of such schemes is more than the savings made through them, there is no point in continuing with such schemes. The organization should discontinue the schemes when their benefits are outweighed by the cost of their maintenance.8

Instantaneous Feedback

As far as possible, the reward available to the employees must be paid immediately. This would make an incentive scheme more relevant and attractive to those who participate in it. Besides, the employees would be more determined in earning the reward if it is going to benefit them in the immediate future. Thus, an effective incentive scheme should pass on the rewards to the employees as quickly as possible.

To accomplish the goals of the incentive schemes effectively, their administrators must have periodic consultations with all the stakeholders of the scheme, namely, the employees, the management, and the trade unions.

Types of Incentive Schemes

Incentive schemes are also known as payment by results. The three factors which favour the payment of wage incentives to employees are: (i) The employees must be rewarded for their additional efforts in the job; (ii) The payment facilitates the earning of higher wages as an inducement for additional efforts; (iii) It improves productivity and organizational profitability.9 The fairness of the outcome (reward) of an incentive scheme determines its ability to win the employees’ cooperation with the scheme. However, the type of scheme is a critical factor in determining the quantum of reward available to the employees. Therefore, an organization must be prudent in choosing incentive schemes as the nature of a scheme has a direct bearing on its outcome. However, the organization must invariably ensure that the incentive scheme chosen must be easy to operate and simple to understand. Broadly, the incentive schemes are classified into four categories: straight piece rate, differential piece rate, task and time bonuses, and merit rating.

Depending upon its compensation policy and incentive goals, an organization may primarily choose from among the following four categories. A brief explanation of each of these categories has been explained as follows.

Straight Piece Rate

This is a simple method where incentives are computed and paid to the employees in direct proportion to their performance in the job. Under this method, the same rate of incentives is paid to the employees for each unit of goods produced by them. The incentive rate remains constant for all levels of production. It is essential to ensure that the incentive rates fixed are accurate and practical; otherwise the scheme would lead to overpayment or underpayment of jobs. In the long run, neither too low rates nor too high ones would help the organization in achieving the goals of the incentive programmes, such as employee satisfaction, organizational efficiency and profitability.

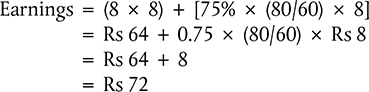

The prerequisites for the implementation of this scheme are: (i) The skill levels required in production must be similar. (ii) Production should be expressible in units or numbers. (iii) Production stoppage for which the employee is not responsible should be compensated adequately. The formula for computing the earnings is:

This method can be better understood through a numerical example. Let us say that there are two employees A and B working in the same department and producing identical products. The piece rate available for each unit of goods produced is Rs 12 per unit. At the end of the day, employee A produces 17 units and employee B 20 units. As per this scheme, the total earnings of A would be Rs 204 (17 units × Rs 12) and those of B, Rs 240 (20 units × Rs 12). Obviously, the extra efforts of employee B has been recognized and rewarded with extra incentives.

While fixing the straight piece rate, the organization must take into consideration the difficulty involved and the time required for performing the job, the quality of machines used, the safety requirements, and the quality standards. In a nutshell, the employee must get reasonable wages for reasonable efforts.

The merit of this method is that it avoids complex computation procedures. In fact, the employees themselves can work out their earnings. The limitation of this method is the non-availability of in-built measures to avoid excessive speed and quality compromises in performance.

Differential Piece Rate

Although the straight piece rate is simple to operate, it fails to recognize, motivate and reward the highly efficient employees in the organizations. It has no provision to sustain their motivation and energy levels on a continual basis. To overcome these defects in rewarding the employees, organizations apply a differential piece rate for determining the employees’ earnings.

In the differential piece rate system, more than one piece rate is offered to the employees. As part of this system, the organization sets several standards of performance and also different wage rates for each standard. An employee reaching a particular standard of output gets his wages computed on the basis of the applicable wage rate for that category. Clearly, the wage rate increases as the output increases and the employees are strongly motivated to reach higher levels of productivity. We shall now see a general example of this system.

The standard output set by an organization for its employees in the production department is 60 units per day. As per its incentive plan, it offers Rs 2.50 per unit for the employees whose production exceeds the standard output and Rs 2 per unit for the employees whose production is less than the standard output. If employee A produces 60 units in a day, he would be eligible for Rs 150 (60 units × Rs 2.50) per day. If employee B produces 49 units, he would be eligible for Rs 98 (49 units × Rs 2 per unit). Under the differential piece rate system, employees are strongly induced to reach the standard output.

However, the major limitations of the differential piece rate system are: (i) It may be difficult to set accurate and agreeable standards of production. (ii) This method may result in the employees cutting corners in their bid to produce faster. (iii) It may create tensions and rivalry between the slow and the fast performers. (iv) The employees may complain of unfairness in the standard setting when they are not able to achieve it.

Task and Time Bonuses

This is a modified form of differential piece rate system. The purpose of this bonus plan is to reduce the wage incentive cost as the output increases.10 As per this incentive scheme, once the employee reaches the standard output, his wage incentive will begin to decline. The purpose behind this move is to discourage haste in the production by the employees, understandably the major defect in the differential piece rate system. Under this system, organizations first set a standard time for each job and the hourly wage rates. Now, the employees who complete the job within the standard time get a bonus for the time saved (difference between the actual time taken and the standard time) in addition to the wage rates applicable for the time worked. However, the other employees, who do not complete the job within the standard time, get ordinary hourly wages for their actual working hours without bonus. We shall now see a simple example of task and time bonus plan.

The standard time fixed for performing job X is 5 hours and the hourly rate payable to the employees performing that job is Rs 10 per hour. The bonus available for the time saved in the job is 100 per cent. Now, employee A completes the job in 4 hours and employee B completes it in 5 hours. In this case, employee A would get Rs 50 (4 hours × Rs 10 per hour + bonus of Rs 10 for one hour saved) for four hours of actual work. Employee B would get Rs 50 (5 hours × Rs 10 per hour) for five hours of actual work.

The merit of this system is that it encourages the employees to work hard but never penalizes them for not reaching the standard time. The limitation of this method is that the organization may deliberately set tough standards for getting rewards so that it becomes simply impossible for the employees to obtain them.11

Merit Rating

This is another form of determining the wage incentives for the employees in areas of activities where these rates cannot be adopted. Merit rating aims at evaluating the relative worth of the employees in the organization before awarding them appropriately. In this method, the organization links a part of the employees’ wages to their actual performance in comparison with the standards set by it. These standards may be in terms of critical job factors like competency, initiative, attitude, safety records, punctuality, regularity, health, dynamism, behaviour, reliability and adaptability. Depending upon the importance of these factors to the job, the organization may assign points to each of these factors. The employees’ overall performance in the job is then evaluated to determine their aggregate scores, which, in turn, decide the incentives payable to them.

The merit of this method is that it can be applied even to those jobs which cannot be measured in terms of production units. In fact, it is found to be more relevant for employees performing administrative and technical jobs.12

Organizations in reality classify their wage incentive programmes on the basis of individual, group and organization-wide performance. Depending upon the objectives of the incentive programmes, an organization may decide to offer schemes for individuals, groups or for the organization as a whole (see Figure 15.2). If the management strongly believes that individual incentive programmes would promote inter-personal rivalry, thereby harming the team spirit of the members, it may decide in favour of group incentive schemes. If the management foresees inter-group enmity as a result of group-based incentives, it might settle for organization-wide incentive programmes. We shall now discuss the individual, group and organization-wide incentive plans in detail.

Individual Incentive Programmes

Organizations usually adopt individual incentive programmes when the performance of each employee can be measured with a fair amount of accuracy. Usually, a portion of the employee’s pay is decided as a function of his performance. The aim of individual incentive programmes is to enhance the efficiency, commitment, involvement and personal satisfaction of the employees. Without doubt, there is a direct and specific link between employee performance and earnings and, as such, this link can be used to enhance the productivity.13 Organizations usually pick one or more schemes from among straight piece rate, differential piece rate or merit rating methods to offer as individual incentive programmes to the employees. We shall now see the different types of individual incentive schemes.

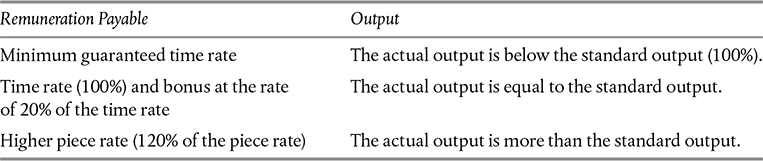

Taylor’s Differential Piece Rate Plan F. W. Taylor is one of the pioneers to advocate differential incentive schemes for individual employees. The purpose of Taylor’s differential piece rate is to encourage efficiency and discourage inefficiency among the employees. Under this piece rate plan, two wage rates are available to the employees. These are: (i) low piece rate for those employees whose performance is less than the standard; and (ii) high piece rate for any performance which is equal to or more than the standard. The standard performance is decided by the organization usually through work study comprising time study, motion study and fatigue study. In this method, the efficiency of the employee can be expressed as a percentage in terms either of the actual time taken for a job against the time allowed or of the actual output against the standard output. The merit of this method is that it grants attractive incentives for highly skilled and hard-working employees. Further, this scheme is easily understandable and executable. A classification based on Taylor’s differential piece rate is presented in Table 15.1.

The formula for computation of earnings under Taylor’s differential piece rate is

We shall now see numerical examples for better comprehension of this method.

Example 15.1

Weekly working hours = 48; Hourly wage rate = Rs 7.50; Piece rate per unit = Rs 3; Normal time taken per piece = 24 minutes

Table 15.2 The Classification Based on the Merrick Multiple Piece Rate Plan

Normal output per week = 120 pieces; Actual output for the week = 150 pieces

We shall now compute the earnings as per Taylor’s differential piece rate.

As per Taylor’s differential piece rate, 125% means above normal, i.e., a 120% bonus is applicable.

The Merrick Multiple Piece Rate Plan It is generally viewed as an improvement upon Taylor’s piece rate plan. It contains three piece rates as against Taylor’s double piece rates. It provides for gradually rising piece rates for the additional range of output produced by the employees. Like in Taylor’s piece rate system, the standard hours for performing a job should be decided by the organization carefully. The merit of this method is its ability to reward the highly efficient employees adequately by keeping one more rate for these high achievers. Besides, the provision of an additional scale for employees performing below the standard output is more acceptable to all the unions since it does not penalize any employee. A classification based on Merrick multiple piece rate plans is presented in Table 15.2.

The formula for the various categories of output:

We shall now understand this method through a numerical example.

Example 15.2

Standard output = 120 units

Piece rate = Re 0.20

Case (i): Output = 100 units

Case (iii): Output = 75 units

Case (i): Output = 100 units

As the efficiency level is more than 83% but less than 100%, we shall apply the ‘110% of the normal piece rate’ category.

Case (ii): Output = 150 units

As the efficiency level exceeds 100%, we shall apply the ‘120% of the normal piece rate’ category.

Case (iii): Output = 75 units

As the efficiency level is less than 83%, we should apply only the ‘normal piece rate’ without any bonus in the present case.

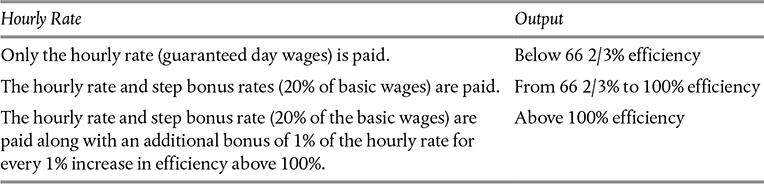

The Emerson Efficiency Plan The main feature of this incentive plan is the availability of guaranteed minimum wages for the employees irrespective of their output in a day. Another uniqueness of this method is the presence of a provision for rewarding the employees according to a graduated scale of improvement in production.13 In the Emerson efficiency plan, a standard time is set for each job and then the hourly rate is determined. Finally, incentives are decided in the form of a bonus for different degrees of efficiency. As per this incentive plan, each employee is eligible for an hourly rate based on the actual working hours and also for the bonus calculated on the basis of his efficiency. This method has wide acceptance among both the employees and the employers. The employees prefer it because they are assured of minimum day wages and also get a bonus depending upon their efficiency. It is preferred by the employers because it encourages the employees to increase efficiency and achieves better employee cooperation. However, its main limitation is that it may not be very effective in inducing the employees to work hard as they are assured of their daily wages. Its incentives may not be sufficient to induce the employees to offer their best to the job. An Emerson plan classification is listed in Table 15.3.

Table 15.3 The Classification Based on the Emerson Efficiency Plan

Standard output = 120 units

Daily wage rate = Rs 80

Piece rate = Re 0.20

Case (i): Output = 70 units

Case (ii): Output = 120 units

Case (iii): Output = 140 units

Case (i): Output = 70 units

Since the output is below the 662/3% efficiency, the daily wage rate of Rs 80 would be paid.

Case (ii): Output = 120 units

Since the output is ‘from the 66 2/3% to 100% efficiency’, a daily wage rate of Rs 80 + a 20% bonus would be paid.

Case (iii) Output = 140 units

Since the output is ‘above 100% efficiency’, the daily wage rate of Rs 80 + 20% bonus + 1% additional bonus for every additional unit produced above standard would be paid.

The Gnatt Task and Bonus System The basic feature of this system is that the employees are eligible to get the specific reward if they are able to perform the job within the standard time and then get an additional bonus if they are able to better that time. Like the other schemes, the basic necessity in this system is the accurate assessment of the time required for performing the job. This system takes into consideration the hourly rate, piece rate, and the bonus plan for deciding the wage earnings of the employees. This method guarantees the payment of minimum wages to employees irrespective of whether they reach the standard time. Table 15.4 presents a classification based on the Gnatt system.

Table 15.4 The Classification Based on the Gnatt Task and Bonus System

In a factory, a standard time allowed for completing a task (50 units) is 8 hours. The guaranteed time wages is Rs 20 per hour. If a task is completed in less than the standard time, a high rate of Rs 4 per unit is payable. We shall now compute the wages of the employees and the rate of earning per hour if the task is completed by employee A in 8 hours and by employee B in 6 hours.

In the case of employee A, the work is completed in 8 hours and thus both the time rate and bonus are applicable.

In the case of employee B, the work is completed in 6 hours and, therefore, the high piece rate is applied.

The Bedeaux System The first step in the Bedeaux system is the determination of the standard time for various jobs. The standard time fixed in the Bedeaux system is usually expressed in terms of minutes, popularly called Bedeaux points (B points). Each B point is equal to one minute and each job has a standard number of B points. This can be explained numerically in this way. The standard time for completing job X is 4 hours, which should be expressed as 240 B points (minutes). Now, employee A completes the job X in 3 hours and 30 minutes, which is equivalent to 210 B points. Employee A saves 30 B points by completing job X within the standard time. Now, the B points are converted back into hours by dividing these B points by 60. As per the Bedeaux system, 75 per cent of the earnings from the time saved should go to the employee concerned and 25 per cent should go to the foreman who supervised the performance of the job. Thus, the employee gets final earnings as per the following formula:

Earnings = actual time taken × time rate + (75/100) × (B points saved /60) × hourly rate

Example 15.5

The standard time for a job is 480 B points and the actual number of points earned in eight hours is 560 B points. The rate of pay is Rs 8 per hour. As per the Bedeaux system, the earnings will be calculated as follows:

The merit of this method is that the employees are eligible for guaranteed minimum wages regardless of whether they are able to reach the standard time or not. The limitation of this method is the difficulty in the conversion of minutes into B points and vice versa. Though it attempts to promote team unity by enabling the foreman to get a share in the employees’ bonus, the attitude of the employees towards such an arrangement is critical. They may not be keen to share their rewards with their superiors if they are aware of the working of the incentive scheme.

The Barth Variable Incentive Plan The distinguishing feature of the Barth plan is the absence of any guaranteed time rate for the employees. As per the Barth scheme, the rise in employee earnings need not be proportionate to the output. Empirically, this scheme is found to be better suited for trainees or learners. The merit of this method is that this method provides more earnings than the straight piece rate does for lower-level jobs and less earnings for the higher-level jobs. In this method, the employee earnings are calculated by multiplying the rate per hour with the square root of the product of standard hour and actual hour.

Let us see the illustration of this plan in an example.

Example 15.6

The standard time allowed for a job is 8 hours and the hourly rate is Rs 10. Employee A took 6 hours to complete the job while employee B took 10 hours. We shall now see the earnings of these employees under the Barth plan.

The Halsey Premium Plan In the Halsey premium plan, the employee is entitled to get the incentive for the time saved by him in a certain proportion. Thus, the employees are induced to complete the work well ahead of the standard time. Besides, minimum wages are assured for the employees even if they fail to complete the job within the standard time. Thus, an efficient employee gets time wages for the actual work done and a bonus in certain percentage for the difference between the actual time and the standard time, i.e., the time saved. Although the bonus is normally fixed as 50 per cent of the time saved, the organization can also fix higher or lower ceilings for the bonus percentage.

The merit of this method is its simplicity as it can be easily installed and operated. It encourages the efficient employees but never penalizes any employee on account of poor performance. It guarantees hourly wage rates even for the employees who are unable to meet the standard time. The limitation of this method is that the incentive available in it is not very attractive to induce the efficient employee to work hard on a continuous basis. The formula for this method is

Time saved = difference between the actual time and standard time

Example 15.7

In a factory, the standard time allowed for producing 80 pieces of a product is eight hours. Employee A produced 80 pieces of that product in eight hours while Employee B produced 80 pieces of it in six hours. The hourly rate is Rs 4.

We shall now calculate the earnings of the employees under the Halsey plan.

Rowan Incentive Plan In this method, an employee gets the time rate for the actual worked hours and also a bonus for the time saved if he completes the job within the standard time. On the other hand, the employee who is unable to complete the job within the standard time gets the time rate for the actual worked time. In this method, the bonus is computed as a proportion of the time rate. This proportion is arrived at by dividing the actual time worked by the standard time.

The merit of this method is that it guarantees the time rate for all the employees for the hours worked by them no matter whether they meet the standard time or not. It helps in eliminating excessive speeding in the job performance as the time saved beyond 50 per cent fetches a decreased bonus. The limitation of this method is that it discourages the employees with exceptional skills by slowing down the rate of growth in earnings beyond 50 per cent of the time saved. It involves a complex computation procedure for determining the earnings of the employees. The equation for calculating the earnings is:

We shall now apply the Rowan incentive plan in Example 15.8.

Example 15.8

In a factory, the standard time allowed for producing 80 pieces of a product is eight hours. Employee A produced 80 pieces of that product while Employee B produced 80 pieces of it in six hours. The time rate is Rs 4 per hour.

Hayne’s Incentive Plan This plan is similar to the Bedeaux system, where time is converted into B points. In the Haynes system, the standard time is expressed in terms of man-minutes called MANT. As per this system, an employee gets the time rate for the actual time worked and also a bonus for the time saved, which is computed in man-minutes. Depending upon the nature of work, the employees and the foreman divide the earnings from the time saved in the ratio of 5:1 in the Hayne’s incentive plan.

Group Incentive Schemes

Organizations offer group incentive schemes for their employees to avoid the problems of inter-personal rivalry resulting in the mutual blocking of performance by the employees. Similarly, when the individual job performance cannot be measured with a fair amount of accuracy, the organizations may opt for group incentive schemes. Thus, the organizations aim at achieving the twin goals of increased employee efficiency and teamwork. Many jobs in modern organizations require collective efforts from many persons and any individualistic attitude might hamper the successful performance of those jobs. Thus, individual success becomes dependent on the group effort and success. In such a situation, it becomes imperative for the organization to offer group incentive programmes to accomplish the organizational and performance goals. The essence of group incentive is gain sharing by the members through cost reduction measures. The two major factors influencing the group incentive scheme decisions are the size of the group and the nature of the activities. It is preferable to have small groups so that the members are aware of one another and develop group cohesiveness. Similarly, it is better to have a common product or service for the entire group so that there is better coordination among the group members.

In any group incentive scheme, the total bonus payable to a group is determined on the basis of its overall performance. This total bonus is then divided among the group members either equally or on the basis of certain predetermined factors like individual time rates and skill levels. Some of the important group incentive schemes are the cost efficiency bonus plan, the Priestman bonus plan, the Rucker incentive plan, Towne’s incentive plan, Scanlon incentive plan, and the Improshare incentive plan. We shall now discuss these group incentive plans.

Cost Efficiency Bonus Plan Under this plan, the organization first determines the standard cost for the various elements of cost. These may be material cost, labour cost and overheads associated with production. Of course, an organization may also decide the standard cost for the total cost of all these elements. Next, it measures the actual cost incurred by the group in accomplishing the production goals or targets. Finally, the actual cost incurred by the group and the standard cost are compared to determine the savings in the cost achieved by the group. As per the cost efficiency plan, a predetermined percentage of the savings is distributed in the form of bonus to the employees.

Suppose the standard cost for production of 1,000 units of product X is fixed at Rs 300,000 for a group and the actual cost incurred by that group for producing 1,000 units is Rs 270,000. This can be summarized as follows:

If the group is eligible for a 60 per cent bonus in cost saved, it would get a bonus of Rs 18,000 (60% of 30,000).

If there are 10 members in the group, each one would get Rs 1, 800 (Rs 18000/10).

Priestman Bonus Plan In this plan, a group of experts set the standard performance in terms of the number of units for the whole work to be carried out by a group within a specific period. Then, the actual performance of the group is measured and this performance is compared with the standard performance. When the actual performance exceeds the standard performance, the group members are entitled to a bonus computed on the basis of the excess production achieved by them. However, when the group’s performance is below the standard performance, they are paid on the basis of time rate without any bonus. This method is suitable for developing collective effort and team spirit among the members of the group. However, it may affect the motivation and efficiency of the individuals as all of them would be sharing the bonus equally.

Example 15.9

A factory has 400 employees in its metal works division. The standard production fixed for a normal month is 12,000 points and the actual production during that month is 15,000 points. The compensation policy of the company permits the transfer of 75% of the increase in the efficiency to the employees in the metal division as a bonus. In this context, we shall now see the group bonus under the Priestman plan.

Rucker Incentive Plan Unlike other incentive schemes, the Rucker plan aims at achieving cost saving not only on the labour cost but also on overheads. The reward for the group is determined on the basis of the difference between the labour cost and the sales value of production. In fact, the total reward available to a group depends upon the savings achieved in terms of the value of production as a result of efficient utilization of machinery, material and other equipment. The ratio in the Rucker plan is calculated in such a way that it expresses the value of production required for each rupee in the overall labour cost. The value of production means the aggregate of labour cost, overhead and profit.

As per this system, any saving achieved by the group in the value of production is used as the basis for determining group incentive. Let us see an example. Suppose the standard ratio of the labour cost to the value of production is fixed at 55 per cent of the total value of production. Now, the members of the group restrict the labour cost to 52 per cent of the total value of production and thus save three per cent in labour cost. The group is now entitled to get a proportion of the saving as a bonus. The organization may distribute half of the savings to the group and divert one-fourth of the savings to a reserve account payable later to the group on occasions when the group fails to meet the standard cost, while the remaining one-fourth of the savings might be taken over by the organization as its own share in the savings.14 In the same way, the group may also get a share in the savings achieved in the ratio of the overhead cost to the total value of production.

Towne’s Incentive Plan This method considers the savings in labour cost alone for determining the rewards payable to the group. In the first step, the standard labour cost for the entire work is determined in advance. Then the actual labour cost for that work is measured and compared with the standard labour cost. Now, the saving in the labour cost is computed and a proportion of the saving in monetary terms is distributed to the group members. However, a part of the saving is usually given to the supervisors as a recognition of their role in cost saving. Of course, the organization may get a share in the saving achieved in labour cost. The merit of this system is its ability to develop collective interest among the group members in cost reduction initiatives. However, its limitation is the small amount of reward available to the members and the absence of individual initiative in goal accomplishment.

Scanlon Incentive Plan The Scanlon incentive plan focuses on achieving savings in the labour cost alone. Yet, this method is different from the Towne’s plan in the sense that it focuses on the total labour cost instead of direct labour cost alone. In this method, the bonus is decided on the basis of the difference between the total labour cost and the sales value, including the closing stock of goods. For example, in the Rucker incentive plan, a portion of the saving in labour cost is retained for payment during lean seasons when the group is unable to achieve any cost reduction. This method can be explained through a simple example.

The average annual sales of an organization for the past four years is: Rs 440,000.

The average annual labour cost for the same period is: Rs 110,000.

The sales achieved during the current year is: Rs 140,000.

The actual total labour cost during the current year is: Rs 30,000.

Now, the ratio (in percentage) for the fixing the bonus is = 110000/440000 × 100 = 25%

The bonus is computed as follows:

Standard labour cost based on average bonus (140,000 × 25%) = Rs 35,000

Actual labour cost during the current year = Rs 30,000

Bonus payable to the group = Rs 5,000

Improshare In this method, an organization seeks to achieve savings by producing predetermined quantity of goods within the standard time. The time and motion study of F. W. Taylor usually forms the basis for deciding the standard time. This method considers the relationship between the targeted output and the standard time (one of the inputs) for deciding the group bonus. A proportion of the time saved as a result of efficient and fast production is used to fix the incentives payable for groups. This plan ignores the factors like selling price and volume, and technology, while determining the bonus payable to the groups. Suppose the targeted production and the standard time for production per day are 32 units and 8 hours, respectively. Now, if a group completes the production of 32 units in seven hours, it would be eligible to get a share in the time saved (i.e., one hour in the present case).

The driving force behind group incentive schemes is their ability to foster team spirit, which leads to increased understanding and cooperation among the members. They can also improve the involvement of members in the group decision-making processes and thus enhance the quality of the decisions. However, group rewards may act as a disincentive for the top performers, who may wish to get special attention and honours.

Organization-wide Incentive Plans

Through organization-wide incentive plans, the organization aims at inducing and motivating all its employees to work hard for it and also for their own interests. The incentives available to the employees under organization-wide plans normally depend upon the overall performance of the organization for a specific period. The primary aim of this method is to develop employees’ unity, cooperation and eventually an ownership interest in the organization. The organization can also avoid competing and conflicting claims of different departments on its resources. The important methods of organization-wide incentive plans are (i) the profit-sharing plan, (ii) the employee stock option scheme and (iii) the stock option. We shall now see these methods in detail.

Profit-sharing Plan This is a method adopted by many organizations to motivate their employees and create among them a personal interest in the affairs of the organization. The crux of the profit-sharing plan is to give out a portion of the organizational profit to the employees. It generally aims at fostering co-partnership among the employees. In this method, the organization first determines the target profit, i.e., the standard profit for the entire organization. At the end of a specific period (maybe a year), it ascertains the actual profit of the organization. Then it compares the actual profit with the standard profit in order to determine the excess profit. Understandably, the employees get a share in the excess profit of the organization. The organization may distribute the profits either on the basis of the base salary or just equally among all its employees. However, it is often guided by the length of service of its employees in determining the quantum of bonus payable to them.

The compensation policy of the organization usually determines the percentage of profit payable as bonus and also the mode of payment. Some organizations may provide the bonus out of the profit in the same year in which the profit is earned or at least in the succeeding year. A few others may defer the payment of bonus by keeping it in a pooled account. These accounts remain locked up for a predetermined period and the bonus amount is distributed to the employees after the expiry of the lock-in period. Sometimes, the organizations may even distribute such profits as one of the retirement benefits. The purpose of such lock-in periods is to use the profit-sharing scheme to retain the employees.

Even though many HR objectives like improved employee motivation, satisfaction, productivity and efficiency can be achieved through the profit-sharing plans, there are a few major problems in their implementation. These are as follows:

- Over a period of time, the employees begin to view bonuses as their basic right and expect the same to be provided even when the organization is going through a distress situation.

- Employees may seek a continuous increase in the quantum of bonus with disregard to the performance of the organization.

- When the organization discontinues the plan for any reason, the move may affect the motivation, morale and efficiency levels of the employees severely.

- The organization may rob the bonus of its real monetary value if it defers its payment for a long period of time, like in offering the bonus as part of retirement benefits.

The Employee Stock Ownership Plan (ESOP) This is another style of profit sharing in which organizations distribute the profit in an indirect form. They aim to accomplish several objectives through ESOP schemes. An ESOP scheme develops a sense of ownership among the employees and thus enhances their involvement in the decision-making process. It enables the employees to understand the problems faced by the organization in the market. It also helps the employees invest their hard-earned money in productive assets like shares. Thus, it prevents wasteful spending of the bonus amount by the employees.

Usually, the organization determines the number of shares to be issued to the employees on the basis of the length of their services and the position they occupy in the organizational structure. Generally, the organization buys the shares from the capital market, keeps them in a pool called the employee stock ownership trust (ESOT), and issues the shares to the employees on some predetermined basis. The employees can sell their shares back to the trust when they want to do so. Certainly, the ESOP schemes are well-regulated by the government through several laws and notifications. For instance, a government order stipulates that any promoter employee already holding more than 10 per cent of the equity shares cannot be given any more shares under the ESOP scheme.

The major limitation of this method is the likely fluctuation in the prices of the shares due to market-driven factors. Besides, when the company performs badly due to some reasons, the employee would suffer in more than one way. On the one hand, their job in the company would be at stake and, on the other hand, their investment value in the form of equity stocks of that company would also be eroded.

Stock Option Plan The stock option plan is another type of an organization-wide profit-sharing plan. It is a slightly different version of ESOP schemes. In a stock option plan, employees are given the right to buy the stocks of their company in specific numbers during a specific period at predetermined rates. The employees can treat stock option as another investment alternative available to them at the time of choosing their investment options. They normally dispose of their stocks when the market conditions are favourable for selling.

Evaluation of Wage Incentive Schemes

There is no doubt that the incentive schemes play a major role in accomplishing several organizational and HR objectives of the organization. They also help the organization in developing a unity of purpose among the employees and make them share the concerns of the management in the areas of productivity, profitability and progress of the organization. Many organizations see these schemes as a way to improve the economic conditions of the employees without losing their profitability and price advantage. All this is possible because the earnings of the employees are directly and formally linked to their productivity. Certainly, the incentive schemes often end up as a win-win formula since not only do they satisfy the employees but also protect the interests of the organization.

The oldest dispute in the world is said to be the dispute between the labour and the management since both have a competing claim over the same resources of the organization, i.e., the profit. When the organization pays less to the employees, it gets more in terms of profit but loses their goodwill. In contrast, if it pays them what they ask for, it can make the employees happy but its own profitability and future could be lost. No wonder then that the labour and the management have remained at war since time immemorial. In such a scenario, incentive schemes have come as a godsend for both of them. They have facilitated the adoption of a mutually beneficial accommodative approach in place of a competing one.

The major merits of incentive schemes are:

- Direct link with performance: Since the pay is directly linked to performance, both should move only in the same direction. The employees can claim higher pay only when there is a significant increase in their performance and productivity.

- No permanent financial commitment: Unlike a fixed compensation scheme like base salary, incentive schemes impose no permanent financial burden on the organization. This is because the wages are a function of employee performance and ability. Thus, the cost of compensation is commensurate with the output and the revenue.

- Sense of responsibility: Incentive programmes have many in-built provisions to improve the efficiency, motivation and morale of the employees. When the employees earn poorly, they have none to blame except their own performance. As a result, the employees identify the reason for their dismal performance rationally and seek the appropriate remedy.

- Optimum utilization of production capacity: Incentive schemes ensure the optimum utilization of the available production capacity of the organization. Any underutilization of the resources of the organization like equipment, plant and material would affect the earnings of both the employees and the employers in the performance-related pay method.

- Low employee attrition: Since employees have control over their own earnings, they may not need to leave the organization on account of poor earnings. They themselves determine how much they should earn. Thus, the organization is able to limit labour turnover and absenteeism among the employees through incentive programmes.

- Better labour–management relations: The organization can avoid strain in the relationship between the labour and the management on account of pay fixation and revision since the earning decisions are left to the employees. This also avoids loss of man-days due to strikes and lock-outs in the event of the failure of salary negotiations since incentive schemes simply link the pay to the performance and leave the rest to the decision of the system.

However, incentive schemes come under fire from the labour and the management alike on account of a few major defects.

We shall now see the limitations of incentive schemes:

- Quality concerns: When the organizations fail to monitor the quality of the goods produced, the first casualty in any incentive scheme could be the quality of the product. In their eagerness to speed up the process of production, employees often make quality compromises. Poor quality of products can defeat the very purpose of the incentive schemes as the cost of production would shoot up when the rejection rate is high.

- Employee attitude: Since the pay is related to the performance, pay determination often becomes too sensitive an exercise for the organization. Once employees get used to the earnings from the incentive schemes, they may not accept any drop in their earnings as this may amount to accepting inefficiency in their performance. In such a situation, they may even blame the incentive system as being defective and biased instead of accepting their own poor performance.

- Exploitation by management: The organization may tend to set high standards deliberately to avoid paying high incentives to the employees even if they really deserve them. In most cases, subjective methods are adopted for fixing the standard performance or time. As such, there remains a wide scope for the management to underpay its employees without attracting any criticisms.

- Internal dissensions: The individual incentive schemes often create unhealthy rivalry among the employees. They also develop enmity between the good performers and the bad ones due to jealousy over an uneven distribution of incentives, even if such a distribution is valid.

- Burnout problems: The employees may find it difficult to work against stiff targets continuously as they may exhaust themselves quickly both mentally and physically. The stress generated by frequent deadlines in the performance may impact their health, forcing them to abstain from work on health grounds or even quitting their jobs. Certainly, the incentive schemes can produce harmful side reactions for the employees and the organization.

Box 15.3

A Weakness of Wage Incentives

Performance-related incentive is an essential element to improve the organizational performance and productivity through the employees’ cooperation and satisfaction. In fact, it brings in a lot of benefits for the organization like avoidance of permanent salary commitment, moving financial risk from the organization to the employees, letting the employees decide their own earnings through their work, and, of course, attracting best talents to the organization and then retaining them by encouraging meritocracy at all levels. In contrast, it also brings in several problems for the organization. For instance, incentive programmes are criticized as techniques for fulfilling the short-term goals of the organizations with the least regard for the long-term and overall interest of the company. There is also a complaint that the performance-linked incentives are mostly decided through subjective assessment and, as such, the senior managers often have an upper hand in determining the beneficiaries and also the quantum of benefits. They may misuse their authority to gain more incentives even during difficult circumstances of the company like economic recession. A management should therefore be guided only by organizational interest while fixing the incentive.

Recently, AIG (American Insurance Group) provided $165 million in bonuses to its top executives at a time when the company was in deep financial troubles and on a bailout package of the government. This gesture of the management providing bonuses to 400 of its employees attracted widespread criticism from the public. Bowing to the public pressures, several of its top managers returned the incentives to the company. In fact, nearly nine of the ten top executives who had received the largest rewards agreed to return their awards to the company. This is exactly the danger associated with bonuses for executives as they usually have a disturbing influence on the incentive determination process.

Adapted from: “Top AIG Executives to Return Bonuses,” The Hindu, 25 March 2009, p. 21.

- Unethical practices: Incentive programmes provide ground for an unscrupulous management to indulge in unethical practices by fixing higher rate of incentives and benefits for the executives in total disregard of the future financial security of the organization. They also allow the senior executives to exploit the resources of the organization legally by influencing the committees in charge for fixing the incentives and fringe benefits.

Box 15.3 delineates one of the weaknesses of wage incentives programmes.

Fringe Benefits

Fringe benefits are a kind of compensation available to employees over and above the usual fixed basic pay and variable wage incentives. The primary purpose of fringe benefits is to enhance the general well-being of the employees of an organization. These fringe benefits are mostly paid in kind in the form of perquisites. Such benefits include, among others, health and accident insurance, contribution to superannuation funds, leave facilities, education facilities, housing facilities, and free or concessional ticket to travel.

Fringe benefits are usually available to all the employees of the organization. The length of service and the position of the employee in the organization normally determine the fringe benefits available to them. Fringe benefits are usually computed as a percentage of base salary payable to the employees. In many countries, including India, fringe benefits are subjected to tax deduction. As far as India is concerned, the government introduced the fringe benefit tax (FBT) in the year 2005 to regulate the payment of fringe benefits to the employees. The fringe benefits provided to employees are subject to 30 per cent tax.

Section 115WB (1) of the Income Tax Act 1961 pertaining to income tax on fringe benefit considers the following as the components of fringe benefits:

- Privilege or facility to employees

- Free or concessional ticket for travel

- Contribution to superannuation fund

- Security or sweat equity to employee

Section 115WB (2) of the Income Tax Act 1961 considers the following as the elements of deemed fringe benefits:

- Entertainment

- Provision of hospitality

- Conferences

- Sales promotion including publicity

- Employees’ welfare

- Conveyance

- Hotel and lodging

- Repair and maintenance of motor cars

- Repair, running (including fuel) and maintenance of aircraft

- Telephones

- Maintenance of any accommodation in the nature of guest house

- Festival celebrations

- Use of health club and similar facilities

- Use of any other club facilities

- Scholarships

- Tour and travel, including foreign travel

- Gifts

The essence of the definitions of fringe benefits is the payment of indirect compensation to the employees for their welfare. Box 15.4 lists some of the important definitions.

We may define fringe benefits as benefits payable to the employees over and above the direct compensation and usually without any reference to their performance.

Box 15.4

Definitions

Fringe benefits is defined as “indirect financial and non-financial payments employees receive for continuing their employment with the company.”15

—Gary Dessler

“Fringe benefits embrace a broad range of benefits and services that employees receive as part of their total compensation packages.”16

—William B. Werther et al.

Objectives of Fringe Benefits

The primary purpose of fringe benefits is to demonstrate the commitment of the organization in the general welfare of its employees. Certainly, it costs a lot to the organization as these benefits are not linked to its performance or productivity. However, a study revealed that the employees enjoying good fringe benefits, especially health benefits, accepted comparatively lower wages than the wages offered by the organization without such facilities.17 We shall now see the specific objectives of fringe benefits.

- Attracting the best talents: Fringe benefits vastly enhance the ability of the organization to attract the best employees. This is because they create goodwill for the organization in the labour market.

- Tax free for the employees: They are normally a non-taxable form of earnings available to the employees. As such, they enable the employees to get the real value of the compensation due to them.

- Improving employee morale: Fringe benefits are often viewed by the organization as an effective technique to improve the morale and motivation of the employees. They facilitate better retention of the employees by limiting employee dissatisfaction and labour turnover.

- Achieving the desired unity: They improve unity among the employees as these benefits are available to all the employees, irrespective of their work performance. They indeed eliminate and prevent envious and other resentful feelings among the employees.

- Improving industrial relations: They are efficient means to improve the industrial relations of the organization. The irritants relating to the basic wages and incentives can be removed through fringe benefits.

- Concern for employee well-being: Fringe benefits are a sure way of expressing the resolve of the organization to improve the health and safety of the employees. They make the employees believe that their management really cares for them.

- Reducing HR cost: Since the fringe benefits are offered to all the employees, the cost of benefits would be less. The cost of some benefits (like transportation and canteen) would come down drastically when they are offered to a large number of persons.

Forms of Fringe Benefits

Financial and non-financial rewards not included in the direct compensation payable to the employees are called fringe benefits. Organizations generally pay most of these rewards voluntarily but some others (like provident fund) are given due to legal requirements. These benefits are usually made available to the employees in different forms. Organizations choose the form which is most suitable for accomplishing the needs of its employees. These needs may differ from one employee to another and also from time to time. Organizations offer a variety of benefits so that the employees can make use of them, depending upon their need and environment. We shall now discuss the important fringe benefits.

Payment without Work Payment without work refers to different kinds of leave facilities offered to the employees. The purpose of providing pay without work is to enable the employees to take rest and refresh themselves. It facilitates the employees to sustain the same level of productivity and interest in the job. It also helps the organization retain the employees for long by keeping them happy and satisfied. This is one of the most important benefits available to the employees. It is also one of the costliest forms of benefits as employees get a lot of time off and there is absolutely no productivity during this period. Employees receive various types of leave with pay, for example, casual leave, medical leave, earned leave, maternity leave, holidays, vacations, and sabbatical leave as part of the pay-without-work scheme.

Health and Safety Care Many organizations are providing insurance benefits to their employees in the form of health insurance and accident insurance in order to help them protect their health and safety. This is also the most expensive form of fringe benefit offered by the organization to its employees. In many countries, health insurance has clearly emerged as number one fringe benefit expenses for the company.18 In addition to the voluntary benefits, the relevant laws of the country also require the institution and maintenance of funds for meeting the expenses arising out of the accidents happening to the employees. For instance, the Accident Compensation Fund facilitates the payment of benefits and income to the employees without any delay.

Retirement Benefits Retirement benefits are those benefits that are made available to the employees after their retirement from the organization. The purpose of providing retirement benefit is to enable the employees to maintain a decent and independent life after their retirement. Retirement benefits assist the employees in setting aside their worries about the future and keeping themselves focused on their job and productivity. In this way, these benefits help the organization achieve the desired level of productivity and efficiency among the employees. The retirement benefits may include gratuity and pension benefits. In India, the Employee Provident Fund and Gratuity are compulsory schemes while supplementary superannuation is a voluntary scheme for the organizations in India. However, hardly 10 per cent of the labour force in India works in the organized sector and is covered under any of the retirement schemes. The important Indian laws and provisions dealing with retirement funds are

- The Employees’ Provident Fund (EPF) Scheme, 1952

- The Employees’ Deposit Linked Insurance (EDLI) Scheme, 1976

- The Employees’ Pension Scheme (EPS), 1995

Housing Facilities An organization may provide housing facilities as part of fringe benefits to its employees. It may provide them housing accommodation or house rent allowance. Of late, the housing facilities under fringe benefits attract tax under the fringe benefits tax. Usually, the fringe benefits tax is payable by the employers. It should be paid even if the fringe benefits are not paid by the employers directly but by third parties or agencies on behalf of the employers.

Other Facilities In addition to these fringe benefits, an organization may also provide other benefits like educational facilities, canteen facilities, transport facilities, party reimbursement facilities, child care facilities like crèche, and relocation benefits. In recent times, organizations are offering customized fringe benefits plans which allow the employees to choose their fringe benefits.19 The employees may choose to receive ready cash or non-cash fringe benefits.

Summary

- Wage incentives are any form of performance-based financial and/or non-financial rewards payable to attract and retain the best talents without any permanent financial commitment for the organization.

- The objectives of wage incentives are (i) developing ownership interest, (ii) enhancing employee motivation, (iii) improving employee retention, (iv) facilitating a greater role for employees in pay determination, (v) increasing performance and productivity, (vi) reducing the labour cost, and (vii) reducing the time and cost of supervision.

- The steps in a wage incentive planning process are (i) setting the objectives, (ii) determining the nature of reward and the mode of payment, (iii) sharing goals with the employees, (iv) evaluating the actual performance, (v) application of incentive plans, and (vi) feedback.

- The prerequisites of a good incentive scheme are transparency, objectivity, measurability, attainability, flexibility, comprehensiveness, cost-effectiveness and instantaneous feedback.

- Incentive schemes can be broadly classified as straight piece rate, differential piece rate, task and time bonuses, and merit rating.

- The individual incentive programmes are Taylor’s differential piece rate plan, Merrick multiple piece rate plan, Emerson efficiency plan, Gnatt task and bonus system, Bedeaux system, Barth variable incentive plan, Halsey premium plan, Rowan incentive plan and Hayne’s incentive plan.

- The group incentive schemes are cost-efficiency bonus plan, Priestman bonus plan, Rucker incentive plan, Towne’s incentive plan, Scanlon incentive plan, and the Improshare plan.

- The organization-wide incentive plans are the profit-sharing plan, the employee stock option (ESOP) scheme, and the stock option plan.

- The merits of incentive schemes are direct link with performance, no permanent financial commitment, self-responsibility, optimum utilization of the production capacity, low employee attrition, and better labour–management relations.

- The limitations of incentive schemes are quality concerns, employee attitude, exploitation by management, internal dissensions, burnout problems, and unethical practices.

- Fringe benefits are benefits payable to the employees over and above the direct compensation and usually without any reference to their performance.

- The objectives of fringe benefits are attracting the best talents, being tax-free for the employees, improving employee morale, achieving the desired unity, improving industrial relations, concern for employee well-being, and reducing the HR cost.

- The forms of fringe benefits are payment without work, health and safety care, retirement benefits, housing facilities, and other facilities.

Review Questions

Essay-type questions

- Evaluate critically the wage incentive planning process with examples.

- Discuss in detail the prerequisites for an effective wage incentive plan.

- Enumerate any four individual wage incentive plans with numerical examples.

- How far is the Merrick plan superior to Taylor’s differential piece plan? State your arguments with numerical examples.

- Write detailed notes on the (a) Barth variable incentive plan and (b) Bedeaux system.

- Critically evaluate the merits and limitations of the Rowan incentive plan with numerical examples.

- Describe the Halsey incentive plan with numerical examples.