Appendix F

Accounting for Partnerships

LEARNING OBJECTIVES

After studying this appendix, you should be able to:

- Identify the characteristics of the partnership form of business organization.

- Explain the accounting entries for the formation of a partnership.

- Identify the bases for dividing net income or net loss.

- Describe the form and content of partnership financial statements.

- Explain the effects of the entries to record the liquidation of a partnership.

APPENDIX PREVIEW

In this appendix, we discuss reasons why businesses select the partnership form of organization. We also explain the major issues in accounting for partnerships.

Partnership Form of Organization

Learning Objective 1

Identify the characteristics of the partnership form of business organization.

A Partnership is an association of two or more persons to carry on as co‐owners of a business for profit. Partnerships are common in retail establishments and in small manufacturing companies. Also, accountants, lawyers, and doctors find it desirable to form partnerships with other professionals in their field. Professional partnerships vary in size from a medical partnership of 3 to 5 doctors, to 150 to 200 partners in a large law firm, to more than 2,000 partners in an international accounting firm.

Characteristics of Partnerships

Partnerships are fairly easy to form. They can be formed simply by a verbal agreement or, more formally, by putting in writing the rights and obligations of the partners. Partners who have not put their agreement in writing sometimes have found that the characteristics of partnerships can lead to later difficulties. The principal characteristics of the partnership form of business organization are shown in Illustration F-1 and explained in the following sections.

ASSOCIATION OF INDIVIDUALS

The voluntary association of two or more individuals in a partnership may be based on as simple an act as a handshake. However, it is preferable to state the agreement in writing. In many jurisdictions, a partnership is a legal entity for certain purposes. For instance, property (land, buildings, equipment) can be owned in the name of the partnership, and the firm can sue or be sued. A partnership is also an accounting entity for financial reporting purposes. Thus, the purely personal assets, liabilities, and transactions of the partners are excluded from the accounting records of the partnership.

Illustration F-1 Partnership characteristics

The net income of a partnership is not taxed as a separate entity. But, a partnership must file an information tax return showing partnership net income and each partner’s share of that net income. Each partner’s share is taxable at personal tax rates, regardless of the amount of net income withdrawn from the business during the year.

MUTUAL AGENCY

Mutual agency means that each partner acts on behalf of the partnership when engaging in partnership business. The act of any partner is binding on all other partners. This is true even when partners act beyond the scope of their authority, so long as the act appears to be appropriate for the partnership. For example, a partner of a grocery store who purchases a delivery truck creates a binding contract in the name of the partnership, even if the partnership agreement denies this authority. On the other hand, if a partner in a law firm purchased a snowmobile for the partnership, such an act would not be binding on the partnership. The purchase is clearly outside the scope of partnership business.

• HELPFUL HINTBecause of mutual agency, an individual should be extremely cautious in selecting partners.

LIMITED LIFE

A partnership does not have unlimited life. It may be ended voluntarily at any time through the acceptance of a new partner or the withdrawal of a partner. A partnership may be ended involuntarily by the death or incapacity of a partner. Thus, the life of a partnership is indefinite. Partnership dissolution occurs whenever a partner withdraws or a new partner is admitted. Dissolution of a partnership does not necessarily mean that the business ends. If the continuing partners agree, operations can continue without interruption by forming a new partnership.

UNLIMITED LIABILITY

Each partner is personally and individually liable for all partnership liabilities. Creditors’ claims attach first to partnership assets. If these are insufficient, the claims then attach to the personal resources of any partner, irrespective of that partner’s equity in the partnership. Because each partner is responsible for all the debts of the partnership, each partner is said to have unlimited liability.

CO‐OWNERSHIP OF PROPERTY

Partnership assets are owned jointly by the partners. If the partnership is dissolved, the assets do not legally revert to the original contributor. Each partner has a claim on total assets equal to the balance in his or her respective capital account. This claim does not attach to specific assets that an individual partner contributed to the firm. Similarly, if a partner invests a building in the partnership valued at €100,000 and the building is later sold at a gain of €20,000, that partner does not personally receive the entire gain.

Partnership net income (or net loss) is also co‐owned. If the partnership contract does not specify to the contrary, all net income or net loss is shared equally by the partners. As you will see later, though, partners may agree to unequal sharing of net income or net loss.

Organizations with Partnership Characteristics

With surprising speed, special forms of business organizations have been created that have partnership characteristics. These new organizations are being adopted by many small companies. Examples of these special forms are limited partnerships, limited liability partnerships, limited liability companies, and “S” corporations.

LIMITED PARTNERSHIPS

In a limited partnership, one or more partners have unlimited liability and one or more partners have limited liability for the debts of the firm. Those with unlimited liability are called general partners. Those with limited liability are called limited partners.Limited partners are responsible for the debts of the partnership up to the limit of their investment in the firm. This organization is identified in its name with the words “Limited Partnership” or “Ltd.” or “LP.” For the privilege of limited liability, the limited partner usually accepts less compensation than a general partner and exercises less influence in the affairs of the firm.

LIMITED LIABILITY PARTNERSHIP

A limited liability partnership, or “LLP,” is designed to protect innocent partners from malpractice or negligence claims resulting from the acts of another partner. LLPs generally carry large insurance policies in case the partnership is guilty of malpractice.

LIMITED LIABILITY COMPANIES

A newer, hybrid form of business organization with certain features like a corporation and others like a limited partnership is the limited liability company, or “LLC” (or “LC”). An LLC usually has a limited life. The owners, called members, have limited liability like owners of a corporation. Whereas limited partners do not actively participate in the management of a limited partnership (LP), the members of a limited liability company (LLC) can assume an active management role. Most taxing authorities usually classify an LLC as a partnership.

“S” CORPORATIONS

An “S” corporation is a corporation that is taxed in the same way that a partnership is taxed. To qualify as an “S” corporation, the company usually is limited to 75 or fewer shareholders, all of whom must be citizens or residents of the country. The advantage of an “S” corporation (also called a subchapter “S” corporation) is that, like a partnership and unlike a corporation, it does not pay income taxes.

Advantages and Disadvantages of Partnerships

Why do people choose partnerships? One major advantage of a partnership is that the skills and resources of two or more individuals can be combined. For example, a large public accounting firm such as Ernst & Young (GBR) must have expertise in auditing, taxation, and management consulting. In addition, a partnership is easily formed and is relatively free from governmental regulations and restrictions. A partnership does not have to contend with the “red tape” that a corporation must face. Also, decisions can be made quickly on substantive matters affecting the firm; there is no board of directors that must be consulted.

On the other hand, partnerships also have some major disadvantages: mutual agency, limited life, and unlimited liability. Unlimited liability is particularly troublesome. Many individuals fear they may lose not only their initial investment but also their personal assets if those assets are needed to pay partnership creditors. As a result, partnerships often find it difficult to obtain large amounts of investment capital. That is one reason why the largest businesses in the United States are corporations, not partnerships.

The advantages and disadvantages of the partnership form of business organization are summarized in Illustration F-2.

Illustration F-2 Advantages and disadvantages of a partnership

The Partnership Agreement

Ideally, the agreement of two or more individuals to form a partnership should be expressed in writing. This written contract is often called the partnership agreement or articles of co‐partnership. The partnership agreement contains such basic information as the name and principal location of the firm, the purpose of the business, and date of inception. In addition, relationships among the partners should be specified, such as:

- Names and capital contributions of partners.

- Rights and duties of partners.

- Basis for sharing net income or net loss.

- Provision for withdrawals of assets.

- Procedures for submitting disputes to arbitration.

- Procedures for the withdrawal or addition of a partner.

- Rights and duties of surviving partners in the event of a partner’s death.

We cannot overemphasize the importance of a written contract. The agreement should be drawn with care and should attempt to anticipate all possible situations, contingencies, and disagreements. The help of a lawyer is highly desirable in preparing the agreement.

Basic Partnership Accounting

Learning Objective 2

Explain the accounting entries for the formation of a partnership.

We now turn to the basic accounting for partnerships. The major accounting issues relate to forming the partnership, dividing income or loss, and preparing financial statements.

Forming a Partnership

Each partner’s initial investment in a partnership is entered in the partnership records. These investments should be recorded at the fair value of the assets at the date of their transfer to the partnership. The values assigned must be agreed to by all of the partners.

To illustrate, assume that A. Rolfe and T. Shea combine their proprietorships to start a partnership named U.K. Software. The firm will specialize in developing financial modeling software packages. Rolfe and Shea have the following assets prior to the formation of the partnership.

Illustration F-3 Book and fair values of assets invested

The entries to record the investments are:

Note that neither the original cost of the equipment (£5,000) nor its book value is recorded by the partnership. The equipment is recorded at its fair value, £4,000. Because the equipment has not been used by the partnership, there is no accumulated depreciation.

In contrast, the gross claims on customers (£4,000) are carried forward to the partnership. The allowance for doubtful accounts is adjusted to £1,000 to arrive at a cash (net) realizable value of £3,000. A partnership may start with an allowance for doubtful accounts because it will continue to collect existing accounts receivable, some of which are expected to be uncollectible. In addition, this procedure maintains the control and subsidiary relationship between Accounts Receivable and the accounts receivable subsidiary ledger.

After the partnership has been formed, the accounting for transactions is similar to any other type of business organization. For example, all transactions with outside parties, such as the purchase or sale of merchandise inventory and the payment or receipt of cash, should be recorded the same for a partnership as for a corporation.

The steps in the accounting cycle described in Chapter 4 also apply to a partnership. For example, the partnership prepares a trial balance and journalizes and posts adjusting entries. A worksheet may be used. There are minor differences in journalizing and posting closing entries and in preparing financial statements, as explained in the following sections.

Dividing Net Income or Net Loss

Learning Objective 4

Identify the bases for dividing net income or net loss.

Partnership net income or net loss is shared equally unless the partnership contract indicates otherwise. The same basis of division usually applies to both net income and net loss. It is customary to refer to this basis as the income ratio, the income and loss ratio, or the profit and loss (P&L) ratio. Because of its wide acceptance, we will use the term income ratio to identify the basis for dividing net income and net loss. A partner’s share of net income or net loss is recognized in the capital accounts through closing entries.

CLOSING ENTRIES

Four entries are required in preparing closing entries for a partnership. The entries are:

- Debit each revenue account for its balance, and credit Income Summary for total revenues.

- Debit Income Summary for total expenses, and credit each expense account for its balance.

- Debit Income Summary for its balance, and credit each partner’s capital account for his or her share of net income. Or, credit Income Summary, and debit each partner’s capital account for his or her share of net loss.

- Debit each partner’s capital account for the balance in that partner’s drawing account, and credit each partner’s drawing account for the same amount.

The first two entries are the same as in a corporation. The last two entries are different because (1) there are two or more owners’ capital and drawing accounts, and (2) it is necessary to divide net income (or net loss) among the partners.

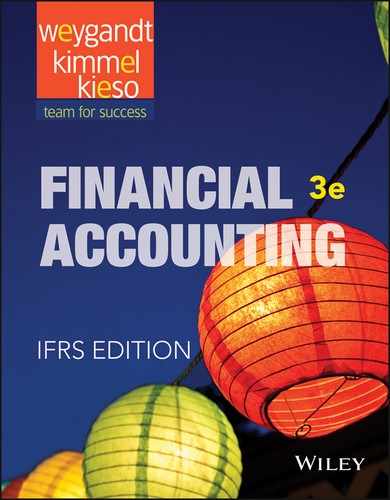

To illustrate the last two closing entries, assume that AB Company has net income of £32,000 for 2017. The partners, L. Arbor and D. Barnett, share net income and net loss equally. Drawings for the year were Arbor £8,000 and Barnett £6,000. The last two closing entries are:

Assume that the beginning capital balance is £47,000 for Arbor and £36,000 for Barnett. The capital and drawing accounts will show the following after posting the closing entries.

Illustration F-4 Partners’ capital and drawing accounts after closing

The partners’ capital accounts are permanent accounts; their drawing acc‐ounts are temporary accounts. Normally, the capital accounts will have credit balances and the drawing accounts will have debit balances. Drawing accounts are debited when partners withdraw cash or other assets from the partnership for personal use.

INCOME RATIOS

As noted earlier, the partnership agreement should specify the basis for sharing net income or net loss. The following are typical income ratios.

- A fixed ratio, expressed as a proportion (6:4), a percentage (70% and 30%), or a fraction (2/3 and 1/3).

- A ratio based either on capital balances at the beginning of the year or on average capital balances during the year.

- Salaries to partners and the remainder on a fixed ratio.

- Interest on partners’ capital balances and the remainder on a fixed ratio.

- Salaries to partners, interest on partners’ capital, and the remainder on a fixed ratio.

The objective is to settle on a basis that will equitably reflect the partners’ capital investment and service to the partnership.

A fixed ratio is easy to apply, and it may be an equitable basis in some circumstances. Assume, for example, that Hughes and Lane are partners. Each contributes the same amount of capital, but Hughes expects to work full‐time in the partnership and Lane expects to work only half‐time. Accordingly, the partners agree to a fixed ratio of 2/3 to Hughes and 1/3 to Lane.

A ratio based on capital balances may be appropriate when the funds invested in the partnership are considered the critical factor. Capital ratios may also be equitable when a manager is hired to run the business and the partners do not plan to take an active role in daily operations.

The three remaining ratios (items 3, 4, and 5) give specific recognition to differences among partners. These ratios provide salary allowances for time worked and interest allowances for capital invested. Then, any remaining net income or net loss is allocated on a fixed ratio. Some caution needs to be exercised in working with these types of income ratios. These ratios pertain exclusively to the computations that are required in dividing net income or net loss among the partners.

Salaries to partners and interest on partners’ capital are not expenses of the partnership. Therefore, these items do not enter into the matching of expenses with revenues and the determination of net income or net loss. For a partnership, as for other entities, salaries expense pertains to the cost of services performed by employees. Likewise, interest expense relates to the cost of borrowing from creditors. But partners, as owners, are not considered either employees or creditors. Therefore, when the income ratio includes a salary allowance for partners, some partnership agreements permit the partner to make monthly withdrawals of cash based on their “salary.” Such withdrawals are debited to the partner’s drawing account.

SALARIES, INTEREST, AND REMAINDER ON A FIXED RATIO

Under income ratio (5) in the list above, the provisions for salaries and interest must be applied before the remainder is allocated on the specified fixed ratio. This is true even if the provisions exceed net income. It is also true even if the partnership has suffered a net loss for the year. Detailed information concerning the division of net income or net loss should be shown below net income on the income statement.

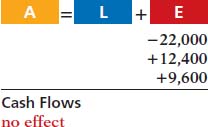

To illustrate this income ratio, assume that Sara King and Ray Lee are co‐partners in Kingslee Company. The partnership agreement provides for (1) salary allowances of €8,400 to King and €6,000 to Lee, (2) interest allowances of 10% on capital balances at the beginning of the year, and (3) dividing the remainder equally. Capital balances on January 1 were King €28,000, and Lee €24,000. In 2017, partnership net income is €22,000. The division of net income is as follows.

Illustration F-5 Income statement with division of net income

The entry to record the division of net income is

Now let’s look at a situation in which the salary and interest allowances exceed net income. Assume that Kingslee’s net income is only €18,000. In this case, the salary and interest allowances will create a deficiency of €1,600 . The computations of the allowances are the same as those in the preceding example. Beginning with total salaries and interest, we complete the division of net income as follows.

Illustration F-6 Division of net income—income deficiency

Partnership Financial Statements

Learning Objective 4

Describe the form and content of partnership financial statements.

The financial statements of a partnership are similar to those of a corporation. The income statement for a partnership is identical to the income statement for a corporation except for the additional section that reports the division of net income, as shown earlier.

The statement of changes in equity for a partnership is called the partners’ capital statement. Its function is to explain the changes in each partner’s capital account and in total partnership capital during the year. The partners’ capital statement for Kingslee Company is shown below. It is based on the division of €22,000 of net income in Illustration F-5 (page F‐8). The statement includes assumed data for the additional investment and drawings.

Illustration F-7 Partners’ capital statement

• HELPFUL HINTPartners’ capital may change due to (1) additional investment, (2) drawings, and (3) net income or net loss.

The partners’ capital statement is prepared from the income statement and the partners’ capital and drawing accounts.

The statement of financial position for a partnership is the same as for a corporation except for the equity section. In a partnership, the capital balances of each partner are shown in the statement of financial position. The equity section for Kingslee is shown in Illustration F-8.

Illustration F-8 Equity section of a partnership statement of financial position

Admission and Withdrawal of Partners

We have seen how the basic accounting for a partnership works. Another issue relates to the accounting for the addition or withdrawal of a partner. From an economic standpoint, the admission or withdrawal of a partner is often of minor significance in the continuity of the business. For example, in large public accounting or law firms, partners are added or dropped without any change in operating policies. Because the accounting for the admission or withdrawal of a partner is complex, it is discussed in more advanced accounting courses.

Liquidation of a Partnership

Learning Objective 5

Explain the effects of the entries to record the liquidation of a partnership.

The liquidation of a partnership terminates the business. It involves selling the assets of the firm, paying liabilities, and distributing any remaining assets to the partners. Liquidation may result from the sale of the business by mutual agreement of the partners, from the death of a partner, or from bankruptcy. In contrast to partnership dissolution, partnership liquidation ends both the legal and economic life of the entity.

From an accounting standpoint, liquidation should be preceded by completing the accounting cycle for the final operating period. This includes preparing adjusting entries and financial statements. It also involves preparing closing entries and a post‐closing trial balance. Thus, only statement of financial position accounts should be open as the liquidation process begins.

In liquidation, the sale of non‐cash assets for cash is called realization. Any difference between book value and the cash proceeds is called the gain or loss on realization. To liquidate a partnership, it is necessary to:

- Sell non‐cash assets for cash and recognize a gain or loss on realization.

- Allocate gain/loss on realization to the partners based on their income ratios.

- Pay partnership liabilities in cash.

- Distribute remaining cash to partners on the basis of their capital balances.

Each of the steps must be performed in sequence. Creditors must be paid before partners receive any cash distributions. Each step also must be recorded by an accounting entry.

When a partnership is liquidated, all partners may have credit balances in their capital accounts. This situation is called no capital deficiency. Or, at least one partner’s capital account may have a debit balance. This situation is termed a capital deficiency. To illustrate each of these conditions, assume that the Ace Company is liquidated when its ledger shows the assets, liabilities, and equity accounts listed in Illustration F-9.

Illustration F-9 Account balances prior to liquidation

No Capital Deficiency

The partners of Ace Company agree to liquidate the partnership on the following terms. (1) The non‐cash assets of the partnership will be sold to Jackson Enterprises for €75,000 cash. (2) The partnership will pay its partnership liabilities. The income ratios of the partners are 3:2:1, respectively. The steps in the liquidation process are as follows.

- The non‐cash assets (accounts receivable, inventory, and equipment) are sold for €75,000. The book value of these assets is €60,000 (€15,000 €18,000 + €35,000 − €8,000). Thus, a gain of €15,000 is realized on the sale. The entry is:

- The gain on realization of €15,000 is allocated to the partners on their income ratios, which are 3:2:1. The entry is:

- Partnership liabilities consist of Notes Payable €15,000 and Accounts Payable €16,000. Creditors are paid in full by a cash payment of €31,000. The entry is:

- The remaining cash is distributed to the partners on the basis of their capital balances. After the entries in the first three steps are posted, all partnership accounts, including Gain on Realization, will have zero balances except for four accounts: Cash €49,000; R. Arnet, Capital €22,500; P. Carey, Capital €22,800; and W. Eaton, Capital €3,700, as shown in Illustration F-10.

Illustration F-10 Ledger balances before distribution of cash

The entry to record the distribution of cash is as follows.

After this entry is posted, all partnership accounts will have zero balances.

A word of caution: Cash should not be distributed to partners on the basis of their income‐sharing ratios. On this basis, Arnet would receive three‐sixths, or €24,500, which would produce an erroneous debit balance of €2,000. The income ratio is the proper basis for allocating net income or loss. It is not a proper basis for making the final distribution of cash to the partners.

• HELPFUL HINTZero balances after posting is a quick proof of the accuracy of the cash distribution entry.

SCHEDULE OF CASH PAYMENTS

Some accountants prepare a cash payments schedule to determine the distribution of cash to the partners in the liquidation of a partnership. The schedule of cash payments is organized around the basic accounting equation. The schedule for Ace Company is shown in Illustration F-11. The numbers in parentheses refer to the four required steps in the liquidation of a partnership. They also identify the accounting entries that must be made. The cash payments schedule is especially useful when the liquidation process extends over a period of time.

Illustration F-11 Schedule of cash payments, no capital deficiency

Capital Deficiency

A capital deficiency may be caused by recurring net losses, excessive drawings, or losses from realization suffered during liquidation. To illustrate, assume that Ace Company is on the brink of bankruptcy. The partners decide to liquidate by having a “going‐out‐of‐business” sale. Merchandise is sold at substantial discounts, and the equipment is sold at auction. Cash proceeds from these sales and collections from customers total only €42,000. Thus, the loss from liquidation is €18,000 (€60,000 − €42,000). The steps in the liquidation process are as follows.

- The entry for the realization of non‐cash assets is:

- The loss on realization is allocated to the partners on the basis of their income ratios. The entry is:

- Partnership liabilities are paid. This entry is the same as in the previous example.

- After posting the three entries, two accounts will have debit balances—Cash €16,000, and W. Eaton, Capital €1,800. Two accounts will have credit balances—R. Arnet, Capital €6,000, and P. Carey, Capital €11,800. All four accounts are shown below.

Illustration F-12 Ledger balances before distribution of cash

Eaton has a capital deficiency of €1,800, and thus owes the partnership €1,800. Arnet and Carey have a legally enforceable claim for that amount against Eaton’s personal assets. The distribution of cash is still made on the basis of capital balances. But, the amount will vary depending on how Eaton’s deficiency is settled. Two alternatives are presented below.

PAYMENT OF DEFICIENCY

If the partner with the capital deficiency pays the amount owed the partnership, the deficiency is eliminated. To illustrate, assume that Eaton pays €1,800 to the partnership. The entry is:

After posting this entry, account balances are as follows.

Illustration F-13 Ledger balances after paying capital deficiency

The cash balance of €17,800 is now equal to the credit balances in the capital accounts (Arnet €6,000 + Carey €11,800). Cash now is distributed on the basis of these balances. The entry is:

After this entry is posted, all accounts will have zero balances.

NON‐PAYMENT OF DEFICIENCY

If a partner with a capital deficiency is unable to pay the amount owed to the partnership, the partners with credit balances must absorb the loss. The loss is allocated on the basis of the income ratios that exist between the partners with credit balances.

For example, the income ratios of Arnet and Carey are 3:2, or 3/5 and 2/5, respectively. Thus, the following entry would be made to remove Eaton’s capital deficiency.

After posting this entry, the cash and capital accounts will have the following balances.

Illustration F-14 Ledger balances after non‐payment of capital deficiency

The cash balance of €16,000 now equals the sum of the credit balances in the capital accounts (Arnet €4,920 + Carey €11,800). The entry to record the distribution of cash is:

After this entry is posted, all accounts will have zero balances.

GLOSSARY REVIEW

- Capital deficiency

- A debit balance in a partner’s capital A debit balance in a partner’s capital account after allocation of gain or loss. (p. F-10).

- General partner

- A partner who has unlimited liability for the debts of the firm. (p. F-3).

- Income ratio

- The basis for dividing net income and net loss in a partnership. (p. F-6).

- Limited liability company

- A form of business organization, usually classified as a partnership and usually with limited life, in which partners, who are called members, have limited liability. (p. F-3).

- Limited liability partnership

- A partnership of professionals in which partners are given limited liability and the public is protected from malpractice by insurance carried by the partnership. (p. F-3).

- Limited partner

- A partner who has limited liability for the debts of the firm. (p. F-3).

- Limited partnership

- A partnership in which one or more general partners have unlimited liability and one or more partners have limited liability for the obligations of the firm. (p. F-3).

- No capital deficiency

- All partners have credit balances after allocation of gain or loss. (p. F-10).

- Partners’ capital statement

- The statement of changes in equity for a partnership which shows the changes in each partner’s capital balance and in total partnership capital during the year. (p. F-9).

- Partnership

- An association of two or more persons to carry on as co-owners of a business for profit.(p. F-1).

- Partnership agreement

- A written contract expressing the voluntary agreement of two or more individuals in a partnership. (p. F-4).

- Partnership dissolution

- A change in partners due to withdrawal or admission, which does not necessarily terminate the business. (p. F-2).

- Partnership liquidation

- An event that ends both the legal and economic life of a partnership. (p. F-10).

- “S” corporation

- Corporation, with 75 or fewer shareholders, that is taxed like a partnership. (p. F-3).

- Schedule of cash payments

- A schedule showing the distribution of cash to the partners in a partnership liquidation. (p. F-12).

WileyPLUS

Many more resources are available for practice in WileyPLUS.

QUESTIONS

The characteristics of a partnership include the following: (a) association of individuals, (b) limited life, and (c) co-ownership of property. Explain each of these terms.

Gina Ryno is confused about the partnership characteristics of (a) mutual agency and (b) unlimited liability. Explain these two characteristics for Gina.

Betty Melton and Sam Kerwin are considering a business venture. They ask you to explain the advantages and disadvantages of the partnership form of organization.

Ellen Brown and Shelly Sampson form a partnership. Brown contributes land with a book value of £50,000 and a fair value of £75,000. Brown also contributes equipment with a book value of £52,000 and a fair value of £57,000. The partnership assumes a £20,000 mortgage on the land. What should be the balance in Brown’s capital account upon formation of the partnership?

Sam Stevens, S. Donal, and J. Lowry have a partnership called Golden Rule. A dispute has arisen among the partners. Stevens has invested twice as much in assets as the other two partners, and he believes net income and net losses should be shared in accordance with the capital ratios. The partnership agreement does not specify the division of profits and losses. How will net income and net loss be divided?

Jordan Marsh and Brent Spader are discussing how income and losses should be divided in a partnership they plan to form. What factors should be considered in determining the division of net income or net loss?

Mandy Elston and Jeff Baker have partnership capital balances of €40,000 and €80,000, respectively. The partnership agreement indicates that net income or net loss should be shared equally. If net income for the partnership is €24,000, how should the net income be divided?

Debbie Hunt and Kyle Keegan share net income and net loss equally. (a) Which account(s) is (are) debited and credited to record the division of net income between the partners? (b) If Debbie Hunt withdraws £30,000 in cash for personal use in lieu of salary, which account is debited and which is credited?

Partners Gina Jocketty and B. Madson are provided salary allowances of €30,000 and €25,000, respectively. They divide the remainder of the partnership income in a ratio of 60:40. If partnership net income is €50,000, how much is allocated to Jocketty and Madson?

Are the financial statements of a partnership similar to those of a corporation? Discuss.

Dean Colson and Bill Linton are discussing the liquidation of a partnership. Dean maintains that all cash should be distributed to partners on the basis of their income ratios. Is he correct? Explain.

In continuing their discussion from Question 11, Bill says that even in the case of a capital deficiency, all cash should still be distributed on the basis of capital balances. Is Bill correct? Explain.

Barb, Matt, and Wendy have income ratios of 5:3:2 and capital balances of £34,000, £31,000, and £28,000, respectively. Non‐cash assets are sold at a gain. After creditors are paid, £119,000 of cash is available for distribution to the partners. How much cash should be paid to Matt?

Before the final distribution of cash, account balances are Cash €25,000; B. Remington, Capital €19,000 (Cr.); L. Seastrom, Capital €12,000 (Cr.); and T. Luthi, Capital €6,000 (Dr.). Luthi is unable to pay any of the capital deficiency. If the income‐sharing ratios are 5:3:2, respectively, how much cash should be paid to L. Seastrom?

BRIEF EXERCISES

Journalize entries in forming a partnership.

BEF-1 Ren Li and Chen Guo decide to organize the ALL‐Star partnership. Li invests HK$160,000 cash, and Guo contributes HK$110,000 cash and equipment having a book value of HK$32,000. Prepare the entry to record Guo’s investment in the partnership, assuming the equipment has a fair value of HK$65,000.

Prepare portion of opening statement of financial position for partnership.

BEF-2 C. Free and G. Mann decide to merge their proprietorships into a partnership called Freemann Ltd. The statement of financial position for Mann shows:

| Equipment | £20,000 |

|

| Less: Accumulated depreciation—equipment | 8,000 |

£12,000 |

| Accounts receivable | 16,000 |

|

| Less: Allowance for doubtful accounts | 1,200 |

14,800 |

The partners agree that the net realizable value of the receivables is £12,500 and that the fair value of the equipment is £10,000. Indicate how the four accounts should appear in the opening statement of financial position of the partnership.

Journalize the division of net income using fixed income ratios.

BEF-3 Guangqing Ltd. reports net income of NT$200,000. The income ratios are Guang 60% and Qing 40%. Indicate the division of net income to each partner, and prepare the entry to distribute the net income.

Compute division of net income with a salary allowance and fixed ratios.

BEF-4 GER Co. reports net income of €65,000. Partner salary allowances are Grand €20,000, Easley €5,000, and Rod €5,000. Indicate the division of net income to each partner, assuming the income ratio is 50:30:20, respectively.

Show division of net income when allowances exceed net income.

BEF-5 Jabb & Nabb Co. reports net income of £32,000. Interest allowances are Jabb £6,000 and Nabb £5,000, salary allowances are Jabb £15,000 and Nabb £12,000, and the remainder is shared equally. Show the distribution of income on the income statement.

Journalize final cash distribution in liquidation.

BEF-6 After liquidating non‐cash assets and paying creditors, account balances in the CAB Co. are Cash €21,000, C Capital (Cr.) €9,000, A Capital (Cr.) €7,000, and B Capital (Cr.) €5,000. The partners share income equally. Journalize the final distribution of cash to the partners.

EXERCISES

Journalize entry for formation of a partnership.

EF-1 Liu Jiqin has owned and operated a proprietorship for several years. On January 1, he decides to terminate this business and become a partner in the firm of Feng and Jiqin. Jiqin’s investment in the partnership consists of HK$140,000 in cash, and the following assets of the proprietorship: accounts receivable HK$130,000 less allowance for doubtful accounts of HK$20,000, and equipment HK$200,000 less accumulated depreciation of HK$45,000. It is agreed that the allowance for doubtful accounts should be HK$28,000 for the partnership. The fair value of the equipment is HK$175,500.

Instructions

Journalize Jiqin’s admission to the firm of Feng and Jiqin.

Prepare schedule showing distribution of net income and closing entry.

EF-2 B. Pedigo and W. Vernon have capital balances on January 1 of €50,000 and €40,000, respectively. The partnership income‐sharing agreement provides for (1) annual salaries of €20,000 for Pedigo and €12,000 for Vernon, (2) interest at 10% on beginning capital balances, and (3) remaining income or loss to be shared 70% by Pedigo and 30% by Vernon.

Instructions

Prepare a schedule showing the distribution of net income, assuming net income is(1) €55,000 and (2) €30,000.

Journalize the allocation of net income in each of the situations above.

Prepare partners’ capital statement and partial statement of financial position.

EF-3 In Royweb Co., beginning capital balances on January 1, 2017, are Ken Rory £20,000 and Diane Webb £18,000. During the year, drawings were Rory £7,000 and Webb £3,000. Net income was £29,000, and the partners share income equally.

Instructions

Prepare the partners’ capital statement for the year.

Prepare the equity section of the statement of financial position at December 31, 2017.

Prepare cash distribution schedule.

EF-4 Daynen Company at December 31 has cash £20,000, non‐cash assets £100,000, liabilities £55,000, and the following capital balances: Day £45,000 and Nen £20,000. The firm is liquidated, and £120,000 in cash is received for the non‐cash assets. Day and Nen income ratios are 55% and 45%, respectively.

Instructions

Prepare a cash distribution schedule.

Journalize transactions in a liquidation.

EF-5 Data for the Daynen partnership are presented in EF-4.

Instructions

Prepare the entries to record:

The sale of non-cash assets.

The allocation of the gain or loss on liquidation to the partners.

Payment of creditors.

Distribution of cash to the partners.

Journalize transactions with a capital deficiency.

EF-6 Prior to the distribution of cash to the partners, the accounts in the KND Company are Cash €30,000, Kolmer Capital (Cr.) €18,000, Noble Capital (Cr.) €14,000, and Dody Capital (Dr.) €2,000. The income ratios are 5:3:2, respectively.

Instructions

Prepare the entry to record (1) Dody’s payment of €2,000 in cash to the partnership and (2) the distribution of cash to the partners with credit balances.

Prepare the entry to record (1) the absorption of Dody’s capital deficiency by the other partners and (2) the distribution of cash to the partners with credit balances.

PROBLEMS

Prepare entries for formation of a partnership and a statement of financial position.

PF-1 The post‐closing trial balances of two proprietorships on January 1, 2017, are presented below.

Yung and Olde decide to form a partnership, Olde Yung Company, with the following agreed upon valuations for non‐cash assets.

Yung Company |

Olde Company |

|

|---|---|---|

| Accounts receivable | £17,500 |

£26,000 |

| Allowance for doubtful accounts | 2,500 |

4,000 |

| Inventory | 28,000 |

20,000 |

| Equipment | 25,000 |

18,000 |

All cash will be transferred to the partnership, and the partnership will assume all the liabilities of the two proprietorships. Further, it is agreed that Yung will invest an additional £3,000 in cash, and Olde will invest an additional £16,000 in cash.

Instructions

- Prepare separate journal entries to record the transfer of each proprietorship’s assets and liabilities to the partnership.

- Journalize the additional cash investment by each partner.

- Prepare a statement of financial position for the partnership on January 1, 2017.

Journalize divisions of net income and prepare a partners’ capital statement.

PF-2 At the end of its first year of operations on December 31, 2017, ABS Company’s accounts show the following.

Partner |

Drawings |

Capital |

|---|---|---|

| Jodi Ames | £23,000 |

£48,000 |

| Jill Bolen | 14,000 |

30,000 |

| Ann Sayler | 10,000 |

25,000 |

The capital balance represents each partner’s initial capital investment. Therefore, net income or net loss for 2017 has not been closed to the partners’ capital accounts.

- Journalize the entry to record the division of net income for the year 2017 under each of the following independent assumptions.

- Net income is £28,000. Income is shared 6:3:1.

- Net income is £34,000. Ames and Bolen are given salary allowances of £18,000 and £10,000, respectively. The remainder is shared equally.

- Net income is £22,000. Each partner is allowed interest of 10% on beginning capital balances. Ames is given a £15,000 salary allowance. The remainder is shared equally.

- Prepare a schedule showing the division of net income under assumption (3) above.

- Prepare a partners’ capital statement for the year under assumption (3) above.

Prepare entries with a capital deficiency in liquidation of a partnership.

PF-3 The partners in RSP Company decide to liquidate the firm when the statement of financial position shows the following.

The partners share income and loss 5:3:2. During the process of liquidation, the following transactions were completed in the following sequence.

- A total of €50,000 was received from converting non‐cash assets into cash.

- Gain or loss on realization was allocated to partners.

- Liabilities were paid in full.

- M. Posada paid his capital defi ciency.

- Cash was paid to the partners with credit balances.

Instructions

- Prepare the entries to record the transactions.

- Post to the cash and capital accounts.

- Assume that Posada is unable to pay the capital defi ciency.

- Prepare the entry to allocate Posada’s debit balance to Ruscoe and Sorenson.

- Prepare the entry to record the final distribution of cash.