APPENDIX G

Subsidiary Ledgers and Special Journals

LEARNING OBJECTIVES

After studying this appendix, you should be able to:

- Describe the nature and purpose of a subsidiary ledger.

- Explain how companies use special journals in journalizing.

- Indicate how companies post a multi-column journal.

APPENDIX PREVIEW

A reliable accounting information system is a necessity for any company. Whether companies use pen, pencil, or computers in maintaining accounting records, certain principles and procedures apply. The purpose of this appendix is to explain and illustrate two components of an accounting information system: subsidiary ledgers and special journals.

Expanding the Ledger—Subsidiary Ledgers

Learning Objective 1

Describe the nature and purpose of a subsidiary ledger.

Imagine a business that has several thousand charge (credit) customers and shows the transactions with these customers in only one general ledger account—Accounts Receivable. It would be nearly impossible to determine the balance owed by an individual customer at any specific time. Similarly, the amount payable to one creditor would be difficult to locate quickly from a single Accounts Payable account in the general ledger.

Instead, companies use subsidiary ledgers to keep track of individual balances. A subsidiary ledger is a group of accounts with a common characteristic (for example, all accounts receivable). It is an addition to, and an expansion of, the general ledger. The subsidiary ledger frees the general ledger from the details of individual balances.

Two common subsidiary ledgers are:

- The accounts receivable (or customers’) subsidiary ledger, which collects transaction data of individual customers.

- The accounts payable (or creditors’) subsidiary ledger, which collects transaction data of individual creditors.

In each of these subsidiary ledgers, companies usually arrange individual accounts in alphabetical order.

A general ledger account summarizes the detailed data from a subsidiary ledger. For example, the detailed data from the accounts receivable subsidiary ledger are summarized in Accounts Receivable in the general ledger. The general ledger account that summarizes subsidiary ledger data is called a control account. Illustration G-1 presents an overview of the relationship of subsidiary ledgers to the general ledger. In Illustration G-1, the general ledger control accounts and subsidiary ledger accounts are in green. Note that Cash and Share Capital—Ordinary in this illustration are not control accounts because there are no subsidiary ledger accounts related to these accounts.

Illustration G-1 Relationship of general ledger and subsidiary ledgers

At the end of an accounting period, each general ledger control account balance must equal the composite balance of the individual accounts in the related subsidiary ledger. For example, the balance in Accounts Payable in Illustration G-1 must equal the total of the subsidiary balances of Creditors X + Y + Z.

Subsidiary Ledger Example

Illustration G-2 lists sales and collection transactions for Pujols Enterprises.

Illustration G-2 Sales and collection transactions

Illustration G-3 (page G-3) provides an example of a control account and subsidiary ledger based on these transactions. (Due to space considerations, the explanation column in these accounts is not shown in this and subsequent illustrations.)

Pujols can reconcile the total debits ($12,000) and credits ($8,000) in Accounts Receivable in the general ledger to the detailed debits and credits in the subsidiary accounts. Also, the balance of $4,000 in the control account agrees with the total of the balances in the individual accounts (Aaron Co. $2,000 + Branden Inc. $0 + Caron Co. $2,000) in the subsidiary ledger.

As Illustration G-3 shows, companies make monthly postings to the control accounts in the general ledger. This practice allows them to prepare monthly financial statements. Companies post to the individual accounts in the subsidiary ledger daily. Daily posting ensures that account information is current. This enables the company to monitor credit limits, bill customers, and answer inquiries from customers about their account balances.

Illustration G-3 Relationship between general and subsidiary ledgers

Advantages of Subsidiary Ledgers

Subsidiary ledgers have several advantages:

- They show in a single account transactions affecting one customer or one creditor, thus providing up-to-date information on specific account balances.

- They free the general ledger of excessive details. As a result, a trial balance of the general ledger does not contain vast numbers of individual account balances.

- They help locate errors in individual accounts by reducing the number of accounts in one ledger and by using control accounts.

- They make possible a division of labor in posting. One employee can post to the general ledger while someone else posts to the subsidiary ledgers.

Expanding the Journal—Special Journals

Learning Objective 2

Explain how companies use special journals in journalizing.

So far you have learned to journalize transactions in a two-column general journal and post each entry to the general ledger. This procedure is satisfactory in only very small companies. To expedite journalizing and posting, most companies use special journals in addition to the general journal.

Companies use special journals to record similar types of transactions. Examples are all sales of merchandise on account, or all cash receipts. The types of transactions that occur frequently in a company determine what special journals the company uses. Most merchandising companies record daily transactions using the journals shown in Illustration G-4.

Illustration G-4 Use of special journals and the general journal

If a transaction cannot be recorded in a special journal, the company records it in the general journal. For example, if a company had special journals for only the four types of transactions listed above, it would record purchase returns and allowances in the general journal. Similarly, correcting, adjusting, and closing entries are recorded in the general journal. In some situations, companies might use special journals other than those listed above. For example, when sales returns and allowances are frequent, a company might use a special journal to record these transactions.

Special journals permit greater division of labor because several people can record entries in different journals at the same time. For example, one employee may journalize all cash receipts, and another may journalize all credit sales. Also, the use of special journals reduces the time needed to complete the posting process. With special journals, companies may post some accounts monthly, instead of daily, as we will illustrate later in this appendix. On the following pages, we discuss the four special journals shown in Illustration G-4.

Sales Journal

In the sales journal, companies record sales of merchandise on account. Cash sales of merchandise go in the cash receipts journal. Credit sales of assets other than merchandise go in the general journal.

• HELPFUL HINT

Postings are also made daily to individual ledger accounts in the inventory subsidiary ledger to maintain a perpetual inventory.

JOURNALIZING CREDIT SALES

To demonstrate use of a sales journal, we will use data for Karns Wholesale Supply, which uses a perpetual inventory system. Under this system, each entry in the sales journal results in one entry at selling price and another entry at cost. The entry at selling price is a debit to Accounts Receivable (a control account) and a credit of equal amount to Sales Revenue. The entry at cost is a debit to Cost of Goods Sold and a credit of equal amount to Inventory (a control account). Using a sales journal with two amount columns, the company can show on only one line a sales transaction at both selling price and cost. Illustration G-5 (page G-5) shows this two-column sales journal of Karns Wholesale Supply, using assumed credit sales transactions (for sales invoices 101–107).

Illustration G-5 Journalizing the sales journal—perpetual inventory system

Note that, unlike the general journal, an explanation is not required for each entry in a special journal. Also, use of prenumbered invoices ensures that all invoices are journalized. Finally, the reference (Ref.) column is not used in journalizing. It is used in posting the sales journal, as explained next.

POSTING THE SALES JOURNAL

Companies make daily postings from the sales journal to the individual accounts receivable in the subsidiary ledger. Posting to the general ledger is done monthly. Illustration G-6 shows both the daily and monthly postings.

A check mark is inserted in the reference posting column to indicate that the daily posting to the customer’s account has been made. If the subsidiary ledger accounts were numbered, the account number would be entered in place of the check mark. At the end of the month, Karns posts the column totals of the sales journal to the general ledger. Here, the column totals are as follows. From the selling-price column, a debit of $90,230 to Accounts Receivable (account No. 112), and a credit of $90,230 to Sales Revenue (account No. 401). From the cost column, a debit of $62,190 to Cost of Goods Sold (account No. 505), and a credit of $62,190 to Inventory (account No. 120). Karns inserts the account numbers below the column totals to indicate that the postings have been made. In both the general ledger and subsidiary ledger accounts, the reference S1 indicates that the posting came from page 1 of the sales journal.

Illustration G-6 Posting the sales journal

PROVING THE LEDGERS

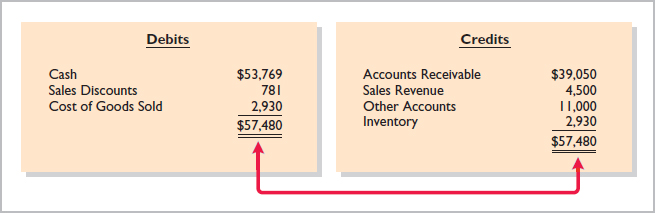

The next step is to “prove” the ledgers. To do so, Karns must determine two things: (1) the total of the general ledger debit balances must equal the total of the general ledger credit balances, and (2) the sum of the subsidiary ledger balances must equal the balance in the control account. Illustration G-7 shows the proof of the postings from the sales journal to the general and subsidiary ledger.

Illustration G-7 Proving the equality of the postings from the sales journal

ADVANTAGES OF THE SALES JOURNAL

Use of a special journal to record sales on account has several advantages. First, the one-line entry for each sales transaction saves time. In the sales journal, it is not necessary to write out the four account titles for each transaction. Second, only totals, rather than individual entries, are posted to the general ledger. This saves posting time and reduces the possibilities of posting errors. Finally, a division of labor results because one individual can take responsibility for the sales journal.

Cash Receipts Journal

Learning Objective 3

Indicate how companies post a multi-column journal.

In the cash receipts journal, companies record all receipts of cash. The most common types of cash receipts are cash sales of merchandise and collections of accounts receivable. Many other possibilities exist, such as receipt of money from bank loans and cash proceeds from disposal of equipment. A one- or two-column cash receipts journal would not have space enough for all possible cash receipt transactions. Therefore, companies use a multi-column cash receipts journal.

Generally, a cash receipts journal includes the following columns: debit columns for Cash and Sales Discounts, and credit columns for Accounts Receivable, Sales Revenue, and “Other Accounts.” Companies use the Other Accounts category when the cash receipt does not involve a cash sale or a collection of accounts receivable. Under a perpetual inventory system, each sales entry also is accompanied by an entry that debits Cost of Goods Sold and credits Inventory for the cost of the merchandise sold. Illustration G-8 shows a six-column cash receipts journal.

Companies may use additional credit columns if these columns significantly reduce postings to a specific account. For example, a loan company, such as Household International (USA), receives thousands of cash collections from customers. Using separate credit columns for Loans Receivable and Interest Revenue, rather than the Other Accounts credit column, would reduce postings.

Illustration G-8 Journalizing and posting the cash receipts journal

JOURNALIZING CASH RECEIPTS TRANSACTIONS

To illustrate the journalizing of cash receipts transactions, we will continue with the May transactions of Karns Wholesale Supply. Collections from customers relate to the entries recorded in the sales journal in Illustration G-5 (page G-5). The entries in the cash receipts journal are based on the following cash receipts.

| May | 1 |

Shareholders invested $5,000 in the business in exchange for ordinary shares. |

7 |

Cash sales of merchandise total $1,900 (cost, $1,240). | |

10 |

Received a check for $10,388 from Abbot Sisters in payment of invoice No. 101 for $10,600 less a 2% discount. | |

12 |

Cash sales of merchandise total $2,600 (cost, $1,690). | |

17 |

Received a check for $11,123 from Babson Co. in payment of invoice No. 102 for $11,350 less a 2% discount. | |

22 |

Received cash by signing a note for $6,000. | |

23 |

Received a check for $7,644 from Carson Bros. in full for invoice No. 103 for $7,800 less a 2% discount. | |

28 |

Received a check for $9,114 from Deli Co. in full for invoice No. 104 for $9,300 less a 2% discount. |

Further information about the columns in the cash receipts journal is listed below.

Debit Columns:

- Cash. Karns enters in this column the amount of cash actually received in each transaction. The column total indicates the total cash receipts for the month.

- Sales Discounts. Karns includes a Sales Discounts column in its cash receipts journal. By doing so, it does not need to enter sales discount items in the general journal. As a result, the cash receipts journal shows on one line the collection of an account receivable within the discount period.

• HELPFUL HINT

A subsidiary ledger account is entered when the entry involves a collection of accounts receivable. A general ledger account is entered when the account is not shown in a special column (and an amount must be entered in the Other Accounts column). Otherwise, no account is shown in the Account Credited column.

Credit Columns:

- Accounts Receivable. Karns uses the Accounts Receivable column to record cash collections on account. The amount entered here is the amount to be credited to the individual customer’s account.

- Sales Revenue. The Sales Revenue column records all cash sales of merchandise. Cash sales of other assets (plant assets, for example) are not reported in this column.

- Other Accounts. Karns uses the Other Accounts column whenever the credit is other than to Accounts Receivable or Sales Revenue. For example, in the first entry, Karns enters $5,000 as a credit to Share Capital—Ordinary. This column is often referred to as the sundry accounts column.

Debit and Credit Column:

- Cost of Goods Sold and Inventory. This column records debits to Cost of Goods Sold and credits to Inventory.

In a multi-column journal, generally only one line is needed for each entry. Debit and credit amounts for each line must be equal. When Karns journalizes the collection from Abbot Sisters on May 10, for example, three amounts are indicated. Note also that the Account Credited column identifies both general ledger and subsidiary ledger account titles. General ledger accounts are illustrated in the May 1 and May 22 entries. A subsidiary account is illustrated in the May 10 entry for the collection from Abbot Sisters.

When Karns has finished journalizing a multi-column journal, it totals the amount columns and compares the totals to prove the equality of debits and credits. Illustration G-9 shows the proof of the equality of Karns’s cash receipts journal.

Illustration G-9 Proving the equality of the cash receipts journal

Totaling the columns of a journal and proving the equality of the totals is called footing and crossfooting a journal.

POSTING THE CASH RECEIPTS JOURNAL

Posting a multi-column journal (Illustration G-8, page G-8) involves the following steps.

- At the end of the month, the company posts all column totals, except for the Other Accounts total, to the account title(s) specified in the column heading (such as Cash or Accounts Receivable). The company then enters account numbers below the column totals to show that they have been posted. For example, Karns has posted cash to account No. 101, accounts receivable to account No. 112, inventory to account No. 120, sales revenue to account No. 401, sales discounts to account No. 414, and cost of goods sold to account No. 505.

- The company separately posts the individual amounts comprising the Other Accounts total to the general ledger accounts specified in the Account Credited column. See, for example, the credit posting to Share Capital—Ordinary. The total amount of this column has not been posted. The symbol (X) is inserted below the total of this column to indicate that the amount has not been posted.

- The individual amounts in a column, posted in total to a control account (Accounts Receivable, in this case), are posted daily to the subsidiary ledger account specified in the Account Credited column. See, for example, the credit posting of $10,600 to Abbot Sisters.

The symbol CR, used in both the subsidiary and general ledgers, identifies postings from the cash receipts journal.

PROVING THE LEDGERS

After posting of the cash receipts journal is completed, Karns proves the ledgers. As shown in Illustration G-10 (page G-11), the general ledger totals agree. Also, the sum of the subsidiary ledger balances equals the control account balance.

Illustration G-10 Proving the ledgers after posting the sales and the cash receipts journals

Purchases Journal

In the purchases journal, companies record all purchases of merchandise on account. Each entry in this journal results in a debit to Inventory and a credit to Accounts Payable. For example, consider the following credit purchase transactions for Karns Wholesale Supply in Illustration G-11.

Illustration G-11 Credit purchases transactions

Illustration G-12 shows the purchases journal for Karns based on these transactions. When using a one-column purchases journal (as in Illustration G-12), a company cannot journalize other types of purchases on account or cash purchases in it. For example, using the purchases journal shown in Illustration Illustration G-12, Karns would have to record credit purchases of equipment or supplies in the general journal. Likewise, all cash purchases would be entered in the cash payments journal. As illustrated later, companies that make numerous credit purchases for items other than merchandise often expand the purchases journal to a multi-column format. (See Illustration G-14 on page G-13.)

JOURNALIZING CREDIT PURCHASES OF MERCHANDISE

The journalizing procedure is similar to that for a sales journal. Companies make entries in the purchases journal from purchase invoices. In contrast to the sales journal, the purchases journal may not have an invoice number column because invoices received from different suppliers will not be in numerical sequence. To ensure that they record all purchase invoices, some companies consecutively number each invoice upon receipt and then use an internal document number column in the purchases journal.

Illustration G-12 Journalizing and posting the purchases journal

POSTING THE PURCHASES JOURNAL

• HELPFUL HINT

Postings to subsidiary ledger accounts are done daily because it is often necessary to know a current balance for the subsidiary accounts.

The procedures for posting the purchases journal are similar to those for the sales journal. In this case, Karns makes daily postings to the accounts payable ledger; it makes monthly postings to Inventory and Accounts Payable in the general ledger. In both ledgers, Karns uses P1 in the reference column to show that the postings are from page 1 of the purchases journal.

Proof of the equality of the postings from the purchases journal to both ledgers is shown in Illustration G-13 (page G-13).

Illustration G-13 Proving the equality of the purchases journal

EXPANDING THE PURCHASES JOURNAL

• HELPFUL HINT A single-column purchases journal needs only to be footed to prove the equality of debits and credits.

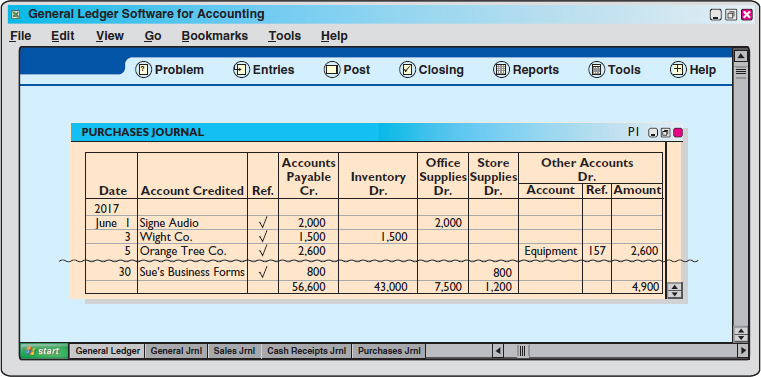

As noted earlier, some companies expand the purchases journal to include all types of purchases on account. Instead of one column for Inventory and Accounts Payable, they use a multi ‐column format. This format usually includes a credit column for Accounts Payable and debit columns for purchases of Inventory, Office Supplies, Store Supplies, and Other Accounts. Illustration G-14 shows a multi-column purchases journal for Hanover Co. The posting procedures are similar to those shown earlier for posting the cash receipts journal.

Illustration G-14 Multi-column purchases journal

Cash Payments Journal

In a cash payments (cash disbursements) journal, companies record all disbursements of cash. Entries are made from prenumbered checks. Because companies make cash payments for various purposes, the cash payments journal has multiple columns. Illustration G-15 shows a four-column journal.

JOURNALIZING CASH PAYMENTS TRANSACTIONS

The procedures for journalizing transactions in this journal are similar to those for the cash receipts journal. Karns records each transaction on one line, and for each line there must be equal debit and credit amounts. The entries in the cash payments journal in Illustration G-15 are based on the following transactions for Karns Wholesale Supply

Illustration G-15 Journalizing and posting the cash payments journal

| May | 1 |

Issued check No. 101 for $1,200 for the annual premium on a fire insurance policy. |

3 |

Issued check No. 102 for $100 in payment of freight when terms were FOB shipping point. | |

8 |

Issued check No. 103 for $4,400 for the purchase of merchandise. | |

10 |

Sent check No. 104 for $10,780 to Jasper Manufacturing Inc. in payment of May 6 invoice for $11,000 less a 2% discount. | |

19 |

Mailed check No. 105 for $6,984 to Eaton and Howe Inc. in payment of May 10 invoice for $7,200 less a 3% discount. | |

23 |

Sent check No. 106 for $6,831 to Fabor and Son in payment of May 14 invoice for $6,900 less a 1% discount. | |

28 |

Sent check No. 107 for $17,150 to Jasper Manufacturing Inc. in payment of May 19 invoice for $17,500 less a 2% discount. | |

30 |

Issued check No. 108 for $500 to shareholders as a dividend. |

Note that whenever Karns enters an amount in the Other Accounts column, it must identify a specific general ledger account in the Account Debited column. The entries for checks No. 101, 102, 103, and 108 illustrate this situation. Similarly, Karns must identify a subsidiary account in the Account Debited column whenever it enters an amount in the Accounts Payable column. See, for example, the entry for check No. 104.

After Karns journalizes the cash payments journal, it totals the columns. The totals are then balanced to prove the equality of debits and credits.

POSTING THE CASH PAYMENTS JOURNAL

The procedures for posting the cash payments journal are similar to those for the cash receipts journal. Karns posts the amounts recorded in the Accounts Payable column individually to the subsidiary ledger and in total to the control account. It posts Inventory and Cash only in total at the end of the month. Transactions in the Other Accounts column are posted individually to the appropriate account(s) affected. The company does not post totals for the Other Accounts column.

Illustration G-15 shows the posting of the cash payments journal. Note that Karns uses the symbol CP as the posting reference. After postings are completed, the company proves the equality of the debit and credit balances in the general ledger. In addition, the control account balances should agree with the subsidiary ledger total balance. Illustration G-16 shows the agreement of these balances.

Illustration G-16 Proving the ledgers after postings from the sales, cash receipts, purchases, and cash payments journals

Effects of Special Journals on the General Journal

Special journals for sales, purchases, and cash substantially reduce the number of entries that companies make in the general journal. Only transactions thatcannot be entered in a special journal are recorded in the general journal. For example, a company may use the general journal to record such transactions as granting of credit to a customer for a sales return or allowance, granting of credit from a supplier for purchases returned, acceptance of a note receivable from a customer, and purchase of equipment by issuing a note payable. Also, correcting, adjusting, and closing entries are made in the general journal.

The general journal has columns for date, account title and explanation, reference, and debit and credit amounts. When control and subsidiary accounts are not involved, the procedures for journalizing and posting of transactions are the same as those described in earlier chapters. When control and subsidiary accounts are involved, companies make two changes from the earlier procedures:

- In journalizing, they identify both the control and the subsidiary accounts.

- In posting, there must be a dual posting: once to the control account and once to the subsidiary account.

To illustrate, assume that on May 31, Karns Wholesale Supply returns $500 of merchandise for credit to Fabor and Son. Illustration G-17 shows the entry in the general journal and the posting of the entry. Note that if Karns receives cash instead of credit on this return, then it would record the transaction in the cash receipts journal.

Illustration G-17 Journalizing and posting the general journal

Note that the general journal indicates two accounts (Accounts Payable, and Fabor and Son) for the debit, and two postings (“201/✓”) in the reference column. One debit is posted to the control account and another debit to the creditor’s account in the subsidiary ledger.

Cyber Security: A Final Comment

Have you ever been hacked? With the increasing use of cell phones, tablets, and other social media outlets, a real risk exists that your confidential information may be stolen and used illegally. Companies, individuals, and even nations have all been victims of cybercrime—a crime that involves the Internet, a computer system, or computer technology.

For companies, cybercrime is clearly a major threat as the hacking of employees’ or customers’ records related to cybercrime can cost millions of dollars. Unfortunately, the number of security breaches are increasing. A security breach at Target (USA), for example, cost the company a minimum of $20 million, the CEO lost his job, and sales plummeted.

Here are three reasons for the rise in the successful hacks of corporate computer records.

- Companies and their employees continue to increase their activity on the Internet, primarily due to the use of mobile devices and cloud computing.

- Companies today collect and store unprecedented amounts of personal data on customers and employees.

- Companies often take measures to protect themselves from cyber security attacks but then fail to check if employees are carrying out the proper security guidelines.

Note that cyber security risks extend far beyond company operations and compliance. Many hackers target highly sensitive intellectual information or other strategic assets. Illustration G-18 highlights the type of hackers and their motives, targets and impacts.

Companies now recognize that cyber security systems that protect confidential data must be implemented. It follows that companies (and nations and individuals) must continually verify that their cyber security defenses are sound and uncompromised.

REVIEW

LEARNING OBJECTIVES REVIEW

- Describe the nature and purpose of a subsidiary ledger. A subsidiary ledger is a group of accounts with a common characteristic. It facilitates the recording process by freeing the general ledger from details of individual balances.

- Explain how companies use special journals in journalizing. Companies use special journals to group similar types of transactions. In a special journal, generally only one line is used to record a complete transaction.

- Indicate how companies post a multi-column journal. In posting a multi-column journal:

- Companies post all column totals except for the Other Accounts column once at the end of the month to the account title specified in the column heading.

- Companies do not post the total of the Other Accounts column. Instead, the individual amounts comprising the total are posted separately to the general ledger accounts specified in the Account Credited (Debited) column.

- The individual amounts in a column posted in total to a control account are posted daily to the subsidiary ledger accounts specified in the Account Credited (Debited) column.

GLOSSARY REVIEW

Accounts payable (creditors’) subsidiary ledger A subsidiary ledger that collects transaction data of individual creditors. (p. G-1).

Accounts receivable (customers’) subsidiary ledger A subsidiary ledger that collects transaction data of individual customers. (p. G-1).

Cash payments (cash disbursements) journal A special journal that records all cash paid. (p. G-13).

Cash receipts journal A special journal that records all cash received. (p. G-7).

Control account An account in the general ledger that summarizes subsidiary ledger data. (p. G-1).

Cybercrime A crime that involves the Internet, a computer system, or computer technology. (p. G-17).

Purchases journal A special journal that records all purchases of merchandise on account. (p. G-11).

Sales journal A special journal that records all sales of merchandise on account. (p. G-4).

Special journal A journal that records similar types of transactions, such as all credit sales. (p. G-3).

Subsidiary ledger A group of accounts with a common characteristic. (p. G-1).

WileyPLUS

Many more resources are available for practice in WileyPLUS.

QUESTIONS

- What are the advantages of using subsidiary ledgers?

- (a) When do companies normally post to (1) the subsidiary accounts and (2) the general ledger control accounts? (b) Describe the relationship between a control account and a subsidiary ledger

- Identify and explain the four special journals discussed in this appendix. List an advantage of using each of these journals rather than using only a general journal.

- Burguet Company uses special journals. It recorded in a sales journal a sale made on account to P. Starch for £435. A few days later, P. Starch returns £70 worth of merchandise for credit. Where should Burguet Company record the sales return? Why?

- A £500 purchase of merchandise on account from Hsu Company was properly recorded in the purchases journal. When posted, however, the amount recorded in the subsidiary ledger was £50. How might this error be discovered?

- Why would special journals used in different businesses not be identical in format? What type of business would maintain a cash receipts journal but not include a column for accounts receivable?

- The cash and the accounts receivable columns in the cash receipts journal were mistakenly over-added by €4,000 at the end of the month. (a) Will the customers’ ledger agree with the Accounts Receivable control account? (b) Assuming no other errors, will the trial balance totals be equal?

- One column total of a special journal is posted at month-end to only two general ledger accounts. One of these two accounts is Accounts Receivable. What is the name of this special journal? What is the other general ledger account to which that same monthend total is posted?

- In what journal would the following transactions be recorded? (Assume that a two-column sales journal and a single-column purchases journal are used.)

-

- Recording of depreciation expense for the year.

- Credit given to a customer for merchandise purchased on credit and returned.

- Sales of merchandise for cash.

- Sales of merchandise on account.

- Collection of cash on account from a customer.

- Purchase of office supplies on account.

- In what journal would the following transactions be recorded? (Assume that a two-column sales journal and a single-column purchases journal are used.)

- Cash received from signing a note payable.

- Investment of cash by shareholders.

- Closing of the expense accounts at the end of the year.

- Purchase of merchandise on account.

- Credit received for merchandise purchased and returned to supplier.

- Payment of cash on account due a supplier.

- What transactions might be included in a multicolumn purchases journal that would not be included in a single-column purchases journal?

- Give an example of a transaction in the general journal that causes an entry to be posted twice (i.e., to two accounts), one in the general ledger, the other in the subsidiary ledger. Does this affect the debit/credit equality of the general ledger?

- Give some examples of appropriate general journal transactions for an organization using special journals.

BRIEF EXERCISES

Identify subsidiary ledger balances.

BEG-1 Presented below is information related to Cortes SLU for its first month of operations. Identify the balances that appear in the accounts receivable subsidiary ledger and the accounts receivable balance that appears in the general ledger at the end of January.

Identify subsidiary ledger accounts.

BEG-2 Identify in what ledger (general or subsidiary) each of the following accounts is shown.

- Rent Expense.

- Accounts Receivable—Nguyen.

- Notes Payable.

- Accounts Payable—Weeden.

Identify special journals.

BEG-3 Identify the journal in which each of the following transactions is recorded.

- Cash sales.

- Payment of cash dividends.

- Cash purchase of land.

- Credit sales.

- Purchase of merchandise on account.

- Receipt of cash for services performed.

Identify entries to cash receipts journal

BEG-4 Indicate whether each of the following debits and credits is included in the cash receipts journal. (Use “Yes” or “No” to answer this question.)

- Debit to Sales Revenue.

- Credit to Inventory.

- Credit to Accounts Receivable.

- Debit to Accounts Payable.

Identify transactions for special journals.

BEG-5 Lazar Co. uses special journals and a general journal. Identify the journal in which each of the following transactions is recorded.

- Purchased equipment on account.

- Purchased merchandise on account.

- Paid utility expense in cash.

- Sold merchandise on account.

Identify transactions for special journals.

BEG-6 Identify the special journal(s) in which the following column headings appear.

- Sales Discounts Dr.

- Accounts Receivable Cr.

- Cash Dr.

- Sales Revenue Cr.

- Inventory Dr

Indicate postings to cash receipts journal.

BEG-7 Serrato Computer Components uses a multi-column cash receipts journal. Indicate which column(s) is/are posted only in total, only daily, or both in total and daily.

- Accounts Receivable.

- Sales Discounts.

- Cash.

- Other Accounts.

EXERCISES

Determine control account balances, and explain posting of special journals.

EG-1 Kimani Ltd. uses both special journals and a general journal as described in this appendix. On June 30, after all monthly postings had been completed, the Accounts Receivable control account in the general ledger had a debit balance of £310,000; the Accounts Payable control account had a credit balance of £77,000.

The July transactions recorded in the special journals are summarized below. No entries affecting accounts receivable and accounts payable were recorded in the general journal for July.

| Sales journal | Total sales £161,400 |

| Purchases journal | Total purchases £54,100 |

| Cash receipts journal | Accounts receivable column total £131,000 |

| Cash payments journal | Accounts payable column total £47,500 |

Instructions

- What is the balance of the Accounts Receivable control account after the monthly postings on July 31?

- What is the balance of the Accounts Payable control account after the monthly postings on July 31?

- To what account(s) is the column total of £161,400 in the sales journal posted?

- To what account(s) is the accounts receivable column total of £131,000 in the cash receipts journal posted?

Explain postings to subsidiary ledger.

EG-2 Presented below is the subsidiary accounts receivable account of Mailee Long.

Instructions

![]() Write a memo to Erica Henes, chief financial officer, that explains each transaction.

Write a memo to Erica Henes, chief financial officer, that explains each transaction.

Post various journals to control and subsidiary accounts.

EG-3 On September 1, the balance of the Accounts Receivable control account in the general ledger of Thone plc was £10,960. The customers’ subsidiary ledger contained account balances as follows: Zeyen £1,440, Lahr £2,640, Bohn £2,060, and Cao £4,820. At the end of September, the various journals contained the following information.

Sales journal: Sales to Cao £840; to Zeyen £1,260; to Han £1,330; to Bohn £1,260.

Cash receipts journal: Cash received from Bohn £1,440; from Cao £2,300; from Han £380; from Lahr £1,800; from Zeyen £1,240.

General journal: An allowance is granted to Cao £185.

Instructions

- Set up control and subsidiary accounts and enter the beginning balances. Do not construct the journals.

- Post the various journals. Post the items as individual items or as totals, whichever would be the appropriate procedure. (No sales discounts given.)

- Prepare a list of customers and prove the agreement of the controlling account with the subsidiary ledger at September 30, 2017.

Determine control and subsidiary ledger balances for accounts receivable.

EG-4 Bill Mellen Company has a balance in its Accounts Receivable control account of €10,200 on January 1, 2017. The subsidiary ledger contains three accounts: Burris Company, balance €4,000; Uhlig Company, balance €2,500; and Lopata Company. During January, the following receivable-related transactions occurred.

| Credit Sales | Collections | Returns | |

|---|---|---|---|

| Burris Company | €9,000 | €8,000 | €–0– |

| Uhlig Company | 7,000 | 2,500 | 3,000 |

| Lopata Company | 8,300 | 9,000 | –0– |

Instructions

- What is the January 1 balance in the Lopata Company subsidiary account?

- What is the January 31 balance in the control account?

- Compute the balances in the subsidiary accounts at the end of the month.

- Which January transaction would not be recorded in a special journal?

Determine control and subsidiary ledger balances for accounts payable.

EG-5 Chia Vang Ltd. has a balance in its Accounts Payable control account of NT$247,500 on January 1, 2017. The subsidiary ledger contains three accounts: Tym Ltd., balance NT$90,000; Keyes Ltd., balance NT$56,250; and Byrne Ltd. During January, the following purchase-related transactions occurred.

| Purchases | Payments | Returns | |

|---|---|---|---|

| Tym Ltd. | NT$196,500 | NT$180,000 | NT$ –0– |

| Keyes Ltd. | 157,500 | 52,000 | 69,000 |

| Byrne Ltd. | 191,250 | 202,500 | –0– |

Instructions

- What is the January 1 balance in the Byrne Ltd. subsidiary account?

- What is the January 31 balance in the control account?

- Compute the balances in the subsidiary accounts at the end of the month.

- Which January transaction would not be recorded in a special journal?

Record transactions in sales and purchases journal.

EG-6 Pashak OAO uses special journals and a general journal. The following transactions occurred during September 2017.

| Sept. | 2 |

Sold merchandise on account to J. Witten, invoice no. 101, R$780, terms n/30. The cost of the merchandise sold was R$420. |

10 |

Purchased merchandise on account from H. Gilles R$600, terms 2/10, n/30. | |

12 |

Purchased office equipment on account from Y. Kojima R$6,500. | |

21 |

Sold merchandise on account to K. Morgan, invoice no. 102 for R$800, terms 2/10, n/30. The cost of the merchandise sold was R$480. | |

25 |

Purchased merchandise on account from G. Harvey R$835, terms n/30. | |

27 |

Sold merchandise to D. Schaff for R$700 cash. The cost of the merchandise sold was R$400. |

Instructions

- Prepare a sales journal (see Illustration G-6) and a single-column purchases journal (see Illustration G-12). (Use page 1 for each journal.)

- Record the transaction(s) for September that should be journalized in the sales journal and the purchases journal.

Record transactions in cash receipts and cash payments journal

EG-7 Newell Ltd. uses special journals and a general journal. The following transactions occurred during May 2017.

| May | 1 |

M. Newell invested £50,000 cash in the business in exchange for ordinary shares. |

2 |

Sold merchandise to A. Belton for £6,340 cash. The cost of the merchandise sold was £4,200. | |

3 |

Purchased merchandise for £7,200 from E. Reed using check no. 101. | |

14 |

Paid salary to M. Hunt £740 by issuing check no. 102. | |

16 |

Sold merchandise on account to S. Spies for £920, terms n/30. The cost of the merchandise sold was £630. | |

22 |

A check of £9,000 is received from N. Eggert in full for invoice 101; no discount given. |

Instructions

- Prepare a multi-column cash receipts journal (see Illustration G-8) and a multi-column cash payments journal (see Illustration G-15). (Use page 1 for each journal.)

- Record the transaction(s) for May that should be journalized in the cash receipts journal and cash payments journal.

Explain journalizing in cash journals.

EG-8 Cosey Company uses the columnar cash journals illustrated in this appendix. In April, the following selected cash transactions occurred.

- Made a refund to a customer for the return of damaged goods.

- Received collection from customer within the 3% discount period.

- Purchased merchandise for cash.

- Paid a creditor within the 3% discount period.

- Paid a creditor within the 3% discount period.

- Paid freight on merchandise purchased.

- Paid cash for office equipment.

- Received cash refund from supplier for merchandise returned.

- Paid cash dividend to shareholders.

- Made cash sales.

Instructions

Indicate (a) the journal, and (b) the columns in the journal that should be used in recording each transaction.

Journalize transactions in general journal and post.

EG-9 Moncado plc has the following selected transactions during March.

| Mar. | 2 |

Purchased equipment costing £9,400 from Aleksic Company on account. |

5 |

Received credit of £410 from Dumont Company for merchandise damaged in shipment to Moncado. | |

7 |

Issued credit of £365 to Gavin Company for merchandise the customer returned. The returned merchandise had a cost of £245. |

Moncado uses a one-column purchases journal, a sales journal, the columnar cash journals used in this appendix, and a general journal.

Instructions

- Journalize the transactions in the general journal.

In a brief memo to the president of Moncado plc, explain the postings to the control and subsidiary accounts from each type of journal.

In a brief memo to the president of Moncado plc, explain the postings to the control and subsidiary accounts from each type of journal.

Indicate journalizing in special journals.

EG-10 Below are some typical transactions incurred by Khiani Company.

- Payment of creditors on account.

- Return of merchandise sold for credit.

- Collection on account from customers.

- Sale of land for cash.

- Sale of merchandise on account.

- Sale of merchandise for cash.

- Received credit for merchandise purchased on credit.

- Sales discount taken on goods sold.

- Payment of employee wages.

- Payment of cash dividend to shareholders.

- Depreciation on building.

- Purchase of office supplies for cash.

- Purchase of merchandise on account.

Instructions

For each transaction, indicate whether it would normally be recorded in a cash receipts journal, cash payments journal, sales journal, single-column purchases journal, or general journal.

Explain posting to control account and subsidiary ledger.

EG-11 The general ledger of Saxena A/S contained the following Accounts Payable control account (in T-account form). Also shown is the related subsidiary ledger.

Instructions

- Indicate the missing posting reference and amount in the control account, and the missing ending balance (in €) in the subsidiary ledger.

- Indicate the amounts in the control account that were dual-posted (i.e., posted to the control account and the subsidiary accounts).

Prepare purchases and general journals.

EG-12 Selected accounts from the ledgers of Masud Company at July 31 showed the following.

Instructions

From the data prepare:

- The single-column purchases journal for July.

- The general journal entries for July.

Determine correct posting amount to control account.

EG-13 Schara Products uses both special journals and a general journal as described in this appendix. Schara also posts customers’ accounts in the accounts receivable subsidiary ledger. The postings (in €) for the most recent month are included in the subsidiary T-accounts below.

Instructions

Determine the correct amount of the end-of-month posting from the sales journal to the Accounts Receivable control account.

Compute balances in various accounts.

EG-13 Selected account balances for Satina SpA at January 1, 2017, are presented below.

| Accounts Payable | €19,000 |

| Accounts Receivable | 22,000 |

| Cash | 17,000 |

| Inventory | 13,500 |

Satina’s sales journal for January shows a total of €100,000 in the selling price column, and its one-column purchases journal for January shows a total of €72,000.

The column totals in Satina’s cash receipts journal are Cash Dr. €64,000; Sales Discounts Dr. €1,100; Accounts Receivable Cr. €48,000; Sales Revenue Cr. €6,000; and Other Accounts Cr. €11,100.

The column totals in Satina’s cash payments journal for January are Cash Cr. €55,000; Inventory Cr. €1,000; Accounts Payable Dr. €46,000; and Other Accounts Dr. €10,000. Satina’s total cost of goods sold for January is €63,600.

Accounts Payable, Accounts Receivable, Cash, Inventory, and Sales Revenue are not involved in the “Other Accounts” column in either the cash receipts or cash payments journal, and are not involved in any general journal entries.

Instructions

Compute the January 31 balance for Satina in the following accounts.

- Accounts Payable.

- Accounts Receivable.

- Cash.

- Inventory.

- Sales Revenue.

PROBLEMS: SET A

Journalize transactions in cash receipts journal; post to control account and subsidiary ledger.

PG-1A Nordeen AG’s chart of accounts includes the following selected accounts.

| 101 | Cash | 401 | Sales Revenue |

| 112 | Accounts Receivable | 414 | Sales Discounts |

| 120 | Inventory | 505 | Cost of Goods Sold |

| 311 | Share Capital—Ordinary |

On April 1, the accounts receivable ledger of Nordeen showed the following balances: Siem €1,550, Milkie €1,200, Jury Co. €2,900, and Afzal €1,800. The April transactions involving the receipt of cash were as follows.

Apr. 1 |

Shareholders invested €7,500 additional cash in the business, in exchange for ordinary shares. |

4 |

Received check for payment of account from Afzal less 2% cash discount. |

5 |

Received check for €1,050 payment of invoice no. 307 from Jury Co. |

8 |

Made cash sales of merchandise totaling €7,845. The cost of the merchandise sold was €4,460. |

10 |

Received check for €600 in payment of invoice no. 309 from Siem. |

11 |

Received cash refund from a supplier for damaged merchandise €680. |

23 |

Received check for €1,500 in payment of invoice no. 310 from Jury Co. |

29 |

Received check for payment of account from Milkie. |

Instructions

- Journalize the transactions above in a six‐column cash receipts journal with columns for Cash Dr., Sales Discounts Dr., Accounts Receivable Cr., Sales Revenue Cr., Other Accounts Cr., and Cost of Goods Sold Dr./Inventory Cr. Foot and crossfoot the journal.

- Insert the beginning balances in the Accounts Receivable control and subsidiary accounts, and post the April transactions to these accounts.

- Prove the agreement of the control account and subsidiary account balances.

Journalize transactions in cash payments journal; post to control account and subsidiary ledgers.

PG-2A Gatske A.S¸ .’s chart of accounts includes the following selected accounts.

| 101 | Cash | 201 | Accounts Payable |

| 120 | Inventory | 332 | Cash Dividends |

| 130 | Prepaid Insurance | 505 | Cost of Goods Sold |

| 157 | Equipment |

On October 1, the accounts payable ledger of Gatske showed the following balances: Deavers Company ![]() 2,700, Greer Co.

2,700, Greer Co. ![]() 2,500, May Co.

2,500, May Co. ![]() 2,100, and Snell Company

2,100, and Snell Company ![]() 3,700. The October transactions involving the payment of cash were as follows.

3,700. The October transactions involving the payment of cash were as follows.

| Oct. 1 | Purchased merchandise, check no. 63, |

3 |

Purchased equipment, check no. 64, |

5 |

Paid Deavers Company balance due of |

10 |

Purchased merchandise, check no. 66, |

15 |

Paid May Co. balance due of |

16 |

Paid cash dividend of |

19 |

Paid Greer Co. in full for invoice no. 610, |

29 |

Paid Snell Company in full for invoice no. 264, |

Instructions

- Journalize the transactions above in a four‐column cash payments journal with columns for Other Accounts Dr., Accounts Payable Dr., Inventory Cr., and Cash Cr. Foot and crossfoot the journal.

- Insert the beginning balances in the Accounts Payable control and subsidiary accounts, and post the October transactions to these accounts.

- Prove the agreement of the control account and the subsidiary account balances.

Journalize transactions in cash receipts journal; post to control account and subsidiary ledgerJournalize transactions in multi‐column purchases journal; post to the general and subsidiary ledgers.

PG-3A The chart of accounts of Domingo Ltd. includes the following selected accounts.

| 112 | Accounts Receivable | 401 | Sales Revenue |

| 120 | Inventory | 412 | Sales Returns and Allowances |

| 126 | Supplies | 505 | Cost of Goods Sold |

| 157 | Equipment | 610 | Advertising Expense |

| 201 | Accounts Payable |

In July, the following selected transactions were completed. All purchases and sales were on account. The cost of all merchandise sold was 70% of the sales price.

July 1 |

Purchased merchandise from Chad Company £7,600. |

2 |

Received freight bill from Pegasus Shipping on Chad purchase £400. |

3 |

Made sales to Effron Company £1,300 and to Pitas Bros. £2,000. |

5 |

Purchased merchandise from Kivlin Company £3,400. |

8 |

Received credit on merchandise returned to Kivlin Company £300. |

13 |

Purchased store supplies from Bowe Supply £910. |

15 |

Purchased merchandise from Chad Company £3,600 and from Goran Company £3,300. |

16 |

Made sales to Felber Company £3,450 and to Pitas Bros. £1,570. |

18 |

Received bill for advertising from Wei Advertisements £640. |

21 |

Made sales to Effron Company £310 and to Musky Company £2,680. |

22 |

Granted allowance to Effron Company for merchandise damaged in shipment £65. |

24 |

Purchased merchandise from Kivlin Company £3,000. |

26 |

Purchased equipment from Bowe Supply £900. |

28 |

Received freight bill from Pegasus Shipping on Kivlin purchase of July 24, £380. |

30 |

Made sales to Felber Company £5,600. |

Instructions

- Journalize the transactions above in a purchases journal, a sales journal, and a general journal. The purchases journal should have the following column headings: Date, Account Credited (Debited), Ref., Accounts Payable Cr., Inventory Dr., and Other Accounts Dr.

- Post to both the general and subsidiary ledger accounts. (Assume that all accounts have zero beginning balances.)

- Prove the agreement of the control and subsidiary accounts.

Journalize transactions in special journals.

PG-4A Selected accounts from the chart of accounts of Valdez SA are shown below.

| 101 | Cash | 401 | Sales Revenue |

| 112 | Accounts Receivable | 412 | Sales Returns and Allowances |

| 120 | Inventory | 414 | Sales Discounts |

| 126 | Supplies | 505 | Cost of Goods Sold |

| 157 | Equipment | 726 | Salaries and Wages Expense |

| 201 | Accounts Payable |

The cost of all merchandise sold was 60% of the sales price. During January, Valdez completed the following transactions.

Jan. 3 |

Purchased merchandise on account from Pirkov Co. R$10,000. |

4 |

Purchased supplies for cash R$80. |

4 |

Sold merchandise on account to Hull R$5,600, invoice no. 371, terms 1/10, n/30. |

5 |

Returned R$300 worth of damaged goods purchased on account from Pirkov Co. on January 3. |

6 |

Made cash sales for the week totaling R$3,750. |

8 |

Purchased merchandise on account from Dubois Co. R$4,500. |

9 |

Sold merchandise on account to Phelan Ltd. R$6,400, invoice no. 372, terms 1/10, n/30. |

11 |

Purchased merchandise on account from Akers Co. R$3,700. |

13 |

Paid in full Pirkov Co. on account less a 2% discount. |

13 |

Made cash sales for the week totaling R$6,260. |

15 |

Received payment from Phelan Ltd. for invoice no. 372. |

15 |

Paid semi‐monthly salaries of R$14,300 to employees. |

17 |

Received payment from Hull for invoice no. 371. |

17 |

Sold merchandise on account to Mayr Co. R$1,200, invoice no. 373, terms 1/10, n/30. |

19 |

Purchased equipment on account from Barb Ltd. R$5,500. |

20 |

Cash sales for the week totaled R$3,200. |

20 |

Paid in full Dubois Co. on account less a 2% discount. |

23 |

Purchased merchandise on account from Pirkov Co. R$7,800. |

24 |

Purchased merchandise on account from Fifer Ltd. R$5,100. |

27 |

Made cash sales for the week totaling R$4,230. |

30 |

Received payment from Mayr Co. for invoice no. 373. |

31 |

Paid semi‐monthly salaries of R$14,300 to employees. |

31 |

Sold merchandise on account to Hull R$9,330, invoice no. 374, terms 1/10, n/30. |

Valdez uses the following journals.

- Sales journal.

- Single‐column purchases journal.

- Cash receipts journal with columns for Cash Dr., Sales Discounts Dr., Accounts Receivable Cr., Sales Revenue Cr., Other Accounts Cr., and Cost of Goods Sold Dr./ Inventory Cr.

- Cash payments journal with columns for Other Accounts Dr., Accounts Payable Dr., Inventory Cr., and Cash Cr.

- General journal.

Instructions

Using the selected accounts provided:

- Record the January transactions in the appropriate journal noted.

- Foot and crossfoot all special journals.

- Show how postings would be made by placing ledger account numbers and checkmarks as needed in the journals. (Actual posting to ledger accounts is not required.)

Journalize in sales and cash receipts journals; post; prepare a trial balance; prove control to subsidiary; prepare adjusting entries; prepare an adjusted trial balance.

PG-5A Presented below are the purchases and cash payments journals for Rosalez Co. for its first month of operations.

In addition, the following transactions have not been journalized for July. The cost of all merchandise sold was 65% of the sales price.

July 1 |

A. Rosalez invested €80,000 in cash in exchange for ordinary shares. |

6 |

Sold merchandise on account to Dorfner Co. €6,900 terms 1/10, n/30. |

7 |

Made cash sales totaling €5,900. |

8 |

Sold merchandise on account to Bonilha €3,600, terms 1/10, n/30. |

10 |

Sold merchandise on account to L. Ortiz €4,900, terms 1/10, n/30. |

13 |

Received payment in full from Bonilha. |

16 |

Received payment in full from L. Ortiz. |

20 |

Received payment in full from Dorfner Co. |

21 |

Sold merchandise on account to M. Putzi €5,000, terms 1/10, n/30. |

29 |

Returned damaged goods to T. Cigale and received cash refund of €520. |

Instructions

- Open the following accounts in the general ledger.

101 Cash 332 Cash Dividends 112 Accounts Receivable 401 Sales Revenue 120 Inventory 414 Sales Discounts 127 Supplies 505 Cost of Goods Sold 131 Prepaid Rent 631 Supplies Expense 201 Accounts Payable 729 Rent Expense 311 Share Capital—Ordinary - Journalize the transactions that have not been journalized in the sales journal, the cash receipts journal (see Illustration G-8), and the general journal.

- Post to the accounts receivable and accounts payable subsidiary ledgers. Follow the sequence of transactions as shown in the problem.

- Post the individual entries and totals to the general ledger.

- Prepare a trial balance at July 31, 2017.

- Determine whether the subsidiary ledgers agree with the control accounts in the general ledger.

- The following adjustments at the end of July are necessary.

- (1) A count of supplies indicates that €210 is still on hand.

- (2) Recognize rent expense for July, €500.

- Prepare the necessary entries in the general journal. Post the entries to the general ledger.

- Prepare an adjusted trial balance at July 31, 2017.

Journalize in special journals; post; prepare a trial balance.

PG-6A The post‐closing trial balance for Amland AG is as follows.

The subsidiary ledgers contain the following information: (1) accounts receivable—M. Barajas €2,500, J. Clare €7,500, and E. Divine €5,000; (2) accounts payable—B. Forrest €10,000, L. Gold €18,000, and A. Qazi €15,000. The cost of all merchandise sold was 60% of the sales price.

The transactions for January 2017 are as follows.

Jan. 3 |

Sell merchandise to T. Payton €4,600, terms 2/10, n/30. |

5 |

Purchase merchandise from P. Yang €2,800, terms 2/10, n/30. |

7 |

Receive a check from E. Divine €3,500. |

11 |

Pay freight on merchandise purchased €300. |

12 |

Pay rent of €1,000 for January. |

13 |

Receive payment in full from T. Payton. |

14 |

Post all entries to the subsidiary ledgers. Issued credit of €300 to M. Barajas for returned merchandise. |

15 |

Send A. Qazi a check for €14,850 in full payment of account, discount €150. |

17 |

Purchase merchandise from E. Monty €1,600, terms 2/10, n/30. |

18 |

Pay sales salaries of €2,500 and office salaries €2,000. |

20 |

Give L. Gold a 60‐day note for €18,000 in full payment of account payable. |

23 |

Total cash sales amount to €9,100. |

24 |

Post all entries to the subsidiary ledgers. Sell merchandise on account to J. Clare €7,400, terms 1/10, n/30. |

27 |

Send P. Yang a check for €950. |

29 |

Receive payment on a note of €37,000 from W. Lague. |

30 |

Post all entries to the subsidiary ledgers. Return merchandise of €300 to E. Monty for credit. |

Instructions

- Open general and subsidiary ledger accounts for the following.

101 Cash 311 Share Capital—Ordinary 112 Accounts Receivable 401 Sales Revenue 115 Notes Receivable 412 Sales Returns and Allowances 120 Inventory 414 Sales Discounts 157 Equipment 505 Cost of Goods Sold 158 Accumulated Depreciation—Equipment 726 Salaries and Wages Expense 200 Notes Payable 729 Rent Expense 201 Accounts Payable - Record the January transactions in a sales journal, a single‐column purchases journal, a cash receipts journal (see Illustration G-8), a cash payments journal (see Illustration G-15), and a general journal.

- Post the appropriate amounts to the general ledger.

- Prepare a trial balance at January 31, 2017.

- Determine whether the subsidiary ledgers agree with controlling accounts in the general ledger.

PROBLEMS: SET B

Journalize transactions in cash receipts journal; post to control account and subsidiary ledger..

PG-1B Caspari Company’s chart of accounts includes the following selected accounts.

| 101 | Cash | 401 | Sales Revenue |

| 112 | Accounts Receivable | 414 | Sales Discounts |

| 120 | Inventory | 505 | Cost of Goods Sold |

| 311 | Share Capital—Ordinary |

On June 1, the accounts receivable ledger of Caspari Company showed the following balances: Detwiler & Son £2,500, Flores Co. £1,900, Glaimo Bros. £1,600, and Loomis Co. £1,800. The June transactions involving the receipt of cash were as follows.

| June | 1 |

Shareholders invested £12,000 additional cash in the business, in exchange for ordinary shares. |

3 |

Received check in full from Loomis Co. less 2% cash discount. | |

6 |

Received check in full from Flores Co. less 2% cash discount. | |

7 |

Made cash sales of merchandise totaling £7,220. The cost of the merchandise sold was £4,800. | |

9 |

Received check in full from Detwiler & Son less 2% cash discount. | |

11 |

Received cash refund from a supplier for damaged merchandise £370. | |

15 |

Made cash sales of merchandise totaling £4,900. The cost of the merchandise sold was £3,180. | |

20 |

Received check in full from Glaimo Bros. £1,600. |

Instructions

- Journalize the transactions above in a six‐column cash receipts journal with columns for Cash Dr., Sales Discounts Dr., Accounts Receivable Cr., Sales Revenue Cr., Other Accounts Cr., and Cost of Goods Sold Dr./Inventory Cr. Foot and crossfoot the journal.

- Insert the beginning balances in the Accounts Receivable control and subsidiary accounts, and post the June transactions to these accounts.

- Prove the agreement of the control account and subsidiary account balances.

Journalize transactions in multi‐column purchases journal; post to the general and subsidiary ledgers..

PG-2B Grypp SE’s chart of accounts includes the following selected accounts.

| 112 | Accounts Receivable | 401 | Sales Revenue |

| 120 | Inventory | 412 | Sales Returns and Allowances |

| 126 | Supplies | 505 | Cost of Goods Sold |

| 157 | Equipment | 610 | Advertising Expense |

| 201 | Accounts Payable |

On November 1, the accounts payable ledger of Grypp showed the following balances: C. Holt & Co. €4,500, O. Kroll €2,350, K. Radaj €1,000, and Weber Bros. €1,500. The November transactions involving the payment of cash were as follows.

| Nov. | 1 |

Purchased merchandise, check no. 11, €1,190. |

3 |

Purchased store equipment, check no. 12, €1,700. | |

5 |

Paid Weber Bros. balance due of €1,500, less 2% discount, check no. 13, €1,470. | |

11 |

Purchased merchandise, check no. 14, €2,000. | |

15 |

Paid K. Radaj balance due of €1,000, less 3% discount, check no. 15, €970. | |

16 |

Paid cash dividend of €500, check no. 16. | |

19 |

Paid O. Kroll in full for invoice no. 1245, €1,200 less 1% discount, check no. 17, €1,188. | |

25 |

Paid premium due on one‐year insurance policy, check no. 18, €3,000. | |

30 |

Paid C. Holt & Co. in full for invoice no. 832, €3,500, check no. 19. |

Instructions

- Journalize the transactions above in a four‐column cash payments journal with columns for Other Accounts Dr., Accounts Payable Dr., Inventory Cr., and Cash Cr. Foot and crossfoot the journal.

- Insert the beginning balances in the Accounts Payable control and subsidiary accounts, and post the November transactions to these accounts.

- Prove the agreement of the control account and the subsidiary account balances.

Journalize transactions in multi‐column purchases journal; post to the general and subsidiary ledgers..

PG-3B The chart of accounts of Ervin A. Ş includes the following selected accounts.

| 112 | Accounts Receivable | 401 | Sales Revenue |

| 120 | Inventory | 412 | Sales Returns and Allowances |

| 126 | Supplies | 505 | Cost of Goods Sold |

| 157 | Equipment | 610 | Advertising Expense |

| 201 | Accounts Payable |

In May, the following selected transactions were completed. All purchases and sales were on account except as indicated. The cost of all merchandise sold was 65% of the sales price.

| May | 2 |

Purchased merchandise from Yan Company |

3 |

Received freight bill from Porter Freight on Yan purchase |

|

5 |

Made sales to Eder Company |

|

8 |

Purchased merchandise from Quirk Company |

|

10 |

Received credit on merchandise returned to Zamora Company |

|

15 |

Purchased supplies from Rizio Supply |

|

16 |

Purchased merchandise from Yan Company |

|

17 |

Returned supplies to Rizio Supply, receiving credit |

|

18 |

Received freight bills on May 16 purchases from Porter Freight |

|

20 |

Returned merchandise to Yan Company receiving credit |

|

23 |

Made sales to Dixon Bros. |

|

25 |

Received bill for advertising from Anshus Advertising |

|

26 |

Granted allowance to Lamb Company for merchandise damaged in shipment |

|

28 |

Purchased equipment from Rizio Supply |

Instructions

- Journalize the transactions above in a purchases journal, a sales journal, and a general journal. The purchases journal should have the following column headings: Date, Account Credited (Debited), Ref., Accounts Payable Cr., Inventory Dr., and Other Accounts Dr.

- Post to both the general and subsidiary ledger accounts. (Assume that all accounts have zero beginning balances.)

- Prove the agreement of the control and subsidiary accounts.

Journalize transactions in special journals..

PG-4B Selected accounts from the chart of accounts of Linvik NV are shown below.

| 101 | Cash | 201 | Accounts Payable |

| 112 | Accounts Receivable | 401 | Sales Revenue |

| 120 | Inventory | 414 | Sales Discounts |

| 126 | Supplies | 505 | Cost of Goods Sold |

| 140 | Land | 610 | Advertising Expense |

| 145 | Buildings |

The cost of all merchandise sold was 70% of the sales price. During October, Linvik completed the following transactions.

| Oct. | 2 |

Purchased merchandise on account from Cutler Company €13,500. |

4 |

Sold merchandise on account to Ebert Co. €7,700, invoice no. 204, terms 2/10, n/30. | |

5 |

Purchased supplies for cash €80. | |

7 |

Made cash sales for the week totaling €8,800. | |

9 |

Paid in full the amount owed Cutler Company less a 2% discount. | |

10 |

Purchased merchandise on account from Frinzi Ltd. €3,500. | |

12 |

Received payment from Ebert Co. for invoice no. 204. | |

13 |

Returned €210 worth of damaged goods purchased on account from Frinzi Ltd. on October 10. | |

14 |

Made cash sales for the week totaling €8,180. | |

16 |

Sold a parcel of land for €27,000 cash, the land’s original cost. | |

17 |

Sold merchandise on account to B. Reblin & Co. €5,350, invoice no. 205, terms 2/10, n/30. | |

18 |

Purchased merchandise for cash €2,450. | |

21 |

Made cash sales for the week totaling €8,200. | |

23 |

Paid in full the amount owed Frinzi Ltd. for the goods kept (no discount). | |

25 |

Purchased supplies on account from Lewis Co. €310. | |

25 |

Sold merchandise on account to Marco Ltd. €5,220, invoice no. 206, terms 2/10, n/30. | |

25 |

Received payment from B. Reblin & Co. for invoice no. 205. | |

26 |

Purchased for cash a small parcel of land and a building on the land to use as a storage facility. The total cost of €35,000 was allocated €21,000 to the land and €14,000 to the building. | |

27 |

Purchased merchandise on account from Lisa Co. €8,500. | |

28 |

Made cash sales for the week totaling €7,540. | |

30 |

Purchased merchandise on account from Cutler Company €14,000. | |

30 |

Paid advertising bill for the month from the Gazette, €400. | |

30 |

Sold merchandise on account to B. Reblin & Co. €4,760, invoice no. 207, terms 2/10, n/30. |

Linvik uses the following journals.

- Sales journal.

- Single‐column purchases journal.

- Cash receipts journal with columns for Cash Dr., Sales Discounts Dr., Accounts Receivable Cr., Sales Revenue Cr., Other Accounts Cr., and Cost of Goods Sold Dr./Inventory Cr.

- Cash payments journal with columns for Other Accounts Dr., Accounts Payable Dr., Inventory Cr., and Cash Cr.

- General journal.

Instructions

Using the selected accounts provided:

- Record the October transactions in the appropriate journals.

- Foot and crossfoot all special journals.

- Show how postings would be made by placing ledger account numbers and check marks as needed in the journals. (Actual posting to ledger accounts is not required.)

Journalize in purchases and cash payments journals; post; prepare a trial balance; prove control to subsidiary; prepare adjusting entries; prepare an adjusted trial balance..

PG-5B Presented on the next page are the sales and cash receipts journals for Wesley Co. for its first month of operations.

In addition, the following transactions have not been journalized for February 2017.

| Feb. | 2 |

Purchased merchandise on account from T. Valentine €4,600, terms 3/10, n/30. |

7 |

Purchased merchandise on account from B. Kucera for €28,000, terms 1/10, n/30. | |

9 |

Paid cash of €1,300 for purchase of supplies. | |

12 |

Paid €4,462 to T. Valentine in payment for €4,600 invoice, less 3% discount. | |

15 |

Purchased equipment for €7,700 cash. | |

16 |

Purchased merchandise on account from E. Nicks €2,700, terms 2/10, n/30. | |

17 |

Paid €27,720 to B. Kucera in payment of €28,000 invoice, less 1% discount. | |

20 |

Paid cash dividend of €1,100. | |

21 |

Purchased merchandise on account from D. Hachey for €7,800, terms 1/10, n/30. | |

28 |

Paid €2,700 to E. Nicks in payment of €2,700 invoice. |

Instructions

- Open the following accounts in the general ledger.

101 Cash 311 Share Capital—Ordinary 112 Accounts Receivable 332 Cash Dividends 120 Inventory 401 Sales Revenue 126 Supplies 414 Sales Discounts 157 Equipment 505 Cost of Goods Sold 158 Accumulated Depreciation—Equipment 631 Supplies Expense 201 Accounts Payable 711 Depreciation Expense - Journalize the transactions that have not been journalized in a one‐column purchases journal and the cash payments journal (see Illustration G-15).

- Post to the accounts receivable and accounts payable subsidiary ledgers. Follow the sequence of transactions as shown in the problem.

- Post the individual entries and totals to the general ledger.

- Prepare a trial balance at February 28, 2017.

- Determine that the subsidiary ledgers agree with the control accounts in the general ledger.

- The following adjustments at the end of February are necessary.

- A count of supplies indicates that €390 is still on hand.

- Depreciation on equipment for February is €160.

- Prepare an adjusted trial balance at February 28, 2017.

COMPREHENSIVE PROBLEM

CPG-1 Zweifel SE has the following opening account balances in its general and subsidiary ledgers on January 1 and uses the periodic inventory system. All accounts have normal debit and credit balances.

In addition, the following transactions have not been journalized for January 2017.

| Jan. | 3 |

Sell merchandise on account to W. Rayms €3,600, invoice no. 510, and M. Fischer €1,800, invoice no. 511. |

5 |

Purchase merchandise on account from K. Zapfel €3,000 and J. Liotta €2,400. | |

7 |

Receive checks for €4,000 from L. Longhini and €2,000 from M. Hall. | |

8 |

Pay freight on merchandise purchased €180. | |

9 |

Send checks to O. Kitson for €9,000 and L. Quinn for €11,000. | |

9 |

Issue credit of €240 to M. Fischer for merchandise returned. | |

10 |

Summary cash sales total €15,500. | |

11 |

Sell merchandise on account to G. Dukes for €1,900, invoice no. 512, and to L. Longhini €900, invoice no. 513. Post all entries to the subsidiary ledgers. | |

12 |

Pay rent of €1,000 for January. | |

13 |

Receive payment in full from W. Rayms and M. Fischer. | |

15 |

Pay cash dividend of €650. | |

16 |

Purchase merchandise on account from L. Quinn for €15,000, from O. Kitson for €13,900, and from K. Zapfel for €1,500. | |

17 |

Pay €400 cash for office supplies. | |

18 |

Return €200 of merchandise to O. Kitson and receive credit. | |

20 |

Summary cash sales total €17,750. | |

21 |

Issue €15,000 note to D. Markoff in payment of balance due. | |

21 |

Receive payment in full from L. Longhini. Post all entries to the subsidiary ledgers. | |

22 |

Sell merchandise on account to W. Rayms for €3,700, invoice no. 514, and to G. Dukes for €800, invoice no. 515. | |

23 |

Send checks to L. Quinn and O. Kitson in full payment. | |

25 |

Sell merchandise on account to M. Hall for €3,500, invoice no. 516, and to M. Fischer for €6,100, invoice no. 517. | |

27 |

Purchase merchandise on account from L. Quinn for €12,500, from J. Liotta €1,200, and from K. Zapfel for €2,800. | |

28 |

Pay €200 cash for office supplies. | |

31 |

Summary cash sales total €22,920. | |

31 |

Pay sales salaries of €4,300 and office salaries of €3,100. |

Instructions

- Record the January transactions in the appropriate journal—sales, purchases, cash receipts, cash payments, and general.

- Post the journals to the general and subsidiary ledgers. Add and number new accounts in an orderly fashion as needed.

- Prepare a trial balance at January 31, 2017, using a worksheet. Complete the worksheet using the following additional information.

- Office supplies at January 31 total €580.

- Insurance coverage expires on October 31, 2017.

- Annual depreciation on the equipment is €1,500.

- Interest of €30 has accrued on the note payable.

- Inventory at January 31 is €12,600.

- Prepare an income statement and a retained earnings statement for January and a statement of financial position at the end of January.

- Prepare and post the adjusting and closing entries.

- Prepare a post‐closing trial balance, and determine whether the subsidiary ledgers agree with the control accounts in the general ledger.