CHAPTER 7

Work Optional (a.k.a. Retirement)

Retirement can sound like a snooze-fest because unless you're close to retiring, you are saving for something that is very far away. It's hard to say no to money now to reap the rewards much later. But the benefits are big.

The Power of Compound Interest

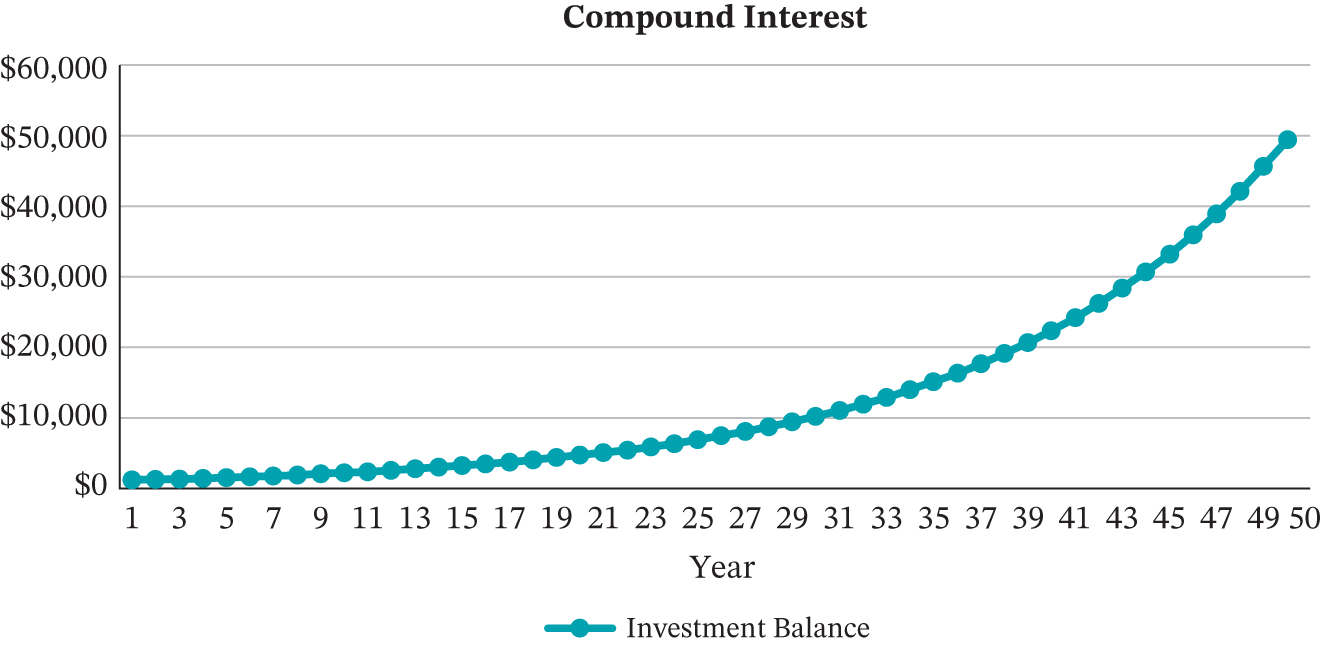

When it comes to investing (for retirement and otherwise), especially when we're starting early, there's a beautiful phenomenon called compound interest that helps our money grow exponentially. Look at this chart:

Oh, it's beautiful! How it works: You invest $1,000 and it grows by 8% each year. Over the past 30 years the S&P 500, which is often used as a proxy for the market, has had an annual return of 8.29% (adjusting for inflation). After the first year you have $1,083, by year 15 you have $3,302, and at year 50 you have $53,631 (over 53× what you started with).

“Fun” poll: Would you rather have a penny that doubles for 30 days or $1,000,000?

Drumroll …

On day 30 the doubling penny would be almost $5.4 million. Well, that escalated quickly.

The rule of 72 states that your estimated return divided by 72 is how long it takes your money to double. What!? So in this case, using 8.29%, your money would double every nine years. Not bad.

TLDR (but please always read): The earlier you start, the more time you're giving your money to compound and grow exponentially.

What Does Retirement Actually Mean?

Retirement means work is optional. Work optional is a term I learned from our friend Tanja Hester (her first book was titled Work Optional). Retirement is often associated with an age, but work optional is the point in your life at which you no longer need to work to pay your bills.

You have saved enough money (in what may be called a nest egg) that you can live off your investments. Your income is made up of a combination of your investment returns (or investment growth and dividends) and selling the investments themselves.

Where Do We Keep This Magical Nest Egg?

One of the first ways we invest is via our 401(k). It's a great place to start and a great place to learn about investing. A 401(k) is a company-sponsored retirement plan. If we have a 401(k) plan with our employer, we can elect to have a certain percentage of our salary taken out and contributed to this plan.

At the very least, we want to maximize our company 401(k) matching because it's free money our company gives us for investing in our own retirement. Wait, what? Yes, free money. Well, not actually free – it's part of your total compensation and if you're not maximizing your match, you're leaving money on the table.

401(k) Matching

If your employer offers 401(k) matching, you will typically see it offered as a percentage of your salary – let's say 3%. That means that if you contribute 3% to your 401(k), your company will match it (i.e., double it). If you contribute 4%, your company will still contribute 3%. If you contribute 1%, your company will contribute 1%. If you earn $75,000, your company match can total $2,250 (3%). That's a 100% return on your first $2,250 of contributions!

Even if your employer doesn't match, there are major tax benefits to contributing to a 401(k).

- The amount you contribute can reduce your taxable income. Off the bat, you're paying less in taxes and this could even put you in a lower tax bracket.

- The investments grow tax-free. In your non-retirement accounts, you have to pay taxes on your profit (more on this in Chapter 8); in your retirement accounts, you don't. These accounts grow and compound for many years, so not paying taxes on this profit will end up saving you a lot of money. Depending on the type of account, you may have to pay taxes when you take the money out of it (more on this soon).

If Your Employer Doesn't Offer a 401(k)

- You can open an IRA (individual retirement account) on your own.

- If you run your own business, you can open a self-employed retirement plan.

- If you work for a nonprofit, you may have a 403(b) that will function very similarly to a 401(k).

- If you work for the federal government, you may have a Basic Benefit plan (a pension) and a Thrift Savings Plan (TSP), which operates a lot like a 401(k). State and local government employees receive similar options with different names.

- If you are a teacher. it's more complicated. I sat down with Dan Otter, the founder of 403bwise, a nonprofit that helps teachers better understand their retirement plans and advocates for access to lower-cost investment choices. I have a must-read guide for you in the Financial Adulting toolkit.

More 401(k) Deets

You elect a certain percentage of your salary to go to your 401(k). The maximum amount you can contribute per year is $20,500 in 2022 (or $27,000 if you are over age 50). The deadline to contribute is December 31st of that year.

It might sound like no fun to have your employer take out part of your paycheck before you even see it, but it feels less painful than it sounds because it's coming out pretax. With your 401(k) you receive a set of investment options to choose from. Some plans have better options than others.

You can withdraw as much money as you want after you're 59½, but if you take money out before then, you pay a 10% penalty (plus the taxes owed). There are exceptions that allow you to take money out without a penalty or you can take out a loan from yourself, but generally, if possible, I like to think of this money as untouchable. We're letting it work its magic.

More IRA Deets

An IRA (individual retirement account) is a plan that you can open up on your own (without your employer). You can contribute up to $6,000 in 2022 (or $7,000 if you are over 50 years old). The deadline to contribute is the same as the tax deadline (typically April 15th). This gives you a few more months than a 401(k).

With an IRA, you can invest in anything available to you in your brokerage account, which is an account that allows you to deposit money and buy and sell investments. I talk about how to choose one in the next chapter. You can even open a self-directed IRA and invest in real estate and alternative investments (anything outside of stocks, bonds, and cash).

The same withdrawal rules apply but vary slightly, depending on whether it's a Roth or Traditional IRA (see the chart in the next section).

What the Heck Does Roth versus Traditional Mean?

Roth and Traditional are essentially tax designations that apply to 401(k)s and IRAs. With a Roth account you pay taxes now. With a Traditional account you pay taxes when you take the money out. In both accounts, the investments grow tax-free.

Which is better?

“Fun” fact: If your tax rate now is the same as your tax rate when you retire, there is no tax difference between what you will owe with a Roth and Traditional account. Cool, right? Yes, I know. My sense of cool is quite warped.

Let's say you earn $100,000, contribute 15% to your 401(k), your income tax rate is 30% both now and when you retire, you're 30 years old, plan to retire at 67 (in 37 years), and you earn 7% return on your investments each year. To keep it simple, let's also say you never earn a raise (I know, that's not cool, but this is pretend, so bear with me).

If you contributed to a Roth 401(k), you'd have $1,683,543 after 37 years. Nice! You wouldn't have to pay any taxes on that money when you take it out. If you contributed to a Traditional 401(k), you'd have $2,405,061 after the same period but you'd still have to pay 30% in income taxes when you take the money out. Apply a 30% tax rate to $2,405,061 and you get $1,683,543. The same number!

Generally, if you think you're in a lower tax bracket now than you will be when you plan to take the money out (i.e., you think you'll be earning more then), then it makes more sense to pay taxes now. Important caveat: This assumes tax rates look similar to what they are now when we retire, but we don't actually know what they will be. Paying taxes now can avoid some tax risk in the case taxes go up.

Contributing to a Traditional IRA has another benefit. It can reduce your tax bill now (depending on your income and if you are offered a 401(k) plan at work). More on this in Chapter 11.

There are some other differences between the two. With a Roth IRA, you can take out the amount you've contributed penalty-free. Roth and Traditional 401(k)s have some penalty-free reasons you may take out funds, but ideally, you leave the money in and let it grow!

The Backdoor Is Open

There is a rule that you can only contribute to a Roth IRA if your income is below a certain amount (this does not apply to a Roth 401(k)). Your MAGI (modified adjusted gross income) must be less than $144,000 for 2022 if you're single and $214,000 if you're married filing jointly.

But if you earn more than the limit and still want to contribute, don't worry. You can do what's called a “backdoor Roth IRA” (for now… there is proposed legislation to change this). It's a completely legal way for you to contribute to a Traditional IRA and roll it into a Roth if you earn above the income limit. Another win for high earners.

Here's a summary of the differences between Roth and Traditional IRAs and 401(k)s.

| Traditional IRA | Roth IRA | |

|---|---|---|

| Funded with | Pre-tax $ | After-tax $ |

| Contribution limits for 2022 | $6,000 ($7,000 if age 50+) | $6,000 ($7,000 if age 50+) |

| Taxes | Contributions may be tax-deductible; taxes are paid when money is taken out | Contributions are not tax-deductible; no taxes are paid when money is taken out |

| Generally best for those who believe their tax rate will be | Lower in retirement | Higher in retirement |

| Income limits | None | $144,000 single; $214,000 married filing jointly (see backdoor) |

| Required minimum distributions | At age 72 | None |

| Withdrawing $ before 59½ years old | 10% penalty on all withdrawals (and income tax)* | The amount contributed can be withdrawn penalty-free; otherwise, 10% penalty* |

* Both Roth and Traditional IRAs offer the same penalty-free withdrawal exceptions including up to $10,000 for a home, qualified education expenses, and health insurance premiums, among others.

| Traditional 401(k) | Roth 401(k) | |

|---|---|---|

| Funded with | Pre-tax $ | After-tax $ |

| Contribution limits for 2022 | $20,500 ($27,000 if age 50+) | $20,500 ($27,000 if age 50+) |

| Taxes | Contributions may be tax-deductible; taxes are paid when money is taken out | Contributions are not tax-deductible; no taxes are paid when money is taken out |

| Generally best for those who believe their tax rate will be | Lower in retirement | Higher in retirement |

| Income limits | None | None |

| Required minimum distributions | At age 72 | At age 72 |

| Withdrawing $ before 59½ years old | 10% penalty on all withdrawals (and income tax)* | The amount contributed can be withdrawn penalty-free; otherwise, 10% penalty* |

* 401(k)s may offer exceptions to the withdrawal penalty, including medical bills and permanent disability. Look at the specifics of your plan.

Show Me the Money – How Much?

Lauren Anastasio, a CFP and director of financial advice at Stash (you met her back in Chapter 5), says 15% of your income is a great retirement savings goal for those looking to retire in their mid-to-late 60s and want to maintain a similar lifestyle. We love simple guidelines!

Another general guideline I've heard many times is that you can calculate how much you need to retire by taking the amount you want to earn in retirement and multiply it by 25. So if you want to earn an annual “salary” of $75,000 in retirement, you'd want to have $1.875 million saved. This assumes you take out (or withdraw) 4% of your nest egg each year and need the funds to last for 30 years.

The thing is, when it comes to planning for retirement, there are a lot of variables, many of which we don't and won't know. Like, “How long will I live?” and “How much will life cost then?” Meaning, what will inflation or the rise of prices have been? “How much will my investments grow each year?”

So we do as much as we can and hope for the best.

Just kidding. LOL. What we do is we (or handy online calculators) make very educated assumptions and we check in on our plans each year.

Head to your Financial Adulting toolkit for links to my favorite retirement calculators. I recommend looking at a few to get a range, given that each will use slightly different assumptions. This will tell you how much you need to retire and then how much you want to be contributing now (each year) to get there.

Some information you'll need to use the calculators:

- How much you already have saved for retirement

- Your age

- The age you want to retire

- Your monthly expenses (or how much you want to earn) in retirement

Using the Retirement Calculators

Don't be afraid to play around with the calculators and to try different assumptions. You might plan to retire by 65 but are also curious what it would take to retire by 50. Check out what you'd need in both situations.

When you use some retirement calculators, they'll assume that your spending in retirement will be 70–80% of your current spending. This is an old assumption based on people paying off their homes by the time they retire. Adjust this spending number to what you want or plan to be spending in retirement. This is personal and you set the terms.

Are All Calculators Created Equal?

Rachel Sanborn Lawrence, CFP and lead financial planner at Ellevest, is a fan of calculators that use Monte Carlo simulation. Wow, flashback to my corporate finance class in college. This means that instead of running one scenario that assumes a perfect 7% return each year (with a 50% success rate), Rachel runs 1,000 scenarios and chooses a retirement amount where 700 cases are successful (a 70% success rate). What's success? When it comes to retirement, success means you are able to cover your expenses all the way up until the end of your life. Doing this makes your plan more conservative, and you may end up with more money than you need in retirement, but Rachel says (and I concur), “That's a really good problem to have.”

The Results

If you use the calculators and realize you're behind (or way behind), that's the way it is for most of us. If you haven't started saving for retirement yet or are far from your goal, don't fret (too much). Remember compound interest? Starting small is okay!

I'm a fan of the sneaky increase. You can up your contributions by as little as 1%. Then set a calendar reminder to increase 1% again in four to six weeks. Some 401(k) plans allow for an automatic increase on contributions to make this process easier for you.

If you're not feeling motivated by this faraway goal, look at your face with an age filter. Or look at an older relative and imagine you are them. No, I'm not kidding. A study out of Stanford showed that when participants looked at themselves at a future age, they allocated more than twice as much to their retirement accounts.1 As you decide how much to contribute, imagine yourself in your 60s or 70s. Your future self will thank you. No, I mean it. Have your older future self thank your current self right now, immediately.

What About Social Security?

Social Security is a program created by Franklin D. Roosevelt to provide an income safety net to the elderly and unemployed. Many of us pay into Social Security over the course of our careers and then when we retire, we get a monthly check in return from the government. Currently, to receive Social Security in retirement you have to earn 40 “credits,” which usually equates to about 10 years of work (and paying into the program!).

To get an estimate of what you can expect to earn, create an account at ssa.gov. While the future of Social Security isn't guaranteed, most financial experts I interviewed were hopeful it will be around for future generations’ retirement. Regardless, Social Security income is not a replacement for saving for retirement – it's just a supplemental form of income.

Retirement Accounts Might Be Only Part of the Plan

In some cases you might need or want to supplement your retirement accounts with other investment accounts.

- If you're maxed out. If you want to contribute more than the max to your 401(k) and/or IRA, you can invest for retirement in your brokerage account (often called a taxable account). This may be because you don't have access to a company 401(k) and have hit the IRA max, want to earn more in retirement, are playing catch-up, or because you plan to retire early.

- If you plan to retire early. If you plan to retire before age 59½, you may want to save funds in a taxable (nonretirement) account in order to make withdrawals penalty-free. In many cases, you may be subject to an early withdrawal penalty when you take money out of your 401(k) or IRA prior to the age the IRS chooses. So, having another investment account can give you access to your funds without penalty if you're lucky enough to stop working before then.

Lauren recommends opening multiple investment accounts or bucketing your investments so it's very clear what money is for which goal. You might have retirement money in your investment account but also money for different savings goals (for us, that's the kids’ bar mitzvahs!). That way it's very clear what each dollar is for and, depending on the time frame, you might invest the money for each goal differently.

Retire Early, You Say? Tell Me More

The Financial Independence/Retire Early (FI/RE) movement has gained a lot of popularity with people looking to reach work-optional life before traditional retirement age. When I first started my money journey, the FI/RE movement was just becoming trendy. I saw a bunch of bros eating beans out of cans to save money and thought, I'll pass. I stayed far away.

More recently, I've been inspired by other personal finance experts claiming the FI/RE movement in a very different way. I talked to Kiersten and Julien Saunders from rich & REGULAR, a lifestyle brand that inspires the Black community to build wealth, about their journey to FI/RE. Here's their advice.

It does not have to be deprivation. It doesn't have to be rigid. It's whatever you want it to be. More expenses means less saving now and higher expenses to cover in the future. It affects the timeline.

Traditional FI/RE calculators assume that your expenses will be the same all the time, or have a very specific period where they'll increase (usually at 65) or they decrease over time. This assumes that life isn't happening to you in the interim. If somebody gets sick or you need to pay for something unexpected, it changes. The idea of a number is more of a North Star for us. It's more of a guideline than it is THE goal. It's very similar to weight on a scale. You fluctuate but stay within a certain range.

Kiersten and Julien also warn about the flashy “win big” stories of people who go from $0 to $10 million overnight by investing in something like Bitcoin or NFTs (more on what these are in the next chapter). Many more people have lost a lot of money this way. The far more helpful story is the one where someone saves and invests for 10 years and is able to retire comfortably. It's less sexy but it's real and it's something people can replicate.

The Gender and Racial Retirement Gaps

While some have the goal of retiring early, for many, retiring at all is nothing more than a pipe dream (Kiersten and Julien call this a “retirement crisis”), and a disproportionate number of those who won't be able to afford their retirement are women and people of color.

Half of all U.S. households are at risk of falling short in retirement.2 54% of Black Americans and 61% of Latinos shared that risk, compared to 48% of white Americans.3 Rachel shared that women retire with two-thirds the amount of money as men.4 Due to the wage gaps and disproportionate representation in low-wage jobs and additional debt, for many there just isn't enough money to save for retirement. This affects not only their ability to save but also how much they earn in Social Security later in life.

There's also a lack of access and eligibility to employee-sponsored retirement plans. As you now know, company 401(k)s allow for more than three times the contributions than IRAs. Over two-thirds of white workers have a company retirement plan option, compared with 56% of Black and 44% of Latino workers.5 Those who do have access might not be able to contribute due to eligibility issues, if they've been at the company less than a year or are working part-time. Those without company-sponsored plans might not have the ability to open an IRA because they are unbanked or underbanked.

What you'll start to see is that everything is connected. Social, racial, and gender disparities touch every aspect of someone's financial life. This has a compounding effect on financial well-being, livelihood, access, choices, health, and freedom, among many other things.

Investing Jargon

The money in your retirement accounts needs to be invested to grow. Before we talk about choosing your investments, let's start with some of the jargon. I wish I could be chosen to rename all the investing jargon – it would be much more fun and straightforward. Maybe our investment portfolio could be called a sundae and our asset allocation is the mix of flavors and toppings. If you dig this, Vanguard, you know where to find me.

But for now, the best I can do is teach you to navigate the current language. And that's all it is; it's like learning any new language. When I hear someone speak in French, I have no idea what they are saying. Once I learn some words, I can start to decipher. Actually, I tried to learn French and I failed, so maybe that's not the best example, but you know what I mean.

Risk

Risk gets a bad rap, but good risk equals more return and return means growth for our money. One of the reasons so many of us are scared to start investing is that we believe we could lose all our money. And by we I mean me, too. I was very wary of getting started.

The worst drop in the market in my lifetime (that I can remember) was in 2008, during the Great Recession. So let's look at what would have happened in that terrible scenario. Let's say that you bought $10,000 worth of the S&P 500 (an index of the largest 500 publicly traded companies in the United States) when the market was at its highest in October 2007 (buying at the highest point is also the worst-case scenario, so I'm making this example very juicy). At its lowest point in the Great Recession, you would have lost 57% and been left with $4,322 (which is terrifying).6 But if you held onto it, as of September 24, 2021, you would have had $28,424 (almost three times your initial investment!), or an annual return of over 7%.

This is why it's so important to invest for the long term. When we don't need the money right away, we can wait out drops in the market before selling. We saw this again more recently during the pandemic in March 2020. There were a few really bad weeks in the market but if you waited it out, things went your way in the end.

S&P 500 Index

Source: Yahoo! Finance.

Important fact to remember: You don't actually make or lose money until you sell your investment. I talk more about this in Chapter 8.

Our risk tolerance is our personal tolerance for risk. Understanding it can help us decide what to invest in and get an idea of how we might react if the market were to drop or get volatile.

The truth is, the riskiest part of investing is that we're human. Fear is real and when we're fearful we make emotional spending decisions like selling when our investments are down. Believe me, it might sound easy to avoid making emotional financial decisions, but in the moment, when you're seeing the frenzy on the news, there can be an urgency to try to cut your losses before there's nothing left.

This is where a financial planner, money coach, or accountability partner (I talk more about them soon) can help keep you from making a mistake and losing a lot of money. Because, remember, we haven't lost money until we sell. Risk has a bad rep, but really it's our behavior that gets us in trouble.

Asset Allocation

An asset is something you own and your asset allocation is your mix of investments (or mix of the things you own). The mix we're usually talking about is of stocks, bonds, and cash (all different asset classes). Typically, stocks are viewed as the most risky, then bonds, with cash being the least risky. This is correlated to their return. Stocks have unlimited upside, bonds have a fixed rate of return, and cash earns whatever you can get in your savings account.

“Fun” fact: In reality, cash is losing value because the cost to buy things goes up over time (hello again, inflation).

There's another asset class called “alternatives,” which I mention in the next chapter. This is a catch-all bucket for anything other than stocks, bonds, and cash.

Stock

There are two ways to invest in a company: owning stock or investing in their debt. When you own a share of stock, you own a piece of a company (albeit a very small one). You might also hear this called “shares” or “equity.” Use it in a sentence: “I own stock in General Motors through an ETF, which is one of 12 Fortune 100 companies with a woman CEO” (For a definition of an ETF, see the upcoming “Fund” section).

Bond

When we buy a bond, we're essentially lending someone money – usually a company or government. And in return, we get our money back plus interest. There is an agreed-upon interest rate, which is why a bond is also called a fixed income investment (we get back a fixed amount). Use it in a sentence: “10% of my retirement portfolio is invested in bonds.”

You might hear the term money market fund thrown around. These are funds specifically invested in short-term U.S. government bonds called Treasury bills or “T-bills” and are very low risk. These are a type of bond or fixed income investment.

Diversification

Diversification means not putting all of your eggs in one basket. One of the best ways to get rid of unnecessary investment risk is to invest in a variety of companies, sectors, and geographies.

When you invest in one individual company or industry, there's a risk that the price will go down if something were to happen – for example, if you own stock in airline companies (a specific sector) and then a pandemic hits that halts almost all air travel (like we saw in 2020). Or you own the stock of a specific company and its CEO is charged with sexual harassment.

When you're invested in a fund (defined in the next section) you're invested in many companies. If something happens at one company, in one industry, or a certain geography, it can affect the share price (the value or price of a share) but on a much smaller scale.

Fund

Also called mutual fund, index fund, or exchange-traded fund (ETF). A fund is a type of investment that's made up of pooled money from investors (a.k.a. us!). This pool of money can be invested in stocks, bonds, or a combination of both. I've also heard a fund aptly described as a basket of investments. There are differences between mutual funds, index funds, and ETFs, but for our purposes (and honestly, my purposes, too), they aren't important. If you want to know the differences between them, I've included a link in the Financial Adulting toolkit. There is so much investing information out there. Part of being a financial adult is knowing what you don't need to know.

Funds are a great way to diversify (see the previous “Diversification” section) because by owning one share you can own stocks or bonds in hundreds of companies. Index funds and ETFs are types of low-fee mutual funds.

Portfolio

Saying portfolio is a fancy way of saying “your investments.” Use it in a sentence: “I want to check what's in my portfolio.” Then you log into your investing account to see what's going on with your investments.

Figure Out Your Asset Allocation

Choosing how your assets are allocated is probably your most important decision as an investor (or so some very smart people say). For retirement, Georgia Lee Hussey says, “If you are younger than 50 and you intend to retire at the standard 65 age range, please God, buy equities and not a lot of bonds. You have so much more risk you can take, because there's a lot of time until you need the money.”

There's a general quick calculation to figure out your ideal asset allocation for retirement. Take 120 and subtract your age. That's the percentage of your retirement portfolio that should be invested in stocks rather than bonds. For example, if you are 30, 120 – 30 = 90% stocks and 100% – 90% = 10% bonds.

This is a simplistic calculation for your asset allocation and assumes you can handle fluctuations in your account without reacting and that you plan to retire at the typical retirement age (in your mid-60s). This is a personal decision. Some people prefer to have more of their portfolios in equities (me!) and some prefer less risk. The general takeaway is, if you're far away from retirement, you have the opportunity to take on more risk (and get after that growth). If you want to level up or there's some nuance to your situation, head to our Financial Adulting toolkit for some asset allocation quizzes.

You can also check out some target date funds (more on these in the next section) and see what their asset allocation is for someone retiring around the same time as you. You'll notice that as you get older (and closer to retirement), your portfolio becomes less invested in stocks and more invested in bonds. Knowing what we do about risk, our portfolio becomes less and less risky as we get closer to using the money. Brilliant.

This asset allocation helps us decide which types of funds to choose. For retirement, we'll want to choose at least one stock fund and one bond fund, or a fund that does this for us.

Target Date Funds

Even if we start out with our ideal balance of stocks and bonds, investments move and we get older (sigh) so our asset allocations will get out of whack. We can rebalance or reallocate (jargon alert!) our investments to fit our ideal balance on our own once per year, or we can invest in target date funds. Target date funds are typically named based on the year we plan to retire. So if you plan to retire in 2055, the target date fund will typically be called something like “Target Date 2055.”

Target date funds take the work out of rebalancing for us because they reallocate as we get closer to retirement. As long as the expenses are low, and the allocation matches what you calculate for yourself, these are a great one-stop shop for retirement investing.

Based on your expected year of retirement, the fund makes sure your assets are allocated among stocks and bonds according to the risk associated with your retirement date. As you get closer to retirement, the allocation becomes more heavily weighted in bonds.

Georgia says, “I love a good target date fund. Just make sure it's cheap. Keep it under 0.25%.” She adds, “Cheap and easy is extremely valuable in financial planning because it's less likely that we are going to let anxiousness impede our vision. And honestly, it's just about f***ing doing something and then stop worrying about it. There's a lot of analysis paralysis in this industry. I think that's intentional to funnel people into buying crap they don't need.” Don't you love her?

Those who aren't fans of target date funds usually point to their high expense ratio (coming up in the “What About the Fees?” section). So if you can find a cheap one, great.

Choosing Our Retirement Investments

Target date funds are just one way to invest and might not even be an option in your 401(k) plan. Start with your list of what's available and do some research on each of the fund options. If you are investing your IRA, you will have many more options. Here's what to include in your research.

First, the Name

I know it sounds silly, but some of these funds have such long names. Some even have corresponding roman numerals – like “Obnoxious Investments Fund III.” Eye roll.

Find the ticker symbol or the letters and numbers used to identify that particular investment. That way when you're doing your research, you know you're looking at the right fund. For example, the Vanguard Target Retirement 2055 fund's ticker symbol is VFFVX. That's much easier to type into Google. Go ahead and google it. If it's a target date fund, make sure the year matches or is closest to your retirement date (they typically round to the nearest multiple of 5 like 2045, 2050, 2055, etc.).

What's in the Fund?

You'll find a few (or a bajillion) sites that can give you more information about the fund. Start by looking at what types of investments this fund holds. Is it a target date fund, a fund filled with U.S. stocks or foreign stocks? Does it specify a certain industry or company size? How does it fit into your asset allocation? Hopefully more and more 401(k)s will include ethical funds like ESG funds, which are funds that screen for company environmental, social, and governance practices. I talk about these in detail in the next chapter.

You can also look at how the fund has performed over the past 10 or 20 years. Past performance doesn't guarantee future performance by any means, but, as Rachel says, “it's the best information we have to move forward with.” Yep.

What About the Fees?

Every fund will have a fee in the form of an expense ratio. If you can't find it on the page, hit ctrl F or Command F and search “expense ratio.” This will be a percentage fee that you are charged each year for owning the fund. It's kind of sneaky in that you won't have to send payment anywhere but the money will just be withdrawn from your investment account.

If the expense ratio is 0.15% and your retirement investments are $50,000, you're paying $75 per year. Some funds have high expense ratios. It depends on the type of fund but I typically consider anything above 0.5% to be high and I try to invest in funds with expense ratios well below that. Tony Molina, Product Evangelist at Wealthfront, says that for the big broad indexes (like the S&P 500 or Dow Jones Industrial Average), you can typically get an expense ratio of 0.08% or lower. Another way to look at this fee? If you are paying a fee of 1% and your portfolio earned 8% that year, you only get to keep 7% of those earnings.

Now it's important to note that when it comes to your 401(k) there are limited options and major tax benefits (I talked about them previously) so I give the funds a bit more leniency as far as expense ratios (especially once you've maxed out your IRA).

If you are feeling pressure, I get it. But the good news about choosing investments in your retirement account is you can always switch them as you learn more or your situation changes.

Where Does Asset Allocation Come In?

If you aren't using a target date fund, you're creating your own asset allocation using a stock and a bond fund (or multiple stock and bond funds). Let's say you decide you want 90% of your retirement money in stocks and 10% in bonds. What does that actually look like? If you have $25,000 invested, you'd want $22,500 invested in stock funds (90%) and $2,500 invested in bond funds (10%). How do you actually make that happen? You have two options:

- After doing some research you might realize that you aren't happy with what you're currently invested in. You can sell what you have and invest in your new funds at a 90/10 split. Going forward, you can have your contributions go toward the same 90/10 split. There aren't taxes associated with buying and selling retirement investments, so this method is very workable. Just make sure there aren't other fees associated with buying and selling.

- If you are happy with your current investments, but you're just looking to change your asset allocation, you can change your contributions to build toward that ideal ratio. Let's say you are more heavily invested in bonds than you'd like. You can put all future contributions toward equities until you get to your 90/10 ideal asset allocation.

The market moves so over time our asset allocation can and will get out of whack. I talk about how and when to rebalance our portfolios in Chapter 14.

Look Out for Other Fees

There are other fees to be aware of when it comes to investing. If you hire a financial advisor (typically 0.5–1.5% of your portfolio's value per year) or robo-advisor (0.25–0.35% of your portfolio's value per year) to manage your retirement account, that fee will be on top of what you are paying in fund expense ratios.

There might also be administrative fees like a quarterly or monthly cost to enroll in your plan. In retirement accounts there aren't usually trading commissions (fees for buying and selling funds), but that's something to look out for as well.

Set Your Investing Up to Be Automatic

Now that you know how much you want to be contributing and what you want to invest in, you can log into your retirement account and set it all up. In your 401(k), you will change your contribution percentage as well as your investment choices. If you aren't sure how or where to do this, reach out to your HR or benefits representative.

You can also set up IRA contributions to be automatic, which takes the work out of making contributions and makes it more likely that you'll actually do it.

Some Frequently Asked Retirement Questions

What Is 401(k) Vesting?

Sometimes your 401(k) matching is not all yours right away. Rude, I know! But this is a way for your company to incentivize you to stay. There will be a vesting schedule that tells you how much of your match is yours each year. If your 401(k) match vests over three years, the first third will be yours in the first year, then you receive another third in the second year, and you get the rest the final year. This happens each year with new matching contributions. When you log into your 401(k) website you should be able to see the vested amount and the total amount. The vested amount is the amount you'd be able to take with you if you left your job today.

Should I Roll Over My 401(k)?

It's generally a good idea to roll over old 401(k)s. There's nothing technically wrong with leaving money in your previous 401(k) unless there's less than $1,000 in the account (see the following “fun” fact). Otherwise, the money is yours, and it sits there. Here are some reasons to roll it over:

- Communication issues. Your company will most likely leave you out of communication about plan changes and updates.

- It's a lot to keep track of. Having a bunch of retirement accounts just makes things more complicated. Rolling your account over into your IRA or current 401(k) keeps things simple to track.

- Better investment options. Your new plan might have better options or, if it's an IRA, it essentially has unlimited options.

- Lower fees. If the account has any administration fees or the fund options have high expense ratios, you'll want to roll it over.

“Fun” fact: In certain cases, your employer can move the money from your 401(k). If you have less than $1,000 in your account, an employer is usually allowed to cash it out and cut you a check. You will pay the 10% early withdrawal penalty and any taxes owed if it's a traditional 401(k). If your 401(k) balance is between $1,000 and $5,000, your employer is allowed to roll it over into an IRA. In those cases, you'd want to make the decision before your employer does! If you have more than $5,000 in the account (from contributions at that job), your employer has to leave your money alone.

When you're ready to do it, head to the Financial Adulting toolkit for some pointers.

Should I Choose an “Aggressive” Investing Plan?

If you're young and your company asks you to choose an investment strategy, you most likely will want to choose the aggressive option. I know, I know. Who wants their money invested aggressively? Aggressive sounds horrible and it makes me so mad that that's the way it's described, but more risk (when it's good risk) means more return. And we want this retirement account to grow like a beautiful tree for you.

Saving for College with 529 Plans

Choosing to save for your child's college expenses is a personal decision and it's important to prioritize your own retirement first. Lauren says it's difficult, but she asks parents who are saving for their children's college expenses and not their own retirement, “How do you feel about the potential to be a burden to your children?” because that's the reality. There are student loans available to pay for school and parents can even help pay for those loans or support children in other ways when they can. You'll always have the option to finance an education, but there's no such thing as a retirement loan.

If you have the opportunity to set money aside for your child's future education, 529 plans allow for tax-advantaged investing, a lot like a 401(k) or IRA. You put money in and it grows tax free (no capital gains tax!). When you take the money out to use it for qualified education expenses (see the Financial Adulting toolkit for an extensive list of them), you get to use the money tax free. Depending on the state you live in and your income, some contributions to your 529 plan may be tax deductions. (Sadly, that's not the case in my state.)

Some important things to know about 529 plans:

- You can open one in most states, even if it's not your own. If your state offers tax deductions for contributions, you'll want to open a 529 plan in it.

- You can change the beneficiary. If you contribute to a 529 plan before your child is born, you can put it in your name and change it later. If your child ends up not using the funds, you can transfer them to another child or to someone else.

- You can make automatic contributions so you can set it and forget it.

- If you use the money for expenses that don't qualify, you will get hit with a 10% penalty and pay taxes on the capital gains in the account.

- Watch out for fees. The plans can be free to open and you should be able to find low-fee funds.

- When applying for financial aid, 529 plans are counted as parental assets.

So how much do you need? When my first son was born, I calculated what we would have to contribute to his 529 plan starting the first month of his life to pay for four years of private college tuition by the time he turned 18. To hit that goal we'd have to contribute over $1,000 per month (for 18 years!).7 What about a public in-state institution? $552 per month. That's just absurd. We don't contribute that amount, but we do what we can. Even though the number will be really high, don't forget about compound interest. This money may have a long time to grow. Also remember, having some money set aside is better than nothing. Every amount will help.

I have a calculator for you in the Financial Adulting toolkit that will tell you exactly how much you want to be contributing now to pay for some or all of your child's education.

Other Investing Benefits You Might Get Through Work

Georgia made me giggle when she said, “The HR benefits booklet is a glory.” But she's 100% right. Your company may offer you an HSA plan (which I talk about in detail in Chapter 10), employee stock purchase plan (an opportunity to buy discount stock), restricted stock units (company shares), or stock options (if you work at a startup). In addition, companies are now offering all types of different employee perks. These might be benefits you missed when you started working there because you were too busy hitting the ground running or maybe they've added new benefits since you joined. Go take a look and see what benefits you can use.

Your Financial Adulting Action Items

- Maximize your company match (if you have it).

- Understand your retirement account options, whatever they are. (Teachers: don't miss your special callout!)

- Run some retirement calculators to decide how much you need and what that means you want to contribute each year.

- Set a calendar reminder if you want to increase your contributions over time.

- Revisit the ways we can close the gender and racial financial gaps (covered in detail in Chapter 2).

- Figure out your asset allocation (there are more calculators in the toolkit for that).

- Research and choose your investment options.

- Create a plan to get to your ideal asset allocation.

- Make your retirement investing automatic.

- Roll over any 401(k)s you have with previous employers (or consolidate IRAs).

- If you're a parent, caregiver, or it aligns with your goals, set up a 529 plan to save for a child's college or other education expenses.

- Understand and maximize your work benefits, if available.

Okay, now that you're set up for retirement, let's talk about all other types of investing, including how to become an investor who grows their money and does good in the world. We'll learn from the experts and I'll walk you through it all step by step.

Notes

- 1. Hal E. Hershfield, Daniel G. Goldstein, William F. Sharpe, Jesse Fox, Leo Yeykelis, Laura L. Carstensen, and Jeremy N. Bailenson, “Increasing Saving Behavior Through Age-Progressed Renderings of the Future Self,” Journal of Marketing Research XLVIII (November 2011): S23–S37, https://vhil.stanford.edu/mm/2011/hershfield-jmr-saving-behavior.pdf.

- 2. “National Retirement Risk Index,” Center for Retirement Risk at Boston College, https://crr.bc.edu/special-projects/national-retirement-risk-index/ (there is updated data in total but not broken down by race).

- 3. Alicia H. Munnell, Wenliang Houand, and Geoffrey T. Sanzenbacher, “Trends in Retirement Security by Race/Ethnicity,” Center for Retirement Risk at Boston College (November 2018), https://crr.bc.edu/briefs/trends-in-retirement-security-by-raceethnicity/.

- 4. Elizabeth Olson, “For Many Women, Adequate Pensions Are Still a Far Reach,” New York Times (June 3, 2016), https://www.nytimes.com/2016/06/04/your-money/for-many-women-adequate-pensions-are-still-a-far-reach.html.

- 5. “Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-accessible-20200928.htm#fig5.

- 6. “SNP – SNP Real Time Price. Currency in USD,” Yahoo! Finance (September 30, 2007–October 30, 2007), https://finance.yahoo.com/quote/%5EGSPC/history?period1=1191196800&period2=1193788800&interval=1d&filter=history&frequency=1d&includeAdjustedClose=true.

- 7. “College Cost Calculator,” Calculator.net, https://www.calculator.net/college-cost-calculator.html?todaycost=26820&useaverage=26820&costincrease=5&collegelength=4&savingpercent=35&balancenow=0&returnrate=7&interesttaxrate=0&startin=18&x=32&y=14.