CHAPTER 13

All About Debt

Now we move into the wild world of debt. And believe me, it is a wild world. More than 191 million people in the United States have credit cards, and 120 million of those (almost half of all adults) have credit card debt, making credit cards the most common form of debt. BIPOC have disproportionately more credit card debt, and that debt comes with higher interest rates.

I have a love/hate relationship with credit cards. Some use them as a tool to pay for vacations with points. For others, having the ability to use a credit card to bridge the gap when cash isn't available is a lifeline (albeit an expensive one) because there aren't better options available – and nearly one in four people in the United States can't get approved for a credit card.

When we do get a credit card, it doesn't come with a manual or even any directions. And considering they can change the financial trajectory of our lives for the worse (or much worse), that's a big problem. Understanding how credit cards work can help us make informed decisions. You know … knowledge is power and all that.

What Are Credit Cards?

A credit card is a revolving loan from a bank or other institution. You can use the card to pay for things, pay the balance down, and build up the balance again. It's up to you. And that's why it's called a revolving loan. The loan comes with a plastic card (or other material) that allows you to make purchases. You are given a certain credit limit, which is the maximum you are able to borrow (or put on the card) at any given point in time.

How Credit Cards Work

Each month you'll have a required payment on your credit card (a.k.a. a minimum payment). This is different from your credit card balance or the total amount you owe at any given point in time. That bears repeating. Your minimum payment is not the total amount you owe. It's much less.

Each credit card company calculates its minimum payment differently, but it's often 1–3% of your balance. That's why it's not uncommon for your balance to increase over time when you make minimum payments, even if you're not spending on the card. Woof. I know.

Then there's the interest rate (also called APR or annual percentage rate), which is the amount we pay to compensate the credit card company for lending us the money. The average credit card interest rate is 14.5%, but for some reason most credit cards I see have interest rates upwards of 20–25%.

The APR is applied to the balance that is not paid off at the end of the month (or cycle). For example, if your balance is $1,000 and you make a $30 minimum payment, you'll pay interest on the remaining $970. For an APR of 20%, that's a 20% interest rate per year, but you are charged interest monthly (20% divided by 12) as part of your monthly bill, which comes to about $16 in interest. If you continue to make payments of $30 per month, it would take you 50 months (over four years) to pay down the credit card and you will have paid $471 in interest or 47.1% more than the original $1,000 balance. To find the exact amount, there is typically a line item on your credit card statement titled “interest charges” or something similar.

If you like to get things on sale (who doesn't?), keeping a balance on your credit card is the opposite. You're paying more for something than it costs. And just like compound interest works wonders for our investments, it works against us with our credit card debt. Most credit card companies compound interest daily, meaning the balance used to calculate your interest goes up each day – interest on interest.

It's Time to Let Go of the Shame

Before we move on, we need to address the shame many of us feel about our debt. Sometimes we feel so much shame, we can't even look at our debt or it can even make us physically ill. But what is debt, really? Debt is just money you owe for something you bought. I'll say it again. Debt is just money you owe for something you bought.

That's all it is. It doesn't mean anything is wrong with you. It's not bad. You're not bad.

It's also important to remember how much we have working against us in the first place. If you need a refresher, head back to Chapter 1. Credit cards add to it because they make it feel like we have more money available than we do. And if we are spending more than we'd like, we don't have to deal with it until next month because we're always paying for last month's expenses. That delay can get our spending all out of whack.

We've Got Some Power

If you get charged a late fee, don't be afraid to call your credit card company and ask for it to be removed. If you notice your interest rate is high, you can try reducing that rate as well. Always mention how long you've been a customer and/or how long it's been since your last late payment (if it's been a while). They usually will let you off the hook for the first late payment or two (which can be a $35 fee!). It's easier to negotiate your interest rate down before you are carrying a balance.

Take Inventory of Your Credit Cards

The first step to paying down or managing debt is to take inventory. I've done this with hundreds of people and I promise, while it can feel scary to see everything in one place, it's most often a huge weight off their shoulders. Until we know what's going on, we can't do anything about it.

Start with your credit cards. You can take inventory right here or you can download the Excel debt tracker from the Financial Adulting toolkit. You'll want to gather the name of the credit card (so you know which one it is), the balance (how much you owe right now), the interest rate (or APR), the minimum required payment, the payment date (this can help us see if we have a lot of things due at the same time), and the credit card limit.

Do this for each credit card you have. If this feels overwhelming, start with one card. Breaking steps that feel too big into smaller manageable steps sets us up for success.

Make Your Credit Cards Work for You

With this information, you can make a plan to use credit cards (or not) in the way that makes sense for you. Test out the strategies that seem like a good fit and don't be afraid to pass on the ones that don't.

- Pay off your credit card balance each week. This makes your bank account a better reflection of the cash you have available.

- Don't carry a balance, if possible, to save in interest.

- Use sinking funds to smooth out larger irregular expenses (detailed directions in Chapter 5).

- If you travel for work, have a separate credit card for work travel expenses. This is especially important if it takes time to get reimbursed or you get confused about what's work-related. Also, when our credit card balances are relatively high (travel can do that!) our everyday expenses feel small or like less of a big deal, which can cause us to spend more.

- Make sure any credit card fees you pay are worth the perks. You can calculate the value of your credit card perks based on your spending and lifestyle. We have a special calculator to help you do that in the Financial Adulting toolkit.

On to Student Loans

Before we can make our debt paydown plan, we have to lay out all of our debt, and for many of us, that includes student loans. 70% of people are graduating with some student loans and with college tuition where it is, it's no wonder!

If you think your student loans are complicated, you're right. If you think the systems where you manage your student loans are opaque, you're also right. The good news is, if you already have your student loans, you don't need to know everything about every type; you just want to understand the details of your loans and what that means for your options.

Types of Student Loans

You can break down student loans into two main categories: federal loans (public) and private loans. Federal loans are loans from the government, which sets the interest rate, and there are certain protections in place, including flexible repayment options. Private student loans are provided by banks, credit unions, state agencies, or schools.

Student Loan Repayment Options

One of the most confusing things about student loans, especially federal loans, is the myriad repayment options. Depending on what types of federal loans you have and when you took them out, your options will be different, so not all of these will apply to you. Here are the highlights.

Federal Loan Repayment Options

- Standard: Fixed payments (same payment every month) for 10 years. This is typically the fastest method with the least amount of interest paid. It's not a good option if you qualify for Public Service Loan Forgiveness (PSLF) because you'd want to minimize the amount you pay before the loans are forgiven.

- Graduated: Still pay the loan over 10 years but payments start smaller and increase over time. You pay a little more interest than the standard but it can be a helpful option if it will become easier to make loan payments as you grow in your career.

- Extended: Pay back your loans over a 25-year period. You will pay more interest but the monthly payment will be a lot lower. You have to have $30,000 or more in student loans to be able to do this.

- Income-based repayment options (payments are calculated based on income):

- REPAYE (Revised Pay As You Earn): Payments are 10% of your discretionary income and are recalculated every year. If you are married, your spouse's income will be included in this calculation. Your loans are forgiven after 20 years for an undergrad loan or 25 years for a graduate loan.

- Income-Based Repayment (IBR): Payments are 10 or 15% of monthly discretionary income. Your spouse's income is only included if you file taxes jointly. If you don't want it included, you can file separately. Loans are forgiven after 20–25 years.

- Income-Contingent Repayment (ICR): Monthly payments are the lesser of (1) what you would pay on a repayment plan with a fixed monthly payment over 12 years, adjusted based on your income, or (2) 20% of your discretionary income, divided by 12. Oh, so much math.

- Income-Sensitive Repayment Plan: Pay your loan off in 15 years, but it's based on your annual income.

IMPORTANT “fun” fact about income-based repayment options: In most cases, when your loans are forgiven, the amount forgiven will be counted as taxable income. Say what? If you have $100,000 in loans that are forgiven, that's $100,000 in taxable income coming your way. Using a debt calculator, you can see how big the balance will be at your forgiveness date given your current monthly payments. Then apply your income tax rate to that balance. Set up a sinking fund for that tax bill with the goal of having the money there waiting for you when it comes time to pay it. Otherwise, when your loans are forgiven, you'll switch from having a monthly student loan payment to a monthly payment to the IRS. Blah.

What About Teacher and Public Service Loan Forgiveness (PSLF)?

If you are a teacher and work for five consecutive years, you can have up to $17,500 in loans forgiven as of 2021. For PSLF, you must work full-time for a qualifying company (i.e., a nonprofit or government organization) and your loans will be forgiven after 120 payments (or 10 years). For teachers and people who qualify for PSLF, there is no tax bill that comes with the forgiveness. It's important to check whether you qualify for PSLF and to know what the requirements are and that you are meeting them. If you are a teacher who stays in your job for four years and then leaves, you will not qualify for forgiveness.

What Is Consolidation?

Consolidation is combining all of your federal loans into one payment. Consolidation doesn't change the interest rate. You can lower your monthly payment through consolidation but you will end up paying more over the course of your loans. It's important to know that when you are consolidating your federal loans, any payments you've made toward income-based repayment or forgiveness will be reset. You might see ads for other types of debt consolidation. Outside of federal student loans, this just means refinancing. We talk more about refinancing soon.

Private Loan Repayment Options

Repayment options for private loans are much more simple. Typically you'll pay a fixed payment over the course of 10 years. There are longer and shorter options but the time frame is not standardized and completely depends on the lender. You can typically make payments immediately, fully defer payments until after you finish school, or something in between. The sooner you make payments, the less interest you'll pay, but this isn't an option for many since they will not be able to make payments while they are in school.

Some of the Problems with Student Loans

I sat down with Chris Abkarians, co-founder of Juno and Suraiya Ali, head of content at Juno, which is a company that bulk-negotiates student loan refinancing for its members to get really low rates. You know I love that. Chris and Suraiya helped break down the student loan landscape.

Federal Student Loans

Federal loans make up 90% of all student loans. Take it away, Chris.

Do You Remember the College Scorecard? The Drama Continues …

From Chris:

Private Student Loans

Private loans make up 10% of all student loans and 89% are undergrad loans. Many undergrads use private loans to fill the gap between federal loan limits and the cost of tuition.

Chris says, “If you were to google ‘best student loans’ right now, you'd find many websites with very similar top 10 lists. A lot of people would reasonably assume that if the same place is in the top 10 over and over, that it is probably pretty good, but banks don't get listed on the top for offering the best rates, they get listed on the top by paying more to be put there.”

On the lists of banks, you'll see very wide interest rate ranges from each lender, which impacts your perception of what's a good deal. Suraiya shares, “If the rate range is 3%–12% and you end up with an 8% offer, that seems really good because you know it could have been as high as 12%. But in reality, with your credit score you should be offered 6% and that difference would save you thousands and thousands of dollars.”

Then if you try to ask a financial aid officer to help guide you in the right direction, in most cases, they won't, because there's a regulation that prevents them from making recommendations.

“Fun” fact: Why can't financial aid offices make student loan recommendations? A scandal. Financial aid offices were accepting dinners and other things from private lenders in exchange for recommending them to their students. The regulatory reaction (Chris calls it an overreaction) was to make it so financial aid offices could no longer make recommendations. Chris says it would be great for financial aid offices to work together to get the best deal for their students, but with the regulation they can't do that.

What's the lesson in all this? If you are looking to take out student loans, do your research, expect information to be misleading, and map out what your student loan payments will look like when you graduate (or before) to see if they are workable.

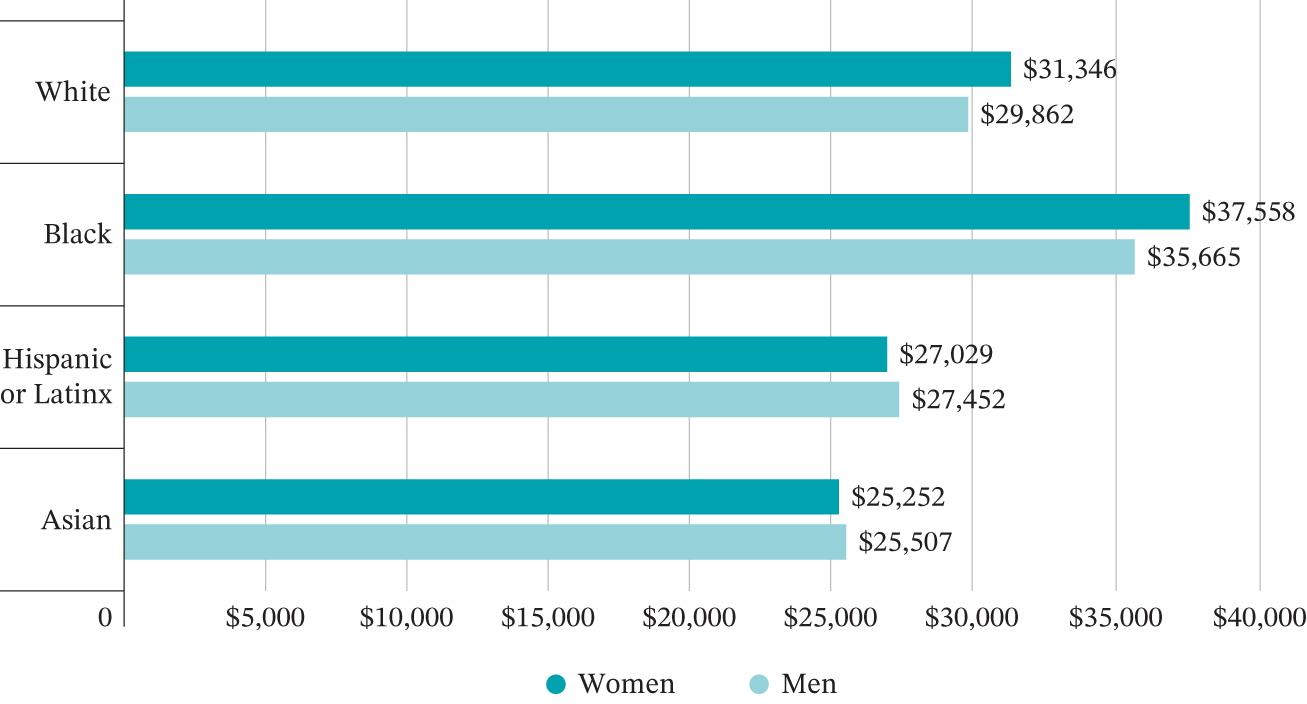

Student Loans Disproportionately Affect the Black Community and Women

Mean Total Borrowed by Gender and Race/Ethnicity

Note: Analysis excludes those who borrowed no money to finance their educations.

Source: AAUW analysis of U.S. Department of Education, National Center for Education Statistics, “B&B:17 Baccalaureate and Beyond Longitudinal Study.”

Suraiya observes, “If a Black individual gets an MBA at the same school as a white individual, and if they're already going to be entering a job market where they're going to be paid less for the same job because they happen to be Black or a person of color, even if they took out the same amount of loans, the amount of time it takes the Black individual to pay those loans off is exponentially higher versus the white individual. And that's only accounting for one type of discrimination – in wages.”

With the wealth gap, BIPOC families are sending their kids to college with less family wealth. If your child isn't going to one of the colleges with a huge endowment to provide financial aid, you have to borrow more. Your child hits a cap on the undergrad loans so you either take out a parent PLUS loan or a private loan. For a private loan, your co-signer's credit score impacts your rate or ability to take out the loan in general and credit scores are racially biased (read up about it in the Financial Adulting toolkit). In many cases, parents take out a parent PLUS loan that they aren't able to pay and the burden is on the student to help them pay that off.

Before You Take Out Student Loans …

If you plan to take out student loans, Chris and Suraiya share two important pieces of advice.

- Reduce the amount you need to borrow. Try to negotiate the amount the school will pay (so you pay less). If you've already been admitted and if you are politely asking for more financial help, the school is not going to rescind your admission in almost any case. Some financial aid officers have shared that men are far more likely to be the ones to ask for a discount than women.

- Rate-shop. Paying for school looks like a pie chart with many pieces adding up to the total. Once you know how much you truly need to borrow and if private loans are part of that, rate-shop!

Take Inventory of Your Student Loans

Now you can take inventory of your student loans. This will look similar to what you did with your credit cards. With student loans, you'll also want to understand when interest starts accruing (if it hasn't already). That information can help you prioritize which loans to pay off first (which comes later).

Add Any Other Debt to Your Tracker

If you have other debt outside of credit cards and student loans, like a mortgage, car loan, or personal loan, you'll want to add those to your debt tracker, too.

Make a Plan to Pay Down Your Debt

Whew! You should be really proud. You've taken inventory of your debt, and it's all organized. Now you are ready to make your debt paydown plan. Here's how to do it.

Prioritize Your Debt; What Comes First?

First you'll want to prioritize which debt you'll plan to pay off first. You'll see a column on your debt tracker where you can rank each piece of debt, starting with #1 (the highest priority) and working your way down the list. How do you decide which comes first? I use one of a combination of three methods.

The snowball method. Pay off the debt with the lowest balance first. This method works really well if you have a card or loan (or a few) with a relatively low balance because it feels amazing to cross it off your list. These wins help us build momentum and I often see people pay down their debt more quickly.

Avalanche method. Pay off the debt with the highest interest rate first. With this method you pay off the most expensive debt first or the debt that technically is costing you the most money. This method works really well if there is a loan or credit card that has a much higher interest rate than the others because paying it off has a big financial impact.

Emotional method. Pay off the debt that has the greatest emotional impact. Sometimes there's a loan that drives us crazy. Maybe you owe your parents money and even though there's no interest you can't wait to pay them back. Or maybe you had a horrible experience with a certain financial institution and you never want to see or hear from them again. If you don't have a loan that elicits a big negative emotional response you can skip this method.

Sometimes our smallest piece of debt also has the highest interest rate. Easy. Sometimes it's really hard to decide which debt comes first. Just go with your gut. I've gone through this exercise with clients and when it's time to put money toward their debt they are moved in a different direction than they had planned. It's okay to change your mind. Just try to understand why you have chosen a certain debt to take priority over the others.

How Much Do You Want to Put Toward Your Debt?

Ideally, if you are paying down credit card debt, you will want to stop using your credit cards so you can clearly see the progress you're making. If you want to continue to use a credit card, I recommend using a separate one, if possible. That way, you can make sure to pay off your balance each month for new expenses.

The most common mistake I see is the tendency to put too much money toward debt each month and then there's not enough money left for expenses and bills so things end up going back on credit cards. I get it, it feels so good to pay down debt – but it then becomes unclear whether you are making progress, because your debt balances are constantly going down and then up again each month. It can start to feel like a futile pay down/build up hamster wheel where you are taking one step forward and two steps back. I don't want that for you.

Plug that amount into your financial plan.

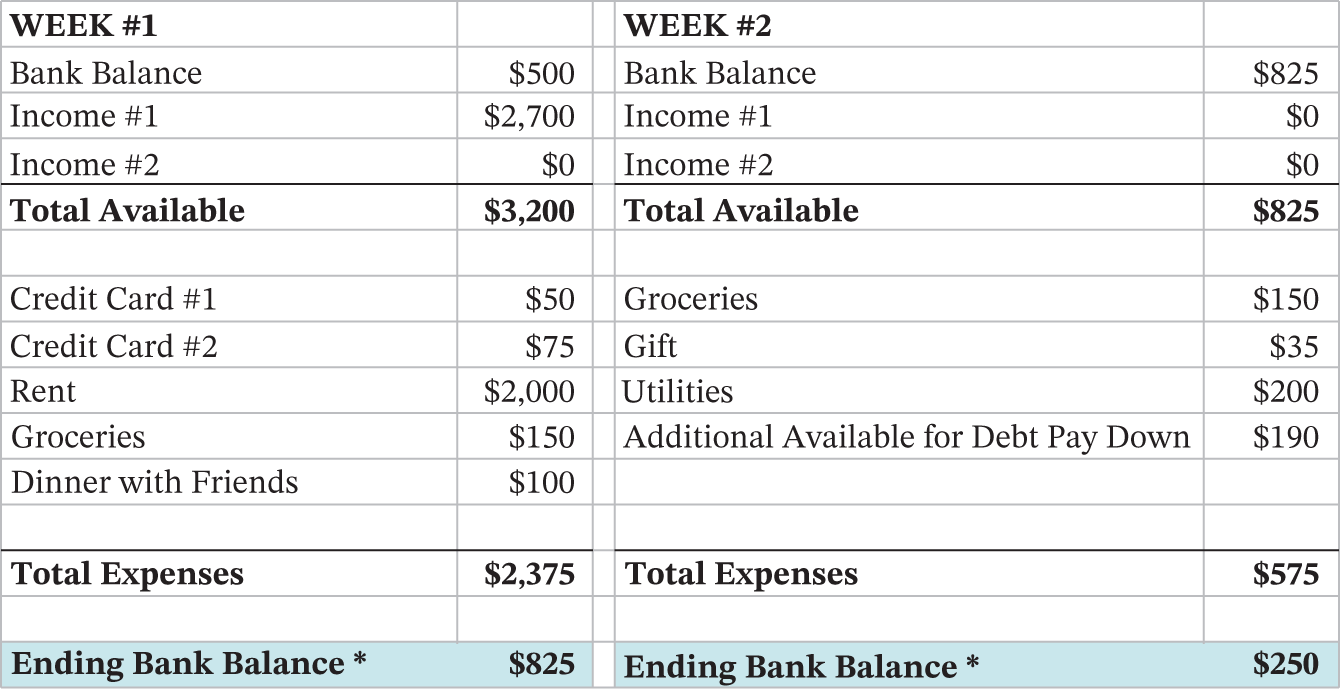

Your New Best Friend – the Cash Tracker

If you want more clarity on how much you can afford to put toward debt, the cash tracker can be life-changing. It does exactly what the name suggests: it helps you map out or track your cash. Start with the amount that will hit your bank account the next time you receive a paycheck or income. Then, list out all the places that money needs to go (including your bills, debt payments, and everyday expenses) over the next week or two weeks.

Look at your calendar when you map out your expenses. If you have dinner plans, you'll want to allocate some money to pay for dinner. If you are going to a birthday party and plan to bring a gift, you'll want to add that to the list. Map out the next two to three paychecks (or four to six weeks). That way, you can account for paychecks or times of the month where you incur higher expenses (like rent or a mortgage).

After you have your plan, it's just as important to enter in what you actually spent as well as update plans when things change. You'll want to use a debit card or cash for the cash tracker to work. Or if you use a credit card, pay off your credit card expenses frequently. We want the amount in your bank account to reflect the amount of cash you actually have as closely as possible.

Your Debt Paydown Recipe

I like recipes or very specific instructions, so that's what you're getting. For your debt paydown plan:

- Pay the minimums and monthly payments on each piece of debt, if possible.

- Any additional amount per month goes toward debt priority #1. You can figure out this amount via your financial plan and cash tracker.

*I like to set a minimum balance for my checking account so there's some cushion. In this case, I used $200.

- Once debt priority #1 is paid off, you will continue to make all the monthly and minimum payments. Any additional money toward debt now goes toward debt priority #2. Don't forget to include the minimum or monthly payment you were paying toward debt priority #1. If that had a minimum payment of $30, that can be an additional $30 that goes to debt priority #2.

- Go down the list until all debt is paid off.

What If I Can't Make My Payments?

If you can't make your debt payments, a great place to start is by creating a health and safety budget (Tiffany Aliche taught us how in Chapter 5) and then once you have an idea of what you can put toward your debt, call up your lender(s). They may offer programs where you can pause payments or decrease the payment amount. If you are unable to make payments on your federal student loans, you may qualify for deferment or forbearance (they are pretty similar). If you qualify for deferment, you can stop making payments on principal (and interest, if your loan is subsidized). If you don't qualify for deferment, forbearance allows you to stop making payments on principal or reduce your monthly payment for up to 12 months. In most cases your loan interest will still accrue and these months won't count toward forgiveness.

During the pandemic in 2020 and 2021, most federal student loans qualified for a student loan payment pause. The interest rate on loans was changed to 0% (for the time) and there were no required payments. Each month still counted toward forgiveness and any payments made went to pay off past interest and then went directly toward principal.

If you are unable to come up with a solution and are not able to make your payments for some time, the late payments will show up on your credit reports and the lender might sell your debt (for a steep discount) to a collections agency. There are very specific ways to handle working with collections. Do some research and even come to the call with a script when you're ready to speak with them.

If your debt situation is extremely unmanageable, there's also bankruptcy, which I mentioned briefly in Chapter 10. This is a huge decision with many repercussions, so it's important to do your research and talk to an attorney before moving forward.

Should I Refinance My Debt?

Refinancing means taking out a new loan (usually at a lower interest rate) to replace some or all of your current debt. The lower interest rate means you'll pay less interest over the course of the loan and it can also lower your monthly payment. You can refinance credit card debt, student loans, and other debt as well. Here's what you need to account for.

Do Your Research without a Hard Inquiry into Your Credit

You'll first do some research to see what's available to you. As you're researching, make sure lenders aren't making hard inquiries into your credit. Hard inquiries typically ding your credit scores for a year and while a few points might not matter, depending on what your score is, that could mean not qualifying for a lower interest rate or could make the difference of your being able to refinance or not.

Run the Numbers

I like to run the numbers on two things: First, how much money I will be saving over the course of the loan with the lower interest rate (you'll find a calculator in the Financial Adulting toolkit). There is usually a fee associated with refinancing – make sure to subtract any refinancing costs from your total savings. If you are saving $100 per month on your loan, and the refinancing costs $300, the cost will break even or start saving you money after three months.

Make Sure the Payment Is Workable

Sometimes when a loan is refinanced, the interest rate is lower but the monthly payment is higher because the loan will be paid off more quickly (in fewer years). It's important to make sure that the new payment is workable with your income and other spending. You don't want to refinance only to feel strapped and stressed to make your monthly payments each month.

Understand What Flexibility and Potential Forgiveness You Are Losing

When you refinance a federal student loan, you'll be taking out a private loan. This means you'll lose the flexibility you get with public loans like the variety of payment options and the forbearance and deferment of payments, and you'll lose any progress toward forgiveness. Chris says he thinks about refinancing like insurance. Look at the difference in your payment (or how much money you'll save from refinancing) against that insurance. Is the difference large enough to be worth it? If it's too small, it won't make sense to lose that insurance.

What About 0% Interest Transfers?

This is a strategy where people move their credit card debt to another credit card that has 0% interest (the 0% lasts for a certain number of months). The idea being you pay everything down while the card is at 0% interest and save all that money. Sounds like a no-brainer, right? The thing is, I've seen this backfire many times. Only do this if you have a very solid plan in place where you are clear based on your income and expenses how you will be able to pay off the credit card before the 0% interest rate expires. It takes discipline and planning. And believe me, the interest rate after the 0% expires is usually extra high. In many cases, people end up with a new high-interest credit card and haven't paid down their initial balance. All this is to say, just like with anything, we need to be honest with ourselves. Does this feel like an option that will work for you? If so, great. If not, stay away.

A Warning When Refinancing Credit Cards

Refinancing credit cards sounds like a great deal (as long as the monthly payment is workable) because credit card interest rates are so high. But this one can be tricky. Brian Walsh shared, “We see a lot of people use the personal loan (from refinancing) to pay off their credit card debt, but if they keep using the credit cards, then a year from now, they have credit card debt and personal loan debt and they're in a worse spot.” I've seen this a lot, too. If you refinance, it works well to close your credit cards, or even all but one if you want to keep something open. If you don't close your credit cards, try to spend with cash or a debit card to prevent building up more credit card debt.

Let's Talk About Buying a Car

For those in the market for a car, I'm sorry. For most people, buying or leasing a car is not a fun process. I think the only person I know who truly enjoys it is Justin (my partner) because he loves to negotiate. He spends days negotiating. Here's how to decide whether buying or leasing is best for you:

- Know your budget (including all the extra things that go into maintaining a car). Don't forget insurance, maintenance costs (scheduled and surprise), gas, and parking (especially if you live in a city).

- Run the numbers. List out what each option (lease vs. buy) would cost you over the next 10 or 20 years (including all the extra things, how long you plan to own the car, and the resale value). I've included an example in the Financial Adulting toolkit. Look at these side by side.

Most financial advice will recommend that you purchase a (used) car. When you run the numbers, buying typically makes the most sense if you keep the car after you pay off the car loan. That's the real kicker. Most people don't do this or don't want to do this. But once you pay off your car loan (which can take 5–10 years) and have a car that's payment-free, that's really when buying rather than leasing saves you a lot of money. Be realistic about your plans. Sometimes seeing how much money it would save is enough to get you on board!

- Do your research and negotiate. It's important to know your stuff going into a negotiation. Know what you want and know what's a good price (resources are in the toolkit). Definitely call up multiple places and negotiate. Give each place a chance to beat the other's lowest price. If they do beat it, go back to the other and continue going back and forth. I know this takes work but it's a big purchase you don't make very often. Some places are looking to meet quotas (especially volume dealers) and will even take a loss on a car in order to meet the quota.

Financial Adulting Checklist

- Let go of the shame around your debt.

- Understand how credit cards work and create strategies to make them work for you.

- Calculate how much you are paying in interest each month.

- Negotiate away late fees, if you have them.

- Understand the student loan landscape and how they disproportionately impact BIPOC and women.

- Before you take out student loans, negotiate the bill (a.k.a. tuition) and shop around.

- Take inventory of your credit cards, student loans, and other debt.

- Make a plan to pay down your debt and update your financial plan to reflect it.

Okay, that's all I've got for debt. You've made it to the final chapter. This is where it all comes together and the magic happens. And I'm excited to introduce you to your new money coach!