9

Initial Public Offerings

Jay R. Ritter

1. INTRODUCTION

An initial public offering (IPO) occurs when a security is sold to the general public for the first time, with the expectation that a liquid market will develop. Although an IPO can be of any debt or equity security, this article will focus on equity issues by operating companies.

Most companies start out by raising equity capital from a small number of investors, with no liquid market existing if these investors wish to sell their stock. If a company prospers and needs additional equity capital, at some point the firm generally finds it desirable to “go public” by selling stock to a large number of diversified investors. Once the stock is publicly traded, this enhanced liquidity allows the company to raise capital on more favorable terms than if it had to compensate investors for the lack of liquidity associated with a privately-held company. Existing shareholders can sell their shares in open-market transactions. With these benefits, however, come costs. In particular, there are certain ongoing costs associated with the need to supply information on a regular basis to investors and regulators for publicly-traded firms. Furthermore, there are substantial one-time costs associated with initial public offerings that can be categorized as direct and indirect costs. The direct costs include the legal, auditing, and underwriting fees. The indirect costs are the management time and effort devoted to conducting the offering, and the dilution associated with selling shares at an offering price that is, on average, below the price prevailing in the market shortly after the IPO. These direct and indirect costs affect the cost of capital for firms going public.

Firms going public, especially young growth firms, face a market that is subject to sharp swings in valuations. The fact that the issuing firm is subject to the whims of the market makes the IPO process a high-stress period for entrepreneurs.

Because initial public offerings involve the sale of securities in closely-held firms in which some of the existing shareholders may possess nonpublic information, some of the classic problems caused by asymmetric information may be present. In addition to the adverse selection problems that can arise when firms have a choice of when and if to go public, a further problem is that the underlying value of the firm is affected by the actions that the managers can undertake. This moral hazard problem must also be dealt with by the market. This article describes some of the mechanisms that are used in practice to overcome the problems created by information asymmetries. In addition, evidence is presented on three patterns associated with IPOs: (i) new issues underpricing, (ii) cycles in the extent of underpricing, and (iii) long-run underperformance. Various theories that have been advanced to explain these patterns are also discussed.

While this chapter focuses on operating companies going public, the IPOs of closed-end funds and real estate investment trusts (REITs) are also briefly discussed. A closed-end fund raises money from investors, which is then invested in other financial securities. The closed-end fund shares then trade in the public market.

The structure of the remainder of this chapter is as follows. First, the mechanics of going public and the valuation of IPOs are discussed. Second, evidence regarding the three empirical patterns mentioned above is presented. Third, an analysis of the costs and benefits of going public is presented in the context of the life cycle of a firm, from founding to its eventual ability to self-finance. This includes a short analysis of venture capital. The costs of going public and explanations for new issues underpricing are then discussed.

2. VALUING IPOs

2.1. The Mechanics of Going Public

In the United States, Securities and Exchange Commission (S.E.C.) clearance is needed to sell securities to the public. The regulations are based upon the Securities Act of 1933, but in practice much case law and professional judgment applies. The S.E.C. is explicitly concerned with full disclosure of material information, and does not attempt to determine whether a security is fairly priced or not. Many state securities regulators in the past attempted to ascertain whether a security is fairly priced (the “blue sky” laws) before allowing investors to purchase an issue, but the National Securities Markets Improvement Act of 1996 has given blanket approval for all IPOs that list on the American Stock Exchange (Amex), New York Stock Exchange (NYSE), or the National Market System (NMS) of Nasdaq.

In preparation for going public, a company must supply audited financial statements. The level of detail that is required depends upon the size of the company, the amount of money being raised, and the age of the company. The required disclosures are contained in S.E.C. Regulations S-K or S-B (covering the necessary descriptions of the company's business) and Regulation S-X (covering the necessary financial statements). For large offerings, Registration of Form S-1 is required, but Form SB-2 can be used by companies with less than $25 million in revenues. Form SB-2 registrations allow the use of financial statements prepared in accordance with generally accepted accounting principles, whereas Form S-1 registrations require that certain details specified in Regulation S-X be followed. The smallest offerings, raising less than $5 million, may register under Regulation A, which has the least stringent disclosure requirements. Disclosure requirements differ for certain industries (such as banking) that are subject to other regulations, and for other industries with a history of abuses (such as oil & gas, and mining stocks).

In going public, an issuing firm will typically sell 20–40% of its stock to the public. The issuer will hire investment bankers to assist in pricing the offering and marketing the stock. In cooperation with outside counsel, the investment banker will also conduct a due diligence investigation of the firm, write the prospectus, and file the necessary documents with the S.E.C. For young companies, most or all of the shares being sold are typically newly-issued (primary shares), with the proceeds going to the company. With older companies going public, it is common that many of the shares being sold come from existing stockholders (secondary shares).

Since, as discussed in section 7.3 below, investment bankers rarely compete for business on the basis of offering lower underwriting discounts (or gross spreads), an issuer will generally choose a lead underwriter on the basis of its experience, especially with IPOs in the same industry. Having a well-respected analyst who will supply research reports on the firm in the years ahead is a major consideration. The investment bankers with large market shares of IPOs include, in addition to large investment banking firms such as Merrill Lynch and Goldman Sachs, five firms that specialize in IPOs: BT Alex. Brown, Hambrecht & Quist, BancAmerica Robertson Stephens, Nationsbank Montgomery, and Friedman, Billings, Ramsey Group.

After the preliminary prospectus (or “red herring,” since on the front page certain warnings are required to be printed in red) is issued, the company management and investment bankers conduct a marketing campaign for the stock. Regulations limit what can be said in this marketing campaign. This marketing effort includes a “road show” to major cities, in which presentations are made before groups of prospective institutional buyers as well as in one-on-one discussions with important IPO buyers, such as mutual funds. If the offering is sufficiently large and has an international tranche, the road show may include presentations in London and Asia.

2.2. Valuing IPOs

In principal, valuing IPOs is no different from valuing other stocks. The common approaches of discounted cash flow (DCF) analysis and comparable firms analysis can be used. In practice, because many IPOs are of young growth firms in high technology industries, historical accounting information is of limited use in projecting future profits or cash flows. Thus, a preliminary valuation may rely heavily on how the market is valuing comparable firms. In some cases, publicly-traded firms in the same line of business are easy to find. In other cases, it may be difficult to find publicly-traded “pure plays” to use for valuation purposes.

The final valuation of the firm going public typically occurs at a pricing meeting the morning a firm is expected to receive S.E.C. clearance to go public. This pricing meeting is described below in section 7.1 concerning bookbuilding. Because the IPO market is especially sensitive to changes in market conditions, and because it takes at least several months to complete the process of going public, going public is a high-stress event for entrepreneurs. Numerous cases have occurred where a firm was expecting to raise tens of millions of dollars, only to withdraw the deal at the last moment due to factors outside of its control.

Because most companies prefer an offer price of between $10.00 and $20.00 per share, firms frequently conduct a stock split or reverse stock split to get into the target price range. Stocks with a price below $5.00 per share are subject to the provisions of the Securities Enforcement Remedies and Penny Stock Reform Act of 1990, aimed at reducing fraud and abuse in the penny stock market.

3. NEW ISSUES UNDERPRICING

3.1. In General

The best-known pattern associated with the process of going public is the frequent incidence of large initial returns (the price change measured from the offering price to the market price on the first trading day) accruing to investors in IPOs of common stock. Numerous studies document the phenomenon, showing that the distribution of initial returns is highly skewed, with a positive mean and a median near zero. In the U.S., the mean initial return is about 15 percent.

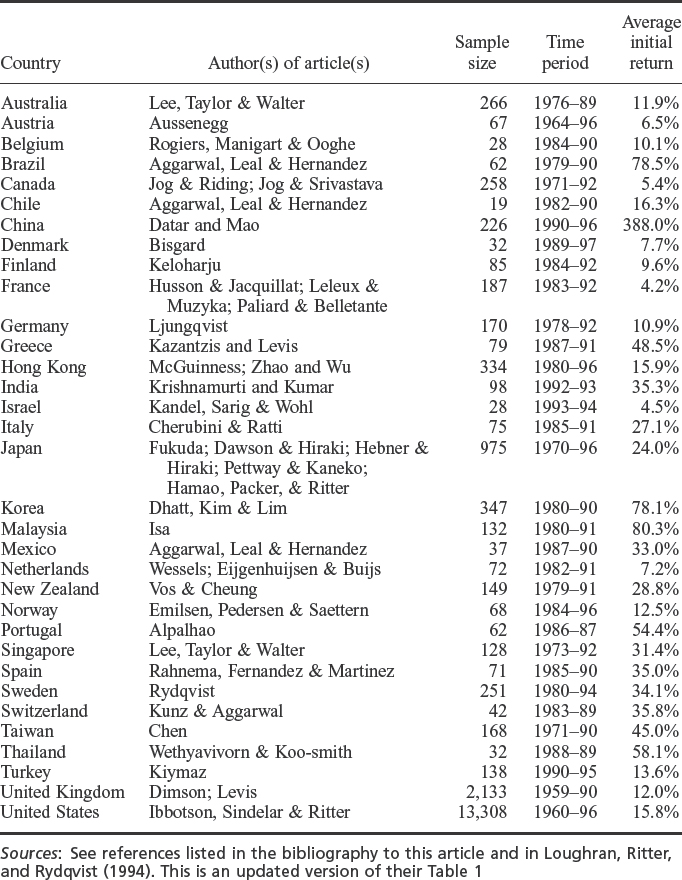

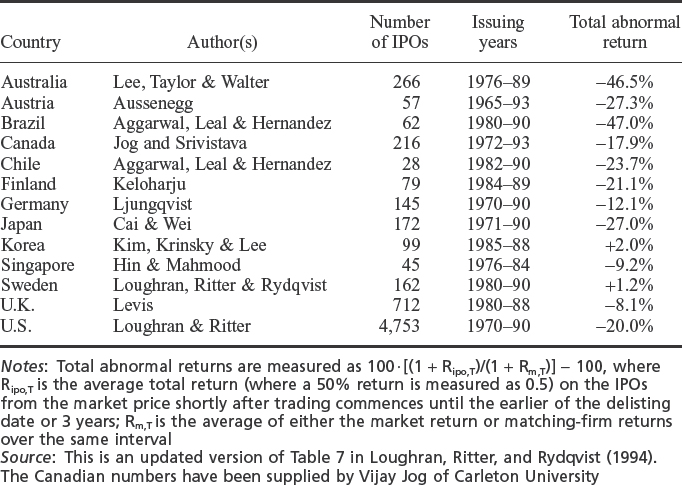

The new issue underpricing phenomenon exists in every nation with a stock market, although the amount of underpricing varies from country to country. (In this article, the term “new issue” is used to refer to unseasoned security offerings, although the term is frequently applied to seasoned (previously traded) security offerings as well. Furthermore, we focus on IPOs of equity securities, even though many security offerings involve fixed-income securities.) Table 9.1 gives a summary of the equally-weighted average initial returns on IPOs in a number of countries around the world. The incredibly high average initial return in China is for “A” share IPOs, which are restricted to Chinese residents.

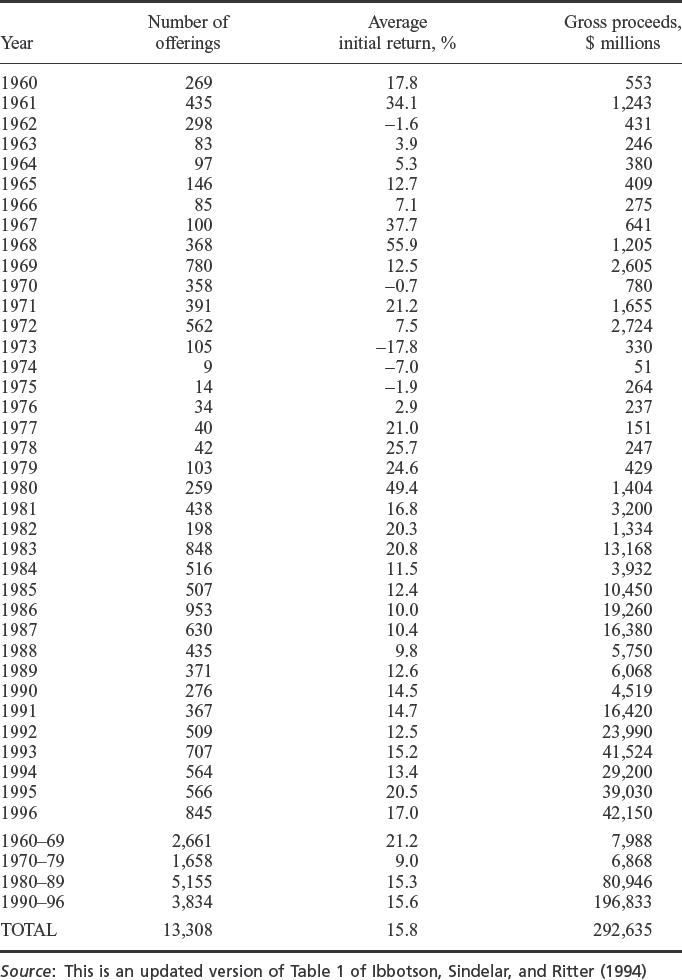

Table 9.2 reports the equally weighted average initial return in the U.S., by year, from 1960–1996. The numbers from 1960–84 include best efforts offerings and penny stocks. The numbers from 1985–1996 include only firm commitment offerings. The 1960–1984 average initial returns are higher and more volatile than if only firm commitment offerings were included.

Table 9.1 Average initial returns for 33 countries

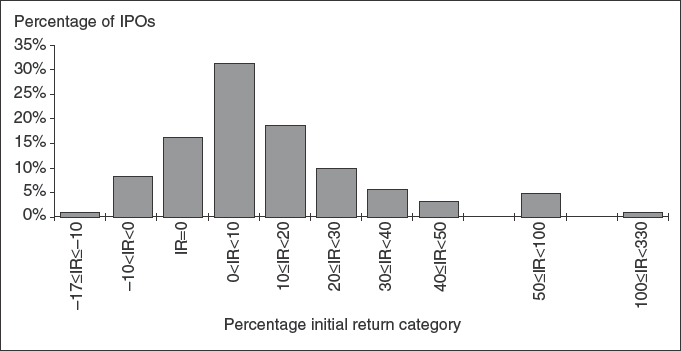

While on average there are positive initial returns on IPOs, there is a wide variation on individual issues. Figure 9.1 shows the distribution of first day returns for IPOs from 1990–1996. One in eleven IPOs has a negative initial return, and one in six closes on the first day at the offer price. One in a hundred doubles on the first day.

Table 9.2 Number of U.S. offerings, average initial return, and gross proceeds of initial public offerings in 1960–96

Figure 9.1 Histogram of initial returns (percentage return from offering price to first day close) for 2,866 IPOs in 1990–96. Units, ADRs, REITs, closed-end funds, and small IPOs are excluded. The average initial return is 14.0%

Source: Barry, Gilson, and Ritter (1998)

3.2. Reasons for New Issues Underpricing

A number of reasons have been advanced for the new issues underpricing phenomenon, with different theories focusing on various aspects of the relations between investors, issuers, and the investment bankers taking the firms public. In general, these theories are not mutually exclusive. Furthermore, a given reason can be more important for some IPOs than for others.

3.2.a The Winner's Curse Hypothesis

An important rationale for the underpricing of IPOs is the “winner's curse” explanation. Since a more or less fixed number of shares are sold at a fixed offering price, rationing will result if demand is unexpectedly strong. Rationing in itself does not lead to underpricing, but if some investors are at an informational disadvantage relative to others, some investors will be worse off. If some investors are more likely to attempt to buy shares when an issue is underpriced, then the amount of excess demand will be higher when there is more underpricing. Other investors will be allocated only a fraction of the most desirable new issues, while they are allocated most of the least desirable new issues. They face a winner's curse: if they get all of the shares which they ask for, it is because the informed investors don't want the shares. Faced with this adverse selection problem, the less informed investors will only submit purchase orders if, on average, IPOs are underpriced sufficiently to compensate them for the bias in the allocation of new issues.

Numerous studies have attempted to test the winner's curse model, both for the U.S. and other countries. While the evidence is consistent with there being a winner's curse, other explanations of the new issues underpricing phenomenon exist.

3.2.b The Market Feedback Hypothesis

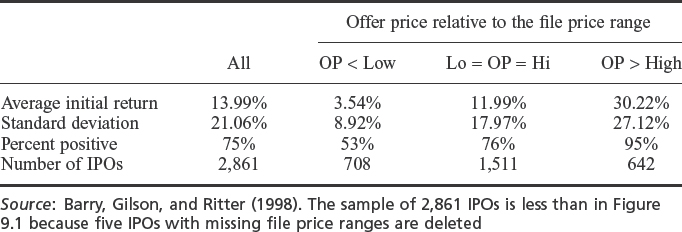

Where bookbuilding is used, investment bankers may underprice IPOs to induce regular investors to reveal information during the pre-selling period, which can then be used to assist in pricing the issue. In order to induce regular investors to truthfully reveal their valuations, the investment banker compensates investors through underpricing. Furthermore, in order to induce truthful revelation for a given IPO, the investment banker must underprice issues for which favorable information is revealed by more than those for which unfavorable information is revealed. This leads to a prediction that there will only be a partial adjustment of the offer price from that contained in the preliminary prospectus to that in the final prospectus. In other words, those IPOs for which the offer price is revised upwards will be more underpriced than those for which the offer price is revised downwards. This pattern is in fact present in the data, as shown in Table 9.3.

3.2.c The Bandwagon Hypothesis

The IPO market may be subject to bandwagon effects. If potential investors pay attention not only to their own information about a new issue, but also to whether other investors are purchasing, bandwagon effects may develop. If an investor sees that no one else wants to buy, he or she may decide not to buy even when there is favorable information. To prevent this from happening, an issuer may want to underprice an issue to induce the first few potential investors to buy, and induce a bandwagon, or cascade, in which all subsequent investors want to buy irrespective of their own information.

Table 9.3 IPOs in 1990–96 with proceeds = $5 million, excluding units and ADRs

An interesting implication of the market feedback explanation, in conjunction with bandwagons, is that positively-sloped demand curves can result. In the market feedback hypothesis, the offering price is adjusted upwards if regular investors indicate positive information. Other investors, knowing that this will only be a partial adjustment, correctly infer that these offerings will be underpriced. These other investors will consequently want to purchase additional shares, resulting in a positively sloped demand curve. The flip side is also true: because investors realize that a cut in the offering price indicates weak demand from other investors, cutting the offer price might actually scare away potential investors. And if the price is cut too much, investors might start to wonder why the firm is so desperate for cash. Thus, an issuer faced with weak demand may find that cutting the offer price won't work, and its only alternative is to postpone the offering, and hope that market conditions improve.

3.2.d The Investment Banker's Monopsony Power Hypothesis

Another explanation for the new issues underpricing phenomenon argues that investment bankers take advantage of their superior knowledge of market conditions to underprice offerings, which permits them to expend less marketing effort and ingratiate themselves with buy-side clients. While there is undoubtedly some truth to this, especially with less sophisticated issuers, when investment banking firms go public, they underprice themselves by as much as other IPOs of similar size. Investment bankers have been successful at convincing clients and regulatory agencies, including the Office of Thrift Supervision (in the case of mutual savings bank conversions), that underpricing is normal for IPOs.

3.2.e The Lawsuit Avoidance Hypothesis

Since the Securities Act of 1933 makes all participants in the offer who sign the prospectus liable for any material omissions, one way of reducing the frequency and severity of future lawsuits is to underprice. Underpricing the IPO seems to be a very costly way of reducing the probability of a future lawsuit. Furthermore, other countries in which securities class actions are unknown, such as Finland, have just as much underpricing as in the U.S.

3.2.f The Signalling Hypothesis

Underpriced new issues “leave a good taste” with investors, allowing the firms and insiders to sell future offerings at a higher price than would otherwise be the case. This reputation argument has been formalized in several signaling models. In these models, issuing firms have private information about whether they have high or low values. They follow a dynamic issue strategy, in which the IPO will be followed by a seasoned offering. Various empirical studies, however, find that the hypothesized relation between initial returns and subsequent seasoned new issues is not present, casting doubt on the importance of signaling as a reason for underpricing.

3.2.g The Ownership Dispersion Hypothesis

Issuing firms may intentionally underprice their shares in order to generate excess demand and so be able to have a large number of small shareholders. This dispersed ownership will both increase the liquidity of the market for the stock, and make it more difficult for outsiders to challenge management.

3.2.h Summary of Explanations of New Issues Underpricing

All of the above explanations for new issues underpricing involve rational strategies by buyers. Several other explanations involving irrational strategies by investors have been proposed. These irrational strategies will be discussed under the heading of the long-run performance of IPOs, for any model implying that investors are willing to overpay at the time of the IPO also implies that there will be poor long-run performance.

Many of the above explanations for the underpricing phenomenon can be criticized on the grounds of either the extreme assumptions that are made or the unnecessarily convoluted stories involved. On the other hand, most of the explanations have some element of truth to them. Furthermore, the underpricing phenomenon has persisted for decades with no signs of its imminent demise.

3.3. Why Don't Issuers Get Upset About Leaving Money on the Table?

The dollar amount of underpricing per share, multiplied by the number of shares offered, is referred to as the amount of money “left on the table.” An extreme example is Netscape's August 1995 IPO, in which (including the international tranche and overallotment options), 5.75 million shares were sold at $28.00 per share. The first-day market price closed at $58.25, leaving $174 million on the table. If the same number of shares could have been sold at $58.25 per share instead of $28.00, the issuing firm's pre-issue shareholders would have been better off by $174 million (before investment banker fees). Instead, the wealth of those who were allocated shares at the offer price increased by this amount. Yet, amazingly, Netscape's pre-issue shareholders weren't visibly upset by this transfer of wealth from their pockets. Why not?

The reason probably lies in the “partial adjustment phenomenon,” illustrated in Table 9.3. The highest initial returns, and therefore the most amount of money left on the table, tend to be associated with issues where the offer price has been revised upwards from the file price range. Furthermore, frequently the number of shares are revised in the same direction as the price. To use the extreme example of Netscape, the preliminary prospectus contained an offer price range of $12–14 per share, for 3,500,000 shares (not including a 15% overallotment option). Thus, just a few weeks before the offering, the company was expecting to raise about $50 million. Instead, it raised $161 million before fees. So the bad news that a lot of money was left on the table arrived at the same time that the good news of high proceeds and a high market price arrived. Because a lot of money is left on the table almost exclusively when it is packaged with good news, issuers rarely complain. And the investment banker will always be willing to argue that the price jump was due to a successful job of marketing the issue by the investment banker.

4. “HOT ISSUE” MARKETS

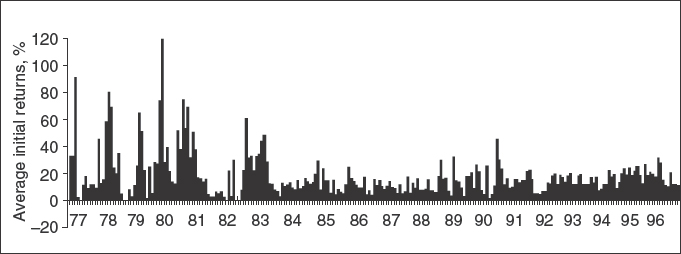

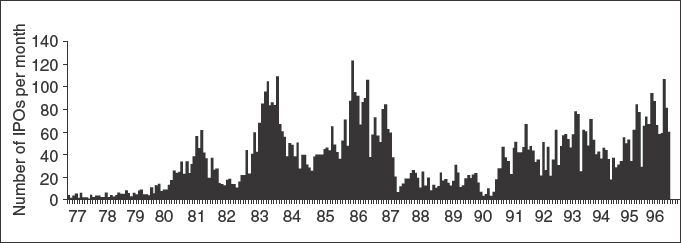

A second pattern is that cycles exist in both the volume and the average initial returns of IPOs. This is illustrated for 1977–1996 in Figures 9.2 and 9.3.

Figure 9.2 Average initial returns by month for S.E.C.-registered IPOs in the U.S. during 1977–96

Source: Ibbotson, Sindelar, and Ritter (1994), as updated

Figure 9.3 The number of IPOs by month in the U.S. during 1977–96, excluding closed-end fund IPOs

Source: Ibbotson, Sindelar, and Ritter (1994), as updated

Inspection of these figures shows that high initial returns tend to be followed by rising IPO volume. The periods of high average initial returns and rising volume are known as “hot issue” markets. The volume of IPOs, both in the U.S. and other countries, shows a strong tendency to be high following periods of high stock market returns, when stocks are selling at a premium to book value. Rational explanations for the existence of hot issue markets are difficult to come by.

Hot issue markets exist in other countries as well as the U.S. For example, there was a hot issue market in the United Kingdom between the “Big Bang” (the end of fixed commission rates) in October 1986 and the crash a year later. In South Korea, there was a hot issue market in 1988 that coincided with a major bull market.

5. LONG-RUN PERFORMANCE

5.1. Evidence on Long-Run Performance

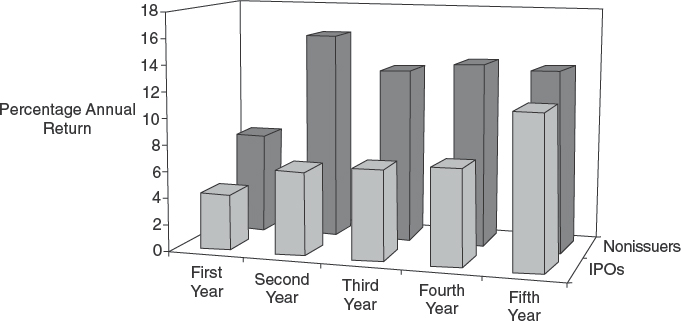

The third pattern associated with IPOs is the poor stock price performance of IPOs in the long run. Measured from the market price at the end of the first day of trading, Figure 9.4 shows that companies going public during 1970–1993 produced an average return of just 7.9 percent per year for the five years after the offering, using the first closing market price as the purchase price. A control group of nonissuing firms, matched by market capitalization, produced average annual returns of 13.1 percent. Thus, IPOs underperform by 5.2 percent per year in the five years after going public.

Figure 9.4 Average annual returns for the five years after the offering date for 5,821 IPOs in the U.S. from 1970–93, and for nonissuing firms that are bought and sold on the same dates as the IPOs. Nonissuing firms are matched on market capitalization, have been listed on the CRSP tapes for at least five years, and have not issued equity in a general cash offer during the prior five years. The returns (dividends plus capital gains) exclude the first-day returns. Returns for IPOs from 1992–93 are measured through Dec. 31, 1996

Source: Loughran and Ritter (1995), as updated

It should be noted that most firms going public have relatively high market-to-book ratios, and most are “small-cap” stocks. Small growth stocks in general have very low returns, and if IPOs are compared with nonissuers that are chosen on the basis of market-to-book ratios, as well as size, the underperformance is less than when the nonissuers are chosen on the basis of size alone.

The low returns in the aftermarket for IPOs partly reflect the pattern that IPO volume is high near market peaks when market-to-book ratios are high. The underperformance is concentrated among firms that went public in the heavy-volume years, and for younger firms. Indeed, for more established firms going public, and for those that went public in the light-volume years of the mid- and late-1970s, there is no long-run underperformance. IPOs that are not associated with venture capital financing, and those not associated with high-quality investment bankers, also tend to do especially poorly. Older firms going public, including “reverse LBOs,” do not seem to be subject to long-run abnormal performance. Reverse LBOs are companies going public that previously had been involved in a leveraged buyout.

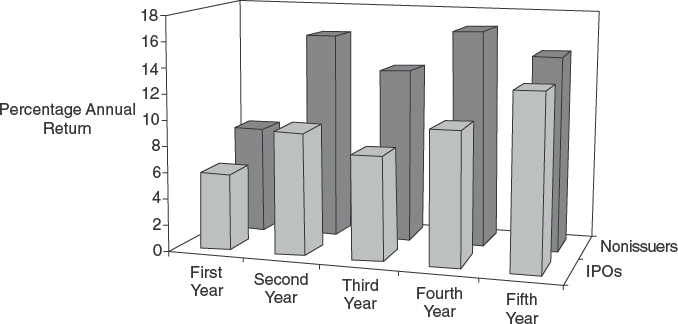

Figure 9.4 treats all IPOs equally, whether the market capitalization was $20 million, with no institutional buyers, or $120 million, with institutions participating. In Figure 9.5, the IPOs are restricted to those with a post-IPO market capitalization of at least $50 million. The average return for these IPOs was 10.1 percent per year, compared to 13.8 percent per year for their matching firms. Thus, the larger IPOs underperform by 3.7 percent per year in the five years after going public. Smaller IPOs do much worse.

Figure 9.5 Same as Figure 9.4, but restricted to firms with a post-issue market capitalization of greater than $50 million (expressed in terms of 1996 purchasing power). Approximately half of all IPOs (lower in the 1970s, higher in the 1990s) meet this criterion

The earnings per share of companies going public typically grows rapidly in the years prior to going public, but then actually declines in the first few years after the IPO. During the first two quarters after going public, firms rarely have negative earnings surprises.

The international evidence on the long-run performance of IPOs is summarized in Table 9.4. Total abnormal performance is calculated as 100% minus the ratio of the average three-year buy-and-hold gross return divided by the average three-year buy-and-hold gross return on the benchmark. Thus, the total abnormal return of –20% for the U.S. can be interpreted as meaning that buying a portfolio of IPOs would have left an investor with 20% less wealth three years later than if the money had been invested in nonissuing firms instead.

The long-run underperformance of IPOs is not limited to operating companies going public. Investors in a closed-end fund IPO pay a premium over net asset value (the market value of the securities that the fund holds), because commissions equal about 7 percent of the offering price. Thus every $10.00 invested at the offering price buys only $9.30 of net asset value. Given that closed-end funds typically sell at about a 10 percent discount to net asset value, it is difficult to explain why investors are willing to purchase the shares at a premium in the IPO. On average, it takes only about six months for closed-end funds to move from their 7 percent premium to a 10 percent discount. Perhaps it is no surprise that practitioners say that “closed-end funds are sold, not bought.” Almost all closed-end fund shares are sold to individuals, rather than more sophisticated institutional investors, at the time of the IPO. Furthermore, new issues of closed-end funds are highly cyclical.

Table 9.4 International evidence on long-run IPO overpricing

REITs are similar to closed-end funds, but they invest in property and mortgage-related securities. REIT shares used to be overwhelmingly purchased by individual investors, as are closed-end funds. With the explosion of REIT offerings in the 1990s, they now comprise a substantial portion of the Russell 2000 index, and many institutional investors now hold REITs. In the 1970s and 1980s, REITs underperformed in the first six months after their IPO, but the pattern has been less clear in the 1990s.

Three theories have been proposed to explain the phenomena of the long-run underperformance of IPOs.

5.2. The Divergence of Opinion Hypothesis

One argument is that investors who are most optimistic about an IPO will be the buyers. If there is a great deal of uncertainty about the value of an IPO the valuations of optimistic investors will be much higher than those of pessimistic investors. As time goes on and more information becomes available, the divergence of opinion between optimistic and pessimistic investors will narrow, and consequently, the market price will drop.

5.3. The Impresario Hypothesis

The “impresario” hypothesis argues that the market for IPOs is subject to fads and that IPOs are underpriced by investment bankers (the impresarios) to create the appearance of excess demand, just as the promoter of a rock concert attempts to make it an “event.” This hypothesis predicts that companies with the highest initial returns should have the lowest subsequent returns. There is some evidence of this in the long run, but in the first six months, momentum effects seem to dominate. One survey of individual investors in IPOs found that only 26 percent of the respondents did any fundamental analysis of the relation between the offer price and the firm's underlying value.

5.4. The Windows of Opportunity Hypothesis

If there are periods when investors are especially optimistic about the growth potential of companies going public, the large cycles in volume may represent a response by firms attempting to “time” their IPOs to take advantage of these swings in investor sentiment. Of course, due to normal business cycle activity, one would expect to see some variation through time in the volume of IPOs. The large swings in volume displayed in Figure 9.3, however, seem difficult to explain as merely normal business cycle activity.

The windows of opportunity hypothesis predicts that firms going public in high volume periods are more likely to be overvalued than other IPOs. This has the testable implication that the high-volume periods should be associated with the lowest long-run returns. This pattern indeed exists.

6. GOING PUBLIC AS A STAGE IN THE LIFE CYCLE OF A FIRM'S EXTERNAL FINANCING

6.1. Financing of Startups

Most startup companies seeking external financing do not immediately utilize the public capital markets, but instead raise capital from private sources. Because young firms frequently have much of their value represented by intangibles such as growth opportunities, rather than assets in place, outside investors face a difficult job of valuing them. Usually, the value of these opportunities is dependent upon the actions taken by the entrepreneur (the moral hazard problem). Self-selection in terms of which firms seek external financing may also create an adverse selection problem for potential investors.

The source of capital for an entrepreneur that is least subject to problems caused by information asymmetries is self-financing: entrepreneurs contribute their own money. With limited resources, however, the ability to grow rapidly will be constrained if external sources of capital are not used. Because of the discipline imposed by social networks, friends and relatives might be the next source of capital. If a firm approaches potential external investors for financing when the entrepreneur and closely associated individuals have not invested a substantial fraction of their own assets in the venture, suspicions will be aroused. Only when these sources have been tapped will non-affiliated sources of capital become readily available. Even then, the ability to disclose proprietary information to potential investors encourages the use of private financing, either from banks, “angels,” or venture capitalists. Angel financing is the term used for capital provided by wealthy individuals who aren't part of formal venture capital organizations.

6.2. Venture Capital

In the U.S., a venture capital industry exists to assist in the financing of private firms in their early stages of growth. Venture capitalists typically specialize by industry, size, or region, developing a network of contacts that can assist them in evaluating potential investment opportunities, and allowing the investments to live up to their potential. Adverse selection and moral hazard considerations are of paramount importance in deciding which deals to finance, and how to structure the deals.

Typically, venture capitalists do not make passive financial investments in young firms. Instead, they typically insist on board membership, and provide advice. This advice-giving role is one of the reasons for industry specialization. Thus, the returns to the venture capitalist are partly a return on capital, and partly a return on the other services provided. Of course, there can be disagreements between entrepreneurs and their financiers, for the interests of the various parties will not be identical. Venture capitalists typically provide capital in stages, with further commitments contingent upon performance up to that time.

While there are advantages to raising capital from a small number of investors who actively monitor the firm and to whom proprietary information can be disclosed, there are disadvantages as well. As long as the firm is private, any equity investment is illiquid, and investors will have to be compensated both for the lack of liquidity and the lack of diversification associated with a blockholding. Furthermore, conflicts between entrepreneurs and venture capitalists may arise. As a firm becomes larger, these disadvantages may come to outweigh the advantages of private financing. This is the point in the life cycle of a firm's financing at which it is optimal to go public, even though there are substantial costs associated with “outside” equity.

6.3. Mechanisms to Distinguish Among Firms

Among those firms that do go public, if investors are unable to fully distinguish the high-value firms from low-value firms, wealth transfers will result. The extent of these wealth transfers is dependent upon the dispersion of values among firms that are being pooled together. This encourages firms to go public when other high value firms go public, and may partly account for the cycles in the volume of IPOs that are observed. At each point in time, however, the high-value firms have incentives to differentiate themselves, in order to raise capital on more favorable terms. A number of mechanisms are employed in practice to accomplish this.

In practice, sophisticated investors do look at whether major shareholders are selling some of their stock in the IPO. Furthermore, insiders frequently agree to retain any stock not sold at the time of the IPO for a specified length of time, known as the lock-up period. This lock-up period is mandated by law to be at least 90 days in the U.S., but frequently insiders agree to a longer time period (usually 180 days). Investors are willing to pay more for a firm where the insiders have agreed to retain their shares for a long period of time for two reasons: i) any negative information being withheld is likely to be divulged before the shares can be sold, reducing the benefit of withholding the information, and ii) as long as the insiders retain large shareholdings, their incentives will be more closely aligned with those of outside equityholders.

Another relevant variable is the structure of compensation contracts: entrepreneurs who are willing to accept low base salaries and who have large amounts of company stock have their incentives more closely aligned with outside equityholders than entrepreneurs who demand large amounts of non-contingent compensation. Relevant corporate governance issues that affect firm valuation include the size and composition of the board of directors, and whether there are antitakeover provisions.

Since most theories of new issue underpricing imply that firms with greater uncertainty about the value per share will be underpriced more, issuing firms have incentives to reduce the amount of uncertainty. One method by which an issuer may reduce the degree of information asymmetry surrounding its initial public offering is to hire agents (auditors and underwriters) who, because they have reputation capital at stake, will have the incentive to certify that the offer price is consistent with inside information. The need to have repeat business gives underwriters a role that issuing firms cannot credibly duplicate. Consistent with this (but not with market efficiency), the long-run returns on IPOs underwritten by less prestigious investment bankers are low.

6.4. Investor Relations After Going Public

The market prince of a stock after going public is primarily determined by market conditions and the operating performance of the company. But there is also a role for an active investor relations program, and, everything else the same, the more analysts who follow the stock, the more potential buyers there will be. Thus, in choosing an underwriter, an important consideration for an issuing firm is that the underwriter has a well-respected analyst following the industry, who can be counted on to produce bullish research reports. These bullish research reports are especially important for creating demand when insiders are selling shares in the open market.

7. CONTRACTUAL FORMS AND THE GOING PUBLIC PROCESS

In the U.S., firms issuing stock use either a firm commitment or best efforts contract. With a firm commitment contract, a preliminary prospectus is issued containing a preliminary offering price range. After the issuing firm and its investment banker have conducted a marketing campaign and acquired information about investors' willingness to purchase the issue, a final offering price is set. The final prospectus is then issued, and when the S.E.C. clears the offering, the IPO goes “effective”. The investment banker must sell all of the shares in the issue at a price no higher than the offering price once this has been set.

With a best efforts contract, the issuing firm and its investment banker agree on an offer price as well as a minimum and maximum number of shares to be sold. A “selling period” then commences, during which the investment banker makes its “best efforts” to sell the shares to investors. If the minimum number of shares are not sold at the offer price within a specified period of time, usually 90 days, the offer is withdrawn and all investors' monies are refunded from an escrow account, with the issuing firm receiving no money. Best efforts offerings are used almost exclusively by smaller, more speculative, issuers. Essentially all IPOs raising more than $10 million use firm commitment contracts.

7.1. Bookbuilding

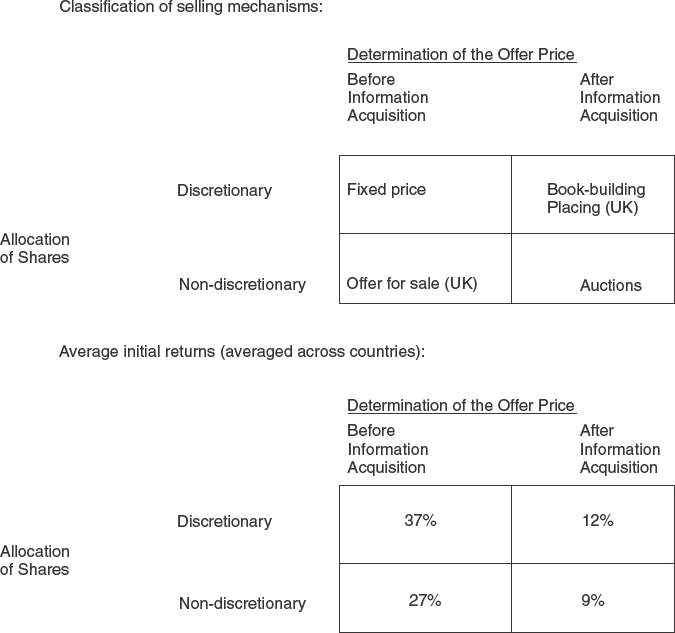

Firm commitment offerings in the U.S. use “book-building.” During and immediately after the road show period, the lead investment banker canvasses potential buyers and records who is interested in buying how much at what price. In other words, a demand curve is constructed. The offering is then priced based upon this information. In contrast, in many countries (and in the U.S. with best efforts offerings), the number of shares to be sold and the offer price are set before information about the state of demand is collected. The international evidence summarized in Table 9.1 shows that countries using fixed price offerings typically have more underpricing than in countries using book-building procedures. This evidence is summarized in Figure 9.6.

Partly because it results in more accurate pricing than if the offer price is set too early, many countries have moved in recent years to book-building, at least in the case of large offerings. Denmark, Finland, and Japan are among these countries.

Book-building is not without its critics, however. Book-building typically results in some offerings being underpriced, with investment bankers allegedly allocating a disproportionate number of shares in hot issues to their favored clients. There is, however, a desirable aspect to this favoritism. One reason, as explained earlier in section 3.2.b with regard to the market feedback hypothesis, is that IPOs are underpriced as a way of giving something back to regular investors who assist an investment banker in getting more accurate pricing. If regular investors can be favored by getting more shares in hot deals, they don't have to be favored by underpricing as much as otherwise would be required. A dark side to the favoritism in allocation surfaced in 1997 with a Wall Street Journal article, and subsequent S.E.C. investigation, alleging that underwriters competed for IPO business partly by allocating shares in hot deals to some venture capitalists and executives of private companies that were likely candidates to go public. This practice, called spinning, is intended to influence the choice of underwriter.

Figure 9.6 Selling mechanisms classified on the basis of how shares are allocated and when the offer price is determined (top), and average initial returns by category (bottom).

Source: Based upon Loughran, Ritter, and Rydqvist (1994).

7.2. Overallotment Options and Stabilization

When taking a firm public using a firm commitment contract, the investment bankers will typically presell more than 100% of the shares offered. Almost all IPOs include an overallotment option, in which the issuing firm or selling shareholders give the investment banker the right to sell up to 15% more shares than guaranteed. The overallotment option is also called the Green Shoe option, since the first offering to include one was the February 1963 offering of the Green Shoe Manufacturing Company. If the investment bankers expect aftermarket demand to be hot, they will typically presell 115% of the issue, with the expectation that they will exercise the overallotment option. If they expect aftermarket demand to be weak, they will typically presell 135% of the offering, with the shares above the overallotment option representing a naked short position in the stock. The advantage of preselling extra shares is that if many shares are “flipped,” that is, immediately sold in the aftermarket by investors who had been allocated shares, the investment banker can buy them back and retire the shares, just as if they had never been issued in the first place.

While it is generally illegal to manipulate a stock price, manipulation is permitted directly after a securities offering. Investment bankers have legal authority to post a “stabilizing” bid, at or below the offer price, at which they stand ready to buy shares once trading has commenced. The existence of this floor price allows investors to get out of an offer before the price declines, and may also head off a larger price drop if no stabilization occurred. Stabilizing a stock is also referred to as supporting the stock.

Why would an underwriter allocate extra shares (the extra 35%) to investors when it expects to buy them back, rather than just allocate fewer shares in the first place? One possibility is that some investors are willing to buy and hold the stock if they can get shares at the offer price when these same investors wouldn't be willing to buy these same shares at the same price in the market, once trading commences. Thus, the inclination to hold the stock may be stronger if more shares are allocated initially. Another reason may be that favored clients of the investment banker are more likely to sell back their shares, and offering price support is a way of favoring some clients over others. Yet a third reason is that by offering price support, the investment banker is telling investors that there are fewer incentives to overprice a deal, and this reassures investors who would otherwise not be willing to buy at the offer price.

For IPOs that are stabilized, on average the price drops by about 4% during the subsequent month (say, from a $10 offer price to $9 5/8). For the roughly two-thirds of issues that aren't stabilized, there is a slight uptrend in price during the month after the issue. When all IPOs are grouped together, the downtrend for stabilized issues and the uptrend for other IPOs tend to cancel out. Thus, there is little in the way of abnormal performance, on average, in the months after an IPO's first day of trading. For IPOs that increase on the first day, there tends to be positive momentum during the following six months. This is especially true when there is relatively little flipping by institutions on the first day.

7.3. The Costs of Going Public

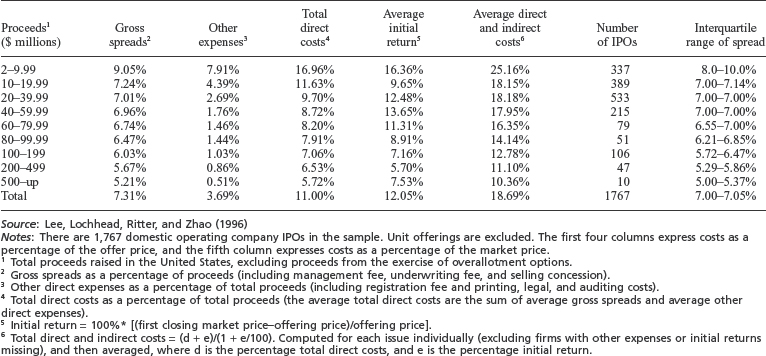

There are a number of direct and indirect costs of going public. One of the direct costs is the compensation paid to underwriters. There are substantial economies of scale in underwriting costs. In spite of these economies of scale, the majority of IPOs raising between $20 million and $80 million have gross spreads of exactly 7.0%. Table 9.5 reports the direct and indirect costs of going public for IPOs from 1990–1994. The indirect cost that is included is the new issues underpricing cost; management time and effort isn't included.

Table 9.5 Direct and indirect costs, in percent, of equity IPOs, 1990–94

The National Association of Securities Dealers (NASD) sets limits on underwriter compensation. One way that underwriters may overcome the limits on direct compensation set by the NASD and state regulators is to include warrants to purchase additional shares as part of the compensation of the investment banker. Underwriter warrants tend to be associated with smaller and riskier issues and low-quality underwriters. Since Table 9.5 does not include underwriter warrants as a cost of going public, their inclusion would boost the average costs associated with smaller offerings. In other words, Table 9.5 understates the economies of scale that exist.

7.4. Direct Public Offerings

Beginning in the mid-1990s, a growing number of small companies have gone public without using an investment banker in what have come to be called direct public offerings (DPOs). According to one count, 190 companies attempted to raise $273 million during 1996 using direct public offerings. Some of these have been consumer product companies (i.e., microbreweries) where the target shareholders have been customers of a company's product. An advantage for an issuing firm of a direct public offering is the possibility of reduced costs. Investors must be wary, however, of the lack of a third party (i.e., underwriter) putting its reputation on the line, especially as regards due diligence and valuation.

8. SUMMARY

Companies going public, especially young companies, face a market that is subject to sharp swings in valuations. Pricing deals can be difficult, even in stable market conditions, because insiders presumably have more information than potential outside investors. To deal with these potential problems, market participants and regulators insist on the disclosure of material information.

Three patterns have been documented for IPOs in the U.S. and many countries: i) new issues underpricing, ii) cycles in volume and the extent of underpricing, and iii) long-run underperformance. In some respects, the poor performance of IPOs in the long run makes the new issues underpricing phenomenon even more of a puzzle.

The U.S. IPO market is enormous in comparison with that of most countries. The contrast with continental Europe is especially noteworthy. Part of the difference is undoubtedly cultural: the willingness of U.S. employees to work for young, unstable companies makes it easier to start a firm. Venture capitalists are willing to finance these firms, knowing that an active IPO market will allow them to cash out if the startup firm succeeds. Because of the immense number of U.S. IPOs, a large infrastructure has developed to create and fund young companies, especially in the high technology sector.

In addition to liquid labor markets, the large volume of IPOs in the U.S. can be partly attributable to a legal system that protects, albeit imperfectly, minority investors. Yet another factor may be the willingness of U.S. investors to, on average, overpay for IPOs. There is evidence that in the choice between an additional round of venture capital financing and going public, firms have some success at choosing periods when the public market is willing to pay the highest valuations. As a result, when the IPO market is most buoyant, investors frequently receive low long-run returns.

SUGGESTED READING

Affleck-Graves, J., S. Hegde, and R. Miller (1996) Conditional price trends in the aftermarket for initial public offerings. Financial Management 25, 25–40.

Aggarwal, R., and P. Rivoli (1990) Fads in the initial public offering market? Financial Management 22, 42–53.

Alexander, J. C. (1993) The lawsuit avoidance theory of why initial public offerings are underpriced. UCLA Law Review 41, 17–71.

Aussenegg, Wolfgang (1997) Short and Long-run performance of Initial Public Offerings in the Austrian Stock Market. Unpublished Vienna University of Technology working paper.

Baron, D. (1982) A model of the demand for investment banking advising and distribution services for new issues. Journal of Finance 37, 955–976.

Barry, C. (1989) Initial public offerings underpricing: The issuer's view – A comment. Journal of Finance 44, 1099–1103.

Barry, C., and R. Jennings (1993) The opening price performance of initial public offerings of common stock. Financial Management 22, 54–63.

Barry, C., C. Muscarella, J. Peavy, and M. Vetsuypens (1990) The role of venture capital in the creation of public companies: Evidence from the going public process. Journal of Financial Economics 27, 447–471.

Barry, C., R. Gilson, and J. R. Ritter (1998) Initial public offerings and fraud on the market. Unpublished TCU, Stanford, and University of Florida working paper. Beatty, R. P., and J. R. Ritter (1986) Investment banking, reputation, and the underpricing of initial public offerings. Journal of Financial Economics 15, 213–232.

Beatty, R. P., and I. Welch (1996) Issuer expenses and legal liability in initial public offerings. Journal of Law and Economics 39, 545–602.

Benveniste, L., and P. Spindt (1989) How investment bankers determine the offer price and allocation of new issues. Journal of Financial Economics 24, 343–361. Benveniste, L., and W. Wilhelm (1990) A comparative analysis of IPO proceeds under alternative regulatory environments. Journal of Financial Economics 28, 173–207.

Benveniste, L., and W. Wilhelm (1997) Initial public offerings: Going by the book. Journal of Applied Corporate Finance 10, 98–108.

Bisgard, S. (1997) Danish initial public offerings, unpublished Copenhagen Business School masters thesis.

Booth, J., and L. Chua (1995) Ownership dispersion, costly information, and IPO underpricing. Journal of Financial Economics 41, 291–310.

Bray, A., and P. Gompers (1997) Myth or reality? The long-run underperformance of initial public offerings: Evidence from venture and nonventure capital-backed companies. Journal of Finance 52, 1791–1821.

Brennan, M., and J. Franks (1995) Underpricing, ownership and control in initial public offerings of equity securities in the U.K. Journal of Financial Economics 45, 391–413.

Cai, J., and K. C. Wei (1997) The investment and operating performance of Japanese IPO firms. Pacific-Basin Finance Journal 5, 389–417.

Carter, R., R. Dark, and A. Singh (1997) Underwriter reputation, initial returns, and the long-run performance of IPO stocks. Journal of Finance 53, 289–311.

Chemmanur, T. J., and P. Fulghieri (1994) Investment banker reputation, information production, and financial intermediation. Journal of Finance 49, 57–79. Chowdhry, B., and V. Nanda (1996) Stabilization, syndication, and pricing of IPOs. Journal of Financial and Quantitative Analysis 31, 25–42.

Chowdhry, B., and A. Sherman (1996) The winner's curse and international methods of allocating initial public offerings. Pacific-Basin Finance Journal 4, 15–30.

Datar, V., and Mao (1997) Initial public offerings in China: Why is underpricing so severe? Working paper, Seattle University.

Drake, P. D., and M. R. Vetsuypens (1993) IPO underpricing: Insurance against legal liability? Financial Management 22, 64–73.

Dunbar, C. (1995) The use of warrants as underwriter compensation in initial public offerings. Journal of Financial Economics 38, 59–78.

Garfinkel, J. (1993) IPO underpricing, insider selling and subsequent equity offerings: Is underpricing a signal of quality? Financial Management 22, 74–83. Grinblatt, M., and C. Y. Hwang (1989) Signalling and the pricing of new issues. Journal of Finance 44, 393–420.

Hamao, Y., F. Packer, and J. R. Ritter (1998) Institutional affiliation and the role of venture capital: Evidence from Initial Public Offerings in Japan, Unpublished Columbia University working paper.

Hanley, K. W. (1993) Underpricing of initial public offerings and the partial adjustment phenomenon. Journal of Financial Economics 34, 231–250.

Hanley, K. W., and J. R. Ritter (1992) Going public. The New Palgrave Dictionary of Money and Finance. London: MacMillan.

Hebner, K. J., and T. Hiraki (1993) Japanese initial public offerings. Restructuring Japan's Financial Markets. Edited by I. Walter and T. Hiraki. Homewood, IL: Business One/Irwin.

Ibbotson, R. G. (1975) Price performance of common stock new issues. Journal of Financial Economics 2, 235–272.

Ibbotson, R. G., and J. F. Jaffe (1975) “Hot issue” markets. Journal of Finance 30, 1027–1042.

Ibbotson, R. G., and J. R. Ritter (1995) Initial Public Offerings. Chapter 30 of NorthHolland Handbooks in Operations Research and Management Science, Vol. 9: Finance. Edited by R. Jarrow, V. Maksimovic, and W. Ziemba.

Ibbotson, R. G., J. Sindelar, and J. Ritter (1994) The market's problems with the pricing of initial public offerings. Journal of Applied Corporate Finance 7, 66–74. Jain, B., and O. Kini (1994) The post-issue operating performance of IPO firms. Journal of Finance 49, 1699–1726.

James, C. (1992) Relationship specific assets and the pricing of underwriter services. Journal of Finance 47, 1865–1885.

James, C., and P. Wier (1990) Borrowing relationships, intermediation, and the costs of issuing public securities. Journal of Financial Economics 28, 149–171.

Jegadeesh, N., M. Weinstein, and I. Welch (1993) An empirical investigation of IPO returns and subsequent equity offerings. Journal of Financial Economics 34, 153–175.

Jenkinson, T., and A. Ljungqvist (1996) Going Public: The Theory and Evidence on How Companies Raise Equity Finance. Oxford: Clarendon Press.

Jog, V. M., and A. Srivastava (1994) Underpricing of Canadian initial public offerings 1971–1992 – An update. FINECO 4, 81–89.

Kazantzis, C., and M. Levis (1995) Price support and initial public offerings: Evidence from the Athens Stock Exchange. Research in International Business and Finance 12, JAI Press.

Keloharju, M. (1993) The winner's curse, legal liability, and the long-run price performance of initial public offerings in Finland. Journal of Financial Economics 34, 251–277.

Kim, M., and J. Ritter (1997) Valuing IPOs, unpublished University of Florida working paper.

Kiymaz, H. (1997) Turkish IPO underpricing in the short and long run. Unpublished Bilkent University working paper.

Krigman, L., W. Shaw, and K. Womack (1997) The persistence of IPO mispricing and the predictive power of flipping, unpublished Dartmouth College working paper.

Krishnamurti, C., and P. Kumar (1994) The initial listing performance of Indian IPOs. Unpublished Indian Institute of Science working paper, Bangalore.

Lee, I., S. Lochhead, J. Ritter, and Q. Zhao (1996) The costs of raising capital. Journal of Financial Research 19, 59–74.

Lee, P., S. Taylor, and T. Walter (1996) Australian IPO underpricing in the short and long run. Journal of Banking and Finance 20, 1189–1210.

Leland, H., and D. Pyle (1977) Informational asymmetries, financial structure and financial intermediation. Journal of Finance 32, 371–387.

Lerner, Josh (1994) Venture capitalists and the decision to go public. Journal of Financial Economics 35, 293–316.

Levis, M. (1993) The long-run performance of initial public offerings: The UK experience 1980–88. Financial Management 22, 28–41.

Ling, D., and M. Ryngaert (1997) Valuation uncertainty, institutional involvement, and the underpricing of IPOs: The case of REITs. Journal of Financial Economics 43, 433–456.

Ljungqvist, A. P. (1997) Pricing initial public offerings: Further evidence from Germany. European Economic Review 41, 1309–1320.

Logue, D. (1973) On the pricing of unseasoned equity issues: 1965–69. Journal of Financial and Quantitative Analysis 8, 91–103.

Loughran, T. (1993) NYSE vs NASDAQ returns: Market microstructure or the poor performance of IPOs? Journal of Financial Economics 33, 241–260.

Loughran, T., and J. R. Ritter (1995) The new issues puzzle. Journal of Finance 50, 23–51.

Loughran, T., J. R. Ritter, and K. Rydqvist (1994) Initial public offerings: International insights. Pacific-Basin Finance Journal 2, 165–199.

Michaely, R., and W. Shaw (1994) The pricing of initial public offerings: Tests of adverse selection and signaling theories. Review of Financial Studies 7, 279–317.

Miller, E. (1977) Risk, uncertainty, and divergence of opinion. Journal of Finance 32, 1151–1168.

Miller, R., and F. Reilly (1987) An examination of mispricing, returns, and uncertainty for initial public offerings. Financial Management 16, 33–38.

Muscarella, C., and M. Vetsuypens (1989) A simple test of Baron's model of IPO underpricing. Journal of Financial Economics 24, 125–135.

Pagano, M., F. Panetta, and L. Zingales (1998) Why do firms go public? An empirical analysis. Journal of Finance, forthcoming.

Rajan, R., and H. Servaes (1997) Analyst following of initial public offerings. Journal of Finance 52, 507–529.

Ritter, J. R. (1984a) The “hot issue” market of 1980. Journal of Business 57, 215–240.

Ritter, J. R. (1984b) Signaling and the valuation of unseasoned new issues: A comment. Journal of Finance 39, 1231–1237.

Ritter, J. R. (1987) The costs of going public. Journal of Financial Economics 19, 269–281.

Ritter, J. R. (1991) The long-run performance of initial public offerings, Journal of Finance 46, 3–27.

Rock, K. (1986) Why new issues are underpriced. Journal of Financial Economics 15, 187–212.

Sahlman, W. (1988) Aspects of financial contracting in venture capital. Journal of Applied Corporate Finance 1, 23–36.

Schneider, C., J. Manko, and R. Kant (1996) Going public: practice, procedures and consequences. This is an updated reprint of a 1981 Villanova Law Review article, available from Bowne Financial Printers of Tampa, Florida.

Schultz, P. (1993) Unit initial public offerings: A form of staged financing. Journal of Financial Economics 34, 199–229.

Shiller, R. J. (1990) Speculative prices and popular models. Journal of Economic Perspectives 4, 55–65.

Siconolfi, M. (1997) Underwriters set aside IPO stock for officials of potential customers. Wall Street Journal November 12, A1.

Simon, C. (1989) The effect of the 1933 securities act on investor information and the performance of new issues. American Economic Review 79, 295–318.

Smith, C. (1986) Investment banking and the capital acquisition process. Journal of Financial Economics 15, 3–29.

Uttal, B. (1986) Inside the deal that made Bill Gates $350,000,000. Fortune (July 21), 343–361.

Welch, I. (1991) An empirical examination of models of contract choice in initial public offerings. Journal of Financial and Quantitative Analysis 26, 497–518. Welch, I. (1992) Sequential sales, learning, and cascades. Journal of Finance 47, 695–732.

Zeune, Gary D. (1997) Going Public: What the CFO Needs to Know. Forthcoming from the AICPA.

Reproduced from Contemporary Finance Digest, Vol. 2 No.1 (Spring 1998), pp. 5–30.