CHAPTER 6

Currency Risk

________________

Currency Market Overview

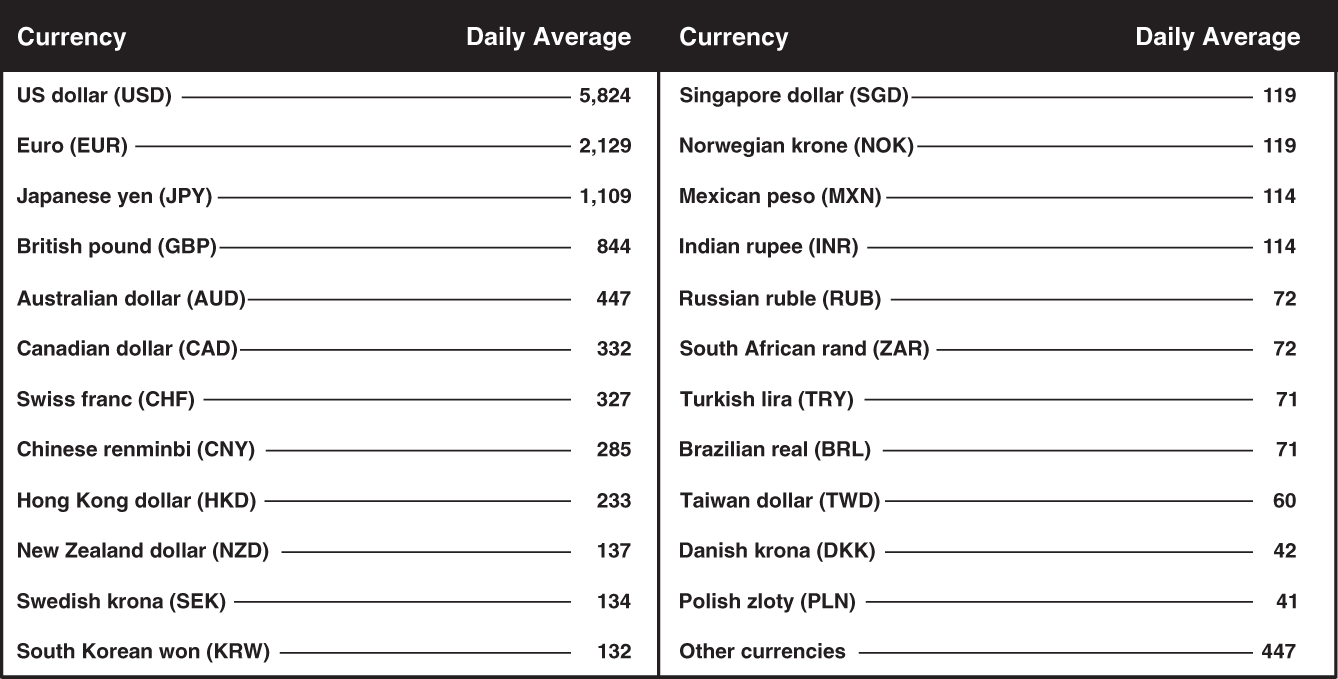

Currencies as we know them today are termed fiat currencies since their value is based on government decree. Most currencies are therefore controlled by the actions of a single government. Currency trading is what enables global trade and facilitates financial transactions of all kinds. In fact, the currency market is considered the largest and most liquid financial market in the world. Daily trading volumes are estimated to be the equivalent of US$6.6 trillion, far surpassing the combined dollar value of all stock and bond trades each day. Figure 6.1 shows the most widely traded currencies in the world as of 2019, including spot and derivative transactions. The term spot transaction refers to trades that are for immediate (typically next day) settlement, while derivative transactions are for settlement at some future date. Keep in mind that each transaction involves a pair of currencies and therefore Figure 6.1 shows double the actual total daily trading volume.

Exchange Rate Dynamics

Like most other assets, the exchange rate between two countries is determined by supply and demand. Demand is generated by trade and investment flows between a single country and all other countries that interact with it. For example, a US company building a manufacturing plant in Japan would need to convert US dollars to Japanese yen in order to pay the local construction firm. It may also need to purchase euros to buy equipment from Germany that will be used in the new factory. Similarly, an investor in the United Arab Emirates may want to buy a bond issued by the government of France, requiring them to convert UAE dirham into euros. Even an individual on vacation in a foreign country becomes a part of this equation.

FIGURE 6.1 The World's Most Traded Currencies (Daily Trade Volume in Billions USD)

Source: Bank for International Settlements, https://www.bis.org/statistics/rpfx19_fx_annex.pdf, accessed January 15, 2022. Data is as of April 2019.

As you can imagine, there are a vast number of currency transactions taking place every day. However, certain types of transactions tend to be much larger in scope and have a greater impact on the final level of demand for a particular currency, the most significant being investment-related currency transactions. Many factors affect investment-related currency transactions, but the most important is the level of real interest rates in each country. The “real” interest rate is simply the interest rate minus the rate of inflation. The currencies of countries that pay a higher real rate of interest on government bonds will likely be strong. Since investors are constantly in search of higher returns, the prospect of future currency appreciation or depreciation is an important consideration. Like most other financial instruments, currency exchange rates have a built-in self-correction mechanism. As a country's currency rises in value, goods produced by that country become increasingly expensive to foreign buyers. This will eventually cause them to import fewer goods from that country, reducing demand for the currency and causing it to fall in value. The opposite is also true—as a country's currency weakens, foreign demand for the country's exports will increase, thus increasing demand for its currency.

How Currencies Affect Investment Returns

As noted in Chapter 3, holding investments denominated in a basket of different currencies is beneficial to investors over the long run. At a minimum it should reduce the overall volatility of your investment returns. Part of the reason for this is that currencies behave differently under varying market conditions. As previously mentioned, some currencies are thought of as safe havens, and investors will often flock to those currencies when crises occur. Safe haven currencies include the US dollar, Japanese yen, and Swiss franc, as they tend to strengthen as global equity markets fall, thereby acting as a natural hedge or “shock absorber” for your portfolio. This was clear in 2008 and at the outset of the global pandemic when, in the first quarter of 2020, the US dollar, Swiss franc, and Japanese yen rallied against most other currencies.

Currency movements, especially in the case of the US dollar, can also affect other asset prices. Since most commodities are traded and priced in US dollars, a stronger US dollar tends to reduce demand for commodities and causes commodity prices to fall. Conversely, a weakening US dollar is generally positive for commodity demand and pushes prices higher. Higher commodity prices in turn will be construed as positive for the currencies and economies of countries that are commodity exporters, such as Australia and Canada.

The same can be said for emerging market equities. A stronger US dollar is regarded as detrimental for emerging market economies while a weaker US dollar is supportive for emerging markets. This is partly because a majority of debt held by emerging market countries is denominated in US dollars, so if the US dollar strengthens, the cost of servicing that debt increases. Equity markets, commodity-linked currencies, and emerging markets are collectively referred to as risk assets, meaning they perform well when investors are willing to accept more risk. Bonds and safe haven currencies, on the other hand, tend to act well when investors want to avoid risk. Broadly speaking, when economic growth is strong, risk assets perform well, and when economic growth weakens, risk assets perform poorly.

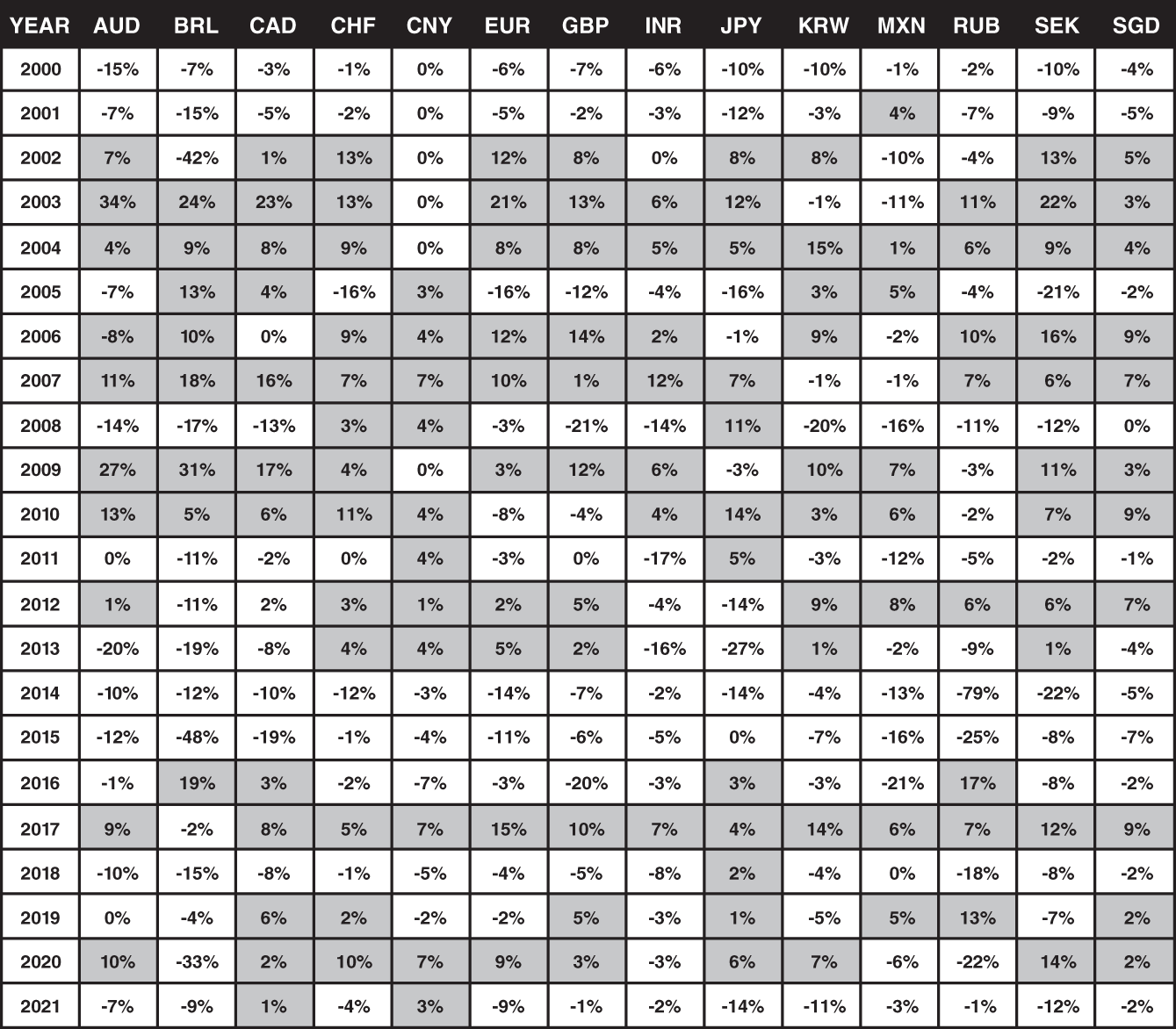

Fluctuations in currency exchange rates are beneficial for investors eventually, but they can have a negative impact on your investment returns in the short term. I recall managing a US equity fund denominated in Canadian dollars and generating a 16% rate of return in US dollar terms for the year but then losing it all to a 16% appreciation in the Canadian dollar. Canadian investors in the fund earned a net return of zero percent that year. It is a difficult conversation to have when investors see the US stock market up 16% and yet they earned a zero percent return for the year after the effect of currency. However, it is important to remember that exposure to foreign currencies can also boost your investment returns and should help make the value of your portfolio fluctuate less over time. Figure 6.2 shows some of the world's major currencies and how they performed over time against a base currency, in this case the US dollar.

The shaded numbers show a period when the currency appreciated against the base currency (the US dollar in this case) and therefore exposure to the foreign currency would have enhanced the portfolio's investment return. Conversely, the unshaded numbers are periods when the foreign currency depreciated and would have reduced the portfolio's investment return. Of the currencies listed here, investors would have been best served owning Chinese renminbi (CNY) in 2021 and the Swedish krona (SEK) in 2020. Owning any currency other than the US dollar was detrimental in 2015, however, since the US dollar appreciated against all other currencies listed.

FIGURE 6.2 Major Currency Returns versus the US Dollar

Data source: Bloomberg, as of January 16, 2022.

You should note that the table in Figure 6.2 can also be used to estimate the relative performance between different currencies in any given year by subtracting the returns shown. The currency with the higher return is the currency that appreciated, or increased, in relative value. For example, in 2021 the Australian dollar (AUD) appreciated against the Brazilian real (BRL) by approximately –7% minus – 9% = 2%, although both fell versus the US dollar. The importance of this table is to highlight the fact that in any given year, currency fluctuations can have a substantial impact on returns and that the best-performing currency changes each year. A few of the currencies shown here have depreciated significantly over the past 20 years, suggesting that investors residing in those countries would have benefited greatly from exposure to the US dollar as well as other currencies that appreciated over the period. Figure 6.3 demonstrates a simplified method for approximating the effect that changes in exchange rates have on investment returns.

FIGURE 6.3 Impact of Foreign Exchange Fluctuations on Investment Returns

This extremely basic example highlights the fact that exposure to foreign currencies can greatly enhance or reduce investment returns, especially over the short term. We noted in Chapter 4 that having exposure to a basket of currencies is beneficial over a long time period due to the positive impact of diversifying currency returns. Conversely, having excessive exposure to a single currency (foreign or domestic) could add significant risk to your portfolio and materially impact your investment return (positively or negatively). It is critical for investors to avoid investing in currencies that are likely to depreciate significantly, which leads us to discuss currency crises.

Currency Debasement and Crashes

Government and central bank policy usually strives to create exchange rate stability, but there are times when a deliberate effort is made to cause a currency to appreciate or depreciate compared to foreign currencies. Countries that wish to help their exporters, for example, may choose to weaken their currency so the goods they produce become less expensive for foreign buyers. Currency debasements like this may be modest and temporary in nature, in which case they would not be cause for concern. However, a continuous or severe debasement of a currency will erode investment gains and is a concern. As an investor, you must watch these situations closely and assess their significance.

The most important currency-related risk for the global investor is a currency crash, where the value of a currency falls significantly versus that of other currencies in a brief period of time. We noted earlier that even without direct exposure to the falling currency, a currency crash can eventually affect markets globally and therefore changes in currency exchange rates must be monitored on an ongoing basis. The most severe currency crashes may prompt investors to shun all risk assets, causing equity markets around the world to fall. Figure 6.4 lists some of the more notable currency crashes that have occurred in the recent past.

One of the examples listed in Figure 6.4 is referred to as the Russian financial crisis, in which declining productivity and rampant inflation led Russia's central bank to devalue the ruble. As a result, the ruble fell against the US dollar by close to 70% in less than a month, from August 14 to September 8, 1998. Stock market investors foresaw the challenges facing Russia at the time and drove stock valuations down almost 90% between late April and early October 1998. By the time the ruble was devalued, the stock market had already fallen by almost 70%. Through the actions of the central bank and aided by a strong recovery in world oil prices, Russia was able to recover from this financial crisis quickly. Domestic businesses also received help from the rapid devaluation of the currency, which made imported goods expensive for domestic consumers.

FIGURE 6.4 Examples of Modern-Day Currency Crashes

Data source: Bloomberg, as of January 16, 2022.

In our earlier discussion of the Asian financial crisis, we noted that some countries peg their currency to a major currency, such as the US dollar or euro. The purpose of doing this is to create exchange rate stability. However, if the country experiences severe economic woes, having a pegged currency can cause the country's economic problems to worsen. In some instances, especially where a currency has been pegged to a foreign currency or basket of foreign currencies, rapid currency depreciation may be deliberate. In other situations, currency depreciation may be the result of a large and sudden increase in inflation, fiscal mismanagement, or a particularly weak economic environment. Either way, if you hold investments in countries that experience a large drop in the value of their currency, your investment returns will be negatively affected.

Managing Currency Risk

As noted previously, most currency exchange rate fluctuations are modest and will reverse over time as they have a built-in self-correction mechanism. The primary concern for investors is avoiding exposure to currencies that are vulnerable to significant depreciation. Fortunately, for investors who are aware of and watching for them, there are warning signs that often precede a currency crisis.

A banking crisis is one event that can lead to currency depreciation. Since banking crises are often preceded by a significant increase in home prices, monitoring changes in house prices and housing affordability around the world is one easy step you can take to protect your portfolio. Of course, not all housing booms lead to a banking crisis. As an investor you must decide whether home price increases are based on sound and sustainable lending standards and what effect a deteriorating economic environment might have on the ability of homeowners to continue to meet their mortgage payments. Low housing affordability combined with elevated levels of consumer debt and rising mortgage rates stands out as a high-risk scenario. It should be noted that house price changes can affect the loan-to-value (LTV) ratio of underlying mortgages. If house prices are declining, the LTV will increase, resulting in the lender having less collateral to guard against a default. This makes the loan riskier and increases the probability that losses will be incurred when loans become delinquent.

Inflation also often precedes currency crashes, especially in countries that have experienced frequent bouts of inflation in the past. According to Reinhart and Rogoff “… by and large, inflation crises and exchange rate crises have traveled hand in hand in the overwhelming majority of episodes across time and countries (with a markedly tighter link in countries subject to chronic inflation, where the pass-through from prices to exchange rates is greatest.”1 As mentioned earlier, countries with high levels of external or domestic debt have a history of stimulating inflation in order to “inflate away” their debt burden and should be avoided. In situations where a country is having trouble repaying debt owed to foreigners or its citizens, it has four options: (1) reduce spending and increase taxes, (2) renegotiate the terms of the debt, (3) default, or (4) devalue the debt through inflation. The first option is the most difficult politically as the impact will be felt most by its citizens. The second option of renegotiating the terms of existing debt is attractive for the borrower but requires the cooperation of those who are owed the money. These lenders may be unwilling to agree to a reduced payment or longer repayment period. The third option of default has been used from time to time, but most countries will use this only as a last resort, as it impacts the country's status on the world stage and may hinder its ability to borrow in the debt markets well into the future. This leaves inflation as a common solution used by countries that have borrowed too heavily to reduce their debt load.

Defaulting on debt through inflation may sound complicated, but the process is quite simple. Assume you are owed a sum of money and while you are waiting to be repaid, the prices of all goods and services double. The money you are owed is now effectively worth one-half of what it was worth when you loaned it out. In earlier times, when currency was based on coinage, monarchs sometimes created money by reducing the amount of gold or silver content in their coins to mint more coins (an old-school version of currency debasement). Today, a country's central bank can simply print money and use it to repay the country's debt. The debt has been repaid but with currency now worth less than before the central bank's actions. This invariably leads to inflation.

Consistently elevated levels of inflation or a sudden and rapid rise in expected inflation indicate an elevated risk of a currency crash. In these circumstances there is no sense in waiting around for this to happen. Government policies that appear to promote price inflation and currency debasement should be taken seriously. If you begin to have significant doubts about where a certain situation is headed, sell the shares of the companies you hold in that country and move on. The world's equity markets are vast, allowing you to exit a country that appears to be heading down the wrong path and find a better opportunity to invest in a great business where a currency debasement or crash is unlikely.

Currency hedging provides another means to mitigate currency risk. However, Jeremy Siegel noted that “[a]lthough hedging seems like an attractive way to offset exchange rate risk, in the long run it is often unnecessary and even detrimental.”2 The best approach to manage currency risk is to diversify your portfolio by currency, watch for the warning signs listed previously, and act if needed. However, if currency risk poses a serious concern and exiting the position is not an option, using currency forwards to hedge (offset) the risk may be possible. A currency forward is a contract that allows you to exchange a set amount of two currencies on a specified date in the future and at a predetermined exchange rate. This can be a very cost-effective method for hedging currency risk but is limited to investors with a sizeable amount of assets, typically with a minimum of several million dollars. Since currency forwards are restricted to institutional and high-net-worth investors, and because exposure to a basket of currencies will help investors over the long term, I will leave the discussion on currency forwards for another day.