11 Revenues and Expenses

This chapter will consider revenue and expense recognition under IPSAS. Public sector entities can derive revenue from exchange and non-exchange transactions (see Figure 11.1). IPSAS 9 Revenue from Exchange Transactions is the current standard to be applied when determining how and when revenue should be recognized for exchange transactions. IPSAS 9 sets the principles for the recognition of revenue arising from the sale of goods and the rendering of services. IPSAS 23 Revenue from Non-Exchange Transactions (taxes and transfers) prescribes the requirements for accounting and reporting for revenue arising from non-exchange transactions. Common sources of non-exchange revenue in the public sector include taxes and transfers. The difference between exchange and non-exchange transactions is the substance rather than the form of the transaction. It should also be noted that within the public sector, revenue transactions can include both exchange and non-exchange components. IPSAS 11 on Construction Contracts sets out the principles for the recognition of revenue arising from long-term construction contracts. In order to cover the accounting for revenue-generating transactions, this chapter will include IPSAS 23, IPSAS 9, and IPSAS 11. The IPSASB Conceptual Framework and IPSAS 1 provide the definition of revenue1 (see Figure 11.1) and expenses.

Figure 11.1 An overview of revenue definitions

Revenue is further defined in IPSAS 1 Presentation of Financial Statements as follows: “The gross inflow of economic benefits or service potential during the reporting period when those inflows result in an increase in net/assets equity, other than increases relating to contributions from owners” (IPSAS 1.7).

The Conceptual Framework highlights the volume and significance of non-exchange transactions within the public sector.

Expenses are defined as: “Decreases in the net financial position of the entity, other than decreases arising from ownership distributions” (Conceptual Framework 5.30). Prior to proceeding with the specific IPSAS on revenue, Example 11.1 will illustrate the difference in practice between exchange and non-exchange revenue.

This chapter will, in addition to explaining the requirements of the IPSAS on revenue, address transactions that contain both exchange and non-exchange components. Accounting for principal–agent transactions is also covered.

Non-Exchange Revenue (IPSAS 23)

What is typical for public sector entities is that:

- A major part of their revenue is received as taxation or other mandatory payments by citizens or companies, rather than being paid in exchange for goods and services; many public sector bodies also receive donations or grants; and

- A major part of their expenditure involves making payments or providing services for no cost, a nominal amount, or an amount which will not recover costs. These may include payments to relieve poverty, debt forgiveness, and other social expenditures.

These are deemed “non-exchange transactions,” as the entities involved do not make exchanges of approximately equal value. This is a key characteristic of public sector financial reporting.2 Sound reporting of the financial consequences of government revenue-raising, current expenditure, and future commitments is crucial if the financial statements of governments and other public sector reporting entities are to be transparent and both to support informed assessments of financial condition and to discharge accountability obligations.

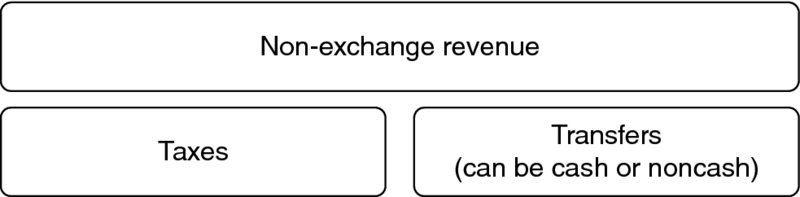

IPSAS 23 Revenue from Non-Exchange Transactions stipulates the requirements for the financial reporting of non-exchange revenue. The standard defines non-exchange revenue as shown in Figure 11.2:

Figure 11.2 Types of non-exchange revenues

In addition to taxes and transfers, IPSAS 23 stipulates special requirements for recognizing non-exchange revenue that is not classified as taxes or transfers, by considering potential stipulations on transferred assets (see Figure 11.2).

The Conceptual Framework elaborates on taxes by stating:

Taxation is a legally mandated, compulsory non-exchange transaction between individuals or entities and the government. Tax-raising powers can vary considerably, dependent upon the relationship between the powers of the national government and those of sub-national governments and other public sector entities. Governments and other public sector entities are accountable to resource providers, particularly to those that provide resources through taxes and other compulsory transactions. International public sector entities are largely funded by transfers from national, regional and state governments. Such funding may be governed by treaties and conventions or may be on a voluntary basis. (para. 6, p. 7)

Transfers on the other hand include debt forgiveness, fines, grants, gifts, donations, goods and services in-kind, bequests, and concessionary loans.

In certain cases of non-exchange transactions the recipient obtains assets for nil consideration and does not make any payment. Certain transactions can also be at subsidized prices – these also constitute non-exchange transactions.

Recognizing Non-Exchange Revenue

IPSAS 23 draws on a transactional approach (cf. Schumesch, 2013) which means that the first step is to determine whether an asset should be recognized in regard to the inflow of resources from the non-exchange transaction. If an asset can be recognized, the revenue is recognized, except to the extent that a liability is recognized in respect of the same inflow.

Recognizing an asset

The principle underlying the recognition of revenue from non-exchange transactions is that if an entity receives an asset in a non-exchange transaction it recognizes revenue in the same amount, provided that the asset can be measured reliably. An asset is defined as: “A resource presently controlled by the entity as a result of a past event” (see Conceptual Framework 5.6). Revenue is recognized when: it is probable that future economic benefits or service potential will flow to the entity; and the amount of revenue can be measured reliably.

Within the public sector assets arising from non-exchange transactions can take a number of forms such as:

- Cash and cash receivable;

- Other assets or receivables which provide economic benefit;

- Assets or assets receivable which have service potential.

Revenue is recognized when the public sector entity exercises control over these resources or has reliable information on enforceable claims on these resources. Control of an asset arises when the entity can use or otherwise benefit from the asset in pursuit of its objectives and can exclude or otherwise regulate the access of others to that benefit.

Revenue should only be recognized when control has passed to the receiving entity, on the basis of information which is sufficiently reliable. Pledges, promises, or announcements of intention to pay are not generally regarded as sufficient to ensure an enforceable claim and thus control of an asset. It should be noted that revenue collected on behalf of third parties is not classified as part of the entity's revenue.

It is important to note that there are three significant situations where assets received are not reflected as non-exchange revenue (see Figure 11.3).

Figure 11.3 Assets received are not reflected as non-exchange revenue

An example of an asset with a linked obligation would be that of funding provided by a donor agency to improve and maintain a school. If such a condition is set, the recipient has an obligation to spend the money in this way and therefore a liability to incur such expenditure, or to return the money received.

Stipulations on transferred assets

IPSAS 23 presents three important definitions in terms of recognition of non-exchange revenue that does not classify as transfers or taxes, namely (Figure 11.4).

Figure 11.4 Stipulations on transferred assets

Stipulations are enforceable through legal or administrative processes. If a term in laws or regulations or other binding arrangements is unenforceable then it is not a stipulation. This means that stipulations cannot be imposed by an entity on itself.

Following IPSAS 23, stipulations can either be in the form of conditions or in the form of restrictions. For both conditions and restrictions, a recipient may be required to use the transferred asset for a particular purpose. The key difference between a restriction and a condition is that a condition has an additional requirement which states that the asset or its future economic benefits or service potential should be returned to the transferor should the recipient not use the asset for the particular purpose stipulated.

Conditions

When applying IPSAS 23, public sector entities typically need to review all agreements with, for example, donors and other parties, and analyze any and all stipulations attached to an inflow of resources, to determine whether those stipulations impose conditions or restrictions. Stipulations can be either conditions or restrictions on the transferred assets.

Stipulations on transferred assets are terms in the agreement, imposed upon the use of a transferred asset by entities external to the reporting entity. Conditions on transferred assets are stipulations that specify that the future economic benefits or service potential embodied in the asset is required to be consumed by the recipient as specified or future economic benefits or service potential must be returned to the transferor.

Restrictions

Restrictions on transferred assets are stipulations that limit or direct the purposes for which a transferred asset may be used, but do not specify that future economic benefits or service potential are required to be returned to the transferor if not deployed as specified.

Recognizing a liability

A present obligation that arises from a non-exchange transaction that meets the definition of a liability is recognized as a liability when, and only when:

- It is probable that an outflow of resources embodying future economic benefits or service potential will be required to settle the obligation; and

- A reliable estimate can be made of the amount of the obligation.

See Figure 11.3. for a description of assets with linked obligations.

The amount recognized as a liability is the best estimate of the amount required to settle the present obligation at the reporting date. The estimate takes account of the risks and uncertainties that are encompassed in the events causing the liability to be recognized. Where the time value of money is material, the liability will be measured at the present value of the amount expected to be required to settle the obligation.

Measurement

As described above, IPSAS 23 recognizes revenue when an asset is received and controlled by the entity and when it can be measured reliably.

Under IPSAS 23, assets acquired through non-exchange transactions are measured at their fair value at the date of acquisition. Revenue is valued at the amount of the increase in assets, less any associated liability attached to the asset. Many such assets are in the form of cash received immediately or within a short period, and establishment of fair values will be straightforward. As with all receivables, questions of collectability due to disputes and delays in payment may need to be addressed (IPSAS 23.42 and 23.48).

Liabilities relating to present obligations also need to be valued. Where non-performance of the obligation would, in principle, require the asset to be returned, these are generally valued at an amount equal to the asset value. The liability will be reduced when the event or events occur to discharge the obligation and these will also trigger revenue recognition.

IPSAS 23 applies to taxes from whatever source, including property taxes, and other transfers such as grants, fines, bequests, gifts, donations, and services in-kind.

Tax Revenue

IPSAS 23 requires a public sector entity to recognize an asset in respect of taxes when the taxable event occurs and the asset recognition criteria (including control, expectation of future economic benefits or service potential, and reliable measurement) are met (IPSAS 23.59).

Taxes are a major source of revenue for many governments and public sector entities. Taxes are defined as economic benefits compulsorily payable to public sector entities, in accordance with laws or regulations established to provide revenue to the government.

Taxes vary significantly from jurisdiction to jurisdiction, but have many common characteristics. Laws and regulations establish a government's right to collect tax and identify the basis on which tax is calculated. They also typically require taxpayers to provide evidence of the level of activity subject to tax, which forms the basis on which the amount of tax is calculated. Tax laws are usually rigorously enforced and often impose penalties on individuals or other entities breaching the law.

The taxable event will vary following the type of tax levied; IPSAS 23 (65) provides a list of frequently seen cases (see Table 11.1).

Table 11.1 Taxable events according to type of tax levied

| Types of taxes | Taxable events |

| Income tax | The earning of assessable income during the taxation period by the taxpayer. |

| Value added tax (VAT) | The undertaking of taxable activity during the taxation period by the taxpayer. |

| Goods and services tax | The purchase or sale of taxable goods or services during the taxation period. |

| Customs duty | The movement of dutiable goods or services across the customs boundary. |

| Death duty | The death of a person owning taxable assets. |

| Property tax | The passing of the date on which the tax is levied or the period for which the tax is levied, if the tax is levied on a periodic basis. |

IPSAS (23.68) describes key features of taxation issues in many jurisdictions which may serve to delay settlement of tax and make the level of settlement uncertain, and may require the development of statistical models or other estimation approaches. These include the long periods allowed for filing of returns, failures to file returns by the due date, complexities in tax law, and inherent problems in gathering relevant information.

Because of the need for governments to maintain cash flows from tax receipts it is normal for tax authorities to require payments in advance, particularly from self-employed persons and businesses. IPSAS 23 makes it very clear that the very significant volume of advance tax receipts encountered in many jurisdictions should not be recognized as revenue until the tax is properly due. Governments applying accruals accounting should recognize tax revenue in line with the taxable events, applying tax rates to taxable income or assets.

The tax area is one where many (perhaps most) governments face significant practical difficulties in producing reliable estimates of total tax due and the likely level of bad debts. In many jurisdictions government will not be able to estimate these even after collection processes have been completed; they may only be able to objectively and reliably measure the net amount of taxes collected.

Furthermore, governments will often face additional constraints from limitations in the systems used to collect and account for tax receipts (whether their own or systems used by other entities collecting tax on behalf of government), which may not provide sufficient information on the period to which tax receipts relate.

For the reasons set out above, many governments either do not account for tax revenue on an accruals basis, or provide accruals information which is limited due to difficulties in producing reliable estimates. IPSAS 23 recognizes the difficulties and requires disclosure of information on “missing” tax revenue.

Application to Other Types of Non-Exchange Revenue

IPSAS 23 applies the same recognition principles to other non-exchange revenue. That is, a public sector entity recognizes an asset when the asset recognition criteria (including control, expectation of future economic benefits or service potential, and reliable measurement) are met. Revenue is only recognized to the extent that a gain from the asset value is not reduced by an associated liability.

Although grants are not defined in IPSAS 23, they represent a significant type of revenue from non-exchange transactions. Grants are frequently provided from one level of government to another or from donor agencies to governments. Several of the examples in the Implementation Guidance relate to grants.

Grants are often provided with limitations on how money should be spent or assets utilized. The standard separates such “stipulations” into:

- Conditions, where the money must be spent as specified or returned to the donor (in other words a performance obligation); and

- Restrictions, where there is a more general requirement to spend the money in a specified area but not to return it if this is not achieved.

This distinction may not always be clear cut and it is necessary to consider the substance of the stipulation and not merely its form. This might take into account the likelihood of enforcement, prior experience with the donor, the extent of specification of detailed requirements, and the degree of monitoring by the donor (IPSAS 23.14–23.19).

Where the recipient entity considers that the donor has imposed conditions, they will set up a liability for the obligation generally to the value of the money received, which will be reduced as the conditions are satisfied (by spending the money or through other actions) in accordance with the agreement. There is no such requirement for grants with restrictions and revenue is therefore recognized immediately.

Other Types of Non-Exchange Revenue

Fines

Fines are levies on individuals or entities for breaches of the law. Fines are recognized in the period in which the fine is imposed (IPSAS 23.88, 23.89).

Bequests

Bequests are instructions in a deceased person's will to transfer cash or other assets to an entity. Bequests are recognized when the nature of the bequest is known and it has been established that the estate is sufficient to meet all claims. As with grants, bequests may contain stipulations as to how the money or assets are to be spent or utilized (IPSAS 23.90–23.92).

Gifts and donations

Gifts and donations are voluntary transfers of cash or other assets to an entity. Gifts and donations are generally recognized on receipt of the cash or other asset. Pledges to give in the future are not generally recognized as they are not controlled by the entity, but may warrant disclosure as a contingent asset. As with grants and bequests, gifts and donations may be subject to stipulations as to how the money or assets are to be spent or utilized (IPSAS 23.93–23.97).

Debt forgiveness

Lenders may waive their right to collect a debt owed by a public sector entity, thus effectively cancelling the debt. In such a case the entity has an increase in net assets/equity and treats the amount forgiven as revenue from a non-exchange transaction (IPSAS 23.84–23.87).

Services in-kind

Services in-kind are voluntary services provided to an entity by an individual or individuals. Such services may include free technical assistance from other governments or international organizations, voluntary work in schools and hospitals, or community services performed by convicted offenders. The standard provides that entities may, but are not required to, recognize services in-kind as revenue and expenditure where the amount can be measured, is material, and its inclusion enhances the presentation of the financial statements. Disclosure of the nature of significant in-kind services in all cases is encouraged (IPSAS 23.98–23.103).

UNESCO recognizes interest-free loans as in-kind contributions, considering the fact of not paying interests on loans benefits UNESCO and is therefore a service in-kind.

Non-Exchange Revenue: Principal–Agent

Amounts collected as an agent of the government or another government organization or other third parties will not give rise to an increase in net assets or revenue of a public sector entity. This is due to the fact that the public sector entity, in this case, cannot control the use of, or otherwise benefit from, the collected assets in the pursuit of its objectives.

Transitional Provisions

IPSAS 23 (23.116–23.123) stipulates the transitional provisions which exist in the standard. IPSAS 23 provides that: (1) Entities are not required to change their accounting policies in respect of the recognition and measurement of taxation revenue for reporting periods beginning on a date within five years following the date of first adoption of IPSAS 23; and (2) Entities are not required to change their accounting policies in respect of the recognition and measurement of revenue from non-exchange transactions, other than taxation revenue, for reporting periods beginning on a date within three years following the date of first adoption of IPSAS 23.

The transitional provisions are providing for entities to apply the transition period to develop reliable models for measuring revenue from non-exchange transactions during the transitional period. Entities may adopt accounting policies for the recognition of revenue from non-exchange transactions that do not comply with the provisions of IPSAS 23 during the transitional period. Considering the difficulty of implementing IPSAS 23, the transitional provisions allow entities to apply IPSAS 23 incrementally to different classes of revenue from non-exchange transactions. It should be emphasized that when an entity applies the transitional provisions in paragraphs 116 or 117, that fact shall be disclosed in order to alert the user of the financial statements to the fact that IPSAS 23 is not yet fully implemented. The entity shall also disclose (a) which classes of revenue from non-exchange transactions are recognized in accordance with IPSAS 23; (b) those that have been recognized under an accounting policy that is not consistent with the requirements of this Standard; and (c) the entity's progress towards implementation of accounting policies that are consistent with IPSAS 23. The entity shall disclose its plan for implementing accounting policies that are consistent with IPSAS 23 (IPSAS 23.119).

In addition, when an entity takes advantage of the transitional provisions for a second or subsequent reporting period, details of the classes of revenue from non-exchange transactions previously recognized on another basis, but which are now recognized in accordance with IPSAS 23, shall be disclosed (IPSAS 23.120).

Disclosure Requirements for Non-Exchange Revenue

IPSAS 23 requires disclosure of the following (IPSAS 23.106–23.107):

- The accounting policies for the recognition of revenue from non-exchange transactions including, for major classes, the basis of assessing fair value;

- Information about the nature of taxes which cannot be measured reliably and are therefore not recognized;

- The nature and types of major classes of bequests, gifts and, donations;

- The amount of revenue from taxation, split by major classes;

- The amount of other revenue/transfers from non-exchange transactions, split by major classes;

- The amount of receivables in respect of revenue from non-exchange transactions;

- The amount of liabilities from amounts received with conditions, and from advance payments, as well as liabilities forgiven;

- The amount of assets subject to restrictions.

The disclosure of information about services in-kind is encouraged (IPSAS 23.108).

UNESCO discloses the accounting policies for the recognition of revenue from non-exchange transactions. UNESCO does not recognize other in-kind contributions such as the services of volunteers. However, the nature of this significant in-kind contribution is discloses in the note relating to non-exchange revenue. UNESCO specifically discloses the amount of receivables in respect of revenue from non-exchange transactions, which relate mainly to assessed contributions from Member States and Associated Members.

Revenue from Exchange Transactions (IPSAS 9)

Public sector entities receive revenue in payment for goods or services under normal contractual arrangements similar to those undertaken by private sector businesses (“exchange transactions”). Examples of services provided by public sector entities for which “equal value” revenue is typically received include the provision of housing and toll roads. Goods sold may include goods produced by the entity for the purpose of sale, such as publications, and goods purchased for resale. Revenue may also be received where others use entity assets in the form of interest, royalties, charges for the use of patents, trademarks, copyrights and computer software, and dividends. Effective and sound accounting for revenue is imperative to disclose the substance of what can be complex transactions.

IPSAS 9 apply to revenue from the following transactions and events:

- The sale of goods

- The rendering of services

- Interest, royalties and dividends.

These standards do not deal with revenue arising from actitivies which are the subject of other standards, and therefore exclude:

- Lease agreements

- Dividends arising from investments accounted for under the equity method

- Insurance contracts in insurance enterprises

- Changes in the fair value of financial assets and financial liabilities

- Changes in the fair value of other assets

- Biological assets, agricultural produce, or the extraction of mineral ores

- Non-exchange revenue transactions, such as taxes and grants.

The primary issue in accounting for revenue is determining when to recognize revenue. Exchange revenue is recognized when:

- It is probable that future economic benefits will flow to the entity

- The amount of revenue can be measured reliably.

All costs associated with the revenue should be accounted for in the same period as the revenue is recognized. This is commonly referred to as the matching of revenue and expenses.

Measurement

Revenue should be measured at the fair value of the consideration received or receivable. It should be highlighted that consideration is not limited to payments in cash (IPSAS 9.14).

The amount of the payment will normally be expressed in the agreement between the buyer and the seller. Revenue is recognized after taking into account trade discounts or volume rebates that are given.

In most cases consideration is in the form of cash and this will be paid on receipt of the goods or services or shortly afterwards. Here the amount of revenue recognized is the amount of cash received or receivable.

In some cases the payment may be deferred for a longer period providing the buyer with an interest-free credit period. In such cases the amount of revenue recognized should be determined by discounting all future receipts to present value.

For all forms of exchange revenue the two general conditions for revenue recognition have to be met, i.e., that (1) it is probable that future economic benefits (or service potential) will flow to the entity; and (2) the amount of revenue can be measured reliably.

The Sale of Goods

The conditions below apply to the sale of goods (IPSAS 9.28):

- It is probable that the future economic benefits (or service potential) will flow into the entity;

- The amount of revenue can be measured reliably;

- The seller must have transferred to the buyer all of the significant risks and rewards of ownership;

- The seller no longer has management involvement or effective control of the goods;

- The costs incurred in relation to the transaction can be reliably measured.

All five of these above-listed conditions must be met before revenue on the sale of goods can be recognized.

The transfer of the significant risks and rewards of ownership to the buyer can sometimes be challenging to determine. Nevertheless, in most instances, the transfer of significant risks and rewards of ownership coincides with the transfer of legal title or the passing of possession to the buyer. This is the case for most sales of goods. In other cases, the risks and rewards of ownership may pass at a different time to the transfer of legal title or the passing of possession to the buyer.

Examples of where the risks and rewards of ownership would not pass to the buyer and where no sale or revenue would be recognized include:

- When the seller retains an obligation for unsatisfactory performance not covered by a normal warranty arrangement;

- When goods are sold on a sale or return basis;

- When the buyer has the right to rescind the purchase and the enterprise is uncertain about the probability of return.

In each of these cases no revenue would be recognized.

The Rendering of Services

Additional conditions also apply to the rendering of services (IPSAS 9.19):

- The stage of completion can be measured reliably;

- The costs incurred and the costs to complete in relation to the transaction can be reliably measured.

All of these conditions must be met before revenue can be recognized.

Revenue is recognized by reference to the stage of completion using what is known as the percentage of completion method. The stage of completion can be determined via a number of methods. IPSAS 9 stipulates three possibilities, namely:

- Surveys of work performed;

- Assessing the services performed to date against the total services to be performed under the contract;

- Assessing the costs incurred to date against the total costs to be incurred under the contract.

When the outcome of a transaction involving the rendering of services cannot be estimated reliably, revenue should only be recognized to the extent that costs incurred to date are recoverable from the customer.

Interest, Royalties, and Dividends

Revenue should be recognized on the following basis (IPSAS 9.34):

- Interest revenue is recognized on a time apportioned basis.

- Royalties are recognized on an accrual basis.

- Dividends are recognized when the shareholders' right to receive the dividend is legally established. This is usually when dividends are declared.

Exchanges of Assets

Special rules apply where goods or services are exchanged.

| Similar goods or services | Dissimilar goods or services |

| Where the entity receives similar goods or services as payment, this is essentially a “swap” transaction. The company is replacing one asset for another similar asset. In such cases no revenue is generated, with no additional cost reported. Such transactions are quite common in the sale of commodities, for example milk, with suppliers exchanging inventories to fulfill demand in a particular location. | When the payment is receivable in the form of dissimilar goods or services, revenue is generated and costs should be recognized. In such cases the transaction is measured based on the fair value of what will be received. If it is not possible to measure the value of the goods or services received reliably, then the revenue should be based on the fair value of the goods or services supplied. |

Disclosure Requirements

The following disclosures should be made in terms of exchange revenue:

- The accounting policies adopted for recognizing revenue, including the methods adopted in determining the stage of completion for transactions involving the rendering of services;

- The amount of each significant category of revenue recognized;

- The amount of revenue recognized from exchanges of goods or services.

Transactions that Include Both an Exchange and Non-Exchange Component

There are instances where a transaction can be a combination of exchange and non-exchange transactions. In these instances the entity needs to determine what portion of the transaction is an exchange transaction and what portion is a non-exchange transaction and then recognize them separately.

For some transactions it can be difficult to distinguish whether or not a transaction is exchange or non-exchange. In order to make the proper classification between exchange and non-exchange, the entity has to consider the substance of the transaction (IPSAS 9.6).

If it is not possible to distinguish between the exchange and non-exchange components, the transaction should be treated as a non-exchange transaction.

Principal–Agent Accounting

This section considers principal–agent relations and their implications for accounting. Principal–agent relations raise a number of complex accounting questions and it should be emphasized that this section only provides an overview of these issues. A number of arrangements within the public sector, between public sector entities, involve principal–agent relationships. These relationships affect whether or to what extent an entity recognizes revenue, expenditure, assets, and liabilities as its own. An example is whether an entity recognizes the full amount earned on a sales transaction or commission as revenue.4

Distinguishing whether an entity acts as a principal or an agent in an arrangement is often subjective. This assessment becomes more complex in the public sector as the lines between agent, principal, transferor, recipient, and service provider are potentially more blurred in transactions between public sector entities. This is due to the different circumstances under which these arrangements are entered into, the structures within government, the motivation for entering into arrangements between entities being to enhance service delivery.

Identification of Principals and Agents

The key issue when dealing with agent–principal scenarios is being able to identify whether an entity is acting as an agent or not. Table 11.2 provides an overview of indicators that can be used in order to distinguish between principal and agent.

Table 11.2 Indicators to distinguish between principal and agent

| No. | PRINCIPAL | AGENT |

| 1 | Indicator: Decision-making ability | |

| The entity has ultimate decision-making discretion, for example the selection of suppliers. | The entity may have some decision-making discretion and authority, although this is limited and often subject to the ultimate approval of another party and can be revoked at the discretion of another party. | |

| 2 | Indicator: Inventory risk | |

| The entity has inventory risk. The entity is not explicitly compensated for the risk assumed. | The entity may have inventory risk conveyed to it (accepted by it) contractually. However, the risk is usually limited and the entity is typically compensated accordingly by the principal. | |

| 3. | Indicator: Credit risk | |

| The entity assumes credit risk for the amount receivable from the end customer. Apart from compensation received directly from the customer in the form of interest or collateral, the entity is generally not compensated by a third party (either explicit or implicit) for the credit risk assumed. | The entity may have credit risk conveyed to it. However, the risk is usually limited and the entity is typically compensated accordingly by the principal. | |

| 4. | Indicator: Price determination | |

| The entity has latitude in establishing prices (within the confines of the economic market and prevailing legislation). It has the ability unilaterally to raise or lower prices (to any level). | The entity may have the ability to determine prices, but subject to the parameters stipulated by a third party. | |

| 5. | Indicator: Value added processes | |

| The entity performs part of the service itself or modifies the goods that are being supplied in some way. | The entity does not add any significant value in the process and merely acts as a go-between. | |

| 6. | Indicator: Accountability | |

| The entity has prime accountability in respect of the arrangement (to other external parties). It does not portray itself as an agent. | The entity is primarily accountable to the principal, rather than to any other party directly. It discloses the fact that it is acting as an agent. |

Principal–Agent Identification Impact on Accounting Requirements

Assessing whether the entity acts as a principal or an agent has an immediate impact on the recording of elements: recognition of revenue, expenses, assets, and liabilities arising from the arrangement. Figure 11.5 illustrates the impact visually.

Figure 11.5 Principal–agent relations and accounting impact

Principal–agent relations also impact the elements to be presented on the face of the financial statements and disclosed in the notes to the financial statements.

UNOPS explains that it had to consider whether it acted as a principal or an agent in its projects, which happened to be very difficult in practice. UNOPS discloses the differences applying to the methods of recognition and presentation of revenue (either in full as principal or in net as agent).

Construction Contracts (IPSAS 11)

The objective of IPSAS 11 is to prescribe the accounting treatment for revenue and costs relating to construction contracts.

Construction contracts may involve:

- Constructing a single asset such as a bridge, building, or dam;

- Constructing a number of interrelated or interdependent assets such as refineries or other complex pieces of plant or equipment;

- Rendering services directly related to the construction of the asset such as the services of project managers or architects; or

- Destruction or restoration of assets.

The dates on which a construction contract starts and ends usually fall in different accounting periods, so the principal concern is how to allocate revenue and costs to the different accounting periods to reflect the reality of the construction activity as it takes place.

Construction contracts represent an important part of the activity of UNOPS, around one third of its total expense in 2012. UNOPS discloses the type of contracts of delivery of infrastructure projects they perform, and the list of its most active projects.

There are two distinct types of construction contract, shown in the following table:

| Fixed price contracts (IPSAS 11.4) | Cost plus contracts (IPSAS 11.4) |

| Where the revenue arising is fixed, either for the contract as a whole or on units of output, at the outset of the contract. Under such contracts there is an element of certainty about the revenue accruing, but not about the costs which will arise. | Where costs will be recoverable plus some agreed element of profit. Under such contracts there is a high degree of certainty about the profit arising although there is no certainty about either the revenue or the costs. |

The distinction between the two types of contract is particularly important when deciding the stage at which contract revenues and expenses should be recognized.

When a construction contract covers two or more assets, the construction of each asset should be treated separately if (IPSAS 11.13):

- Separate proposals were submitted for each asset;

- Portions of the contract relating to each asset were negotiated separately;

- Costs and revenues of each asset can be identified.

A group of contracts should be accounted for as a single contract when (IPSAS 11.14):

- They were negotiated together;

- The work is interrelated;

- The contracts are performed concurrently or in a continuous sequence.

In case a contract gives the customer an option to order additional assets, construction of each additional asset should be accounted for as a separate contract if (IPSAS 11.15):

- The additional asset differs significantly from the original asset(s); or

- The price of the additional asset is separately negotiated.

Determination of Contract Revenue and Contract Costs

Contract revenue includes (IPSAS 11.16):

- The amount agreed in the contract initially;

- Contract work variations, claims, and incentive payments.

Contract work variations, claims, and incentive payments are only included to the extent that (a) they are expected to generate revenue; and (b) they can be measured reliably (IPSAS 11.16).

Contract costs concern costs (IPSAS 11.23)

Contract costs include:

- Those directly relating to the specific contract;

- Costs that are attributable to the general activity of the contractor to the extent that they can be systematically and rationally allocated to the contract;

- Other costs that can be specifically charged to the customer under the terms of the contract.

Application of the percentage of completion method

In case the outcome of a construction contract can be estimated reliably, revenue and costs related to the contract should be recognized in proportion to the stage of completion of contract at the reporting date (IPSAS 11.30).

An entity can estimate the outcome of a contract reliably when it is able to make a reliable estimate of total contract revenue, the stage of completion, and the costs to complete the contract (IPSAS 11.31–11.32).

The stage of completion of a contract can be determined in different ways, including the following methods (IPSAS 11.38):

- The proportion that contract costs incurred for work performed to date bear to the estimated total contract costs;

- Surveys of work performed;

- Completion of a physical proportion of the contract work.

What if the outcome of the contract cannot be estimated reliably?

In case the outcome cannot be estimated reliably, contract revenue should only be recognized to the extent that contract costs incurred are expected to be recoverable and contract costs should be expensed as incurred (IPSAS 11.40).

Expected deficits on construction contracts should be recognized immediately as an expense as soon as such deficit is probable, but only when it is intended at inception that the contract costs are to be fully recovered (IPSAS 11.44). In case of a non-commercial contract where the contract costs will not be fully recovered from the parties to the contract, when the deficit will be compensated by a government appropriation, general purpose grant, or allocation of government funds to the contractor, the requirement of the recognition of the deficit does not apply (IPSAS 11.46).

Disclosures

The following disclosures are required:

- Amount of contract revenue recognized;

- Method used to determine contract revenue;

- Method used to determine stage of completion of the contract.

For contracts in progress at the reporting date:

- Aggregate costs incurred and recognized surpluses (less recognized deficits);

- Amount of advances received;

- Amount of retentions.

Expense Recognition

There is no one specific IPSAS that details all accounting requirements for expenses and expense recognition. Expenses are defined in the Conceptual Framework, and can be considered against the requirements of accrual basis accounting. This results in a “balance sheet” approach to expense recognition, with analysis as to whether an event or transaction has resulted in a decrease in assets or an increase in liabilities. Specific types of expenses are dealt with directly by other standards, for example, IPSAS 17 for depreciation relating to property, plant, and equipment.

Expenses are decreases in economic benefits or service potential during the reporting period in the form of outflows or consumption of assets or increases in liabilities that result in decreases in net assets/equity, other than those relating to distributions to owners.

Expenses such as for example, cost of sales, employee costs, and depreciation result in the consumption of assets such as cash, inventory, and property, plant and equipment, or the increase in a liability such as an accrual or accounts payable. Expenses also result if a liability is recognized for a provision, or when an asset is reduced due to impairment.

Under the accrual basis, expenses are recognized when the transaction or event causing the expense takes place. The recognition of the expense is thus not linked to when cash or its equivalent is received or paid. An expense can result from a transaction that does not have to involve an outflow of cash.

A distinction should be made between the word “expense” and the word “expenditure” from an accounting perspective. It is helpful to restrict the use of the word “expenditure” to cash outlays. Expenditures may be cash outlays for capital assets (capital expenditures) or cash outlays for operating purposes (operating expenditures). A capital expenditure, for example the purchase of a vehicle, generally does not immediately result in an expense, although expenses will follow later as the asset is consumed and depreciation or amortization expenses are accrued. An operating expenditure may follow an expense.

Table 11.3 provides examples of expense amounts and recognition points.

Table 11.3 Overview of expenses with corresponding recognition points

| Type of Item | Expense Amount | Examples | Recognition Point |

| Purchase of an item that is not capitalized | The cost of the item | Office supplies Utilities Plant and equipment below the capitalization threshold | Delivery of the item |

| Inventory | The cost of the item | Restaurant stock that meets the definition of inventory | Inventory is sold, distributed, and control passes from the public sector entity in question |

| Depreciation of property, plant, and equipment | Depreciation expense as determined by IPSAS 17 – a part of the cost of the asset | Computers, vehicles, buildings | As the asset is used (over its useful life) |

| Impairment | Depends on the estimated decrease in the value of the asset below its previous book value | Impairment affects a variety of different assets, including property, plant, and equipment | An event (such as damage or obsolescence other than normal usage) to cause a drop in asset value |

| Salary and consulting expenses | Gross salaries or amounts agreed in a contract for consulting services | Salary | Services are provided with the result that the public sector entity in question is obliged to remunerate the staff member or consultant |

| Provisions | The amount of the provision or increase in the provision as determined by IPSAS 19 | Provision for litigation | An obligation that is probable and can be reliably measured exists as a result of a past event |

Non-Exchange Expenditure

Governments and public sector entities provide a wide range of services and payments to benefit the general public, individuals, and households. Such items are generally known as social benefits and are, for the most part, either provided free or for a small consideration, and therefore constitute non-exchange transactions. The overall aim of social benefits is to seek to provide all citizens with acceptable minimum standards in such areas as for example education, health, and security.

No standard covering non-exchange expenditure has yet been issued (see Chapter 18 which highlights that this topic is on the future work agenda of the IPSASB). Accounting for non-exchange goods and services is generally considered straightforward. Accounting for cash transfers raises difficult questions about when a liability should be recognized. This is a challenging and politically sensitive area. Expense recognition is discussed in more detail at the end of this chapter.

Types of non-exchange expenditure

The IPSASB distinguishes between these main types of social benefits as follows:

- Collective goods, individual goods, and services;

- Cash transfers to individuals and households.

In essence, these are services provided to all members of the public or to all those within a particular area. They include such major activities as:

- National defence;

- International relations;

- Public order and safety (including police services, fire protection services, law courts, and prisons);

- The efficient operation of the social and economic system of a country;

- Certain components of services to individuals such as formulation and administration of government policy; setting and enforcement of standards, regulation, and licensing of personnel and institutions; and applied research and experimental development.

Overall, these services can be seen as seeking to provide a secure environment in which all citizens may live.

Individual goods and services

Most often these are services provided by public sector entities to individuals who have particular need of them. Key examples include education and health services. Governments generally provide schooling for children of the relevant ages. Many governments also provide health services, including consultations with doctors, the supply of medicines, and care in hospitals. Such services may be provided free or at heavily subsidized charges.

Cash transfers to individuals

These include such expenditure as child benefits, invalidity and sickness benefits, unemployment benefits, housing benefits, and old age pensions. A common feature of these benefits is that they are almost always paid in cash, thus leaving the spending priorities to the discretion of the recipients. Otherwise the conditions and eligibility requirements are likely to vary considerably between jurisdictions. In particular, old age benefits (state pensions) may be available to all citizens above a certain age, or only to those who have participated in the workforce or who have paid taxes or contributions for a specified period.

Accounting for non-exchange expenditure and wider views of liability

Accounting for collective goods and services, and for individual goods and services, is generally considered straightforward and expenditure is mostly recognized in the normal way when:

- A liability relating to goods or services is incurred through transactions with an employee or a third-party provider; or

- Assets are depreciated.

When accounting for transactions carried out for nil consideration in particular, there is no significant requirement to recognize expenditure based on a liability to the recipients of goods and services. Whilst a liability to service recipients may be considered to arise, this is normally deemed to closely match the other liabilities so that no separate accounting is needed.

The question of whether, and when, governments should recognize liabilities to recipients of cash transfers is a sensitive matter on which there is considerable debate. Some suggest that the application of private sector reporting approaches means that liabilities do not need to be recognized, or should be recognized very shortly before settlement of the liability through cash transfer. Others suggest that a more general liability might be seen to arise by virtue of taxpayers as a whole providing (or being expected to provide) revenue through taxation which the taxpayers expect to be used for social benefit purposes amongst other things.

Pensions paid to former employees represent an exchange transaction. The pension payment is part of the benefits payable in return for services provided as an employee, which can be interpreted differently from minimum pensions payable to old persons who have not contributed enough to the system and who live below the poverty line. In the latter case, they represent non-exchange transactions.

UNESCO discloses its policy relating to non-exchange expenditure, explaining that expenses are recognized when the transaction or event causing the expense to occur (not when cash is received or paid): when funding is legally in force (except when there is a condition on transferred assets), when revenue is recognized from in-kind contributions.