17 Specific Standards: Accounting for Agriculture and Accounting in Hyperinflation Economies

This chapter covers IPSAS 27 Agriculture and IPSAS 10 Financial Reporting in Hyperinflationary Economies. These are two specific IPSAS standards, one linked to the activity, the other one linked to the economical and monetary environment:

- IPSAS 27 relates to reporting on agricultural activity, which is of marginal relevance to most public sector entities; and

- IPSAS 10 is aimed at entities whose functional currency is the currency of a hyperinflationary economy.

Agriculture (IPSAS 27)

Reporting on agricultural activity is of marginal relevance to most public sector accounts preparers, although significant in some jurisdictions, notably in countries where part or all of agricultural land and activities are state owned. An agricultural activity is the management by an entity of the biological transformation of biological assets: for sale, into agricultural produce, or into additional biological assets.

Farming and the agricultural sector have many unique aspects. For example, animals and plants, described as biological assets, have characteristics which are not present in other industries. Another significant feature is that government assistance in the agricultural sector is common and is often substantial. However assistance does not necessarily mean that IPSAS 27 is to be applied to these activities.

For instance, the mission of World Food Programme (WFP):

is to end global hunger. Every day, WFP works worldwide to ensure that no child goes to bed hungry and that the poorest and most vulnerable, particularly women and children, can access the nutritious food they need. WFP supports national, local and regional food security and nutrition plans. It partners with other United Nations agencies, international organizations, non-governmental organizations, civil society and the private sector to enable people, communities and countries to meet their own food needs (WFP, 2014)

Nevertheless, none of WFP activities are within the scope of IPSAS 27 on Agriculture. They fall in the scope of IPSAS 12 on Inventories.

Agricultural activity is described as the management by an entity of the biological transformation of living animals or plants (biological assets) for sale, or for distribution at no charge or for a nominal charge or for conversion into agricultural produce or into additional biological assets (IPSAS 27, IN1; para. 9). Biological assets are to be measured at fair value less costs to sell unless fair value measurement is unreliable. The standard presumes that the fair value of agricultural produce can be determined reliably, which serves as the costs basis for application of IPSAS 12 Inventories subsequently.

Agricultural produce is the harvested product of the entity's biological assets and a biological asset is a living animal or plant (IPSAS 27, para. 9). IPSAS 27 provides a table with examples of biological assets, agricultural produce, and products that are the result of processing after harvest – see Table 17.1 (IPSAS 27, para. 6):

Table 17.1 Biological assets, agricultural produce, and products that are the result of processing after harvest

| Biological assets | Agricultural produce | Products that are the result of processing after harvest |

| Sheep | Wool | Yarn |

| Trees in a plantation forest | Felled trees | Logs |

| Plants | Cotton | Thread, clothing |

| Dairy cattle | Milk | Cheese |

| Pigs | Carcass | Sausage |

IPSAS 27 applies to (IPSAS 27.2):

- Biological assets;

- Agricultural produce at the point of harvest, described as the detachment of produce from a biological asset or the cessation of a biological asset's life processes.

IPSAS 27 does not apply to:

- Land related to agricultural activity;

- Intangible assets related to agricultural activity;

- Biological assets held for the provision or supply of services.

IPSAS 27 does not establish any new principles for land related to agricultural activity. Instead, an entity follows IPSAS 16 Investment Property or IPSAS 17 Property, Plant and Equipment, depending on which standard is appropriate in the circumstances.

Recognition

A biological asset or agricultural produce is recognized in the statement of financial position when, and only when, the following three criteria are met:

- Past event has occurred and resulted in the entity having control over the asset;

- It is probable that the future economic benefits, or service potential, associated with the asset, will flow to the entity; and

- The fair value or cost of the asset can be measured reliably.1

Measurement

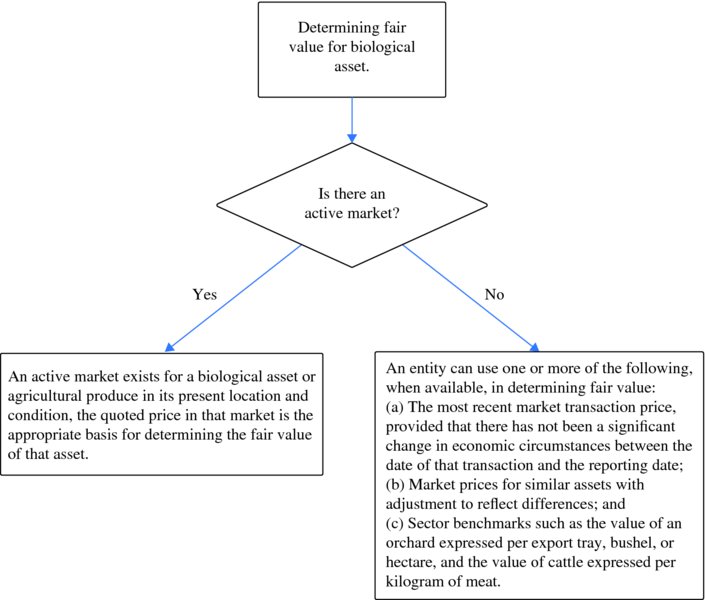

A biological asset shall be measured on initial recognition and at each reporting date at its fair value less costs to sell (see also footnote 1). Determining fair value is achieved by considering if there is, or is not, an active market. Figure 17.1 below illustrates the two options for determining fair value (see IPSAS 27.21 and 27.22).

Figure 17.1 Options for determining fair value under IPSAS 27

Agricultural produce harvested from an entity's biological assets shall be measured at its fair value less costs to sell at the point of harvest. That measurement is the cost at that date when applying IPSAS 12, or another applicable standard. Establishing the fair value for a biological asset or agricultural produce may be facilitated by grouping biological assets or agricultural produce according to significant attributes; for example, by age or quality. An entity selects the attributes corresponding to the attributes used in the market as a basis for pricing (IPSAS 27.18, 27.19).

A gain or loss arising on initial recognition of a biological asset or agricultural produce at fair value less costs to sell is included in surplus or deficit for the period in which it arises. A change in fair value of a biological asset is also recognized in surplus or deficit.

Since all biological assets are valued at fair value, all costs (other than costs to purchase the biological asset) related to these assets are expensed when incurred. Therefore the purchase price approximates fair value.

IPSAS 27 includes the following guidance on determining the fair value of a biological asset or agricultural produce (IPSAS 27.21–27.22, 27.24–27.27):

- The quoted market price in an active market is a reliable and preferred basis for determining the fair value of that asset. The fair value of a biological asset is based on the current market price and is not adjusted to reflect the existence of a contract that stipulates delivery at a future date.

- If an active market does not exist, a market-determined price such as the most recent market price for that type of asset, or market prices for similar or related assets, or sector benchmarks is to be used.

- If reliable market-determined prices are not available, the present value of expected net cash flows from the asset must be used, discounted at a current market-determined rate.

IPSAS 27.28 stipulates that the cost of the asset could be an indicator of its fair value, particularly when little biological transformation has taken place or the impact of biological transformation on price is not expected to be material.

IPSAS 27.34 presumes that fair value can be reliably measured for biological assets. However, this presumption can be rebutted when the biological asset does not have a market determined price and for which alternative methods of estimating fair value are clearly unreliable. In that case, the biological asset is measured at cost less accumulated depreciation and impairment losses. Afterwards, when the fair value becomes reliably measurable, the biological asset is to be measured at fair value less costs to sell.

Gains and Losses

On initial recognition of biological assets and agricultural produce, a gain may arise. One example could be when a calf is born, or as a result of harvesting. A loss may also arise on initial recognition, due to the fact that estimated point-of-sale costs are deducted in determining fair value less estimated point-of-sale costs of biological assets or agricultural produce. The gains and losses should be included in surplus or deficit in the period in which they arise.

Disclosure

IPSAS 27 requires the following disclosures:

- Aggregate gain or loss on biological assets and agricultural produce for changes in fair value;

- Description of each group of biological assets;

- The nature of the entity's activities involving each group of biological assets;

- Non-financial estimates of the physical quantities of each group of biological assets and the output of agricultural produce;

- Methods and assumptions in estimating fair value;

- Fair value of agricultural produce harvested during the period; and

- A reconciliation of changes in the carrying amount of the biological assets between the beginning and end of the period.

The entity should also disclose information on risks, commitments, and restrictions on biological assets which are important for the readers of the financial statements:

- Existence and carrying amount of biological assets whose title is restricted or that are pledged as security;

- Nature and extent of restrictions to use or sell biological assets;

- Commitments for development or acquisition of biological assets;

- Financial risk management strategies related to the agricultural activity.

When fair value cannot be measured reliably, the entity shall disclose the following:

- Description of the biological assets;

- The reason why fair value cannot measured reliably;

- If possible, a range of estimates within which fair value is highly likely to lie;

- Depreciation method used;

- Useful lives or depreciation rates applied;

- The gross carrying amount and the accumulated depreciation, at beginning and end of the reporting period.

In case biological assets are measured at cost less accumulated depreciation and impairment losses, the entity shall disclose:

- Gain or loss upon disposal of these assets;

- A reconciliation of the carrying amounts at the beginning and end of the period;

- Impairment losses, reversal of impairment losses, and depreciation included in surplus or deficit.

Moreover, in case the fair value of biological assets previously measured at cost becomes available, the entity is to disclose the following additional information:

- Description of the biological assets;

- Explanation of why fair value has become reliably measurable;

- Effect of the change.

All these disclosures are aimed at helping the readers of the financial statements to understand the value of biological assets, especially when they are not valued at fair value, which is the preferred treatment.

Below is an example of presentation of biological assets in the Biosev S.A. consolidated interim financial statements for the three-month period ended 30 June 2014, financial statements being prepared under IFRS.

Financial Reporting in Hyperinflationary Economies (IPSAS 10)

IPSAS 10 Financial Reporting in Hyperinflationary Economies prescribes the accounting treatment of financial statements of entities whose functional currency is the currency of a hyperinflationary economy to ensure that these financial statements are useful and meaningful to the readers of the financial statements. Therefore, the financial statements (including comparatives) should be restated to reflect the change in the purchasing power on the basis of a general price index. Hyperinflationary economies are those with very high rates of general inflation which have such a depreciating effect on the country's currency that it loses its purchasing power at a very fast rate. IPSAS 10 does not include any absolute rate or definition of hyperinflation. Professional judgment is needed to assess when restatement of financial statements is required.

IPSAS 10 includes characteristics of an economy, which are indicators that can assist in determining whether an economy is hyperinflationary. Figure 17.2 below outlines the key indicators.

Figure 17.2 Indicators that can assist in determining whether an economy is hyperinflationary under IPSAS 10

Hyperinflation causes particular problems for entities operating in such economies since money loses its purchasing power at such a high rate that comparisons are at best unhelpful, and potentially misleading. This includes the comparison of results between accounting periods and for similar transactions within the same accounting period.

Thus, where an entity has operations in a hyperinflationary economy it is likely that without the restatement required by IPSAS 10 Financial Reporting in Hyperinflationary Economies the reporting of operating results and the financial position in the local currency will become distorted over time.

Restatement of Financial Statements in Hyperinflationary Economies

The financial statements of an entity whose functional currency is the currency of a hyperinflationary economy are stated in terms of the measuring unit current at the end of the reporting period. Corresponding figures in relation to prior periods are also restated. The gain or loss on the net monetary position is included in surplus or deficit and separately disclosed.

It should be noted that the application of the restatement principles included in IPSAS 10 requires professional judgment. The objective is not to be accurate but rather to provide relevant information that can be compared over time (Schumesh et al., 2012).

Restated financial statements of an entity whose functional currency is the currency of a hyperinflationary economy are as follows:

Table 17.2 Restated financial statements and a functional currency in a hyperinflationary economy

| Statement of financial position | Statement of financial performance | Statement of cash flows |

Restatements are made by applying a general price index:

|

Restatements are made by application of the change of a general price index to all revenues and expenses since the date they were actually recorded. | All items in the statements of cash flow are expressed in terms of the measuring unit current at the end of the reporting period. Corresponding figures for the previous reporting period are restated by applying a general price index. |

Gain or Loss on the Net Monetary Position

The gain or loss on the net monetary position should be included and disclosed separately in the statement of financial performance. This gain or loss is an indicator of the purchasing power gain or loss as a consequence of the inflation and may be derived by different methods.

Consolidation

Controlling entities, reporting in the currency of a hyperinflationary economy themselves, when consolidating an entity in a hyperinflationary economy should restate the financial statements of this entity in the measuring unit current at the reporting date before consolidation.

Economies Ceasing to be Hyperinflationary

When an economy ceases to be hyperinflationary, the entity shall discontinue the preparation and presentation of financial statements prepared in accordance with IPSAS 10. It shall treat the amounts expressed in the measuring unit current at the end of the previous reporting period as the basis for the carrying amounts in its subsequent financial statements.

Disclosure

IPSAS 10 requires disclosure of the following:

- The fact that the financial statements and prior comparative figures are restated for changes in the general purchasing power of the functional currency, in terms of the measuring unit current at the reporting date;

- The identity and level of the price index at the reporting date and the movement in the index during the current and the previous reporting periods.

Moreover, the surplus or deficit on the net monetary position should be disclosed on the face of the statement of financial performance to inform the reader of the impact of hyperinflation on the value of the financial statements.

Conclusion

IPSAS 27 and IPSAS 10 are two very specific standards, the first because of the nature of the activities covered by IPSAS 27 Agriculture, the second because hyperinflationary economies are fortunately not so common, at least among entities applying accrual basis of accounting IPSAS.