Chapter 6

Inherent Risk: Credit and Market Risks

1. INTRODUCTION

Islamic finance has grown significantly since its rise to prominence in the last decade, with a growing number of countries adopting Islamic finance as the emblem of their financial services sector. The prominence received a further boost with the global financial crisis, when doubts were cast on the role of the conventional financial system in financial intermediation insofar as it was evident that the conventional financial system increasingly was decoupled from the “real” economy.

Nonetheless, while the interest in Islamic finance has grown, the management of the risks inherent in the operation of Islamic financial institutions (IFIs), particularly relating to specificities of Shari’ah-compliant products and services, is still relatively new and developing. Although some progress has been made through the establishment of Islamic finance risk and governance frameworks, advances in the area of risk management for Islamic finance have not kept pace relative to the growth of the industry.

The chapter explores the risk specificities of Shari’ah-compliant products and services, particularly the credit and market risks of these products and services.

2. DISTINCTIVE RISKS

IFIs are faced with risks that are distinct from those of their conventional counterparts. The tenets of Islamic finance are based on the conformity to Shari’ah law, which is the juristic code of Islam based on the Qur’an and the hadith, and forbids certain practices that are common in conventional finance. It is this distinction that gives rise to the contrasting risk profiles between conventional and Islamic finance products and services.

IFIs are bound by:

- The prohibition of speculation (maysir) and of the receipt and payment of interest (riba).

- The need to avoid uncertainty (gharar) or highly uncertain financial transactions.

- The prohibition of the financing activities that are themselves prohibited (haram).

- The principles of promotion of fairness in transactions and the prevention of exploitative relationships.

- The requirement to honour contracts.

- The principle of sharing risks and rewards between the principals in a transaction.

- The requirement that transactions should carry elements of materiality, which lead to tangible economic purpose.

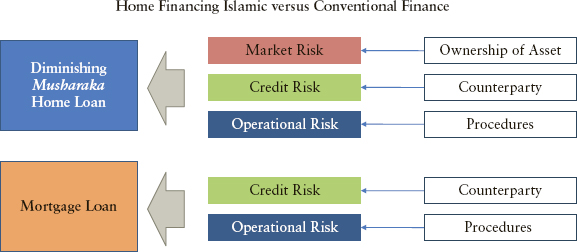

As a result, Shari’ah compliant products and services have distinct and different risks from conventional finance products and services. An example of the differences between the financial risks arising from an IFI’s products as compared to conventional finance can be seen when considering the concept of risk sharing. In the case of a financial product such as home purchase financing plans structured on the basis of the diminishing musharakah concept (a type of partnership), the IFI takes joint ownership of the asset, and is faced with market risks should the counterparty default and the price of the asset fall below market value, which is not the case for conventional mortgages. This is illustrated in Exhibit 6.1.

EXHIBIT 6.1 Unique Islamic Risk

To understand the unique nature of the risks of Shari’ah-compliant products and services, it is important to understand the structure of these products and services. The different structures used could lead to distinct and different risk profiles.

3. INHERENT RISKS IN SHARI’AH-COMPLIANT PRODUCTS AND SERVICES

Shari’ah-compliant products and service involve inherent risks, including credit, market, and displaced commercial risk, as described next.

3.1 Credit Risk

The risk of counterparties not fulfilling predetermined obligations is not so dissimilar for IFIs compared to conventional financial institutions. An IFI deals with counterparties who at the onset agree to meet the stipulated terms of repayment. However, there is the potential that these counterparties may not meet these terms.

Credit risk exposures for IFIs result from, but are not limited to:

- Accounts receivable in murabahah contracts.

- Accounts receivable and counterparty risk in istisna’a contracts.

- Counterparty risk in salam contracts.

- Equity investment risk in musharaka contracts.

- Lease payments receivable in ijarah contracts.

3.2 Market Risks

Market risk is the risk of losses in on- and off-balance sheet positions arising from market prices. Conventional financial institutions are exposed to these risks from the positions they hold in financial instruments. These positions are held, amongst other objectives, intentionally to secure a short-term profit from price or interest-rate variations, or to hedge against other elements of the trading book.

However, due to the unique nature of the IFIs’ way of doing business, speculative transactions and contracts connected to the incidence or non-incidence of future events are prohibited. This includes conventional derivatives and some other hedging transactions. While IFIs are therefore not exposed to speculative market risks, this does not limit their exposure to other market risks, some of which are unique to the IFIs due to the manner in which contracts are required to comply with Shari’ah principles concerning the materiality of transactions and the sharing of risk and rewards. As a result, IFIs carry out multiple asset-based transactions in which they take ownership of physical assets in the course of a financing transaction (such as a credit sale or a lease-to-buy purchase), which exposes them to market risk associated with the price of these assets.

3.3 Displaced Commercial Risk

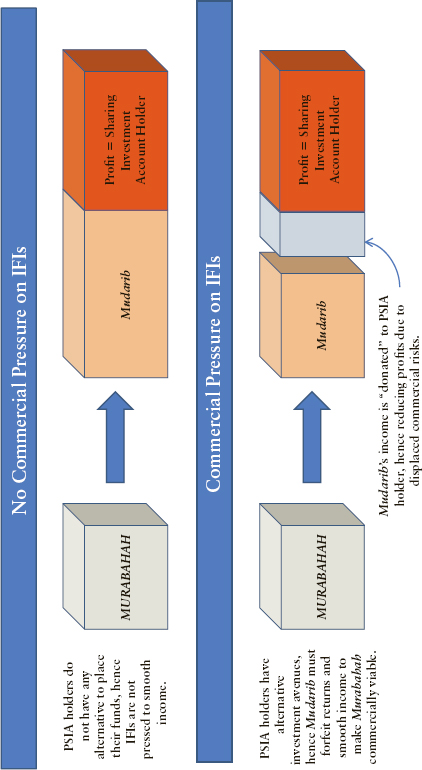

The notion of displaced commercial risk is peculiar to IFIs, and arises mainly from fluctuations in the rate of return required by profit-sharing investment account (PSIA) holders. Fluctuations in the rate of return oblige IFIs to increase the rate given to their PSIA holders in order to retain their funds in the institution. Thus, an IFI may have to give up a portion of its share of profits as mudarib (i.e., manager), normally allocated to the IFI’s shareholders. This is illustrated in Exhibit 6.2.

EXHIBIT 6.2 Displaced Commercial Risk

Displaced commercial risk arises through rate of return risks; when PSIA funds are placed in assets such as murabahah with long-term maturities, the rates of return on which are no longer competitive with alternative investments. Although in theory IFIs are not obliged to provide smoothing of income to the PSIA holders (due to the nature of risk sharing), supervisory authorities and commercial pressures may in fact oblige them to do so.

Because the nature of Islamic finance is governed by the rules and principles of the Shari’ah, the following premises add a unique dimension to risk management in an IFI’s operations:

- The role of IFIs in mudarabah and musharakah financing, whereby the IFI takes on the risk of not receiving payment from the other party or finding itself potentially liable for taking delivery of an asset.

- The commencement of credit risks that underlie various financing modes vary according to the recognition of the binding or nonbinding nature of some contracts (e.g., murabahah) or the transformation of a customer’s mudarabah or musharakah investment into a debt in case of proven negligence or misconduct of the IFI as mudarib or musharakah managing partner.

- The prohibition of penalties to be imposed in certain contracts, except in the case of deliberate procrastination, which reduces the IFI’s ability to use guarantees as risk mitigants to protect it against capital impairment.

- In addition, the restrictions on the use of conventional derivatives and the limited availability of Shari’ah-compliant derivatives, which limit the IFI’s ability to manage its balance sheet and liquidity as thoroughly and effectively as conventional banks do.

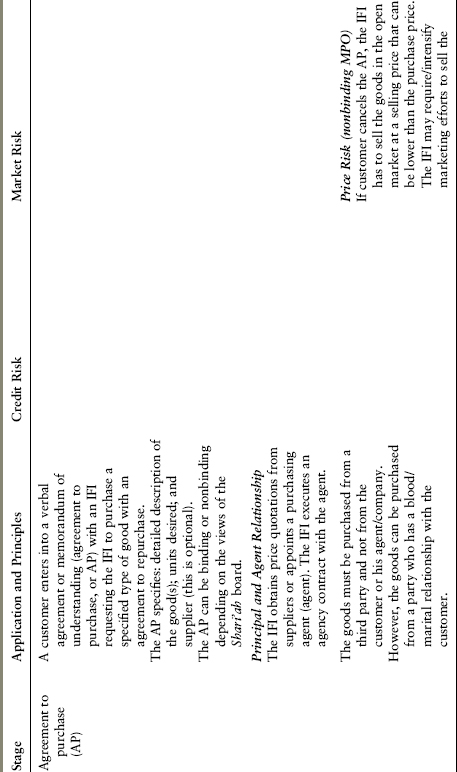

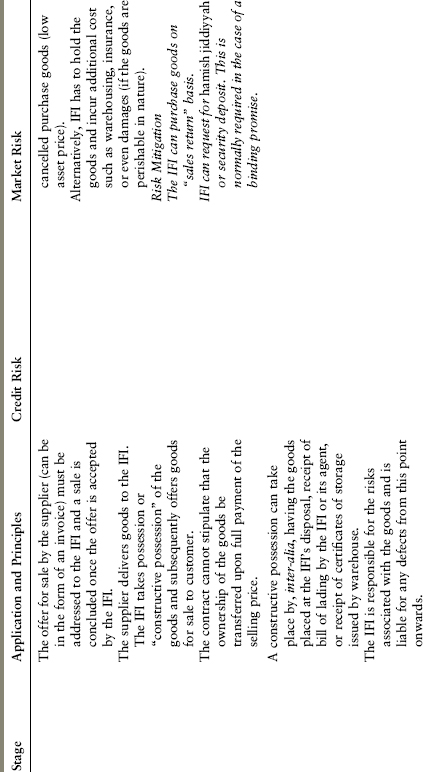

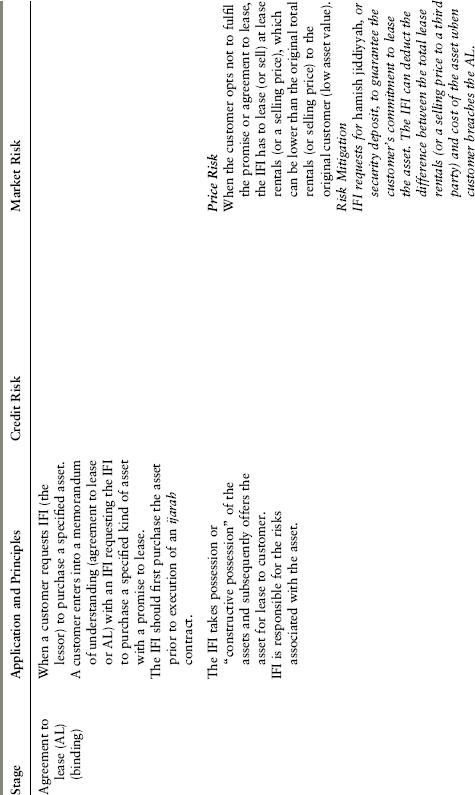

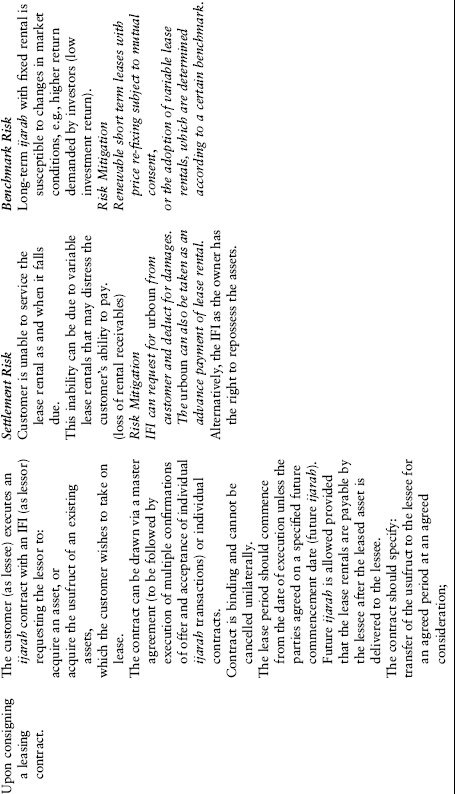

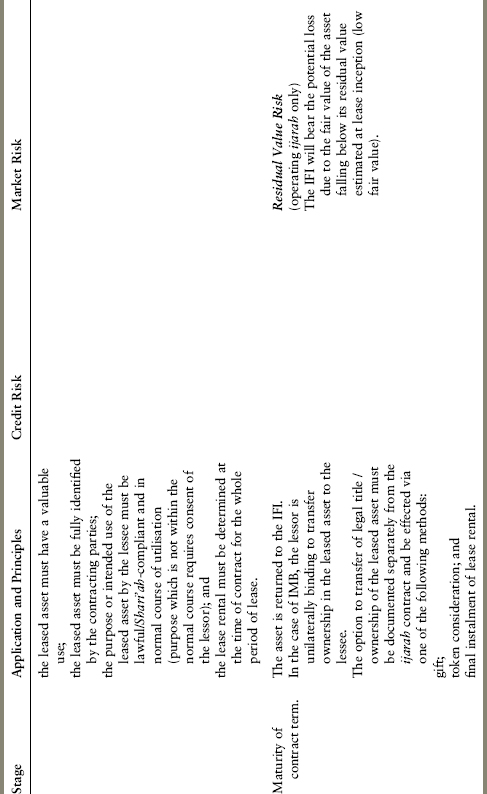

Since IFIs employ a number of structures, the review of inherent risk in IFIs requires the risk assessment process be structured in a matrix format. For each structure, the initial step would be to review each stage on one side and exposure to credit and market risks on the other side. The high-level overview of inherent credit and market risk exposures in a number of Shari’ah-compliant products and services are provided in the Appendix. Note that the IFIs are also exposed to other risks, such as operational and liquidity risks, this article considers only credit and market risks.

4. CONCLUSION

Risks are inherent in the operations of both Islamic and conventional financial institutions. Although the risk exposures of a conventional financial institution are somewhat different from those of an IFI, the main principles of risk management still apply.

However, Islamic risk management sophistication has to be product driven. Even though as a matter of economic substance Shari’ah-compliant products and services may closely resemble their conventional counterparts, they may nevertheless have distinct and different risk profiles.

The tenet of Islamic finance that encourages the sharing of risk and reward between the principals in a transaction has yet to be fully realised. This aspect of Islamic finance seems most promising as a clear differentiator of Islamic finance from conventional finance.

APPENDIX

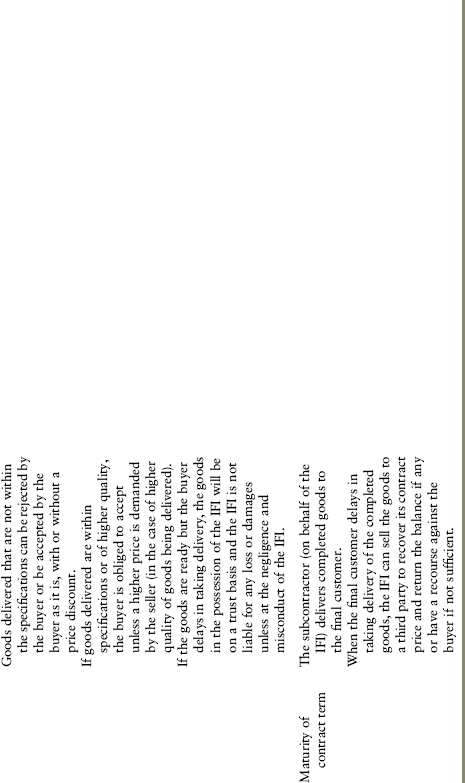

Exhibits A.1 to A.6 show a high-level overview list of inherent credit and market risks associated with different Shari’ah-compliant products and services.

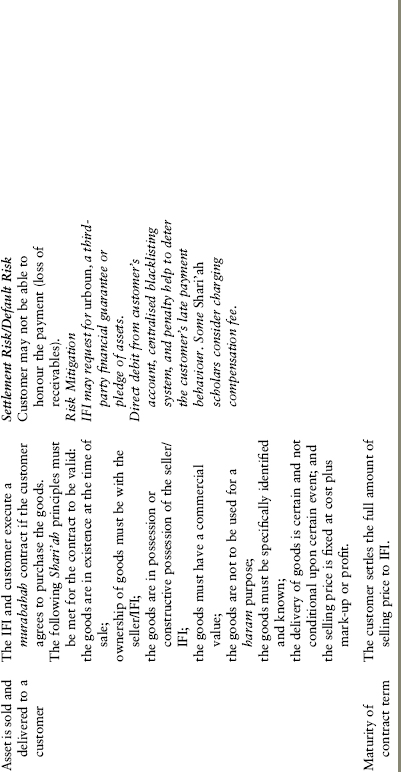

EXHIBIT A.1 Murabahah for the Purchase Orderer (MPO)

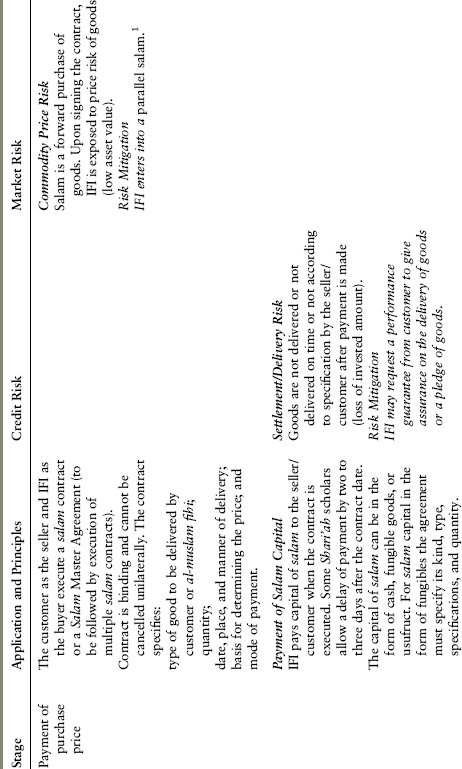

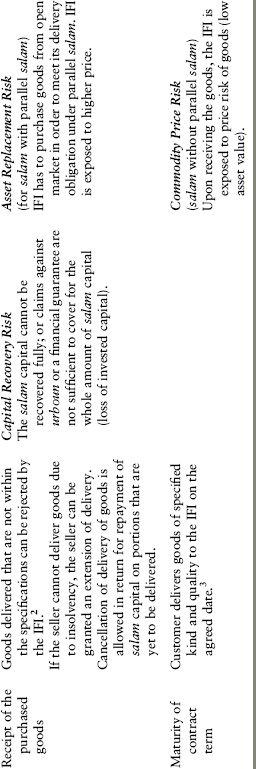

EXHIBIT A.2 Salam (and Parallel Salam)123

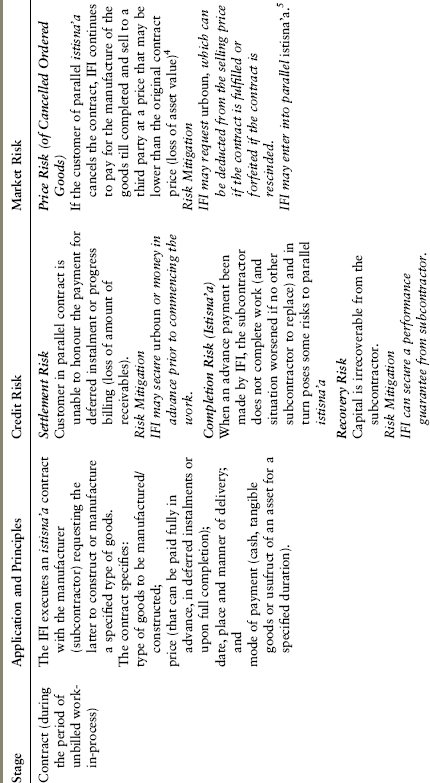

EXHIBIT A.3 Istisna’a and Parallel Istisna’a45

EXHIBIT A.4 Operating Ijarah and Ijarah Muntahia Bittamleek (IMB)

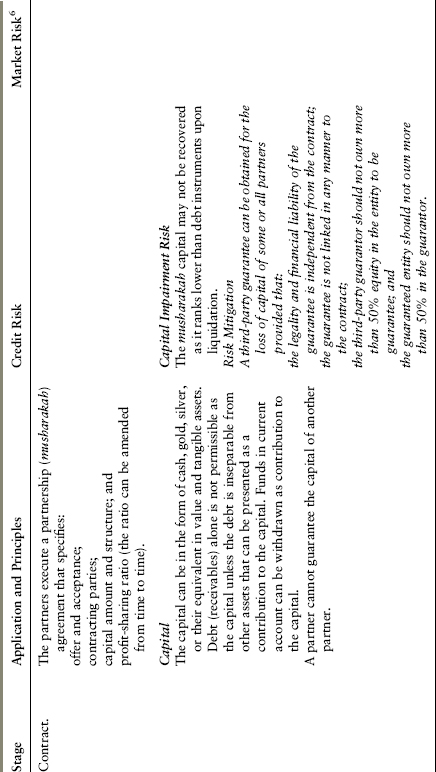

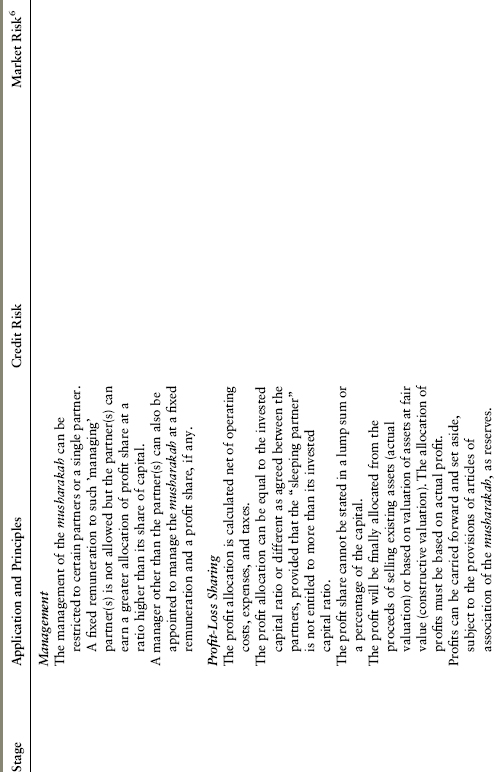

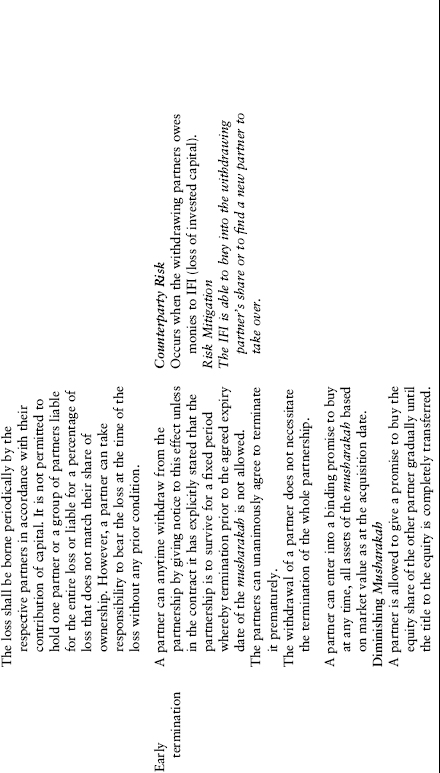

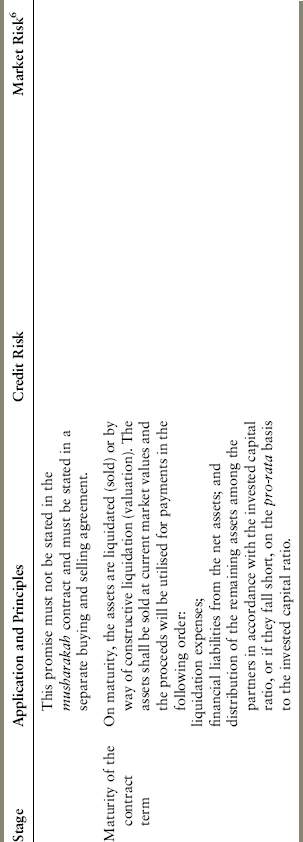

EXHIBIT A.5 Musharakah6

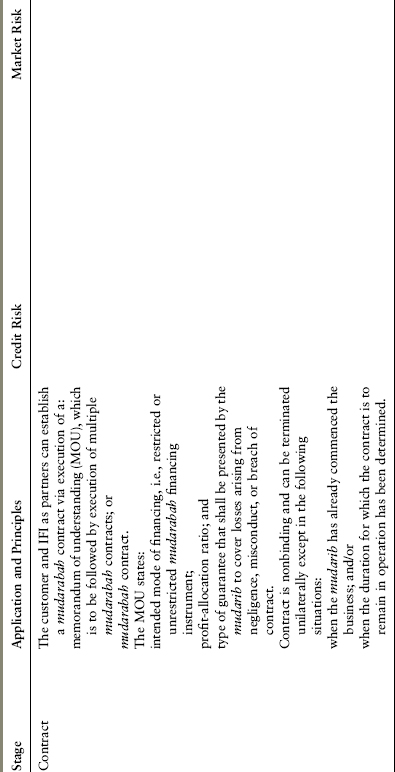

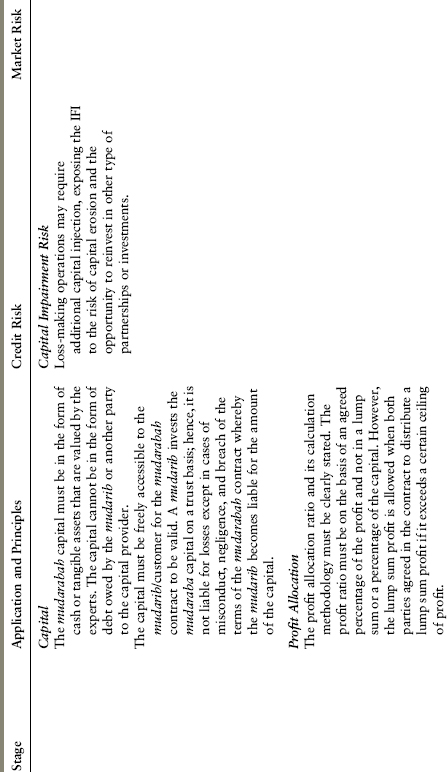

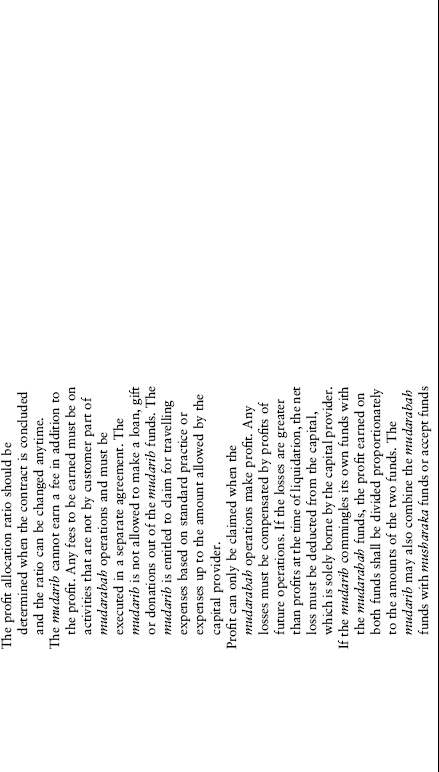

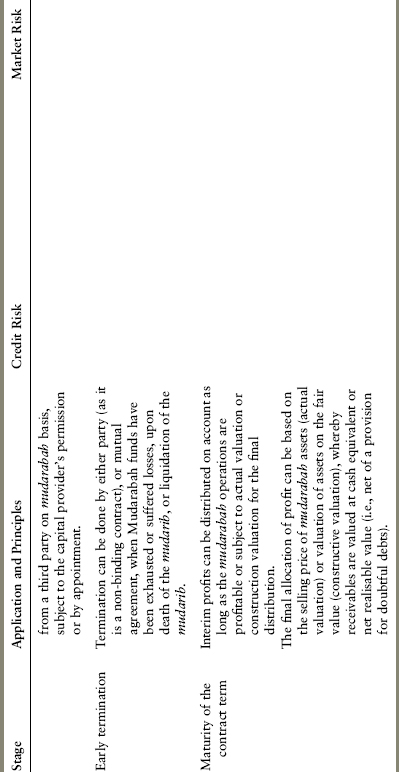

EXHIBIT A.6 Mudarabah

NOTES

1. IFI can sell goods to a party other than the salam customer (or a company, which is owned less than a third by the salam customer). The parallel salam contract must be independent of Salam contract. An IFI’s obligation to deliver goods under parallel salam is not inter-conditional on the performance obligations under direct salam contract.

2. If goods delivered are within specifications or of higher quality, the IFI is obligated to accept unless the seller (in the case of higher quality of goods being delivered) demands a higher price.

3. The IFI may decide not to sell the goods immediately upon receipt; hence, the goods will be exposed to selling-price fluctuations.

4. Cancellation of contract is allowed as long as the IFI has not commenced work and, hence, the IFI is not exposed to price risk.

5. The IFI may enter into a parallel istisna’a contract with a final customer (off-taker) to take delivery of the goods ordered (alternatively, the IFI may enter into an istisna’a with a view to taking possession of the asset on completion). The IFI may be required to give a guarantee to the subcontractor. The parallel istisna’a contract must be independent of the istisna’a contract. IFI assumes the liability of ownership risk plus maintenance and insurance expenses.

6. The types of underlying assets of musharakah may give rise to market risk.