Introduction: Trading and Market Micro-structure

An on-going increase of computer-driven trading

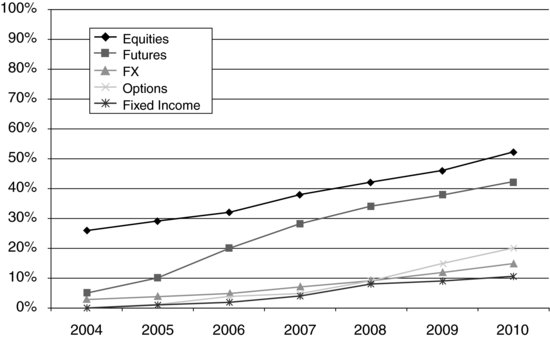

The last few years have seen dramatic changes in trading practices: the use of computers to buy and sell financial products went from zero to 25 % (depending on the asset class) in 2004 to 10 to 60 % in 2010 (see Figure 1 and Hendershott et al., 2011).

To be more accurate: “algorithmic trading” encompasses only the orders that are explicitly sent by an investor (pension fund, hedge fund, investment bank, etc.) to a server hosting trading algorithms. Three other activities should be added to these figures: “program trading” (orders that are sent as portfolios to servers), “high frequency market making” (proprietary traders providing electronic quotes in publicly available order books), and orders sent to human intermediaries who are themselves using trading algorithms to access the order books. Adding all those numbers together, at least 70 % of the trades on equity markets in the US (50 % in Europe, 35 % in Japan) are said to have a computer-operated counterpart.

Figure 1 Evolution of the use of algorithmic trading from 2004 to 2010 on US markets.

Source: Aite Group.

The main factors of these on-going changes are:

- A preference by policy-makers and regulators for transactions on electronic market transactions rather than over-the-counter ones. The main reason is that they have the feeling that the monitoring and controlling of systemic risk is easier when supported by large data centers storing the history of positions of all market participants.

- The decline of margins and increase of competition in the trading industry encouraging more automated approaches to guarantee reliable performances.

- A broader access to fast hardware solutions allowing data capture, storage and processing that were previously only used by the defense and aerospace industries (mainly for artificial vision; see Granado and Garda, 1997).

Besides, the financial crisis put the emphasis on liquidity issues and short-term proprietary trading strategies (to reduce inventory exposure to market risk).

The competition between market operators increased during the same period: the mergers of NYSE with Euronext, the one of the London Stock Exchange and Turquoise, or between Chi-X and BATS Europe are side effects of this competition. In Asia the convergence operates at a slower rate; the alignment of trading hours and some mergers are nevertheless ongoing.

Early academic answers and old practices

The academic literature slowly addressed this change of trading practices. While market micro-structure has been addressed long ago by economists (see Ho and Stoll, 1981; Mendelson, 1982; Garman, 1976; Glosten and Milgrom, 1985; Kyle, 1985), theoretical frameworks to optimize the point of view of a trader trying to optimize his trading process have been proposed only recently (mainly from the viewpoint of “optimal trade scheduling”; see Almgren and Chriss, 2000; Bertsimas and Lo, 1998). On their side, econophysicists studied empirically the market impact of trades on any scales (Bouchaud et al., 2002; Lillo et al., 2003). More recently statistical and econometric studies focused on the cost of trading (Dufour and Engle, 2000). Last but not least, probabilists developed an interest for rounded diffusion processes that could be considered as a model of the diffusion of the price on a discretized price grid (Jacod, 1996).

From the practitioner's viewpoint, the topics of interest at the end of the 1990s were mainly:

- To understand the “slippage” of the trading process, with respect to explanatory variables mixing the market context (volatility, momentum, traded volume, etc.) and the liquidity of the traded instrument (bid-ask spread, average trade size, imbalance, etc.).

- To control the risk of a large buy or sell order using “trading curves” to avoid trading too fast (to avoid market impact and adverse selection) or too slow (to minimize the exposure to market risk).

Two regulation changes, Reg NMS in the US (2005) and MiFID in Europe (2007), promoted the fragmentation of markets. The financial crisis reduced the margin of almost all market participants and increased the intraday and extra day volatility, putting more emphasis on the trading costs and intraday risk control. The complexity of buying or selling a large amount of lots increased because of two major effects:

- The liquidity was now spread over four to seven trading destinations, demanding to split each already small order before sending it to the trading venues.

- The latency became an issue: first to capture instantaneous crossing of the best bid and ask on two different venues, then to be aware of the availability of liquidity on a trading venue before other participants.

New practical needs and academic recent advances

Optimal trading or quantitative trading is now an area of quantitative finance, combining and refining results enhancing the understanding of the price formation process, such as:

- Statistical methods to use high frequency data emerged, aiming to decompose the price moves between randomness and micro-structural effects (Zhang et al., 2005; Hayashi and Yoshida, 2005; Robert and Rosenbaum, 2010; Bacry et al., 2011).

- Market impact has been studied more intensively with respect to its interactions with a trading process (Gatheral, 2010).

- The effect of market design choices and the nature of market participants on the efficiency of the price formation process have been tested empirically and theoretically (Foucault et al., 2005; Menkveld, 2011).

These results provide the tools to put in place more sophisticated trading techniques as follows:

- The mean-variance framework that gave birth to the first optimal trading curves can now be replaced by stochastic control approaches (Bouchard et al., 2011), and the high frequency market-making problem has also been formalized (Guéant et al., 2011).

- Forward optimizing methods, inspired by statistical learning, have been proposed to take into account very short time scale statistical properties of the order flow (Pagès et al., 2009; Laruelle et al., 2011).

This field is now expanding fast, offering practitioners a wide toolbox to choose from . All aspects of optimal trading have nevertheless not yet been investigated, especially:

- Performance analysis: once a trading algorithm is implemented, its efficiency and its performance are periodically reviewed: first from the point of view of a trader confronting variations of the same algorithm to different market conditions and then from the point of view of a large investor using different (unknown) algorithms hosted by different execution providers to buy or sell instruments according to different investment motivations (alpha extraction, hedging, risk reduction, etc.).

- Stress testing: before putting a trading algorithm on real markets, there is a need to understand its exposure to different market conditions, from volatility or momentum to bid-ask spread or trading frequency. The study of “Greeks” of the payoff of a trading algorithm is not straightforward since it is inside a closed loop of liquidity: its “psi” should be its derivative with respect to the bid-ask spread, its “phi” with respect to the trading frequency, and its “lambda” with respect to the liquidity available in the order book.

Let us hope that events such as this International Conference help in mixing mathematical, economic, and physicist cultures to continue to bring better answers to the needs of practitioners and regulators.

REFERENCES

Almgren, R.F. and N. Chriss (2000) Optimal Execution of Portfolio Transactions, Journal of Risk 3(2), 5–39.

Bacry, E., S. Delattre, M. Hoffmann and J.F. Muzy (2011) Modeling microstructure noise with mutually exciting point processes.

Bertsimas, D. and A.W. Lo (1998) Optimal Control of Execution Costs, Journal of Financial Markets 1(1), 1–50.

Bouchard, B., N.-M. Dang and C.-A. Lehalle (2011) Optimal Control of Trading Algorithms: A General Impulse Control Approach, SIAM Journal of Financial Mathematics.

Bouchaud, J.-P., M. Mezard and M. Potters (2002) Statistical Properties of Stock Order Books: Empirical Results and Models, Quantitative Finance 2, 251–256.

Dufour, A. and R.F. Engle (2000) Time and the Price Impact of a Trade, Journal of Finance 55(6), 2467–2498.

Foucault, T., O. Kadan and E. Kandel (2005) Limit Order Book as a Market for Liquidity, Review of Financial Studies 18(4), 1171–-1217.

Garman, M.B. (1976) Market Microstructure, Journal of Financial Economics 3(3), 257–275.

Gatheral, J. (2010) No-Dynamic-Arbitrage and Market Impact, Quantitative Finance 10(7), 749–759.

Glosten, L.R. and P.R. Milgrom (1985) Bid, Ask and Transaction Prices in a Specialist Market with Heterogeneously Informed Traders, Journal of Financial Economics 14(1), 71–100.

Granado, B. and P. Garda (1997) Evaluation of the CNAPS Neuro-computer for the Simulation of MLPS with Receptive Fields, in Biological and Artificial Computation: From Neuroscience to Technology, J. Mira, R. Moreno-Diíz and K. Cabestany, (Eds), Vol. 1240 of Lecture Notes in Computer Science, Chapter 84, Springer, Berlin/Heidelberg, pp. 817–824.

Guéant, O., C.-A. Lehalle and J. Fernandez-Tapia (2011) Dealing with the Inventory Risk, forthcoming in SIAM Journal on Financial Mathematics.

Hayashi, T. and N. Yoshida (2005) On Covariance Estimation of Non-synchronously Observed Diffusion Processes, Bernoulli 11(2), 359–379.

Hendershott, T.J., C.M. Jones and A.J. Menkveld (2011) Does Algorithmic Trading Improve Liquidity? Journal of Finance 66(1), 1–33.

Ho, T. and H.R. Stoll (1981) Optimal Dealer Pricing Under Transactions and Return Uncertainty, Journal of Financial Economics 9(1), 47–73.

Jacod, J. (1996) La Variation Quadratique Moyenne du Brownien en Présence d’Erreurs d’Arrondi. In Hommage a P.A. Meyer et J. Neveu, Vol. 236. Asterisque.

Kyle, A.P. (1985), Continuous Auctions and Insider Trading, Econometrica 53(6), 1315–1335.

Laruelle, S., C.-A. Lehalle and G. Pagès (2011) Optimal Posting Distance of Limit Orders: A Stochastic Algorithm Approach.

Lillo, F., J.D. Farmer and R.N. Mantegna (2003) Econophysics – Master Curve for Price – Impact Function, Nature 421(6919), 129.

Mendelson, H. (1982) Market Behavior in a Clearing House, Econometrica 50(6), 1505–1524.

Menkveld, A.J. (2011) High Frequency Trading and the New-Market Makers, Working Paper.

Pagès, G., S. Laruelle and C.-A. Lehalle (2009) Optimal split of orders across liquidity pools: a stochatic algorithm approach, forthcoming in SIAM Journal of Financial Mathematics.

Robert, C.Y. and M. Rosenbaum (2010) On the Microstructural Hedging Error, SIAM Journal on Financial Mathematics 1, 427–453.

Zhang, L., P.A. Mykland and Y.A. Sahalia (2005) A Tale of Two Time Scales: Determining Integrated Volatility with Noisy High-Frequency Data, Journal of the American Statistical Association, 100(472).