Crafting the Investor Marketing Strategy

Investor relations (IR) is not an administrative activity, but a highly flexible discipline that needs to be guided with a clear strategy. The IR strategy model shown in Figure 8.1 presents the four strategic choices that the IR function faces. IR strategy is the combination of these four decisions:

1. Disclosure level

2. Degree of targeting

3. Selection of disclosure channels and

4. Level of resource

Figure 8.1 The IR strategy model

Disclosure Level

Disclosure level refers to the amount of information that is disclosed above and beyond the legally required information. Investors are asking IR officers for ever more information. Ninety-one percent of corporations worldwide provide extra information to investors. Effective disclosure remains the raison d’être of the IR function.

Degree of Targeting

Targeting is the essence of modern marketing. No product can satisfy the entire market, because customers have different desires, preferences, incomes, intellects, and lifestyles. Nor can the corporation afford to individually customize products for any but the most significant customers. The answer for most products lies in between these two extremes of perfect homogeneity and perfect heterogeneity, with segmentation and targeting. Segmentation is the process of dividing the market into groups, each group being united by similarity according to at least one significant variable. The firm then chooses one or more of these segments and develops a specialized marketing mix for each segment. In IR, targeting means deciding which investors fit best with the stock; which investors are most likely to buy the stock and then exhibit positive behaviour, such as holding the stock for a long period, and being generally supportive of corporate strategy.

In markets for long term financial products, the “quality” of customers is often important, since a purchase begins a long-term relationship between seller and buyer. The seller is looking for the right kind of buyer, not just any interested buyer.

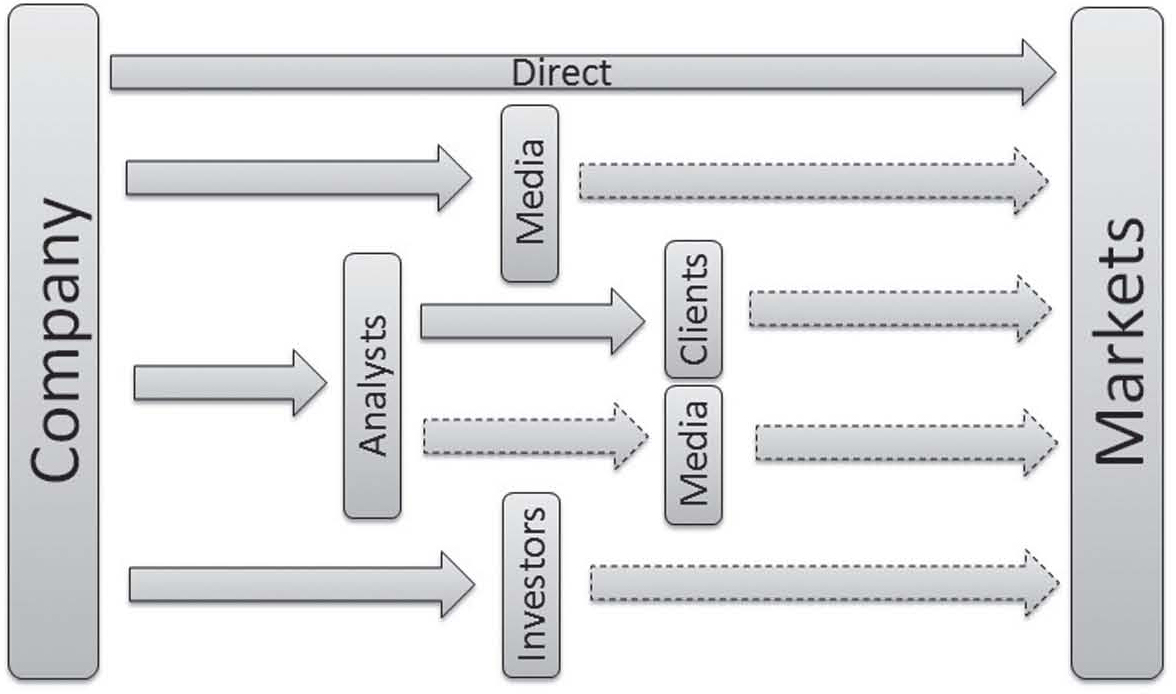

Channel Selection

There are four principal channels for corporate information as shown in Figure 8.2: analysts, the media, direct contact with investors, and public disclosure. The mix of channels used will depend on the complexity of the information, the credibility of each channel, the ability of the channel to transmit the information in a clear and secure way; and the reach (i.e., audience) of each channel. Increasingly, companies are communicating directly with investors and disintermediating analysts and journalists. The dotted arrows represent communication that is not controlled by the firm. The firm only retains complete control with direct communication, all other forms of communication involve uncertainty about whether messages will be delivered in the desired form.

Figure 8.2 Channels of disclosure

Level of Resource

IR resource commitment is a sign of the influence that investors have in the corporation. Resources consist chiefly of not the IR personnel, but the time given to the IR function by the chief executive officer (CEO) and chief financial officer. The Chairman and Senior Independent Director (SID) may also have significant roles, but customarily these officers only get involved if the investors are unhappy with the performance of the CEO.