The Two-Stage Model of Investor Marketing

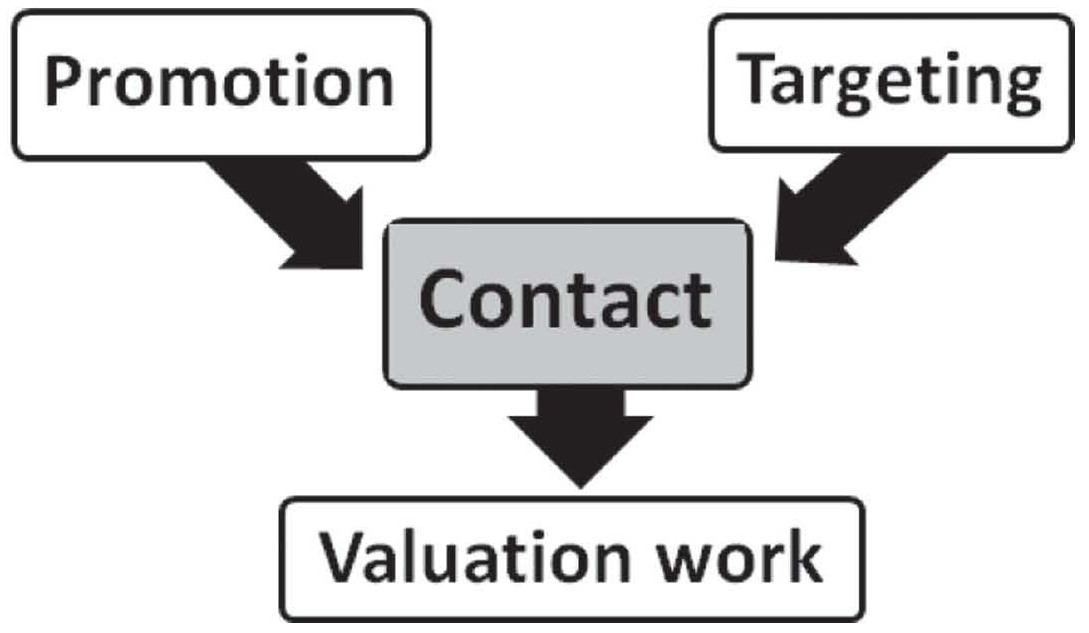

The two-stage model of marketing shown in Figure 9.1 utilizes two complimentary methods of stage one marketing: (1) targeting of investors and (2) corporate promotion. These two methods are designed to generate plenty of enquiries and opportunities for stage two marketing. Stage two then works with the investors to guide them through the valuation process which enables them to invest.

Both targeting and promotion rely on the firm having an agreed, consistent, and compelling story and brand identity and careful micro-segmentation (see Chapter 4 of Coe, 2004 for more information on micro-segmentation). Segmentation is essential for the effective use of targeting and also for networking and conference work, as the large number of investment-related conferences means that careful selection is essential.

Figure 9.1 The two-stage model of investor marketing

Where does a company get its ideas about which investors it should target? The corporate network of brokers and analysts will provide ideas, although there are problems with their recommendations, since both often get paid for arranging these meetings.

What does a good investor look like? A formula for a good investor may look something like this:

IS = EL × EI × ESR

In this example, the overall investor score (IS) is a multiple of three factors: the expected longevity of the investment (EL), the expected size of the investment (EI), and the expected service ratio (ESR) which is the ratio between the cost of servicing an investor (such as time spent meeting the investor) and the benefits received from that investor (such as useful strategic feedback). Once the investor relations officer (IRO) has formed a clear idea of what constitutes good investor behavior, then he can begin a search for those characteristics.

Search methods include (a) good media monitoring. Following up any comments about your firm or industry, if they are critical, then you may be able to correct any misunderstandings, and if they are positive, then this might be a good time to schedule a presentation to that investor or analyst to convert a positive comment into a sale, and (b) regularly analyzing your share register to benchmark the profile of your shareholder register against that of your peers. From this analysis consider which segments of the investor community you should target. Then identify the investors who are most likely to want a long-term relationship, and then identify the decision makers within each of the investors. The direct approach then requires making personal contact by phone or e-mail with a target investor and offering to meet to present the corporate case personally.

Promotion—the Four Ways of Getting Noticed

As well as seeking out specific investors, the firm should raise its general profile so that investors notice it and approach it. Good marketing requires a deep understanding of product characteristics, consumer needs, and how the product characteristics satisfy the consumer’s needs. In a stock universe of tens of thousands of stocks, getting noticed and onto the radar of investors is the first essential step in getting a full valuation. The four ways of getting noticed by investors are shown in Figure 9.2.

Figure 9.2 Four methods of getting investor attention

The four methods for appearing on investors’ radar are (1) using conferences and other events to present the company’s case and meet investors directly, (2) obtaining a favorable media profile and getting noticed through positive news stories in those media channels respected by investors, (3) getting recommendations from financial analysts, and (4) getting through investors quantitative screens by performing well in one or more of the financial metrics that investors use to reduce the stock universe into a “long list” of stocks that are worth further analysis (for instance yield or P/E).

These four methods are all stage one marketing. Stage two marketing involves personally walking an analyst or investor through the valuation process. During the process of assisting an analyst or investor with their valuation model, it may be necessary to provide information that is not already in the public domain. This is a sensitive process that should be managed by the IRO to avoid the selective disclosure of material information. Raising disclosure levels is an important part of a stock promotion strategy, but needs to be handled with care as the markets generally expect extra disclosure to be maintained in perpetuity.

As well as a marketing role, the IRO has a specific sales role. Sales has been defined as: “an interpersonal confrontation where at least one party has the aim of influencing an exchange” (Buttle, 1986).

There are several personal encounters between company management and investors:

• The results briefing

• The one-on-one investor meeting

• The one-on-one analyst meeting

• The small group meeting (usually analysts but could be smaller investors also)

Each of these meetings has a different personality depending on a number of factors including the following:

• The number of people involved

• What stage in the buying process the participants are at

• How positive the participants are about the stock

• The corporate performance context

• The macroeconomic context

The face-to-face meeting is still an important event in the investment process, despite the role of technology. Although many index investors will not request meetings, for other investors the meeting is an important stage in the investment decision. In addition to the information that may be communicated in the meeting, the meeting has a symbolic function; it is an indication to the investors that management regards them as important, and analysts value the meetings for the credibility that personal meetings give them with their own clients. For management, meetings represent opportunities to:

• Demonstrate their knowledge of the firm and its market

• Establish rapport with investors

• Understand the financial community better

• Impress investors with intellectual ability and personality

• Correct misperceptions

Although meetings are effectively interviews or trials, with one side requesting information and the other side providing it, at their best they are exercises in mutual understanding where management also gains information:

• What does the market think about our company?

• What does the market think of our current strategy?

• Who is the most positive and most skeptical of our analysts?

• What are the big obstacles to investment?

• How do they compare us with our competitors?

• What risks does the market associate with our company?

• How is the economy likely to develop in the future?

• What social trends and other macro factors will shape the market in the next few years?

• What investment philosophies guide our main investors?

Managements may find that certain investors, who combine industry knowledge with openness, may provide a useful sounding board on proposed projects, policy changes, and other corporate initiatives. Testing ideas in private with a few investors is a way of de-risking corporate decision-making, although the company must take care to avoid disclosing material information.

Meetings should always be documented. Formal results meetings must now be audio recorded (or video recorded depending on management/ investor preference) and posted online so that all investors have the chance to listen to management, and so new investors can see the past few meetings. For the smaller events, we suggest that the IRO documents the questions asked and the answers given. At least two corporate officers should always be present when meeting with investors, analysts, or journalists. In some circumstances, the IRO may meet with small investors alone, although this is less than ideal, but even then some notes must be taken. The notes of questions asked serve as a very valuable log of investor/analyst interest and attitude. Clearly, it is very useful when preparing for meetings with an investor or analyst to have a record of the questions they asked last time the company met with them. The notes also have value for psychological purposes (the mere fact that notes are taken will help prevent company officers disclosing material information) and for compliance purposes (to act as a defense if the company is accused of selective disclosure).

Meetings tend to follow a three-step pattern with a descending degree of formality:

1. The pitch

2. The Q&A

3. The mingle

Viewed as a sales call, the investor/analyst meeting is somewhat different from normal business-to-business selling:

• The investor will not make a decision to buy during the encounter.

• The investor’s decision may never be known.

• The company management is not authorized to give investment advice; they cannot recommend that the investor buy their stock.

• The company is not actually selling anything; the investor will buy from an existing owner of stock. That is, the company is effectively promoting the second-hand market in its own stock.

• The audience uses the meeting to gauge the quality of management, which is the one thing that the financial results don’t tell them. Some of the questions may be asked not so much for the conveyance of information, but as tests of managerial knowledge, intellectual ability, and overall competence.

• The meeting is heavily driven by explanation of historic accounting numbers and policies, and also by expectations of future corporate performance.

But in other respects, the investor relations investor meeting is like a typical sales call:

• The seller will make a pitch, covering recent events, corporate strengths, and any objections that the investor is thought to have.

• After the pitch, there will be a series of questions from the investor.

• Management will highlight the strengths of the product, but also handle objections.

• The aim of the meeting is for the audience to be more positive about the product at the end of the meeting than they were at the start.

One-to-one meetings are likely to remain an essential part of the investment process because of both side’s preferences for privacy. Solomon and Soltes (2013) found that private meetings are still productive for U.S. investors, despite RegFD, and especially for hedge funds who have greater flexibility in their trading patterns, and are able to make full use of the intelligence that they gather in these meetings.