CHAPTER 6

Project Development

Viability and Financeability Essentials

Project development is where preparations, planning, analyses, evaluations, and decision events occur and activities that span project definition to creation of the project company's business plan take place. It is the preparation to manage complex, rigorous, and comprehensive processes that cultivates a conducive project environment in the host country and fair regulatory treatment. It is the stage where a balanced risk allocation, a bankable feasibility study, a thorough due diligence, and a sound project financing plan materialize. Project development is a lengthy process to assess, prepare for funding, and bring a project to completion. It is part of the project finance process, which has three main stages: The project prebid or development, contract development and negotiation, and raising the required funding.

The prerequisites of effective project finance are sound budgeting, comprehensive planning, financial modeling, and financial control and reporting systems and providing convincing evidence and clarity of project value creation. There are a multitude of activities in the project development phase which should meet those prerequisites and be guided by the following objectives:

- Creation of a project plan with clear objectives, processes, and guidelines

- Determination and assessment of the true project stakeholders' interests and objectives

- Bringing in PFO and project associates who possess the right skills and qualifications

- Determining stakeholders' abilities to deliver on financial, human resource, and credit enhancement support

- Structuring the project effectively to ensure financeability and financial viability

- Creating a foundation for decision making in each project phase whether executed in parallel or sequentially

The project development stage is important because what happens in this stage affects all subsequent stages and processes and the likelihood of getting expected results. It determines the financing of the project and value creation. It shapes the likelihood of project success when it meets prerequisites and delivers the proper execution of processes and activities described in following sections.

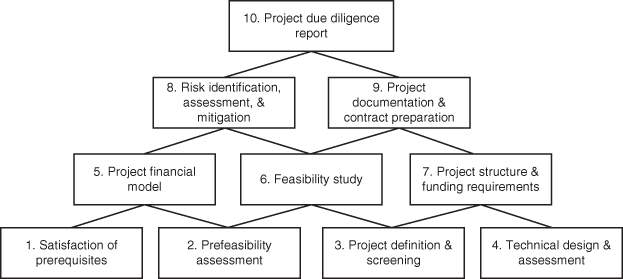

The key deliverables for the development stage are displayed in Figure 6.1, and a successful effort ordinarily produces the following results:

Figure 6.1 Project Development Stage Deliverables

- Project definition, screening, and selection among different opportunities and options

- Creation of the right project environment to harness sufficient political support internally and on the customer side

- Appropriate strategic, portfolio, and operational fit assessments

- Development of project objectives consistent with corporate strategy and new business development objectives

- Harmonization of project stakeholder requirements and objectives and management of expectations

- Identification and allocation of skills and resources required to execute the project successfully

- The project team and subteams are established with specific roles and responsibilities assigned

- Effective project management framework is established to ensure unimpeded, ongoing, 360 degree, unimpeded communication, coordination, cooperation, and collaboration (4Cs)

- Completion of a thorough project economic analysis and timely feasibility study

- Development of a project financial model to capture influencing factors, estimate relationships, and provide financeability measures

- Comprehensive due diligence that validates the feasibility study results and reports on the project's financeability

The content of this chapter is an introduction to chapters dealing with the development‐stage deliverables of project finance. Section 6.1 summarizes the prerequisites of project development that need to be satisfied to build a sound decision basis. Section 6.2 discusses the major undertakings necessary to determine whether to proceed with project development; that is, the activities around completing the project pre‐feasibility study. Section 6.3 is dedicated to project definition activities where project rationale is articulated and project objectives are developed, while Section 6.4 discusses technical design and assessment preparatory activities. The effort required to complete the project feasibility study is crucial—it marks a major decision junction for a project—and it is discussed in Section 6.5.

The project due diligence considerations and report‐related activities of vital importance to all project participants are the subject of Section 6.6 and the development of project and financial structure undertakings are discussed in Section 6.7. Project contract and agreement development and negotiations are the subject of Section 6.8. Section 6.9 presents the events that take place in preparation for marketing a project to investors to attract debt and equity financing. Section 6.10 presents project development cost estimates and success factors. The topics discussed in this chapter are primers to the activities, processes, analyses, evaluations, and decisions made in each phase of project development that are treated in more detail in subsequent chapters.

6.1 PROJECT DEVELOPMENT PREREQUISITES

For reviews and approvals to take place expeditiously, project team preparations and internal sponsor company and customer planning should be guided by funding source processes and requirements. There are some universal project development fundamentals and capability requirements that are necessary to develop projects successfully. Starting with experience and impartiality in selecting advisors, other project team and stakeholder skill prerequisites for successful project development include:

- Expertise in bid preparation and evaluation, procurement experience, and skill in responding to requests for proposals and receiving a contract award

- Experience in project assessment, structuring, and financial markets and instruments

- Well versed in project risk identification and allocation and experienced in assessing adequacy of risk insurance coverage

- Have established a global network of insurance providers with the ability to deliver on the contracted risk coverages in full

- Expertise in macroeconomic country and industry analysis, cost estimation, competitive project company output pricing, cost–benefit analysis, and dealing with regulatory issues

- Accurate assessment of the project's political environment and ability to obtain political support to take the project through the host government's evaluation

- Strong civil, industrial, and environmental engineering, technical design and technology, and equipment evaluation capabilities

- Experience managing the construction of projects and providing input and guidance concerning technical issues in the creation of contracts

- Extensive knowledge of commercial and investment banking, unilateral and multilateral agencies, export credit agencies (ECAs), project credit rating, and in‐depth understanding of lender and investor requirements, as well as those of the host government ceding authority

- Experience in commercial lending, bond financing, insurance and pension fund investing, and private placements

- Strong internal links with all project stakeholder organizations and an extensive network throughout the technology and engineering, legal, and financial communities

- Skilled in developing sound project objectives and preparing project plans to drive the project through the development process

- Competence in providing analysis and inputs and working with legal teams to draft and negotiate project agreements and contracts

- Superior capabilities in managing complex processes and integrating outputs of different participants into the mainstream project process

- Experience in presenting the work of the project development stage to senior management and the due diligence team and addressing issues and concerns

Regardless of how project development is defined or the order of activities, there are some key deliverables common to most infrastructure projects as shown in Figure 6.1. Common phases are the project prefeasibility, the project definition, the technical design, the feasibility study, the due diligence, the financial structure assessment, and the preparation for marketing and raising the financing phases.

6.2 PREFEASIBILITY ASSESSMENT

In this phase, needs are identified and ways to satisfy them are explored and focus is directed to project development. If more than one sponsor is interested in participating in the project, a project development agreement is signed. It spells out the project definition details, voting rights, and sharing of project predevelopment costs; confidentiality, and nondisclosure. It also defines functions to be performed, each partner's roles and responsibilities, and allowance for withdrawal from the project (Hoffman, 2008).

Contact is initiated with the host government and ceding authority to get consensus and political support, local partners are vetted to facilitate the response to request for proposal, and the sponsor or developer project team is established. A project design team is engaged to consider project design options, operational performance expectations, and preliminary project specifications to meet project requirements at competitive cost levels. Assessment of the political, economic, and investment environments takes place along with initial assessment of project risks. Also, the ability of the host government and the ceding authority to deliver on their obligations is evaluated. Then, a project briefing to the sponsor company's senior management team takes place.

A project financial model is developed with some initial assumptions and first cut estimates of capital costs, operational expenses and revenue estimates are produced. The planning, preparations, and assessments that come out of this phase are important because they provide initial estimates of project funding requirements and indications of financeability. These estimates form the basis for the decision to proceed with the project and move to the next phase; that is, project definition. Notice, however, that the project definition and the prefeasibility assessment may take place simultaneously or in some cases the order may be reversed.

6.3 PROJECT DEFINITION

The first step in defining a project is a clear statement of project rationale explaining the background and motives leading to considering the project. This is followed by a strategic, portfolio, and operational fit assessment where complementarity, consistency of objectives, sponsor company strengths and weaknesses, and competitor threats are considered vis‐à‐vis the project opportunity. It is important to determine how consistent the project being considered is with corporate goals and objectives and risk appetite, if it complements the company's portfolio and is operationally feasible, and how it fills current or expected gaps. In the process of doing the fit assessments, the company's situational analysis is revisited to determine if the company has the required resources for the project to be executed successfully. That is, if sufficient resources with the right skills and qualifications can be allocated to the project.

A key element of project definition is ensuring that project needs are correctly identified and determining objectively how and to what extent the project fills those needs. When proceeding to the project definition stage, all project participants are identified and additional skills are brought into the project team to conduct required analyses. Next, each participant's objectives and constraints are examined closely and stakeholder representatives are assigned roles and responsibilities. At this point, it is crucial that a common communication, coordination, cooperation, and collaboration plan is introduced to the project team. This plan is needed because of the complexity of project managing a large project financing; without it the likelihood of project success is diminished.

In the presence of more than one project option, a screening of related opportunities and selection of a most fitting project takes place. This provides the rationale of taking the project to the next phase after the opportunity costs of doing and not doing the project are considered. The activities mentioned so far are meaningful and valid only when project objectives are clearly defined and unambiguously stated. There should be no vagueness, implicit considerations around project objectives, and conflict with strategic, new business development, and corporate financial objectives. Objectives should be reasonable, realistic, and feasible, given the sponsor's resource constraints, and there is a high level of confidence that they can be achieved. However, in order for this to occur, the project team's scope needs to be specified and fixed; otherwise, project objectives become a moving target and so does the value created by the project.

6.4 TECHNICAL DESIGN AND ASSESSMENT

Some of the primary events of the project development phase involve the creation of a technical facility design consistent the performance requirements and initial specifications while capital requirements, timelines, and operational costs are firmed up. Physical and cyberspace security considerations and different options and costs are examined; then, a project design that satisfies the customer and key stakeholders is achieved. Feasible project parameters are determined, and technical project plans are crated along with a project technical implementation timetable. Detailed technical design and technical management plans are developed and the information created is then passed on for decisions and broader project planning and evaluations.

A preliminary technical assessment is performed to identify project design and specification strengths and weaknesses in the prefeasibility study, and a more in‐depth assessment is conducted in the technical design and assessment phase before any proposal is created. Some of the activities involved in the project technical assessment include:

- Project site and technology vendor visits and interviews of host government authorities to ensure there no problems, conflicts, or misunderstandings in the technical area

- Collection and evaluation of technology, cost, reliability and other types of information and data to determine the useful life of the project

- Estimation and evaluation of project costs and benefits of competing projects or project configurations, and selection of the project and configuration most appropriate given sponsor strategic objectives and customer needs

- Identification of technology‐related project risks and issues and making recommendations for project parameter variations that affect risk mitigation and costs

- Providing inputs to the project financial model, the feasibility study, and the due diligence, and recommendations on how to optimize project value creation

6.5 FEASIBILITY STUDY

In this phase, more in‐depth technical, economic, environmental, legal, and financial assessments take place to determine project financing needs, economic viability, and financeability. If advancing the project to the next phase is warranted, senior management approvals are obtained and additional required resources are allocated. This phase is important because it generates and validates data, information, and updates evaluations needed for senior management decisions. The feasibility study forms a basis for the due diligence phase, the sponsor and ceding authority business cases, the project company's business plans, and the project's risk assessment and mitigation. A sound feasibility study incorporates the findings of all project assessments, including physical and cyberspace security, into a report that serves as a guide to implement the project management plan.

The sequence of activities undertaken in the feasibility study fulfills a number of project team responsibilities, which include the following:

- Revisiting the scope and objectives of the project in light of final project definition

- Ensuring consistency of stakeholder interests and objectives, determining if additional participants should be added, and identifying and screening potential new participants

- Understanding the true project‐stakeholder needs and expectations and managing them to levels consistent with project facts and the reality of the project's environment

- Engaging project advisors and consultants to assist in activities, briefings, and presentations to stakeholders' key decision makers

- Probing deeper in the host country's legal, industry, and regulatory environment analysis. The industry analysis examines current versus needed capacity, costs and rates, market shares, and marketing, pricing, and sales aspects

- Investigating project company accessibility to skilled labor and pricing of adequate production inputs to the project company and their availability

- Conducting an updated technical options analysis and defining more precisely technical and operating performance specifications

- Developing, updating, and testing a more complete set of assumptions and obtaining project stakeholder consensus and support

- Evaluating the findings of the environmental impact study and assessing costs associated with needed remediation to include in the total project cost

A second set of project team activities in the feasibility study encompasses the following undertakings:

- Setting up the project governance structure, which is the set of policies, functions, processes, roles, and responsibilities that guide management and control of the project

- Performing political, economic, social, technical, legal, educational, and demographic (PESTLED), megatrend, and subtrend analyses to support a robust demand analysis of the project company's output and developing reasonable scenarios

- Determining if required skills and capabilities are brought in the project and if not, ensuring that adequate resources and skills are allocated

- Ensuring that in addition to project development, capex, and operational expenses, costs related to site preparation and physical and cyberspace security are included in funding requirements

- Expanding the project financial model and incorporating new and updated assumptions, data, and information inputs to firm up project financing needs and financeability

- Conducting additional reality checks on the assumptions, cost and revenue data, information compiled, and the results of the financial model

- Identifying, evaluating, and allocating risks to parties best able to manage and obtain insurance and other project support needed

- Verifying the robustness of the physical and cyberspace security package to protect the project from vandalism, sabotage, and terrorist attacks

- Ensuring that the implementation agreement includes grants and project incentives, such as tax holidays, tax rate reductions, and payment and performance obligation guarantees and a waiver of host government immunity and import duties

The sequence of project development activities can be changed or performed in parallel and the various feasibility study elements, timing, and evaluations are discussed in subsequent phases. The key elements of the feasibility study can be varied in order to satisfy information and evaluation requirements. Project feasibility study costs can be high, but entirely justified, because of the important elements that come out of it which include the following:

- A technical design and engineering project plan with detailed specifications meeting customer requirements

- The foundations for the project due diligence, which helps to identify shortcomings and adequacy of the risk management plan and address issues of concern and validate the evaluation results

- Updated inputs for the project financial model and an outline of project structuring and financing plans with initial supporting material

- A project schedule, inputs needed for the project management plan monitoring and controlling activities, and project milestones and deliverables

- Assignment of clear objectives and deliverables to each project stakeholder and project team member

- Required information, data, and guidance for drafting project agreements and contract negotiations

- Preparation of inputs and guidance to draft agreements and produce and package tender documents and project public releases as needed

- Creation of draft project company business plan, development of indicators of project performance, and draft plans for project course correction when necessary

- Development of project viability and financeability evidence that creates a higher comfort level for senior management decisions

- Recommendation to advance the project to the next phase and obtain senior management approvals

6.6 DUE DILIGENCE

In project financing, due diligence is an in‐depth investigation focused on identifying issues of concern and confirming data, claims, and contract representations. It evaluates analyses and validates assessments before decisions are made and project agreements are signed. It also determines gaps in evidence, assumptions, and assessments; highlights problems, and investigates the extent to which risk assessment and mitigation have been achieved. Additionally, the due diligence does a thorough check on the participants' ability to meet current and future obligations and produces an independent assessment report of the project's funding needs and financeability potential. It also provides a common understanding to lenders and all project participants; that is, a common platform for decision making.

Ordinarily the due diligence is performed by advisors of lending institutions and it is paid for by the project sponsors; however, the project team is involved from the start of the project and plays an important role in it. The expertise of the lenders' advisors includes legal, environmental, technical, insurance, and economic and market analysis, demand forecasting, financial modeling, and other areas of expertise as needed. Additionally, it includes reviews and assessment of the host country investment environment, policies, and regulatory regime; technical and environmental issues, operational requirements, and expected commercial performance using a risk matrix approach.

The due diligence examination includes key items needed to validate technical feasibility, economic viability, and project financeability, such as:

- Government and ceding authority project objectives and constraints in their ability to meet required contributions and contractual obligations

- The project team's understanding and compliance with the public procurement process

- Industry and market analysis, and pricing and tariff setting in the host country

- Concessionaire obligations and property and land use rights

- Risk insurance, other project support, and adequacy of the lenders' protection package

- Dispute resolution and sovereign immunity

- Default issues and termination compensation

- Lender direct agreement and security package

The nature of due diligence varies by project type and stakeholder, but there are elements common to all due diligence efforts that include assessment of the following:

- Project definition and screening details

- Project design, technical specifications, scope of work, and schedule

- Technology design and engineering and equipment assessment

- Project risk identification, assessment, and allocation and mitigation

- Project cost and revenue forecasts and the project company's business plan

- The financial model structure and validated essential inputs and outputs

- Construction specifics and commercial acceptance requirements

- Operations and maintenance program over the project lifecycle

- Draft project documentation and review of legal contractual agreements

- The parties' ability to deliver on their obligations

- Lender covenants and restrictions and systems to ensure repayment

Due to the limited recourse nature of project financing and risks associated with investing outside the sponsor's country, legal due diligence plays a key role in determining project bankability. Some practitioners maintain that project financing is contract financing and that contract review and negotiation includes assessment of applicable laws of the sponsor and host country and its legal framework and regulation. The review also includes laws concerning public procurement processes, environmental considerations, employment and labor practices, consumer protection, and taxation.

For PPP projects, the due diligence must also validate the best value for the money (BVM) principle in order to satisfy host government agency/ceding authority requirements. This principle seeks to validate project cost effectiveness; quality project design, technology, and construction that meets agreed‐to specifications; and project sustainability. Sustainability means that the economic and social benefits shown in the business case support ceding authority and local government objectives and are equitably distributed. BVM is an accepted approach to evaluate the 4Es of the project; namely, its efficiency, economy, effectiveness, and equity.

6.7 PROJECT AND FINANCIAL STRUCTURES

The project ownership structure is a key determinant of the financing structure. It is determined by the customer or host country tender requirements, the debt and equity levels to be raised, control of the project, the tax laws of the host country, and accounting treatment of the project company considerations. A second key determinant of the financing structure is the project capital structure, which is determined by projections of revenue and capital and operational costs, operating cash flow, the risk allocation scheme and credit enhancements, debt service requirements versus debt service capacity, and net cash obtainable by sponsors.

The different key considerations in developing the project and financial structures include consideration of a number of factors, such as:

- Defining a project company ownership structure; i.e. a corporate, joint venture, general partnership, or limited liability company structure

- Ascertaining the amounts and timing of equity contributions, involvement and commitment of sponsors, and debt‐funding requirements

- Assessing the costs and benefits of different project delivery options, such as build, operate, and transfer of ownership at project completion(BOT), build, own, operate, and transfer (BOOT), design, build, operate, transfer DBOT, etc. to the host government's ceding authority

- Performing in‐depth project returns to sponsors and economic and ratio analysis to determine project viability

Infrastructure or other large project financings are collaborative and iterative efforts to balance participant interests, ensure project viability, and arrive at some optimal scheme of raising the required funding. Once the project feasibility study, the due diligence, and identification of the sources of funding for the project are completed, addressing risk allocation and credit enhancements needed in a manner acceptable to lenders comes into focus. In this phase, knowledge of financial markets and instruments along with extensive networks, close contacts with financial institutions, and a strategy for drawdowns and repayments are of paramount importance.

Financial structuring is determining the type and blend of funds used in financing the project, primarily the amount of debt to raise and its repayment schedule, intended to maximize the sponsors internal rate of return (IRR). Financial structuring also defines the financial support from different participants, drawdowns, their timing, and repayments to various sources of funds.

Parenthetically, the financial structure used in a project is also known as the project model and because of the variety of projects, there are numerous financial structures used, depending on the particulars of project definition.

In addition to the role of public sector involvement in the project, other project financial structure considerations are the parties involved in the project, their decision‐making process, and their debt and equity contributions. Again, flow of money and contractual agreements, timing of drawdowns and repayments, project risks and their mitigation, and a credit‐support package are prime concerns. The project financing structuring elements are addressed in the project financing plan discussion of Chapter13.

The kind of project financing and the sources of funding are also dependent on the project stage. In the project development phase, funding comes from sponsors/developers and grants from governments or multilateral financing institutions, while construction financing comes primarily from short‐term commercial bank debt. In the operational phase, refinancing with long‐term maturity takes place. Notice that from the public participant perspective the essence of financial structure refers to the structure of the contractual agreements. From the project company's perspective, financial structure refers specifically to the project company's financial structure.

6.8 AGREEMENTS AND NEGOTIATIONS

Infrastructure project development is a lengthy process that, among other matters, addresses business and risk issues, documenting agreements, and drafting, preparing, and negotiating project contracts. In project finance, contracts are created when parties that have the capacity to deliver on contract terms reach agreements that define their rights and obligations. Contracts are legally binding and enforceable when the responsibilities and rights of the participants are stated in clear form and unambiguous language. For contracts to be valid and enforceable in the host country, they must be equitably made, balance the interests of the parties involved, and be consistent with the host country's laws, regulations, and policies that protect their integrity.

The purpose of project contracts is to allow stakeholders to tailor the contents of agreements, shape the participants' relationships, manage expectations, and define how negative project outcomes can be resolved. Also, well‐structured contracts ensure that the parties involved understand the details of the agreements and their implications. Contracts are important because they guide processes that form the foundation for raising funding for a project. However, they are crucial in the case of disputes to ensure that not honoring their terms results in fair compensation for work done, products or services delivered, funds advanced, etc. Besides preparation for contract creation, contract management is important since it spans the initiation, planning, drafting, negotiating, and implementation of the project, and monitoring contract compliance in operations.

Infrastructure project finance contracts cover all key aspects of project ownership structure, the project company's structure, and the resulting financial structure. They also cover participant contributions and the procurement, project delivery, and payment parts such as, the duration of a project's concession, pricing, quality and performance, security packages, and costs. Contracts may cover many project aspects, but they cannot cover everything. Some things are best managed through relationships among the parties involved, such as flexibility, willingness to allow minor deviations from contract terms, and renegotiating contracts when it is necessary.

Project finance is considered contract finance by some project participants because the interweaving of contractual arrangements makes project financing possible. This is so because contracts are the venue and tool where risks are identified and mitigated or allocated through negotiations to entities best able to handle them. While the project type and its particulars determine what contracts are required, there are some elements common to most projects, such as the implementation or concession agreement, the offtake and supply agreements, the construction contract, and the operations and maintenance agreement. Other common contracts involved are the lenders' direct agreement between the government, the project company, and the lenders and the loan agreement. Also, performance bonds, collateral guarantees, and the loan term sheet are components of the project contractual framework.

Development and negotiation of contracts is a lengthy and strenuous activity that produces voluminous documentation. In one large infrastructure project financing in the mid‐1990s, the contracts and related paperwork filled boxes that took up the entire space of a 20x20x12 room in the offices of a law firm in Washington, DC. Preparation for contract negotiations is essential because drafting agreements requires the engagement of the entire project team for:

- Thorough review of the technical evaluation details, the feasibility study, and the due diligence report along with evaluation of financial model outputs

- Briefings to the negotiations team with a package containing at least:

- Key issues and terms to be negotiated

- Data, analyses and evaluations, and reports to support the team's negotiating positions

- Opening, fallback, revised, and walk‐away positions

- Assessment of impacts of contract variations and assumptions by the financial model

Important activities of the project team in preparation for contract creation and negotiation include the following activities and contributions:

- Engaging legal counsel and expert advice early to manage participant expectations early

- Developing a clear set of project objectives and contracts required to help achieve them

- Conducting research on key project areas and planning according to those findings

- Starting with a wish list, such as one of the term sheets, and creating a negotiation plan

- Taking a reasonable and balanced approach to negotiations

- Outlining reasonable negotiation positions and suggestions on how to move along positions

- Being sensitive to cultural differences and different negotiating styles

- Preparing for a long, tedious, going back and forth process ahead

- Staying positive and seeking compromises and concessions to bring financing to closure

- Learning from earlier experiences and introducing innovation along the negotiation process

6.9 PROJECT MARKETING AND RAISING FINANCING

The marketing of an infrastructure project is an integral part of raising financing and its foundations rest on the project economics of the feasibility study, the due diligence report, and the output of the project financial model. Various forms of project marketing are used to attract sponsor partners, lenders, and investors in different stages of a project. Nevertheless, the objectives of marketing an infrastructure project are to communicate effectively and convince potential participants of the value generated by the project and demonstrate how their interests and objectives are satisfied under a reasonable risk mitigation plan. Infrastructure marketing materials are not only lender and investor presentations, such as project prospectuses and information memorandums but, also, material information included in bid proposals or submissions to requests for proposals.

The project prospectus, or information memorandum, is a composite of the sponsor's business case and the business plan of the project company prepared for investors. Along with other marketing material they highlight the important aspects of the project investment opportunity. However, the information memorandum includes in a summary and succinct form for investor scrutiny with more analyses and evaluations than a prospectus does. The analyses and evaluations and supporting materials are prepared by the project team in conjunction with the legal team, project advisors, and consultants. The prospectus or information memorandum, marketing material, and presentations are packaged professionally and presented to different audiences by the sponsor's investor relations and public relations groups.

The project prospectus and the information memorandum contain synopses of work performed in the project development phase. They typically include the following required elements:

- Market Review and Project Background and Rationale

- Project description and the project schedule

- Project technical design and performance specifications

- Host country political, economic, and investment environment review

- Assessment of the industry structure, competition issues, and industry trends

- Appraisal of the host country's legal and regulatory framework

- Evaluation of environmental, health and safety, and labor market issues

- Project company structure, management team, objectives, and business plan

- Project sponsors/developers and other participants involved and identified

- Design, engineering, and technology partners participating in the project

- Permits and approvals already secured, ceding authority support for the project, and compliance to the schedule and other requirements

- Main assumptions underlying the revenue projections already validated

- Costs and benefits of the project, both financial and social and environmental, and the project contributions to the local economy's development

- Balanced and fair risk mitigation on a best able to handle and cost‐benefit basis

- Structure of the project agreements and all applicable contracts

- Project financial plan showing funding requirements, capital structure, drawdowns and repayments

- Results of the financial model analysis: project net present value (NPV), cash flow projections, investor IRR, and debt ratios

- Risk factors and their mitigation and the insurance and credit support package

- The project's long‐term viability and the investment opportunity sustainability

- The key success factors and the likelihood of achieving the project objectives

- A summary of the value of the project and supporting appendices

The PFO's and the project team's responsibilities in the preparation of the information memorandum include:

- Demonstrating to customers or the host government's ceding authority that the project as structured meets their needs and supports their objectives

- Establishing that the project fully meets the requirements of the best value for money principle

- Showing that the project is indeed producing adequate returns and is a long term economically viable investment

- Confirming the reasonableness of assumptions underlying the financial model, the risk mitigation, and the credit support package

- Establishing the transparency of project company governance and financial reporting

- Creating, projecting, and maintaining a positive sponsor company image of the project throughout its lifecycle

- Demonstrating the necessary efficiency of financing developed to support competitive bids

6.10 DEVELOPMENT COSTS AND SUCCESS FACTORS

Sources of funding for project development vary by type of project, but the most common sources of project development financing are:

- The host government various agencies' project funding budgets

- Assignment of host government human resources and in‐kind contributions

- Private capital, project developers, and sponsors

- Sovereign loans and credits from development banks

- US Agency for International Development

- Sovereign loans and credits from development banks

- Grants from trust funds and donor programs

Project development costs are high and vary not only by project type and size, but also by the skills of project participants, funding source, and host country economic development. High project development costs are due to acquisition of expertise residing in advisors and consultants, contacts with host government authorities, rigorous analyses and the due diligence effort, the identification of project risks and their effective mitigation, and the lengthy contract drafting and negotiation process of contracts. MacKinzie and Cusworth (2007) estimate project feasibility costs around 2.3% of total project costs. However, estimates of project preparation range from 5% to 10% depending on timing, definitions, and other project parameters. As an example, the Infrastructure Consortium for Africa (2014) reports the following estimates:

- Average Africa regional projects: 7%

- World Bank estimate: 5% to 10%

- Ifraco Africa projects: 10%

Success factors for project development are factors that create a solid foundation for a project to achieve key project stakeholder expectations; that is, to satisfy everyone's interests and needs in an effective manner. Remember, the main objective of project development is to create the conditions for:

- Accurate assessment of project characteristics via the technical evaluation and the feasibility study

- Thorough identification, analysis, evaluation, risk allocation and mitigation

- Ensuring the long‐term project economic viability

- Obtaining efficient project financing to allow timely and on‐budget completion

- Value creation and adequate returns to all project participants

From the host country perspective, the best project‐development strategy is to plan and structure an infrastructure project that meets its needs with minimal environmental impacts and maximum social benefits. Successful project development also requires the principle of value for the money to be operative and that approvals, processes and procedures are closely followed. From the sponsor's perspective, project success is judged by close strategic, portfolio, and operational project fit; the NPV created, an acceptable IRR, strong debt ratios, and project company ability to make payment of dividends.

Effective project management is crucial for successful project development and in order for the objectives of successful project management to be realized, a number of pre‐conditions need to be satisfied, such as:

- Planning, organizing, and assigning a project team early on and staffing it with associates possessing the right skills and qualifications

- Considering the opportunity costs of doing and not doing a project. These costs are often ignored, but are crucial in new business development decisions

- Developing clear and effective processes that help form the project plan

- Selecting an appropriate project‐delivery strategy and vehicle

- Scrutinizing cost and revenue forecast assumptions, models, and scenarios used and developing realistic project feasibility assessments

- Objectively assessing project schedules, expected deliverables, critical paths, dependencies, and risks to the project

- Creating participant consensus and obtaining buy‐in and political support

- Ensuring all around unimpeded communication, coordination, cooperation, and collaboration is prevalent