Chapter 3

Loan Agreement

There are no standard terms and conditions for commercial structured real estate financing agreements, and each agreement is negotiated individually without any predefined standard form contracts. Moreover, the rules applicable to loan agreements differ from country to country, as more closely detailed in Part Two of the book.

The following rules and clauses are those which frequently appear in structured real estate loan agreements:

- parties1 to the transaction (bank, borrower company, and guarantors, if applicable);

- object and purpose of the loan;2

- conditions precedent;

- amount of the loan;

- loan repayment schedule;

- allocation of the loan;

- interest rate;

- interest rate risk hedging;

- fees charged by the bank;

- frequency and procedures of drawdown;

- events of default (i.e. situations which will end the agreement or establish entitlement to terminate or withdraw);

- collateral;

- insurance;

- representations and warranties by the borrower;

- contractual covenants;

- duties to provide information;

- costs, taxes, and ancillary charges;

- clauses relating to assignment/transfer/syndication;3

- choice of law and jurisdiction.

The contents of the aforementioned contractual clauses will differ depending upon the relevant legislation in force in the country in which the agreement is concluded. In common law countries, all matters are regulated under the loan agreement as it is the only source of rules governing the relationship between the parties (bank and borrower). In civil law countries on the other hand, contracts should be more concise as it is possible to refer to statutory provisions as a source of regulation for the contractual relationship, which means that the sources of law applicable to the relationship are the contract and the reference legislation, which can often not be set aside in the contract.

Having clarified this aspect, the following sections will describe the most significant contractual clauses which are common to the various legal systems, while the clauses specific to each country will be described in Part Two.

3.1 Object and purpose of the loan

The clause relating to the object is generally drawn up as follows.

Subject to the terms of this agreement the Lender makes available to the Borrower a medium term loan facility for the amount up to the commitment.

A structured loan sometimes specifies the intended use of the loan and consequently, in addition to the obligation to repay the loan and to pay interest, places the borrower under a further obligation to allocate the amounts received in order to fulfil a specific purpose. For example, agreements relating to the provision of credit in the construction sector will contain a clause requiring the borrower to allocate the amount to the construction of the property.

Purpose: The Loans may only be used for financing the construction cost of the properties.

3.2 Conditions precedent

The effectiveness of the loan agreement could be conditional upon the lender having received, by no later than the date of execution of the contract, a set of documents in form and substance satisfactory to him.

The most common conditions precedent to effectiveness and to initial funding are the following:

- Constitution: a certified true copy of the constitutional documents of the borrower entity.

- Certificates: a good standing certificate of the borrower entity issued by the competent companies register, dated not earlier than a few calendar days4 before the first funding date and including a non-insolvency statement.

- Legal opinions:

- a legal opinion from an approved legal counsel to the borrower, addressed to the lender which states the borrower's due incorporation, power, and capacity to enter into the loan agreement to which the borrower is a party and the fact that the execution and performance of the loan do not conflict with the constitutional documents of the borrower;

- a legal opinion addressed to the lender in respect of each guarantor's power (if present) and capacity to enter into any guarantees.

The lender is not obliged to provide any further funding tranche until some conditions are fulfilled to his satisfaction, the most common of which are the following:

- Funding Notice: the borrower has delivered a funding notice requesting the funding portion.

- Commitment: the principal outstanding after providing the funding portion will not be greater than the commitment amount.

- No default clause: no default or event of default has occurred or will result from the funding portion being provided.

- Authorizations: all corporate authorizations which are required to be obtained by the borrower to deliver the funding notice have been obtained.

Each certified document given to the lender by the borrower must be certified to be a true copy of the original document by a director of the borrower, no more than a few days before the date on which it is provided.

Usually no funding notice may be given, if at any time the borrower has already required the provision of a certain defined funding portion (regardless of the amount of any undrawn commitment).

3.3 Amount of the loan

The amount loaned depends mainly on three variables:

- the project which the loan is intended to fund, and hence the value and/or construction cost of the property and its profitability;

- the collateral provided;

- the borrower's creditworthiness.

This amount may be granted in one single line of credit, or alternatively through secondary lines such as for example a loan to cover the costs resulting from the acquisition.

For loans intended to pay for the construction costs of a property, the amount will be specified in the agreement, and will be drawn down in line with the state of progression of work (stating the maximum amount of drawdown, subject to the conclusion of supplementary agreements). The amount which is actually drawn down will depend upon the covenants stipulated in the agreement (including in particular LTC, LTV, DSCR, and ICR), as in the following example of clause.

The lenders make available to the borrowers a term loan facility in an aggregate amount equal to the lower of:

- the total commitments;

- 70% of the cost;

- 50% of the value of the properties (as determined from the initial valuation).

The facility can also be drawn down in different tranches when the project requires cash (i.e. development project). Moreover, in countries where a tax on financing is applied,5 tranches allow deferral of the point in time when the tax is payable.

3.4 Interest rates

The interest rates specified in a loan agreement include the standard rate (base rate plus margin) and the default rate.6

Loan agreements may be subdivided into two major classes7 with regard to the standard interest rate: fixed-rate loans and floating-rate8 loans.

The type of interest rate and the spread will be negotiated between the parties. It is clear that the more risky the operation, the higher the spread will be: this element must remunerate amongst other things the bank's intermediation services and absorb the credit risk9 component.

The actual interest rate agreed upon will track a reference rate:

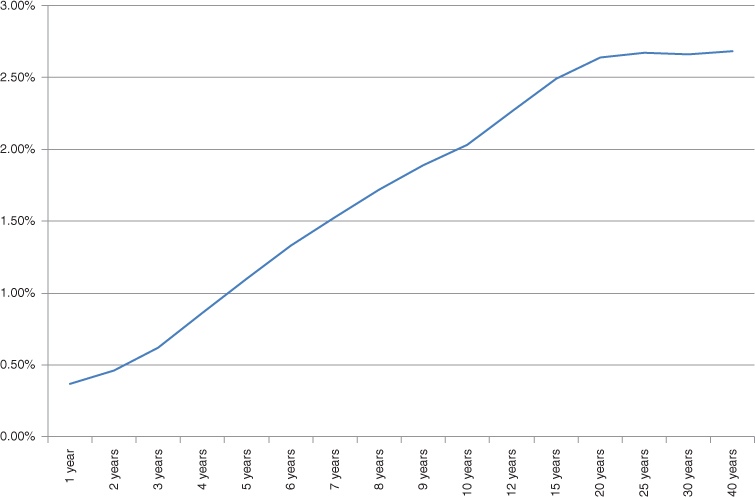

- If a fixed rate is chosen, the IRS10 (Interest Rate Swap) rate is often used (in Figure 3.2 an example of EURIRS rates is presented)

- If a floating rate is chosen, in the Euro countries the reference rate will be the EURIBOR (Euro Interbank Offered Rate), whilst for other major currencies the LIBOR11 (London Interbank Offered Rate) is used (in Figure 3.1 an example of EURIBOR rates trend is presented).

Figure 3.1 EURIBOR rates trend14

Figure 3.2 EURIRS rates on different maturities on a fixed date15

For fixed-rate loans, the interest rate remains the same for the full term of the loan (or for a pre-set period), and the precise amount of the instalments due is known from the outset.12

This type of loan, under which the borrower is not exposed to interest rate rises, does however entail two negative aspects: a greater potential cost (in the event of a fall in interest rates) and generally an interest rate which is higher than a floating rate on a loan with equivalent characteristics.

For floating-rate loans, the interest rate is not set at the start for the full term of the loan, but is regularly reviewed in line with changes in the reference rate (EURIBOR or LIBOR from 1 to 12 months). A floating rate will offer a lower initial cost, but will entail full exposure by the borrower to the interest rate risk.13

If the borrower delays any payment a default rate is applied. It is usually determined as the sum of the interest rate and a negotiated overdue margin and calculated on the number of days of delay in the payment. If, for example, there is a 15 day delay on the payment of a €1,000 loan instalment, and the default rate is set at 7%, the amount due is €2.88 (€1,000 * 15 days / 365 days * 7%).

3.5 Interest rate risk hedging

In structured real estate loans, cash flows from the project (e.g. rental payments and/or amounts received from the sale of properties financed) are used in order to repay the loan instalments. It is therefore necessary to strike a balance between incoming cash payments (rent and/or sales) and outlays (instalments plus costs) for the real estate project financed. An increase in the instalment following a rise in the floating rate could lead to a potential default on the deal. For this reason, if a fixed interest rate is not chosen, it will be necessary to hedge against the interest rate risk. The various forms of hedging16 which are considered are principally Caps, Collars, and Swaps.

3.5.1 Interest Rate Cap

An Interest Rate Cap, or simply a Cap, is an instrument for hedging against the risk of an interest rate rise; the borrower will continue to pay the floating rate whilst he will also acquire (generally from a bank, though not necessary the lender) for a fee the right to apply an Interest Rate Cap. If the interest rate exceeds the agreed Cap, a third party defined as the counterparty will pay the bank the difference between the Interest Rate Cap and the actual interest rate at the time each instalment falls due.17

It is clear that an Interest Rate Cap will be chosen in order to ensure that debt servicing18 remains at sustainable levels, and hence that operating cash flows (e.g. rental payments) and financial covenants (e.g. DSCR and ICR) will be calculated on the basis of the level of Cap chosen.

The lower the Interest Rate Cap, the higher the fee the borrower will be required to pay to the counterparty (and vice versa).

3.5.2 Collar

The Interest Rate Cap cost may be reduced or eliminated by using a Collar, which by contrast enables a kind of uniformity to be imposed on the instalments due. In practice, a Collar is comprised of a combination of a Cap and a Floor (the latter being the exact opposite of a Cap, in that it sets a minimum interest rate rather than a maximum rate), thereby creating a range within which the interest rate may vary. A transaction incorporating a Collar will entail the purchase of a Cap and the sale of a Floor. If the interest rate exceeds the Cap, the difference will be paid by the counterparty, whilst if it falls below the Floor, the difference will be paid to the counterparty. Figure 3.3 shows an example of hedging using Caps and Collars.

| Time | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

| Spread | a | 2% | 2% | 2% | 2% | 2% | 2% | 2% |

| Cap | b | 6.5% | 6.5% | 6.5% | 6.5% | 6.5% | 6.5% | 6.5% |

| Floor | c | 3.5% | 3.5% | 3.5% | 3.5% | 3.5% | 3.5% | 3.5% |

| Eurirs | d | 4% | 4% | 4% | 4% | 4% | 4% | 4% |

| Euribor | e | 2.5% | 2.75% | 3.25% | 4.75% | 4% | 2.25% | 0.75% |

| Difference | f = d - e | 1.5% | 1.25% | 0.75% | –0.75% | 0% | 1.75% | 3.25% |

| Fixed rate | g | 6% | 6% | 6% | 6% | 6% | 6% | 6% |

| Floating rate | h = a + e | 4.5% | 4.75% | 5.25% | 6.75% | 6% | 4.25% | 2.75% |

| Cap | i = min (b; h) | 4.5% | 4.75% | 5.25% | 6.5% | 6% | 4.25% | 2.75% |

| Floor | j = max (c; h) | 4.5% | 4.75% | 5.25% | 6.75% | 6% | 4.25% | 3.5% |

| Collar | k = max (if (b>h; h; b); c) | 4.5% | 4.75% | 5.25% | 6.5% | 6% | 4.25% | 3.5% |

| Fixed - Floating | l = g - h | 1.5% | 1.25% | 0.75% | –0.75% | 0% | 1.75% | 3.25% |

| Fixed - Cap | m = g - i | 1.5% | 1.25% | 0.75% | –0.5% | 0% | 1.75% | 3.25% |

| Fixed - Floor | n = g - j | 1.5% | 1.25% | 0.75% | –0.75% | 0% | 1.75% | 2.5% |

| Fixed - Collar | o = g - k | 1.5% | 1.25% | 0.75% | –0.5% | 0% | 1.75% | 2.5% |

Figure 3.3 Hedging using Caps and Collars

3.5.3 Interest Rate Swap

Another form of interest rate hedging may be obtained by procuring an Interest Rate Swap (IRS). Under such contracts the parties undertake to pay or collect at pre-determined dates amounts calculated on the basis of the differences between various interest rates. In practice, a Swap may be regarded as an exchange of interest rate payments between two parties which are seeking hedge against changes in the interest rate.

A Swap involves an exchange of interest payments calculated on a certain agreed reference principal (notional) for a predetermined period of time until the term of the agreement: the borrower will pay a fixed level of interest to the counterparty, whilst the latter will pay a floating rate, and the reference principal under the agreement is at no time exchanged between the contracting parties.

The contracting parties will exchange interest rate payments based on a fixed rate and a floating rate, whereby the fixed rate is due to the seller (usually a bank) and the floating rate is due to the buyer (borrower); the difference between the two rates will establish the amount payable and the party to which it will be due. As long as the floating rate does not exceed the fixed rate agreed upon during the term of the contract, the counterparty bank will have a cash inflow; however, if the floating rate (e.g. EURIBOR) exceeds the fixed rate agreed upon, the counterparty will have a cash outflow which will be used to pay the interest rate on the loan.

In contrast to fixed-rate loan agreements, interest rate Swap agreements are concluded separately with a counterparty which is not necessarily the lending bank; in such cases, the payments (cash outflows for the counterparty and cash inflows for the borrower) must be clearly earmarked for the loan by an express commitment or assignment. Moreover, in some cases, these contracts may be transferred from one loan agreement to another and, in the event that the loan is redeemed, may result in entitlement or liability to payments on the part of the borrower, depending upon the level of the interest rate at the time of redemption.

An Interest Rate Swap contract provides for the conclusion of numerous agreements between the seller of the IRS (the bank) and the buyer (the borrower):

- the reference amount on which the interest rate flows exchanged is to be calculated (notional amount);

- the currency in which the reference amount is denominated;

- the fixed rate, also known as the IRS rate, representing the price of the Swap.

The defined level of the interest rate is the principal element of the agreement, and will depend upon numerous factors, such as:

- the term of the agreement;

- the parameter chosen as a reference for the floating rate (generally the 3 or 6 month EURIBOR or the LIBOR for non-Euro transactions) and any other element characterizing the transaction;

- the fixing date on which the floating rate is set;19

- the frequency20 of payments at the fixed or floating rate when interest payments are due (annually, quarterly, or every six months).

A simple example may assist in clarifying the IRS mechanism.

Alongside the simple structure presented, it is possible to use Swap agreements based on the hedging requirements for the specific loan. In particular, an amortizing Swap enables the notional principal to be reduced in line with the term of the loan. For example, the parties may agree for a particular loan that the interest rate difference is calculated on a different notional amount at the end of each period, which is reduced in line with the repayment plan for the loan which it is intended to cover.

A Swap may be combined with a Swaption, an option granting the buyer the right, but not the obligation, to conclude a Swap agreement on a given future date according to terms specified in advance (term and reference rates).

The combination of a Swap and a cancellation option will create a cancellable Swap, which entitles one of the counterparties to cancel the IRS at a certain date without any requirement to pay penalties.

Finally, rather than concluding a hedging agreement or choosing a fixed rate of interest, the parties may incorporate a “Drop Lock” clause into the loan agreement, namely a clause under which the borrower provides the bank with an irrevocable mandate to convert the floating rate into a fixed rate when the IRS reaches a specific agreed threshold.

3.6 Loan allocation

Loans relating to property portfolios which provide for redemption of the loan through the sale of individual properties will allocate the debt to individual properties in an Allocated Loan Amount (ALA) table. This allocation is fundamental since, if the borrower sells one of the properties, but no provision has been made for the transfer of the debt to the buyer, the seller will be required to repay an amount equal to a percentage (which is generally greater than 100% and is defined as the release factor or release price) of the debt allocated to the property mortgaged which has been sold as stated in a table agreed upon between the parties and appended to the agreement.

This mechanism is used in order to reduce the risk for the lender since the reduction in the debt is more than proportional to the reduction in the value of properties provided as collateral: in this way, even if the “best properties”21 are the first to be sold, the bank's effective exposure will be reduced by a proportion in excess of the properties sold (in order to avoid a situation in which the bank has a residual loan with the same LTV, but which is guaranteed by properties which are vacant and/or difficult to market). A simple example is presented to explain ALA.

3.7 Loan repayment schedule

In general, this clause sets out the repayment schedule for the loan and the regularity (monthly, quarterly, half-yearly, or annually). Depending upon the specific contractual terms and the object of the loan agreement, the parties may choose between a range of mandatory repayment procedures that are illustrated in Chapter 4. Some of the most common are:

- bullet payments;

- interest-only repayment plans (semi-bullet);

- balloon payments;

- fixed repayment plans.

Repayment of the amount borrowed may be made either in advance by the borrower in one single instalment, or alternatively the borrower or the lender may request that advance payment may be made if certain prerequisites are met (e.g. a change of control of the borrower, change of the sponsors, change of the tenants, disposal of the property).

The borrower must repay the outstanding amount of the loan borrowed in full on the final maturity date together with all other amounts then due or outstanding from that borrower under the finance documents.

As stated in this example of a clause, prepayments could be mandatory or voluntary.

3.8 Fees

Fees represent a further element of the lender's remuneration and a cost for the borrower. The most common are:

- Arrangement Fee;

- Commitment Fee;

- Agency Fee;

- Syndication Fee;

- Prepayment and Cancellation Fee or Early Repayment Fee.

The Arrangement Fee is a form of early remuneration22 which is paid by the borrower to cover the loan organization activity prior to initial drawdown and is calculated as a percentage of the total loan negotiated.

The Commitment Fee is equivalent to a percentage of the loan agreed upon which is not used, and must be paid to the bank (in general every quarter) from the time when the agreement is concluded. The Commitment Fee shall accrue from the date of this agreement and is payable in arrears on the utilization date.

The Agency and Syndication Fees are paid by the borrower as consideration for arranging the loan and for loan syndication activity. They are generally paid regularly (on an annual basis) or up-front to the arranging bank.

The Early Repayment Fee, which may naturally be waived by the bank, is required in return for the borrower's right to repay the loan in advance: this fee, which is specified under contract, is calculated as a percentage of the principal repaid early. This is a clause which benefits the debtor since under loan agreements, the repayment term for the amount drawn down is deemed to be set in favour of both parties, which means that the debtor may not redeem an obligation to repay the loan over a particular period of time without the bank's approval. Payment of an early redemption fee therefore performs the function of indemnifying the bank, which will be remunerated both for the risks and charges resulting from the redemption of the loan facility, as well as for the fact that it will no longer receive regular remuneration for its financial intermediation (through the loan spread), which essentially amounts to its remuneration for the activity carried out.

The following is an example of common clauses.

In order to calculate the overall cost of a loan, it is necessary to calculate the IRR on the comprehensive stream of cash flows which takes account not only of drawdown and principal repayments, but also of all the other costs (e.g. financial charges, taxes, and fees).

In Figure 3.6 an example of loan fees is presented.

| Loan Amount | € 1,000,000 | Agency Fee | € 500 | |||

| Arrangement Fee | 1.10% | Syndication Fee | € 700 | |||

| Commitment Fee | 0.45% | Fixed Interest Rate | 5.00% | |||

| Time | 0 | 1 | 2 | 3 | 4 | 5 |

| Loan Balance BoP | € 350,000 | € 650,000 | € 850,000 | € 1,000,000 | € 550,000 | |

| Committed amount | € 1,000,000 | € 650,000 | € 350,000 | € 150,000 | € 0 | € 0 |

| Drawdown % | 35% | 30% | 20% | 15% | ||

| Drawdown | € 350,000 | € 300,000 | € 200,000 | € 150,000 | € 0 | € 0 |

| Repayment % | 45% | 55% | ||||

| Repayment | € 450,000 | € 550,000 | ||||

| Loan Balance EoP | € 350,000 | € 650,000 | € 850,000 | € 1,000,000 | € 550,000 | € 0 |

| Arrangement Fee | € 11,000 | € 0 | € 0 | € 0 | € 0 | € 0 |

| Commitment Fee | € 0 | € 2,925 | € 1,575 | € 675 | € 0 | € 0 |

| Agency Fee | € 500 | € 500 | € 500 | € 500 | € 500 | € 500 |

| Syndication Fee | € 700 | € 700 | € 700 | € 700 | € 700 | € 700 |

| Interest | € 0 | € 17,500 | € 32,500 | € 42,500 | € 50,000 | € 27,500 |

| Total cash flow | € 337,800 | € 278,375 | € 164,725 | € 105,625 | –€ 501,200 | –€ 578,700 |

| Actual cost | 5.77% |

Figure 3.6 Loan and bank fees

The actual cost of the financing is calculated using the internal rate of return formula and it also represents the actual return for the lender. Due to the various fees it is higher than the agreed interest rate only.

3.9 Frequency of drawdown and procedures

The first loan drawdown23 is generally conditional upon the provision of all guarantees in the forms and according to the priority ranking specified in the agreement and upon completion of legal, tax, and technical due diligences confirming all assumptions made at the time the loan was granted.

Following receipt by the bank, any requests for drawdown are irrevocable and are subject to a range of conditions. In particular, they must specify the drawdown date, which must under all circumstances be later than the date on which the drawdown is requested, and for example must coincide with the date of conclusion of acquisition of the property in relation to which the borrower has requested drawdown.

The request must also specify the amount requested for drawdown in relation to the respective financing line.

3.10 Events of default

The financing agreement contains all provisions that trigger the default of the financing, with the consequence that the lender is entitled to ask for the total repayment of the capital. Some examples of event of default clauses follow.

3.11 Property insurance

The borrower is responsible for all insurance costs in order to restore the original value of the collateral property (in cases involving partial damage) or to redeem the debt in full in the event that the property provided as collateral is destroyed (for example as the result of fire or explosion). In cases involving leased properties, an insurance policy may also be required which provides partial compensation for losses resulting from the inability to let out a damaged property.

Furthermore, should the value of the collateral fall, due inter alia to a general or local fall in property prices as certified by an official surveyor's report based on objective market parameters, the contract will grant the bank a right to require that the collateral be increased accordingly, or the provision of suitable collateral and/or the partial redemption of the loan.

The following is a detailed example of clauses.

3.12 Representations and warranties

Representations and warranties constitute statements by the borrower on an on-going basis during the term of the loan and are used to inform the parties to the loan agreement of the fact that the loan was granted on the basis of the economic, financial, legal, and tax situation disclosed by the borrower at the time the agreement was concluded; should any substantial discrepancies or breaches emerge between the information provided and that subsequently ascertained, the bank may terminate the agreement and/or to refuse to advance funds.

These agreements generally take the following form. The borrower makes the representations and warranties set out in this clause to each finance party.

A very detailed example of clauses follows.

3.13 Duty to provide information

In order to secure greater protection, the lender must also negotiate a series of clauses which are capable of providing it with timely information on the “state of health” of the borrower and regarding the transaction. Under the terms of these clauses, the borrower is obliged to inform the lender of any disputes, arbitral proceedings, or administrative procedures initiated after conclusion of the agreement which may have a substantial detrimental effect.

Other clauses have been finalized with the goal of monitoring the real estate operation during the term of the loan. The borrower may be required to inform the bank with sufficient advance notice of its intention to sell or exchange the property or to establish any other real right of possession over it. Particularly restrictive clauses on the borrower may require it to secure the prior approval of the lender if the property financed is subject to a new property management agreement.

The abovementioned duties of disclosure will also include a right for the lender to appoint a surveyor in order to ascertain the OMV of the property. An example of a disclosure obligation follows.

3.14 Costs, taxes, and ancillary charges

In addition to the fees due to the bank, the agreement must also specify the costs which are to be borne by the borrower, including the costs of regular notices provided for under bank transparency legislation. The agreement may grant the right to vary the interest rate or any other price or condition to the detriment of the borrower; such a right must be expressly provided for in the agreement and the relative clause must be specifically approved by the borrower, subject in addition to compliance with bank transparency legislation.

3.15 Contractual covenants

A covenant is a contractual clause agreed upon during the negotiation stage which grants the bank the right to renegotiate or terminate the agreement following the occurrence of the events expressly specified in the clause. Under a covenant a borrower will undertake not to carry out acts which could be detrimental to the rights of the bank or otherwise increase the risk of default, whereby the bank is generally granted the right to renegotiate or terminate the loan where the conditions of the covenant are breached (negative covenant), or alternatively to act in such a manner as to enable the bank to monitor the loan over time (positive covenant).

Under some covenants, the borrower undertakes to repay the loan (in full or in part) should any situations arise which increase the risk associated with the transaction for the bank.

Compliance with covenants may result in:

- improvements to the financial terms of the loan, or more stringent financial terms in the event of a deterioration in the parameters of valuation of the creditworthiness of the company and/or transaction (in order to offset the lower or higher credit risk of the transaction and the resulting spread applied);

- termination where a change in the conditions deemed to be fundamental at the time the loan was granted requires the bank to request early repayment of the loan (event of default).

In particular, covenants may be divided between:

- balance sheet covenants;

- financial covenants.

3.15.1 Balance Sheet Covenants

Under balance sheet covenants, the clause is based on individual or consolidated balance sheets, usually with reference to the past performance of the main economic and financial parameters of the borrower company and/or its sponsors (in cases involving SPVs) and setting out “red lines” in order to ensure that the assets and financial structure of those entities remain compatible with the level of debt taken on.

Balance sheet covenants include commitments on the part of the borrower company to maintain for the full term of the loan:

- a net balance sheet capital level which is not lower than a specified minimum;

- the ratio of total indebtedness to net capital within a given limit;

- a current liquidity indicator which is not lower than a specified minimum;

- financial charges within a specified percentage limit of turnover.

3.15.2 Financial Covenants

Financial covenants are closely related to the real estate transaction being financed. The following financial ratios are those most commonly used in the aforementioned covenants.

Interest Cover Ratio24 (ICR) is the ratio between the operating income,25 the income gained from the lease and/or sale of the properties, and the amount of interest due to the bank on the loan over the same period.

Depending upon the type of property, this ratio may exceed 120–170%. If the ratio is lower than this, but still higher than 100%, the bank may activate other guarantees, request the provision of equity, or withhold all assigned rental payments (known as a “Cash Sweep” clause26) until the ratios have been re-established. A figure below 100% will result in an event of default, since the interest due on the loan will no longer be covered by the operating income.

Debt Service Cover Ratio (DSCR) is the ratio between the operating cash flows gained from the lease of the properties and the amount of the instalments (principal and interest) due to the bank on the loan over the same period. Depending upon the type of property and the financial structure of the transaction, this ratio must at all times exceed 120–140%. Below this ratio the arrangements applicable to the ICR apply.

Loan to Value Ratio (LTV) is the amount of the loan granted or the residual amount due to the bank as a percentage of the OMV of the property at the time the indicator is calculated. Depending upon the type of property and their risk, this ratio must not exceed 60–80% of the value of the properties (although for mezzanine financing may be as high as 90%); obviously, these percentages vary over time in line with market conditions. In the event that the limit is breached, the borrower must reduce the loan in order to restore the agreed LTV, and if it fails to do so, the bank may terminate the agreement.

Loan to Cost Ratio (LTC) means, at any given time, the amount of the loan granted or the residual amount due to the bank by the borrower as a percentage of the construction cost of the property at the time it was calculated. Depending upon the type of property, this ratio must not exceed 60–70% of the construction cost of the properties (although for mezzanine financing may be as high as 80–85%). In the event that the limit is breached, the borrower must reduce the loan in order to restore the agreed LTC, failing which the bank may terminate the agreement. This ratio is usually used to regulate drawdown amount in construction financing rather than being used as a covenant.

It is a straightforward matter to render changes to the financial terms of the loan conditional upon these ratios: an increase in ICR and/or DSCR and/or a fall in LTV/LTC may result in a reduction in the spread for the transaction (and vice versa).

Yield on Debt means, at any given time, the net rental payments relating to the property financed as a percentage of the amount of the loan due by the borrower to the bank at the same time (Net Operating Income/Loan amount). For bullet financing arrangements, an exit yield on debt clause may be inserted specifying the minimum ratio which must apply upon maturity of the loan (Net Operating Income/Loan amount after … years' loan term).

Project Cover Ratio (PCR) means the present value of cash flows for the entire lifetime of the project as a portion of the present value of the debt. This makes it possible to assess the capacity of the cash flows generated to repay the debt over the entire lifetime of the project, thus also including the period after that stipulated for repayment. In order to be satisfactory it must be higher than 1, and the higher that value, the greater protection will be provided to lenders, given the financial solidity of the project. On the contrary, the borrower will attempt to maintain its value as close to 1 as possible in order to maximize the use of financial leverage.27 However, it is not possible to define a standard absolute value, as the banks also take into account other qualitative factors. Moreover, its significance is limited since the level of this ratio may depend upon the cash flows generated after the repayment period specified in the loan agreement has ended.

Loan Life Cover Ratio (LLCR) means the present value of cash flows between the date of valuation and the deadline for repayment of the debt and the residual (or outstanding) debt on the date of valuation. This ratio will be meaningless before the property has entered its operational stage. However, it is more useful than the previous ratio (PCR) since it focuses its analysis exclusively on the cash flows generated during the period specified for repayment of the loan. This ratio should also be higher than 1 in order to ensure that the loan is repaid in accordance with the repayment plan specified, whilst at the same time leaving funds available to remunerate shareholders.

The last two ratios are predominantly used in infrastructure project finance deals rather than properties.

A simple numerical example describes the procedure for calculating some of the covenants presented above.

The following is an example of a financial covenants clause.