CHAPTER 8

The nuts and bolts of the sharemarket

In addition to decisions about which asset classes — and which assets within these asset classes — you are going to invest in, you also need to navigate the actual buying and selling of these assets. When it comes to shares, that usually means the sharemarket. In this chapter we will take you through the various types of securities and company codes, what the markets for stocks actually look like on the screen and what you can do if you want to transfer shares off-market.

Types of securities

Shares may be one of the simplest financial products in which to invest, but there are different types of shares traded on the ASX, each with different characteristics.

It is important to understand these distinctions because the characteristics of different types of shares can significantly affect the way you decide to invest. The different types of shares include:

- ordinary shares

- preference shares

- trust units

- stapled securities

- partly-paid shares.

Ordinary shares

Most shares traded on the ASX are ‘ordinary’ shares. Ordinary shares carry no special or preferred rights. Holders of ordinary shares usually have the right to vote at a general meeting of the company, and to participate in any dividends or any distribution of assets on winding up of the company on the same basis as other ordinary shareholders.

Preference shares

Preference shares usually give their holder a priority or ‘preference’ over ordinary shareholders to payments of dividends or on winding up of the company. There are different kinds of preference shares with different rights and characteristics. Holders of preference shares usually have voting rights that are restricted to particular circumstances or particular resolutions; however, this will depend on the terms of the shares.

Trust units

Trust units are increasingly popular in the form of property trusts, equity trusts and cash management trusts. While unitholders have less control than shareholders, from an investor’s point of view units in listed trusts are similar to ordinary shares except that, instead of a dividend, a full distribution of profit is made to unitholders.

Stapled securities

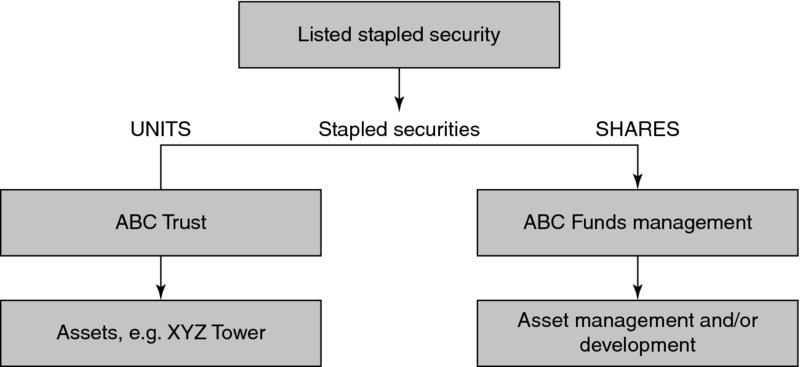

A stapled security is where investors own two or more securities that are generally related and bound together through one vehicle. Typically, stapled securities consist of one trust unit and one share in the funds management company that can’t be traded separately.

The trust holds the portfolio of assets, while the related company carries out the funds management and/or development opportunities. Figure 8.1 shows a typical stapled security structure.

Figure 8.1: an example of a stapled security

Partly-paid shares

Partly-paid shares (also known as contributing shares) are issued without the company requiring payment of the full issue price. These instruments can appeal for things such as infrastructure projects where not all the capital for the project is required at the outset. At a specified future date or dates, the company is entitled to call for all or part of the outstanding issue price, and the shareholder at the time the call is due is legally obliged to pay the call. (No-liability companies are not required to specify the date or dates on which calls will be made, and the shareholder at the time the call is due may pay the call or forfeit the share.)

Partly-paid shares traded on the ASX are usually identified by a five-letter code consisting of the company code and a two-letter suffix, generally CA to CZ (not including CP).

Generally, a holder of a partly-paid share has the same rights as an ordinary shareholder to vote, and to dividends on winding up of the company, but those rights will be proportional to the amount paid on the share (except for a vote by show of hands, where a holder of a partly-paid share has one vote, the same as any ordinary shareholder).

Retail investors are now required to sign a client agreement with their broker before first trading in partly-paid shares, to acknowledge that they understand the risks involved. This requirement was introduced after investors got caught out when they bought partly-paid shares and did not realise they were legally obligated to pay additional contributions when called upon to do so by the issuing company. In some cases the subsequent payments required were significantly higher than the initial outlay and some investors did not have the funds to meet their obligations. This is why much fuller disclosure of the obligations of partly-paid shares is now required.

Rights and bonus issues

Companies can make special issues of rights or bonus shares to shareholders. As a shareholder, it is important to understand what each issue entails and the dates involved. If you have any doubt about such issues, you should contact your adviser.

Bonus issues

Bonus issues are shares issued free of charge to shareholders. Bonus issues are made on a predetermined pro-rata basis — for example, 1-for-5. This means you will receive one new share for every five you own. For example, if a company in which you hold 1000 shares announces a 1-for-10 bonus issue, you are entitled to 100 extra shares at no cost, which would bring your total holding to 1100 shares. Once a bonus is issued, the share price usually drops as the value of the company’s assets is now spread over a larger number of shares. Bonus shares dilute the market price of the shares in direct proportion to the increase in the total number of shares on issue.

This price adjustment occurs on the ex-bonus (XB) date. An investor who buys the existing shares on or after the XB date is not entitled to the bonus shares — they belong to the previous owner of the shares. The closing date is the date on which the company closes its books to determine which shareholders are registered to receive the bonus. Hence it is important for investors to remember the XB date if they are considering buying shares in a company that is offering a bonus issue.

Rights issues

A rights issue entitles existing shareholders to take up additional shares in the company at a below-market price without having to pay brokerage. Rights issues enable the company to raise additional funds from shareholders for expansion or to repay debt. The process for a rights issue is similar to a float insofar as a product disclosure statement is prepared and an underwriter is often appointed. Shares are offered on a predetermined pro-rata basis — for example, one for four. This means that for every four shares you own, you can purchase an additional share at the discounted price.

A rights issue may be renounceable or non-renounceable. Renounceable means shareholders are entitled to sell their rights to other investors on the sharemarket if they do not wish to take up the additional shares themselves. Non-renounceable means only existing shareholders can participate and they must either take up the shares or forfeit the rights. If you are not a shareholder and wish to be, you may be able to purchase renounceable rights from shareholders who did not want to take up the rights and preferred to sell them.

To take up shares in a rights issue the shareholders complete a form and submit a cheque for the number of shares they want. The form is lodged with the company’s share registry, so the transaction is done off-market and does not incur brokerage. Shareholders are not obliged to take up their full allocation.

Companies usually structure the rights issue so that the cost of purchasing new shares is at a slight discount to the market price at the time of issue or alternatively at a discount to a price established at the close of the offer. This makes sense because otherwise shareholders may prefer to just buy the shares on market.

Let’s look at an example.

Assume you own 10 000 XYZ shares and a 1-for-5 renounceable rights issue is made. The shares are currently trading at $10 and the rights offer entitles you to take up additional shares at a price of $9 per share. As you own 10 000 shares you are entitled to purchase up to 2000 additional shares.

If you wanted to buy the full allocation you would send in a cheque for $18 000 ($9 × 2000). If you only wanted 500 shares you would send in a cheque for $4500. If you elected to not take up the offer at all or to apply for less than your full allocation you might consider selling your remaining rights on-market because in this example the rights are renounceable.

It follows that because the new shares are being issued for a price lower than the current market, this will have a diluting effect on the value of the existing shares. The bigger the discount to the current prices of the shares, the greater the dilution effect of the rights issue.

Market announcements

Companies are required to provide a steady stream of information to the market. This assists investors in making informed assessments about the suitability of a particular company’s shares for their portfolio. The market announcements are important to the active investor. Announcements providing information about the prospects of a company and those describing growth strategies by senior company board members or the CEO are of particular use.

The ASX’s continuous disclosure regime is based on the principle that information that may affect share prices or influence investment decisions must be disclosed. Investors can find all market announcements published live and freely available on the ASX website. In general, listed companies must lodge the following with the ASX:

- annual report

- half-yearly report

- preliminary final report

- half-yearly ASIC accounts

- annual audited financial statements lodged with ASIC

- quarterly cash flow report — only required for mining exploration entities and commitments test entities

- quarterly activities report — for mining exploration or production entities

- takeover information

- security holder notifications.

To find out when to expect the routine announcements, such as annual reports, you can refer to the Reporting Calendar available on the ASX website (www.asx.com.au).

Codes, codes and more codes

The massive amount of data communicated via feeds and displayed on screens means there is a need to abbreviate wherever possible. Securities, security types, indices and trading conditions all have codes.

What is a ticker code?

Anything traded on financial markets has an individual code that uniquely identifies it in an abbreviated form. You may be familiar with these codes, which are displayed on ASX ticker boards and are included alongside company names in newspaper sharemarket tables.

Codes uniquely identify a tradeable instrument so that it can be tracked throughout trading, settlement and price reporting systems. These codes are important. Whenever you make an order to buy or sell you will need to know the ASX code for the instrument you want to trade.

ASX sometimes uses a different length of ticker code to indicate to investors and traders that there is something different about a listed product.

A good rule to remember is that a three-character code typically indicates the ordinary shares in a company. Where there are more or fewer than three characters, there is most likely something different from the ordinary shares of a company.

ASX will have regard to certain principles when allocating codes to products that can be found on the ASX website.

How many characters are there in ticker codes?

Initially, all codes were confined to three characters; however, formats have grown considerably due to the number and types of instruments now available for trading. There are far more companies listed these days and there are other markets such as options, warrants and futures that also require codes.

Listed companies — the ASX three-character code

Most ASX listed companies’ codes have three characters. This three-character code represents that company. All securities issued by that company will incorporate its three-character code.

The three-character code is typically used for the primary issue of shares by that company. This is the case for listed companies, A-REITs, listed investment companies, infrastructure funds and conventional exchange traded funds.

Listed companies — secondary issues

A company may issue options that can be exercised for shares traded on-market. For example, an option over XYZ Company may have the code XYZO and a rights issue may use the code XYZR.

The Telstra fully-paid ordinary stock code is TLS; however, at the time of its capital raising through an instalment receipt (IR) structure those instalment receipts traded as TLSCA, indicating that there were differences between Telstra ordinary shares and the instalment receipts.

Special-condition codes

A fourth character that is added to the underlying three-character codes indicates a special circumstance or product type. For example, if ASX undertook a share split, it may trade on a deferred settlement basis for a period. This would be identified by the code ASXDA.

For a partly-paid security where an additional payment of money is required to be made by the holder, the security would be identified by the fourth character, ‘C’; for example, ASXCA.

Listed companies — bonds and hybrids

Listed companies may issue various types of interest-rate securities. These securities have a four-, five- or six-character code. Again, the three-character issuer code will be the prefix, followed by a character to identify the type of security (for example, H: unsecured note; G: convertible note; or P: preference share).

A company may issue a series of a particular type of interest-rate security. In this case it becomes necessary to be able to identify each particular series. Alpha characters are added sequentially to each series as they are issued. For example, WOWHA represents the first unsecured note on issue by Woolworths Limited and CBAPB represents the second preference share issue by the Commonwealth Bank of Australia.

Exchange-traded products (ETPs)

ETPs include exchange-traded funds (ETFs), managed funds and structured products. These products may have three-, four- or six-letter ticker codes.

Share price indices

Share price indices are identifiable by a three-character code. It is useful to remember that the code for the S&P/ASX 200 is XJO and that the prefix XJO is used for all exchange-traded options and warrants over the S&P/ASX 200 index.

Index codes are also used to plot the performance of various indices on a chart. The ASX website provides more information on the various coding conventions as well as a helpful tool for looking up the codes for various companies and financial instruments.

ASX trading hours and market phases

It is helpful to have an understanding of the trading hours and the key market phases because your order will be treated differently depending on when it was entered. For example, if you enter an order before the market opens it will become part of the opening phase, whereas this will not be the case if your order is entered when normal trading has commenced. (These phases are correct as at March 2015 and include bonds, hybrid securities, exchange-traded products and managed funds.)

The market goes through a number of phases on any trading day. The particular market phase determines the type of action that may be taken for an order on ASX Trade (the ASX trading system), which in turn affects how trading is conducted.

Pre-opening phase

Pre-opening takes place from 7 am to 10 am, Sydney time. During pre-opening:

- brokers enter orders into ASX Trade in preparation for the market opening

- investors may enter orders online. The orders are queued according to price–time priority and will not trade until the market opens.

Opening phase

Opening takes place at 10 am Sydney time and lasts for about ten minutes. ASX Trade calculates opening prices during this phase. Securities open in five groups, according to the starting letter of their ASX code:

- Group 1: 10:00:00 am +/− 15 seconds 0–9 and A–B; for example, ANZ, BHP

- Group 2: 10:02:15 am +/− 15 seconds C–F; for example, CPU, FXJ

- Group 3: 10:04:30 am +/− 15 seconds G–M; for example, GPT

- Group 4: 10:06:45 am +/− 15 seconds N–R; for example, QAN

- Group 5: 10:09:00 am +/− 15 seconds S–Z; for example, TLS.

The time is randomly generated by ASX Trade and occurs up to 15 seconds on either side of the times given above; for example, group 1 may open at any time between 9:59:45 am and 10:00:15 am. So, if you are interested in a stock commencing with a ticker code that starts with the letter ‘A’ you can expect an opening price and initial trades to be completed quite soon after 10 am. The further down the alphabet the company’s ticker code is, the longer it will take.

Normal trading

Normal trading takes place from 10 am to 4 pm, Sydney time. Brokers enter orders into ASX Trade and ASX Trade matches the orders against each other in price/time priority on a continuous basis. The vast majority of trades take place during normal trading.

Pre-CSPA

Between 4:00 pm and 4:10 pm, Sydney time, the market is placed in Pre-CSPA. Trading stops and brokers enter, change and cancel orders in preparation for the market closing.

Closing single price auction

The closing single price auction takes place between 4:10 pm and 4:12 pm, Sydney time.

ASX Trade calculates closing prices during this phase. This is important because a lot of calculations are based on closing prices.

Status notes

There are a number of codes used by the trading system to provide further information about the trading status of a security. These codes are known as status notes.

You may not have much interest in these condition codes now, but when you come to buy and sell you will see these codes on screens and you will need to understand what they mean. A complete list is displayed on the ASX website, together with an explanation for each, but here are some key ones.

XD — ex dividend

XD shown against a company’s three-letter ASX code means the security is currently quoted on an ex-dividend basis and that trading in this security does not carry the entitlement to the dividend payment. If there is no code displayed alongside a security, then the security is trading on a cum basis where cum means ‘with’. To be entitled to a dividend you must purchase the share before the ex-dividend date.

XB — ex bonus issue

XB displays for a security from the morning of the ex-bonus date and remains until the close of trading on the bonus issue date. Trading in a security displaying XB does not carry the right to receive the bonus issue. All orders are purged at the end of the trading day prior to the security being quoted on an XB basis.

XC — ex return of capital

XC first displays for a security from the morning of the ex-capital return date and remains until the close of trading on the payment date. Trading in securities displaying XC on the trading system does not carry the entitlement to the return of capital payment. All orders are purged at the end of the trading day prior to the security being quoted on an XC basis.

XI — ex interest

XI first displays for a security from the morning of the ex-interest date and remains until the close of business on the payment date. XI indicates that interest has been paid on the securities. Trading in securities displaying XI does not carry the entitlement to the current interest payment. All orders are purged at the end of the trading day prior to the security being quoted on an XI basis.

XR — ex rights issue

XR first displays for a security from the morning of the ex-rights date and remains until the close of business on the application’s close date. Trading in securities displaying XR does not entitle the holder to receive securities in the rights issue. All orders are purged at the end of the trading day prior to the security being quoted on an XR basis.

Off-market transfers

You do not have to buy or sell your shares on market, although it is by far the most common way. A typical situation where you may not want to transfer via an on-market transaction would be a transfer between family members or transfers from deceased estates. Off-market transfers do not use a stockbroker as the intermediary; instead, the transfer is executed through the use of an Australian standard transfer form. Off-market transfers of securities held on the CHESS sub-register occur electronically through CHESS. The Australian standard transfer form is not required for transfers through CHESS. For this type of transfer you will need to go through your stockbroker.

To obtain an Australian standard transfer form, contact the share registry of the company whose shares you wish to transfer, or go to the Securities Registrars Association of Australia Incorporated website, www.sraa.com.au. For advice on completing the form, consult your stockbroker or financial planner.

Reading share price tables — common terms

In addition to business news about listed companies, many websites and newspapers publish tables of information on share prices, changes in value and volume of trades from the previous ASX trading day. See table 8.1 (overleaf), for example.

Table 8.1: sample per share price

| Quote | 52 week | Dividend | |||||||

| Company name | Last sale price | + or − | Bid | Offer | High | Low | Rate | Yield % | PE ratio |

| AMP Ltd | 5.42 | +7 | 5.41 | 4.420 | 5.96 | 4.11 | 13.00p | 4.37 | 24.19 |

| Ansell Ltd | 22.37 | +2 | 22.37 | 22.39 | 23.00 | 17.73 | 42.00 | 1.87 | 71.86 |

| Argo Invest. | 7.89 | −1 | 7.86 | 7.89 | 8.14 | 7.18 | 28.00f | 3.55 | 26.09 |

| ASX Ltd | 36.67 | −1 | 36.66 | 36.67 | 37.93 | 34.07 | 178.08f | 4.86 | 18.47 |

| BHP Billiton Ltd | 27.36 | −61 | 27.36 | 27.37 | 39.79 | 27.29 | 131.00f | 4.68 | 10.13 |

| Coca-Cola Amatil | 9.14 | +16 | 9.13 | 9.15 | 12.35 | 8.19 | 52.00f | 5.59 | 23.1 |

Let’s have a look at some of the information in the table:

- Bid — the price at which someone is prepared to buy shares.

- Offer — the price at which someone is prepared to sell shares.

- Price range for 52 weeks — the range of prices over the last 52 weeks.

- Dividend rate — the dividend shown as cents per share. This figure may be followed by ‘f’, which means fully franked, or ‘p’, which means it has been partly franked.

- Dividend yield — the dividend shown as a percentage of the last sale price for the shares.

- P/E ratio — the number of times the price covers the earnings per share.

A great deal of information is available via the internet. This includes the ASX’s website, brokers’ websites and listed companies’ websites. Some of the most popular information from these sources is company reports, daily company announcements, historical and current share prices, and company news.

* * *

For many people, the strongest association with the sharemarket is when they hear about movement in the share price index in the evening news. Indices can be a great barometer of how the market is faring, but you need to know what they are measuring and how they measure it.