CHAPTER 25

Employment Taxes

Employment taxes and associated payroll costs, such as workers’ compensation and health insurance, equal between 10 and 25 percent of an exempt organization’s payroll. These taxes represent a substantial expense to most organizations and there is sometimes a temptation to classify a worker as an independent contractor, in order to avoid such costs. Until 1973, exempt organizations (EOs) were exempt from Social Security taxes, and their employees were eligible to be covered only if the organization elected to participate in the system. Until 1989, Internal Revenue Service (IRS) exempt organization examiners had no authority to look at employment taxes. For these reasons, many EOs ignored the complexities of employment taxes, until the IRS announced its intention to emphasize employment tax issues. This posture was particularly costly to many colleges and universities that were assessed payroll tax liabilities in the millions for part-time student workers after mid-1990 IRS audits.

Since 1978, the IRS’s hands have been tied by a congressionally mandated safe harbor that prevents IRS reclassification of workers for an entity that uses some reasonable basis for its policy and files information returns reporting compensation to nonemployees. An organization is presumed to be correct if it relies on IRS precedent, longstanding industry practice, or a prior IRS audit. Generally, exempt organizations have operated under this safe harbor. However, the General Accounting Office and the Treasury Department actively look for ways to enhance collection of income taxes from independent contractors, so these issues are important.

The character of payments made by exempt organizations to individuals—whether employees or independent contractors—is basically governed by the same rules as those applied to nonexempt businesses. There are a few exceptions, but the rules for payroll tax deposits, annual reporting, fringe benefits, and taxability of pensions paid to retirees are mostly the same. If there is any doubt about the importance of employment tax issues to an exempt organization, proof can be found in the tax law changes in recent years. Several provisions enacted at that time affect EO employers.Employer-Provided Educational Assistance

- . IRC §127(a) retroactively extended the tax-free treatment of nongraduate-level educational assistance for up to $5,250 per individual.1

- Medical Research Institution Employee Housing. IRC §119(d)(4)(A) was added to the code to exempt subsidized housing for employees of certain medical research institutions that are classified as §170(b)(1)(a)(iii) organizations.2 This exemption previously applied only to schools.

- Long-Term Care Insurance. Benefits paid under a qualified long-term care contract are treated like payments from an accident and insurance plan and are excluded from income as amounts received for personal injuries and sickness,3 with a cap of $175 per day. Payments for such plans, effective in 1997, are deductible as medical expenses.4

- Health Insurance Portability. Group health plans, including health maintenance organizations (HMOs) covering two or more persons, must contain provisions intended to enhance continued coverage for employees who change jobs and those with preexisting conditions.5 Governmental, accident, dental or vision, Medicare supplement, disability income, liability, and certain other insurance plans are not covered.

25.1 Distinctions Between Employees and Independent Contractors

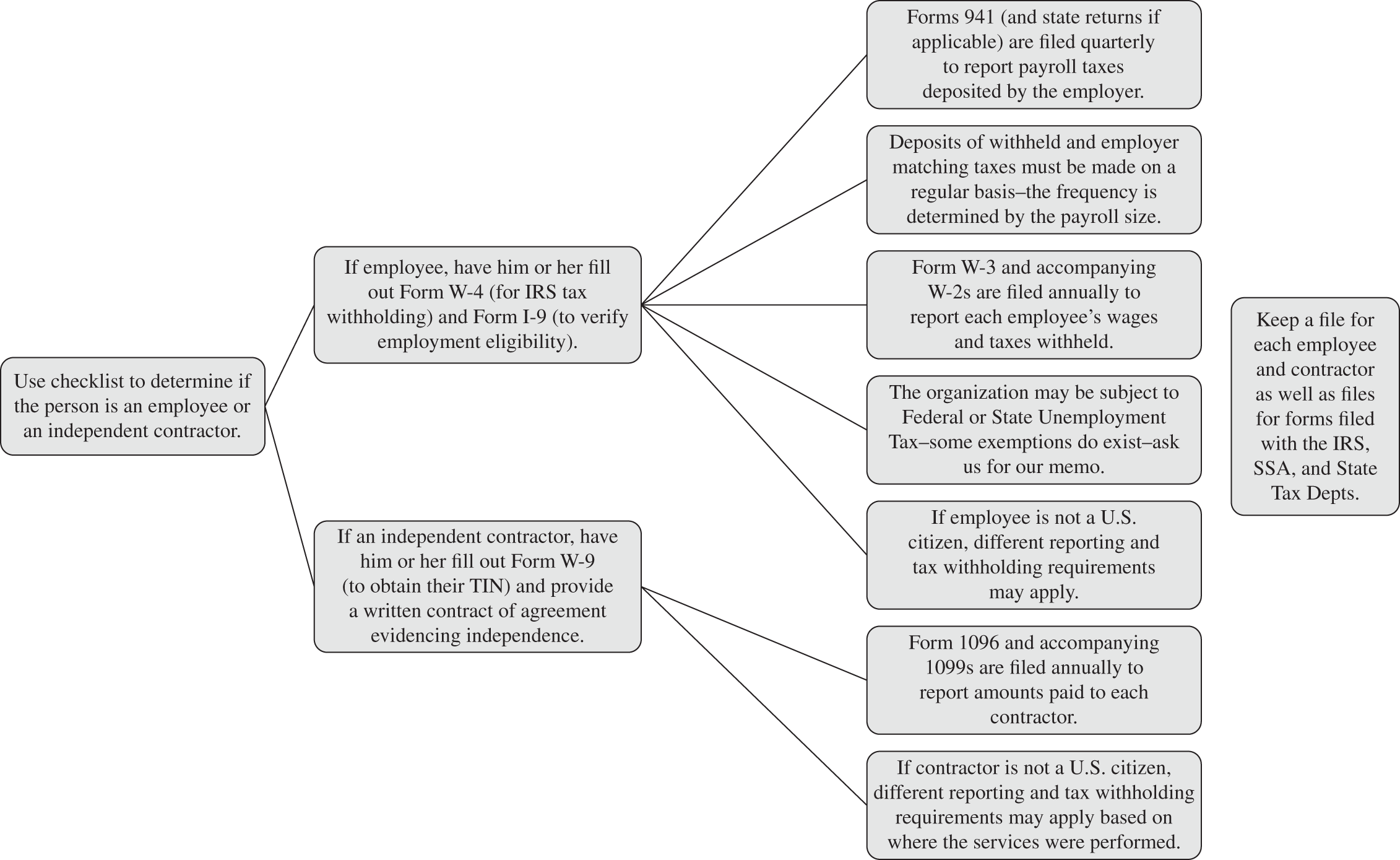

Whether a worker is an employee or an independent contractor is a factual question based on common law, which often requires a detailed analysis. The case law and rulings provide some guidance, and the IRS has developed a 20-factor test.6 IRS Form SS-8, Determination of Employee Work Status, and Exhibits 25.1 and 25.2 reflect these factors. The IRS announced a voluntary worker classification settlement program from September 2011 to 2013 that allowed relief from payment of certain past payroll tax obligations.

(a) Employees

Employees are typically subject to tighter employer controls than independent contractors are: Hours of work are regular and specified; the place of work is the employer’s; compensation is regular and continuing; and tools, training, and work supplies are normally furnished by the employer, among other benefits and advantages. Employees are given paid vacations and accrue pension and sick pay benefits, and are generally thought to have a more secure position than independent contractors.

The term contract worker is often misleading. Typically, workers hired on a part-time or temporary basis are given this title, and are often not treated as employees, partly because they are not given certain advantages of employees. Nonetheless, the fact that a worker is not hired for a permanent position does not determine his or her status as an employee, and most contract workers are employees subject to withholding.

(b) Independent Contractors

As the title implies, independent contractors work when they please, use their own tools, have independent professional standing, and bear a risk of loss if the job is not completed satisfactorily or within the prescribed time. Outside accountants, computer consultants, fund-raising advisors, and consulting psychologists are examples of independent workers.7 No vacation or sick pay is provided, no taxes are withheld, pension eligibility is not furnished, and the engagement is for a limited time period for a specific task.

Form SS-8 should be completed to evidence the status of each worker treated as a contractor. This form can be used to show that the organization made a good-faith effort to determine a worker’s proper classification. The form’s length and the variety of criteria developed by the IRS indicate the subjective nature of the distinction and the difficulty that may occur in identifying the proper category for a worker.

EXHIBIT 25.1 Flowchart: Employees versus Independent Contractors

EXHIBIT 25.2 Employee versus Independent Contractor IRS Checklist

| Revenue Ruling 87-41 lists the primary characteristics distinguishing employees from independent contractors. These characteristics are listed on this checklist. Whichever blank best describes the predominant characteristic of a worker or position is to be checked. There is no specific mathematical test, although more than one-half of the checkmarks on either line is a strong indication. The facts and circumstances of each payee–payor relationship should be analyzed. Classifying a worker as an employee is seldom challenged; finding justification for treating one as independent is more troublesome. The most common reason for making the distinction is to identify persons—the employees—who are subject to federal income tax withholding and unemployment taxes. Independent contractors are abbreviated as ICs. | ||

| INSTRUCTION AND TRAINING | Yes | No |

| Employees are required to comply with instructions as to when, where, and how work is performed, and their training is provided either by formal program or work supervision. | ||

| ICs are free to perform work according to their own professional standards, use their own methods, and receive no training from purchasers of their services. | ||

| PAYMENT TERMS | ||

| Employees are paid by the hour, week, or month on a regular, indefinite, and continuous basis. Employees’ business expenses are paid. Fringe benefits are usually provided. | ||

| ICs are often paid by the engagement with a fee calculated without regard to time spent. ICs are not paid for excess time to perform the task nor given paid vacation or sick leave. ICs pay their own expenses. | ||

| ENGAGEMENT TERMS | ||

| Employer has the right to discharge an employee; control is exercised with threat of dismissal. Employees have the right to quit without incurring liability. | ||

| ICs complete the agreed task without regard to the time it takes and may suffer damages if work is not performed as contracted. | ||

| RELATION TO ENTITY | ||

| Employees’ services are an integral part of the ongoing success and continuation of the organization. Services are rendered personally by employees, who work only for, have loyalty to, and do not compete with the employer. Employees are bonded and provided workers’ compensation. | ||

| ICs consult on a per-job, limited-term, or special-project basis. ICs can hire and pay assistants to perform the work. ICs’ services are available to others on a regular basis. Some ICs work under a company name. | ||

| WORKPLACE AND HOURS | ||

| Employees work on business premises or are physically directed and supervised by employer. Hours of work are established by employer. | ||

| ICs often work at their own places of business, and usually set their own time for performing work. | ||

| INVESTMENT | ||

| Employees are dependent on employer for tools and facilities, and usually make no investment in the job. Employees bear no risk of loss for financial costs of employer. | ||

| ICs buy their own tools, hire workers, pay licensing fees, and are responsible for costs of engagement. ICs bear the financial risk of losing money. | ||

EXHIBIT 25.3 Sample Contractor Engagement Letter

This letter is intended to serve only to provide suggestions. Qualified legal assistance may be required.

In consideration of payment to _________ (name of contractor)

Fixed fee or

Hourly rate $_________ per hour times _________ hours = _________

Reimbursable expenses (describe nature and estimated cost):

____________________________________________________

____________________________________________________

____________________________________________________

Invoices for services will be issued monthly, along with receipts and other documentation for reimbursable expenses listed above. For consideration, we (I) agree to perform the following services:

We (I) agree to perform the specified services in good order in a timely fashion. We (I) are independent contractors, not employees or agents of _______, and are responsible for all federal and state payroll taxes and insurance in connection with this engagement. This agreement may be terminated by either party at any time after payment for any unpaid charges for services rendered up to termination. In acknowledgment of our understandings, we have both signed below.

By: _________ Date: _________ By: _________ Date: _________

Name of Contractor __________ Name of Organization ___________

The terms of engagement should validate a worker’s status as an independent contractor. At the minimum, three important documents evidence the arrangement and prove that the person is not an employee:

- A contract or other type of engagement letter with the contractor (see Exhibit 25.3) describing the respective responsibilities and terms of the contract, including three important elements:

- The engaging company does not essentially control the work product of the independent contractor.

- The contractor’s engagement can be terminated if the work is not performed to specifications and all obligations are not met.

- The contractor has the right to hire and fire assistants.

- A signed Form W-9 is obtained to show that the contractor claims exemption from withholding and that the organization is not responsible for backup withholding. This step also obtains the federal identification number for purposes of preparing Forms 1099.

- An invoice or periodic billing statement evidences the independence of the contractor. The billing should appear professional and support the organization’s position that the worker is independent.

(c) Employee Benefits

Payments made on behalf of employees for fringe benefits, expense reimbursements, and deferred compensation are, as a general rule, not taxed to employees. The rules governing the taxability of such payments are the same as for employees working for nonexempt entities. For example, an exempt organization employee’s car allowance is reportable on Form W-2 unless the employee submits an accounting for the mileage reimbursement.

An exempt organization can adopt a cafeteria plan to provide day care, tuition, and other benefits.8 Health insurance and medical reimbursement plans can be established for employees.9 Most types of qualified pension plans, including defined benefit, defined contribution, thrift, 401(k) plan, and simplified employee plans (SEPs), can be provided for exempt organization employees. A §403(b) plan can also be adopted by a (c)(3) organization. Special limitations are placed on deferred compensation arrangements.10 A thorough discussion of pension benefits is beyond the scope of this book.

(d) Volunteer Fringe Benefits

An exempt organization may pay certain expenses on behalf of its volunteers, and may reimburse its volunteers for expenses they incur on behalf of the organization in conducting its projects. After some years of question, the regulations provide that an exempt organization volunteer who performs services (including services as a director) for an organization or for a federal, state, or local governmental unit, is deemed to have a profit motive for purposes of IRC §162.11 This means that such expenses, up to the value of services rendered, are not taxable to the individual volunteer and are not reportable by the organization as compensation. Of particular importance to some exempt organizations, this rule applies to officer and director liability insurance and indemnification. Payment of premiums previously had to be reported as compensation to the officers, directors, and volunteers.

(e) Fellowships, Scholarships, and Awards

Although it seems incongruous with the motivation for making grants to individuals, certain individual grants must be reported to the IRS on Form 1099 or Form W-2, and taxes must be withheld, as the following discussion outlines.

Tuition and Fees. A scholarship grant is fragmented into two parts. The portion awarded for payment of tuition and related expenses required for enrollment in an educational institution (such as books, fees, supplies, and equipment) is not taxable to the recipient, nor is it reportable to the IRS by the organization. Such payments are called qualified scholarship payments and are specifically excluded from gross income of a person who is a candidate for a degree.12

IRC §6050S requires reporting of tuition payments by schools. The information reporting requirements were designed to aid in calculating the HOPE Scholarship and Lifetime Learning credits under IRC §25A.

Room and Board. Payments for room, board, travel, and any other expenses may be includable in income after the 1986 Tax Reform Act. However, such taxable payments are not reportable to the IRS as income unless they represent compensation.13 The 2003 instructions to Form 1099 clearly state, “DO NOT use this form to report scholarship or fellowship grants.” They go on to say, “Other taxable scholarship or fellowship payments do not have to be reported to the IRS on any form, unless section 6050S requires reporting of such amounts by an educational institution on Form 1098-T, Tuition Statement. See section 117(b)–(d) not required to be reported by you to the IRS on any form.”14

Teaching Fellows and Other Student Workers . For income tax purposes, scholarships or fellowships paid on the condition that recipients teach, perform research, or provide other services for the institution granting the scholarship do produce taxable income.15 Such income is considered to be wages reportable on Form W-2, even though students are eligible to claim an exemption from income tax withholding.16

Social Security taxes may or may not have to be withheld, matched, and paid for amounts paid to students for work performed for colleges they attend. Students receiving payments from a state or federal agency that does not participate in the Social Security system are not subject to FICA. IRC §3121(b)(10) provides what is referred to as a Student FICA exception, which exempts payments for employment services to a student who is enrolled and regularly attends classes at a school, college, or university (whether or not it is tax-exempt), or an affiliated organization of such an institution. The regulations somewhat vaguely say that a student performing services incident to and for the purpose of pursuing a course of study at a school, college, or university qualifies. After significant controversies during examinations of colleges and universities, the IRS established specific standards.17 The ruling contains a series of questions designed to provide answers to schools employing students eligible for exclusion from the FICA tax.

To qualify for the exemption, the student must be a part-time undergraduate or professional student as those terms are defined by the Department of Education. Services for career employees, postdoctoral students and fellows, and medical residents and interns do not qualify. The definitions contained in the procedure should be carefully studied by any institution exempting students from FICA withholding. The IRS previously had taken the position that a student had to take 12 credits of courses and work less than 20 hours a week to be qualified for the exemption.

Awards. Prizes or awards paid to recognize someone’s accomplishment are taxable to the recipient and reported on Form 1099-MISC. Only if the money is paid by the recipient to a charitable organization does the award escape taxation.18 See discussion in §25.3(f) regarding raffles and gaming awards.

Disaster relief payments, defined as an amount paid by a federal, s, or local government, or agency or instrumentality thereof, in connection with a qualified disaster in order to promote the general welfare,19 are not treated as taxable income.

Medical Residents. Imposition of FICA tax on medical residents was a controversial subject for several years. The issue was whether the services they performed were incident to pursuing a course of study. The IRS said, “We believe that medical residents are engaged in a structured form of on-the-job training.”20 The IRS denied hundreds of applications for refund of FICA tax imposed on medical residents. The Mayo Clinic took the battle to court and initially convinced a court that it was an institution of higher education, that residents regularly attended classes, and that the patient care they provided was incident to, and for the purpose of, pursuing their medical education.21 The IRS response came in April 2005 with the issuance of regulations defining a school, college, or university as an institution with a primary function of formal instruction. An individual who works 40 or more hours is an employee, not a student, even if the work has an educational component. In view of the court decisions against them, the IRS honored timely filed refund claims for FICA withheld and paid before the effective date of the regulations. The Supreme Court settled the argument in 2011 because of “a reasonable distinction between students who work and workers who study.”

Foreign Grant Recipients. For foreign grantees, the portion of a scholarship grant paid for study, training, or research in the United States (not including tuition and fees) is also taxable. As a general rule, income tax must be withheld at the rate of 14 percent on the taxable portion.22 Tax withholding generally is not required on funds granted to a foreign organization or individual for programs to be conducted outside of the United States.23 If the U.S. organization expects no services or goods to be provided in return, its payment may not be considered compensatory.24 The IRS ruled that no withholding was required in a situation where a portion of its funding would be spent by the foreign recipient to attend conferences and seminars in the United States.25 Treaties may exempt certain of these payments. A withholding agent may not give a treaty benefit to anyone who does not have an individual taxpayer identification number. Forms W-8 and 8233 have been redesigned to meet the needs of organizations making payments of compensation or scholarships to foreigners. Additionally, the rules applicable to U.S. residents for travel and expense reimbursements can be followed for nonresidents; if accounted for, the payments are not reportable compensation. After a number of years of controversy, the withholding requirements for foreign grant recipients are determined by the situs or residence of the person or organization making the payment, in addition to the residence of the recipient.26 In two circumstances, fellowship or scholarship payments are not subject to withholding:

- The payor is a U.S.-based citizen, domestic partnership, or corporation, a state, or a federal agency, and payment is made to a non-U.S. person for study pursued outside the United States.

- The payment is made for study within the United States by a foreign government, international organization, or person other than a U.S. citizen.

The regulations specifically say that this rule does not apply to salary or other compensation for services, but does apply to prizes and awards for artistic, scientific, or charitable achievements. Reporting requirements are outlined in §25.3(d). IRS Publication 515, Withholding of Tax of Nonresident Aliens and Foreign Corporations, reflects withholding rates and tax treaty provisions for this purpose.

25.2 Ministers

Duly ordained ministers of a church hold a special place in employment tax procedures. The clergy of some sects take vows of poverty and, as a matter of religious conscience, take no compensation for their work. The procedures for reporting compensation of ministers evolved to respect the separation of church and state in recognition of the status of churches in American society and of their rights guaranteed by the First Amendment to the U.S. Constitution.

(a) Who Is a Minister?

The term minister is defined in the Internal Revenue Code and Regulations by a job description. Services provided by a minister in the exercise of his or her ministries include:27

- Ministration of sacerdotal functions (marriage, baptism, funerals, and similar services).

- Conduct of religious worship.

- Conduct, control, and maintenance of religious organizations, including religious board, societies, and other integral agencies of such organizations (such as schools).

- Performance of teaching and administrative duties at theological seminaries.

A minister need not be ordained and may be commissioned, licensed, appointed, or otherwise authorized by a religious organization. The important criterion is that the minister must perform religious duties within the scope and practices of a religious denomination.28 Interestingly, these standards use the term religious organization, not church, although the criteria for defining organizations performing the foregoing functions apply to churches and their integrated auxiliaries for exempt-status purposes.29 Qualifying ministers have also included a probationary member of the United Methodist Church,30 cantors of the Jewish faith,31 and retired ministers.32 Not qualifying as ministers are chaplains not employed by a religious organization or its integral auxiliary. Ministers do not include chaplains employed to teach at a university,33 employed at a human-services organization34 or the Veterans Administration,35 or chaplains in the Armed Services (chaplains are commissioned officers).36

Importantly, employees of a church, other than qualified ministers, are subject to the rules discussed in §25.1. For instance, failure to follow the employment tax rules for its personnel resulted in a $3.5 million assessment against the Indianapolis Baptist Temple.37

(b) How Ministers Are Special

Ministers are exempt from income tax and Social Security tax withholding,38 and a portion of the compensation for services they perform as a minister may not be subject to income and the self-employment tax in the situations discussed in this section. Whether the minister is subject to one or both of these taxes, the compensation is considered to be attributable to the carrying-on of a trade or business,39 which permits the deduction of ordinary and necessary expenses in arriving at taxable income for both income (as an itemized deduction for employees) and self-employment purposes.40 A 42-page Tax Guide for Churches and Religious Organizations is available on the IRS website.41 Payroll tax reporting issues unique to ministers are explained, with a reminder that most church workers are normal employees subject to withholding and other rules outlined in this chapter. Ministers are accorded tax benefits for income, Social Security, and Medicare taxes, as previously discussed. These special rules present several potential examination issues on ministers’ tax returns in addition to the income and expenses issues found in most examinations.

Income Tax. Any amounts paid as compensation to a minister for services are subject to income tax, just as for other individual taxpayers. Offerings and fees received for marriages, baptisms, funerals, and the like are taxable income. Ministers are classified as employees or independent contractors by applying the standards listed in §25.1. If the minister is classified as an employee, the income tax liability is paid either through the estimated tax system or through voluntary income tax withholding. An employed minister receives Form W-2, in most cases reflecting only the gross wage amount. If the minister is not an employee, the tax is paid individually through the estimated income tax system, and the church reports the compensation on Forms 1099.

The taxability of “gifts” to ministers from grateful followers are determined by the intention of the giver. The IRS says, “The value of property acquired by gift is excluded from gross income if it:42

- Comes from a detached and disinterested generosity;

- Is made out of affection, respect, admiration, charity, or like impulses;

- Is not made from any moral or legal duty, nor from the incentive of anticipated benefit of an economic nature;

- Is not in return for services rendered.”

In one instance, a minister who solicited funds on a radio program had to report the contributions as income because the contributions were not gifts, but instead were given to continue hearing the minister’s message on the radio program.43 Similarly, a minister was required to include in income substantial cash gifts he received on three “special occasions” each year that congregation leaders collected from individual church members who contributed anonymously. The congregation funds the church, including the minister’s salary. The special-occasion gifts were substantial compared to the minister’s annual salary. The congregation, collectively, knew that without these substantial, ongoing cash payments, the church likely could not retain the services of a popular and successful minister at the relatively low salary it was paying.44

Self-Employment Tax. A minister’s earnings are excepted from “employment” for the purpose of imposing the Social Security tax.45 A minister is instead subject to the self-employment tax, unless he or she is one of the following persons:46

- Member of a religious order whose members have taken vows of poverty.47

- Duly ordained minister who has not taken a vow of poverty but who makes an individual election out of the Social Security system on Form 4361. A statement must be signed indicating that the minister is opposed by conscience or religious principle to the acceptance of any public insurance and is so informing his or her church.

- Clergy member of a church or church-controlled organization that makes the election for its employees to be exempt from Social Security coverage pursuant to IRC §3121(w). This exemption applies only to remuneration of less than $100 per year and generally applies to “vow of poverty” situations.

In some instances, the independent contractor rules have been applied to find that a minister was an employee and not self-employed for purposes of claiming business expense deductions on Schedule C.48

A claim to be a minister exempt from self-employment taxes, when activities producing profits are promotion of abusive tax arrangements, was correctly denied by the Tax Court.49

Housing Allowances. Amounts designated by a church as housing allowances for its ministers are not taxable for income tax purposes,50 but are subject to self-employment tax. The allowance must be designated in advance of its payment or provision, as evidenced by an employment contract, church budget, deacons’ resolution, or similar official action. The minister must expend the amount provided. Any allowance not used or used for nonresidential purposes is taxed.51 The taxable amount is equal to the fair rental value of housing (including utilities and other costs). A parsonage may be furnished rent-free, or allowances may be paid to cover the parsonage utilities and other maintenance, or to cover rents, or to cover the minister’s costs of individually owning and maintaining a house. A minister with a principal residence and a lake home was only allowed the tax-free allowance for a single home.52

The Freedom from Religion Foundation, an atheist organization, argued successfully in a Wisconsin district court that the housing allowance exemption for ministers was unconstitutional.53 The Seventh Circuit Court of Appeals reversed the decision and held that the §107(2) exclusion for clergy housing (“parsonage”) allowance is constitutional. It held that the tax code does not violate the Establishment Clause of the U.S. Constitution.54

(c) Conscientious Objectors

As noted previously, a minister may make an individual election not to participate in the Social Security system by filing Form 4361, Application for Exemption from Self-Employment Tax for Use by Ministers, Members of Religious Orders and Christian Science Practitioners. A minister is, however, subject to income tax on compensation paid for services he or she renders that is not otherwise excluded as a fringe benefit. Some religious organizations, peace groups, and other exempt organizations employ persons who protest payments of federal income taxes for spiritual reasons. These conscientious objectors have traditionally objected to money allocated to armaments that bring harm to human beings caused by war or to government-supported abortions. How should an organization respond if it is asked not to levy taxes against such an employee? What is the responsibility of the organization to the IRS? The IRS holds the exempt organization responsible, but may use some leniency.

The Quakers produced answers to some of these questions when they faced a federal district court in December 1990. The judges decided that the collection of taxes applied to all citizens, and did not specifically regulate religious practice or beliefs. The church was therefore required to withhold the full amount of taxes from its regular employees’ wages. Out of deference to the church’s exercise of religious freedom, however, the court imposed no penalties for failure to withhold the taxes in question.55

25.3 Reporting Requirements

Whether paid to employees or individual contractors, almost all payments made by exempt organizations to individuals or unincorporated entities are reportable to the IRS. The annual Form W-2 is filed for employees. The Form 1099, Miscellaneous (also called an information return), is filed for most other payments to independent contractors and other nonemployees. Exhibit 25.4 is used to facilitate annual compliance review.

(a) Penalties

The penalty for failure to file an information return is $250 per return, up to a maximum of $1,000,000 for an organization with gross receipts of not more than $175,000 or $3,000,000 when receipts exceed $5,000,000.56 The fee for a correction of the failure made within 30 days of its due date is $250.

When the IRS determines that a contractor should have been classified as an employee, the exempt organization will be billed for all employment taxes that would have been payable if the worker had been classified as an employee, plus interest and penalties. Before 1997, responsible parties, starting with the board members, were assessed a penalty up to 100 percent of this amount for failure to withhold the taxes. Congress followed the lead of the many states that encourage board service by allowing a degree of immunity from penalties for volunteers serving on nonprofit organization boards. IRC §6672 contains an important exception from the penalties for failure to collect and pay employment taxes for an unpaid, volunteer member of a board or a trustee or director of a tax-exempt organization that possesses the following characteristics:57

- Is serving solely in an honorary capacity.

- Does not participate in the day-to-day or financial operations of the organization.

- Does not have actual knowledge of the failure on which such penalty is imposed.

(b) Tax Withholding Requirements

An exempt organization is subject to the income and Social Security tax withholding system for most of its employees.58 An individual paid less than $100 is only subject to income tax withholding, not to Social Security tax withholding. Special rules apply to ministers and foreigners, as discussed previously, and in the special circumstances discussed later in this section.

(c) Unemployment Tax

Only charitable organizations classified as exempt under IRC §501(c)(3) are exempt from the federal unemployment tax; all other exempt organizations are subject to such tax. Exemptions may be available in some states. For example, in Texas the following state exemptions apply:

- Charities with fewer than four employees are not subject to the tax.

- A charity may elect to be a reimbursing employer by agreeing to directly pay any benefits that may come due as employee claims are made.

(d) Backup Withholding

The backup withholding system allows the U.S. Treasury to collect funds up front from independent contractors who potentially will not pay their taxes. Form W-9, Request for Taxpayer Identification Number and Certification, is furnished by organizations to payment recipients. This is the same form used by banks and stockbrokers to ask individuals to verify their federal identification numbers and to claim exemption from backup withholding.

Unless the organization receives a signed W-9 reflecting a Social Security number from nonemployees receiving payments for services and from individuals receiving taxable grant or fellowship payments, income tax at the rate of 22% for 2020 must be withheld from the payments.59 Absent completion of Form W-9, or when there is some reason to believe that the Social Security number furnished is incorrect, a flat 24 percent of the amounts paid must be withheld and remitted. The system is designed to cause the organization to collect the tax if the individual is unable or unlikely to do so.

The Institute of International Education reported that 547,867 non-U.S. citizens were studying in the United States during the academic year 2000–2001. Dizzying arrays of tax treaties allow different exemptions and exceptions and impose significantly different tax burdens on foreign students.60

EXHIBIT 25.4 Employer Tax Requirements Checklist

| Nonprofit organization employers are subject to the same rules that govern for-profit employers, including rules administered by the Department of Labor, workers’ compensation statutes, the Employee Retirement Insurance Security Act (ERISA) rules, and federal and state employment taxes. Because the costs of employee benefits range from 10 to 30 percent of direct payroll costs, these matters deserve close attention. Severe penalties in the Internal Revenue Code are imposed on failure to pay over employment taxes. | |

| 1. Does the organization have a policy for distinguishing between employees and independent contractors? | |

| • Verify satisfaction of at least four factors in Exhibit 25.2, Employee versus Independent Contractor IRS Checklist. | |

| • Review questions on Form SS-8, Information for Use in Determining Whether a Worker Is an Employee for Federal Employment Taxes and Income Tax Withholding. | |

| • Does the organization have a contract and a signed Form W-9 for independent contractors? [See Exhibit 25.3.] | |

| • Have Social Security numbers been secured? | |

| • Are invoices obtained from independent contractors to prove their professionalism? | |

| 2. Are meals, cars, tuition, or housing allowances furnished to employees? Determine whether they are reportable compensation and whether withholding is required. | |

| 3. Does the pension plan adhere to ERISA rules? | |

| 4. Is Form 5500, 5500C, or 5500R required for an employee plan? | |

| 5. Are the terms of any qualified or nonqualified deferred compensation plan being adhered to? | |

| 6. Do Consolidated Omnibus Budget Reconciliation Act (COBRA) rules entitle former employees to continued medical benefit coverage? | |

| 7. Is workers’ compensation coverage required? | |

| 8. Verify adherence to federal withholding requirements. Study IRS Circular E, Employer’s Tax Guide, and Publication 15-A for filing requirements and an excellent chart on wages subject to or exempt from taxes. The types of employment taxes are as follows: | |

| • Income tax withholding. Most wages are subject to this tax, but certain ministers, members of religious orders, student workers, and fellowship or grant recipients are exempt. | |

| • Social Security tax. Review Circular E chart; wages >$100 are taxable. | |

| • Federal unemployment tax. §501(c)(3) organizations are exempt from this tax. Several types of compensation subject to income tax are also exempt. See Circular E. | |

| 9. Verify timely filing of the following IRS reports: | |

| • Form 940, federal unemployment tax report (due January 31) (Form 940 is not filed by §501(c)(3) organizations) | |

| • Form 941, employer’s quarterly federal tax return (due January 31, April 30, July 31, and October 31) | |

| • W-2 Forms for all employees (due January 31) | |

| • W-3 Form to IRS with copies of W-2s (due February 28) | |

| • W-4 placed in each employee’s file | |

| • Form 1099-MISC for all independent contractors | |

| • Form W-2G, Prizes and Awards | |

| • Form W-2P, Statement for Recipients of Pensions | |

| 10. Verify timely deposit of federal employment taxes. | |

| • Taxes deposited by fifteenth of next month following wage payment. | |

| • Tax deposited biweekly for employers whose tax for prior year exceeded $50,000. | |

| • Tax deposited electronically. | |

| 11. Is the exempt organization subject to unemployment taxes? | |

| • On the federal level, only 501(c)(3)s are exempt. | |

| • On the state level, obtain instructions from the employment commission of the state where the worker is employed. The rules differ by state. | |

| • Many states exempt 501(c)(3) EOs with fewer than four employees. | |

| • A reimbursing or self-insured employer status may be available. | |

| 12. Are state employment (workforce) commission requirements satisfied? | |

| • Are quarterly returns filed and is tax paid on time? | |

| • New organizations must first obtain an account number by filing a status report. | |

| 13. Verify timely payment of federal unemployment tax liability (if applicable). | |

Nonresident Aliens. Reporting and withholding requirements for nonresident aliens depend on the alien’s visa status, the existence of a treaty between the alien’s home country and the United States, and the character of the payments the alien receives. The IRS has a Foreign Payments Division to coordinate enforcement issues related to this complicated subject. After some years of confusion and controversy, the IRS wrote regulations governing these withholding requirements under IRC §1441.61 An organization making such payments should obtain information by calling 800-829-4933, or go to irs.gov/eo for “Help with International Taxpayer Questions”.

(e) Payroll Depository Requirements

Nonprofits with tight cash flows are sometimes tempted to pay the employees the net amount of salary (less taxes) and use the tax money to pay the rent or some other pressing expense. However, the amounts withheld from an employee’s salary are held in trust on behalf of the employee, so the money does not belong to the organization. The penalties for failure to pay over such taxes are steep. Taxes withheld are due to be deposited in as few as three days from the date wages are paid.

The deadline for paying withheld employment taxes to the IRS varies according to the amount of the payroll tax liability. The current version of IRS Publication 15-A, Employer’s Supplemental Tax Guide, should be studied because the rules may change from year to year. All taxes must be deposited electronically.

(f) Withholding for Bingo, Raffles, and Other Contests

Income taxes are imposed on gambling winnings, including prizes of all sorts won in a raffle, sweepstakes, lottery, or other contest. The rules for exempt organizations are the same as those for nonexempts.62 A serious trap for the unsuspecting exempt is the withholding requirement placed on an organization (exempt or nonexempt) awarding any prize with a value in excess of $5,000. Form W-2G is due to be filed reporting the winnings. See Exhibit 24.3 for a checklist on this subject.

(g) Form 1099-INT

Interest income must be imputed for a no- or low-interest loan to a charity exceeding $250,000.63 Such interest must be reported as paid by the charity to the lender on Form 1099. Correspondingly, the charity should issue a donation acknowledgment to the lender to disclose the gift of the imputed interest. On the donor’s side, the reporting of the income, combined with an itemized deduction for the gift of interest, does not always result in new taxable income of zero.64

Notes

- 1 Small Business Job Protection Act §1202.

- 2 Small Business Job Protection Act §1123.

- 3 IRC §§106(c), 125(f), 807(d)(3)(A)(iii), and 4980B(g)(2); Health Insurance Portability and Accountability Act §321.

- 4 IRC §§162(1) and 213(d)(1)(C); Health Insurance Portability and Accountability Act §401. See Gaylor v. Lew, 119 AFTR2d 2017-515 (C.D. Wis. 2017); Gaylor v. Mnuchin, 120 AFTR2d 2017-6128, 6532 (C.D. Wis. 2017); and Alliance Defending Freedom v. IRS, 120 AFTR2d 2017-5924 (C.D. Colo. 2017).

- 5 IRC §§9801-9806 and 4980B(f).

- 6 Reg. §§31.3401(c)-1(a) and (d); Rev. Rul. 87-41, 1987-1 C.B. 296, distinguished by Priv. Ltr. Rul. 8908033. Also see Priv. Ltr. Rul. 201251024.

- 7 See Priv. Ltr. Rul. 9231011 regarding a part-time grant proposal writer and Priv. Ltr. Rul. 9227025 about a food bank manager—both deemed employees.

- 8 IRC §125.

- 9 IRC §106.

- 10 IRC §457.

- 11 Reg. §1.132-5.

- 12 IRC §117.

- 13 Prop. Reg. §6041-3(q).

- 14 See IRC §§117(b)-(d) and IRS Notice 87-31, 1987-1 C.B. 475.

- 15 IRC §117(c).

- 16 Reg. §1.117-6(d)(4); it is presumed a student’s earnings will not exceed the minimum standard deduction.

- 17 Rev. Proc. 98-16, 1998-5 IRB 19; superseded by Rev. Proc. 2005-11, 2005-1 C.B. 307 (regarding student FICA withholding under §3121(b)(10)).

- 18 IRC §74.

- 19 IRC §139. See Publication 3833, Disaster Relief: Providing Assistance Through Charitable Organizations.

- 20 IRS Internal Legal Memorandum 200212029.

- 21 Mayo Foundation for Medical Education and Research v. U.S., USTC 50,143, AFTR2d 2011-341 (2011), aff’d, 103 AFTR2d 675 (8th Cir.), aff’d, USTC 50,143 (Sup. Ct. 2011.

- 22 IRC §1441(b)(1).

- 23 There could be local tax issues in certain foreign jurisdictions.

- 24 Rev. Rul. 2003-12, 2003-1 C.B. 283; see §24.1(a) for definition of a donation.

- 25 Priv. Ltr. Rul. 200529004.

- 26 Reg. §1.863-1(d), effective August 25, 1995.

- 27 Reg. §1.1402(c)-5(b)(2).

- 28 Rev. Rul. 78-301, 1978-2 C.B. 103.

- 29 See §3.2.

- 30 Wingo v. Commissioner, 89 T.C. 922 (1989).

- 31 Rev. Rul. 78-301, 1978-2 C.B. 103; Silverman v. Commissioner, 73-2 USTC 9546 (8th Cir. 1973), aff’d, 57 T.C. 727 (1978).

- 32 Rev. Rul. 63-156, 1963-2 C.B. 79. See also Priv. Ltr. Rul. 9221025.

- 33 Boyer v. Commissioner, 69 T.C. 521 (1977).

- 34 Rev. Rul. 68-68, 1968-1 C.B. 51.

- 35 Rev. Rul. 72-462, 1972-2 C.B. 76.

- 36 Reg. §1.107-1(a).

- 37 The church lost its battle in court to claim that its First Amendment religious liberties were violated by the employment taxes. U.S. v. Indianapolis Baptist Temple, 224 F.3d 627 (7th Cir. 2000).

- 38 Reg. §31.3401(a)(9)-1; IRS Publication 15-A, Supplement to Circular E, Employer’s Supplemental Tax Guide.

- 39 IRC §1402(c)(2)(D).

- 40 Rev. Rul. 80-110, 1980-16 IRB 10.

- 41 www.irs.gov; as of September 18, 2019, Pub. 1828 was last updated in August 2015.

- 42 See §24.1(a) and Commissioner v. Duberstein, 363 U.S. 278, 285-286 (1960).

- 43 Webber v. Commissioner, 219 F.2d 834 (10th Cir. 1955).

- 44 Goodwin v. United States, 67 F.3d 149 (8th Cir. 1995).

- 45 IRC §3121(b)(8)(A) for purposes of the Federal Insurance Contributions Act; see IRS Publication 15-A, Employer’s Supplemental Tax Guide.

- 46 IRS Publication 517, Social Security and Other Information for Members of the Clergy and Religious Workers.

- 47 IRC §1402(c); see also §3.3.

- 48 Weber v. Commissioner, 103 T.C. No. 19 (Aug. 25, 1994), aff’d, 95-2 USTC 50,409 (4th Cir. 1995). For cases involving Assembly of God ministers, see Alford v. U.S., 116 F.3d 334 (W.D. Ark. 1996), and Richard G. and Anne C. Greene v. Commissioner, T.C. Memo. 1996-531.

- 49 Gardner v. Commissioner, 119 AFTR2d 2017-395 (9th Cir. 2017).

- 50 IRC §107; IRS Publication 525.

- 51 Reg. §1.107-1(c).

- 52 Driscoll v. Commissioner, 2012-1 USTC 50187 (11th Cir. 2012), rev’g 135 T.C. 557, citing Commissioner v. Schleier, 515 U.S. 328 (1995), based on consideration of congressional intent.

- 53 Freedom from Religion Foundation, Inc. v. Lew, 112 AFTR2d 2013-5565 (C.D. Wis. 2013).

- 54 Gaylor v. Mnuchin, 123 AFTR2d 2019-510 (7th Cir. 2019).

- 55 U.S. v. Philadelphia Yearly Meeting, Religious Society of Friends, 753 F. Supp. 1300 (E.D. Pa. 1990).

- 56 IRC §6721.

- 57 Taxpayer Bill of Rights §904.

- 58 IRS Publication 15-A, Employer’s Supplemental Tax Guide.

- 59 IRS Publication, 15-T, Federal Income Tax Withholding Methods.

- 60 Helpful charts of the rules applicable to each country are contained in an article by Edmund Outslay, “The U.S. Taxation of International Students: An Analysis and Call for Reform,” EXEMPT ORGANIZATION TAX REV. (September 2002), 439–452.

- 61 Reg. §1.1441-4.

- 62 IRC §3402.

- 63 IRC §7872.

- 64 See Priv. Ltr. Ruls. 200503004 and 9526003.