CHAPTER 17

Taxable Expenditures: IRC §4945

- 17.1 Lobbying

- 17.2 Voter Registration Drives

- 17.3 Grants to Individuals

- 17.4 Grants to Public Charities

- 17.5 Grants to Foreign Organizations

- 17.6 Expenditure Responsibility Grants

- 17.7 Noncharitable Expenditures

- 17.8 Excise Taxes Payable

- Appendix 17–1: Examples of Emergency, Hardship Grant Application, Church and Foreign Equivalency Grants

In response to abuses uncovered by the Filer Commission and reported to the Congress,1 a sanction was added to the Internal Revenue Code (IRC) to limit the manner in which a private foundation (PF) can spend its money to accomplish its exempt purpose. Whereas other types of exempt organizations can engage in some amount of nonexempt activity without losing their exempt status, private foundations have no such leeway and are subject to a tax on any violations if any money is spent for noncharitable or other prohibited purposes.

A private foundation (a foundation or PF) must first meet the organizational and operational tests of IRC §501(c)(3)2 requiring that it operate exclusively—meaning its major focus, but not necessarily 100 percent—for charitable purposes. IRC §4945, however, adds the absolute. Thus, a foundation operates under a higher standard than a public charity: It can conduct absolutely no nonexempt activity. Potential foundation creators and managers need not be discouraged by this fact. The rules are somewhat broader than they sound and once understood, and with procedures in place to review compliance, a PF has some latitude in developing its grant and program activity. Efforts directed at improving matters of broad social and economic impact, such as health care or the environment, have needlessly been forgone by some foundations. Educational and scientific efforts involving such subjects are not necessarily legislative efforts, even if the problems are of a type that government would ultimately be expected to deal with.3

Essentially, IRC §4945 prohibits transactions called taxable expenditures. The private foundation and its disqualified persons (DPs) will incur an excise tax, and the PF may possibly lose its tax-exempt status,4 if any amounts are paid or incurred for the following purposes:5

- To carry on propaganda or otherwise attempt to influence legislation.

- To influence the outcome of any specific election, or to carry on any voter registration drive, except efforts involving at least five states.

- As a grant to an individual for travel, study, or other similar purpose, except according to a preapproved plan.

- As a grant to an organization unless one of the following is true:

- Such organization is a public charity, described in §509(a)(1) or (2), or a Type I, Type II, or Type III functionally integrated §509(a)(3) supporting organization.

- It is an exempt operating foundation,6 a special type of PF controlled by a public board.7

- The PF making the grant exercises expenditure responsibility.

- For any purpose not specified in IRC §170(c)(2)(B), that is, religious, charitable, scientific, literary, educational, to foster national or international amateur sports competition, or to prevent cruelty to children or animals.8

17.1 Lobbying

A private foundation is strictly prohibited from carrying out propaganda or otherwise attempting to influence legislation. This is defined to include any attempt to influence any legislation through:9

- An attempt to affect the opinion of the public or any segment thereof (called grassroots lobbying).

- An attempt to influence legislation through communication with any member or employee of a legislative body, or with any other government official or employee who may participate in the formulation of the legislation (called direct lobbying), except technical advice or assistance provided to a governmental body or to a committee or other subdivision thereof in response to a written request by such body or subdivision, other than through making available the results of nonpartisan analysis, study, or research.

The definition of impermissible lobbying for a private foundation is cross-referenced to the regulations applicable to those public charities that elect to lobby.10 Those rules provide a clear framework to distinguish a foundation's educational activity involving public issues that may eventually be or are now the subject of legislation from those activities that are actually impermissible lobbying. There was uncertainty for the many years between the passage of the tax code on which the following rules are based (1976) and the issuance of final regulations in 1990 after several versions were proposed and re-proposed.11 Under the regulations, a lobbying communication is one that refers to specific legislation, defined as follows:

- Legislation that has been introduced in a legislative body or a specific legislative proposal that the organization supports or opposes.

- In the case of a referendum, ballot initiative, constitutional amendment, or other measure that is placed on the ballot by petitions signed by a required number or percentage of voters. The subject issue becomes specific legislation when the petition is first circulated among voters for signatures.12

A grassroots lobbying communication is an attempt to influence any legislation by affecting the opinion of the general public or any segment thereof.13 Such a communication must encompass all three of the following elements to constitute impermissible lobbying:

- Refer to specific legislative proposal(s).

- Reflect a view on such legislation.

- Encourage its recipient to take action with respect to the legislation.

To constitute encouragement of the recipient to take action, also referred to as a call to action, the communication must specifically do the following:14

- State that the recipient should contact a legislator, staff member, or other governmental official,

- Give the address, telephone number, or similar information (e-mail or website) about the individual(s) to be contacted, and

- Provide some material to facilitate the contact (such as a petition or postcard), or

- Identify one or more legislators who will vote on the legislation as opposing the communication's view of the legislation, being undecided with respect to it, being the recipient's representative in the legislature, or being a member of the committee or subcommittee that will consider the legislation.

A private foundation and its founder were deemed liable for excise taxes for costs of producing and broadcasting radio messages attempting to influence legislation.15 The founder, both a disqualified person and manager, approved the expenditures. In addition to the initial penalty tax, the expenditures were not recouped to timely correct the violation, so additional excise taxes were due.16 The messages, plus newspaper advertisements, were deemed direct lobbying because they targeted a state ballot initiative, in which voters are considered the legislative body.17

A communication that refers to a ballot measure “by name or, without naming it, employs terms widely used in the measure or describes the content or effect of the measure is lobbying.”18 The foundation's argument that the communications at issue constituted “nonpartisan analysis, study, or research,”19 and thus were not forms of lobbying, was rejected by the court. The court also found that the messages contained information that was not educational. Facts were distorted and conclusions expressed were based more on strong feelings than on objective evaluations. Inflammatory language and disparaging terms were used. Both the PF (20 percent) and the manager (5 percent) were subject to the §4945 excise tax.

(a) Germane Lobbying

A foundation can spend its money to make an appearance before, or communicate to, any legislative body with respect to a possible decision of such body that might affect the existence of the PF, its powers and duties, its tax-exempt status, or the deduction of contributions to it. This type of activity is referred to as self-defense lobbying.

The existence of the organization is not threatened for this purpose merely by a possible loss of economic support that might affect the scope of a foundation's programs.20 Lobbying in favor of an appropriations bill funding a program under which the PF has received support in the past is not self-defense. Similarly, a PF that provides care for the elderly is lobbying when its executive director appears before the state legislature to favor or oppose a bill authorizing the state to provide nursing care for the aged. Likewise, a PF receiving governmental grants to support its research programs is lobbying when it testifies about the advisability of continuing the program (unless it was asked to testify). It is the economic condition and the resulting scope of the PF's operation, not its underlying existence, that is at issue in these examples.

Examples of legislation that could affect the foundation's existence or its powers, and is thereby a permissible subject of lobbying, might include the following:

- A state's reformation of its charitable corporation statutes to include provisions not now in a foundation's charter, such as a rule limiting the life of a foundation to some term certain.

- Provision that would restrict the power of a foundation to engage in transactions with certain related parties.

- Change in the excess business holdings provisions that would cause the foundation to have a self-dealing transaction.

- Proposal to require inclusion of outside directors on a foundation's governing body.

- Limitation on administrative expenses included as qualifying distributions that effectively increase the mandatory payout and result in a diminution in use of foundation principal.21

(b) Nonpartisan Study of Social Issues

Sponsoring discussions or conferences, conducting research, and publishing educational materials about matters of broad social and economic subjects, such as human rights or war and peace, are appropriate and permissible activities for a private foundation. These topics are often the subject matter of legislation, involve public controversy, and raise the possibility of the foundation being treated as conducting prohibited legislative activity. However, a foundation is safe in sponsoring such discussions and studying such issues as long as (1) the activity constitutes engaging in nonpartisan analysis, study, or research, and (2) the results of the work are made available to the general public, a segment of the public, or to governmental bodies, officials, or employees.22

The phrase nonpartisan analysis, study, or research means an independent and objective exposition or study of a particular matter. To be nonpartisan, or impartial, the activity must be considered educational.23 The report can advance a particular position or viewpoint if there is a sufficiently full and fair exposition of the pertinent facts to enable an individual or the public to form an independent opinion or conclusion. A communiqué could say that oil tankers should have double hulls to lessen the possibility of oil spills so long as the information forming the basis for the viewpoint is unbiased. Mere opinion, unsupported by pertinent facts, is not nonpartisan. The regulations contain 12 examples that can be studied.24

The making available test is satisfied when the results of the nonpartisan research or study are distributed in articles, reports, conferences, meetings, discussions, press releases, and other public forums. The communications cannot be directed solely toward those who are interested in one side of the issue. Additionally, subsequent use of the research in grassroots lobbying by a grantee or other organization permitted to lobby may result in a taxable expenditure for the foundation that finances the study. The somewhat complicated rules distinguishing research materials from advocacy communications look to the primary purpose for which the study was conducted to determine whether the research was intended to influence legislation.25

A broadcast or publication series must meet the same standards as printed matter. One of the presentations can contain biased information if another part of the series (broadcast within six months of the initial viewing) contains contrary information or the other side of the argument. If the PF selects the time for presentation of information to coincide with a specific legislative proposal, the expenses of preparing and distributing that part of the study may be treated as lobbying and result in a taxable expenditure.26

The foundation's communications, either directly with members of the public or with the legislators themselves, may not:

- Mention or refer to the merits of or take a position on specific legislation.

- Recommend that the reader or listener take any steps to contact legislators, employees of legislators, or government officials or employees involved in legislation, or contain a call to action.27

(c) Grants to Public Charities that Lobby

A PF can make a grant to a public charity that conducts legislative lobbying, regardless of whether the grant recipient has made the §501(h) election. Importantly, the foundation's money cannot be earmarked for lobbying or electioneering. There must be no agreement, oral or written, that the granting PF can direct the manner in which the funds are expended.28 Also, the PF's grant cannot be more than the amount needed to fund the recipient organization's budget for nonlobbying projects. If, after a grant satisfying these rules is paid, the grant recipient loses its exempt status due to excessive lobbying, the money paid is not a taxable expenditure only if:29

- The grant was not earmarked for lobbying.

- The recipient had a valid determination of its public status and notice of the revocation was not published when the grant was made.

- The foundation does not control the public charity.

A foundation may want to protect itself from any question that its grant pays for lobbying by specifically requiring that its public charity grantees agree not to do so. For grantees significantly involved in public affairs, the prudent foundation can retain, and is entitled to rely on, financial information supplied by a prospective grantee that reflects the portion of the public charity's budget spent on lobbying.30 A foundation can also document its efforts to ensure that its funds are not spent on lobbying with the grant approval checklist (Exhibit 17.2), with a request for signature on the grant payment transmittal letter (Exhibit 17.4). Such precautions are not, however, required.

Due to the reluctance on the part of some private foundations to support public charities that conduct lobbying activity, the organization Charity Lobbying in the Public Interest31 engaged the law firm of Caplan & Drysdale to prepare a letter addressing a series of questions about such grants. Some of the questions are addressed in this subsection with the following exceptions:

- Q: What constitutes “earmarking” of a grant for lobbying?

- A: “Earmarking” a grant for lobbying is making a grant with an oral or written agreement that the grant will be used for lobbying.

- Q: Absent a specific agreement to the contrary, will the recitation in a grant agreement that “there is no agreement, oral or written, that directs that the grant funds be used for lobbying activities” be sufficient to establish to the satisfaction of the IRS that there has been no earmarking for lobbying?

- A: Yes, absent evidence of an agreement to the contrary.

- Q: Is a foundation required to include a specific provision in its grant agreements that no part of the grant funds may be used for lobbying?

- A: A specific provision is required only if the grantee organization is not a public charity, or if the private foundation earmarks the grant for use by an organization that is not a public charity.

- Q: Under what circumstances can a foundation make a grant to a public charity for a specific project that includes lobbying?

- A: Such a grant can be made if (1) no part of the grant is earmarked for lobbying; (2) the foundation obtains a proposed budget signed by an officer of the public charity showing that the amount of the grant, together with other grants by the same foundation for the same project and year, does not exceed the amount budgeted, for the year of the grant, by the public charity for activities of the project that are not lobbying; and (3) the foundation has no reason to doubt the accuracy of the budget.

- Q: Similarly, does it matter that the public charity's proposal indicates that it will be seeking funds for the specific project from other private foundations without referring to other additional sources of funds?

- A: No, the specific project grant rules in §53.4945-2(a)(6)(ii) of the regulations do not require the foundation to concern itself about the other sources of funding for the project in such situations.

- Q: What if, in the conduct of the project, the public charity makes lobbying expenses in excess of its estimate in the grant proposal?

- A: If there was no earmarking and no reason to doubt the original accuracy of the budgets, no taxable expenditure occurs. However, knowledge of the excess may provide a reason to doubt the accuracy of subsequent budgets submitted by the public charity.32

The absolute prohibition against the foundation itself conducting lobbying or electioneering does not extend to conduct of its officials acting on their own behalf. Even though such persons are closely identified with the foundation, their personal actions are not constrained by these rules. The guidelines for determining when a minister active in public affairs represents himself or herself rather than the church should be studied by foundation officials.33

(d) Summary of Permissible Activity

To summarize this important constraint, a private foundation and its managers on its behalf can participate in efforts that involve matters of public policy. Such activities do not constitute legislative intervention in the following situations:

- Self-defense (or germane) lobbying.

- Technical assistance or expert testimony given upon request.

- Grants (not earmarked for lobbying) to public charities that lobby.

- Nonpartisan analysis, study, or research.

- Programs involving topics that are the subject of legislation.

- Direct communication with government officials, including legislators, and also with the general public, without reference to and not in support of specific legislation.

- Efforts to influence regulations or other administrative rules clarifying and interpreting existing laws.

- Lobbying efforts of managers acting on their own behalf.

17.2 Voter Registration Drives

All charitable §501(c)(3) organizations, including foundations, are prohibited from participating or intervening in elections of public officials with the intent to influence the outcome. The phrase participation or intervention in a political campaign is defined and explained in Chapter 23. Certain educational efforts in connection with the electoral process may, however, be permitted. What a foundation is specifically forbidden to do is to attempt to influence the outcome of any specific public election, or to carry on, directly or indirectly, any voter registration drive.34 In the South during the early 1960s, certain foundations financed voter drives aimed specifically at registering blacks to vote, in connection with the foundations' effort to eliminate discrimination. Partly as a result, very specific rules govern a PF's participation in such efforts. A foundation is permitted to make a grant to another organization, including another PF, that itself conducts a voter registration drive if the recipient organization meets the following requirements:35

- The organization is a charitable one exempt under IRC §501(c)(3).

- Activities of the organization are nonpartisan, are not confined to one specific election period, and are carried on in five or more states.

- At least 85 percent of the organization's income is spent directly on the active conduct of its charitable purposes.

- At least 85 percent of its support (other than gross investment income as defined in IRC §509(e)) comes from other tax-exempts, the public, and governmental units, and not more than 25 percent comes from a single organization.

- Contributions for voter registration drives cannot be earmarked for particular states or political subdivisions.

An advance ruling for approval of the foundation's procedures for conducting a voter registration drive can be requested.36

17.3 Grants to Individuals

A private foundation may make grants to individuals for purposes that advance the PF's charitable purposes. Differing levels of documentation, however, are required. The highest level is required for grants in support of individual travel, study, or other similar purposes, followed by grants in aid to the poor, sick, homeless, or victims of disasters. Such grants may be made only under the terms of a written plan that has been preapproved by the Internal Revenue Service (IRS) based on submission of Form 8940. The IRS has issued a Guide Sheet for Advance Approval of Individual Grant Procedures (available on the Internet).

(a) Meaning of “Travel, Study, or Other Purposes”

A taxable expenditure results if individual grants are not paid pursuant to an approved plan. Individual grants also cannot be earmarked to be used for political, legislative, or other noncharitable activities.37 Grants to individuals in need of shelter and food, no-strings-attached awards for achievement, and certain other types of grants to individuals may not require a preapproved plan.

A grant to an individual for travel or study, or grants for similar purposes, must also be one of the following three types:

- Grant constituting a scholarship or fellowship grant that would be subject to the provision of IRC §117(a) as it was in effect prior to the Tax Reform Act of 1986 to be used at an educational institution qualifying as a school.38

- Prize or award39 paid to a recipient selected from the public.

- Grant to achieve a specific objective; produce a report or other similar product; or improve or enhance a literary, artistic, musical, scientific, teaching, or other similar capacity, skill, or talent of the grantee.40

Only grants paid to individuals for these three purposes are subject to the prior plan approval rules. By far the most numerous private rulings issued for exempt organizations address individual grants under this provision. The concepts are illustrated in three scenarios.41 In the first, the grant is not subject to IRS approval, but in the second and third, approval is required.

Scenario 1. A PF organized to promote the art of journalism makes awards to persons whose work represents the best examples of investigative reporting on matters concerning the government. Potential recipients are nominated; they do not apply for the award.42 The awards are granted in recognition of past achievement and are not intended to finance any specific activities of the recipients nor to impose any conditions on the manner in which the award is expended by the recipient. Therefore, because the payments are not to finance study, travel, or a similar purpose, the awards project was not subject to prior approval.

Scenario 2. Assume instead that the annual award recipients are required to take a three-month summer tour to study government at educational institutions. These awards are subject to prior approval because the payment is required to be used for study and travel.

Scenario 3. The facts are the same as in Scenario 1, except that the award must be used to pursue study at an educational institution and qualifies as a scholarship. Again, prior approval is required. A similar conclusion was reached in a ruling concerning grants to science fair winners that required them to use the prizes for their education. The program was a scholarship plan requiring approval.43

Other Purposes. The meaning of “grants for other similar purposes” can be elusive. Importantly, a person receiving the grant must be a member of a charitable class.44 The regulations say that student loans and program-related investments do constitute such grants.45 When the payment is given with the expectation or requirement that the recipient perform specific activities not directly of benefit to the foundation, the grant program requires preapproval. Research grants and payments to allow recipients to compose music or to choreograph a ballet are examples of awards for other purposes when the recipient must perform to earn the award.46

A payment to an indigent individual for the purchase of food or clothing is not paid for an “other similar purpose.”47 Grants and interest-free loans made to persons who incur extraordinary medical expenses or funeral or burial costs or who suffer financial hardship due to medical emergencies, natural disasters, or violent crimes are not grants for other purposes and do not require preapproval. Such grants are awards to relieve suffering, not to finance study, travel, or similar purpose. A PF's proposal to make a grant to an organization to fund sabbaticals, combined with increased compensation for the second-in-command, for the chief executives of public charities was approved.48

No-Strings-Attached Awards for Achievement. Preapproval is not required for a program to award grants to individuals in recognition of past achievement with no conditions on how the awards are expended (no strings attached). A grant paid without intention to finance or specify the future activities of the individual, as illustrated in Scenario 1, is not a other purpose grant. Awards paid to winners of a craft school competition on an unconditional and unrestricted basis were also approved.49 Grants in recognition of literary achievement not given to finance future activity, not imposing any future condition on the recipient, and not paid for travel, study, or other purpose do not require preapproval.50

The criteria for choosing recipients of such awards should be designed to achieve and relate to a charitable purpose. Although the objective and nondiscriminatory standard does not technically apply, it's suitable that the award criteria evidence an intention to benefit a reasonably open class of potential awardees. Publicity making the public aware of the awards evidences impartiality. The criteria should evidence no favoritism toward persons related to the foundation creators, managers, or friends. The Nobel Peace Prize or the MacArthur Lifetime Achievement Awards are good examples of prizes that serve to acknowledge persons who work to advance science, education, culture, health, and other charitable pursuits that benefit all. The awards honor past achievements and do not specify how the monetary award is expended. The PF making such awards should keep records to document its criteria for choices, the charitable purposes it intends to achieve, and evidence of lack of any relationship between the recipient and the foundation's disqualified persons.51

A Model Plan. There are plenty of private letter rulings seeking approval for scholarship plans that contain selection criteria based on scholastic performance and leadership potential. Fewer in number are rulings that seek approval for fellowships and other similar purposes. The following criteria were approved by the IRS for a foundation granting prizes and awards to achieve a specific result, produce a report, or improve or enhance literary, artistic, musical, scientific, or other skill or capacity:52

- Potential benefit to the proposed activities in the community and specific population to be served.

- Capacity of the organization or individual to achieve the result.

- Adequacy of proposed financial and time budgets for achieving the desired result.

- Evidence of cooperation and coordination with other organizations and individuals working in the same field.

- Likelihood of ongoing support from other sources for the program.

- Other factors indicating that the program will accomplish the foundation's charitable purposes.

Importantly, the ruling also confirmed the distinctions between grants for future performance and those for past accomplishments. Prizes and awards the foundation proposed to present for past achievement were not subject to preapproval. A complex and detailed plan to award research grants for medical research, enabling basic medical research in the areas of heart disease, cancer, and AIDS, received IRS approval. The ruling contained explicit requirements that might be considered by PFs applying for IRS approval of their individual award procedures.53

(b) Compensatory Payments

Payments for personal services, such as salaries, consultant fees, and reimbursement of travel and other expenses incurred on behalf of the foundation, for work performed on the foundation's own project(s), are not grants requiring a preapproved plan. A foundation can freely hire persons to assist it in planning, evaluating, and developing projects and program activity by consulting, advising, and participating in conferences organized by the foundation.54 Persons hired to develop model curricula and educational materials, for example, are not grant recipients.55

In 1986, Congress reduced the tax-free portion of scholarships, fellowships, and prizes. All payments other than those paid for tuition, books, and fees are taxable to grant recipients. Certain scholarships and, particularly, teaching fellowships are taxable for another reason: the fact that the recipient is expected to render services in return for receiving the grant. Where there is an exchange of services for pay, the grant is made primarily for the benefit of the granting foundation and the approval rules do not apply. Scholarships paid by a foundation formed to aid worthy college students planning to teach in state public schools were found to have strings attached—services to be rendered for the state. As a condition of the grant, recipients had to indicate that they were willing to teach for two years in state public schools after receiving their degrees. The obligation carried no financial guarantee and was merely a moral obligation of the student, but the IRS nonetheless found that such scholarships were not described in IRC §177(a) and, therefore, prior approval was not required.56 Essentially, the grants were paid in exchange for future services.

(c) Food, Shelter, and Aid for the Poor and Distressed

Programs to make grants-in-aid to individuals who lack the resources to satisfy their basic human needs do not require advance IRS approval. Before 2000, few foundations made such hardship grants. The regulations contain only one example of persons deserving such support: buying furniture for a poor family. No income or asset standards for measuring poor to determine financial need are provided. A foundation must decide at what level of financial resource a family ceases to be poor. There has been no guidance regarding information that should be obtained and maintained to document the worthiness of recipients.

In response to the outpouring of financial support in aid to the victims of the September 11 World Trade Center disaster, the IRS issued Publication 3833, entitled Disaster Relief: Providing Assistance Through Charitable Organizations,57 applicable to both private and public charities. As described later, this useful guidance makes a distinction between victims of a disaster in immediate need and those needing longer-term aid. The publication states that “providing aid to relieve human suffering that may be caused by a natural or civil disaster to relieve an emergency hardship is charity in its most basic form.” The use of existing organizations, such as churches, was encouraged by saying they “are frequently able to administer relief programs more efficiently and can offer assistance over a long period of time.”58 Seemingly in response to skeptics questioning what would happen to the generous support for September 11 relief efforts, the publication reminds readers that the assets of a charitable organization must only be spent on and are permanently dedicated to accomplishing its mission.

A needy and distressed test must be in place for disaster relief and emergency hardship organizations. A set of objective criteria by which distributions to financially or otherwise distressed individuals is described. Adequate records to support the basis upon which assistance is provided must also be maintained. The publication distinguishes between short-term and long-term assistance and notes that the type of information needed to support assistance may vary depending on the circumstances:59

Individuals do not have to be totally destitute to be needy; they may merely lack the resources to obtain basic necessities. Under established rules, charitable funds cannot be distributed to individuals merely because they are victims of a disaster. Therefore, an organization's decision about how its funds will be distributed must be based on an objective evaluation of the victim's needs at the time the grant is made. [The publication added new standards in a section entitled “Employer-Sponsored Assistance Programs” for defining the charitable class of eligible recipients for aid.]60

The publication makes it clear that a private foundation can help victims in a variety of ways, including aid to individuals and businesses. Aid may be provided in the form of funds, services, or goods to ensure that persons have basic necessities such as food, clothing, and shelter. The type of aid that is appropriate depends on the individual's needs and resources. A program to distribute short-term emergency assistance requires far less documentation, in the way of victims establishing that they need relief assistance, than the distribution of long-term aid. In the face of an immediate disaster—providing a drug rescue and telephone crisis center or recovery to a person lost at sea or trapped by a snow storm—would not require a showing of financial need, as the individual requiring these services is distressed irrespective of the individual's financial condition. However, “they may not require long-term assistance if they have adequate financial resources.”61 The IRS bottom line for this test is that persons who are needy and/or distressed are appropriate recipients of charity.62

Adequate standards for providing long-term aid to the needy still do not exist. At what income level a person or family is deserving and the type of hardships a foundation should address are not specified. A foundation can make such grants-in-aid but has a burden of proving that the recipients are chosen to accomplish a charitable purpose in a nondiscriminatory fashion. The criteria for awarding such grants for food, shelter, and medical care should be designed to award funds only to those who are indeed qualified for charitable assistance or persons also referred to as members of a charitable class. To document the charitable nature of the program, a written policy, including an application form, should be used to describe the basis for the decision to grant aid. Facts such as income levels, cause of the hardship, recommendations of a government agency, or referrals from a church are among the factors that might be used to make the choice.

The need to establish criteria to evidence the charitable nature of such programs was also indicated in the IRS's refusal to approve a program to grant funds to ministers to pay outstanding educational loan balances related to studying for their ministry.63 It is important to note that the proposed grant was not one requiring prior IRS approval because the ministers were not required to perform any specific acts. The factors the IRS found lacking included:

- The foundation did not request that the ministers establish that the funds would be used for charitable purposes. (With the right words in their grant documents, it could have been asserted that the program served religious purposes.)

- Grantee ministers were not required to provide any follow-up reports or accounting of the fashion in which they used the grant. (In connection with awards made in honor of achievement, no follow-up reporting is required.)

- Grantees were not required to evidence financial need to qualify for the grants. (Since the grants were not awarded on the basis of achievement, this factor should have been present.)

IRS has refused to grant tax-exempt status to an organization that provides financial aid to disadvantaged patients who have a medical need for marijuana, because the use of marijuana is illegal.64

(d) Designing an Individual Grant Program

Once a foundation chooses to make grants subject to the approval process, it must adopt a suitable plan. The primary criterion for approval of a plan for making individual grants is that the grants must be awarded on an objective and nondiscriminatory basis. A “racially nondiscriminatory policy as to students” is defined as meaning that the school admits students of any race to all the rights, privileges, programs, and activities generally accorded or made available to students at that school and the school does not discriminate on the basis of race in administration of its educational policies, admissions policies, scholarship and loan programs, and athletic and other school-administered programs.65 The plan must contain the following provisions:66

- An objective and nondiscriminatory method of choice, consistent with the PF's exempt status and the purpose of the grant, is used. IRS policy requires, despite the lack of such terms in §170(b)(1)(A)(ii) or applicable regulations, that a school operate pursuant to a racially nondiscriminatory policy as to students.67

- The group from which grantees are selected is sufficiently broad so as to constitute a charitable class.68 The size of the group may be small if the purpose of the grant so warrants, such as research fellows in a specialized field.

- Criteria used in selecting the recipients include (but are not limited to) academic performance, results of tests designed to measure ability and aptitude motivation, recommendations from instructors, financial need, and conclusions a selection committee might draw from a personal interview as to an individual's potential ability and personal character.

- Selection committee members do not derive a private benefit, directly or indirectly, if one person or another is chosen. A selection committee made up of persons unrelated to foundation officials to evidence objectivity is not required.69

- Grants are awarded for study at an academic institution, or as fellowships, prizes, or awards for study or research involving a literary, artistic, musical, scientific, or teaching purpose.

- Procedures to obtain reports are provided for scholarships, fellowships, and research or study grants.

Class of Potential Grantees. The second criterion in the preceding list requires the group from which the grantees are chosen to be sufficiently broad. A group including all students in a city or all valedictorians in a city or state clearly qualifies. The regulations sanction a plan to grant 20 annual scholarships to members of a certain ethnic minority living within a state.70 However, a group of girls and boys with at least one-quarter Finnish blood living in two particular towns was found to be a discriminatory group and not sufficiently broad.71 Likewise, a plan that gave priority to family members and relatives of a disqualified person was found to be discriminatory.72 Although self-dealing does not technically occur if a grant is made to a niece or nephew of the creator,73 awards to such relatives could be considered to give private inurement to the creator. A program to award scholarships at two named colleges to members of a particular 603-person family group (surname specified) was not a broad enough group.74 The IRS found that the fact that the school made no effort to recruit minority children to balance its ethnicity evidenced discrimination.

Scholarships and Fellowships. A report of the grantee's courses and grades earned in each academic period must be collected at least once annually and verified by the educational institution. If scholarship funds are paid directly to the school and the school agrees to monitor the student's ongoing qualification, such reports are not necessary.75 For grantees whose work does not involve classes but only the preparation of research papers or projects, such as a doctoral thesis, the foundation should receive an annual report approved by the faculty members supervising the grantee, or another school official. Upon completion of a grantee's study, a final report must also be obtained.

Investigation of Diversions. Procedures must be established to investigate when no reports are filed or when reports indicate that funds are being diverted. The foundation will not be treated as making a taxable expenditure if the recipient has not previously misused funds and if the PF takes the steps outlined later in this chapter during its investigation. Additional grant funds must be held until delinquent reports are received, and reasonable steps to recover the funds should be taken.76

Research or Study Grants. At least annually, a report of progress and use of funds is due. A final report describing the grantee's accomplishments and funds expended with respect to the grant must also be made.

- During the investigation, the PF must withhold additional payments until it receives the grantee's assurances that future diversions will not occur and must require the grantee to take extraordinary precautions to prevent future diversions from occurring.

- The PF must take reasonable steps to recover the funds.

- If a grantee was reprieved after an initial investigation and the PF reinstituted the grant only to have the funds diverted for a second time, a taxable expenditure will not occur if the same steps are repeated and the diverted funds are recovered.77

Record-Keeping. A foundation making individual grants must maintain and keep available for IRS examination documentation that the recipients are chosen in a nondiscriminatory manner and that proper follow-up is accomplished. The regulations do not specify a required time period.

The following records must be kept:

- Information used to evaluate the qualification of potential grantees.

- Reports of any grantee/director relationships.

- Specification of amount and purpose of each grant.

- Grade reports or other progress reports approved by a faculty member, which must be received annually.

Income Tax Reporting. A foundation's grant to an individual does not necessarily represent taxable income to the grant recipient. In a circumstance in which the recipient award represents payment for services rendered or a business recruitment or employee retention program, the scholarships payments may be taxable either on Form W-2 or Form 1099.78

(e) Company Scholarship Plans

The regulations and countless rulings have approved scholarship plans established by a company's foundation for children of the company's employees.79 One issue with such plans is whether they discriminate in favor of the corporate executives or shareholders and thus represent a means of paying additional compensation. Specific guidelines exist and should be carefully studied prior to application for approval of such a plan.80 Similar rules apply to a company foundation's educational loan program.81 The nine primary criteria are as follows:

- The scholarship plan must not be used by the employer, the PF, or the organizer thereof to recruit employees or to induce continued employment.

- The selection committee must be wholly made up of totally independent persons, not including former employees, preferably including persons knowledgeable about education.

- Identifiable minimum requirements for grant eligibility must be established and eligibility should not depend on employment-related performance, although up to three years of service for the parent can be required.

- Employees, or children of employees, must meet the minimum standards for admission to an educational institution82 for which the grants are available and are reasonably expected to attend such an institution.83

- Selection criteria must be based on substantial objective standards such as prior academic performance, tests, recommendations, financial need, and personal interviews.

- A grant may not be terminated because the recipient or parent terminates employment. If the grant award is subject to annual review to continue support for a subsequent year, the recipient cannot be ineligible for renewal because the individual or his or her parent is no longer employed.

- The courses of study for which grants are available must not be limited to those of benefit to the employer.

- The terms of the grant and course of study must allow recipients to obtain an education in their individual capacities solely for their personal benefit and must not include any commitments, understandings, or obligations of future employment.

- In its original ruling on company plans, the IRS said that no more than 10 percent of the eligible persons and no more than 25 percent of the eligible persons who submitted applications and were considered by the selection committee can be awarded grants.

Essentially, the facts and circumstances should not indicate that the awards represent an additional source of compensation to a significant number of employees and their children who routinely receive the scholarships. Additionally, the plan must be made known, or publicized, to all eligible employees. The IRS did permit a company foundation plan to be amended to include educational grants to employees and children of employees who are victims of a qualified disaster.84

Due to the self-dealing rules, no grants can be paid to children of disqualified persons. The plan must avoid a disproportionate amount of grants to executives' children. Application for approval is the same as for other scholarship plans, although satisfaction of the nine tests just listed must be outlined.

(f) Seeking Approval

An application for approval of a scholarship plan is submitted on Form 8940. The approval procedure does not contemplate specific approval of particular grant programs but rather approval of a system of standards, procedures, and follow-up designed to result in grants which meet the requirements. Thus, such approval applies to a subsequent grant program if the procedure under which it is conducted do not differ materially from those described in the request to the Commissioner.85 The PF submits its proposed procedures for awarding grants as illustrated in Exhibit 17.1, including the methods of meeting the selection process requirements.86

If within 45 days after submission of the plan, no notification is received that the procedures are unacceptable, the PF can consider the plan approved; silence signifies approval. Written IRS approval is customarily sent to successful applicants, but usually well beyond 45 days. In one instance, scholarship payments made prior to the date on which the PF sought IRS approval were taxable expenditures, not only because of the lack of approval but also because the company had insufficient data to prove that the plan was objective and nondiscriminatory.87 In contrast, payments made after the 45 days have passed and prior to receipt of written approval are not deemed a taxable expenditures. Even if the IRS denies approval or suggests modifications to the plan submitted, the foundation is protected before notice of disapproval by the assumed approval date.88 Newly created foundations can seek approval for a plan in connection with filing Form 1023 by submitting proper and fully disclosed responses on Schedule H. The instructions do not, however, contain the 45-day rule.

“Approval of an organization's exemption application does not in itself constitute approval of the organization's grant-making procedures unless the exemption letter so provides. If the organization has fully disclosed its scholarship grant-making procedures in its application, however, it may nevertheless NOT be subject to the section 4945 excise taxes on taxable expenditures by operation of the 45-day rule. If you believe that the omission of such language from your organization's determination letter was an error on our part, please see Internal Revenue Manual 21.3.8.12.19 for information on how to request a corrected/superseding letter.”89

As a foundation administers a scholarship plan over time, it may wish to change or expand the program. The issue becomes whether the revision is a “material” change in the originally approved system of standards, procedures, and follow-up procedures that requires submission of a request for approval from the IRS. For example, is a change allowing a student five, instead of four, years to complete an undergraduate degree a material change? What if the foundation wishes to award funds for graduate study to its successful undergraduates? What if it wishes to expand the permitted course of study from art history to liberal arts? It is likely that such expansion of benefits to recipients chosen under the approved plan would not be considered material. However, there is no IRS guidance on the issue. The intent of this provision in the tax code focuses on objectivity and lack of discrimination in choosing recipients and an intention to serve an educational or charitable purpose with individual grants. In view of that criterion, the three examples posited here would likely not be material.

EXHIBIT 17.1 Request for IRS Approval of Individual Grant Program

| Internal Revenue Service Center Exempt Organization Group P.O. Box 192 Covington, KY 91012-0192 |

|

| RE: Sample Foundation EIN #44-4444444 Request for Approval of Scholarships |

Dear IRS:

From 1982 to 2002, the Sample Foundation operated a medical research facility and was classified as a public charity pursuant to Internal Revenue Code (IRC) §509(a)(1). During that time a scholarship fund was established in the memory of Dr. XYZ, one of the founders of Sample. For the past 20 years, scholarship grants have been paid annually. As of MMMM, 20XX, Sample discontinued the research facility and was reclassified as a private foundation. Your approval for the scholarship program is hereby sought.

The XYZ Scholarship will further Sample's educational purposes by enabling deserving men and women to complete a medical-related education in the graduate schools of their choice, so that they will be able to serve honorably and effectively in their chosen medical field.

The scholarship will be a “grant” within the meaning of IRC §4945(d)(3) and will satisfy the requirements of IRC §4945(g) in all respects.

The grant will be awarded on an objective and nondiscriminatory basis. The grant will be excluded from gross income under IRC §117(a), to the extent that it is used for tuition, books, and equipment required for educational courses. The purpose of the grant is to promote medical-related education for graduate degree candidates, and the recipient of the grant will be selected from the population of medical school graduate students.

As provided in Life Cycle of a Private Foundation, Advance Approval of Grant-Making Procedures, the grant-making procedures will be as follows:

Grantee class. Any graduate college student seeking a degree in medical-related education may be considered for the scholarship.

Selection criteria. The selection criteria for the scholarship will include, but not be limited to, the student's demonstrated academic ability and desire, character, good citizenship, and economic necessity. A recipient cannot be related to a member of the committee or to any “disqualified persons” in relation to Sample.

Selection committee. The selection committee will be composed of members of the board of directors of Sample. Members of the selection committee will not be in a position to receive private benefit, directly or indirectly, if certain potential grantees are selected over others.

Progress reports. The scholarships will be about $5,000 per semester and can be renewed annually for a maximum of three years, provided that the student is not on academic or disciplinary probation and is making satisfactory progress toward completion of a medical-related degree. A student need not have an “A” average, but should be of a caliber to indicate an ability to profit from and be intellectually equal to work on a graduate level. Progress reports will be obtained and verified with the educational institution each semester. Upon completion of the grantee's study, a final report will be collected from the grantee.

Report follow-up. If no report is filed by the student, or if reports indicate that the funds are not being used in furtherance of the scholarship purpose, a member of the board of directors will investigate the grant. While conducting this investigation, Sample will withhold further payments from the grantee and will take reasonable steps to recover grant funds until it has determined that the funds are being used for their intended exempt purpose.

Record keeping. The foundation will retain all records submitted by the grantees and their educational institutions for four years beyond disbursement of the last payment. Sample will obtain and maintain in its file evidence that no recipient is related to the foundation or to any members of the selection committee.

Sample trusts that the above criteria and purpose for its educational scholarship satisfy the requirements of IRC §4945 and respectfully requests your approval of its procedures.

Under penalties of perjury, I declare that I have examined this request, including accompanying documents, and to the best of my knowledge and belief, the facts presented in support of the request are true, correct, and complete.

Date Sample Officer

(g) Individual Grant Intermediaries

A foundation wishing to avoid the administrative burden and cost of applying for approval and disbursing scholarships directly can alternatively fund a grant program at an independent public charity. The foundation may be involved in the process. As long as the foundation has no control over the choice of recipients, it is not considered to have made the grants directly to the individuals.90 There must be no agreement, oral or written, that the PF can dictate the selection of particular individuals. No earmarking is permitted, only suggestions.

The parameters of the grant, such as the study discipline—medicine or law, for example—or qualifications, such as grades or civic achievement, can be stipulated by the foundation, though the class of grantees should be relatively broad. Grants to fund scholarships for children of employees may be considered grants by the company foundation itself, not by the college administering the plan.91 Actually suggesting an individual grantee is permitted, as long as there is an objective manifestation of the public charity's control over the selection process. Maintaining the right to veto a potential recipient is de facto control.92 Likewise, a research grant disbursed by a college was found to be a direct grant when the funding was contingent on supervision by the professor designated by the PF with reserved rights to patents, inventions, and publications arising from the research, and the PF retained authority to approve the professor's project and any of his scientific work.93 The regulations contain useful examples for further study.94

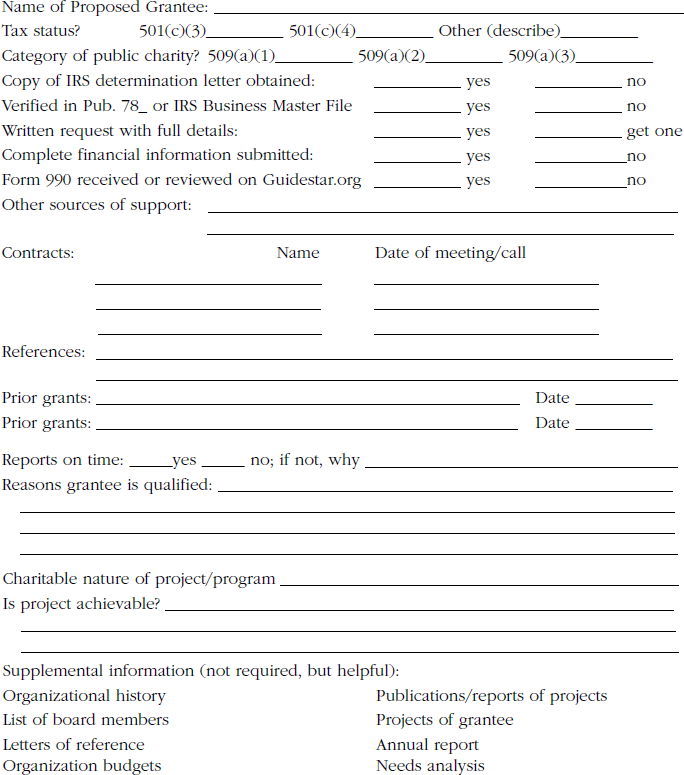

17.4 Grants to Public Charities

Most private foundations make grants to public charities or those grant recipients specifically excluded from the taxable expenditure list by IRC §4945(d)(4)(A), primarily including §§509(a)(1) and (2).95 This is true partly because so much charitable work is performed by those organizations and private foundations have traditionally used their endowments to fund such institutions. The tax law favors private foundation grants to public charities by making their administration simple and by permitting support of a public charity that conducts lobbying and individual grant programs.

A foundation is, however, permitted to make a grant to any type of entity, exempt or nonexempt, if it properly documents its purposes in making the grant and ensures the transaction with expenditure responsibility agreements.96 The purpose of these rules is to ensure that PF funds are used to benefit the public, not the private interests of their creators. Public charities commonly serve a broad constituency that monitors their responsiveness to public needs and use of their funds for charitable purposes.

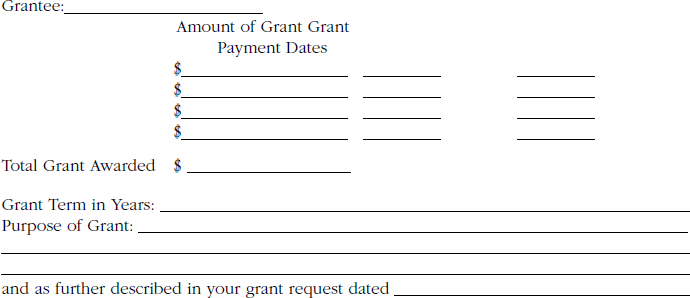

The responsibility to ensure that a private foundation's funds are expended for charitable purposes still applies when the foundation makes a grant to a public charity. Completion of the checklist in Exhibit 17.2 is the first step. If the proposed grantee is a supporting organization,97 the grantee is a public charity, but the grant cannot be counted for payout purposes. The certificate in Exhibit 17.3 should be completed. Lastly, a grant agreement with the grantee (Exhibit 17.4) should require that the funds be spent for charitable purposes and request a follow-up report (Exhibit 17.5). Many foundations now publish their grant applications on a website to describe these requirements.

EXHIBIT 17.2 Grant Approval Checklist

For use of a private foundation (PF) to obtain required documentation before it issues a check for a grant.

OBTAIN DOCUMENTATION OF CHARITABLE PURPOSES OF GRANT

- Obtain a grant request indicating the exempt purpose of the program(s) to be funded. If the PF is unilaterally giving a grant to an established public charity, a transmittal letter accompanying the grant check which states that it is for general support may suffice. A grant agreement and completion of this checklist is recommended in either case.

- Ascertain, either from grant request, or interviews with grantee representatives, that funding will not be spent for electioneering, lobbying, individual grant, or a re-grant to another private foundation.

OBTAIN PROOF THAT GRANTEE IS ELIGIBLE PUBLIC CHARITY

A PF can make a grant, without further steps, to an organization that either (1) is listed in the IRS Business Master File (BMF) with a Foundation code between 10-16 or (2) is listed in IRS Publication 78 and provides an IRS letter which states it is a §509(a)(1) or §509(a)(2) public charity (IRS Notice 2006-109). [Seek grantee verification of status, see Exhibit 17.5 later in the chapter]. If the IRS letter states the grantee is a §509(a)(3) public charity or the Foundation code in the BMF is 17, extra steps are required (see below). Proof needed:

- Classification as §509(a)(1) or (2) in IRS Business Master File (BMF). Alternatively, classification displayed on Guidestar's Charity Check (a fee is charged to access this information on www.guidestar.org) or Grantsafe, available free of charge on www.Foundationsource.com.

OR

- Copy of the grantee's current IRS determination letter and listing (with code =) in Publication 78, Cumulative List of Organizations Described in IRC §170 at www.irs.ustreas.gov.

OR

- Churches and governmental entities, if they meet specific criteria, are treated as eligible public charities for this purpose even though they are not required to seek IRS recognition of exempt status and may, therefore, not have an IRS determination letter. The PF should take steps to obtain information to satisfy itself that the grantee possesses the criteria for such classification by the IRS though it is not required to file with the IRS for recognition. See Exhibit A17.2 and A17.3.

EXTRA STEPS FOR APPROVAL OF GRANT TO SUPPORTING ORGANIZATION

A grant cannot be made to a §509(a)(3) supporting organization (SO) without additional information. SOs are categorized as being a Type I, Type II, or Type III SO, but sadly enough, until very recently that identity was not entered on their IRS determination letter, Form 990, IRS BMF, or Publication 78 (still not entered on BMF or Pub. 78). Complete the attached Certification of Type in order to determine whether the grantee is a Type I, II, III—Functionally Integrated, or III—Other. Grants to Type III—Other organizations require another special step called Expenditure Responsibility (see below section for PFs) and such grants do not count as qualifying distributions.

EXTRA STEPS FOR APPROVAL OF GRANT TO PRIVATE FOUNDATION

A grant made to a private foundation results in a taxable expenditure unless expenditure responsibility is exercised. To exercise expenditure responsibility, a foundation must take very specific steps. All eight specific requirements listed in the ER Control Checklist must be followed. Additionally, such a grant does not count as a qualifying distribution unless the grantee agrees to redistribute the funds. Redistribution by the grantee is accomplished where, not later than the close of the first taxable year after the grantee's taxable year in which such contribution is received, the grantee makes a distribution equal to the full amount of such contribution. Additionally, the grantee may not count the distribution toward satisfying its own requirement, but instead must treat its re-granting of the money as a payment out of corpus. The PF must obtain adequate proof that the redistribution was accomplished. The grantee should provide a report describing the names and addresses of the charitable organizations to which it redistributed the funds. Most important, the grantee must declare that it did not claim its re-grants as qualifying distributions counting towards its own payout requirement.

EXTRA STEPS FOR APPROVAL OF GRANT TO A NON §501(C)(3) ORGANIZATION

A PF may make a grant to a non §501(c)(3) organization, such as a social club or even a for-profit company, if the grant is specifically dedicated to charitable purposes and expenditure responsibility is followed. To exercise expenditure responsibility, a foundation must take very specific steps. All eight specific requirements listed in the ER Control Checklist must be followed.

EXTRA STEPS FOR APPROVAL OF GRANT TO A FOREIGN ORGANIZATION

A grant to a foreign government and any agency or instrumentality thereof is treated as a grant to a public charity. A foreign charitable organization that does not have an IRS determination of its public charity status, but is substantially equivalent to, and would in fact qualify as, a public charity if it sought approval may also be treated as a public entity. A private foundation is entitled to make a good faith determination of the foreign organization's status. An affidavit from the foreign entity or an opinion of counsel is obtained. The grant agreement with the foreign organization must also contain restrictions requiring that the funding be used for strictly charitable purposes. Facts concerning the operations and support of the grantee that would allow the IRS to determine that the organization would qualify as a public charity must be gathered. Detailed financial information, organizational documents, program activity descriptions, and other information that evidences the foreign charity's ability to qualify as a public charity under the U.S. Tax Code must be obtained. If the evidence gathered supports classification as a private foundation rather than a public charity, then the steps (ER and redistribution) described in the grants to private foundations must also be taken.

Seeking the appropriate information described in the preceding subsection from a foreign organization is not so simple and is often troublesome due to language, currency, and legal differences. Because of these difficulties, a private foundation will sometimes find it more comfortable to treat such foreign grants as expenditure responsibility. In that case, all eight specific requirements listed in the ER Control Checklist must be followed.

EXHIBIT 17.3 Certificate of Supporting Organization Type

| This certification should be obtained by a private foundation to document a supporting organization's status as a Type I, II, or III. | |

| NAMF OF SUPPORTING ORGANIZATION | |

| ADDRESS | |

| CITY, STATE, ZIP | DATE |

Dear Director, Executive Officer, or Financial Officer:

The Pension Protection Act of 2006 (PPA), signed into law on August 17, 2006, contains several provisions that impact charitable organizations. One of the provisions concerns grants made by private foundations to supporting organizations. We have identified your organization as one that is classified as a supporting organization under Internal Revenue Code § 509(a)(3).

What Is a Supporting Organization?

All § 501(c)(3) charities are classified as either public charities or private foundations. Some types of charities, such as churches, schools, and hospitals, are classified as public charities because of the nature of their activities. Others qualify as public charities because they meet a “public support test” that indicates they receive support from a broad base or contributors.

A supporting organization qualifies as a public charity because it has a close relationship with another § 501(c)(3) public charity. A supporting organization provides meaningful support—financial, programmatic, or both—and gives some degree of structural and operational control to the public charity it supports.

Types of Supporting Organizations

In general, supporting organizations (SOs) fall into one of three categories, depending on the nature of the relationship between them and the charity being supported.

- Type I—Operated, supervised, or controlled by: This type is often described as a parent-subsidiary relationship and generally involves the supported charity's officers, directors, trustees, or members having the right to appoint a majority of the officers, directors, or trustees of the SO.

- Type II—Supervised or controlled in connection with: This type usually has an overlapping board relationship where at least a majority of the members of the SO's governing board are also members of the supported charity's governing board.

- Type III—Operated in connection with: This type may have no, or minimal, board overlap. Accordingly, it operates with a greater degree of independence from the organization it supports, but it is required to have procedures designed to ensure that the SO is responsive to the supported organization.

New Limitations on Grants to Type III Supporting Organizations

Previously, private foundations could treat a grant to any types of SO as a qualifying distribution just as they would any other public charity grant. Under the PPA, Type III SOs are essentially treated as private foundations. Grants to certain Type III SOs do not count toward a foundation's mandatory payout requirements. A deficiency in the 5% payout results in a 30% (of the deficiency) a year penalty until grants are paid to eliminate the underdistribution. Plus, expenditure responsibility (ER) procedures, including a written agreement, must be entered into before the grant is paid. Failure to follow ER procedures results in a taxable expenditure for which the penalty is 20% of the grant each year until the ER is in place.

The impediment on foundation grants to Type III SOs does not apply if the SO qualifies as a “functionally integrated” Type III SO.

Your Organization

As noted above, the IRS determination letter and the IRS Business Master File that identifies your organization as a supporting organization does not indicate whether it qualifies as a Type I, II, or III SO. Determining which type of SO your organization is requires a review of the governing documents in view of the specific requirements outlined above.

It may be clear that your organization is a Type I SO. As an example of a Type I supporting organization, the Houston Parks Board is a supporting organization to the City of Houston (the public Charity in this example). The Mayor appoints, with City Council approval, all of the members of the board of directors of the Houston Parks Board.

If your governance structure does not provide that a majority of the members of the board of your SO are appointed or elected by the supported organization, you may want to confer with legal counsel or a tax advisor to determine which type of SO your organization is. If the legal counsel or tax advisor who originally helped obtain your exempt status with the IRS is available, that would be a good place to start. If not, you may want to engage legal counsel or a tax advisor with expertise in the law of tax-exempt organizations to advise you.

It your organization is a Type III SO, additional documentation will be required to determine whether it is a “functionally integrated” Type III SO.

The enclosed form will allow us to comply with IRS Notice 2006-109, Interim Guidance Regarding Supporting Organizations and Donor Advised Funds. Before we can continue processing your grant application for make payment on your previously approved grant], we must receive the enclosed form and the additional documents indicated. The form must be signed by the president or chief executive officer of your organization.

Sincerely,

Foundation Representative

REPRESENTATION OF SUPPORTING ORGANIZATION STATUS

[NAME OF SUPPORTING ORGANIZATION] hereby represents that it qualities as a public charity because it is a supporting organization as defined by § 509(a)(3).

- The organization supports:

Name of Supported Organization(s)

- The organization represents that its SO type is:

_____ Type I—“Operated, supervised, or controlled by” one or more publicly supported organizations: A majority of the governing board is elected or appointed by the supported organization(s).

_____ Type II—“Supervised or controlled in connection with” one or more publicly supported organizations: A majority of the governing board consists of individuals who also serve on the governing hoard of the supported organization(s).

_____ Type III—“Operated in connection with” one or more publicly supported organizations: Not a Type I or Type II.

- Describe the process by which your governing board is appointed and elected.

Attach articles of incorporation, bylaws, or other documents that detail the process. Please highlight the article(s) or section(s) of the material that prescribes the process.

If the organization is a Type I or Type II SO, skip section 4 and go to the signature section below.

If the organization is a Type III SO, complete section 4.

- Type III SOs are either functionally integrated or not functionally integrated with the organization(s) they support.

- As a Type III SO, the organization represents that it is:

- _____ functionally integrated with one or more supported organizations, or

- _____ not functionally integrated with one or more supported organizations. If not functionally integrated, skip remainder of section 4. If functionally integrated, complete the rest of section 4.

- If the organization represents that it is functionally integrated, identify the one or more supported organizations with which it is functionally integrated:

- If the organization represents that it is functionally integrated, it must provide one of the following documents. Please indicate which of the following is attached.

_____ A written representation signed by an officer, director, or trustee of each of the supported organizations with which the grantee represents that it is functionally integrated describing the activities of the grantee and confirming that but for the involvement of the grantee engaging in activities to perform the functions of, or to carry out the purposes of, the supported organization, the supported organization would normally be engaged in those activities itself. Such written representation must meet the requirements outlined in Section 3 of IRS Notice 2006-109.

or

_____ A reasoned written opinion of counsel representing the organization concluding that the grantee is a functionally integrated Type III supporting organization.

- As a Type III SO, the organization represents that it is:

| NAME OF SUPPORTING ORGANIZATION | ||

| By: ________________________________ | ||

| Signature | ||

| ___________________________________ | ||

| Printed Name | ||

| ____________________________ | ||

| Title or Corporate Office Held | ||

| Date: ____________________________________ | ||

EXHIBIT 17.4 Grant Payment Transmittal Letter

This letter conveys the grant payment check for repeating grant recipients.

GRANTEE ORGANIZATION

ADDRESS

DEAR GRANT RECIPIENT:

We are happy to enclose our check for $_____in payment of a grant for Tnamel project as described in your request dated [date].

As a private foundation, we must document that our grant is expended for a charitable or educational purpose. We must ask that you use our funds exclusively to carry out the project described in your request. You must not use any of our funds to influence legislation, to influence the outcome of any election, or to carry on any voter registration drive.

Please verify that your organization continues to be exempt under Internal Revenue Code §501(c)(3) and is still classified as a public charity pursuant to IRC §509(a)(1), (2), or (3). Kindly send us a copy of your most recent Internal Revenue Service tax determination letter, your financial statements, Form 990, and any annual report for the year in which our grant funds are expended.

Finally, we must ask that any funds not expended for the purposes for which the grant is being made be returned to us. Please indicate your agreement with these conditions by returning a signed copy of this letter.

Thank you.

| ____________________________________________ | ||

| for Sample Foundation | ||

| Acknowledged by:____________________ | ||

| Date: ___________________ | ||

EXHIBIT 17.5 Grant Agreement

This letter requests tax status information before a grant is paid.

GRANTEE ORGANIZATION

ADDRESS

DEAR GRANT RECIPIENT:

As a private foundation, Sample Foundation must ascertain that your organization is exempt from income tax under Internal Revenue Code §501(c)(3) and is classified as a public charity under IRC §509(a)(1), (2), or (3).

According to information furnished to us with the proposal, your organization is so qualified. Please inform us only if there has been a change in your tax status since then.

In addition, we must be assured that our grant will be expended for an educational, scientific, literary, or other charitable purpose. We ask that you use our funds exclusively to carry out the project described in the application. Also, we ask you not to use any of our funds to influence legislation, to influence the outcome of any election, or to carry on any voter registration drive.

Finally, we ask that any funds not expended for the purposes for which the grant is being made be returned to us.

Please signify your agreement with these conditions by returning a signed copy of this letter to us.

Thank you.

| ____________________________________________ | ||

| for Sample Foundation | ||

| Acknowledged by:____________________ | ||

| Date: ___________________ | ||

In the interest of efficiency and to streamline its operations, a PF asked the IRS if it were acceptable to maintain its grant-making activity records only in electronic form.98 Grant requests, correspondence, and reports to and from grantees would be conveyed electronically. Grant agreements would be signed by both foundation and grantee officials. The state in which the foundation operated permits the use of electronic records and signatures in most contracts and other writings of legal significance. Further, the origination and maintenance of all books and records for tracking investments, charitable activities, and all other matters were kept electronically. The IRS determined that electronic records met the requirements of Reg. §1.6001-1 and are proof of public status for IRC §§4945(a)(4) and 4945(h) with respect to expenditure responsibility.

Good documentation should be maintained by PFs making grants to public charities that conduct lobbying99 and scholarship grants to intermediary entities (other than directly to the student).100

(a) Proof of Public Status

A grant-making private foundation must adopt procedures to document the tax character of grant recipients. Due to significant improvements in irs.gov/charities-non-profits, the information may be available on the IRS website if the grantee's name and federal identification number are known. Continuing to request the letter can be useful to allow a correct search on the new Publication 78, called Tax Exempt Organization Search (Pub 78).

As discussed in §18.1(e) and §18.2(c), any IRC §501(c)(3) organization that failed to file a Form 990, 990-EZ, 990-N, or 990-PF automatically has its exempt status revoked. Many organizations listed in Pub 78 now say their exempt status was revoked. Members of an affiliated group of organizations centralized under the common supervision and control of a parent organization do not individually obtain a determination letter and are not listed in Pub 78. Therefore, to verify their public charity status, the foundation should request documentation that the entity is indeed a member of a group (most issue a certificate), look up the parent organization on Guidestar or Pub 78, and observe whether the front page of the grantee's Form 990 indicates that it is a member of such group.