CHAPTER 21

Unrelated Business Income

- 21.1 IRS Scrutiny of Unrelated Business Income

- 21.2 History of the Unrelated Business Income Tax

- 21.3 Consequences of Receiving UBI

- 21.4 Definition of Trade or Business

- 21.5 What Is Unrelated Business Income?

- 21.6 “Regularly Carried On”

- 21.7 “Substantially Related”

- 21.8 Unrelated Activities

- 21.9 The Exceptions

- 21.10 Income Modifications

- 21.11 Calculating and Minimizing Taxable Income

- 21.12 Debt-Financed Property

- 21.13 Museums

- 21.14 Travel Tours

- 21.15 Publishing

Exempt organizations (EOs) receive two types of income: earned and unearned. Unearned income—income for which the organization gives nothing in return—comes from grants and donations. One can think of it as one-way-street money. The motivation for giving the money is generosity and/or of a nonprofit character, with no expectation of gain on the part of the giver; there is donative intent. In contrast, an organization can furnish services and goods or invest its capital in return for earned income: An opera is seen, classes are attended, or health counseling is given. The purchasers of the goods and services do intend to receive something in return; they expect the street to be two-way. An investment company or bank holding the organization's money expects to have to pay a reasonable return for using the funds, and the organization receives earned income. The important issue this chapter considers is when earned income becomes unrelated business income (UBI) subject to income tax.

The tax on unrelated business income applies to all organizations exempt from tax under §501(c) other than corporations created by an act of Congress. It also applies to the following:

- Tax-exempt employee trusts, described in IRC §401.

- Individual retirement accounts.

- State and municipal colleges and universities.

- Qualified state tuition programs, described in IRC §529.

- Education individual retirement accounts, described in IRC §530.

The rules that govern when earned income becomes unrelated business income are complex. The concepts of UBI are vague and contain many exceptions that have been carved out by special-interest groups. The House of Representatives Subcommittee on Oversight held hearings and drafted revisions over a four-year period from 1987 to 1990. Though proposals to limit deductions and tax a variety of items were not passed, two very important changes resulted from the studies. The Internal Revenue Service (IRS) was directed to expand the Form 990 to report details of revenue sources to reveal when an organization should file Form 990-T.1 For-profit subsidiary payments in the form of rent, interest, royalties, or other expense deductible to the subsidiary may be taxed to the tax-exempt parent under an on-again-off-again rule.2

Tax planning of the sort practiced by a good businessperson is in order for organizations receiving UBI. Indeed, the income tax rules applicable to nonexempt businesses apply for Form 990-T purposes. The best method for reducing unrelated business income tax (UBIT) is to keep good records. The accounting system must support the allocation of deductions for personnel and facilities with time records, expense usage reports, auto logs, and documentation evidencing the nature of expenses allocable to taxable business income. Minutes of meetings of the board of directors or trustees should reflect discussion of relatedness of any project claimed to accomplish an exempt purpose, if the relatedness of the activity could be questionable. For example, contracts and other documents concerning activities that the organization wants to prove are related to its exempt purposes should contain appropriate language to reflect the project's exempt purposes. An organization's original purposes can be expanded and redefined to broaden the scope of activities or to justify the proposed activity as related. Such altered or expanded purpose can be described in Schedule O, Form 990, to evidence the relatedness of a new activity. If loss of exemption3 is a strong possibility because of the extent and amount of unrelated business activity planned, a separate for-profit organization4 can be formed to shield the organization from a possible loss of exemption due to excessive business activity.

21.1 IRS Scrutiny of Unrelated Business Income

Since 1989, with Core Part VIII of Form 990 and Part XVI-A of Form 990-PF, the IRS has had a tool with which it can scrutinize the UBI issue. Until an analysis of revenue-producing activities was added to the forms, UBI was not identified in any special way on Forms 990. The UBI was simply included with related income of the same character. The congressional representatives and the IRS agreed that there was insufficient information to propose changes to the existing UBI rules. Returns currently separate income into three categories:

- Related or exempt function revenue including program service revenue identified with a business code from Form 990-T that describes its nature.

- Unrelated business revenue that should be reported on Form 990-T.

- Revenue excluded from tax under §§512, 513, or 514. The IRS's first scrutiny of the new information found a 50 to 60 percent compliance rate with UBIT requirements. When it assessed the years 1997 and 1998, it found that a large number of social clubs were failing to file Form 990-T. The preliminary report on the IRS nonprofit colleges and universities tax law compliance study reported that they planned to analyze the data to determine “whether it indicate[d] a broader compliance concern in the unrelated business income areas.”

A significant portion of the private letter rulings issued consider this subject. If it is examined, a tax-exempt organization should expect the IRS to carefully scrutinize the nature and source of earned income to determine related or unrelated character. The IRS 2012 Annual Report and FY 2013 Work Plan announced that they will continue exams for organizations that report unrelated business income and fail to file Form 990-T. The IRS also said it planned to analyze Form 990-T data to develop risk models that will help the division identify organizations that report “significant gross receipts” from unrelated business activities but do not declare any tax due. This effort will be used in connection with a “coming UBIT project.”5 The July 2015 Update on the IRS's Priority Guidance plan made no mention of the project.

21.2 History of the Unrelated Business Income Tax

Before 1950, a tax-exempt organization could conduct any income-producing activity, and in fact many operated businesses and paid no income tax on the profits. Under a destination-of-income test, the income earned from a business was tax-free so long as it was expended for exempt activities. In view of its extensive operations, the IRS tried in the late 1940s to tax New York University Law School's profits from its highly successful spaghetti factory.6 The court decided that no tax could be imposed under the then-existing Tax Code, as the profits were used to operate the school.

In response to pressure from businesses, Congress established the unrelated business income tax in 1951 with the intention of eliminating the unfair competition charitable businesses represented; however, the rules do not prohibit its receipt. The congressional committee thought that the

[t]ax free status of exemption §501 organizations enables them to use their profits tax free to expand operations, while their competitors can expand only with profits remaining after taxes. The problem … is primarily that of unfair competition.7

A key question in identifying UBI is, therefore, whether the activity that produces earned income competes with commercial businesses and whether the method of operation is distinguishable from that of a for-profit entity. The second question is whether the income-producing activity accomplishes the organization's exempt purpose. These questions are sometimes difficult to answer. The distinction between for-profits and nonprofits has narrowed over the years as organizations search for creative ways to pay for program services. Consider what the difference between a museum bookstore and a commercial one is, other than the absence of private ownership. Privately owned for-profit theaters operate alongside nonprofit ones. Magazines owned by nonprofits, such as National Geographic and Harper's, contain advertising and appear indistinguishable from Traveler or Time magazine. The health-care profession is also full of indistinguishable examples. The Tax Court in one case was of the opinion that “unfair competition plays a relatively insignificant role in the application of the amended unrelated business tax.”8 A circuit court expressed the same sentiment, saying that “competition alone does not determine whether an unrelated trade or business should be taxed.”9 The organization had argued that it was not competing with any taxable business, while the government argued that tax on unrelated business income is not limited to competitive business.10

21.3 Consequences of Receiving UBI

There are potentially several unpleasant consequences of earning unrelated income.

- Payment of unrelated income tax. Unrelated net income is taxed at corporate or trust rates, with estimated tax payments required. Social clubs, homeowner's associations, and political organizations also pay the UBI tax on certain passive investment income in addition to the unrelated business income.

- Exempt status revocation. The organization's tax-exempt status could be revoked if the unrelated business activity becomes its primary activity, in which case all income is taxed. IRC §501 requires a nonprofit organization to be both organized and operated exclusively for an exempt purpose, although exclusively does not mean 100 percent.11

- Excess business holdings. A private foundation may not operate a business and is limited in the ownership percentage it can hold in a separate business entity.12

In evaluating the amount of unrelated business activity that is permissible, not only the amount of gross revenue but also other factors may be taken into consideration. Nonrevenue aspects of the activity, such as staff time devoted or value of donated services, are factors that might be determinative. The basic issue is whether the operation of the business subsumes, or is inconsistent with, the organization's exempt activities.

A complex of nonexempt activity caused the IRS to revoke the exemption of the Orange County Agricultural Society.13 Its UBI averaged between 29 and 34 percent of its gross revenue. Private inurement was also found because the society was doing business with its board of directors. A medical aid plan producing 22 percent of revenue was found to be a primary, nonexempt purpose.14 In contrast, the IRS privately ruled that a 50–50 ratio of related to unrelated income was permitted for a day care center raising funds from travel tours.15 The revenue ratio was not solely indicative of the primary exempt activity of caring for children.

An organization with unrelated income in excess of 15 to 20 percent of its gross revenue must be prepared to defend its exempt status by showing that it focuses on its mission purposes rather than on its business activities. An organization can run a business as a substantial part of its activities, but not as its primary purpose.16 The presence of a single nonexempt purpose, if more than insubstantial in nature, can defeat exemption, regardless of the number or importance of the truly exempt purposes.17

Where there is concern that the amount or character of unrelated activity might cause a challenge to the organization's underlying exempt status, distributing the activity to a for-profit subsidiary might be necessary.18 The IRS, however, has said in one instance that a parent's exempt status may be jeopardized if the commercial activities of its subsidiary can be considered to be in fact activities of the parent. If the parent corporation so controls the affairs of the subsidiary that it is merely an instrumentality of the parent, the corporate subsidiary may be disregarded. This is because the subsidiary is in reality an arm, agent, or integral part of the parent.19

The possibility of loss of exempt status when a significant portion, if not all, of an organization's income is unrelated business income is a question with no precise answer. Even if all of an organization's income stems from unrelated sources, all of the facts and circumstances must be considered.20 The most important issue is whether the mission is the primary focus of the organization. What is referred to as the commensurate test is one method of finding an answer.21 It is important to note that there are very few cases or rulings reaching the conclusion that exempt status should be revoked.

21.4 Definition of Trade or Business

To have unrelated business income, the nonprofit must first be found to be engaging in a trade or business. Trade or business is defined very broadly to include any activity carried on for the production of income from the sale of goods or performance of services.22 The Tax Court added to this by describing a trade or business as one that is conducted with “continuity and regularity” and in a “competitive manner similar to commercial businesses.”23 This is an area where the tax rules are very gray. The word income does not mean receipts or revenue and also does not necessarily mean net income. IRC §513(c) says: “Where an activity carried on for profit constitutes an unrelated trade or business, no part of such trade or business shall be excluded from such classification merely because it does not result in profit.”

The regulations couch the definition in the context of unfair competition with commercial businesses, saying that “when an activity does not possess the characteristics of a trade or business within the meaning of §162,” the UBIT will not apply.24 However, these regulations were written before the IRC §513(c) profit motive language was added to the code. They are the subject of continuing arguments between taxpayers and the IRS, and the confusion has produced two tests: profit motive and commerciality.

(a) Profit Motive Test

Under the profit motive test, an activity conducted simply to produce some revenue without an expectation of producing a profit (similar to the hobby loss rules) is not a business.25 An insurance program entered into with “dominant hope and intent of realizing a profit and otherwise possessing the character of a trade or business” is unrelated.26 This test is applied in situations when a nonprofit has more than one unrelated business. Losses from the unprofitable activity or hobby cannot necessarily be offset against profits from other businesses. Likewise, the excess expenses (losses) generated in fundamentally exempt activity, such as an educational publication undertaken without the intention of making a profit, cannot be deducted against the profits from a profit-motivated project.27 Social clubs have continually battled with the IRS about this issue.28

(b) Commerciality Test

The commerciality test looks to the type of operation: If the activity is carried on in a manner similar to a commercial business, it constitutes a trade or business. This test poses serious problems for the unsuspecting because there are no statutory or regulatory parameters to follow. A broad range of UBI cases where the scope of sales or service activity was beyond that normally found in the exempt setting have been decided by examining the commercial taint of the activity.29 The primary purpose for the activity is determined by reference to the “manner in which the activities are conducted, the commercial hue of those activities, and the existence of and amount of annual or accumulated profits.”30 An organization regularly operating an investment service business, even though its customers were other tax-exempt organizations, was found not to qualify for tax exemption because providing investment services on a regular basis for a fee is a trade or business ordinarily carried on for profit.31

Similarly, because a conference center was operated in a commercial manner on a break-even basis, it too was denied exemption.32 It organized and sponsored more than 600 educational conferences a year in areas as diverse as civil and human rights, international relations, public policy, the environment, medical education, mental health, and disability. Twenty percent of the events were held for government clients, 50 percent for nonprofit and/or educational clients, and 30 to 40 percent for “other” users, including many weddings and other private events. Only a few of the events were financially subsidized with lower prices. The court said, “as it is clear from the facts that plaintiff engages in conduct of both a commercial and exempt nature, the question whether it is entitled to tax-exempt status turns largely on whether its activities are conducted primarily for a commercial or for an exempt purpose” and decided the former was true.33 The fact that Airlie was seeking to recover tax-exempt status previously lost due to private inurement issues may have influenced the case. Exhibit 21.1 highlights characteristics which indicate that an organization is operating in a commercial fashion.

EXHIBIT 21.1 Commerciality Test Checklist

| “YES” answers to questions are warnings that signal the EO's exposure to a challenge that the organization operates in a commercial manner and may not be exempt. | ||

| Yes | No | |

| COMPETITIVENESS: Does the exempt organization's activity compete with for-profit businesses conducting the same activity? Is there a counterpart for the activity in the business sector, particularly a small business? | ||

| PERSONNEL MOTIVATION: Do managers receive generous compensation? Is the activity run by well-paid staff members? | ||

| SELLING TECHNIQUES: Are advertising and promotional materials utilized? Are retailing methods, such as mail-order catalog or display systems, similar to those of for-profit enterprises? | ||

| PRICING: Is the highest price the market will bear charged for goods and services? There are no scaled or reduced rates available for members of a charitable class. | ||

| CUSTOMER PROFILE: Are the organization's services and goods for sale to anyone? Are they available to the general public on a regular basis, rather than only for persons participating in the organization's other exempt activities? | ||

| ORGANIZATION'S FOCUS/GOOD WORKS RATIO: Does the organization conduct significant other charitable program activity? Is the income-producing activity its primary focus rather than exempt ones? | ||

| CHARACTER OF ORGANIZATION'S SUPPORT: Is very little or none of the organization's support from voluntary contributions, grants, or other unearned sources? | ||

Dedicating the profits to charity (sounding like Newman's Own) from selling flowers at market prices on a website failed the “commerciality test” factors listed in Exhibit 21.1. The activity competed on a regular and continuous basis with for-profit businesses, and the fact that the purchaser could designate the charitable recipient did not make the activity a qualifying exempt function.34 Another question to consider is whether the business represents a “substantial nonexempt purpose.” A coffee shop started by members of a church for the express purpose of prayer and proselytization, and planning to give away all the profits, still failed the exempt purpose test.35 Religious activities were not conducted. It was located in an area with no other shops, open for regular business hours, and was rented to others for private events.

Promotion of a professional sports rodeo and advancement of information and knowledge concerning rodeos was found not to serve an educational purpose qualified for tax-exempt status.36 Similarly, an organization planning to “design and sell clothing online to consumers ‘while reaching out to the needy and to veterans'” did not have an acceptable exempt purpose. The fact that for every shirt sold a shirt was donated to someone in need did not remove the “commercial hue” of the selling activity.37 Providing durable medical equipment to patients discharged from hospital but still needing rehabilitation at commercially competitive prices was deemed an unrelated business.38

(c) Fragmentation Rule

Further evidence of the overreaching scope of the term trade or business is found in the fragmentation rule.39 This rule carves out an activity carried on alongside an exempt one and proves that unrelated business does not lose its identity and taxability when it is earned in a related setting. Take, for example, a museum shop. The shop itself is clearly a trade or business, often established with a profit motive and operated in a commercial manner. Items sold in such shops, however, often include educational items, such as books and reproductions of artworks, that serve an exempt purpose. The fragmentation rule requires that all items sold be analyzed to identify the educational, or related, items the profit from which is not taxable, and the unrelated souvenir items that do produce taxable income. The standards applied to identify museum objects as related or unrelated are well documented in IRS rulings.40

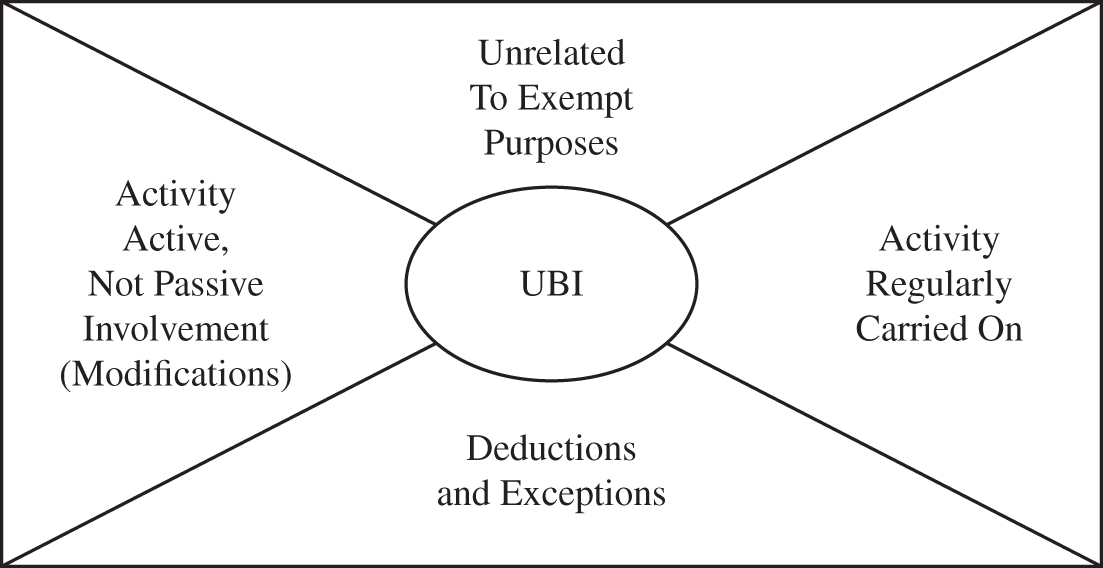

21.5 What Is Unrelated Business Income?

“Unrelated business income” is defined as the gross income derived from any unrelated trade or business regularly carried on, less the deductions connected with the carrying-on of such trade or business, computed with modifications and exceptions.41 The italicized terms are key to identifying UBI. Exhibit 21.2 shows them graphically. Characteristics in all four prongs surrounding the circle must be considered to determine when earned income is to be classified as UBI.

EXHIBIT 21.2 Components of Unrelated Business Income

In a complex nontax case involving a violation of the Pension Benefit Guaranty Corporation (PBGC) standards, a private equity fund was found to be conducting a business42 owned by an employer pension plan, which acquired controlling interests in struggling companies. It became involved in restructuring and operational plans, building management teams, and otherwise involved itself in operating the companies. The fund did not sell goods or perform services, but instead sought to enhance the value of the companies in which it invested. The court deemed that the activity went beyond passive investing and instead was a trade or business because it was an “investment plus.” The approach taken by the PBGC has been dubbed an “investment plus” standard.

21.6 “Regularly Carried On”

A trade or business regularly carried on is considered to compete unfairly with commercial business and is fair game for classification as a taxable business. In determining whether an activity is regularly carried on, one looks at the frequency and continuity of an activity in comparison to commercial enterprises. The normal time span of comparable commercial activities can also be determinative.43 Exhibit 21.3 compares regular and irregular activities.

(a) Meaning of Irregular

Intermittent activities may be deemed regularly carried on or to have commercial characteristics unless they are discontinuous or periodic. For example, the revenue from a monthly (certainly weekly) dance is likely to be classified as UBI; an annual fund-raising event that features dancing would not. By the same token, ads sold for a monthly newsletter would be classed as regular commercial activity; program ads sold for an annual ball may not. Where the planning and sales effort of a special event or athletic tournament are conducted over a span of time throughout the year, the IRS deems the activity itself to be regularly carried on despite the fact that the event occurs infrequently, on an annual or biannual basis.44

EXHIBIT 21.3 Determining Regular Activity

| Irregular | Regular |

| Sandwich stand at annual county fair | Café open daily |

| Annual golf tournament | Racetrack operated during racing “season” |

| Nine-day antique show | Antiques store |

| Gala Ball held annually | Monthly dance |

| Program ads for annual fund-raising event | Advertisements in quarterly magazine |

Congress specifically mentioned income derived from an annual athletic exhibition in stating that the UBI applies only to business regularly carried on.45 When the IRS proposed taxing broadcast rights, it argued that preparatory time, not the actual playing time, determines regularity. If an event or program takes the entire year to produce, the span of time spent negotiating contracts and otherwise working on the event is considered. Examples of the arguments follow:

- Time spent by volunteers in soliciting advertisements or sponsorships were to be considered in evaluating the time span of the activity.46

- An eight-month concert season program was ruled to be comparable to commercial entertainment operations and thereby regularly carried on.47

- The National College Athletic Association (NCAA) convinced the court that an independent company's year-round effort to sell ads for the Final Four championship basketball tournament program was not attributable to the NCAA. The three-week duration of the tournament made it irregular and the program income excludable from UBIT even though the activity was an unrelated business.48

- Year-round sales effort for ads in a labor organization's yearbook, in the IRS's eyes, meant the activity is regularly carried on. The facts indicated that the yearbook had relevance to the members throughout the year and the vast majority of advertisements carried a definitely commercial message.49

- One private ruling, however, said it would be difficult to conclude that an annual ball, which occurs only once each year, is regularly carried on.50

- Biannual publication of a business league's directory was also ruled to be a regular activity; the every-other-year publication cycle was regular or normal in commercial settings. The IRS opined that continuity did not necessarily mean “continuously,” but rather having a connection with similar activities in the past that will be carried forward into the future.51

Payment made to a statewide farm federation under a nonsponsorship and noncompetition agreement was made in a nonrecurring transaction.52 Although there was profit motive in making the agreement, no regular trade or business activity occurred when the federation agreed not to compete with the successor to its regional cooperative organization.

When the Museum of Flight Foundation rented the first Boeing 747 back to the company to use for testing purposes, the IRS contended that the personal property rent paid by Boeing to borrow the plane back for testing purposes was taxable unrelated business income. A court overturned the decision and found that the lease was not a business regularly carried on and agreed with the museum that the transaction was a “one-time, completely fortuitous lease of unique equipment.”53

(b) Seasonal Activity

Activities conducted during a period traditionally identified as seasonal, such as Christmas or Thanksgiving, if conducted during the season, will be considered regular and the income will not qualify to be excluded from UBIT. Greeting cards sold during October or November or Independence Day balloons sold in June/July would be regular sales activity.

21.7 “Substantially Related”

An activity is substantially related only when it has a causal relationship to the achievement of the organization's exempt purpose,54 that is, the purpose for which the organization was granted exemption based on its Form 1023 or 1024 and subsequent Forms 990 filings. This requirement necessitates an examination of the relationship between the business activities—producing and distributing goods or performing services—that generate the particular income in question and the accomplishment of the organization's exempt purposes.55

Any business the conduct of which is not substantially related (aside from need to make money) to the performance of an organization's charitable, educational, or other purposes or function constituting the basis of its exemption is defined as unrelated.56

The size and extent of the activity itself and its contribution to exempt purposes are determinative. The nexus—association, connection, or linkage—between the activity and accomplishment of exempt purposes is examined to find relatedness. The best way to illustrate the concept is with examples. Notice, in reviewing the following examples, that relatedness must be considered in the context of the entity's category as an educational and charitable organization rather than a business league or social club.57

(a) Examples of Related Activity

Related income-producing activities include the following:

- Admission tickets for performances or lectures.

- Student or member tuition or class fees.

- Symphony society sale of symphonic musical recordings.

- Products made by handicapped workers or vocational trainees.58

- Hospital room, drug, and other patient charges.

- Commercial stores employing developmentally or emotionally disturbed persons.59

- Agriculture college sale of produce or student work.

- Sale of educational materials (see §21.13 for museum issues).

- College golf course usage by students and faculty.60

- Secretarial and telephone answering service training program for indigent and homeless persons.61

- Sale of online bibliographic data from EO's central databases.62

- “Public entertainment activities,” or agricultural and educational fair or exposition (§21.9(d)).

- “Qualified conventions and trade shows” (§21.9(e)).

- Producing tapes of endangered ethnic music.63

- Birthing center operated as a part of a church in respect of its religious tenets and belief that birth is a sacred and spiritual event.64

- Coffee shop designed as a convenient eating place for cultural center; visitors and employees accessed from inside the building.65

An “interactive virtual library” selling access to both its collections and staff over the Internet, just as if one were visiting the library in person, as well as providing advice based on its expertise in library science to other libraries and businesses, was considered a related activity for a library.66 Sales of caskets for use in connection with religious burial ceremonies or services of the church of which the monastery is a part furthers its exempt religious purposes, but sales of caskets to members of the general public would be unrelated business activity for the religious group.67

(b) Sales of Goods or Merchandise

Many tax-exempt organizations sell physical items that are used in connection with conducting programs. In deciding why and when the sale of such goods is treated as an activity that has a causal relationship to an organization's mission, several factors must be considered. Items reflecting the organization's mission, such as a T-shirt displaying the universal symbol of breast cancer in pink68 or a reproduction of a work of art on playing cards sold in a museum gift shop,69 are treated as advancing the mission.

A private ruling that is worth study involved an EO dedicated to educating the public that early detection of breast cancer saves lives. The organization advanced this mission through various means, including a website, help line, community-based breast education, screening and treatment programs, and a variety of educational materials designed to meet the breast health and breast cancer information needs of the population.

The educational materials cover the topics of general breast health, risk factors and prevention, early detection, diagnosis, treatment, after treatment, support issues, specific populations, and resources. Merchandise displaying the pink universal symbol of breast cancer awareness is sold on the EO's website, including shirts and other apparel, jewelry, pins, and other items. Each item offered for sale is evaluated for its relevance and appropriateness to the mission. A bookmark providing a recommended three-step approach to positive breast health is included with each purchased item. E-mail confirmation statements confirming a purchase recommend regular screening for breast cancer as well as the toll-free number and website. The IRS found that the sale of the items was related to the organization's exempt purposes and does not constitute an unrelated trade or business.70

Operation of a weekly flea market by the alumni association of a community college was deemed unrelated to its exempt purpose of providing financial and civic support to the college. Additionally, the fees received from market vendors were not rent excludable from the unrelated business income as a modification.71 Other alumni associations have received rulings on revenue-raising activity that one should study in this context.72

In what one might think is an alarming private ruling, the IRS, with no description of the “products” sold through an online catalog and a print catalog at various retail outlets, deemed the sales activity to be an unrelated business. Because the ruling lacks sufficient details to understand the negative conclusion, it is important to reread 1973 revenue rulings that have formed the standards for evaluating relatedness of such sales.73

EXHIBIT 21.4 Sale of Merchandise

NATURE OF ITEMS SOLD:

- Are the objects actually used by the purchaser to participate in the organization's exempt activities?

- What is the intended use of the merchandise by the purchaser?

- Are items sold through a website or shop open to the general public?

- Is the nexus between information on items sold and objects displayed and used in the school, church, museum, or other type of exempt organization sufficient to create necessary relatedness?

METHODOLOGY OF SALES ACTIVITY:

- Does the manner in which the sales activity is conducted evidence commerciality? Use the Exhibit 21.1 checklist to find this answer. For publications, apply tests found in §21.15.

MOTIVATION FOR SALES ACTIVITY:

- Was a gift shop established to generate profits or to distribute educational items?

- Does the shop sell both related and unrelated items? Standards discussed in §21.13 for museum shops to fragment or identify those objects that qualify as related to exempt purposes and those that do not can be applied.

NONCOMMERCIAL CHARACTER:

- Does one of the exceptions apply evidencing the noncommercial nature of the sales activity? See §21.9.

- Are the shop personnel volunteers?

- Is merchandise donated?

- Is the sales activity irregularly conducted? See §21.6.

Exhibit 21.4 presents a checklist of issues to consider when the tax-exempt organization sells merchandise.

(c) School Athletic and Entertainment Events

College-sponsored events have traditionally been thought to foster school spirit and advance the educational purposes of the schools. Revenues produced through sales of admission tickets, event programs, refreshments, and similar items have not normally been treated as UBI. Legislative history underlying the UBI provisions states that “athletic activities of schools are substantially related to their educational functions. For example, a university would not be taxable on income derived from a basketball tournament sponsored by it, even where the teams were composed of students from other schools.”74

Payments for radio and television broadcast rights, however, have been controversial. In 1977, the IRS advised Texas Christian University, Southern Methodist University, the University of Southern California, and the Cotton Bowl Athletic Association that revenue derived by the universities from the telecasting and radio broadcasting of athletic events constituted unrelated trade or business income. In 1978, the IRS reversed its position after a challenge by the Cotton Bowl and National College Athletic Association.75 In 1979, the IRS further expanded its position regarding such events and provided a good outline to determine if the income is UBI:76

- Sales of broadcast rights were regularly carried on and the activity was looked at as a profit-motivated trade or business activity, with extensive time expended in training the teams and preparing for the game.

- The events were regularly carried on (systematic and consistent, not discontinuous or periodic).

- Games, however, were related to the Cotton Bowl's exempt purpose. Income from sale of the game broadcast was a byproduct because it was presented in its original state and provided a simultaneous extension of the exempt-function game to the general public.

A long series of IRS proclamations on the subject were issued in following years concerning the sale of broadcast rights by colleges, all of which ruled that such sales produced related income.77 These arguments eventually led to a Tax Code revision that permits payments in the form of a sponsorship, acknowledged with noncommercial language, to be treated as a contribution.78

In 1981, the IRS applied the commerciality test79 to find the promotion of rock concerts in a “multipurpose college auditorium” a taxable unrelated activity. The college's goal to maximize revenue to the exclusion of other considerations indicated that the facility was not operated as an educational program. The nature of the entertainment and the audience were not the criteria used to judge the activity's relatedness; instead, the detrimental fact was the college's selection of events based on their profitability. The facts outlined in the ruling evidencing the businesslike manner of conduct were as follows:80

- During the school year, 45 ticket events were held, 44 percent of which were rock concerts.

- Contemporary professional entertainers comprised 40 percent of the concert season.

- The facility was managed by a director with more than 30 years' experience in promoting commercial events.

- The school's fine arts department had no involvement in the selection of events to be held at the center and normally did not participate.

- Twenty-six percent of the tickets were sold to nonstudents.

- Tickets were sold through a commercial ticket service.

- Ticket prices for students were not discounted.

- Concerts were generally indistinguishable by price or type of performance from similar events provided by commercial impresarios.

- Compensation to the performers was negotiated and generally the same as compensation paid by for-profit centers.

In another ruling, spouses and children of students, spouses and dependents of a university's employees, university alumni, and members of a President's Club (big donors and guests) were deemed to be unrelated users of a university's golf course. The IRS ruled that only use by full- and part-time students and employees was substantially related and that there was no causal relationship between the university's educational purposes and use of its golf course by any other persons.81

An alumni association was found to be on the wrong side of the fine line between fund-raising and performing exempt functions. The association claimed to be attracting new students and donors for a low-income community college. The association aided the college with scholarships, facility and library improvements, and traditional alumni events for students, faculty, alums, and community leaders.

The IRS found that the website only promoted the events and did not feature recruitment information for students and alums in classifying the events, thus producing unrelated business income. Weekly parties were held in the college parking areas featuring arts and craft vendors, entertainment, a farmers' market, and refreshment booths. The events were not staffed by volunteers. In sum, the IRS found that the events did not advance the association's mission and did not qualify for excusal from the unrelated business income tax classification. Nonetheless, the IRS has for many years held that fund-raising and grant making can be charitable activities if the commensurate test is met.82 In this instance the lack of information about their mission and accomplishments, both at the events and on the alumni website, inspired the IRS decision, which perhaps was in error.83

21.8 Unrelated Activities

The types of income that potentially can be treated as unrelated income are numerous, as the following types of income that have been controversial illustrate. The examples do not always follow a logical pattern because courts and the IRS do not always agree, and the IRS has not always been consistent in its rulings. To further complicate the matter, rules applicable to one type of income are not necessarily applied to another type.

(a) Rentals

Rentals of equipment and other personal property (such as computers or telephone systems) to others are specifically listed in IRC §512(b)(3) as a type of unrelated business income. Such a rental is presumed to be undertaken only to collect revenue to cover costs, with no direct connection to the organization's own exempt purposes. Whether rental charges are at, below, or above cost can be determinative in evaluating relatedness. A full fair market value rental arrangement might be considered evidence of lack of exempt purposes, although the taint can be overcome by other reasons for the rental, such as dissemination of specialized educational information. Such rental is said to exploit the exempt holding of the property. However, this general rule is not applicable in situations where the rental serves an exempt purpose, such as the following:

- Renting to, or sharing with, another nonprofit or, conceivably, an individual or a for-profit business is related if the rental expressly serves the landlord's exempt purposes. A museum's rental of artworks—which would otherwise be kept in its storage—to other institutions to ensure maximum public viewing of the works serves an exempt, and thereby a related, purpose.

- Rental of computers to its students, to facilitate their learning experience, would be a related activity for a school.

When the practice first became prevalent, the IRS took the position and fought hard to treat the fees for use of an organization's mailing list as unrelated rental income. After several unsuccessful court battles, they conceded that the income was excludable under the passive exception for royalties.84 Real estate rentals are also excluded from UBI under the passive exceptions, but only if the property is unencumbered and not debt-financed property.85

(b) Services

Rendering services by a charitable organization for its exempt constituents—students, patients, the underprivileged, or the parishioners—that accomplish an organization's mission is unquestionably a related activity. Certain types of services are inherently treated as related exempt activities: teaching, healing the sick, feeding the poor, or performing religious rites, for example. Organizations exempt under IRC §501(c)(3) perform services in pursuit of eight specific, but fairly broad, exempt purposes.86 Services that other types of exempt organizations may provide are actually narrower. A business league, labor union, social clubs, and others must perform only services that accomplish the mission and benefit the industry, the union, or the club, not the EO's members as individuals. Services normally provided by commercial companies, such as job placement or employment counseling, do not serve a charitable purpose.87

Services Provided to an Unrelated Nonprofit. Rendering services, such as billing, technical assistance, or administrative support, to other nonprofits does not serve the exempt purposes of the service provider, and is considered unrelated.88 The fact that sharing creates efficiencies that allow all the nonprofits involved to save money, or improves program administration of the other nonprofits, does not necessarily cause the activity to be related. Providing services for a fee below, at, or for cost plus a modest profit may also not serve an exempt purpose and “is not charitable because of the absence of a donative intention.”89 Only where the services themselves represent substantive programs better accomplished by selling the services to other organizations is the revenue considered related.

- The Tax Court sanctioned the sharing of computer database technology for a group of libraries based on the concept that if an activity was a necessary component part of the operation of one library, it served an exempt purpose to provide the service to other exempt organizations.90 A regional computer network to collect and disseminate scientific and educational information for member educational organizations posed a similar case.91

- Assistance in management of endowment funds by participating colleges and universities for a charge substantially below cost was an exempt purpose.92

- Training courses furnished by a university to a business were sanctioned.93

- An HMO service provider created to provide management consulting to other exempt HMOs was not itself exempt.94 Similarly, the exempt status of an organization providing management and administrative services to rural hospitals was revoked despite the fact that it had been a tax-exempt organization since 1956.95

- Internet service providers are considered to sell business services and have mostly been found not qualified for tax exemption.96

- A entity formed by unrelated exempt organizations (two (c)(3) and two (c)(6)) was not granted (c)(3) recognition of exemption for a new entity formed to provide centralized administrative functions of payroll, personnel, accounting, and fund-raising. The IRS said the activity was no different than an ordinary commercial business.97

- Drug testing for a commercial company is not an exempt activity.98

A nonprofit formed to create an 800-mile high-speed fiber-optic broadband telecommunications network to provide a backbone to support the proposed expansion of various high-speed telecommunications services in a rural area was found to serve a substantial nonexempt commercial purpose and therefore not be qualified for charitable exemption. The rural area in which the network would be established was serviced by standard telephone, cellular, and Internet technologies. The new entity sought to be the “carrier's carrier” by providing wholesale high-speed broadband connection paths to commercial telecommunication companies, who would then provide retail high-speed broadband communication services to individual subscribers. In other words, the IRS found it would provide the “backbone” through which commercial providers would offer their services to the public. The network would be open to all commercial providers or others requiring high-speed broadband.99 Taking a contrasting position, a subsidiary of the business league was found to realize related, rather than unrelated, income. It performed lab testing for manufacturers seeking to gain certification with proof that their products meet the standards. Testing was essentially done on behalf of its parent organization, which creates and maintains the industry standards. The IRS ruled that the testing service benefited the industry as a whole by ensuring public health and safety.100

The fact-driven issue of whether rendering services serves an exempt purpose brings many private ruling requests. Services offered to the general public continue to be treated as serving the purpose of the purchaser of the services rather than the mission. The first fact on which the rulings rest is whether the purchasers are members of a charitable class, such as the sick, poor, or uneducated. Examples of services offered for the purposes embodied in the charitable genre include:

- Providing hospital lab testing services to nonhospital patients was found to promote health and to serve an exempt purpose when there was no other hospital laboratory within a reasonable distance for those living in the area in which the hospital was located. Therefore, the services were related to the hospital's charitable mission.101

- A's performance of laboratory testing for the patients of private physicians located in B and the surrounding communities served by A is a related business. The provision of laboratory services for those doctors was deemed to be substantially related to A's tax-exempt purpose of improving the health of B and its surrounding communities.102

- A website established to provide an “automated fundraising online marketplace” for manufacturers, distributors, and other corporations to donate net profits from sales to charities was deemed to be a commercial business conducting an unrelated activity. The applicant undoubtedly thought the activity was exempt because all of the profits went to charity, but the IRS opined that it failed the operational test.103

- The IRS continues to distinguish between services that are charitable because they accomplish a charitable purpose and those they deem to be administrative and clerical commonly conducted by the business community and not unique to the charitable sector, particularly when it involves electronic media.104 During 2014, they applied this opinion to refuse to grant exemption to an organization formed to provide information access to unserved and underserved business communities and to prevent business deterioration in minority communities through technology.105

- Collecting donations earmarked by donors to specific “partners” with a “secure mass donation process” is not an activity qualifying for exemption under §501(c)(3). As a coordinator of software that allows donations from mobile devices, the entity would provide marketing, donation processing and collection, and distribution and reporting of results for fees including a monthly fee for use of a keyword and transaction fees based on the amount of credit card processing fees. As discussed earlier in this section and later for community foundation services, such services include those that are administrative and clerical and are not unique to the charitable sector, and instead are readily available throughout the business community.106 Similarly, a scholarship program created by a §501(c)(4) organization that conducts a beauty pageant could not qualify for exemption under §501(c)(3) because it “provided private inurement to the benefit of a private shareholder or individual.”107

Grant management services provided by a community foundation to private foundations in its community were fragmented into those services that accomplished an exempt purpose and those that did not. The expressed goal in providing the service was to educate and assist funders to provide more efficient support to the “citizens of X and ultimately for them to establish cooperative relationships with you that will maximize the pool of charitable resources available for the strategic funding of X-based programs.”108 The services “sold at a reasonable fee” were as follows:

- Assist to establish a grant-making program—guidelines and processes and procedures for reviewing requests, and so forth.

- Review/evaluate grant requests, prepare reports on findings, conduct site visits and interviews or other pre-grant inquiries.

- Prepare research in specific grant-making areas of interest and/or those entities conducting programs in specific areas of interest.

- Design and/or maintain a system of monitoring funded programs.

- Identify opportunities for collaborating with other funders.

- Handle day-to-day inquiries (via mail or telephone) from potential grant applicants.

- Print checks (for review/signature by authorized representative of the enrollee) for approved grants/expenses and balance the checking account.

- Organize/staff board and grant committee meetings.

- Track all grant applications and grants awarded and generate related reports.

The IRS found that items 1, 2, 3, and 5 rely on the particular knowledge and skills the foundation had developed through years of awarding grants and coordinating grant-making for the benefit of the entire community. The foundation's work helps to direct charitable giving in the local community more efficiently and increases the foundation's knowledge regarding charitable causes and programs in the community to enhance coordination of its own grant-making program with the grant-making of others.

Conversely, items 4, 6, 7, 8, and 9 were deemed to be administrative and clerical, with the IRS stating,

Your administrative group of services consists of activities requiring the expertise of office staff skilled and educated in general business administration and business management, personnel management and office procedures. The skill set required to conduct these activities is not unique to the charitable sector or to you. Rather, these activities are conducted throughout the business community on a daily basis by individuals such as office administrators, personnel managers, and executive assistants.109

Therefore, those services were unrelated to the mission and would be treated as unrelated business income.110

A nonprofit formed to facilitate fund-raising by individuals and reduce the cost of soliciting such funds to registered organizations was deemed to be conducting a commercial business, not a charitable activity. The nonprofit creates and manages a website for registered charities to accept, process, and forward donations. The nonprofit engaged a related for-profit to manage an “e-commerce” element for the buying and selling of products. Purchasers and sellers can designate a portion of the sales transaction fee to a selected charity registered with the company. Two of the nonprofit directors were co-owners and founders of the for-profit entity. The IRS declared that impermissible private benefit (would better have been described as inurement) resulted from the arrangement so that the nonprofit did not qualify for tax exemption.111

A's performance of laboratory testing for the patients of private physicians located in B and the surrounding communities served by A was found not to be an unrelated trade or business. The provision of laboratory services for those patients was deemed substantially related to, and contributing importantly to, A's tax-exempt purpose of improving the health of B and its surrounding communities, following the unique circumstances test of Rev. Rul. 85-110. Accordingly, A's revenue from such activity is not taxable as UBI.112

Alumni associations have received a wide range of rulings on revenue-raising activity that one should study in this context.113

Services Provided to an Affiliated Organization. Although providing business services to an unaffiliated organization is usually treated as an unrelated activity, such services provided to an affiliated exempt entity may be related.114 When services rendered by one member of a related group of organizations to others in the group are essential to the exempt functioning of the group, the services are considered to accomplish an exempt purpose. A wide range of services, including campus security, telephone and mail service, a central steam plant, financial services, an auditorium, a faculty house used for meals and meetings, a medical center, a library, and an interfaith fellowship center, provided by a graduate school to its related “small colleges arranged around a library,” were related to accomplishment of the school's exempt purposes.115 Similarly, cash management and investment services for school districts were an acceptable mission for an educational organization.116 Though each entity was legally separate, the graduate school's board of fellows included the presidents and board chairs of each member of the group; matters concerning central programs and service were subject to a two-thirds vote. The constitution and the college's bylaws provided for a council made up of the presidents of each college in the group to provide policy guidelines on the administration and development of common programs and facilities.

One ruling considered a hospital support organization created to purchase and operate a computer system for the medical faculty group practice117 and a motel located a short distance from the medical center.118 The doctors using the computers taught medical students, supervised interns and residents, and served private patients. The motel operation was operated as a convenience119 to the patients of the related hospital.

A supporting organization functioning as the parent of its affiliates was found to have related revenue from providing oversight, supervision, management, and strategic planning services to its closely related exempt organizations. The stated IRS rationale was that the sharing of resources “permit[ted] all of the entities to more efficiently carry out their respective tax-exempt operations” and that “transfers were a matter of accounting” and not generally considered a business activity.120

Affiliate organizations for this purpose are usually referred to as being an integral part121 of a group or system. Integrated health-care delivery systems have led the way in clarifying this issue.122 Services rendered to the for-profit organizations in such a group may, however, be treated as unrelated activity.

Cooperative Efforts. When an organization is created to serve a consortium of organizations with a common building or pooled investment funds, the IRS has generally allowed its exemption when the new organization itself is partly supported by independent donations. When services are program related, the cooperative performance of charitable or educational functions has generally been acceptable to the IRS.123

- Certain cooperative service organizations are specifically exempt. IRC §501(e) grants exempt status to cooperative hospital organizations formed to provide, on a group basis, specified services including data processing, purchasing, warehousing, billing and collection, food, clinical, industrial engineering, laboratory, printing, communications, record center, and personnel services. Note that laundry is not on the list.

- Cooperative service organizations established to “hold, commingle, and collectively invest” stocks and securities of educational institutions are also provided a special exempt category under IRC §501(f).

- IRC §513(e) allows a special exclusion from UBI for the income earned by a hospital providing the types of services listed in IRC §501(e) to another hospital that has facilities to serve fewer than 100 patients, provided the price for such services is rendered at cost plus a “reasonable amount of return on the capital goods used” in providing the service.

Member Services. Services furnished to members must also accomplish an exempt purpose to be treated as related. Services provided by churches, schools, hospitals, and most other charitable organizations are ordinarily treated as related. Classification of member services by business leagues, labor unions, and other non-(c)(3) organizations is not always clear. The question is whether the service yields private inurement to the individual member or to the profession as a whole and therefore to the general public. Excessive unrelated member services can imperil an association's exempt status. Chapters 7 and 8 present extensive consideration of this issue.

The fact that services provided to member cooperatives are not directly proportional to the amount of the fees paid indicates that individual economic benefits are not directly tied to the payments. Educational programs to promote farm cooperatives, information regarding economic and social conditions for farmers and farm products, and other services were found by the Tax Court to be conducted by a statewide federation of local county farm bureaus for exempt purposes.124 Regarding a payment under a noncompete agreement, the revenue was found not to stem from the performance of services or the sale of goods so as to produce unrelated business income.125

(c) Licensing Use of the Organization's Name

Licensing the use of an organization's name normally is accomplished by a contract permitting use of the organization's intangible property—its name—with the compensation constituting royalty income that is excluded from UBI.126 Such arrangements can constitute commercial exploitation of an exempt asset if the nonprofit agrees to endorse products, distribute materials on behalf of the list renter, and perform other services associated with use of its intangible property.127 In 1981, the IRS began to propose that the sale of names and mailing lists in connection with insurance programs and other commercial marketing plans resulted in unrelated business income.128 The IRS argued that the extensive involvement of the exempt organization in servicing the membership lists alone made such activity an active business. Later the Tax Court forced them to admit that the licensing of the organization's name and logo alone produces passive royalty income. Endorsements and promotion by the organization in its publications and member/donor correspondence, however, constituted the performance of valuable services that produced unrelated income.129 An agreement containing a requirement that promotional or other services be performed by the organization should be bifurcated to separate the consideration for the royalty and mailing list aspects of the contract.

(d) Advertising

Sale of advertising in an otherwise exempt publication is considered unrelated business income unless an exception applies.130 Advertisements are said to promote the interests of the individual advertiser or company and cannot therefore be related to the charitable purposes of the organization. The corporate sponsorship rules adopted in 1997 bifurcated the rules for advertising. The language and business logo displays permitted for ads placed in a special-event catalog, in a bowl game program, or on a nonprofit television or radio station program are much more favorable than the information that can be displayed in periodicals.131 When the sponsorship standards for quantitative and qualitative data do not apply, what constitutes an advertisement will be a display similar to those found in newspapers and magazines and on radio and television. Except for addressing the question of expense allocations, the regulations contain no mention of periodical advertisements. Most of the guidance available on this subject predates the sponsorship bifurcation. The definitions for advertisement and periodical found in the sponsorship regulations quoted in the next section are said to apply only for that purpose. Readers will, however, find those definitions useful in identifying the character of ads contained in periodicals and should be alert for new developments.

An advertisement contains quantitative and qualitative information that promotes the sale of the sponsor's product or engagement of its services. The following examples are indicative of IRS thinking:

- The American College of Physicians was unsuccessful in arguing that the drug company ads in its health journal published for physicians educated the doctors. The college said the ads provided the reader with a comprehensive and systematic presentation of goods and services needed in the profession and informed physicians about new drug discoveries, but the court disagreed.132

- A college newspaper training program for journalism students enrolled in an advertising course produced related income.133

- Sponsors listed without typical advertising copy may be considered contributors, not advertisers. Different sizes of acknowledgments indicating different amounts of money donated do not cause the ad to be classified as commercial.134

- Advertising revenues received by a police troopers' labor union from sale of business listings and ads in its annual publication were found to be unrelated business income.135 The firm hired to sell the ads and produce the Constabulary was acting on the union's behalf and under its control in an agency relationship136 similar to that found in the NCAA case.

- A professional 501(c)(6) society did not receive taxable UBI in its scholarly journal from advertising under the terms of an agreement with the publisher, because commercial advertising wasn't regularly carried on. The publishing agreement provided that the publisher publishes, produces, sells, distributes, and internationally promotes the journal at its own expense.137

Despite classification of ad revenues as UBI, the formula for calculating the taxable UBI often results in little, if any, taxable income. Using the exploitation method,138 the cost of the publication in which the ads appear, net of any revenue associated with its distribution, are deductible against the net advertising revenue. This formula sometimes yields surprising results that permit ad sale programs to escape tax. See Exhibit 21.5 for the calculation worksheet.

EXHIBIT 21.5 Calculating the Taxable Portion of Advertising Revenue

| BASIC FORMULA: A – B – (C – D) = TAXABLE INCOME | |

| A = GROSS SALES OF ADVERTISING | |

| B = DIRECT COSTS OF ADVERTISING: | |

| Occupancy, supplies, and other administrative expenses | $ ______ |

| Commissions or salary costs for ad salespersons | $ ______ |

| Clerical or management salary cost directly allocable | $ ______ |

| Artwork, photography, color separations, etc. | $ ______ |

| Portion of printing, typesetting, mailing, and other direct publication costs allocable in the ratio of total lineage in the publication to ad lineage | $ ______ |

| Total direct cost of ads | $ |

| C = READERSHIP COSTS: | |

| Occupancy, supplies, and other administrative expense | $ ______ |

| Editors, writers, and salary for editorial content | $ ______ |

| Travel, photos, other direct editorial expenses | $ ______ |

| Portion of printing, typesetting, mailing, and other direct publication costs allocable in ratio of total lineage in publication to editorial lineage (in general, all direct publication costs not allocable to advertising lineage) | $ ______ |

| Total readership costs | $ |

| D = READERSHIP (OR CIRCULATION) REVENUES: | |

| If publication sold to all for a fixed price, then readership revenue equals total subscription sales. | $ ______ |

| Or | |

| If 20% of total circulation is from paid nonmember subscriptions, then price charged to nonmembers times number of issues circulated to members plus nonmember revenue equals readership revenues. | $ ______ |

| Or | |

| If members receiving publication pay a higher membership fee, readership revenue equals excess dues times number of members receiving publication, plus nonmember revenue. | $ ______ |

| Or | |

| If more than 80% of issues is distributed to members free, readership revenue is the membership receipts times the ratio of publication costs over the total exempt activities costs including the publication costs. | $ ______ |

(e) Sponsorships

Sponsorships of a wide variety of events—golf tournaments, fun runs, football bowl games, public television, art exhibitions, and so on—are a favorite form of business support for exempt organizations. The appeal of wide public exposure for sponsoring worthy causes and cultural programs has gained extensive popularity and is thought to make good business sense. The Cotton Bowl Association's payments from Mobil Oil Company were, in 1991, after a lengthy controversy, treated as UBI.139 The IRS found that substantial benefit in the form of advertising was given to Mobil. After an outcry from the exempt community, and in the face of proposed legislation to exempt such payment, the IRS issued proposed regulations concerning the character of sponsorship payments in 1993. The proposals were said to reflect an IRS policy decision not to be responsible for hampering an exempt organization's need to raise private support. The regulation intended to distinguish between commercial advertising and benevolent payments.

In 1997, Congress codified the proposed regulations to delineate those sponsorship payments that constitute a donation from those that represent payment for an advertisement taxable as UBI.140 The provision reduced the uncertainty of reliance on a proposed regulation, but significantly narrowed the definition of an acceptable acknowledgment. The code says the term unrelated trade or business does not include the activity of soliciting and receiving qualified sponsorship payments.141

Qualified Sponsorship Payment. The term qualified sponsorship payment means any payment of money, transfer of property, or performance of services by any person engaged in a trade or business with respect to which there is no arrangement or expectation that the person will receive any substantial return benefit. In determining whether a payment is a qualified sponsorship payment, it is irrelevant whether the sponsored activity is related or unrelated to the recipient organization's exempt purpose.

It is also irrelevant whether the sponsored activity is temporary or permanent. The sponsored activity can be either related or unrelated to the organization's exempt purpose. Qualifying sponsorships can be received in connection with ongoing activities of an extended or indefinite duration and in support of an exempt organization's operations, not just a single event or special series.

When a sponsorship payment is considered unrelated income because return benefits are provided, the payment may still be modified or excluded from tax under another of the many exceptions applicable to unrelated business income, including a once-a-year event or one run by volunteers.142 Importantly, the entire amount of a qualified scholarship payment is treated as a contribution in calculating the public support test.143 The following types of sponsorship payments are not qualified and are subject to the unrelated business income tax rules:

- Any payment that is contingent upon the level of attendance at one or more events, broadcast ratings, or other factors indicating the degree of public exposure to one or more events. The possibility that the event may not occur is not a contingency for this purpose.144

- Periodical and trade show payments that entitle the payor to the use or acknowledgment of the name or logo (or product line) of the payor's trade or business in regularly scheduled and printed materials published by or on behalf of the payee organization that is not related to and primarily distributed in connection with a specific event conducted by the payee organization.145

- Any payment made in connection with qualified convention or trade show activity.146

Substantial Return Benefit. A substantial return benefit does not include (1) goods, services, or other benefit of insubstantial value that are disregarded or (2) the use or acknowledgment of the name or logo of the sponsor's trade or business in connection with the activities of the exempt organization. A benefit provided to the payor may include (1) advertising; (2) certain exclusive provider arrangements;147 (3) providing facilities, services, or other privileges to the sponsor or persons designated by the sponsor; and (4) granting the sponsor an exclusive or nonexclusive right to use an intangible asset, such as a trademark, patent, logo, or designation of the exempt organization.148

Use or Acknowledgment. The code only specifically mentions the use or acknowledgment of the sponsor's name and logo. Anyone watching public TV or radio sees and hears not only the sponsor's name and logo, but also its address, phone number, and often extensive “value-neutral descriptions” of its business. A typical sponsor announcement says, “Black, Brown & White is a 90-year-old plaintiff's law firm with offices around the world serving a broad base of international business clients.” The regulations broaden the code definition by saying:149

Use or acknowledgment may include exclusive sponsorship arrangements; logos and slogans that do not contain qualitative or comparative descriptions of the payor's product-line or services; a list of the payor's locations, telephone numbers or Internet address; value-neutral descriptions, including displays or visual depictions, of the payor's product-lines or services; and the payor's brand or trade names and product or service listings. Logos or slogans that are an established part of a payor's identity are not considered to contain qualitative or comparative descriptions. Mere display or distribution, whether for free or remuneration, of a payor's product by the payor or the exempt organization to the general public at a sponsored activity is not considered an inducement to purchase, sell, or use the payor's product for purposes of the section.

The use of the name or logo (or product lines) of the sponsor in connection with the activities of the exempt organization is not treated as providing a substantial return benefit. The regulations include 12 examples to clarify the rules. Permitted acknowledgments include display of the auto manufacturer's latest-model cars; the sponsor's name in promotions and advertisements of an event; naming the event after the sponsor; the sponsor's name and logo on uniforms, goalposts, and drink cups; and display of the sponsor's logo that sounds like an ad (“Better Research, Better Health”). Items constituting a return benefit include dinners, event tickets, pro-am playing spots, a program advertisement, souvenir flags bearing the team name, a licensing organization's logo, and product endorsements.

Advertising. An advertisement is any message or other programming material that is broadcast or otherwise transmitted, published, displayed, or distributed and that promotes or markets any trade or business or any service, facility, or product. Advertising includes messages containing qualitative or comparative language; price information or other indication of savings or value; or an endorsement or an inducement to purchase, sell, or use any company, service, facility, or product. A single message that contains both advertising and an acknowledgment is advertising. Purchase of broadcast time by the sponsor to be aired during a sponsored event is not treated as an advertisement placed by the organization.

Certain Goods or Services Disregarded. Substantial return benefit does not include goods, services, or other benefits provided to the sponsor or designates that have an aggregate fair market value of no more than 2 percent of the amount of the payment.150 Token items—bookmarks, calendars, key chains, mugs, posters, or T-shirts—bearing the organization's name or logo that have an aggregate cost within the limit established for low-cost articles can be provided to sponsors. The values of all return benefits are combined to determine whether excess benefits are provided. When the 2 percent limit is exceeded in total, the value of all benefits is unrelated income. Say, for example, a $100,000-a-year sponsor requires the exempt organization to place an advertisement in its program that has a value of $2,000. The ad alone does not exceed the 2 percent limit. If tickets for employees worth $1,000 are also provided, the total of $3,000 would be treated as unrelated income. If a $4,000 dinner is instead provided for the sponsor's executives, $4,000 would represent a substantial return benefit, and only $96,000 of the payment is a qualifying sponsorship.

The quid pro quo disclosure rules require that benefits in excess of $75 be valued and reported to corporate sponsors so that even though the benefits are disregarded for sponsorship classification purposes, the donor acknowledgments should report the value of benefits. The fair market value is determined by the willing buyer–willing seller rules.151

Hyperlinks. Happily, a hyperlink to a sponsor's website address is deemed an acknowledgment that does not constitute advertising on behalf of the sponsor. A permissible acknowledgment occurs when a symphony orchestra lists its sponsors on its website and includes a hyperlink to each sponsor's site. If the link is to a page on which the sponsor displays the organization's endorsement of its products, a valuable benefit is provided to the sponsor, and an advertisement has occurred.152

Exclusivity Arrangements. An arrangement for exclusive sponsorship of an exempt organization's activities or representation of a particular trade or business in connection with programs generally does not result in substantial return benefit. However, a sponsorship arrangement that limits the sale, distribution, availability, or use of competing products, services, or facilities in connection with an organization's activity is deemed to be a substantial benefit.153