Ensuring that payment occurs is critical for organizations. Now that items have been ordered, shipped, or delivered in some fashion, it is critical for the enterprise to make sure that it requests payments; this is often done through invoices. It is important to send out correct invoices that correspond to the appropriate orders, shipments, or work efforts. The enterprise needs to set up systems that facilitate getting paid, and this could involve setting up appropriate billing accounts; matching invoices to orders, billing for shipments, invoicing for work efforts; sending out invoices; tracking payments against invoices; recording deposits, and issuing statements.

Questions that enterprises need to know about invoicing include the following:

- How does each invoice relate to orders, shipments, and/or work efforts?

- What are the products, features, and other charges for which payments are due?

- Who owes how much to whom?

- What is the status of each invoice?

- What is the payment history of each party?

Models discussed in this chapter are as follows:

- Invoice and invoice items (alternate model also provided)

- Invoice roles

- Invoice billing account

- Invoice specific roles

- Invoice status and terms

- Billing for shipment items

- Invoicing of work efforts and time entries

- Billing for order items

- Invoice payments (alternate model also provided)

- Financial accounts, withdrawals, and deposits

Invoices, like shipments and orders, may have many items showing the detailed information about the goods or services that are charged to parties. The items on an invoice may be for products, features, work efforts, time entries, or adjustments such as sales tax, shipping and handling charges, fees, and so on.

Figure 7.1a provides a data model with some of the key entities for invoicing. Each INVOICE is composed of INVOICE ITEMs that represent any items that are being charged. The INVOICE maintains header information about the transaction, and the INVOICE ITEM maintains the details of each item that is being charged. Each INVOICE ITEM may have a many-to-one relationship to either PRODUCT or PRODUCT FEATURE. The INVOICE ITEM may also be related to a SERIALIZED INVENTORY ITEM because maintaining the actual instance of the product that was bought with its serial number may be useful. For instance, computer manufacturers often record the serial number of the computer that was bought and invoiced.

Figure 7.1a Invoice and invoice items.

Because INVOICE ITEMs do not relate only to products (i.e., they also relate to work efforts, time entries) other relationships to other entities will be covered later in this chapter. If the item represents a one-time charge item that is not catalogued, then the item description attribute within the INVOICE entity may be used to record what was charged. Each INVOICE ITEM may be categorized by an INVOICE ITEM TYPE, which could include values such as “invoice adjustment,” “invoice item adjustment,” “invoice product item,” “invoice product feature item,” “invoice work effort item,” or “invoice time entry item.” Each INVOICE ITEM has a recursive relationship as it may be adjusted by one or more other INVOICE ITEMs, which would be of INVOICE ITEM TYPE “invoice item adjustment.” Each INVOICE ITEM may also be sold with other INVOICE ITEMs that would be of type “invoice product feature item.”

As with shipments, many things are needed in order to send a correct bill to customers. The first thing to record about the invoice (besides a unique identifier) is the invoice creation date or invoice date. This will be an important piece of information used in tracking the progress of the invoice when a client calls to discuss his or her bill. Some systems may want to include a specific note or message to the customer on the invoice, so the model includes the attribute message. The description attribute describes the nature of the invoice. Table 7.1 shows sample data for the INVOICE entity.

Table 7.1 Invoice Data

Because each INVOICE ITEM may be for a product, product feature, work effort, or time entry or because it may be described via an item description for non-standard items, the relationships to PRODUCT and PRODUCT FEATURE are both optional. When features are shown in invoice items, the recursive relationship sold with should be recorded in order to indicate that the feature was invoiced for a specific invoice item that was for a product. The quantity is optional because there may only be an amount and not a quantity for items such as features where the quantity really isn't necessary and is not applicable.

Instead of tying an INVOICE ITEM recursively to another INVOICE ITEM to record the feature for a product, why not just record both the product and feature on an invoice item? This would not account for invoices that have the same product on two different invoice items. For instance, if an organization bought two different computer servers with different features on each, it would be important to record which combination of features corresponded with which specific products. What if a feature was later added (and invoiced) on an existing product that the customer already has? The invoice item could be related to the initial invoice item that had the product charge.

Table 7.2 provides an example invoice with four items being charged, three for products and one for the feature of special glossy paper for the Johnson fine grade 8½ by 11 bond paper. The second item, which is for extra glossy finish for the Johnson fine grade 8½ by 11 bond paper, includes a recursive relationship to the invoice item for the product in order to show that the item is for a feature within the context of a product.

Table 7.2 Invoice Item Data

In addition to the invoice ID and product or feature, the details include the quantity of items being billed, the amount, and whether this is a taxable item through the taxable flag attribute. Note that product-specific information, such as unit of measure for the quantity, can be derived through the relationship from PRODUCT to UNIT OF MEASURE (see Chapter 3 for more on product definition). Also, notice that the extended price for the item is not an attribute because this is derivable information.

The taxable flag is stored on the invoice item to signify if the item is to be taxed. This cannot always be determined by the item being invoiced because the taxability of an item could vary depending on many circumstances, such as the source and destination of the shipment or the tax status of the purchasing organization. The information needed to calculate taxes is not included in this model because it is highly dependent on the rules and regulations of each geographic boundary.

Other information that enterprises may want to know about an invoice include adjustments to the invoice such as the total tax (after it is calculated), freight charges, and handling charges. Each adjustment is stored as an instance of INVOICE ITEM because these are also charged items. Why was ORDER ADJUSTMENT a separate entity in the order chapter, but invoices include adjustments as instances of an INVOICE ITEM? The reason is that when parties order something, they do not request adjustments such as sales tax, fees, handling charges, and so on. These adjustments are recorded as ORDER ADJUSTMENTs in order to maintain potential expected charges; however, they are still not “ordered items.” INVOICE ITEMs represent charges that are incurred, and these adjustments are included in this definition.

The INVOICE ITEM TYPE could include different types of adjustments such as “miscellaneous charge,” “sales tax,” “discount adjustment,” “shipping and handling charges,” “surcharge adjustment,” and “fee.” If needed, a percentage attribute could be added to the INVOICE ITEM to store the percentage of the adjustment, such as .07 for sales tax.

Table 7.3 contains examples of adjustment data for an invoice.

Table 7.3 Invoice Item Adjustment Data

Using this structure, an enterprise can include any number of adjustments to an invoice that could be of many different types. This is much more flexible than including attributes such as tax amount or freight charge on the INVOICE entity because new attributes would have to be added to the entity if the enterprise discovered that other adjustments needed to be tracked. With this model, the enterprise simply defines new invoice items that may have different INVOICE ITEM TYPEs and then relates additional instances to either the INVOICE or INVOICE ITEM (through a recursive relationship).

Invoice items may be adjusted by other invoice items in another way. For example, suppose there was a mistake in which the quantity of items invoiced was 10 instead of 8, the correct quantity. A future invoice item showing a credit of 2 items could be used to correct the invoice. This correction could be implemented using an INVOICE ITEM with a quantity of -2 that related back to the original INVOICE ITEM that had a quantity of 10. Many enterprises will show corrections using this approach as opposed to modifying the invoice, which could lead to control and audit issues. The recursive relationship around the INVOICE ITEM provides the information necessary for relating invoice items together.

Figure 7.1b provides an alternative model that more specifically illustrates the subtypes of INVOICE ITEM. The INVOICE ADJUSTMENT shows the various adjustment subtypes, and the INVOICE ACQUIRING ITEM represents the items that the party really got, whether they were a product, feature, work effort, or time. Instead of showing the recursive relationships around INVOICE ITEMs to handle features sold with products or adjustments to invoice items, this model has relationships from INVOICE PRODUCT ITEM to INVOICE PRODUCT FEATURE ITEM as well as from INVOICE ACQUIRING ITEM to INVOICE ADJUSTMENT, which enforce more specific business rules.

Figure 7.1b Invoice and invoice items-alternate model.

Of course, enterprises also need to know where to send the invoice and where it came from. Standard models often record only the customer address, and the supplier address is assumed to be the enterprise doing the billing (the “I” model). This model accommodates a more flexible structure for both sales and purchase invoices for a multilocation or multicompany organization.

Figure 7.2 provides a basic data model for the parties involved in the invoice. Each INVOICE may be billed to or billed from any PARTY, and therefore it may accommodate both incoming (PURCHASE INVOICE) and outgoing invoices (SALES INVOICES). The billed to and billed from are the two main roles and represent the party owing the money and the party that is requesting payment.

Figure 7.2 Invoice parties.

In addition to these two key roles, additional roles may be involved in the invoice. The additional roles are maintained by the INVOICE ROLE, which records each PARTY involved in each INVOICE ROLE TYPE for an INVOICE. For example, invoice role types may include “entered by,” “approver,” ”sender,” and “receiver.” The datetime attribute indicates the date and time that the person or organization performed the role.

Flexible means of sending and receiving invoices are needed in order to record from where and to where the invoice was sent because there are many ways to send an invoice. Therefore, Figure 7.2 shows that each INVOICE also needs to maintain the CONTACT MECHANISMs to which the invoice is addressed and the CONTACT MECHANISM from which it was sent. This is related to the supertype, CONTACT MECHANISM, because the INVOICE may be sent or received via numerous subtypes of CONTACT MECHANISM including POSTAL ADDRESS, ELECTRONIC ADDRESS, or TELECOMMUNICATIONS NUMBER. In these days of e-commerce, sending an invoice via e-mail, which is a form of ELECTRONIC ADDRESS, is becoming more and more common. An invoice may be faxed, which is a type of TELECOMMUNICATIONS NUMBER. Finally, an invoice could be sent the old-fashioned way, by addressing it via a POSTAL ADDRESS.

Table 7.4 shows example data for the information maintained about the invoice parties.

Table 7.4 Invoice Parties.

Notice that invoice #30002 has standard addressed to and sent from locations, but #30005 is addressed to an Internet e-mail address. In this situation, the invoice is being sent via e-mail (however, the data shows only the physical address of the sender). For invoice #30010, the data indicates that the invoice is being sent from one electronic mail address to another e-mail.

As more and more enterprises and people get online, this type of transaction will become more prevalent; thus, the need for a more flexible data model will become apparent. Current invoicing systems that require a physical address to mail an invoice may become unusable in the future.

The PARTY CONTACT MECHANISM PURPOSE entity (see Chapter 2, Figure 2.10) could be used for additional validation if an enterprise wanted to implement additional business rules to see if the invoice contact mechanism recorded is valid for invoicing purposes. A possible example would be a rule that states that an invoice may be related only to a PARTY CONTACT MECHANISM with a role of “location for receiving invoices.”

As shown in Figure 7.3a, there is another way to bill a customer in addition to sending a bill to a PARTY, namely through the use of a BILLING ACCOUNT. This method of billing is used only in certain circumstances for specific types of businesses. Therefore, the BILLING ACCOUNT, BILLING ACCOUNT ROLE, and PARTY entities and their associated relationships in Figure 7.3a are optional and are included only if the enterprise has a need to maintain billing accounts.

Figure 7.3a Billing account.

A BILLING ACCOUNT provides a mechanism for grouping different types of items on different invoices. A client might want one account for his or her office supplies and another account for furniture purchases. A billing account allows customers to receive separate invoices to track different types of items separately. Banks and credit card companies use this concept frequently to allow separation of various charges for their customers. A telecommunications company may set up separate billing accounts for different telecommunications lines. Perhaps one account is for standard telephone service, while another account is set up for the enterprise's dedicated lines.

Figure 7.3a adds to the previous model shown in Figure 7.2 by providing for invoices that may be sent to a BILLING ACCOUNT as an alternative to sending it directly to a PARTY. Some enterprises may have a need to track more than one party that is responsible for paying an invoice that is sent to a BILLING ACCOUNT. Therefore, the model in Figure 7.3a has an intersection entity called BILLING ACCOUNT ROLE between PARTY and BILLING ACCOUNT, allowing for maintenance of the various parties involved on the account. The BILLING ACCOUNT ROLE allows each PARTY to play a BILLING ACCOUNT ROLE TYPE in the account. Roles could include “primary payer,” indicating the main party that is supposed to pay, or “secondary payer,” indicating other parties that could pay in case of default. There may be other roles as well, such as “customer service representative,” “manager,” and “sales representative,” that could be involved with the account as well. Other attributes needed on the BILLING ACCOUNT ROLE include the from date, which is when the party became active on the account, and the thru date, which indicates through when the role is involved.

Each invoice may then be billed to either a BILLING ACCOUNT or directly to a PARTY with this model. The BILLING ACCOUNT has a from date (when it became active), a thru date, and a description identifying the nature of the billing account. In order to determine where to send the invoice, the account in question must, in turn, be related to a CONTACT MECHANISM. Eventually, all invoices must end up at a location of some sort. Also, note that if the enterprise uses billing accounts, the order models in Chapter 4 (Figures 4.3 and 4.5) should include a with a requested bill to relationship to the BILLING ACCOUNT entity, with a mutually exclusive arc similar to the arc in the invoicing model.

Table 7.5 provides the example of ACME Corporation setting up an account for its office supplies and a separate account for using consulting services.

Table 7.5Billing Account Data

Table 7.6 shows sample data for an account with more than one party assigned to it. The sample data shows a typical situation that could occur for a credit card account, a bank account, a telecommunications account, or a utilities account, possibly with many individuals on it. Initially the account was opened with both Jane and Joe Smith assigned to the account on April 15, 2000. Jane had primary responsibility for paying for the account and if, for some reason, she did not pay, then John would be held accountable in his role as the secondary payer. Then, on June 16, 2001, Joe Smith was added to the account, replacing John Smith as the secondary payer on the account. Because the thru date is blank, it can be inferred that both Jane and Joe are still active on the account.

Table 7.6 Billing Account with More Than One Party

Cards can be issued against an account-for example, a banking card or credit card. If this is needed, then a CARD or MEDIA entity, maintaining banking card or credit card information, could be added and related to BILLING ACCOUNT as well as PARTY. Based on the business rules of the enterprise the relationship from the CARD entity could be a one-to-many or a many-to-many relationship to either the BILLING ACCOUNT or the PARTY.

Another common example of the usage of billing accounts is in the telecommunication industry. In some cases, all phone services for several phone numbers might appear on one billing account, while all charges for other phone numbers for the same location might appear on a different account. This could allow the charges for standard telephone service to be included on one account while other services, such as dedicated line and network services, might appear on another account. Again, telephone cards may be issued that give the customer the right numbers to charge calls to the account.

An alternative to the data models in Figure 7.2 or Figure 7.3a is to relate the invoices to the specific entities that represent roles for invoicing. Figure 7.3b provides additional relationships to represent the key roles of BILL TO CUSTOMER, INTERNAL ORGANIZATION, and SUPPLIER, which are subtypes of PARTY ROLE and are still tied to PARTY.

Figure 7.3b Invoice specific party roles.

This model defines more specific rules for the way that SALES INVOICES and PURCHASE INVOICES operate. A SALES INVOICE must be billed to a BILLING ACCOUNT or directly to a BILL TO CUSTOMER. If billing accounts are not used at the enterprise, then just remove the BILLING ACCOUNT entity relationships to this entity. The SALES INVOICE must be billed from an INTERNAL ORGANIZATION. A PURCHASE INVOICE must be billed to a BILLING ACCOUNT or an INTERNAL ORGANIZATION. The PURCHASE INVOICE must be billed from one and only one SUPPLIER.

Each of these roles, BILL TO CUSTOMER, INTERNAL ORGANIZATION, and SUPPLIER, are subtypes of PARTY ROLEs, which are each related to a PARTY. This allows the same PARTY to act in multiple PARTY ROLEs, each of which may be related to different invoices in different ways. Thus, this data structure still maintains the idea that a PARTY may have the same information that can still be stored once, independently of the information associated with the various roles that the party may play.

The advantage of this alternative data model over the more generic models in Figure 7.2 or Figure 7.3a is that it conveys more specific business rules showing the specific roles that parties are required to play in the sales and purchase invoicing. For instance, it shows that the INTERNAL ORGANIZATION is the party role that receives the PURCHASE INVOICE and the party role that is the sender of each SALES INVOICE.

The disadvantage of this alternative model is that it is less flexible than Figure 7.2 and Figure 7.3a because it conveys specific business rules that may or may not hold up over time. For instance, what if an AGENT of the enterprise is a party that may be the sender of the INVOICE? What if other roles change the nature of the way that INVOICEs are processed?

As a general guideline, one should use the more specific models such as the one in Figure 7.3b when the relationships between the entities are very stable and will probably not change over time. If one knows that there will always be one and only one SUPPLIER that is always going to be the sender of PURCHASE INVOICEs, then it is safe to model this relationship as such.

Like orders, shipments, and many other transactions, invoices also have status and terms. Figure 7.4 shows that the INVOICE entity can have multiple INVOICE STATUSes and that either the INVOICE or INVOICE ITEM entity can have multiple INVOICE TERMs.

Figure 7.4 Invoice status and terms.

Similar to orders, the state of an invoice changes over time. To track this, the entity INVOICE STATUS is used. It is an intersection entity between INVOICE and INVOICE STATUS TYPE (which is another subtype of STATUS TYPE). Examples of statuses include: “sent,” “void,” and “approved.” “Paid” is not a valid status because it can be determined via payment transactions, which will be discussed later in this chapter. Additionally, the need to know when this status took effect is provided by the attribute status date. Table 7.7 shows how this data might look.

Table 7.7 Invoice Status Data

| INVOICE ID | STATUS TYPE | STATUS DATE |

| 30002 | Approved | May 25, 2001 |

| Sent | May 30, 2001 | |

| 30005 | Sent | June 5, 2001 |

| Void | June 6, 2001 |

To find the current status, look for the most recent date. Note that if the number of statuses is somewhat limited, these items would be good candidates for denormalization in a physical model. If the model was denormalized, there may be approved date, sent date, and void date as attributes within the INVOICE entity instead of as records within the INVOICE STATUS entity.

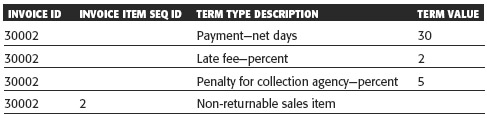

Some systems or enterprises might need to record various terms and conditions on invoices, such as payment terms. Terms may sometimes apply at the item level. The model handles this with the INVOICE TERM entity, which must be related to either the INVOICE or INVOICE ITEM entities.

Table 7.8 shows three terms that were applied to an invoice and one term that is applied to only one of the items on that invoice. The first three rows describe terms for payment, late fees, and penalties that apply to the INVOICE. This data indicates that for invoice #30002, the payment is due in 30 days. If it is late, there is a 2 percent late fee added. If the invoice is sent to a collection agency, then there is an additional 5 percent added to the amount due. The last row provides an example of a term that is applied to the INVOICE ITEM, namely that the second item on invoice 30002 is nonrefundable.

Table 7.8 Invoice Term Data

Invoice and Associated Transactions

Invoices generally stem from associated transactions, which may include shipments, work efforts, and time entries, or directly from orders. An invoice represents a request for payment, and each invoice item identifies each part of the request as it relates to the items that are chargeable. Each invoice item may include moneys that are owed from shipment items, work efforts, time entries, or order items,. In each of these cases the invoice item may group together the items from which the charge came. There could be many shipment items, work efforts, time entries, or order items for an invoice item.

Also, there may be multiple invoice items for each order item, shipment item, or work effort due to two factors. The first factor is that the invoice item may only partially bill for the amount due and bill the rest at a later point in time. The second factor is that additional invoice items may be added in order to correct the initial shipment item, work effort, time entry, or order item.

The following three data models and corresponding sections describe how shipment items are related to shipment items, work efforts, and order items, respectively.

A very common relationship is from the invoice item to the shipment item because these shipments often represent the delivery of goods that need to be paid after they have been received. How does one ensure that everything shipped actually gets billed?

The SHIPMENT ITEM BILLING entity allows enterprises to track this information (see Figure 7.5). This entity provides a means to store intersection information between INVOICE ITEM and SHIPMENT ITEM. Each of the invoice items should represent the bill for one or more shipment items. Conversely, one shipment item could be related to many invoice items in the case where adjustments to the original invoice item were needed. For example, if some of the goods for the original shipment were damaged, a credit for these items would be needed. The credit would take the form of an invoice item on a second invoice. Thus, the one shipment item would actually have a relationship to two different invoice items. It is unlikely that one shipment item would be related to two invoice items on the same invoice (though this would need to be enforced with a business rule).

Figure 7.5 Billing for shipment items.

Table 7.9 gives some examples of the data held by this entity. The table shows an example of a single shipment that resulted in two invoice items. Observe that the same shipment item (shipment ID #1235, item #1) is related to two invoice items. The first invoice item was a bill for the shipment of 1,000 items. On receipt, the customer found 10 items damaged; therefore, on a subsequent invoice another invoice item was to credit the customer for the 10 damaged items. This adjustment was then linked to the original shipment item to allow for proper tracking. Therefore, there were two invoice items for the same shipment item.

Table 7.9 Shipment Invoice Data

The example of shipment ID #1330 shows the opposite situation. In this case, three shipment items are mapped to only one invoice item. This can occur when the shipment items show component parts for an item, but the invoice shows only the price for the entire assembly. This situation could also occur when three shipments on different dates are grouped together into one invoice (perhaps due to a prearranged billing agreement).

Notice that there is not a quantity attribute on the SHIPMENT INVOICE and that the quantity shown in Table 7.9 comes from the INVOICE ITEM. The reason for this is that an enterprise will usually not partially invoice for items that have been shipped. If this case can exist and it is necessary to map quantities of invoice items to shipment items, then the quantity attribute could be added.

Keep in mind that there will not always be a SHIPMENT INVOICE record for every shipment. Some shipments, such as transfers, will not show up on an invoice unless the enterprise wants to keep track of internal transactions.

Billing for Work Efforts and Time Entries

The previous section identified how the delivery of goods is usually invoiced. How are services invoiced then? Services are generally invoiced one of two ways: The organization performing the services bills their client for either their time or for progress on specific work efforts.

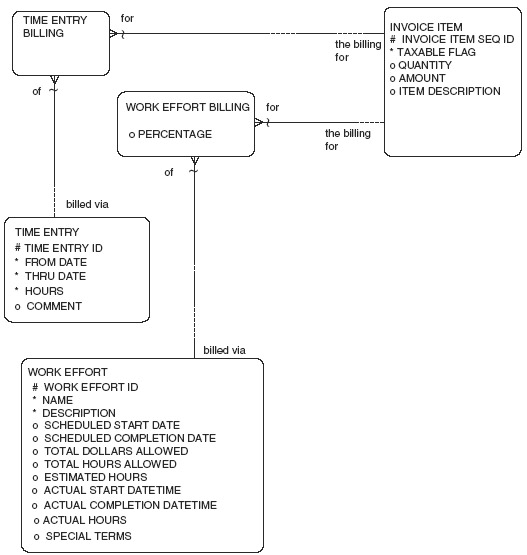

Figure 7.6 provides a data model for billing of work efforts and/or time entries. For many of the same reasons that SHIPMENT ITEMS have a many-to-many relationship to INVOICE ITEMs, both WORK EFFORT and/or TIME ENTRY are also related in a many-to-many fashion to INVOICE ITEM. Each WORK EFFORT may be billed by many INVOICE ITEMs and vice versa. The associative entity WORK EFFORT BILLING accommodates this many-to-many relationship. Similarly, the associative entity TIME ENTRY BILLING resolves the many-to-many relationship from TIME ENTRY to INVOICE ITEM.

Figure 7.6 Billing of time entries and work efforts.

A WORK EFFORT may have many INVOICE ITEMs because it is common for companies to charge progress payments on the work effort. For instance, a professional services firm such as a consulting organization may charge a client 30 percent of a project (i.e., a type of work effort) on starting, 30 percent on initial delivery, and 40 percent 30 days after the project's completion. This would represent three INVOICE ITEMs for the same work effort. The percentage attribute allows recording of how much of the work effort was invoiced in that invoice item. Many WORK EFFORTS could be combined and invoiced in a single INVOICE ITEM. For example, a law firm may agree to perform three different efforts for a set fee, which is invoiced as a single INVOICE ITEM.

Each TIME ENTRY may have many INVOICE ITEMs associated with it. Suppose a TIME ENTRY was for five hours of consulting services. The client called and complained that he or she did not get what was expected in the five hours, and the consulting firm responded by agreeing to issue a credit of two hours regarding that time entry. Therefore, this led to two INVOICE ITEMs for the same TIME ENTRY. Usually partial invoicing of a time entry is not done; however, if this is possible then an hours attribute could be added to the TIME ENTRY BILLING record to show how much of each time entry was billed.

Instead of assuming that each TIME ENTRY can be billed via more than one INVOICE ITEM to handle adjusting invoice item entries, can corrections to invoices be handled with a relationship from one INVOICE ITEM to the previous INVOICE ITEM? One of the problems with handling it via a recursive relationship on INVOICE ITEM is that the INVOICE ITEM may represent multiple time entries on different dates. In this case, it may be important to record to which of the three time entries the adjusting INVOICE ITEM applied. For this reason, this data model assumes that each should be related directly to the source transaction(s) that generated the invoice item.

Many TIME ENTRYs could also be combined on the same INVOICE ITEM, particularly if the time entries had similar information except for the date. An accountant may work two hours on Monday, three hours on Wednesday, and four hours on Friday, and the invoice may show an INVOICE ITEM for nine hours with an attached time sheet that could show the related time entries.

What if the enterprise bills based on the order? Perhaps payment is due after ordering the goods and/or services. Or perhaps the enterprise does not track the shipment or work effort associated with the order and tracks only the order and its following invoice. For example, enterprises will not always track the work efforts associated with purchase orders for services rendered.

Figure 7.7 provides an additional data structure to show that ORDER ITEMs may also have a many-to-many relationship with INVOICE ITEMs. The associative entity ORDER ITEM BILLING lets order items be grouped together on an INVOICE ITEM or, conversely, more than one INVOICE ITEM for an ORDER ITEM. The amount and quantity attributes on the ORDER ITEM BILLING entity are provided to record the distribution of the amount or quantity from an order item to multiple invoices or vice versa.

Figure 7.7 Billing for order items.

Take, as an example, a purchase order item for a year's worth of accounting services at a cost of $120,000. The accounting firm invoices monthly. An invoice arrives with an invoice item for $10,000. This is then linked to the appropriate order item on the purchase order (using ORDER ITEM BILLING), and the amount of $10,000 is entered to show that $10,000 of the original $120,000 has been billed. This allows the enterprise to easily track over time how much of the original commitment has actually been billed to date (and also to notice if it has been billed beyond the amount of the purchase order). This example illustrated that a single ORDER ITEM may be related to many INVOICE ITEMs.

To show that a single INVOICE ITEM may be for multiple ORDER ITEMs, consider an enterprise in need of hardware support for its internal computer systems. Over the course of time, it executes three separate purchase orders to the same external company to provide this support. Each order has an order item for 40 hours of on-site support, for a total of 120 hours. Again, over time, the services are delivered, but due to the billing cycles at the vendor company, the first invoice has one order item for 100 hours. The final 20 hours are billed on the next invoice. Table 7.10 shows the details for these transactions.

Table 7.10 Billing for Order Items

Using this construct, it is possible to handle almost any combination of order and invoicing. Why go to such lengths to provide this flexibility in the data model? An enterprise has no real way of controlling service vendors and how they invoice; with this model that does not matter. How the vendor chooses to do business regarding customer purchase orders will make no difference to the enterprise because this model is flexible enough to handle a variety of situations. Additionally, this model provides flexibility in recording the billing of both sales and purchase order items.

Invoices are issued to request payment. The tracking of payments issued and received is a very important universal data concept for most businesses because it represents the flow of money from and to the enterprise.

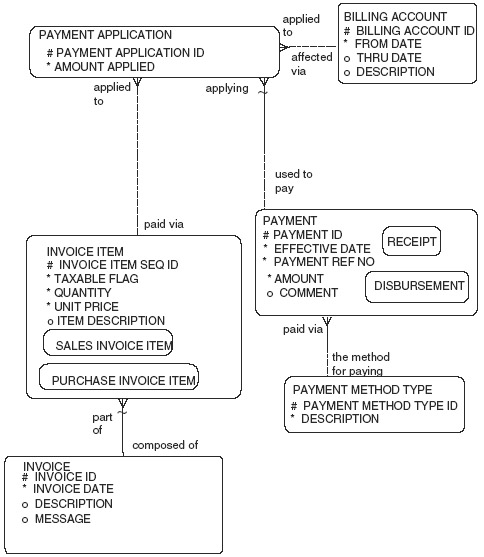

Figure 7.8a provides a data model to track payments against invoices and billing accounts. Each PAYMENT may be applied toward many INVOICEs through the PAYMENT APPLICATION. Conversely, multiple payments may pay for a single INVOICE when partial payments are made.

Figure 7.8a Invoice payments.

Alternatively, the payment may be applied “on account,” which means it is applied to a BILLING ACCOUNT without being applied to specific invoices. This allows for situations where a payment comes in and it is not clear for which invoice(s) it is paying. Also it allows moneys to be accepted in advance of charges. In either of these cases, the payments can be properly allocated later to the appropriate invoice items, once this is known.

The PAYMENT APPLICATION provides for the many-to-many relationships that can exist between the PAYMENT and INVOICE ITEM as well as between the PAYMENT and BILLING ACCOUNT.

The PAYMENT entity represents instances of moneys transferred from a PARTY and to a PARTY. A RECEIPT subtype represents incoming moneys to an internal organization of the enterprise, and a DISBURSEMENT represents outgoing payments of moneys sent by an internal organization of the enterprise. A payment made from one internal organization to another internal organization results in two PAYMENT instances; one internal organization will record a RECEIPT, and the other internal organization will record a DISBURSEMENT.

The PAYMENT entity is related to the PAYMENT METHOD TYPE entity whose description identifies the kind of payment such as “electronic” (for electronic transfers of moneys), “cash,” “certified check,” “personal check,” or “credit card.” The payment ref num references a payment identifier such as a check number or electronic transfer identifier. The effective date documents when the payment can be realized. For instance, an electronic transfer may be for a future time, or a check may be postdated and take effect at a later time. The comment provides an attribute to fully describe any circumstances involved in the transaction such as “payment was made with a message that complimented the service provided.”

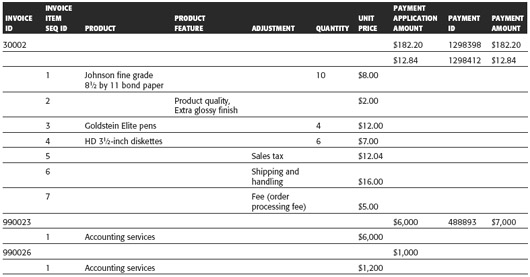

Table 7.11 shows example data for payments. The amount owed on invoice ID #30002 is $184.04, which can be calculated by extending each of the invoice items (multiplying the quantity times the unit price) and adding them together. The enterprise received a partial payment check for $182.20 against invoice #30002 because the paying organization had an outstanding issue with the Goldstein Elite pens and did not pay at first. After resolving the issue, they paid the other $12.84 (12.00 plus .84 for the sales tax for the pens) against the same invoice #30002, thus fully paying off the invoice. This example illustrates that when partial payments are issued against an invoice there can be more than one payment for an invoice.

Table 7.11 Invoice Payments

The other two invoices, purchase invoices #990023 and #990026, have one payment that is for both of them. $6,000 of the $7,000 payment was applied to invoice #990023, and the enterprise decided to pay only $1,000 of the $1,200 due, leaving $200 additional due on the second invoice.

In some enterprises, invoices are very complex and are tracked at an invoice item level. For instance, a large consulting firm that outsources the information systems function of an organization may have a single bill for all the engaged consultants. The paying firm may pay against only the invoice items with which it is comfortable, and the receiving firm may want to track which invoice items have been paid.

The previous example in Table 7.11 for Invoice #30002 shows why the enterprise may also desire to track the payments against the invoice items to see which invoice items are outstanding. The company fully paid off three of the invoice items, and they may want to track which invoice items are outstanding as opposed to just recording that the invoice was partially paid off. The decision to track payments against invoice items would depend on the organization and how often individual invoice items are paid versus how often the full invoice is paid. The trade-off is that tracking by invoice item is more specific; however, it requires more work and more database records because there would be at least one PAYMENT APPLICATION record for every INVOICE ITEM.

Figure 7.8b provides an alternate data model to handle tracking payments at an invoice item level. In this model the PAYMENT APPLICATION relates to an INVOICE ITEM, thus tracking payment of each part of the invoice. This structure allows the enterprise to know for which invoice items they have received moneys and for which invoice items they have disbursed moneys. Of course, with this model, it assumes that the enterprise has the necessary information as well as the desire to record which items corresponded to which payments.

Figure 7.8b Invoice item payments.

A common example of payments is to invoice item charges occurring in the banking industry. When loans are due, invoices may be issued. Then when a partial payment for a loan amount is received, business rules determine which invoice items should be paid off first. Therefore, tracking which invoice items are paid is important. For instance, the moneys could be first applied to fees, then applied to interest due, and then applied to the principal.

A third possible data model is to account for the PAYMENT APPLICATIONs being related to either INVOICEs or INVOICE ITEMs. This would allow the enterprise to record full payments of invoices easily and, when necessary, record payments against individual INVOICE ITEMS. This option has a large drawback because the option to apply payments against either invoices or invoice items may lead to more confusion (with procedures and invoice tracking) than it is worth.

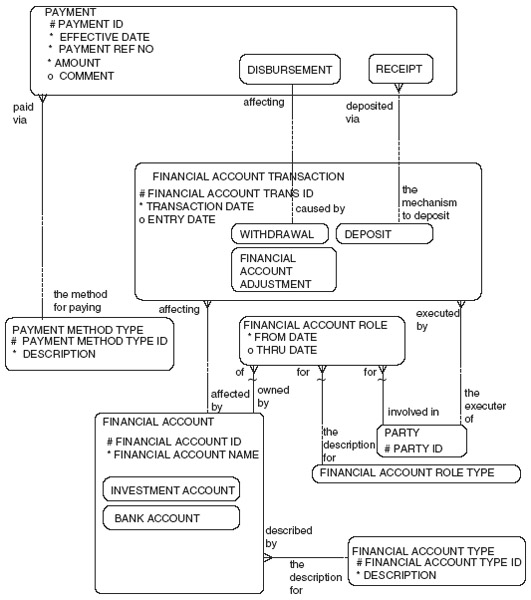

Financial Accounts, Deposits, and Withdrawals

Once payments are received, it is important to deposit these receipts into a bank account, investment account, or some form of financial account where funds are kept. This section describes the handling of receipts and withdrawals that are recorded as transactions against financial accounts.

Figure 7.9 provides a data model to handle financial accounts, deposits, and withdrawals. A FINANCIAL ACCOUNT is a vehicle for maintaining funds, and subtypes include a BANK ACCOUNT and an INVESTMENT ACCOUNT. There could be other types of FINANCIAL ACCOUNTs, such as a “checking account,” “savings account,” “IRA account,” “mutual fund account,” and so on, which could be described in the FINANCIAL ACCOUNT TYPE entity. Each PAYMENT may be either a RECEIPT or DISBURSEMENT, which is linked to different types of FINANCIAL ACCOUNT TRANSACTIONS, namely DEPOSIT and WITHDRAWAL. One or more RECEIPTs could be included in a DEPOSIT, which is a type of FINANCIAL ACCOUNT TRANSACTION that affects a FINANCIAL ACCOUNT. Each DISBURSEMENT may be related to a WITHDRAWAL, which is a type of FINANCIAL ACCOUNT TRANSACTION that affects a FINANCIAL ACCOUNT.

Figure 7.9 Financial accounts, withdrawals, and deposits.

For example, an enterprise may receive three incoming checks (i.e., RECEIPTs) and have a DEPOSIT transaction that records that these three checks have been deposited into a bank account (FINANCIAL ACCOUNT). This enterprise may issue a check (i.e., DISBURSEMENT) that ultimately results in a WITHDRAWAL of funds, which is a FINANCIAL ACCOUNT TRANSACTION, which also affects a FINANCIAL ACCOUNT, for example, a BANK ACCOUNT.

Table 7.12 provides an example of a typical case of a DEPOSIT, which consists of four RECEIPTs. There are also two withdrawals, which consist of two checks. The first two receipts are the receipts from the previous example in Table 7.11, and two additional receipts that have not previously been shown are included to illustrate the idea of recording each deposit and its corresponding receipts.

Table 7.12 Deposits and Withdrawals.

This chapter has provided models for invoice and invoice items for products, product features, adjustments, shipments, work efforts, and orders. Other models described in this chapter have been invoice roles, invoice billing accounts, invoice status and terms, invoice payments, and financial account deposits and withdrawals. The main entities and relationships are shown in Figure 7.10. It is the interrelationships with other parts of the model and the intersection entities that will allow for the development of a robust, integrated solution. These models should, once implemented, minimize the occurrence of redundant data and simplify the maintenance of the database.

Figure 7.10 Overall invoice model.

Please refer to Appendix A for a listing of entities and attributes. SQL scripts to build tables and columns derived from the logical models in this book can be found on the full-blown CD-ROM, which is licensed separately.