CHAPTER

8

Accounting and Budgeting

Many accounting functions are very similar across enterprises. Enterprises need to record transactions, post these transactions to each internal organization's chart of accounts, set up budgets, track variances to their budgets, and report on the results of their business operations.

An accounting and budgeting data model needs to maintain financial information to answer many important questions that affect an enterprise's existence:

- What is the financial position of the enterprise, and how did this change from previous periods?

- What types of transactions occurred in each period, and how much of each transaction occurred? For instance, what payments were made to which invoices, and what invoices are still outstanding?

- What expenses were incurred during various periods?

- What effect did transactions such as depreciation, capitalization, and amortization have on the enterprise?

- What budgets were set up, and how did the enterprise perform compared to these budgets?

This chapter illustrates data models with the following types of information:

- Chart of accounts

- Business transactions versus accounting transactions

- Accounting transactions

- Accounting transaction detail

- General ledger account associations and subsidiary ledger accounts

- Asset depreciation

- Budget definition

- Budget revision

- Budget review

- Budget scenario

- Use and sources of budgeted money

- Budget versus general ledger

Chart of Accounts for Internal Organizations

Generally, the first step in setting up an accounting system is determining a chart of accounts for each organization. A chart of accounts is simply a list of the buckets or categories of transactions that the enterprise will use to track its business activity for accounting purposes.

Figure 8.1 shows a data model that can establish and maintain a chart of accounts for each organization within the enterprise. The GENERAL LEDGER ACCOUNT represents a type of financial reporting bucket to which transactions are posted, for example a “cash” account or a “supplies expense” account. Each GENERAL LEDGER ACCOUNT may be categorized by one and only one GENERAL LEDGER ACCOUNT TYPE to specify the type of account (for instance, “asset” or “liability”). Each INTERNAL ORGANIZATION may be using many GENERAL LEDGER ACCOUNTs, and each GENERAL LEDGER ACCOUNT may be associated with more than one INTERNAL ORGANIZATION. The ORGANIZATION GL ACCOUNT resolves this many-to-many relationship. Each internal organization needs to establish the ACCOUNTING PERIOD for which it reports its business activities. Each ACCOUNTING PERIOD is of PERIOD TYPE such as “fiscal year,” “calendar year,” “fiscal quarter,” and so on.

Figure 8.1 Chart of accounts for internal organizations.

General Ledger Accounts and Types

General ledger accounts are mechanisms to categorize similar types of transactions together for the purpose of financial reporting. The field name shown in the GENERAL LEDGER entity identifies the name of the account that will be used for reporting purposes in financial statements. Examples of general ledger account names include “cash,” “accounts receivable,” “notes payable,” or “advertising expense.” The description attribute provides a definition behind the account to ensure that it is understood properly.

The key to a GENERAL LEDGER ACCOUNT entity in this model is the general ledger account ID and is filled with a non-meaningful unique number. Many other accounting systems assign a meaningful mnemonic to the general ledger account ID so that accounts are easily identified. The key may start with an organization component, then have a suborganization portion, then have the type of account, and then have a number representing the account. An example of this ID structure is ABC100-200-A-101, where “ABC100” represents the organization, “200” represents a specific division, “A” stands for asset, and “101” represents the account “cash.” The problem with having a meaningful key is that if things change within the enterprise, such as a reorganization of the enterprise, then it creates a major problem for the system because key values and foreign key values need to be changed and there is a high chance of data inconsistencies. This is not what is desired, especially in an accounting system that needs to be precise.

The GENERAL LEDGER ACCOUNT TYPE entity identifies the classification of the GENERAL LEDGER ACCOUNT. Valid classifications include “asset,” “liability,” “owners equity,” “revenue,” and “expense.” This information provides a mechanism to group information on financial statements. The “asset,” “liability,” and “owners equity” categories, along with the associated general ledger accounts, are generally used for the organization's balance sheet. The “revenue” and “expense” categories are generally used for the income statement.

Table 8.1 shows examples of general ledger accounts along with the type associated with each account.

Table 8.1 General Ledger Accounts

Now that general ledger accounts have been established, they need to be related to the internal organizations that use them for reporting. Each INTERNAL ORGANIZATION may have many GENERAL LEDGER ACCOUNTs associated with it. Conversely, each GENERAL LEDGER ACCOUNT may be reused to satisfy the needs of many INTERNAL ORGANIZATIONs. The ORGANIZATION GL ACCOUNT shows which internal organizations use which general ledger accounts. The from date and thru date attributes on the ORGANIZATION GL ACCOUNT entity indicate when general ledger accounts were added to an internal organization's chart of accounts and for what period of time they were valid.

The ORGANIZATION GL ACCOUNT represents the instance of a general ledger for a particular internal organization and is therefore a very significant entity. For instance, accounting transactions will be related to this entity, thus allowing maintenance of all the transactions for a particular balance sheet or income statement account.

The ACCOUNTING PERIOD entity indicates the periods of time that the organization uses for its financial reporting. This may be to define a fiscal year, fiscal quarter, fiscal month, calendar year, calendar month, or any other time period that is available in the PERIOD TYPE. The acctg period num(ber) identifies the relative number of the accounting period. For instance, if there are 13 accounting periods in a year, the acctg period num would vary from “1” to “13” for this type of period. Quarters may vary from “1” to “4.” The from date and thru date attributes define the time period for each instance.

An alternative structure is to use a from day and thru day to identify the starting day and ending day of a period, instead of the attributes from date and thru date. These would be character strings and not date domains because they specify only part of a date such as the month and day for the start and end of a period. The benefit of this design is to be able to define a period once. For example, the fiscal from day may be “Mar 1” and the fiscal thru day may be “Feb 28” to identify a PERIOD TYPE of “fiscal year,” instead of having to reen-ter the accounting period for each year. One downside of this data structure is that it creates complications in handling leap years for periods ending at the end of Feb. Another downside of this data structure is that it is less practical to implement because date conversions will be needed to figure out which transactions should be posted to which periods, versus explicitly storing the dates, as shown in Figure 8.1.

Each ACCOUNTING PERIOD may be within one and only one ACCOUNTING PERIOD, as shown in the recursive relationship. This allows monthly periods to be rolled up to quarters, which can be rolled up to years.

Table 8.2 illustrates examples of the chart of accounts for ABC Corporation and ABC Subsidiary. Notice that while many general ledger accounts are used within both organizations, some accounts are different. For example, ABC Corporation has a “trade show expense” account whereas the subsidiary doesn't have this account because it is not involved in trade shows.

Table 8.2 Organization GL Account

Also, notice that each organization has its fiscal year accounting periods associated with it (ACCOUNTING PERIOD from date and thru date). The two organizations shown have the same fiscal year period; however, it is possible for internal organizations within the same enterprise to have different accounting periods. For example, an organization with a fiscal period from June 1 to May 31 may have been recently merged into an internal organization whose fiscal period is January 1 to December 31.

The ORGANIZATION GL ACCOUNT from date and thru date provide the ability to track which GL accounts existed for which INTERNAL ORGANIZATIONs at what periods of time. For example, Table 8.2 shows that on January 1, 1997, ABC Corporation divided its “marketing expense” account into two accounts: “advertising expense” and “trade show expense.”

Accounting Transactions Definition

In various parts of this book, there are transactions that affect the accounting of the organization. For example, in Chapter 7, the creation of an INVOICE will result in a related accounting transaction, namely a SALES ACCTG TRANS. In Chapter 3, the identification of an ITEM VARIANCE to adjust INVENTORY ITEMs will lead to an ITEM VARIANCE ACCTG TRANS. Thus, there is a need in enterprises to maintain information about the accounting transactions.

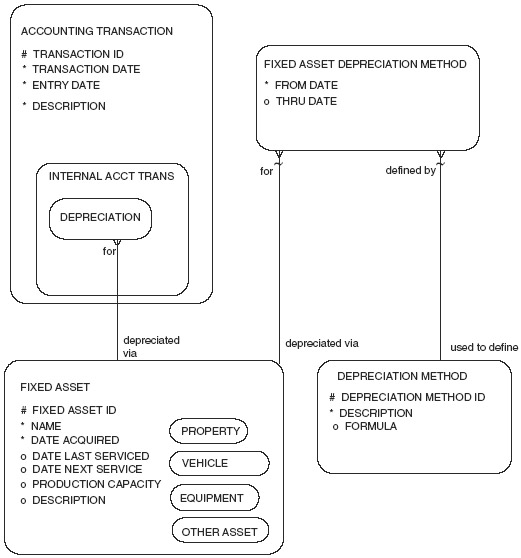

Figure 8.2 provides the initial part of the accounting transaction data model. The ACCOUNTING TRANSACTION entity is a supertype that encompasses all the transactions that affect the financial statements of the enterprise. It includes INTERNAL ACCTG TRANS such as DEPRECIATION, CAPITALIZATION, AMORTIZATION, ITEM VARIANCE ACCTG TRANS, and OTHER INTERNAL ACCTG TRANS that document adjustments to the internal organization's financial position. Accounting transactions may also be EXTERNAL ACCTG TRANS that involve either OBLIGATION ACCTG TRANS or PAYMENT ACCTG TRANS made. Each PAYMENT ACCTG TRANS represents either a RECEIPT ACCTG TRANS for moneys coming in or a DISBURSEMENT ACCTG TRANS for moneys going out.

Figure 8.2 Accounting transactions.

Each ACCOUNTING TRANSACTION may be related to its business transaction from which it originated. Thus the SALES ACCTG TRANS must be originated from each INVOICE instance, each PAYMENT ACCTG TRANS is originated from a PAYMENT instance, and each ITEM VARIANCE ACCTG TRANS must be originated from a INVENTORY ITEM VARIANCE instance that shows adjustments to inventory.

The relationship from ACCOUNTING TRANSACTION to ACCOUNTING TRANSACTION TYPE provides a specific low-level categorization of each transaction. Types may include further breakdowns of the subtypes such as “Payment Receipt for Asset Sale” or “Payment Disbursement for Purchase Order.”

Business Transactions versus Accounting Transactions?

Each ACCOUNTING TRANSACTION may be originated from a corresponding business transaction, which is any transaction through the enterprise's data model that will affect the financial status of the organization. The model shows a few of these corresponding business transaction relationships, and there may be many others depending on the nature of the organization. The model shows that INVENTORY ITEM VARIANCE instance may be posted via a corresponding ITEM VARIANCE ACCTG TRANS transaction. Similarly, each INVOICE may be posted via a SALES ACCTG TRANS, and each PAYMENT corresponds to a PAYMENT ACCTG TRANS.

Are each of these business transactions such as an INVOICE actually a separate entity tied to an accounting transaction, or are they really a subtype of an ACCOUNTING TRANSACTION? One may think that these business transactions and accounting transactions are the same thing because they have a one-to-one relationship and they represent the same thing: a transaction that affects the books of the enterprise. On the other hand, there may be a timing difference between the business transaction and the accounting transaction. For instance, an INVOICE may be maintained by the enterprise even though, at a particular point in time, there may not be a related accounting transaction because it has not yet been posted. Furthermore, the INVOICE may have a status of “pending approval from manager,” thus maintaining it as an INVOICE but not as an ACCOUNTING TRANSACTION. Therefore, the data model shows that each of the business transactions is a separate entity from the corresponding accounting transactions.

Each ACCOUNTING TRANSACTION instance represents a journal entry in accounting terms. The ACCOUNTING TRANSACTION entity has a transaction ID that uniquely identifies the particular transaction. The transaction date is the date on which the transaction occurred. The entry date is the date on which the entry was made into the system. The description attribute describes the details behind the transaction. Note that there is no amount attribute because the transaction amounts are maintained in the transaction detail, which will be covered in the next section.

Accounting deals with two main types of transactions. An ACCOUNTING TRANSACTION may be either an INTERNAL ACCTG TRANS or an EXTERNAL ACCTG TRANS. INTERNAL ACCTG TRANS are adjustment transactions that affect only the books of the internal organization being affected. EXTERNAL ACCT TRANS are transactions that involve transactions with a party that is external to the enterprise for whom the books are kept.

The subtypes reveal examples of INTERNAL ACCTG TRANS such as DEPRECIATION, CAPITALIZATION, AMORTIZATION, ITEM VARIANCE ACCTG TRANS, and OTHER INTERNAL ACCTG TRANS that adjust the financial position of the internal organization.

The OBLIGATION ACCTG TRANS subtype is broken down into various other subtypes that represent different forms of a party owing moneys to another party. One subtype of OBLIGATION is a NOTE. It may be a note payable, where the internal organization owes money, or a note receivable, where the organization is due money. Another subtype is CREDIT MEMO, which is a transaction where credit is given from one party to another party. TAX DUE is an obligation to pay taxes to government agencies. The SALES ACCTG TRANS entity represents the obligation to pay for products sold. CREDIT LINE represents money actually borrowed from a line of credit extended from a financial institute to another party. There may be other forms of obligations depending on the business; therefore, the OTHER OBLIGATION subtype is included.

The PAYMENT ACCTG TRANS subentity represents collections of moneys received by an internal organization (RECEIPT ACCTG TRANS) or payments of moneys sent by an internal organization (DISBURSEMENT ACCTG TRANS). A payment made from one internal organization to another internal organization results in two PAYMENT ACCTG TRANS instances; one internal organization will record a RECEIPT, and the other internal organization will record a DISBURSEMENT.

Accounting Transactions and Their Related Parties

The INTERNAL ACCTG TRANS identifies transactions that serve as adjustments to the books of an internal organization. Because there is only one organization involved in the transaction (namely, the internal organization whose books are being adjusted), there is a single relationship to an INTERNAL ORGANIZATION.

The EXTERNAL ACCTG TRANS subtype models accounting transactions that affect two parties. An EXTERNAL ACCTG TRANS may be either an OBLIGATION ACCTG TRANS or a PAYMENT ACCTG TRANS. An OBLIGATION ACCTG TRANS represents a transaction where one party has recognized that it owes moneys to another party. Therefore, the from and to relationships identify the parties involved on both sides of a transaction. A PAYMENT ACCTG TRANS represents a transaction where one party is paying another party; therefore it also relates to two parties.

Table 8.3 provides examples of various types of accounting transactions. The first row (transaction ID 32389) is an example of an internal transaction that records a depreciation expense for a piece of equipment. Only one party is affected—the internal organization that owns that piece of equipment, ABC Corporation. The rest of the transactions are various types of external transactions that involve a “to” party and a “from” party. For instance, transaction 39776 describes a receipt (incoming payment) to pay off $700 owed by ACME Company to ABC Corporation.

Table 8.3 Accounting Transaction

Accounting Transaction Details

Figure 8.3a adds to the previous accounting transaction model by adding the transaction detail debit and credit entries to the accounting transaction as well as relating the transaction detail to the organizations' general ledger accounts. Each ACCOUNTING TRANSACTION is broken down into numerous TRANSACTION DETAILs that represent the debits and credit entries for the transaction. Each debit or credit entry will affect one of the internal organization's accounts and therefore is related to an ORGANIZATION GL ACCOUNT, which is the bucket for a GENERAL LEDGER ACCOUNT for an INTERNAL ORGANIZATION.

Figure 8.3a Accounting transaction details.

As shown in Figure 8.3a, each ACCOUNTING TRANSACTION must be composed of one or more TRANSACTION DETAILs, which show how each part of the transaction affects a specific ORGANIZATION GL ACCOUNT. A TRANSACTION DETAIL instance corresponds to a “journal entry line item” in accounting terms.

According to the principles of double-entry accounting, each transaction has at least two detail records, a debit and a credit. For instance, an ACCOUNTING TRANSACTION of type INVOICE may result in two TRANSACTION DETAIL instances: a debit to the general ledger account “accounts receivable” (showing that moneys are due) and a credit to the general ledger account “revenue” (showing that revenue is recognized). Table 8.4 illustrates the details of this transaction (transaction ID 38948 in the table).

Table 8.4 Transaction Detail

Each transaction is related to the general ledger account within a specific internal organization, which is why the organization GL account column of Table 8.4 references the “ABC Corporation” in parentheses. Appropriate business rules need to be put in place to make sure that the organization associated with the ORGANIZATION GL ACCOUNT makes sense in relation to the PARTY associated with the ACCOUNTING TRANSACTION. For instance, if there is an INTERNAL TRANSACTION for ABC Corporation, then the TRANSACTION DETAIL records need to be related to ORGANIZATION GL ACCOUNTs of “ABC Corporation” and not of another internal organization.

The transaction ID and the trans detail seq id uniquely identify the TRANSACTION DETAIL because it is a detail record that breaks down the ACCOUNTING TRANSACTION. The debit/credit flag indicates whether the transaction detail is posted as a debit or credit to the appropriate general ledger account. The amount indicates the amount of that portion of the transaction. Many physical database designs implement the debit/credit flag as a positive or negative sign within the amount field so that arithmetic functions can be easily used to offset debits and credits.

It was stated that an ACCOUNTING TRANSACTION has at least two TRANSACTION DETAIL records. In many cases, an accounting transaction may have more than two detail entries. Consider the third transaction in Table 8.4, transaction ID 39776. This transaction was a payment against an invoice with a 2 percent discount taken for early payment. The transaction resulted in three detail records, a credit to clear the accounts receivable of $900, a cash increase of $882, and a discount expense of $18.

The fourth transaction in Table 8.4 (transaction ID 47874) provides an example of an accounting transaction with four detail records. The sale of a piece of equipment, in this case the pen engraving machine, resulted in a debit to cash of the $1,000 received, a debit of $200 that clears the accumulated depreciation of the machine, a credit of $800 that was the book value of the asset, and a credit to record the capital gain on the transaction of $400 ($1,000 received minus the net value of the equipment of $600).

Relationships between Accounting Transaction Details

Businesses need to answer questions regarding the relationships between certain transactions. For example, which invoices have been paid off through which payments, and which invoices are still outstanding? Which invoices have been reduced via credit memos issued to customers? Which payments were subsequently sent back to the originating party because they did not correspond to an invoice or amount due?

The recursive relationship around TRANSACTION DETAIL provides the capability to track which accounting transaction details are associated with other transaction details. Using this recursive relationship, the model can provide the information to answer the previous questions.

Is there a need for TRANSACTION DETAIL recursions showing which payment was for which obligation? Is this not derived information, as one can see that a payment for $500 paid off an obligation of $500? What if there were several obligations for $500? It is necessary to maintain which payment paid off which obligation. When partial payments occur, it is even more important to track which payments are paying off which obligations. Similarly, it is also important to track which obligations are related to which obligations (an invoice with a related credit, for example).

Table 8.5 illustrates how the model can be used to relate different accounting transactions to one another. A very common type of related transaction is what payments are made against which invoices. Transaction ID 38948 shows that $900 is due as an accounts receivable. The next transaction shown (39776) is a payment that is applied to this invoice. The last column, Associated Transaction ID and TRANS Detail Seq ID, represents the recursive relationship from one transaction detail to another transaction detail. In this case, it identifies that the credit to accounts receivable is specifically regarding transaction 38948, which was the original invoice that was paid off.

Table 8.5 Transaction Detail Relationships

Table 8.5 also shows that two invoices (transactions 50984 and 50999) were paid off via a single payment (transaction 60985). In this case, the transaction detail representing the “accounts receivable” entry was split into two detail records in order to identify the amounts allocated for each of the two invoices.

This model can accommodate any type of transaction relationship that occurs in accounting. For instance, it can provide the information to maintain credit memos that reduce invoice amounts (obligations related to other obligations), refunds of payments (payments related to other payments), partial payments applied to invoices (payments to obligations), and sales of depreciated equipment applied to the original purchase transaction (payments related to payments and to internal transactions; namely, depreciation).

Account Balances and Transactions

Should each TRANSACTION DETAIL be related to the ORGANIZATION GL ACCOUNT, as it is in the previous model, or should it be related to an entity that stores the balances for the account for each accounting period?

There is a strong argument for modeling the account balance as an entity. After all, the financial statements and other financial reporting will most likely be based on account balances, making this is a critical piece of information. Also, managers will frequently want to see the balance for a particular general ledger account for a period without necessarily looking up the related transactions. Furthermore, the related transactions may be archived for account balances for previous years.

The model in Figure 8.3a does not show the account balance as either an entity or attribute because the account balance amount is derived information from the transactions that affect the account. Whenever derived data is included in a data model, there is redundant information. When there is redundant information modeled in a system, data synchronization issues occur that can affect the accuracy of data. Regarding account balances, one can argue that the information doesn't change much after the period ends so it is not much of a data synchronization issue. Retroactive accounting adjustments for past periods could complicate matters and make the storing of account balances in a logical model unwise.

Certainly in the physical implementation of this logical model, it may be a good idea to include account balances for various time periods. Managers will no doubt need fast access to this information, and the physical design should not have to scan through the transactions associated with the general ledger account to determine the account balance.

Even though the modeling of account balance does not represent a “pure” data modeling practice, many data modelers would argue that it needs to be included for the model to be complete and practical. Therefore, Figure 8.3b shows an alternate model that includes account balance information. This data model would represent a very practical database design for implementation purposes.

Figure 8.3b Accounting transactions detail with account balances.

Figure 8.3b shows that the ORGANZATION GL ACCOUNT BALANCE has been inserted between the TRANSACTION DETAIL and the ORGANIZATION GL ACCOUNT. This allows direct access to the critical attribute amountin the ORGANIZATION GL ACCOUNT BALANCE, which stores the current balance of the ORGANIZATION GL ACCOUNT for a certain ACCOUNTING PERIOD.

In accounting, organizations often keep subsidiary ledgers to track the status of specific accounts. There may be an “accounts receivable” general ledger account to show how much is owed to the enterprise. This account may be composed of accounts receivable subsidiary ledger accounts showing the amounts owed and paid for each bill-to customer or other party that owes moneys. Similarly, the general ledger “accounts payable” account has subsidiary ledger accounts, each of which represents suppliers or other parties that owe money to the enterprise. General ledger accounts to represent various products or product categories may also be captured as separate general ledger accounts and rolled into an overall product revenue account.

Figure 8.4 provides a data model to capture the information requirements of subsidiary ledgers. The diagram has a recursive relationship showing that each ORGANIZATION GL ACCOUNT may comprise one or more other ORGANIZATION GL ACCOUNTs. The parent general ledger account represents an account such as accounts payable or accounts receivable. The recursive comprised of relationship relates to the associated subsidiary ledger accounts, which each maintain information about a specific customer, supplier, product, or product category. Each of those subsidiary accounts may be related to other entities in the data model such as BILL TO CUSTOMER (a subtype of PARTY ROLE), SUPPLIER (a subtype of PARTY ROLE), PRODUCT, or PRODUCT TYPE. General ledger accounts may be related to particular products in order to track the revenues produced by a specific product, or if there are a great deal of products, then the general ledger accounts may be related to product categories.

Figure 8.4 General ledger account associations and subsidiary ledger accounts.

Subsidiary general ledger accounts are related to the roles of BILL TO CUSTOMER and SUPPLIER, which represent very specific roles of parties. It could be that other parties in other roles owe moneys to the enterprise and/or the enterprise owes moneys to them. Therefore, the model could show relationships to PARTY as an alternate, more generic structure, instead of tying them to the specific roles of BILL TO CUSTOMER and/or SUPPLIER.

Additional entities are used to determine how certain accounting transactions are calculated. This section illustrates the means by which a common type of internal transaction, namely, depreciation, is calculated.

As shown in Figure 8.5, each DEPRECIATION transaction is specifically for one and only one FIXED ASSET (described in Chapter 6). A FIXED ASSET may be depreciated using DEPRECIATION METHODs. The same depreciation method may be used to depreciate more than one fixed asset, and a fixed asset may have more than one DEPRECIATION METHOD over time because a fixed asset's depreciation method may change (although this may be regulated by agencies such as the IRS). Therefore, the FIXED ASSET DEPRECIATION METHOD entity documents which depreciation method was used on each fixed asset during various periods of time.

Figure 8.5 Asset depreciation.

The DEPRECIATION METHOD entity has a description attribute that specifies the type of depreciation such as “straight line depreciation” or “double declining balance depreciation.” It also describes the formula for calculating depreciation. Table 8.6 illustrates examples of the type of information maintained for depreciation calculation purposes. In this example, the pen engraver used “double-declining balance” as a method for the year 1999; starting in 2000, it began using the “straight-line depreciation” method of depreciation. Although it may be very interesting to describe the formulas behind these depreciation methods (for a very select breed), this information can be found in any accounting book and is beyond the scope of this book.

Table 8.6 Fixed Asset Depreciation Method

Another aspect of financial control is budgeting. Figure 8.6 illustrates a data model that provides information on budgets that are set up to monitor the spending of moneys. Each BUDGET may be an OPERATING BUDGET for expense type items or a CAPITAL BUDGET for fixed assets and long-term items.

Figure 8.6 Budget definition.

The BUDGET TYPE allows the flexibility to categorize other types of budgets according to the needs of the organization. The BUDGET entity describes the information about the amounts of moneys needed for a group of expense items over a certain period of time. STANDARD TIME PERIOD maintains possible time periods for which budgets could be allocated. Each BUDGET may have many parties involved in various BUDGET ROLEs and several BUDGET STATUSes over time. BUDGET ROLEs for PARTYs (which may be a person or an organization) include the initiator of the budget request, the party for whom the budget is requested, the reviewer(s) of a budget, and the approver of the budget. Each BUDGET must be composed of one or more BUDGET ITEMs, each of which is described by a BUDGET ITEM TYPE that describes the budgeted items. BUDGET ITEMs may be recursively related to other BUDGET ITEMs, allowing for a hierarchy of budget item rollups.

Budgets are mechanisms for planning the spending of moneys. Figure 8.6 has a BUDGET entity that describes the key information regarding budgets. A budget is uniquely identified by a budget ID. The relationship to STANDARD TIME PERIOD identifies the time period for which the budget applies, including the from date and thru date for that period. This may represent different types of periods for different enterprises. The entity PERIOD TYPE identifies the particular type used by each defined period. Common period types are “month,” “quarter,” or “year.” The description attribute describes the budget at a high level.

Table 8.7 illustrates examples of the information in the BUDGET entity. Budget ID 29839 represents the 2001 annual budget submitted by the marketing department of ABC Corporation for its marketing expenses. Budget ID 38576 is a monthly budget, for June of 2002, from the administration department of ABC Corporation for its planned office expenses. Budget 39908 is a capital budget for the purchase of manufacturing machines in 2001.

Table 8.7 Budget Data

Notice that budgets are defined for individual parties that may be departments, divisions, organizations, or whatever organizational structure the enterprise uses. The budget should be defined at the lowest level in the organizations, thus allowing the enterprise the ability to roll up budgeted amounts to various levels.

Each BUDGET must be composed of one or more BUDGET ITEMs, which store the details of exactly what is being budgeted. The amount attribute defines the total amount of funds required for the item within the time period. The purpose attribute identifies why the items are needed, and the justification attribute describes why the budgeted amount of money should be expended. Each BUDGET ITEM is described by a BUDGET ITEM TYPE so that common budget item descriptions can be reused. BUDGET ITEMs may be comprised of other BUDGET ITEMs via the recursive relationship around BUDGET ITEM. Table 8.8 provides two simple examples of budget items within the budgets described in the previous section.

Table 8.8 Budget Item

Each BUDGET generally moves through various stages as the budget process unfolds. A budget is typically created on a certain date, reviewed, submitted for approval, then accepted, rejected, or sent back to the submitter for modifications.

Figure 8.6 shows that each BUDGET has one or more BUDGET STATUSes over time, each of which is described by a BUDGET STATUS TYPE, which is another subtype of STATUS TYPE. This structure provides for the tracking of the history of a budget through its various stages.

Table 8.9 illustrates examples of budget statuses. Notice that on November 15 when the budget was sent back to the submitter for modifications, it created the need for a new revision of the budget, which will be discussed in the next section.

Table 8.9 Budget Status

Each budget will usually go through a process whereby several budget revisions are created for a BUDGET. Figure 8.7 provides two alternatives for how BUDGET REVISION information may be stored, depending on the needs of the enterprise. If the enterprise does not need to track each change to a budget and if it considers each revision to a budget a whole new budget, then the top model will work. If the enterprise wants to track changes to each budgeted item over time, then the bottom model is needed.

Figure 8.7 Budget revisions.

The top model in Figure 8.7 simply shows that budget revisions may simply be handled by creating and maintaining a whole new budget each time a revision is needed. The old budget can then be related to the next budget via the recursive relationship around BUDGET. While this model is very simple, the disadvantage is that the whole budget needs to be rerecorded, even though many of the budgeted items may remain consistent from one revision to the next. Also, this model will not track the history of changes that were made from one budget revision to the next. This model is designed for organizations with relatively simply budgets and budgeting needs.

The bottom model in Figure 8.7 shows that each BUDGET may have one or more BUDGET REVISIONs over time, which can affect many parts of the BUDGET. Each BUDGET is composed of one or more BUDGET ITEMs, each of which may be affected by one or more BUDGET REVISION IMPACTs. Each BUDGET REVISION may affect more than one BUDGET ITEM and vice versa, thus resulting in the many-to-many relationship between BUDGET ITEMs and BUDGET REVISIONs, resolved by the BUDGET REVISION IMPACTs, which is an associative entity.

The revised amount attribute of BUDGET REVISION IMPACT maintains the reduction or increased amount of a budgeted item. The add delete flag shows which budget items have been added or deleted according to the budget revision. The revision reason attribute shows why each budgeted item needed to be changed.

Because budgets may go through many revisions or versions, the BUDGET REVISION entity is used to maintain each revision in its entirety. Each BUDGET REVISION is uniquely identified by the budget ID and the revision seq that specifies the version of the budget.

Table 8.10 illustrates examples of the information in the BUDGET REVISION entity. This example shows that budget 29839 had two revisions, 1.1 and 1.2.

Table 8.10 Budget Revision Impact

The initial budget was subsequently revised by revision 1.1. Revision 1.1 consisted of changes to items 2 and 3 and adding an item for Internet advertising. This shows that a BUDGET REVISION can affect more than one BUDGET ITEM. Revision 1.2 was needed to adjust the direct mail budget again, showing that the same BUDGET ITEM may be affected by more than one BUDGET REVISION. This example, which confirms the need for a many-to-many relationship, is accounted for using the BUDGET REVISION IMPACT entity, which stores the changes to the BUDGET ITEMs. With this structure, both the current and change history of the budget can be maintained and accessed.

In the budgeting process several people may be involved in reviewing a budget for approval. Depending on the degree of formality in the budget process of the enterprise, there may be a need to track the results of each budget review. The BUDGET REVIEW, PARTY, and BUDGET REVIEW RESULT TYPE entities in Figure 8.8 provide for the tracking of the parties involved in budget reviews as well as the results of the budget review process.

Figure 8.8 Budget review.

The BUDGET REVIEW entity provides the information about which parties were involved in the review process via the relationship from BUDGET REVIEW to PARTY. The review date identifies when they were involved in the review. The comment attribute allows any personal opinions about the review to be documented. Each person's decision regarding the budget review is indicated via the relationship to BUDGET REVIEW RESULT TYPE.

Is the budget review process related to the BUDGET entity or the BUDGET REVISION? While each revision may be reviewed, each BUDGET REVISION is really a part of the BUDGET and is thus covered in the review process. Therefore, the BUDGET REVIEW is related to the BUDGET, which may include one or more BUDGET REVISIONs.

Table 8.11 illustrates the information that may be contained in the BUDGET REVIEW process. The example provides information on the people involved in the budget review process and their comments and conclusions. This information serves as supporting information regarding budget reviews and could ultimately affect the BUDGET STATUS, which was defined in Figure 8.6.

Table 8.11Budget Review

One may think that the BUDGET REVIEW entity is related to the BUDGET STATUS because the result of the reviews may affect the budget revision status. In reality, there is not really a direct data relationship between these entities because reviews and statuses each exist independently for a budget. The enterprise, however, may maintain business rules to determine what review results would constitute moving from one status to the next.

Budgeted items frequently have different figures associated with them based on various scenarios. For example, there may be different moneys allocated to a budgeted item depending on whether the market conditions are excellent, fair, or poor. The data model then needs a way to show what the budgeted amount is for the items under different conditions or scenarios.

Figure 8.9 provides a model that allows variations on the amounts budgeted based on different BUDGET SCENARIOS. Each BUDGET SCENARIO has a description that stores the type of scenario such as “excellent market condition,” “poor market conditions,” “worst case,” “best case,” “major deal signed,” “no major deal signed.” This allows maintaining multiple budgeted figures based on these conditions. Each BUDGET or BUDGET ITEM may have several BUDGET SCENARIO APPLICATIONs, which store either an amount change or a percentage change for each BUDGET SCENARIO. This means that these amounts or percentages may be applied uniformly across the whole budget (if it is related to the BUDGET) or may vary for each budgeted item (if it is related to the BUDGET ITEM). The amount change or percentage change maintains either the dollar amount of the change or the percentage of the change that is applied to each BUDGET ITEM amount, which will vary based on the particular BUDGET SCENARIO. For instance, there may be $10,000 more in the budget item for “marketing” if the BUDGET SCENARIO description is “excellent market conditions,” but there will be -$5,000 for the same BUDGET ITEM with a BUDGET SCENARIO of “poor market conditions.”

Figure 8.9 Budget scenario.

The BUDGET SCENARIO RULE stores the standard percentage change or amount change with which to raise or lower the amounts or percentages for standard BUDGET ITEM TYPEs. These rules may be the default amounts or percentages tied to the BUDGET ITEM SCENARIO; however, they may be different than the values for specific budgeted items because more might be known at budgeting time.

Table 8.12 provides an example of the values that may be in budget scenarios. The table shows that the budgeted item amounts may vary based on different scenarios. The “trade show” budget is $20,000; however the data structures provide for a 20 percent higher budget if there are excellent marketing conditions and 20 percent lower if poor marketing conditions. This implies that the budget is still $20,000 and is not changed in average marketing conditions. THE BUDGET SCENARIO RULE PERCENTAGE CHANGE column represents the suggested increase or decrease for the budget item type. The BUDGET SCENARIO APPLICATION PERCENTAGE CHANGE represents the actual percentage change that was used for the specific budget. The example that follows shows that the rule was used to define changes on scenarios for all budget items except for trade shows under “poor marketing conditions,” where the budget specified -20 percent instead of the suggested -15 percent.

Table 8.12 Budget Scenarios

Usage and Sources of Budgeted Amounts

Now that budgets have been set up, how does the organization monitor whether financial commitments have the proper budgeting appropriated for them and monitor what commitments and expenses have been made to each budget item? Certain transactions, such as requirements, orders, and payments, may need to be related to budgeted items in order to monitor ongoing use of budgets. The following models may be used to track budgets for expenditures (usages of budgeted amounts) or to track budget revenues (sources of budgeted amounts).

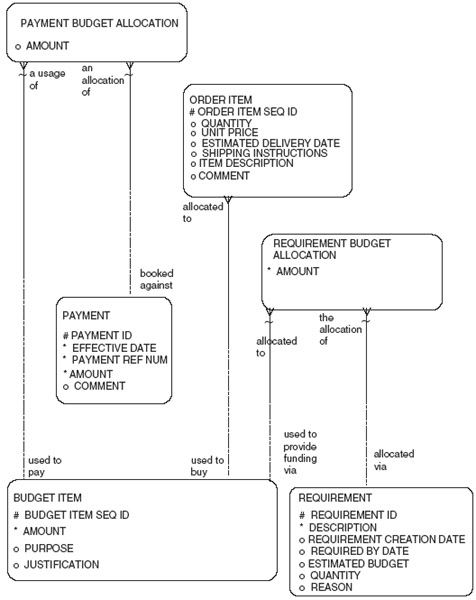

Figure 8.10 provides a data model to answer these questions. Each ORDER ITEM may be authorized via and allocated to a specific BUDGET ITEM. This relationship establishes what commitments (and dollar amounts) have been made to various budget items. A REQUIREMENT may be funded via many BUDGET ITEMS (and vice versa) through the entity REQUIRMENT BUDGET ALLOCATION. This relationship provides information about the outstanding needs for the use of budgets.

Figure 8.10 Budget allocations.

The many-to-many relationship between PAYMENT and BUDGET ITEM is resolved by using a PAYMENT BUDGET ALLOCATION entity. The PAYMENT BUDGET ALLOCATION records both disbursements and receipts against budget items, but only for disbursements that do not have a corresponding order associated with them. For disbursements that have a purchase order, the relationship between ORDER ITEM and BUDGET ITEM records the commitment of moneys against the budget. To determine the payment of moneys (which is the next step beyond the commitment) for disbursements that have a purchase order, the PAYMENT BUDGET ALLOCATION is not used because the budget item allocation can be derived from relationships from the PAYMENT to the corresponding PURCHASE ORDER ITEM of the purchase order.

The next two sections describe the model in Figure 8.10, which illustrates how to track commitments against budgeted amount, such as placing an order, as well as payments against budgets, such as the disbursement of funds.

Most enterprises involved in budgeting are interested in two types of comparisons against the budget: what commitments exist against a budget item, and what has been expended against a budget item. This section addresses the information needed to track commitments against a budget.

After a budget is approved, enterprises are interested in tracking commitments against a budget. An item on a purchase order may establish a commitment against a budget item. Therefore, in Figure 8.10, the data model illustrates that each ORDER ITEM may be allocated to one and only one BUDGET ITEM. The order item will generally be from a purchase order; however, for revenue budgets the same model can also be used for sales orders. For example, a purchase order item for 20 “Johnson Elite Pens” may be recorded against an administration department's budget item for “office supplies.”

One may conclude that each purchase order item is for a specific product and that each product corresponds to a particular budget item. This would result in a PRODUCT to BUDGET ITEM relationship instead of the ORDER ITEM to BUDGET ITEM. Although this may work in some circumstances, the allocation of a commitment is very dependent on the particular situation and usually cannot be generalized.

Consider the purchase of a personal computer (PC). On one purchase order, the PC is used for a systems development project and is tied to the budget item for that project. On another purchase order for a PC, the PC is for a particular employee and may be allocated to a computer equipment budget item. Therefore, rather than perform budget allocations based on the product being ordered, the ORDER ITEM determines the allocation to a BUDGET ITEM so that individual circumstances can be accommodated.

Budget items may also be used to provide funding for REQUIREMENTs to determine if those requirements can actually be implemented. In other words, before committing to a requirement, there may be a need to allocate it to a budget item in order to determine if there is enough money in the budget for this item. The cost of the requirement may need allocation to one or more BUDGET ITEMs. Figure 8.10 shows that each REQUIREMENT may be allocated to many BUDGET ITEMs and that one BUDGET ITEM may be used to fund more than one REQUIREMENT. Hence, this many-to-many relationship is resolved with the entity REQUIREMENT BUDGET ALLOCATION. The amount attribute is used to store the dollar allocation information so that total requirements for any given item are easily calculated.

For example, an internal repair order (i.e., a work requirement) to repair a personal computer may have an estimated cost of $50 per hour for the employee who is fixing it. This may represent a possible commitment toward a specific budget item such as “PC Repairs” (if the requirement is acted on). Over time, there could be many such orders against the same budgeted item.

On the other hand, a WORK REQUIREMENT for a project may require $100,000 total from several different budget items. In order to pay the project staff, the work order may need $80,000 from the BUDGET ITEM for “salary” that is included in a budget for research projects. In addition, the project may also need $20,000 for office supplies, which comes from a budget item for “office supplies” in the overhead budget for the enterprise.

In addition to knowing what commitments have been made against budget items, organizations also want to know what payments have been made against each budget item. The commitment, such as a purchase order item, represents an obligation to pay, whereas the payment, such as a disbursement, represents actual payments made against the budget item.

The data model shown in Figure 8.10 provides the ability to capture payments against budgets under two different scenarios: when there is an order prior to the disbursement and when there is an payment without an order preceding it.

When there is an order prior to the payment, the payment may be traced back to the corresponding order item. This is necessary to determine how much of the purchase order item is now expended versus what was committed against the budget item. In other words, the data model tracks disbursements against the corresponding order that is tied to the budget item. For instance, a $50,000 purchase order for an “office supplies” budget item may have a $25,000 disbursement against it. The $50,000 represents the budget item commitment. The $25,000 represents disbursements against that commitment.

The PAYMENT is related back to the ORDER ITEM through a series of data model transversals. The PAYMENT is related to the INVOICE ITEM entity through the INVOICE PAYMENT ITEM APPLICATION. Then each INVOICE ITEM is related to either SHIPMENT ITEMs (for goods) or directly to the ORDER ITEM (for services purchased). The SHIPMENT ITEM is then related back to an ORDER ITEM of a purchase order.

Needless to say, the relationships from a disbursement back to the originating order item are very complex and require numerous business rules. For instance, payments may pay off partial orders or many orders for various shipments. The enterprise will need business rules regarding how to allocate the disbursements to the appropriate purchase orders.

While it may be complex to trace back a payment to an order, it is also necessary if the budget is to accurately reflect committed and expended amounts against a budget item. Whether the information is stored in the database or a person manually figures out the budget allocation, the same process needs to occur: The disbursement needs to be mapped to the corresponding invoice, mapped to the shipment, then mapped to the order details, in order to figure out the proper budget allocation.

In some circumstances, an order may not be in place before the payment is made. For example, an employee may go out to a store and pay for items with a check, without a purchase order. Yet, this disbursement may still need to be allocated against a budget item. The data model shown in Figure 8.10 accommodates this circumstance by using the PAYMENT BUDGET ALLOCATION entity. This is an intersection entity between the BUDGET ITEM and the PAYMENT. The amount attribute records how much of each payment is allocated to each budget item.

Table 8.13 gives an example of a disbursement budget allocation. In this case, an employee went out to an office supplies store and wrote out a check for $2,000 for the purchase of a chair and some office supplies. This payment needs to be allocated between two budget items: office supplies and furniture. The first two columns of the table describe the budget and the item budgeted. The next three columns describe information about the disbursement. The last column shows that $500 of the transaction was allocated to the “office supplies” budget item and $1,500 was allocated to the “furniture” budget item.

Table 8.13 Disbursement Budget Allocation

This budget data model is intended to accommodate not only the purchase order commitment and disbursement side of budgeting but also the projected revenue and receipts of moneys. The model in Figure 8.10 can be used to accommodate the usage and source of moneys, meaning tracking sales order commitments and receipts against budgeted projections.

The PAYMENT BUDGET ALLOCATION may be for a RECEIPT or DISBURSEMENT, thereby including receipts of moneys as they relate to projected sales invoices. Also, the relationship from BUDGET ITEM to ORDER ITEM should allow tracking of items on sales orders as well as purchase orders. This model allows the enterprise to set up budgets for incoming and outgoing moneys.

Budget Relationship to General Ledger

Budgets are used for different purposes than general ledger accounts. Budgets are used to monitor disbursements; general ledger accounts are used to report the financial performance of an enterprise. Department managers may define budget items in any fashion that helps them control costs. Accountants categorize their chart of accounts to meet tax needs and various financial reporting needs.

Therefore, budget items may not correspond directly with general ledger accounts. It is very helpful (and sometimes required) to be able to tie budget items to general ledger accounts. An enterprise may want to see how much was budgeted and expended for a specific general ledger account such as “marketing expense.”

Figure 8.11 shows a data model that relates budget item types to general ledger accounts. Each BUDGET ITEM TYPE may be related to many GENERAL LEDGER ACCOUNTs and vice versa. Therefore, the GL BUDGET XREF entity resolves the many-to-many relationship.

Figure 8.11 Budget relationship to general ledger.

Table 8.14 illustrates examples of relationships between budget items and general ledger accounts. The first example illustrates a situation that accountants love! When a departmental manager uses the general ledger account name for budgeting purposes, then the budget item (“office supplies”) has a one-to-one mapping to the general ledger account (“office supplies expense”).

Table 8.14 General Ledger Budget Xref

The second example, illustrated by the second and third rows in Table 8.14, shows that many budget item types may correspond to a single general ledger account (this is still easy for accountants to track and audit). Budget items were set up for a sales director position and for a sales representative. These are both mapped to a general ledger account called “salaries expense.”

The third example is the most complex and will require more work on the part of the enterprise to maintain correctly. The fourth and fifth rows of Table 8.14 show that “marketing” budget items should be mapped 50 percent to “trade show” and 50 percent to “advertising expense” general ledger accounts.

The rules for how budget items map to general ledger accounts may change over time. The from date and thru date attributes on the GL BUDGET XREF entity allow different mappings over time. This model assumes that the mappings will be the same for different organizations within an enterprise.

Budgeted Items versus General Ledger Accounts

The previous model showed that there are standard mappings from budget item types to general ledger accounts. Another common information requirement is to show the budgeted figures as they compare to general ledger accounts. For example, there may be budgets for certain classifications of expenses, for depreciation, for projected revenues, or for any other general ledger account.

The model in Figure 8.11 can be used to find out the budgeted amount for each general ledger account. Each BUDGET ITEM is of a BUDGET ITEM TYPE that relates to one or more GENERAL LEDGER ACCOUNTs (thru GL BUDGET XREF), which then relates to the ORGANIZATION GL ACCOUNT, hence tying the budget item amount back to the specific general account for an organization. This relationship transversal is complex because of the fact that there may be many-to-many relationships between general ledger accounts and budgets. If there is always a one-to-one correspondence, the model could be changed to put in a one-to-one relationship between the GENERAL LEDGER ACCOUNT and BUDGET ITEM TYPE instead of the associative GL BUDGET XREF. Furthermore, with a one-to-one relationship, one could show budgeted amount as a field in the ORGANIZATION GL ACCOUNT in lieu of the BUDGET and BUDGET ITEM structures, if there was no need to store other budget information.

There are many similar accounting and budgeting information requirements among various enterprises. This chapter has included data models to establish charts of accounts for internal organizations, track accounting transactions, set up budgets, record budget revisions, maintain budget scenarios, maintain budget review process information, record commitments and allocations against budgets, and cross-reference budgets to general ledger accounts.

Figure 8.12 shows an overall view of the accounting and budgeting models included in this chapter.

Figure 8.12 Overall accounting and budgeting model.

Please refer to Appendix A for a listing of entities and attributes. SQL scripts to build tables and columns derived from the logical models in this book can be found on the full-blown CD-ROM, which is sold separately.