Chapter 5

Ancillary Arenas, Rights, & Products

Introduction

This chapter presents the ancillary arenas as they presently operate, points to where they are inextricably advancing, and the opportunities these changes present to producers and their teams. Perhaps of greatest value to some will be the revelation that for the most successful motion picture producers, their largest audiences and producer profits have and will continue to come from these ancillary areas—and how these producers strategically plan for these during development to assure they receive their full benefits.

Global Ancillary Arena Changes

As history proves, markets eventually adjust until they deliver consumers what they want. Accordingly, traditional release windows will continue to shorten and overlap. Other important, major changes will also continue in content ownership, in licensing terms between content owners and content delivery systems, and in existing and new online content delivery systems and their audiences. This evolution will advance, some of it quickly, until perfectly audience-dialed-in.

As always occurs in major cultural shifts, there are unique opportunities for one or more new or existing players to usher in the big changes. Surely one of the of the most anticipated is the entity deft, bold, and visionary sufficient to become the OTT (over-the-top) content streaming delivery system that global audiences eagerly seek. This will arrive with extraordinary acclaim, as it gives audiences the robust features to which they have become accustomed. Perhaps most especially this entity will provide its subscribers (almost surely free) access from a single source, to all the content they most relish, with an easy transaction selection of sponsor or pay, with no content clutter or asynchronous ads. Audiences love champions. Consider Apple, Google, and Amazon’s meteoric rise. This time, the entity true to the people’s vision of what must be will become a global media distribution powerhouse, optimizing the relationship between audiences, content, and advertisers—and be positioned to accomplish extraordinary, long-term good.

The advent of this entity is near term and will have a broad beneficial settling effect on the entertainment sector, uniquely beneficial for producers. Producers currently are enjoying an unparalleled season of production, largely enabled by technology that has increased consumer viewing, as they most always have a screen and internet connectivity, and new distribution entities, eager to connect them with the most sought after content. The future in many respects is renaissance-bright for producers and audiences.

Each Project’s Relationship Between Its Premier Release, Audiences, and Profits

The premier of every project is its most important life-point. The value of its entire earnings life is reflected from this brief event. The most successful producers do all possible to assure their project’s premier release uses every advantage to capture their target audience’s must-see commitment.

This is true for a project produced primarily to premier to mobile, or in theaters, or to traditional home entertainment, or to stream to all screens, or made for premium cable, network television, cable network, or a game platform. Regardless, the premier and ancillary arenas should all be planned during each project’s development and the premier only occurs when, and in a manner, that it will best optimize the project’s ancillary life.

During the passion of a project’s premier is when its brand is established and each target audience member decides if the project is important enough to experience, and if it is, if they will they see it during its premier, or later.

Projects Deserving Audiences

For a project to warrant being made at all, it should have what it takes to meet its target audiences’ expectations. Audiences want every project to set off an emotional fire in them worthy of telling others they must have this experience. Even the most outrageous special effects are never an audience-acceptable substitute for a compelling story, well told.

Entertainment industry icon Peter Guber put it this way, while speaking with independent producers during an American Film Market session:

“So is there a specific ingredient that’s essential for [a picture’s] success? My instinct, my curiosity, and my experience tell me that the key component is emotion. The story must have resonance and emotion. It must reside in the story…Watch your audience come out of a movie and see their state. Ask them to tell you about the film…When they tell you, or better yet show you, the impact it has on them, the emotion generated, then you better buckle your seat belt because you have a hit, even if the reviews aren’t good. That doesn’t mean a film can’t be thoughtful, it means the emotion must carry the information, not the other way around. What you have to move are not boxes of popcorn, or subs on a cable system, but people’s hearts and spirits.”

Audience reactions are the ultimate measure of a project’s entertainment power. If a project does not deserve its audiences, then it does not deserve the time, talent, and investment to produce and promote it.

Projects that emotionally ignite their audiences are the quest of great producers. This is the hungry search of all audiences, and every distributor among all its ancillary players.

When CNN’s Jason Carroll interviewed James Cameron about the imminent release of Avatar, Mr. Cameron said,

“When people have an experience that’s very powerful in the movie theatre, they want to go share it. They want to grab their friend and bring them, so that they can enjoy it. They want to be the person to bring them the news that this is something worth having in their life.”

This chapter demonstrates the essential power of story, brand establishment during each project’s premier, and how it is during their ancillary play that most fully developed projects are experienced by their largest audiences and earn producers their greatest profits. As you consider this chapter’s references, especially consider their application to the entire spectrum of projects. For instance, James Cameron’s Avatar and Aardman Animation’s Shaun the Sheep. Their budgets are as diverse as their premier windows, theme songs, electronic games, merchandisable items, and theme park attractions, but both share important qualities that demonstrate the benefits of producers focusing on story development, knowing their target audiences, playing to them, taking the project’s needed development time, and creating each project to deliver its full entertainment merits, in their premier brand development and ancillary arenas.

Audience Sizes in each Earnings Arena

In Chapter 2, we reviewed how improbable it is in most major global territories for theatrical release motion pictures to become profitable from their theatrical distribution alone. In this section, we will examine from where a project’s audiences and earnings come. As producers want to earn the most income possible from the most lucrative global territories, we use the U.S. as the prime example, with occasional references to other territories. Producers residing outside the U.S. should research, prepare, and use the income and audience information for their home territory and each of their other major global territories.

In the United States, for the 2016/2017 television season, there were approximately 320 million people total in the country—but material to a producer seeking project income from the U.S. is that there were 118 million television households and a potential audience of 2.6 per household (those between the ages of 5 and 80). This creates a total U.S. audience of 302 million consumers for each project’s several distribution segments.

Each project’s audience universe varies depending on the target audiences to whom it appeals; in which platform the project premiers; the dynamics of the picture’s campaign; and the heat of its media buy and promotion— especially viral and social media campaigns.

Theater Audiences

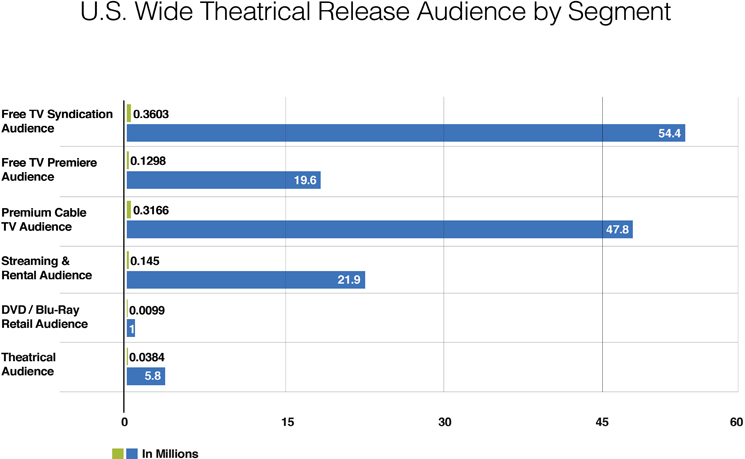

Per Box Office Mojo, the average U.S. theatrical gross box office revenue (GBO) among all 732 pictures released in 2016 was $15.4 million per picture. These numbers begin to be useful when knowing that 95 percent of that year’s total $11.3 billion GBO was earned by the leading 130 pictures. Further, the top 165 pictures were serious enough to reach at least 600 screens in their widest release, with an average $66 million GBO per picture. This chapter’s charts use U.S. released pictures attaining $50 million GBO or higher, as they had sufficiently strong brands to be seen by at least 50 percent of all U.S. audiences by the time they completed their initial U.S. television syndication.

At the 2016 average ticket price of $8.65, the average $50 million GBO picture played to a theatrical audience of approximately 5.8 million people, which is only 4 percent of its eventual audience.

It is beneficial for producers to see their projects’ theatrical audiences are a small percent of their total eventual audience. Though the theatrical window is crucially important for projects that premier in it, substantially determining the audiences and incomes in subsequent ancillary release segments, the theatrical audiences and profits to its producers are typically a small portion of the total audiences and producer’s profits. A study of Figure 5.1 below demonstrates the audiences in each distribution segment. This chart is for a U.S., wide release motion picture, with a GBO of $50 million, has multiple target audiences, so would likely be viewed by 50 percent of the U.S. audience by the end of its third year in television syndication.

Figure 5.1 U.S. Audience Distribution from “American Leisure Time Study (BLS. Gov).

Source: Fierce Cable.com and the-numbers.com

Streaming and Home Entertainment Audiences

Based on 2016 income performance of wide release pictures, this U.S. theatrical motion picture with a GBO of $50 million would earn a gross DVD/Blu-ray retail sales income of approximately $9.8 million and a streaming and rental income of about $59 million. This segment increases its audience by 23.4 million viewers, 16 percent of this project’s eventual total audience and four times its theatrical audience.

This segment includes all screens and audiences, except theater, inflight, and audiences viewing delivery via traditional cable or satellite systems.

Premium Cable Audiences

As with every prior rigid window, this one is also being distribution-upgraded. HBO is the U.S. lead premium cable network. As it began producing its own audience-powerful programming, holding and advancing its U.S. Premium Network lead position, so followed the other networks, Showtime and Starz-Encore. As their original programming increased the audience demand from non-HBO subscribers for their original programming, HBO released them alternatively via DVD and Blu-ray. As the demand increased, HBO renegotiated their cable and satellite systems license agreements, allowing them to stream their product to the substantially larger audiences that were not HBO’s subscribers. As is the way with the market, as consumers are given what they want, there is a flooding response from them when it is available.

This is yet another declaration that audiences want access to all content, by every open-market means. They are willing to pay for it. For premium cable networks, this clearly signals audience-willingness to pay to stream a program or series for a one-time streaming fee, if they are not subscribers, as well as consider alternate subscription relationships.

These new accesses make audiences happier, provide new revenues for premium cable networks—as well as to producers who provide or create content for them.

For content that was theatrically premiered in the U.S., approximately six months after its premiere, most pictures are released on premium cable, and this picture that has become a household name still has not been seen by 81 percent of its potential audience. U.S. premium cable audience penetration in 2016 was 92.2 million homes (including HBO Go and HBO Now, though there may be some duplicates). A reasonable premium cable audience allowance for a picture with a U.S. theatrical gross of $50 million will deliver another 47.9 million viewers. This increases the total U.S. audience reach to 77 million, still just over half its eventual total U.S. audience.

Free Television Broadcast or Cable Network

With an audience of almost 74 million new viewers who will see the picture during its free television segments, this is a valuable window for free television networks. The major broadcast networks license very few theatrically released pictures, leaving this content open for the cable networks, who are able and active licensees. This window traditionally opens 30 months after a picture’s theatrical release, playing to an audience of about 19.6 million.

Free Television Syndication

The free television syndication arena usually provides a picture’s largest audiences. For this picture, about 54.4 million viewers.

In every distribution segment, there are also repeat viewers, which are not included in this or the previous total audience figures. These are especially important revenue-building audiences for network, cable, and syndicated television.

Many theatrically released motion pictures become important social references that are a must-see-early for their target audiences and a free television curiosity tune-in for their distant fringe audiences. Whether it is The One Hundred Foot Journey, Captain America, or Hidden Figures, most of the 300 million potential U.S. audience members will eventually experience theatrically released motion pictures, even if seen partly on their phone, their tablet, and finally at home on their surround-sound, large-screen television. Theatrically released motion pictures are written and produced to be powerful, emotion charging, occasionally inspiring, and always thoroughly audience entertaining attractions. Each of these deserve to be carefully, dynamically branded, and full ancillary platform prepared to satisfy their audiences and be fully revenue generating.

Untethered Ancillary Audience Characteristics

Finally, we are ushering in the era in which audiences can consume the entertainment pitched to them, as soon as it’s available, on any device, at any time. Every studio, dialed-in producers, and all other major players are preparing.

Associated with this is the signaling of the new long-form productions, which are being voraciously audience-consumed. Not that long ago, many novelists wrote their novels, releasing them in chapters to anxious audiences, sending them off to distant lands, with readers desperately waiting on the docks to exchange hollers between them and passengers, asking if the boy lived; or who the woman chose to marry; or if the city’s wall held against the marauding horde.

Now audiences find themselves perched at the top of a story cliff for which they MUST know the outcome, before they go to bed. They have work or school the next day. But is Poldark ruined? Does Jack get the information needed to save the nation? Does Mr. Bates go to prison? Is Kinsey eaten? Did Gandalf just drop into the abyss of no return!

We have officially entered the era of the unfettered long-form to find audiences are not at all distracted by length. Like an awesome novel, they want it to last until there is no more story. Twenty one-hour episodes or 12 episodes of varying lengths. Regardless, the audience only cares about the story. Binge watching is now the new norm.

The new rule? The same as the old rule, just no attention to length. Story is all that matters. No longer adapting to 110/120 page scripts, now it’s only the optimal any-screen version of the story. How long will the first FULL form script be of Les Miserables, Tom Sawyer, Pinocchio, Starship Troopers, et al?

Exhibitors are resisting, yet futurists are anticipating an appropriately higher cost (about the cost of four theater tickets: $60–$80) to secure premium streaming available, day and date with the theatrical premier. From the distributors’ and producers’ point of view, this will increase each project’s brand heat, theater attendance/income, and reduce pirating. The marketplace will be healthier and audiences happier.

With the advent of a free, cloud-based distribution system providing secure access, content owners, subscribers and sponsors, will largely open a new era of creativity, production, distribution, and entertainment consumption never-before available and eagerly anticipated by all stake-holders.

Until then, the four major ancillary windows (home entertainment, premium cable, network television, and cable/syndicated television) will continue to bend and mold to growing audience needs/demands.

Consumers are passionate about making entertainment decisions, as these carry unique social importance. Movies are exotic merchandise, universally known and talked about, and our opinions about them and their impact on us help define who we are and where we socially fit.

Most people decide how they will view a picture by the time they have seen a picture’s third commercial/trailer. Typically, emotions rule over financial and even review considerations. Choosing among a theater ticket ($9 in the United States), a DVD/Blu-ray purchase ($10 to $15 in the United States), a rental or stream ($2 to $3 in the United States), a monthly premium cable subscription ($5-$12 in the United States), or free network/cable/syndicated television is rarely as important as wanting to see it now, or with a friend, or on a theater screen, or in its full uninterrupted length.

Some pictures are so compelling they override our viewing preferences and habits. Many people who never see a movie at a theater, or never buy/rent/stream/download, or who never see a movie twice will do so with certain pictures. This is demonstrated by audience-overwhelming entertainment like any of the Bourne, The Lord of the Rings, Harry Potter, or Twilight series, all of which drew uncommonly high audiences in all distribution windows.

In addition to our emotional connections with pictures, capriciousness often sways a person’s viewing choice. A consumer may just feel like seeing a picture at a theater, buying, renting, or streaming one, so the consumer goes online, goes to the local multiplex, or visits a retailer and seeks a title. If the movie the viewer wanted to see is not available, then they most often buy a ticket, a copy, or stream/download/rent a picture anyway. It may even be a picture they have relegated to see in a later ancillary window, but the viewer takes a chance.

Because they are aware of this phenomenon, producers and distributors often stage their release windows when school is out of session (the summer) or during holidays (especially Christmas and New Year for much of the world). These are the dominant seasons during which consumers seek more movie experiences, often making their picture selection while they are in the marketplace. This tendency is largely the motivation behind the industry’s glut of pictures during the holidays and then five to six months during the longer summer season. Many of the strongest pictures are released in these two highest-consuming distribution windows (theatrical and home entertainment). U.S. audiences consume more entertainment, in more windows, than any other territory’s audiences; yet all major European and Asian audiences are quickly closing the gap, China being the standout growth territory.

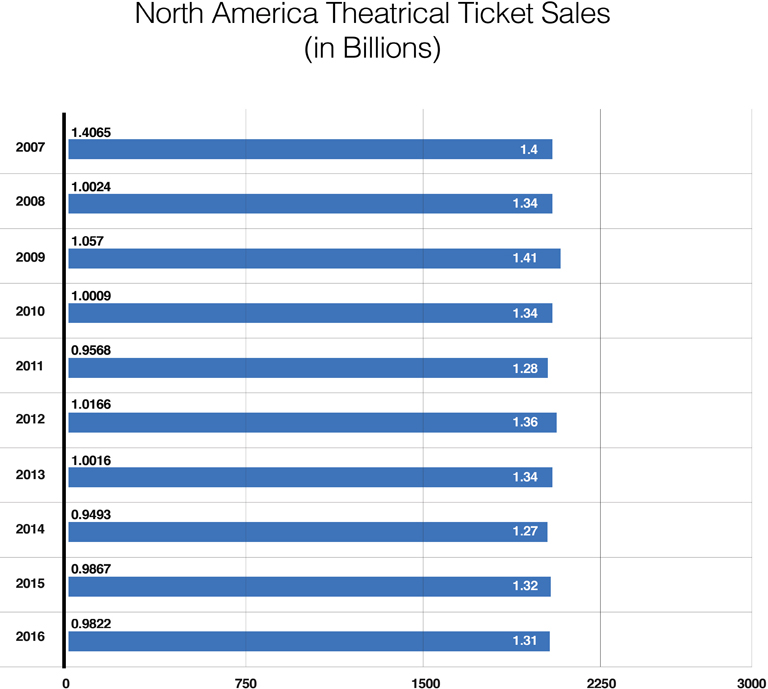

Despite the increasing availability and audience acquisition of sophisticated home entertainment equipment, theater audiences have sustained a steady market position in most global markets, significantly increasing theaters and ticket sales in most Asian territories, while shrinking in most western European territories. As Figure 5.2 demonstrates, ticket sales have remained approximately unchanged during the past 10 years in North America, so a slight per capita decrease, ticket prices increases indicating a year over year income increase.

During this same period, entertainment consumption has steadily increased in every major ancillary window except DVD/Blu-ray.

Youth are the greatest consumers of their targeted motion pictures in all media. As a group, they attend the theater more often than other segments and theirs is the leading cord-never group (they have never been cable/satellite/telco connected), so they stream/download on all screens more than any other group. They are also easier to sell projects for whom they are the targets, as they view and listen to more advertisements, are less influenced by critical reviews, and are most influenced by peer/social network comments and emoji.

MPAA (Motion Picture Association of America) statistics reveal the continuing trend of more women attending theaters than men. Producing pictures for adult women continues to be smart business.

Statistics are important indicators that are worthy of analysis by those who produce, distribute, and license motion pictures. However, statistics are easily misinterpreted. The reason women have become more aggressive entertainment consumers is because more entertainment in all sectors is being produced and distributed that interest them. Producers and studios are increasing their delivery to this powerful audience.

Regarding family movie viewing, there is a fairly-even split among industry mavens, between those who believe families don’t attend theaters more regularly because they spend less discretionary money than other audience categories and those who believe that there are simply fewer motion pictures that are targeted to couples with children at home.

Horror, chick, and fight pics have strong single-audience skews, whereas films like The Secret Life of Pets, Jungle Book and Dr. Strange are made for multiple target audiences, pulling from a much larger audience universe, so have higher potential income in all distribution windows and rights sales. Smart business.

Producers Rely on Ancillary Earnings

For U.S. and all major international territories, the theatrical release is unquestionably the most important distribution window through which each motion picture passes. This is where audience perceptions of each picture’s entertainment value are established, the size of the audiences in each distribution sector can be interpreted, and their respective earnings in them.

If the theatrical window is analyzed alone, neither the producer nor the distributor would release the picture. But when the ancillary windows weigh-in, projects often become sound business.

Projects premiering theatrically have a reputation that their stories are significant enough for the ultimate big screen. This provides them an unprecedented value available in no other way.

Ancillary Income: Project and Producer’s Gross Incomes

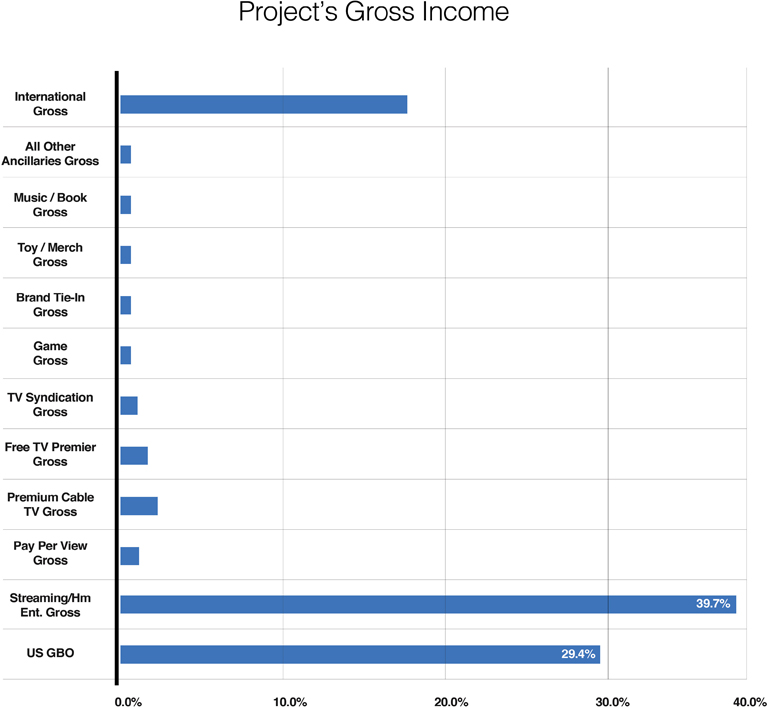

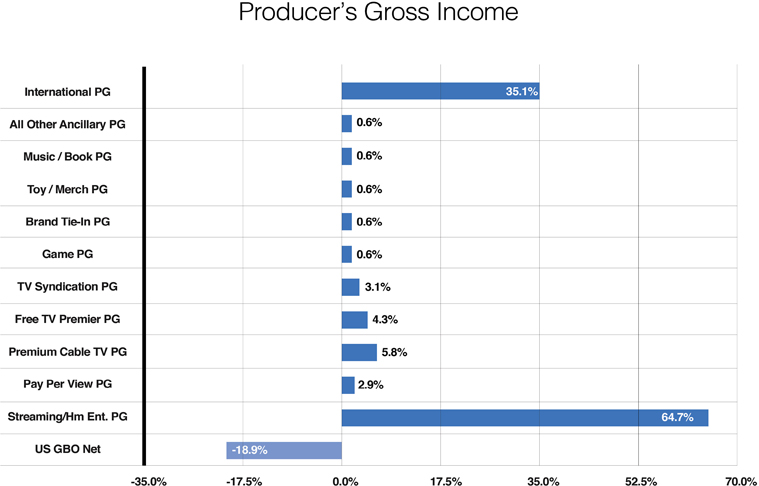

Figures 5.3 below shows the Project Gross Income that are the forecasted gross earnings amounts from this project in each earning sector, and in 5.4 shows the Producer’s Gross Income, which are the forecasted gross income amounts that would be paid to the production entity as earned from each sector.

Figure 5.3 Project’s Gross Income

Figure 5.4 Producer’s Gross Income

These are shown in percentages and use the same wide-release motion picture basis defining the audience forecasts in Figure 5.1. This thirty-thousand-foot view provides a perspective of a project’s audiences engagement and earnings for the U.S.

The First Ancillary Window: Home Entertainment Distribution

Every producer thrives on their projects’ experiences with audiences in theaters. Especially globally. It can only be experienced to understand the connection with hundreds of millions of people that used to be strangers, but with whom we exchange personal experiences by this extraordinary means. Producers create and bring their stories to market and massive audiences buy the ticket and spend the time to experience it.

Yet, study the two charts, above. Via streaming, each project connects with four times or more audience members than in theaters. The project earns 40 percent of its income from streaming—and 65 percent of producer’s earnings comes from streaming. Streaming is where the action is today—and it is destined to grow. With content available to consume everywhere, with ever-improved video and audio, streaming will continue to expand. VR (virtual reality) will surely EXPLODE as an audience must-experience. The high cost of VR gear may bring the masses to it initially via VR arcades. Expected to grow by multiple times per year through 2020, the real explosion will come as user volume increases passed the production tipping point, dropping the per unit cost. VR will become a massive consumer electronics phenomenon.

As introduced earlier in this chapter’s Audience section, the global Home Entertainment segment is quickly advancing through an extraordinary metamorphosis that will eventually launch one or more free OTT systems that provide audiences access to all content for which they have an interest, with shortened or overlapping window access, defined/regulated by cost-to-stream and sponsor interconnection with their unique targets.

When this occurs, the current theatrical window will retain, if not sharpen, its current reputation for being the ultimate venue for the most important stories, produced and presented in the most emotionally overwhelming manner. However, for projects initially released theatrically, this window will only be the set-up for the most dynamic home-entertainment window that will be dominated by streaming in all its forms and screens.

Currently, this powerhouse window opens about three months after a picture’s theatrical premiere. Video-on-demand (VOD) is first available via cable/satellite/Telco/online systems. Soon after, DVD/Blu-ray copies are available via retail. This window’s brief waterfall has already collapsed for some studios and other distributors. Then comes streaming, download, and rentals. These timings are expected to collapse, perhaps with a cascading of availability/streaming costs.

When these pictures open in their home entertainment window, they still carry their theatrical marketing power and sometimes are still playing in theatrical situations (usually second-run theaters). Some smaller independent distributors (Magnolia, IFC Films) are releasing films day-and-date with theatrical and VOD. IFC Films now operates two VOD channels, one for films in limited theatrical release and one for films that have appeared only at film festivals and will never make it to a theater.

As indicated previously, most members of the potential audience (96% for an average project) still have not seen this picture. For audience targets who missed seeing the picture while in theaters, they are either waiting for its home entertainment release or for a later ancillary window.

To differentiate and promote sell-through DVD/Blu-ray, these versions typically include extra features of above-the-line talent commentary, omitted scenes, out-takes, and sometimes alternate endings. The most popular pictures, three to six months after premiering in home entertainment, are released again at 40 percent to 60 percent less than their original sales price.

For breakout pictures in the U.S. with box office earnings of at least $120 million, the home entertainment strategy is especially well crafted. The strongest of these titles have the capacity to earn five times or more than their film rental and typically are released at lower sell-through prices to optimize volume and overall profits.

Though 2016 home entertainment gross and net income for DVD and Blu-ray income in the U.S. remained relatively constant and transparent, 2016 streaming incomes were challenging to calculate and apply to each picture, as the license terms varied, and license fees were at an historic all-time high (though expected to load-balance by 2020). Overall, streaming income from audiences is anticipated to continue its significant increase through 2020.

In 2016, a non-franchise, broad-audience animated motion picture with a GBO of $50 million was earning about $13.5 million from retail DVD/Blu-ray and $61.6 million from streaming to all screens and rentals.

Because home entertainment earnings in the U.S. represent the highest single income category for most pictures, every studio’s home entertainment distribution department concisely designs a separate release strategy for each picture.

The producer’s home entertainment distribution agreement with the studio is typically and appropriately linked with the picture’s theatrical distribution agreement. Terms vary, but the traditional relationship pays the studio a 25 percent to 35 percent distribution fee and recoups the studio’s direct distribution expenses, then the studio’s loss-carry-forward from theatrical distribution, if there is any. A returns reserve is usually also held, and, finally, the balance goes to the producer.

The Second Ancillary Segment: Premium Cable Television

Consumers eagerly embraced this subscriber fee, primarily major-theatrical-release motion picture, commercial-free release window, and it experienced aggressive growth in the United States during the early 1980s with HBO’s bold advent, later joined by competitors Showtime/TMC and Starz/Encore. The premium cable networks also provide mostly high-profile, award-winning original series and motion pictures. Subscriber growth was static, until recent license renegotiations with cable/satellite/Telco systems that allowed for direct OTT subscriptions. This has significantly increased their income and will likely continue its aggressive climb as these services also allow streaming of the content on a per stream basis for the much larger audience who are not subscribers. This will surely also increase their subscriber population. Premium cable service is growing in other international markets and continues to be introduced in other territories.

Premium cable is an important audience and earnings window, far simpler for producers and their teams to manage. There is a short list of potential licensees in each major global territory. In the United States these include HBO/Cinemax and their sister channels, Showtime, Starz/Encore, and EPIX.

These networks are very competitive for pictures because of the stability and growth of their subscriber bases, which are determined by the popularity and quantity of the pictures and series they broadcast. These networks gain subscribers by delivering major theatrically released motion pictures and original series. There is no revenue sharing on this playing field. The license fees paid are the total income from this release category.

In this segment, the initial exclusive premiere license is the greatest single income tier.

The premiere license provides for a limited number of airings for a limited time. The fee is determined by each picture’s theatrical release success. For pictures with unimpressive theatrical tickets sold, they may receive a license fee in the United States of five or six figures, if at all. For moderately and better performing pictures, they may engage U.S. license fees of seven or low eight figures. For licenses engaged before a picture’s theatrical release, they should include a license fee escalator clause. This clause calls for the license fee to increase if the picture’s GBO earnings exceed a certain minimum (for instance, $40 million) and then increases it again for every additional gross box office increments attained (for instance, each $10 million), but not to exceed a total license fee amount (for instance, $20 million).

The nonexclusive premium cable license tier allows for a greater number of airings for a substantially reduced license fee and for pictures with lower GBO may be included in the premiere license agreement. This tier continues until the free television network premiere occurs. Following the network premiere, the picture may still be licensed by premium cable networks, but for lesser amounts.

Subscriber marketing in this window is accomplished by the licensee network, primarily through network promotional spots, crossover network advertising through cable systems, and print ads.

Producers with slates (producing several pics over several years) manage these licenses directly. The producer must know each picture’s value to the network. Producers discover this as they research each picture during the preparation of the picture’s first draft global sales breakdown. This is discussed in Chapter 1 and is reviewed in Chapter 14. Basically, this is the process of identifying recently released pictures with similar target audiences, campaigns, and media buys. Then producers identify these pictures’ audience and financial performance in the United States and other leading international territories. This information allows the producer to more accurately forecast earnings as well as confidently prepare and negotiate these and other rights.

To assist them in securing and managing these licenses, producers often use an independent producer sales representative, hire an employee experienced in ancillary sales management, or use an industry attorney well exercised in this process.

The Third Ancillary Window: Network or Cable Television Premiere

Licensing network television is similar in some respects to licensing premium cable networks, although the marketplace is quite different. Broadcast networks are only interested in the biggest brands. They sell their audiences on their series, rarely a one-off event. The Academy Awards is a major exception. If a producer has a picture that big, then the broadcast networks are possible. Otherwise, the television premier will likely be a cable television network.

The network premiere of motion pictures is one of the most important distribution windows for two reasons: The network premiere is the first opportunity for audiences to view the picture without cost, and, more important, it is the first opportunity for almost every person in that territory to watch the picture at the same time.

Network executives are constantly challenged to capture high audience shares for their respective network, well-branded theatrically released motion pictures consistently deliver dominant audience shares. In some respects, the time from a picture’s theatrical release to its network premiere works to build its audience. Many viewers who have enjoyed the picture before will tune in again. Pictures that have been advertised so heavily through the three prior windows can pull especially large new and repeat audiences to their network premieres.

Though the approach to this license sale is similar to premium cable, there are a greater number of potential licensees in the market for television premieres. These primarily include NBC, ABC, CBS, Fox, and the CW broadcast networks, and the major cable television networks, especially TNT, TBS, USA, Discovery, A&E, and Lifetime, in this expanding license arena. Unlike premium cable, this license typically calls for single digit airings during 12 to 24 months.

Because each picture’s forecasted audience share determines its value to the network, there is a broad range of potential license fees. Most pictures forecasted 5 to 8 percent of GBO.

As with premium cable, larger producers license broadcast television directly. The preparation for this license is a natural part of the development and production process. Before earnest development, producers should have identified the most likely network license candidate and the value of the picture to this network, if it meets its box office forecast. By preparing thoroughly, producers can explore entering pre-theatrical release licenses with a network that can accommodate a tie-in “film-about-the-film,” which could provide programming to the network and additional marketing heat for the picture during its theatrical release. The network provides promotion and advertising for the picture principally via tune-in promotional spots over its own network.

Most producers use either in-house ancillary sales talent, or a producer’s representative to fulfill and maintain these relationships, with the producer’s attorney participating in this process. Occasionally producers license directly to network television, collapsing the premium cable window altogether. Producers electing to do this are typically motivated by an aggressive network willing to pay license fees equal or close to the combined fees for traditional premium and free television.

The Fourth Ancillary Window: Free Television Syndication

Television syndication is the evergreen audience and earnings television window. Syndication opens 12 to 24 months following the network premiere and continues to license-renew as long as the picture has audience draw. This is often several decades.

This window is sophisticated in every global territory because it deals with many television station groups and independent stations. It requires continual sales, license management, and digital delivery maintenance. This window usually is managed by a television syndication organization in each territory, which is compensated through distribution fees and expense recoupment. License fees vary widely in this window, depending substantially on the global territory, how long the picture has been in syndication, the number of airings allowed, the audience reach, the number of stations, and the length of the license.

Other Ancillary Rights

Producers should examine, identify, plan, and exploit every rights platform that may be applicable to each of their pictures. Some nontraditional ancillary rights actually may exceed the producer’s share of the picture’s traditional earnings areas. In the case of electronic games, this category alone can generate, in U.S. dollars, nine-figure incomes for some pictures. Their closely correlated marketing campaigns can also substantially increase income from traditional primary release windows.

Novelization

There are profits for producers from novelizing the picture’s screenplay or re-releasing an existing novel on which the picture is based. Typically, the greatest benefits to these licenses are realized by having the novel released four to twelve weeks prior to a picture’s theatrical premiere, with the picture’s one-sheet (poster) on its front cover. Producers are best served if they negotiate first with publishers for the quantity of the run and retail placement, then for profit participation. Having the novel for sale at mass merchandise, supermarket, drugstore, bookstore, and airport checkout lines just prior to a picture’s theatrical premiere is valuable advertising, perhaps more than book royalties.

The management of novelization rights begins during the motion picture literary rights negotiations. Some producers manage the whole universe of their pictures, including novelization rights, as part of their negotiations for their picture’s story. No matter how strong the novel has been previously, the motion picture likely will become a household name and drive novel sales as no other influence can.

If producers fail to acquire their picture’s novelization rights, then they should at least participate in the novelization (or re-release) publishing profits and should receive publisher commitments relative to the novel’s distribution tie-in to the picture’s theatrical marketing.

Each picture’s novelization should be scheduled with the publisher before principal photography commences, allowing at least five months for the publishing process after the novel has been completed.

Product Placements vs Branded Entertainment

Product placement is the insertion of brand logos and merchandise into films and television. Branded entertainment is a fairly new term for the sophisticated use of product placement and the integration of advertising into the entertainment content whereby the brands are embedded into storylines of a project.

Product Placement

An effective unit production manager (UPM) will make notes of proprietary items needed for principal photography. These brands must be cleared to be used in the project. Depending on a picture’s target audiences and how these products or locations may appear in the picture to the audiences, they typically are provided to the production company at no cost.

Motion pictures are the most powerful merchandise vehicles with which other branded merchandise can be associated. Even negative use of a product in a motion picture may have substantial positive marketing affect. For this reason, sophisticated brands increasingly participate within and in conjunction with motion picture marketing, which helps propel their products with greater power than they can achieve from alternative promotion and advertising processes. There are well over a hundred excellent examples of this effect, such as Wall Street. Motorola was one of the only players in the then sluggish cell phone business. It just was not launching at dynamic proportions. When audiences around the world watched Michael Douglas using his cell phone as an indispensable lifestyle device, an entire industry was dramatically launched. Delivery services, cars, motorcycles, mobile phones, computers, soft drinks, clothes, food products, airlines, hotels, destinations are all major categorical players in this arena, and it is growing.

Producers should carefully review their pictures, even period productions, for opportunities to engage brand relationships that have mutual benefits. Product placement companies will make these arrangements for a modest fee.

Branded Entertainment

Branded entertainment requires co-development and collaboration between the producers, media, and the brand company. Brands are seeking to integrate their product into the message of the film in a way they can control. In fact, many brand companies now have dedicated divisions just for branded entertainment and are substantially funding entertainment products to be in on the ground floor during development to showcase their products. Typically, they bring in up to 20 percent of a budget if the opportunity is right. Examples have been Hasbro with Battleship and Transformers, as well as Swaroski Entertainment funding 100 percent of Julian Fellowes’ Romeo & Juliet. See Chapter 6 Financing for more detailed information about branded entertainment as a form of financing for projects.

There is no income amount that should motivate producers to infringe on the creative integrity of their pictures; however, the best brand relationships have deepened pictures’ creativity, increased their profits, and pumped up their marketing campaigns.

The makers of most brands, from private aircraft to bottled water, are eager to establish these relationships. A call to most corporate headquarters will put a staffer in touch with the company’s executive directing product placement or branded entertainment. With a little research on prior pictures, the producer can use comparable brand relationships to assist in negotiations for his or her picture.

These relationships must be documented, the producer’s attorney review the documents and address the many unique questions. For instance, who is the insurer in the event of product loss or damage? If the contract language is “a minimum of five seconds/minutes of brand name recognition or integration” and the picture delivers less, what are the parties’ easy reconciliation provisions? Working through these details up front may seem like a bother at the time, but it will seem like a dream when problems are easily resolved when they arise.

Premium Tie-ins

Like product placement, premium tie-ins are related to consumer brands becoming more dominant through their association with a motion picture. A fast-food restaurant chain gives away or sells products related to the motion picture. The public can receive the products only through these outlets. They include character figures, special cups, hats, T-shirts, toy tractors or spaceships. Whatever they are, these products must mobilize the picture’s target audience to come to a brand outlet primarily through wide television or Internet advertising. As they do this, they also sell the picture. How much are the producers paid to participate in such a promotion? Usually, not anything directly. They are paid indirectly, however—$5 million or $10 million or more—when they engage a television ad or Internet campaign that simultaneously markets the picture. Some of these relationships have more than doubled the amount of advertising that would have been spent launching the motion picture. In 2009, the strongest opening picture of all time was Avatar. With an amazing number of promotional tie-in partners, the picture grossed more than $77 million its opening weekend. Promotional partners with kid-, youth-, and family-target audiences received reciprocal benefits from the producers, whose picture grossed $761 million in the United States, more than $2 billion in international territories, $395M in DVD/Blu-ray sales in just the U.S.

Sound Tracks and Music Publishing

The sound track for certain motion pictures can become a substantive income-producing product, as well as high-impact promotion element, especially with active Internet using target audiences. For some pictures, including Moana and La La Land, these earnings can be formidable, well worth putting a team on to orchestrate these earnings. In India’s Bollywood, music is the primary sales and marketing element for some pictures’ theatrical releases. Music is released and heavily promoted weeks before each picture’s release. By the theatrical premiere, target audiences, high on the music, are easily motivated to see the movie.

The powerful effect music has on each picture’s marketing should inspire how producers do the following:

- Select the composer and needle drops (use of already released music in the picture).

- Create a separate sound track production and distribution plan.

- Set the sound track production and release schedule.

- Handle contract deal points with the composer and other related music contributors to enable the promotion and earnings plan.

- Negotiate the sound track distribution and music publishing license(s) to enable the promotion and earnings plan.

Sound tracks are especially powerful earning and marketing elements of a motion picture when one of the picture’s primary target audiences is youth.

Again, the most reliable approach to managing these rights is researching recently released pictures with similar target audiences that have well-managed sound track marketing and licensing. Producers should study the successful deals that have been made, with whom they made them, and how these relationships were managed. From this information, the producer should create the model they are confident best serves the picture and will be served by it. After consulting with an attorney, the producer should then move forward with the marketing and licensing plan.

Sound track and music publishing normally is licensed to one or two highly skilled and experienced companies. The producer’s task is to understand the earnings and promotion power of this license area, evaluate the license, negotiate and manage the license relationship, and set a schedule that allows these rights to be exploited to the maximum earnings and promotion benefit for the picture.

Toys and Merchandising

Even motion pictures that appear unlikely candidates for toys and merchandising should be carefully considered. Often, there are toys or other merchandise items for adult, youth, or children’s audiences that seem like an amazing stretch. As producers become more involved in this licensing area, the wide appeal of movie merchandise for extensive global audiences becomes more apparent.

Each picture should be examined exclusively from the perspective of this license category. After a potential product list is made, research ought to be performed using projects with comparable target audiences. After the producer prepares a basic merchandise plan, approaches should be made by, through, or after consulting with a producer’s representative, who specializes in that licensing area. Though it is best to give them more time, these licensing companies will need 14 to 18 months prior to the motion picture’s theatrical release to prepare their licensing arena.

Retail Game Sales and Electronic Games

For some pictures, this category of products may have a substantially larger earnings capacity than all other earnings areas combined. Companies specializing in the game industry understand the power motion pictures have in launching games of all kinds. This category includes paper-based role-playing games, board games, electronic handheld games, console games, computer games—all sold at retail—as well as arcade games, motion control rides, the ever-expanding massively multiplayer online games (MMOs), and games specifically for mobile phones—which has become the single largest game player base, the most market influential and wildfire-viral spread.

Producers and their representatives specializing in this licensing area should analyze a picture’s game licensing prospects for the opportunity of representing the picture to this industry. It is best to have each picture reviewed by at least two competing representatives and have an attorney review the representative’s and all license agreements.

In-Flight

One of the most important and valuable audiences for almost every theatrically released motion picture is made up of air travelers, whose numbers will continue to grow for the foreseeable future. Especially on flights longer than two hours, airlines have learned that time passes fastest for passengers while they sleep or view entertainment. Whether they are offered an individualized selection or a passenger group screening, a theatrically released motion picture is the first entertainment preference of most passengers. Airline licenses represent an important incremental income and crossover promotion that builds additional ancillary audiences and income.

There are only a handful of excellent and very competitive in-flight distribution companies. Each studio also has an exceptional in-flight department. Producers should meet with competing companies and, with the support of an attorney, enter a distribution relationship.

Planning for this version in development and preproduction allows the producer to budget for cover shots (additional material that will be uniquely required in one or more territories outside the core territory for which the picture was produced; for example, less violence for Europe, no rough profanity or nudity for in-flight screenings, and so on), postproduction time, and to deliver a print at the opening of this market, which is after a picture’s premiere but during its theatrical release.

Hotels and Motels, Military, Schools, Indian Reservations, Ships at Sea, and Prison Systems

It is common for independent producers to use the studio that is theatrically distributing their picture to distribute these rights. Each of these rights areas is a small, five-and six-figure income category, but together they can earn a seven-figure income. Understanding that these ancillary earnings niches exist allows producers to plan for them, enter relationships with studio or ancillary rights distributors, exploit these rights, and expand the audience and earnings for their pictures.

Producing Cover Shots Needed for Ancillary Windows

During development, each picture should be reviewed for cover shots that may be needed to optimally service its ancillary markets. These additional elements increase expenses during principal photography and post, but they earn and/or save much more money and time later. They increase the picture’s ancillary value and allow the producer to deliver a seamless version of the picture to each participating licensee. Cover shots may be needed for unique international versions, airline audiences (in-flight versions), and the network version that must comply with network schedules and standards. Planning for and executing these during the development can allow for elements that are most acceptable to the director, producers, and other creatives that otherwise may not be possible.

Chapter Postscript

The most successful producers pour all their inspiration and genius into each story, its production, branding, and business strategy. Accordingly, they direct the planning, engagement, and oversight of their project’s full array of ancillary rights, knowing that these rights earn them their largest audiences and profits.

Producers are the parents and ultimate stewards of each project. It is the producer’s responsibility to assure every project fully exploits every feasible ancillary right and relationship. They will measure them, plan them, and with the participation of their team, always including their attorneys, they will enter relationships with strategic partners to dynamically create, exploit, manage, and ensure the best possible performance within each release window.

As if these were not enough, they will also track the several dynamic market changes, assuring their license agreements allow their content to adjust with new media changes—and they will begin developing the content for which audiences eagerly wait.