Chapter 6

Production Financing

Introduction

This chapter reviews the primary processes of production financing. It explores the many sources actively participating in this funding. Further, it demonstrates how balanced producers develop and use these relationships that include state and national production funding, production incentive programs, licenses, presales, third-party co-branding relationships, private equity, as well as international territory gap/estimate financing, to determine the funding that will provide each project the most benefits, including funding cost. Further, this chapter examines the use of a Production Financing Worksheet that leads producers through careful consideration and selection of these production funding sources, automatically calculating interest and other costs, simplifying setting up each project’s optimal financing architecture.

Planning is Essential to Funding

Beginning with the end in mind is a life practice of many successful people. This is especially true in assessing, planning, and engaging each project’s production funding. Most investors participate only in industries they understand by their own experiences in them. If they do make exceptions, it is most likely they would do so as a minor partner, relying on other investors experienced in entertainment.

Establishing a fully functional independent production entity involves:

- understanding the formidable benefits related to selecting each project’s unique funding partners

- having a working knowledge of and access to these production financing sources that include a relationship with a bank or alternate financial institution with an entertainment department able to aggregate each project’s funding from cash investors, collateral and guarantee providers, and

- fulfill the investment return objectives expected by all partners.

Development and Production Funding

Although it is less expensive, the development of each project is often more sophisticated, takes longer, and is a less predictable process than its production. Consequently, development is typically financed separately from production financing. This process is reviewed in Chapters 11 and 12.

Production Funding’s Present Global Bullish Condition

Perhaps not since the beginning of the motion picture industry has content been in greater global demand, more old-line and new funding sources active in entertainment financing, and, consequently, has there been such abundant production and distribution funding resources available to producers. The following two lists review the primary causes for this pleasant condition. As you review these lists, consider not only related funding sources, but also current and coming content creation opportunities.

The Internet has and/or is bringing:

- The steady growth of streaming audiences on all screens (the global infrastructure delivery to whom is currently being dominantly assured by Netflix, Google, and other major global players)

- The advent of almost every person having a small screen with them all the time, in major and medium territories

- Content’s ubiquitous availability on all screens

- Audiences steady content consumption growth

- Interactivity that gives distributors the ability to feed each audience member their own preferred content and ads

- Social networks that assure almost immediate audience-branding, after each project’s premier (though media-sophisticated and expensive advertising and promotion are still crucial to each project’s branding before it is released)

- The conversion of cable/satellite/telco television to OTT systems, that deliver audiences both linear programming and VOD

- VOD audience viewing selection, rather than scheduled programming, that will clearly become the dominant audience program selection process

- Global audiences’ inter-connectivity that enables dynamic new forms of global content branding

- The radical reduction in distributors’ content delivery costs (and able to deliver almost everywhere the Internet reaches, on every screen)

- The ability for producers to distribute directly to each audience member (beneficial if their content is sufficiently branded).

Other big items, not directly linked to the internet:

- Production’s technological advancements continue to allow filmmakers to create their projects at increasingly lower costs—growing profits, reducing risk, to the delight of all producer partners.

- More major territories are producing projects for global territory release.

- China commenced its serious global content creation and distribution presence by overhauling and radically expanding its production infrastructure, using top global production and distribution talent and acquiring distribution/production/exhibition/transmission operations within other major global territories.

- United States studios continue to produce fewer independent budgeted projects, focusing on massive budgeted tent-poles, franchises, and comic book heroes; providing further opportunities for Indy producers to create a greater number of more story-reliant projects with comparatively modest budgets.

- The global middle class is growing entertainment’s audiences by tens of millions per year.

- In the United States a big change came in 2016 when the JOBS (Jumpstart Our Business Startups) Act made available to independent producers a significant provision—Title III crowdfunding for non-accredited investors—opening film investment to the average person. Many independent investors have shifted at least part of their investments from large companies/projects to smaller companies/projects.

These favorable entertainment industry conditions are and will continue the entertainment industry’s boom as new, well-funded entrants lay their claims to content distribution turf that is just being forged. The battle for global audience dominance led by the long preparing, strategy-keen, well capitalized YouTube, and by the most high-profile-content-creation-active Netflix and Amazon, also includes each territory’s cable/telco/satellite entities that are certain to lose the overall game by nature of their fatally flawed technologies, but that are prime to win at least the near-term battle for each home’s fundamentally needed high-speed Internet.

This battle will continue until audiences choose their sweet-spot for the new distribution system(s) and their content preferences from the unprecedented content glut that is beyond the audience’s ability to consume and, what continues to be the biggest conversion-prevention in the United States: big licensing fees paid from cable/satellite/telco systems, the terms for which have prevented some of the highest profile content to be available via the Internet.

Most importantly for producers, the winners of these battles will largely be determined by those who license/acquire the most audience-favored content. As always, the producers delivering this content will be the most long-term rewarded.

Because the market is positive and hyperactive, independent producers may be tempted to produce without regard to distribution. This remains a disastrous course, unless there is high-probability-engagement plan for branding and distribution.

For project financing, successful producers are especially looking for their share from those sources spending the most on programming, have extraordinary global branding power, and offer producers a fair profit participation. Globally, these sources are Netflix and Amazon. Their basic production relationship structure may be reviewed on their websites. Production relationships with them is clearly material-centric. Even knowing Jeff Bezos or Reed Hastings will have little effect on getting a project greenlit. Powerhouse content and highly marketable talent attachments are the exclusive head-turners.

If you are outside the United States, especially in any of the leading 30 territories, find out who is the chief for Netflix and the chief for Amazon in your territory. Today there are mostly ground-floor opportunities, each potentially very beneficial for Indy producers. Their game is to produce audience-engaging, universal stories from that territory and release them to most all other territories. This is the key to their dynamic brand establishment in that territory and provides the greatest benefits to related content.

Consider how Netflix launched their first original series in Brazil. While first necessarily focusing on building Brazil’s Internet infrastructure, they then also secured what appeared was a Brazil story that would be huge there and potentially well received in their other 180 territories. They cast major Brazil stars, launched a major Netflix branding campaign (“Change Everything”), produced the first eight episodes of the first Netflix Brazil original series (entitled 3%) and the day after the launch were mobbed with overwhelming positive audience response, many of them having binge-watched all eight episodes overnight!

These indicators of where audiences already are show us where the entertainment industry is heading. Successful producers are developing stories to fill that space.

Private Equity Funding

Each year, an increasing number of entertainment projects are entirely financed by private investors. Some of these projects are from solid independent producers who smartly prepare their projects’ branding/release, as well as their production. However, private financing is:

- (1) often the most expensive cost of money

- (2) provides no creative or marketplace check and balance for the producer or investor(s), and

- (3) is often a sign of the producer’s lack of business connectivity to less costly and more beneficial industry capital sources.

Where private investors can be smart for the investor and producer is in providing a minority portion of production funding. This allows these investor(s) the stability of partnering with entertainment industry funding partners, and could allow the producer to license certain rights more favorably, reducing production cost-of-money by increasing the project’s income.

Entertainment Industry Funding and Financing Sources

Fortunately, today’s producers have a broad array of production financing sources available to them than ever before in motion picture history.

In addition to private investors, these sources include the following:

-

Government Funding Programs

Like other government grants, these media funding programs have qualifying criteria necessary to be met to qualify for funding that usually become only a portion of, but occasionally provide 100 percent of a project’s budget. Requirements typically include the producer being a native-born citizen of the granting country, but some allow co-productions with non-granting-citizen partners. Applications usually have 1 to 3 submission deadlines each year and many now require a signed distribution agreement, discovering the failure of most projects that do not have at least some distribution set-up before its production. The cost of these funds in equity and profit participation is often very reasonable, yet the creative restrictions are often narrow. If your government offers this funding, we recommend thoroughly understanding compliance, as these can be highly beneficial. - Production incentive programs (see Chapter 7)

- International territory presales

A presale is a contract whereby a distributor agrees to buy or license certain project rights in a specific territory, for a pre-agreed amount, of which typically 10 percent to 20 percent is payable upon signing and the remainder upon acceptance of delivery and first release window. - Ancillary presale

Like an international presale, but with an ancillary participant such as premium television or electronic game. - Gap/estimate financing

A bank or other lender, lends the producer an amount equal to a discounted amount, typically 50 percent, of the value of the unsold international territories, based on their estimated value provided from a qualified/bankable international sales agent. Some banks have a lending limit for this facility of $2.5 million or 20 percent of the budget, whichever is less. - Talent profit/equity

This is all or a portion of a key talent’s compensation converted to picture profits participation that could result in their being compensated much more than otherwise. - Vendor profit/equity

Commonly referred to as “contra deal,” in which key vendor compensation is converted to project profits participation providing opportunity for higher earnings. - Crowdfunding (Donations. See Chapter 4) and Crowdfinancing (Equity)

- Corporate sponsorship or brand tie-ins (See Chapter 5)

As producers use multiple funding facilities to finance each project, their bank, or alternative funding source, becomes the crucial aggregating and participating financing participant.

Regardless of the combination of financing sources, the bank or alternative source is almost always used for each project’s depository, cash disbursements, and loans against the broad variety of collateral and guarantee instruments. It must be stressed that banks provide loans, not equity capital. They take “no risk,” charge interest as well as fees for their services, and expect full repayment within specified terms. Every bank financing arrangement requires a completion bond and a collection account. The two main U.S.-based bond companies are Film Finances and UniFi Completion Guarantors. The two main collection account managers are Freeway Entertainment and Fintage House. Completion bonds and collection accounts are necessary for producers to convert presales, gap financing, or other bank collateral sources into production capital.

Balanced producers typically receive and exercise most their production financing through their bank. Knowing that a project’s production financing is managed through a bank’s full-service entertainment department indicates that the project’s financing has likely been derived from sources that provide the greatest creative and marketplace benefits.

The Banking Business

Banks are often referred to as institutions. They are certainly governed by more agencies than most other businesses, but banking is a business. Banking decisions are profit motivated and predicated on sound business principles.

Every time the trade papers carry a story stating that a specific bank has supplied production funding to an independent producer, that bank’s entertainment department receives calls from naive producers. They set up appointments and arrive, armed with a script and a budget, ready to pitch to the bank as if it were a studio or equity financier. But banks make decisions with different criteria than those used by studios.

Knowing someone at a bank, like knowing someone at a studio, is helpful, but it has little effect on the bank’s lending decisions. The similarity between banks and other financing sources is that to obtain their support, it is critical to understand their unique criteria for making decisions and the way they operate.

Every bank’s inventory is its money. Banks principally earn profits by lending this money at interest. Like most businesses, banks sometimes have shortages or excesses of inventory. Though lending decisions have limited elasticity, when a bank’s lending reserves are low, its lending decisions become more restrictive. When lending reserves are high, its lending decisions are more relaxed. It is an important question, and proper form, to ask your loan officer the status of the bank’s current lending reserves.

Banks with strong entertainment divisions will always have the capacity to lend, even if they are not primarily lending their bank’s funds. If the division is making “good” loans, then their loss ratio is low, the loans serviced according to terms are high, and overall profits are high. With a strong loan portfolio, these divisions can perform as the lead (syndicating) bank with other participating banks, as well as engage other outside lending-capital scenarios.

When choosing the lead bank that will manage your production borrowing, select one that has a sound, experienced entertainment banking team. Bank lending in most markets is very conservative, as banks typically lend only on premium collateral. Producers’ funding planning and documentation are thoroughly reviewed in this chapter.

There are several major banks with entertainment departments active in motion picture financing including: Comerica, Union, Bank Leumi, East West Bank, First Republic Bank, and MUFG Union Bank. All these are active in the United States. There are also numerous funds that do entertainment lending as well, including: 120dB Films, Aperture Media partners, and VX119 Media Capital.

Each bank has loan amount preferences. There are small banks seeking loans in the six-to low-seven-figure amounts, midrange banks seeking loans in the seven-to low-eight-figure amounts, and more sophisticated banks seeking loans in the mid-eight-to low-nine-figure amounts. It is important to know a bank’s loan size criteria.

Basis of Lending Decisions

Banks make their lending decisions based on a combination of elements that must be represented clearly and completely in the loan package presented in this chapter. For loan approval, the loan package must demonstrate that the bank has collateral assurance for its return of principal, fees, and interest and that the loan can be reasonably debt-serviced through the production company’s regular course of doing business.

The ultimate assurance of repayment to the bank loan is the strength of the producer’s pledged collateral. Collateral alone, however, is not sufficient for loan approval. Banks do not want to lend if there is even a modest probability that they will be forced to call on collateral to recover a remaining amount due. Producers must demonstrate their ability to produce on budget and on schedule as assured by a completion bond, which is part of the loan package.

Each loan memorandum submitted to a bank should include, and its approval is substantially determined by, the following items.

Cover Letter

This letter provides a summary of all elements in the bank package. It describes the production company, a brief description of the project being produced, the requested production loan amount, the expected interest rate, the production timing and loan term, and the plan and timing for loan processing. The collateral is summarized and may include

- (1) production incentive program(s) and their portion of production budget contribution

- (2) writer, director, or actor payment offset for profit participation or project (special effects) equity ownership

- (3) SFX (special effects) entity or other production participant payment offset for larger payment from profits, profit participation, or project equity ownership

- (4) presales and their entities, amounts, and terms

- (5) major brand participants and their amounts and terms

- (6) gap or other funding requested by the bank and these amounts and terms

- (7) private equity participants and their amounts and terms.

Table of Contents

The pages of the bank memorandum should be numbered, and there should be a table of contents following the cover letter, which will assist the bank in reviewing the completeness of the package and in easily locating information in the memorandum.

Application

The bank’s loan application should be filled out, signed, and made a part of the memorandum. Some parts of the application may be referenced by “see page number” if the information is completely set forth in another section of the package.

Activity and Cash Flow Projections

Each of these projections should be month-to-month for the first year and cover at least six months beyond the anticipated active loan period. Each of these projections should have narrative “Notes to Projections,” which describe important characteristics about the projections that are not self-evident. The cash flow projection must include the loan proceeds and debt servicing, calculated at the rate represented in the cover letter.

Distribution Sectors and Liquidation Breakdown Summary

This section reveals the project’s planned distribution arenas and a conservative version of the liquidation breakdown estimate, including the producer’s share of gross receipts. This is especially important, in backup to international sales estimates, if the bank is requested to provide gap or related financing.

Collateral

In the initial loan memorandum, this is a descriptive list of the license agreements, international sales estimates, production incentives or equity, brand tie-in relationship(s), talent or vendor offset relationships, private equity relationships, and any other parties associated with providing collateral or direct investments in the project. Even if the bank is not managing these elements, it and the completion guarantor will need to verify that the production entity has access to the project’s complete production budget.

Conditional Documents

The bank will not take any substantial risk. If the license agreements used as collateral specify any conditions not satisfied by the completion bond, these further conditions must also be satisfied. The most common additional condition in international presale or domestic ancillary license agreements is that the project must be released in a specific territory (for instance, the United States) by any one of a specified list of distributors. If this is a condition, a copy of the distribution agreement or a binding commitment letter acceptable to the bank must also be included in the loan package.

Collection Account Commitment

The bank will require that a collection account manager (CAM) be secured to protect all parties. The collection account manager monitors the revenue collection process, the allocation and payment of revenue, and the exploitation of all potential revenue streams. There are two companies whose services we recommend: Freeway Entertainment and Fintage House. Both have been the collection account manager for hundreds of film and television productions, and 99 percent of the independent world works with them: Woody Allen, Annapurna Pictures, Lionsgate, Martin Scorsese, to name a few. The collection account manager computes revenue streams, provides the relevant stakeholders with regular reports, and splits revenues between each party in accordance with the party’s contractually agreed entitlement. Knowing the producer is using a collection account manager mitigates risk and provides confidence and security to potential investors, talent, and other profit participants.

Completion Bond Commitment

In the initial loan memorandum, this may be in the form of a conditional commitment letter that will be replaced with the bond commitment in the final loan documentation.

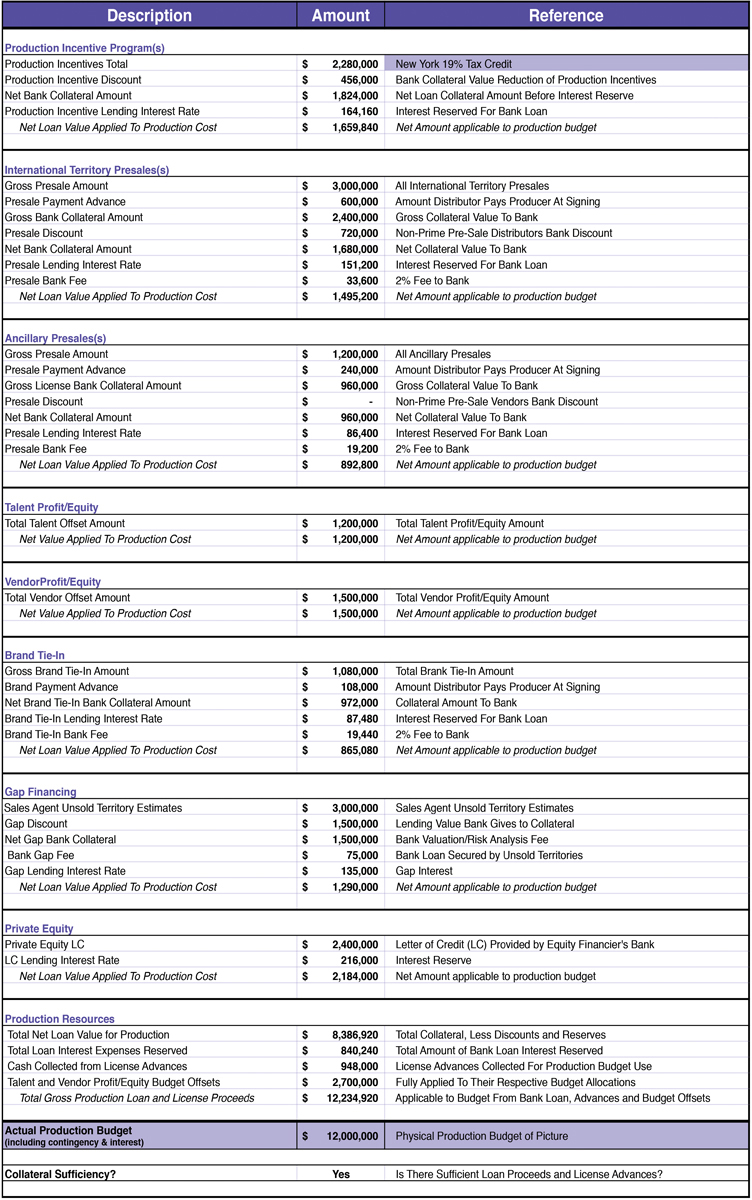

Production Financing Worksheet

To simplify your understanding of this worksheet, Figure 6.1 is below and a formula-charged excel worksheet is included on this book’s eResources page, www.routledge.com/9781138050938. As you see, the upper right is a financing sources planning section to be filled initially with placeholders of intended participants while determining each project’s financing architecture and eventually changed to the actual sources and amounts. The upper left is an assumption section for interest, fees, and collateral discounts. Once these are completed, the main body automatically calculates and completes the worksheet, revealing the individual collateral net amounts of each category’s subtotal, the net loan value applied to production cost, and the total gross loan and license proceeds. These are compared with the project’s total production budget (including the completion bond, 10 percent contingency, and reserve for residuals if required by applicable guilds or unions), and a “Yes” is revealed when the plan yields sufficient to produce the project.

The Project’s Creative Information

This section should include the project’s title, a brief story synopsis, a list of the project’s primary talent and their referenced credits, the project’s production dates and locations, and the projected core-market theatrical release date.

Business History

The production company may be new, a resurrection of a prior company, a merger of companies, or something else. Regardless how short or long, the bank needs to know about the company’s genesis and progress.

Organization Chart

This is a simple chart that reveals the members of the production company team by their responsibilities and relationships to one another. There is a production company chart in Chapter 11 and a worksheet on the book’s eResources page, www.routledge.com/9781138050938.

Principals’ Biographies and Balance Sheets

The operators of the business are a key factor in a bank’s loan review. The bank looks at the experience of those who manage the business and the experience and balance sheets of those who substantially own the business. The bank may not ask for owners to guarantee the loan, but the owners’ financial profiles demonstrate their combined experience and success in asset management. This information typically is presented to the bank through brief, but specific, biographical summaries and in some instances a recent balance sheet of each individual.

Company Financials

These are the production company’s current balance sheet and, if applicable, a recent profit-and-loss statement. These should be signed by either an in-house accountant or, preferably, reviewed and signed by the company’s certified public accountant.

References

This is a list of references that importantly points to the way in which the producer does business and with whom. This list typically includes the completion guarantor (the firm and the producer’s contact); the producer’s law firm and primary attorney; the producer’s current bank and officer; the producer’s accounting firm and primary accountant; substantial trade references and contacts; and clients, studios, distributors, and licensees with whom the producer has dealt, along with each of their contacts.

The Loan Approval Process

Producers usually work with a bank loan officer. This officer helps the producer to do the following:

- Identify the strongest international sales agent and international distribution companies.

- Complete the loan package. The package must be complete before it can be reviewed.

- Perform a preliminary review. If the loan package underperforms in the loan officer’s evaluation, it is rejected. Common reasons for underperformance include insufficient or unstable collateral, an unstable management team, or an unpredictable repayment plan.

- Present the package to the bank’s loan committee. The bank loan committee then reviews the package and approves or declines the loan.

- Deliver the decision to the producer.

- Prepare and process the loan documentation.

- Open the funding facility to the producer.

Finance Plan: Production Financing Worksheet

Starting at the development phase of every project, the producer should prepare a production financing worksheet that is the basis for the presale plan and the bank financing package. At the development phase, most if not all of it will be estimated and projected. As the producer continues through the financing process, the estimated numbers will be replaced with actuals and the financing plan adjusted accordingly.

Throughout the project’s development process, global distributor relationships should begin early and intensify as development proceeds (see Chapters 1, 3, and 14). These relationships should include the core-territory distributor(s), typically providing at least theatrical, all-screen streaming and home entertainment (DVD or home VOD) distribution; distributors in the leading international markets; as well as prospective premium cable, network television, and other key ancillary licensees. As these relationships advance, it becomes increasingly apparent which of these licensees will enter presale contracts. (See Chapter 5.)

Before the producer ever approaches the major international territories for their initial presentation and consideration, the producer will have prepared the project’s first cash flow projections (a global gross and net earnings forecast for all major windows and ancillary earnings), compared the project to at least ten others with similar target audiences and campaign elements, and identified the international distributors with the greatest propensity to garner the highest gross for this project in their particular territories.

If fewer than four distributors in the major international territories respond positively and agree to correlate with the producer as the project continues its development (see the nine distribution relationship points listed in Chapter 3), then producers should either replace their commitments with alternative distributors or not commence development at that time. Though there is no license agreement during this time, all the participating distributors will be involved in the project’s development and preproduction, and will eventually place the project on their release schedule. The producer will exclusively correspond with and give press, promotion, and advertising materials to these distributors. However, the project will likely not be licensed to these distributors until development is close to completion.

At the very first distributor contact, these distributors have little motivation to tie up the project’s rights. But as the project becomes more substantive—with a shooting script, director, lead cast, locations, production design, video and print promotion materials, representation at the major markets, firm release dates, and as novelization and other rights mature—each of these distributors becomes increasingly motivated to secure the project’s presale license for its territory.

The production financing worksheet becomes an extension of the cash flow analysis and places on paper the various financing scenarios, allowing the producer to select the most advantageous course. This financing strategy becomes the basis for the finance plan.

Using the production financing worksheet should be exceptionally empowering, allowing you to apportion each project’s budget among several participants, consider the relationships, synergies, earnings, probabilities of engaging each, cost of money, and timing.

Figure 6.1 Production Financing Worksheet

Courtesy of Entertainment Strategy and The Gillen Group, LLC from “The Producer’s Business Handbook”

At the bottom of the worksheet is the question-and-answer section, as final proof that the financing architecture configuration provides sufficient collateral and capital to fully fund the production. The ‘Yes or No’ cell shifts from “No” to “Yes” when there is sufficient collateral to yield the full production capital.

Approaching each project’s financing by this method spreads the responsibilities and risk in a manner that makes the investment much more accessible to each participant and often retains major creative and business decisions for the producer. Private investors are especially motivated to participate when producers can represent that over half the funding is raised, is provided by multiple participants and most of them from the entertainment industry.

Using the worksheet enables producers to analyze and configure each project’s production funding plan early in development, and to adjust the worksheet as the project matures to the point of production, based on the final commitment of each participant. The final worksheet will reflect the actual elements provided and will be part of the bank loan memorandum submitted for approval. This sample worksheet is configured to deliver the project’s production budget of $12 million, from the proceeds of the collateralized loan, cash advances, equity, and production cost offsets.

Let’s now walk through each section of the production financing worksheet. All areas highlighted in green need to be filled in, which will then automatically calculate and fill in all other amounts and percentages.

Assumptions

The producer fills in this section as accurately as possible. Initially these will be estimates, but as financing coalesces, this section will be completed with actuals:

- The borrowing period of the loan should be listed in months. This will typically be 12 to 24 months.

- Presale, brand tie-in, and letter of credit (LC) interest rate is estimated at 6 percent (4 percent over LIBOR [London Interbank Offered Rate], here assuming LIBOR is 2 percent). This is a reasonable percentage spread with which to begin for fully secured collateral.

- Presale, brand tie-in, and letter of credit (LC) bank fees are estimated at 2 percent.

- Presale discount, international territory presale. If the distributor issuing the contract is not financially strong, the bank will discount the value of the contract anywhere from 10 percent to 50 percent. Our sample is a 30 percent discount. If the distributor is financially strong, no discount will be necessary, and then this line item would be at 0 percent.

- Presale discount, ancillary presale. If the distributor issuing the contract is not financially strong, the bank will discount the value of the contract anywhere from 10 percent to 50 percent. Our sample shows a 0 percent discount.

- The bank typically discounts production incentives 20 percent for U.S. programs, 10 percent for Canadian programs, and 10 percent to 25 percent for most international programs. In our example, because we are assuming a shoot in New York, we are discounting by 20 percent. Also, please note under Description: Production Incentive Programs–Amount, we are only taking a total of 19 percent of the full 30 percent below the line, because not every line item in the budget will be considered a New York spend.

- The incentive programs lending rate is calculated at 6 percent (4 percent over LIBOR, here assuming LIBOR is 2 percent).

- The presale payment advance is usually required by the bank to be a minimum of 20 percent of the total amount for licensing of all rights in a specific territory.

- The brand tie-in advance is usually required by the bank to be a minimum of 10 percent of the total amount for licensing of those rights.

- The gap lending interest rate is calculated at 6 percent (4 percent over LIBOR, here assuming LIBOR is 2 percent).

- The gap discount is typically 50 percent and terms currently with some banks are a maximum $2.5 million or 20 percent of the budget, whichever is less.

- The gap bank fee is calculated at 5 percent, as this is much higher risk collateral.

Financing Participants

This section sets forth the ten-primary production budget financing categories, including an “Other” line for anything not covered in the listed categories.

First the producer enters the project’s name, then the lead distributor. Next is the production budget at the top. Then, in the financing participant section, each of the ten funding categories is engaged by entering an amount in each that are expected to participate. This will automatically formulate a percentage of the budget, that is shown in the column to the left of each amount.

- 1. Government Production Funding Net Received

As discussed more thoroughly earlier in the chapter’s section “Entertainment Industry Related Funding,” this amount includes all net amounts received from that category of funding, typically at the national level, usually reserved for citizens, to both foster that nation’s entertainment industry, as well as possible cultural objectives. As these funds typically operate as a grant, there are rarely any discounts and often no repayment obligation. Consequently, these funds are shown as Net proceeds and automatically added into this worksheet’s Total Production Proceeds. - 2. Crowdfunding Net Receipts

As also reviewed in this chapter’s section “Entertainment Industry Related Funding and Financing Sources,” this amount includes all net amounts received from crowdfunding sources. - 3. Production Incentive Programs (See Chapter 7: Production Incentives)

There are numerous program variations worldwide, most covering 10 percent to 30 percent of the budget. Regardless the plan, their rebate or tax credits comes after the project is produced, allowing the final accounting to be done according to how much money verifiably was spent in the city, state, province, or country, this spending being the incentive source’s motivation to offer it. Banks and private funds such as 120dB in the U.S. and Hindsight Media in the UK (see Chapter 7) are typically engaged to advance these incentives for the production budget. - 4. International Territory Presales (Reviewed in Chapter 3)

Especially with the entity consolidations of the late 1990s, most participants financially strong enough to advance a presale are major distributors whose contract will be bank acceptable as collateral. If they are not rated high enough for your bank, the bank will either discount the value of the contract from 100 percent to as low as 50 percent or it may require a letter of credit from the distributor. In our sample, we are securing only presale contracts from “A” list distributors and no letter of credit is required. - 5. Ancillary Presales (Reviewed in Chapter 5)

These are presold rights, like international territory presales, and may be any of the participants reviewed in Chapter 5. - 6. Talent and Vendor Profit and Equity Offsets

Negotiating with one or more of each project’s key talent to be chiefly paid alternatively with an increased amount based on the project’s projected profits can potentially increase a talent’s earnings and potentially give them enhanced tax advantages while providing the project with a significant amount of its budget. This allows talent to earn appreciably more income if the project meets or exceeds its global projections.

Production participants who are a significant part of the project’s total cost should be considered as possible funding participants through having part or all their costs paid from the project’s profits. These participants are most often lead cast, director, VFX, and post production facilities.

The motivation for these profit participants is that the producer agrees to pay them an amount more than what they would have otherwise been paid, typically 10 percent to 20 percent more, pay it to them from a prioritized portion of producer’s gross profits, plus pay them an ongoing percentage of all the project’s producer’s net before EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) that could represent income several times their fee.

The greater each funding participant’s portion of the total production budget, the more alluring is the producer’s offer to them. The big items to negotiate are:- How much more will they be paid?

- As their primary concern is being paid at least what they would have received if they chose not to participate, what priority producer’s gross profits participation position (exceeding the participant’s percentage of the overall investment) will they be paid until they have at least been paid what would have earned?

- If their participation is significant enough to pay them an ongoing percentage of producer’s net profits before EBITDA, what percentage will this be?

- If the producer respects the participant’s production experience and opinion, and their participation warrants it, they may be provided a creative voice in the project and a producing title.

For instance, if the project’s budget is $20 million and the director’s fee is $2 million, their fee investment is 10 percent of the budget. The producer’s offer could agree to pay the director from 40 percent of the producer’s gross (that’s four times their investment amount) until they have been paid $2.5 million (125% of their direction fee) and then a continuing 3 percent of the producer’s net profits for the duration of the project’s long earnings life.

Especially with director and key acting talent, if they are given the opportunity to earn significantly more than they would have, the positive impact on their performance and the resulting production could be major and well worth the extra incentives.

It is crucially important to create the deal architecture for each of these relationships before any of them are negotiated. When producers are negotiating, they need to know the earnings and cash flow impact each deal has upon them and all other participants. They are benefited by having a deal points sheet with everyone’s target deals, so when in negotiations, all deals can be weighed, numbers adjusted, and even explanations given as to the producer’s terms ceilings.

- 7. Brand Integration (See Chapter 5)

Branded entertainment or integration is a fairly new term for the sophisticated use of product placement and the integration of advertising into the entertainment content whereby the brands are embedded into storylines of a project. Branded integration is an entertainment-based vehicle that is funded by and complementary to a brand’s marketing strategy. Ultimately, the motion picture gives the brand an opportunity to connect with its audience in a unique and engaging way. An extreme example is The Lego Movie—in essence the audience is just watching a 2-hour advertisement. The James Bond movies have always been strong in brand integration. Heineken tops the list paying a reported $45 million for a product integration in the 2012 film Skyfall.For many brands, entertainment projects represent their highest impact and most reasonably priced marketing expenditures and strategies, especially global brands. As projects proceed through each successive release window to increasingly larger audiences, motion pictures become the ever more effective and price-efficient marketing tool. For producers, these brands can also increase a project’s creative integrity and cross-promote/market the project. These negotiations typically need to conclude a year before a project’s premier release and early enough in the development phase of the screenplay to have the brand creatively integrated into the project. They have and continue to provide a project’s significant production and/or distribution funding. The key to securing branded financing is guaranteed distribution. The brand needs to know upfront that their audience eyes will be on the project before they will commit.

- 8. Gap/Estimate Financing

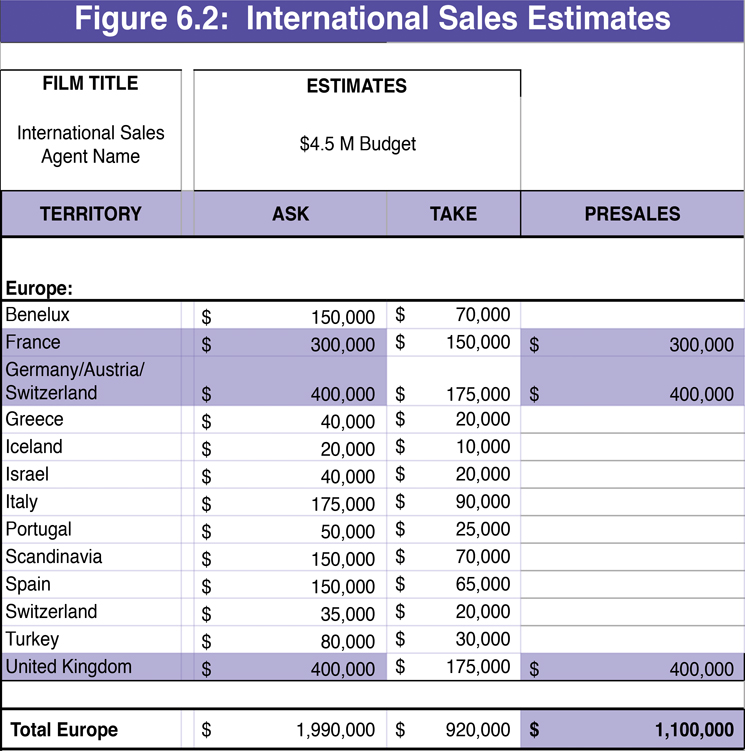

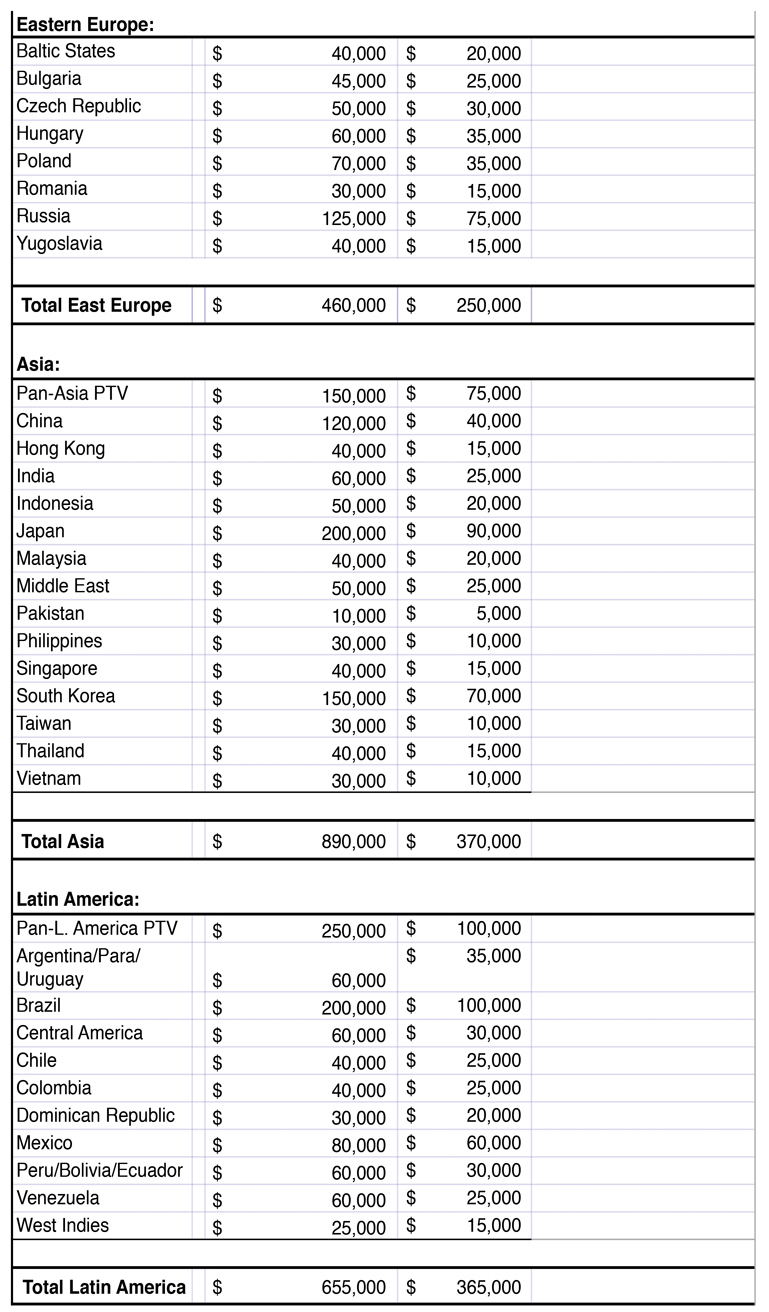

Gap financing is calculated based on the estimates received from a qualified/bankable ISA on the value of each international territory that was not presold. A sample ISA Estimates list is below (Figure 6.2). It is calculated at Ask price (or highest price for MG) and Take (lowest acceptable MG). The bank will discount up to 50 percent of the territories’ aggregate value based on the Take (low) price only. This discounted amount is then lent to the producer as part of the production financing (typically capped at $2.5 million or 20 percent of the budget, whichever is less). Gap financing is a risky model, and banks that do lend on these international sales estimates are constantly assessing the credit worthiness of ISAs and distributors worldwide. Typically, a bank will only accept a handful of ISAs’ estimates. Producers must approach the bank early to be sure they are working with an ISA acceptable to the bank.Though the bank loan fee is high, the producer’s advantages to gap financing are primarily that fewer presales are made, allowing these licensees to earn higher after-film-completion licenses, and the producer does not have to do the pre-sale work for these territories. The bank will require two and many times three presales from the top 12 territories before doing gap financing. These sales enable the bank to more closely evaluate the estimates supplied by the ISA.

- 9. Private Equity

The private equity sources in this example use collateral (CDs, treasury bills, securities, and so on) rather than cash. This example uses $2.4 million in private equity secured by a letter of credit, which therefore requires the bank to charge both an interest rate and a fee. If, however, the equity is in the form of cash, neither of these charges will be required. - 10. Other

This may include donations from a non-profit anxious to see the picture produced to benefit their cause and mission, or a loan from the production company or other sources. If this is used, include the net proceeds. This amount will automatically add in the total production proceeds.

Types of Loans

If the production loan is in the form of a line of credit, the producer has access to the entire loan amount but is charged interest only on the loan amount actually drawn. With more than $500,000 in potential interest, even a 20 percent interest savings (which is very possible with prudent cash management) will save more than $100,000.

When to Approach the Bank

Using bank production funding strengthens many aspects of producer operations. The bank relationship and its other related benefits should become integrated into and affect many aspects of the producer’s business.

New producers should meet with their bank of choice before completing their project’s development. Well before their need for production borrowing, producers should have initial meetings with their bank loan officer, introducing the production company’s business plan, the company’s development and production schedule, and clearly show the bank’s essential participation in the company’s overall success.

Producers should ask the loan officer for permission to use the bank and the officer as references to others relative to the producer’s intention to use the bank as the production funding source for projects. Most bank entertainment divisions are willing to allow producers to do this, if their representations are in keeping with the relationship. Using the bank as a reference to potential licensees and other sources in connection with the producer’s finance plan lends substantial positioning strength, especially for producers introducing new production entities.

In addition to production financing and later operating capital funding, bank officers can be well used as business consultants and mentors, contributing excellent business expertise to the production company and opening the way for expanded business relationships.

Private Equity: The Benefits of a Solid Business Plan

Securing private equity partners as part of each project’s financing has become more essential than ever. The financing sources of recent years (Abu Dhabi, India, and Russia) have been replaced by new sources including China, Singapore, and South Korea.

Equity partners expect a priority return-of-investment position, until they have been returned their total investment, and sometimes more (between 5% to 20%) than this amount. Their priority position typically provides them a percentage of profits that is greater than their investment’s percentage of the total capital raised. Once the investor has received the agreed amount, then their profit-sharing account indicates they have an “overage” until future profits distributions balances their account. Thereafter, with all other investor participants, they are paid their investment’s proportional share of the producer’s net profits before EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization).

To secure private equity partners, producers need to have a sophisticated and well-thought-out business plan with financial projections (sometimes referred to as a waterfall) that is tightly structured within an offering that is compliant with the securities laws of the areas in which it is offered (see Chapters 9 and 12). The business plan should include the following elements:

Executive Summary

One or two paragraphs that gives a concise overview of each of the following: the project, the company, the management and advisor team, the goals of the company, the finance plan, the marketing plan, the distribution plan, the investment opportunity, risk and its mitigation.

The Project

Give more detail about the genre; include a synopsis; explain the stages of development, production, and distribution; identify your target audience; and delineate your budget and how you intend to control costs. Explain the Finance Plan (how all the financing collateral will come together).

The Company

Explain the legal entity that has been or will be formed to produce the project. Include narrative bios on the managers/producers.

Marketing

Explain who your target and secondary audiences are; describe how you intend to engage them, even during development, preproduction, and production of the film (prerelease marketing), and explain any other methods you intend to use to develop and grow awareness of the film.

Securing Distribution

Without distribution, your investors have no opportunity to receive a return on their investment. Describe your clear and concise model and explain how you intend to implement it to offset the financial risks involved. An overview explaining the different media and ancillary markets, as well as a breakdown of fees and costs, is also recommended to be included in this section.

Investment Opportunity

Include detail about the financing sources that you will utilize and what you are offering the equity investors (i.e., rate of return and profit participation).

Risk Mitigation

Explain that as with all investment, the incentive for extraordinary earnings is tempered by the possibility of complete loss. To mitigate risk, explain all the balanced-producer models this book advocates: some form of distribution in place before beginning production, bank loan for collateral agreements, bond company, production incentives, and collection account.

Advisory Team

Attach résumés for all advisory team members on the film, and explain how they will assist management.

Appendices

These should include, but are not limited to, a budget top sheet, project comparables or greenlight analyses (see Chapter 14), a finance plan, financial projections, a production incentives program outline, talent attachment verification(s), letters of intent for distribution or agreements, and any other research information pertinent to the film.

To write a solid business plan, the producer must first develop a financial plan showing how the investors will receive a return on their investment based on buyers’ estimates, presales, and a smart distribution and marketing plan.

Chapter Postscript

The current entertainment industry boom condition has opened new production, distribution, and funding opportunities. Regardless the project type or total amount of production funding needed, there are multiple players we should consider to provide each project’s crucial capital. Each of the major nine funding participant categories presented in this chapter should be considered in relation to their impact on the overall project’s value, their predictability to engage, and their overall capital cost.

Our engagement of a solid bank entertainment department and/or film fund is vital to pulling all the funding elements together. Understanding how these entertainment departments operate prepares producers to approach them with confidence and wonderful predictability.

Banks and film funds are powerful allies. In addition to production financing and operating capital, they can provide helpful international and domestic data (useful in many areas, including liquidation breakdowns, international distributor valuations, international currency protection, and global industry trends), as well as other information and services. Producers should engage these relationships early and keep them well exercised, assuring they receive all the benefits from their bank and film fund partners.