Chapter 2

The Best Portfolios Are Mixtures of Many Different Asset Classes

The only guarantee in finance is something will go wrong.” This is the Wealth Code Golden Rule and a statement I like to make to every client who joins my firm or comes in for financial education. I tend to repeat it time and time again to reinforce the concept that everything has risk and at some point something will not go as planned.

Take a certificate of deposit at your local bank. FDIC insured, correct? It’s comforting to know you have that guarantee as long as you stay below the protection limits. The sad part, when looking at the assets of the FDIC, or really the lack thereof, is that the FDIC really boils down to being a front for the Federal Reserve which will essentially cover any losses that are FDIC protected in case your bank goes belly up.

In 2005 you probably felt pretty good about the 5 percent the banks were paying on the typical one-year certificate of deposit (CD). You might have looked at your income needs and calculated that at 5 percent you would be doing okay. The problem of course is when that one year term ended and the new rate dropped to 2 percent; now you were in a pickle and the income you counted on took a hit. The previous rate was not guaranteed forever. The drop in the CD rate from 5 percent to 2 percent in 2006 and even lower to 1 percent in 2009 and possibly even lower in the foreseeable future really put a damper on your income and financial well-being.

The other likely outcome of CDs is losing to inflation. There’s only been one decade where CDs have outperformed inflation and that was in the 1980s. Oh, the days of neon and hairspray.

The Real Meaning of Portfolio Diversification

Knowing that the only guarantee in finance is that something will go wrong can be a very powerful tool to have in your financial tool chest. Most people will say they understand it, yet when I look at their portfolios, which are comprised of only one or two asset classes, I would beg to differ.

Take for instance the word diversification. You may have been told that if you have lots of stocks, bonds, and mutual funds, you are diversified. In actuality, your portfolio has a lot of only one asset class-equities.

KEY WEALTH CODE CONCEPT

KEY WEALTH CODE CONCEPTBasketball is a great way to demonstrate the concept of a True Asset Class diversified portfolio.

Does it seem a bit unfair that in the Olympics the USA basketball team has the best players from the NBA all working together? By cherry picking the superstars from each team—knowing their statistics, their abilities, and track records—and crafting them together to make a super team, Team USA fields the most competitive team available.

I was watching a game between team USA and team Argentina in the 2012 Summer Olympics; the final score was 126 to 97. Pretty close compared to other matches that team USA had already played. I noticed during the game that players would substitute in and out. At one point Kobe Bryant, the superstar from the LA Lakers, took a five-minute break. Lo and behold, the score became more and more imbalanced, even though one of the greatest players in the NBA was not on the court. Why? Because LeBron James, Kevin Durant, and others were still playing, and each was a superstar in his own right. I would argue that if Kobe Bryant had broken his leg in this game, LeBron and the rest of the guys still would have won and eventually still would have captured the gold medal.

If Kobe broke his leg during the regular season with the Lakers, it would have a devastating outcome for his team because Kobe is the all-star of his team. His team is not really diversified. But, on the Olympic team, he is one of many all-stars, and it would have been a minor setback for Team USA at best.

The difference in skill between the Lakers and the all-star Olympic team is the same as the difference between a portfolio that got crushed in 2008 and one that survived the storm and actually grew because of true diversification.

True diversification is the philosophy of a Wealth Code portfolio. It requires bringing many different asset classes together for the purpose of consistent wealth building.

Diversification is a word that means different things to different people. It is supposed to make people feel better about their investments and believe that they are doing the right thing. The problem is the viewpoint of the person promoting the idea. As previously discussed, most financial advisors view the world in two colors: stocks and bonds.

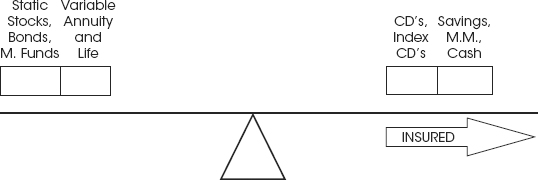

I will proceed to show you one prevalent view of diversification and then my own view. One common viewpoint of the financial world looks like the teeter-totter in Figure 2.1.

Figure 2.1 Typical Financial Portfolio

This example of diversification includes stocks, bonds, mutual funds, ETFs, variable annuities, and CDs, which I jokingly call Certificates of Depreciation or Disappointment. More on that later.

If I were a carpenter and I had a business building one-legged dining room tables, it’s easy to imagine that these tables would fall over due to instability at the slightest push, and my business wouldn’t last very long (Figures 2.2 and 2.3). No one would be silly enough to buy a one-legged table because ultimately it would not do the job intended—provide a stable platform for eating.

Figure 2.2 Undisturbed Table

Figure 2.3 Disturbed Table

Stocks, bonds, mutual funds, ETFs and variable annuities represent essentially one asset class, or one leg of a multi-leg financial table. The other legs are asset classes whose values are generally independent of the stock market. Examples include real estate, oil/gas programs, collateralized notes, equipment leases, rare coins, and fixed annuities. These are called non-market correlated investments.

KEY WEALTH CODE CONCEPTFigure 2.4 Wall Street Single Leg Diversification

Wall Street can be compared to the carpenter building unstable one-legged tables, although this narrow approach is all that most groups offer the majority of investors. There are several reasons why the vast majority of investors invest all their hard-earned money in one-legged tables: It’s all they know, it’s all their advisors know, and these are the only opportunities offered as investments by most large firms holding their money.

In Summary

If you go to the grocery store very hungry and the store only has apples and oranges for sale, guess what? You are going to buy apples and oranges. You don’t have any other choice since you choose to shop at a grocery store with limited options. That is Wall Street’s version of “diversification,” a one-legged table built of stocks, bonds, mutual funds, ETFs and variable annuities. Although variable annuities do represent another leg on the table, the foundation for variable annuities is still the stock market and thus is essentially the same leg.