Chapter 6

True Asset Class Diversification

In the beginning, I introduced a chart of all the investment classes into which you can invest your hard earned money. I talked about why the Olympic basketball team could still win the gold medal even though one of its stars, Los Angeles Laker Kobe Bryant, was not on the court.

The goal of this chapter is to present a new common sense approach to portfolio diversification that is easy to understand but is usually not recommended by the Wall Street crowd.

The General Asset Classes

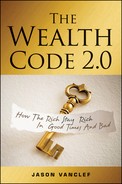

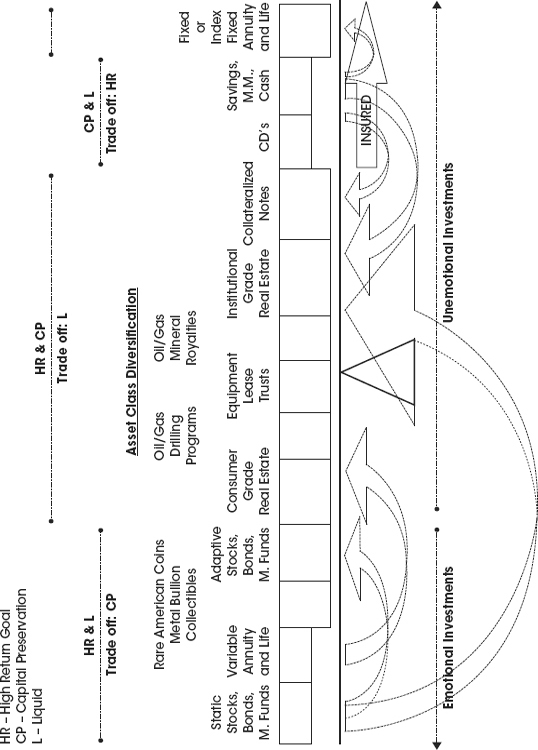

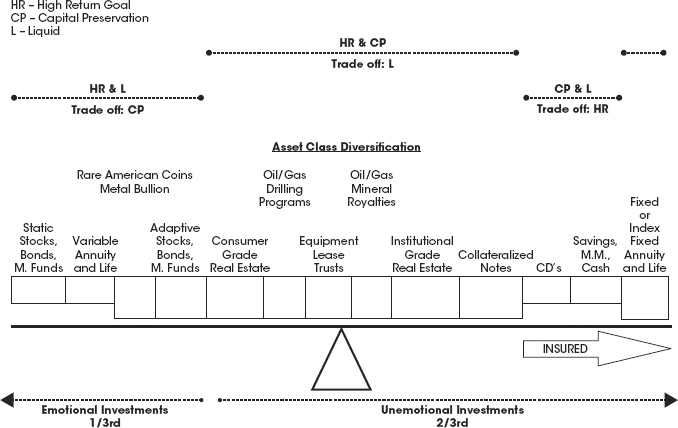

There are simple descriptions for each of the general asset classes (see Figure 6.1). These descriptions are meant to keep you reading by providing a basic understanding of each asset class, and building on your knowledge without bogging you down with nitty gritty details. My goal is to leave you with the big picture and a general comprehension of The Wealth Code. More detailed discussions of each investment class are provided in Appendix B, after the full concept and case examples are presented.

Figure 6.1 All Possible Investments

Static Stocks, Bonds, Mutual Funds

This category includes any stock, bond, mutual fund, or derivative that is held longer than one year. I call this the-hope-and-pray leg on the financial table. The vast majority of investors only know this asset class. This class tends to do well in bull markets. The problem since 2000, however, is that we have been in a bear market, a market that has trended mostly sideways or down. Historical comparisons to previous bear markets suggest we could be in this sideways pattern of ebbs and flows for years, if not for decades to come. A recent example is Japan. They have been in a bear market since 1989 to the present, 2012, with no resolution in sight.

Variable Annuities

These are essentially the same as static accounts, except they offer more bells and whistles such as death benefits and generally have more fees associated with them. Variable annuities can be liquidated quickly for the account balance minus any surrender fees and recent additions to these contracts are the various guaranteed income riders and withdrawal benefits. Guaranteed income riders can provide income streams over an investor’s lifetime or guaranteed minimum withdrawal amounts.

Adaptive Managed Stocks and Bonds

This category includes investment managers who take an active role in changing the portfolio throughout the year to adapt to what is going on in the economy and world. The managers I tend to recommend essentially rebuild the portfolios from scratch every quarter or more often and do not have restrictions in terms of which types of equity classes they can use to build the overall portfolio. For instance, they can use bonds, stocks, or commodities. They have the ability to mix and match any of the three equity classes as they see fit. The main criteria for the advisors I hire is that they cannot use leverage. They work with all cash, which eliminates hedge funds.

Side note: How many times did your investment advisor change your portfolio in the year 2008? How many times did he or she even call you in 2008?

Consumer Grade Real Estate

In general, real estate valued at $5 million or less, including residential homes, apartment buildings, as well as small commercial properties, is considered Consumer Grade Real Estate.

Their prices tend to fluctuate far more than prices for large commercial properties because the buyers are generally less sophisticated than a group purchasing say a $100M property. More emotion is involved, which causes larger increases in good years but more significant drops in bad years.

One of the most popular investments I refer clients to is single family homes in various parts of the middle of the country where home values are generally much more reasonable compared to states such as California, Florida, or New York.

Families who would love to buy but do not have sufficient cash to buy the house outright, are forced to rent. Usually you cannot get a mortgage on these homes because the price of the house is below lending thresholds for mortgage minimums. Thus, people who do not wish to live in an apartment and do not have $60,000 or $70,000 cash in the bank are forced to rent and pay disproportionately high amounts. Typically the rents run about 15 percent of the gross value of the home. In California for instance, it is rare to pay rent above 4 to 6 percent of the value of the home.

Collectibles

What assets are considered collectibles? Anything that can be purchased and potentially demand higher prices in the future due to its rarity and popularity. Collectibles include everything from trading cards, stamps, books, and automobiles to the most popular types which are bottles of wine, fine art, and rare coins.

The most important thing to consider in whether to jump into the collectible investment game is the total net price you think you can command at the time of the sale. You then must calculate your compound annual growth rate based upon how long it takes you to sell. If the figure is substantially more than you expect to make from any of your other investments, it may be worth considering. Why must the return be significantly more than other investments such as real estate or stocks and bonds? The commissions paid are far higher than any other type of investment, typically in the 15 to 20 percent or more on both the buy and sell side. If you are going to pay a minimum of 30 percent round trip, then the collectible needs to appreciate by at least that to just break even.

The danger with valuations is that collectibles are subject, to a large degree, to the individual tastes and preferences of the populace at the time. What makes a Rembrandt or a Picasso worth $20M, $50M, or $100M? Simply the fact that others will pay such prices. Unlike an oil field or chain of taco restaurants, there is no underlying cash stream upon which the value is based. With the latter type of investment, it doesn’t matter if the value of the real estate the restaurants sit on crashes—you can still rely upon the customers who are generating cash for you. There’s also the issue of theft; you can’t exactly throw a building into the back of a pickup truck and make a break for it like you can with a case of valuable wine.

A final danger is the simple fact of destruction. The highest price paid for a Ming porcelain vase to date is $21M in October 2011 at a Sotheby’s auction. Another vase which was estimated to be worth $4M was sold at the knock-down price of $550,000 because the ill-informed owner had turned it into a cheap lamp. Imagine if the $21M vase was dropped on its way to the auction or fitted with GE light bulbs. Whoops.

For the above reasons, you may want to insist upon an additional margin of safety. A rare book set, normally trading at $2,000, may be compelling at $1,800. If you come across it for $900, however, you have left yourself ample room for attractive investment returns even if the item were to suffer a substantial shrinkage in value. Such opportunities are ephemeral, yet they do occur from time to time.

The main strength for collectibles as an investment is their tendencies to protect against inflation. The main weaknesses are of course the illiquidity, difficulty in determining value, and no cash flow to offset price fluctuations.

Rare American Coins and Bullion

Most investors focus on metal bullion but for my discussions, I prefer rare coins, which have a higher multiple against inflation. That is, for instance, if gold goes up 50 percent, rare coins in general might have a 100 percent appreciation.

As for investing in bullion such as gold and silver, there are many different routes you can take. It really depends on your level of trust/paranoia as to who has the gold or silver, will they be able to ship it to you, or do they even have it. Morgan Stanley paid $4.4M to settle a lawsuit in June 2007 which claimed Morgan Stanley charged millions in storage fees on gold held for clients which Morgan Stanley never actually possessed. In 2011 UBS was sued for the same situation but this time for charging storage fees on phantom silver. Needless to say, investors have good reason to question who is purchasing and storing their precious metals.

The easiest route to own precious metals is to use an exchange traded fund (ETF) such as SIVR, SGOL, or others. With these ETFs you never have the right to call them up and ask for the underlying precious metal. You do have the ease of these ETFs trading on a public exchange and the correlating ability to buy and sell quickly.

For those who wish to know with certainty that they COULD get their gold or silver, you can use an allocated custodian such as Bullionvault.com or Goldmoney.com. They store the precious metals for you in allocated accounts, which are individually audited and guaranteed to be in possession. With these types of bullion ownership you could request they send you your precious metals. Of course if all hell is breaking loose, good luck getting the delivery.

This brings up the last version of bullion ownership, having your gold, silver, platinum, or other metals physically in your possession under your pillow. My recommendation to most of my clients is a happy medium among the three types is the best route, but for most intents and purposes, the ETFs work just fine.

Oil/Gas Investments

These include everything from exploration and developmental to royalty programs.

Equipment Leases

Investments in companies that specialize in purchasing and leasing equipment to other companies, generating cash flow, and later selling that equipment after the lease period expires. The biggest problem with this type of equipment leasing investment is predicting what the residual value of the equipment will be when they need to sell it. Other versions of these investments are based on lending money to big companies for equipment they are purchasing, with the equipment being collateral along with the full faith and credit of the company. The lender version of equipment leasing tends to be the prevalent trend with these types of investments as the biggest problem with the purchasing version, predicting the residual value, is taken out of the final equation. They simply supply money for a loan and are paid back the loan principal at the end.

Institutional Grade Real Estate

This is generally real estate valued at $5M or more, either single or portfolio properties, Tenant-in-Common, Delaware Statutory Trusts (DST), or Real Estate Investment Trusts (REITs). There are two types of REITs: stock exchange REITs and non-traded REITs. Non-traded REITs are not available on the stock market and thus fall into the illiquid category. I prefer these types of REITs simply because it allows me to evaluate the real estate and not be concerned with the stock market as a whole. REITs that trade on the stock market are classified as static mutual funds. Though they are real estate, since they trade on the markets, they tend to follow the markets in general and lose much of their non-correlation status. Did the real estate underlying the stock exchange REITs drop close to 85 percent as did the stock market REIT index did during the 2008 market collapse? Most likely not, but the emotionality of the rest of the equity market caused investors to oversell the REIT shares to far below book value prices. An example of how the stock exchange REITs had lost their correlation to the underlying asset they represent due to emotion and not fundamentals.

Collateralized Notes

These, in a nutshell, are pools of debt instruments and loans collateralized by real estate, company assets, or life insurance policies.

A mortgage pool is collateralized by real estate. These are usually first position deeds only, but under certain circumstances blended pools of first position and some subordinated loans are used to enhance overall return.

Business Development Corporations (BDCs) are investments of loans collateralized by a company and its assets. These loans are generally senior secured debt, the highest in the pecking order of a company. If a company goes out of business, as was the case of General Motors in June 2009, the investors in GM senior secured debt were paid back 100 percent, whereas the stock, bond, and preferred stock holders were almost all completely wiped out.

BDC investments basically allow an investor to act like a bank and loan money to a private company. These companies use the proceeds for any number of reasons such as growing the business, buying manufacturing plants, managing cash flow, and so forth. Many of the loans are structured with interest rates that vary with LIBOR and thus can potentially provide an inflation hedge for the BDC investment.

Normally BDCs were only available to investors with deep pockets such as pensions, college endowments, and ultra-wealthy families. But, with the global credit crunch the investment groups who sponsor these BDCs were in need of other investment capital infusions and opened themselves up to the general public by accepting smaller financial commitments.

Finally, life settlement notes are collateralized by large pools of life insurance policies which individuals have sold to an investment group. The return for the investment group as well as investors in the life settlement note is generated as the various life policies within the note pool pay out. That is, when an insured passes away, the life settlement note as the new beneficiary collects the death proceeds.

Certificates of Deposit

Bank instruments that are FDIC insured. This category includes a new investment vehicle called structured CDs. These CDs are tied to a stock market index, some with guarantees of principal via FDIC insurance.

Cash

Bank instruments that are FDIC insured as well as cash held in foreign denominations

Fixed Annuity

Either fixed or index fixed, these are similar in design to variable annuities from an insurance standpoint. They include the same types of annuitization features, income riders, and bonuses, yet they are not directly in the stock market as variable annuities are. Recently, the Securities and Exchange Commission (SEC) ruled that index fixed annuities, since they correspond to various market indexes, should be considered securities and must be sold by licensed individuals. The insurance industry fought back and got the ruling reversed. I feel index fixed annuities should be classified as a security because many insurance-only licensed agents have represented themselves as full-service advisors, discussing the stock market in general yet not having any of the required licenses or true breadth of knowledge the basic security licenses minimally require for them to pass. Oh, the power of lobbyists.

The last category that has not been discussed is life insurance as an investment. Life insurance has many purposes, and many different advisors use it depending on their viewpoint. Some only sell life insurance so that two years down the road they can sell the policy in the settlement market for a cash payout. Others use it for estate planning purposes, and others use it as a long-term retirement vehicle. These are a few of the uses for life insurance and all have their advantages and pitfalls. In Chapter 9, I will discuss my viewpoint of the various ideas I see coming across my desk. Insurance is a very important part of financial planning for some people, but it doesn’t make sense for others. It depends on the client and his or her needs.

This has been just a brief overview of the different asset classes. After being introduced to the whole Wealth Code plan, you can continue your in-depth education of the various asset classes by reading Appendix B.

20,000-Foot Viewpoint on Money

The next sections are included to provide a different viewpoint on money; one that I think is simple to grasp yet powerful to know. Most people will tell you that finance is too complicated. I remember a fellow advisor who once told me that if they could make a children’s book out of Einstein’s theory of relativity, then teaching people about finance should be a walk in the park.

Let’s start with the view at 20,000 feet and begin to look at money in terms of general groupings.

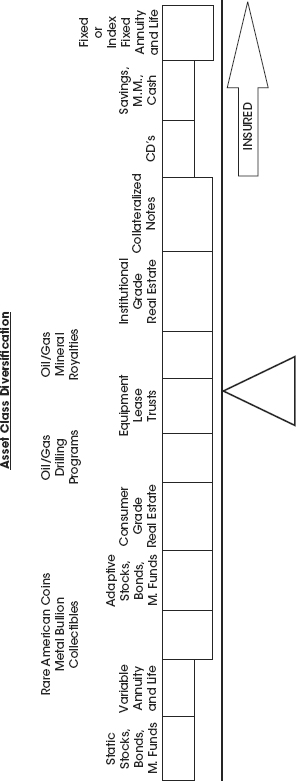

The investments on the left side of the following teeter-totter are generally emotional investments (see Figure 6.2). They trade, and their prices fluctuate based on fear and greed. The general public has the ultimate control. When they get greedy, the prices tend to jump quickly. Of course, when fear sets in, prices tend to drop even faster. Why? Fear is a more powerful emotion than greed.

Figure 6.2 Emotional versus Unemotional Investments

The investments on the right side of the teeter-totter tend to be unemotional investments. A CD is a good example. You buy a CD, assume 4 percent interest for one year, and over the duration of that year you will earn 4 percent. There isn’t a lot to worry about with a CD, unless of course the bank you have your money in goes belly up. Even though you are probably within the FDIC’s limits, no matter what people say, it is still unnerving to be in a bank that becomes insolvent.

KEY WEALTH CODE CONCEPT

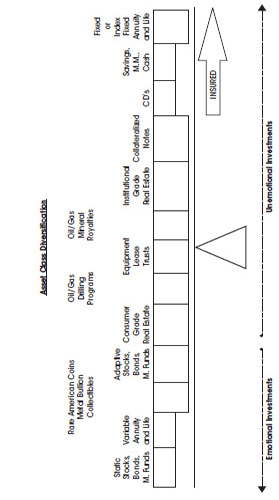

KEY WEALTH CODE CONCEPTComing down to the 10,000-foot level, investments can generally be thought of in three categories:

| High Return (HR) | Goal of 10% or more per year; |

| Liquid (L) | Access to all your money essentially within 30 days; |

| Capital Preservation (CP) | The reasonable assumption your money is protected and the balance won’t fluctuate much if at all. |

There is a fourth description that applies to fixed annuities or index fixed annuities, and that is:

Mid-Return(MR)—Goal of 3 to 5 percent per year.

Fixed annuities are meant for someone who has very specific goals. I don’t necessarily feel they will keep up with inflation in the long run and thus are not part of the three main groupings. Annuities do serve a purpose, however, and will be discussed in Chapter 9.

With capital preservation, as always, assumptions must be made. The key word is reasonable assumptions. For instance, let’s say a particular oil royalty program effectively pays 5 percent when oil is at $50 per barrel. At $80 per barrel, the distributions will effectively be around 8 percent and at $100 oil, the cash flow could be around 12 percent.

No two royalty programs are the same, and there is never a guarantee of distributions or return of principal.

With that being said, after some detailed due diligence on the group that is bringing out the royalty program, let’s say you feel the above percentage payments will generally match those oil prices. The overall assumption that needs to follow is your own. If you personally think oil is going down to $5 then you would never want to get into this particular investment. Anytime the price of oil drops, you’ll call your adviser in a panic and want to sell. On the flip side, if you believe oil is going to average $80 and will at least stay above $50 for the foreseeable future, then you believe your distributions should be 5 percent or more.

You would be going into the investment with eyes open and with assumptions that are reasonable. When the price of oil ebbs and flows, because you firmly believe oil in the long run is going up then you won’t stress a whole lot about the inevitable fluctuations in your corresponding distributions. When people don’t stress or panic, they tend to not make as many irrational buy/sell decisions with their investments and thus see greater returns overall. They tend to avoid the buy high and sell low dilemma we see all too often with investors.

KEY WEALTH CODE CONCEPT KEY WEALTH CODE CONCEPTThere is no such thing as an investment that meets all three goals: High Return, is Liquid, and offers Capital Preservation. If someone tells you about an investment with all three general descriptions, I have a great bridge from Brooklyn to sell you.

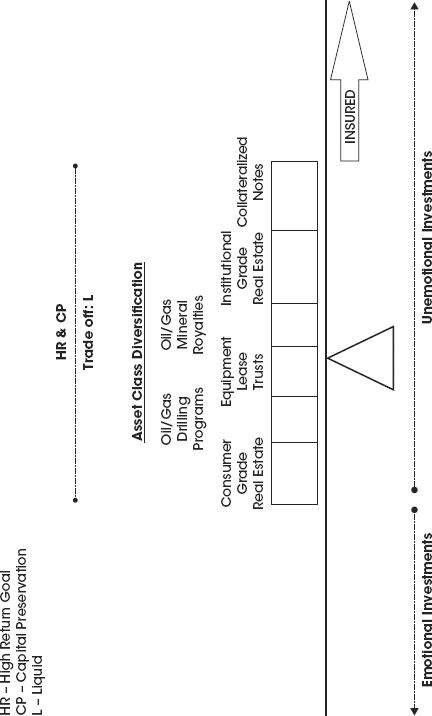

| Goal: | High Return and Liquid (Figure 6.3) |

| Trade off: | Capital Preservation |

Figure 6.3 High Return and Liquid Investments

As a group, investments that fall into the emotional category tend to be described as High Return and Liquid (HR-L).

Stocks and bonds can be thought of as high return and liquid, as can bullion and rare coins. The tradeoff for these investments is you give up the preservation of your capital and take on increased volatility and risk of principal. Between October 2008 and March 2009, it’s interesting to observe that there were more plus/negative 5 percent moves in the stock market during those five months than in the previous fifty years combined. It gives new meaning to volatility and high risk.

You might think, “My bonds are conservative and they preserve my capital.” Do they? In January 2009, 30-year Treasury bonds sustained their biggest losses in U.S. history, around 12 percent. That’s a loss of 12 percent in a single month. Does that sound like an investment that preserves one’s capital?

Bonds perform well in an environment of falling interest rates, such as we have had between 1982 and 2012, but ask yourself a simple question: How much lower can interest rates go? How much longer can the Federal Reserve artificially keep interest rates contained? If history is any guide, these secular or long-term interest rate trends move in roughly 20-year cycles. We are long overdue for the trend to reverse, and, unfortunately when it does, it will not be pretty for fixed interest investments such as bonds and preferred stocks.

Variable annuities are in the HR-L category but with a few caveats. Yes, they can be liquid but for a price, a surrender fee. Variable annuities also can provide account protection in case the stock market tanks. This is generally accomplished via guaranteed withdrawal benefits and death benefits. In terms of guaranteed withdrawal benefits, to activate you generally have to get your initial money back over many years or even your lifetime and of course to get the death benefit, well, you have to die. How’s that for a benefit.

| Goal: | High Return and Capital Preservation (Figure 6.4) |

| Trade off: | Liquidity |

The investments in the middle of the teeter-totter are as follows: consumer grade real estate, oil/gas, institutional grade real estate, equipment leases, and collateralized notes. These generally fall into the High Return and Capital Preservation (HR-CP) category, but the catch to these investments is that you give up liquidity.

Figure 6.4 High Return and Capital Preservation

The key to these investments is time and collateral. There is something backing the money that in general provides an inflation hedge. Look at the wealth of the very rich. The majority of it was built from tangible assets: real estate, oil/gas, timber, or from building a business.

When Enron went out of business, the stockholders lost everything. The bond holders lost everything. Who didn’t lose? The real estate group that owned the Enron headquarters building. They lost a tenant and some rent for a while. But, as soon as they got new tenants, they were back in business.

If Fed Ex were to go out of business, the stock and bond holders would get nothing. The equipment leasing group that owns the plane Fed Ex is using would simply take back the plane, paint it brown, call it UPS, and re-lease it. Then they would sue Fed Ex for the difference in lost lease payments.

The key is that there is more than a promise and a stock certificate backing the investment.

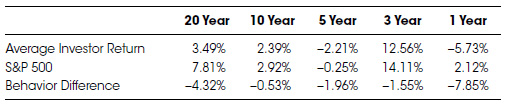

Many will argue that stocks over time will provide the same inflation hedge. I disagree. As reported in a 2012 Study from DALBAR, Inc., a Boston based research firm:

“From January 1, 1992 to December 31, 2011, the average equity mutual fund investor earned 3.49 percent annually: compared to inflation of 2.50 percent and the 7.81 percent that the S&P 500 index earned annually for that 20 year time period.”

DALBAR studied the cash inflows and outflows of the market over these time periods which demonstrate the emotional buying and selling of the typical investor. Buying at the top (Greed) and selling at the bottom (Fear) dramatically affected the long-term performance results of their portfolios.

Table 6.1 shows the various holding periods and the results for the average investor.

Table 6.1 DALBAR 2012 Results

Now that you’ve seen the results, perhaps you’re wondering why investors have done so poorly in achieving returns in line with the most popular benchmark. Well, I believe the answer stems from one main issue: emotion.

Buy high and sell low. Wall Street preaches the opposite, but in practice, few people achieve great results in the markets. Few people have the patience to ride out the rough times. This results in the behavior difference between the S&P 500 index results and the results of the average mutual fund investor.

When the going gets tough, many people panic. They sell at the wrong times, miss rebounds, and buy at the emotional tops before the next correction, further compounding poor performance.

Yet, most people swear up, down and sideways that they are making money hand over fist. Over the years, as I’ve met literally thousands of prospective clients and discussed their investments, they tend to exaggerate dramatically the performance of their portfolio. They, almost subconsciously, do this to justify the years they have been in the markets. Yet, when the numbers are crunched, they generally have made little to nothing in terms of growth. The dollars in the accounts are mostly from good old hard savings.

A gentleman came in and said, “Morgan Stanley did a great job. I started with $300,000 12 years ago. I’ve pulled out over $200,000, and I still have $280,000 today. My advisor says I’ve averaged over 10 percent.” It is easy to say something, and most investors lack the tools to double-check a statement made to them about their performance results.

My favorite side companion is my HP10bII calculator. It’s a very simple financial calculator to use, and I strongly suggest anyone who wants to have a clearer picture of their finances pick one up and learn simple calculations like future value, interest earned, and so forth.

Handing it to the man, I had him punch in the appropriate numbers.

I asked him whether he likes watching his accounts go up and down, and he responded that he hated it. The stress drove him nuts. The realization that he had made basically what a CD would have paid over the same period of time eroded his belief in the stock market.

A doctor came in raving about the great performance of his mutual funds within his 401(k). “I started with $100,000, and today I have $200,000 in my accounts a mere five years later. Can you match that?” he asked. I then pointed out that his statements showed he had contributed another $100,000 over that five-year period, in addition to the $100,000 he started with. He looked sternly at me and said, “I’m too busy working to make any money!”

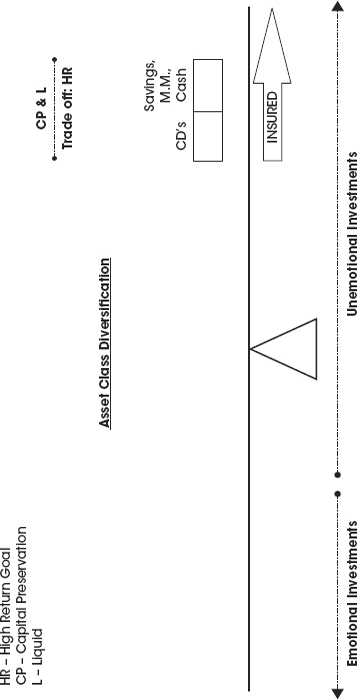

| Goal: | Capital Preservation and Liquid (Figure 6.5) |

| Trade off: | High Return |

Investments in the Capital Preservation-Liquid (CP-L) category are generally the banking and brokerage products: CDs, savings, cash, and money market accounts. These investments are generally for emergencies and short-term financial goals. I’ve described these investments to clients as short-term parking spots. If you park a car on a street and forget about it for a week, what happens? You get a ticket, or worse, your car gets towed.

The penalty you incur for keeping your money in these investment products is that you are losing to inflation. Your purchasing power on the dollars in these investments is going down, thus the joke, “Certificates of Depreciation.” The only decade when CDs have outpaced inflation and taxes was the 1980s, and only by a smidgen.

Figure 6.5 Capital Preservation and Liquid

In 1980, inflation spiked to more than 13.5 percent while a six-month CD paid on average 12.94 percent. The owners of these CDs actually lost 0.56 percent in purchasing power that year because of inflation. To put this in actual dollars, if you had put $10,000 into a CD, your statement at the end of the year would have shown a balance of $11,294. It looks pretty good. The problem is that $11,294 would only buy $9,951 worth of goods in terms of the previous year’s dollars. Worse yet, if you were in the 20 percent tax bracket and 4 percent state tax bracket, now you would be down to $9,677. The inflation diet is having a powerful, negative impact on your savings.

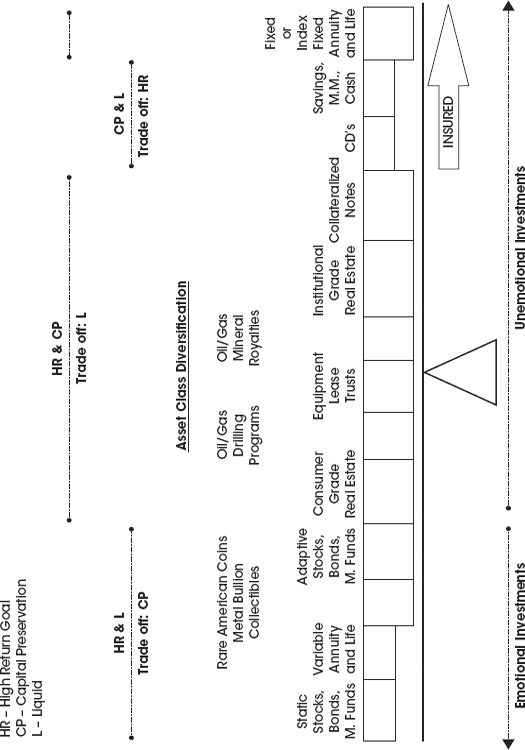

Using the completed teeter-totter (see Figure 6.6), I want to give you a way to look at your money from a new perspective and show you how to build a solid financial table.

Figure 6.6 Complete Financial Teeter-Totter

I feel the best portfolios are mixtures of these investment categories, having money in the HR-L bucket, as well as the HR-CP bucket and CP-L bucket. You never want just one or the other.

Liquidity, though often overstated in terms of necessity, is important for part of your money. High return is vital to keep up with the hidden tax called inflation, and preservation of your capital is the foundation for the other two.

In general, I believe moving people away from static stocks, bonds, and mutual funds, as well as from variable annuities down the teeter-totter is important for achieving the goals of most investors. Some of the money in the CP-L category can be moved a little bit up the teeter-totter because you can be too safe with your money and lose to inflation.

Sometimes, people will move from this category down the teeter-totter into the fixed annuity asset class (see Figure 6.7). Although moving from other categories into the fixed annuity asset class will not keep up with inflation in the long run, it is sometimes what is needed. There are times when it is appropriate to provide a high degree of protection and the tax deferred attributes of a fixed annuity, or the pension-like payouts that are possible under an annuity.

Figure 6.7 Possible Portfolio Improvements

KEY WEALTH CODE CONCEPT

KEY WEALTH CODE CONCEPTFigure 6.8 Wealth Code Rule of Thumb Allocations

Each person is different, and each situation ultimately determines the appropriate category into which their money is placed. Sit down with your advisor and find placements appropriate for you.

A guy comes in for a consultation. I notice he has 100 percent of his money (over a million) in his checking account. After listening to him and his lifestyle choices, I encouraged him to put his money into a higher insured deposit account, up to $50M, and wished him well. Most people would think this was lousy advice. He is losing to inflation; his money is not growing at all.

Yes, your arguments are all correct.

The man was a bit eccentric. The greatest pleasure he had in his life was going to an ATM, withdrawing twenty dollars, then leaving the ATM slip on the counter and watching from a distance as the next passerby who used the ATM would notice the slip and the large amount and then possibly look around to see who was Mr. or Ms. Big Bucks. He would do this five to ten times per day for the pure enjoyment of seeing the reaction on people’s faces as they noticed the large dollar amount.

To each his own . . .

Liquidity Leak Reexamined

At this point, we have seen a new way to look at money. We understand there are many investment asset classes, and we have begun to categorize those classes by common characteristics such as high return, capital preservation, and liquidity. We know that all investments have tradeoffs and the best portfolios are mixtures of the investment asset classes that best match each individual personally. I tend to believe that mixtures of the three general categories provide the best protection in uncertain times.

When I discuss liquidity, it is very important to understand the pitfalls of emotion. In early 2009, a typical headline or business program lead would declare that the next shoe to drop would be commercial real estate. Bad loans and high leverage were the usual reasons. Because of all the publicity, commercial REITs on the stock market were utterly destroyed in the first eight weeks of 2009. Many were down more than 50 percent when the overall market was down 25 percent at that point.

Everyone was panicking because of what they heard about commercial real estate and were selling the stock market REITs as fast as they could. Did any of these people who were selling the REITs spend the time to find out how the actual buildings within the REIT were performing? Before they sold, did they find out who the tenants were, how long the leases were, what percentage of the leases was to expire soon, and how many tenants were leaving? Or did they just sell the shares because that was the only thing they knew to do emotionally?

I argue most did the latter.

Non-traded REITs are another form of investment in large commercial real estate. Many of these groups are in the exact same types of properties that the stock market REITs are in yet, since the shares cannot be sold on a whim, these investors are having far fewer sleepless nights than those holding stock market REITs.

Stock market REIT valuations are essentially controlled by the general public’s fear and greed and generally uninformed opinion, whereas non-traded REITs are controlled by people who manage them as a business and know the status of their tenants, their leases, their occupancy, and so on.

If you want to sell your shares in a non-traded REIT, the originator of the shares will potentially redeem them at the market value of the actual buildings. The value is determined by the people who bought the buildings, know the leases, the tenants, and in fact know as much as possible about the buildings to determine the NAV, or Net Asset Value.

Yes, in non-traded REITs, there is a penalty for withdrawing your funds based on how long you’ve been invested with them. Yes, if necessary, the sponsor, the official name for the group who bought all the buildings, can even stop redemptions if they feel that investor withdrawals are taking out too much of the principal and will hurt the overall portfolio and fellow investors in the portfolio. This would result in investors being unable to sell their investment and withdraw the principal. They would most likely still be receiving their rent checks, just not have the ability to cash out of the investment. A similar situation is seen for any type of real estate if the economic times are not conducive for selling.

Like stock traded REITs, the sponsors can reduce the dividends if they feel it is in the best interest of the portfolio. There are many actions that both types of REITs share in common but there are other significant reasons that non-traded REITs are performing reasonably well now—such as access to cash infusions, low debt, and long-term debt—which distinguish them and will be explained in greater detail later.

Why do I like single-focused professionals controlling my money and not the general public? Carefully chosen professionals tend to be much less emotional in their decisions and make more consistent and informed choices. We hire them for a reason. They understand their investment class very well, and we are going to let them do their job without the interference of the less-informed general public, which tends to overreact to the latest headline.

Lately, the stock market REITs are following the trend of the general stock market. They are no longer acting as a non-correlated investment which is one of the main purposes of owning them: diversification. When the market goes up, they tend to go up. When the market goes down, they go down.

In early 2009, I’m sure that the managers of stock market REITs knew that we were in some of the best times in history to buy large commercial real estate, but they could not act on it due to limited access to credit and falling stock prices. The non-traded REITs, who were actively raising money, did not have that problem. They had access to cash from investor inflows and could gobble up deals not seen in 40 years. Thus, they were building their portfolios, making them even stronger amidst the chaos of 2008 and 2009.

There will be a more detailed discussion of the different REITs in Appendix B, but for this discussion, they serve to help distinguish the effects of liquidity on the performance of a portfolio. In general, I do not want the public determining the outcome of my investments. I prefer to hire groups who can make reasonably informed decisions about investments with my money and not make irrational decisions based on little knowledge of the facts.

This does not mean that there are no investors able to understand investments as well as seasoned professionals. As evidenced by the market turmoil of 2008 and the global credit crunch, many seasoned professionals on Wall Street obviously didn’t anticipate—or care—what the outcomes of their reckless endeavors would be.

In general, however, someone who has spent a lifetime working in one profession, whether it is in real estate or underwater pearl diving, will have knowledge of the subject far superior to the general public. That is the person I want investing my money.

Finally, liquidity needs to be a piece of one’s portfolio, but it comes with a price. It is appropriate to meet short-term goals, emergencies, the what ifs, as well as providing available funds for investment opportunities found in the future. Giving up either capital preservation or high return is the price paid for liquidity. Thus you are forced into either the stock market or CDs.

The next chapter will focus on understanding fundamental concepts of the legs on the financial table, and Chapter 8 will combine all previous chapters to provide a comprehensive understanding of building your own financial blue print.