The golden rules of the rich

The first three chapters have concentrated on some relatively simple changes you can make to ensure that, when you make a financial decision, you give yourself the very best opportunity to enjoy the very best possible outcome. We have looked at changing the way you go about taking ‘advice’, and ensuring you make your borrowing decisions knowing all you need to know about the true cost of the finance. Applying what you have learned will not be easy, as it requires you not only to change the way you think about money but, more importantly, to change your habits – habits that are not financially productive but comfortable all the same. Einstein’s definition of madness was: ‘… doing the same thing over and over again and expecting a different result’. The way you have thought about and managed your money in the past has not made you financially free, and if you continue to manage it that way you are likely to end up as a relatively impoverished senior citizen. If you want a different result in the future, you are going to have to do things differently from now on.

If you stopped reading now, and simply applied what you have learned so far to your own circumstances, you would be a good deal better off when you retire than you would otherwise have been. But to really make a difference to your present and future financial existence, you need to master the Golden Rules.

These ‘rules’ are used by the rich to create wealth, because they understand that the end result of any financial decision has as much to do with how you take an action as it does with what action you might take.

Golden Rule No. 1: Borrow to create financial freedom

One of the real tricks of the rich is that they often make their money with other people’s money. They use debt simply as a tool with which to build their financial future. As you read on, you will see that the introduction of debt has the potential to seriously increase the returns on your investments, even if debt is not needed.

Good debt and bad debt

I want to emphasise that the debt referred to here is not consumer debt. In my experience, people’s view of debt can be polarised: some people will borrow as much as a bank will let them have (no matter what is being purchased with the money) and some, quite simply, will not borrow for anything.

Like most things in life, the issue is not black or white. Debt is neither bad nor good in itself: it is the use you make of the money that dictates whether you add to, or subtract from, your personal asset value. ‘Bad debt’, as far as this book is concerned, is debt that offers no potential for you to get wealthier – we saw some examples in Chapter 3. ‘Good debt’ is debt that offers potential for you to get wealthier; it is raised for investment purposes, where the investment itself offers the potential for returns greater than the real cost of the finance.

I started my working life in 1980 and, since then, the average net asset value of most people in the western world has been rising steadily. For the most part, this is not because we are saving more or investing more prudently – not deliberately, at least – it has been the product of our love affair with property. For example, 79% of the Irish adult population own their own home1 and in the UK 70% of people own their own home. Of course, people have bought these homes with someone else’s money – with the lender’s money. As the underlying value of the property has risen at a pace greater than the cost we pay to the bank, we have been getting wealthier. In most cases, this growth in our wealth has been achieved without any real effort or worry on our part. The house was bought ‘because we liked it’ and the lender’s money was used because ‘that is the norm’.

Let’s look at the wealth that a typical Irish homeowner would have accumulated over those 20 years. I’m using an example from Ireland, but similar figures would also apply to the UK. In 1985, the average family home in Ireland cost €46,542.2 Typically, this would have been purchased with a 90% home mortgage, with the bank providing €41,888 and the borrower putting up the extra €4,654. Assuming an average home loan interest rate over the term of 5%, the cost of this ‘investment’ in cash outlay terms was:

- Deposit: €4,654

- Average monthly loan repayment: €280.10

(Note: I use the Euro currency here but the mathematics is the same whether you use British pounds, American dollars – or any other currency, for that matter.)

The value of this average house had risen to €264,472 by 2005, which means that, had this property been purchased for cash at the outset, the return to the purchaser would have been 9.08% per annum.

However, the fact that the homeowner used the bank’s money has increased his real gains. Since he did not buy for cash but borrowed 90% of the purchase price, there was a cash outlay of €4,654 on Day 1 and then 240 payments of €280.10 per month. Although this gives a total cost of €71,878, the timing of the payments means that the investor has achieved a real return of 10.44% per annum. The ‘good debt’ used by our investor has increased the annual return by 1.36% or, in other words, by 15% in total. By using the lender’s money instead of his own, our clever homeowner has achieved an increased return, not by buying a different property or by investing more money, but by simply paying attention to how the property was bought.

The more recent and well-documented fall in property prices would, of course, affect the return the purchaser has enjoyed, but that in and of itself is of little importance to the point being made. If we assume that the value of the ‘average’ property has fallen say by 30% from the ‘highs’ quoted earlier, it is now worth €185,130 – still more than was paid originally – and so the mathematics will deliver similar benefits. The point being made here is that debt itself, due to the fact that it means the purchaser does not have to come up with cash up-front, is making the investment more profitable for the investor.

This example illustrates that debt (‘good debt’) has a major role to play in your future attempts to create wealth. What surprises me, as I talk to people who have benefited by borrowing for the purchase of their home, is that when I recommend they do the same thing with investment property, they somehow perceive a far greater risk. To be truthful, the financial risk is higher with your home than for a rental property. Not only do rental properties offer similar capital appreciation potential to your home, but they produce income too! When you borrow money for your home, you must repay the loan, in its entirety, from your own income. When you borrow money for an investment property, you are able to repay at least some of it with rent from your tenant (i.e. with someone else’s income).

Returning to our previous example for a moment, let’s assume that the property was bought as an investment, using the same 90% loan/10% cash deposit, and that the investor had averaged a rental income of €125 per month, net of tax. The cost of the property then would be €41,878 (the €4,654 initial outlay and 240 out-of-pocket payments of €155.10 per month – the actual monthly payment less the net rental income the investor received) and the investor’s real annual return would have grown to 13.64% – a 50% increase!

So, as you can see, by changing how you make an investment, and introducing debt as a tool to accelerate the rewards, you can massively increase your return. Of course, there are risks here, additional risks than when simply buying for cash. Indeed, you could say that it is the risk of borrowing that, in our historical example, is delivering the additional gains. The property is the same, the interest rate assumptions are the same, only the risk being taken has changed. At times, investment debt is easily arranged; at others it is all but impossible to raise (the credit crunch being a very good example), but loan availability does not alter the mathematics. No matter whether the economic environment is ‘booming’ or ‘busting’, the maths is still in the investor’s favour.

I am not for a moment suggesting that the economic environment has no affect whatsoever, but careful planning in advance of making an investment decision will ensure that you do benefit. I personally have a number of investment properties, all purchased with investment loans, which recently have seen serious drops in value. However, I can afford the monthly repayments, the tenants are still paying their rents and so the value of my properties today is of little importance; my sole concern is their value as and when I am targeting to reach financial freedom. You see, in advance of accepting the loan offer, I did the calculations. Over any extended period of time, my expectation is that my properties will rise in value (inflation will make sure of that, I suspect), but I am also painfully aware that, over relatively short periods of time, the valuations can fall too. I wanted to be sure that I could sustain my loans in such an event, so I did not simply accept the loan because I could afford the monthly repayments, I stress tested the mathematics in advance.

The people who are losing money right now are those who did no such testing, who bought property on the false assumption that it always goes up in value or that interest rates do not fluctuate. They are the ones who find themselves unable to pay the loans, unable to sell the properties and thus losing huge amounts. They lose money when they are forced out of the investment; anyone who can ride out the economic turmoil and await the inevitable recovery does not lose at all. So, when you raise finance, do not simply make your decisions based on the current economic environment, for although I am not a clairvoyant, I can confidently predict that it will change.

Releasing equity to create new investment assets

Now, armed with the knowledge that investing other people’s money can work for your own gain, you need to look for opportunities in your current circumstances. Many of you reading this book will already own your own home and will have sizeable equity built up in that property. The ‘wealth’ that this equity represents is useless, unless you decide to put it to work on your behalf. Many of us make the mistake of thinking that our homes (for the majority of homeowners, their home is by far their most valuable possession) can contribute to our financial well-being. Unfortunately, this is not true unless:

- You sell your home at some stage in the future and downsize

- You use the equity you have built up to re-mortgage and invest in income-producing assets.

Your home is, of course, an asset, but it is not one that can contribute to your financial freedom. A ‘financial freedom asset’ is one that produces income, while a ‘financial freedom liability’ is one that consumes income. I know which one best describes my home and I imagine it is the same for you – our homes consume our income!

During a recent conversation with my dad, this subject arose as we were discussing his assets. ‘Your house is not really your asset,’ I told him, ‘It is mine.’ At first a little perturbed by my statement, his concern faded as I told him that his house does not contribute to his income – indeed, it consumes his income. ‘However,’ I explained, ‘It will contribute to my income when I inherit it.’ He conceded that I was correct – that, while his home was valuable, it produced nothing tangible for him or my Mum (other than a place to live, of course).

If, as an existing homeowner, you do not use your house to create financial freedom assets, then you will end up like my dad – and, I imagine, so many other dads – asset-rich and cash-poor. Remember, financial freedom and thinking like the rich is about having enough income-producing assets to replace your lifestyle without the necessity to work. Not only does your home not produce income, it consumes income. So, if you want to be financially free, you have to do something about it.

Selling your home in the future and downsizing to a less expensive property can allow you to create income from this asset. But I believe that the luxuries you have worked so hard for in the past should be maintained and so my preference is the equity release system. Let us look at an example.

Let us assume you have a home valued at £500,000, on which there is an outstanding mortgage of £100,000. So, your equity stands at £400,000 and a 10% rise in property values produces a 12.5% rise in your wealth. In other words, when the value of your home rises by 10% (from £500,000 to £550,000), you realise £50,000 (12.5% increase) in additional wealth from a £400,000 investment.

Many lenders are happy to grant investment loans on a 70% loan-to-value basis and are willing to take your home as security for such finance. This means you should be able to raise a total debt of £350,000 on your £500,000 asset, giving you an additional £250,000 (once you have paid off the existing mortgage) to invest.

This £250,000 can now be used as a 30% deposit on a new property, which should allow you to invest around £830,000. At the end of this process, you will have total property assets of £1,330,000 (a £500,000 home and an investment property worth £830,000).

Of course, overall, your property wealth has not altered. You own £1,330,000 in property and owe £930,000 (£350,000 borrowed against your home and £580,000 borrowed for the investment property), thus you still have £400,000 in net assets. Now, however, if the value of your properties (note the plural) rises by 10%, your wealth increases by £130,000 – a 32.5% increase on your investment of £400,000.

‘Ah yes,’ I hear you say, ‘But what about the rent? Will my tenant pay? Will the rent be enough to repay the loan or will I have to add money from my own pocket? What about property values in the future – will they continue to rise? What about tax – will it simply erase all of my profit?’

All these are valid questions and all need to be answered satisfactorily before you take any action. Of course, some of these questions arise out of fear and it’s normal to be scared of the unknown. The questions about the future rise (or fall) in property values and about a reliable tenant are more related to risk than fear. And you do need to consider risk against potential profit.

Don’t let fear paralyse you when it comes to financial matters. You have already seen the potential that this idea has to generate real wealth into the future and do not forget that risk is an essential part of becoming financially free. The rich know this, and you need to learn it. I have said it before, but I’ll repeat it: if you are not prepared to take some risk, stop reading now. You are simply wasting your time and there are far more enjoyable and entertaining books awaiting you in the fiction section of your local bookstore or library.

If you can overcome this fear, if you can force yourself to raise good debt in the pursuit of real investment assets, then the next money-saving idea involves how you repay that debt.

The proper repayment structure creates even more wealth

Most people are uncomfortable with large debt (and yet the same people think nothing of having sizeable outstanding credit card balances on which they are paying interest of 17%+ per annum) and rush to repay their investment loans. This may not be the best use of your money!

In Ireland, there are full tax deductions on the interest payments when the loan is for investment property (some other forms of investment activity also attract such tax relief) and you need to ascertain whether the same type of tax concession is available where you earn your income. Assuming it is, what this means is that, insofar as the rent you receive on your investment property (or properties) is used to repay interest on your loan, that rental income is tax-free! This is a huge tax benefit and sizeably reduces the real cost of repaying interest of this nature. Despite this fact, lenders typically do not provide loans that allow borrowers to take full advantage of this concession.

Capital and interest repayment loans

Most investment loans are issued on a ‘capital and interest’ basis, which means that the bulk of your monthly payment is used to pay the interest on the loan; the balance is used to pay down the capital borrowed. As you repay the loan, less and less of your annual payments are interest – as the outstanding loan reduces, the interest also falls, leaving more in each monthly payment to pay down capital, which in turn reduces the interest and so on. But this means that, as the years roll by, more and more of your rental income is exposed to tax and, in real terms, the debt becomes more expensive to service.

Example 3 below shows the capital and interest repayment method, illustrating the annual costs of repaying a £250,000 loan over a 15-year period on a rental property. The property costs £280,000, inclusive of all costs, so the borrower must put up £30,000 in cash. I have assumed a rental yield (that’s the money you’ll get from your tenants) of 5% per annum (£14,000), which stays constant throughout the loan term (in reality, you would expect some increases in rent over the years) and an interest rate of 4% per annum. I have also assumed a personal tax rate of 50%, which may be higher or lower for you. The question then is: what is the after-tax cost of this property?

Example 3

Capital and interest repayment loan

Tax rates vary dependent upon the extent of your income and the manner in which that income is earned. As with all examples used in this book, you will need to check the benefits you can enjoy based on your personal tax liabilities.

Because the percentage of your monthly repayment that is interest is falling each year, the real cost of a capital and interest repayment loan such as this is rising each year. This is due to the fact that you have fewer and fewer tax deductions and so pay more and more tax.

I am not for a moment trying to put you off investing with capital and interest debt. As long as the property rises in value over the 15 years, you will make substantial profit, even if you use this repayment structure. If we assume a 5% annual increase in the value of the property,3 then if it is worth £280,000 today, it should be worth £582,100 in 15 years’ time. Selling for this price would give you an annual return of 10.17% per annum over the term. While this is a good return, there may be other methods of repayment that allow you to reduce your tax liabilities substantially and, in so doing, to reduce your out-of-pocket costs and thus increase your real profit.

There are two mortgage types worth considering:

- interest-only loans

- retirement-backed loans.

Interest-only loans

Some lenders, depending upon the property being purchased and the overall financial proposition presented by you (the borrower), will lend to property investors on an interest-only basis.

As its name suggests, this type of loan allows you to repay just interest; you do not repay the capital at all. The idea is that, when the property is eventually sold on, you repay the capital.

The advantage of this type of loan is that, in our example at least, it may be possible to purchase an investment property that, on an ongoing basis, costs you nothing in out-of-pocket terms. Example 4, which uses the same underlying assumptions as Example 3, illustrates how this loan works.

Example 4

Interest-only loan

| Loan | |

| Loan amount | £250,000 |

| Term: | 15 years |

| Interest rate: | 4% |

| Income tax: | 50% |

| Loan type: | Interest only |

| Annual payment to lender: | £10,000 |

| Income | |

| Annual rental income: | £14,000 |

| Average annual tax: | (£2,000) |

| Average annual after-tax rental income: | £12,000 |

| Overall cost to investor | |

| Annual interest payment to lender: | £10,000 |

| Average annual after-tax rental income: | £12,000 |

| Average annual after-tax cost: | (£2,000) |

Tax rates vary dependent upon the extent of your income and the manner in which other income is earned. As with all examples used in this book, you will need to check the benefits you can enjoy based on your personal tax liabilities.

As the figures in this example illustrate, and assuming you live in a jurisdiction that allows tax concessions of this nature, it is possible to service the loan and to generate extra income of around £2,000 a year (the difference between rent received and payments to the lender).

Using the same capital growth assumption as used earlier, selling the property in 15 years’ time for £582,100 would mean an average return of 22.3% per annum – 12.13% per annum more than by repaying the loan on the conventional capital and interest basis. In this example, the clever investor increases the return to 220% of what it would have been by changing how the money is borrowed. The interest-only structure has one other advantage – it allows you to buy more property, since the cost of servicing the loan(s) is lower. However, interest-only has one main disadvantage too: you have to sell the property to repay the loan (to get the yield above, you have to unlock your cash and the only way to do this is sell). Becoming financially free is about keeping the wealth you create and, therefore, this method is not advisable if you wish to keep the property long-term, hence the reason for showing you one more option.

Retirement-backed loan

The interest-only method is more lucrative than the conventional capital and interest repayment method, due to the fact that it makes use of the tax law and avoids capital repayments altogether. The savings are made because the borrower can use his rental income to pay all the interest and gets an additional £166.67 per month into the bargain. Savings are also made as the borrower no longer has to pay tax on any capital repayments. Consider it this way: if you pay 50% income tax and have to repay a £250,000 loan out of after-tax income, the cost to you will be £500,000 in pre-tax income. You have to earn the half-million, pay tax on it and then give back the money to the lender. The interest-only method avoids that problem by planning to repay the debt after the property is sold. The retirement-backed method delivers similar rewards, but this time uses a retirement plan to accumulate the capital repayments so that you may keep the property rather than have to sell it to unlock your gains.

You have already seen how greater tax efficiency can hugely improve the returns you receive, thus increasing your wealth and speeding up your journey to financial freedom.

The ordinary capital and interest method both exposes more of your rental income to tax and requires repayment of capital out of after-tax income. In contrast, the retirement-backed structure allows you to accumulate the capital repayment with tax-free money too.

In essence, this repayment structure uses the interest-only facility from the lender, alongside which you have a retirement plan. Most retirement structures around the world offer substantial tax advantages to those who use them; if you do not know your own entitlements may I suggest that you ask your financial adviser as soon as possible. Inside the retirement plan, you accumulate a tax-free lump sum of £250,000 (continuing our previous example) net, which matures in 15 years and is then used to repay the loan. Example 5 illustrates the costs.

Example 5

Retirement-backed loan

| Loan | |

| Loan amount: | £250,000 |

| Term: | 15 years |

| Interest rate: | 4% |

| Income tax: | 50% |

| Loan type: | Retirement-backed |

| Annual payment to lender: | £10,000 |

| Income | |

| Annual rental income: | £14,000 |

| Average annual tax: | (£2,000) |

| Average annual after-tax rental income: | £12,000 |

| Retirement contribution | |

| Annual pre-tax payment: | £15,660* |

| Annual tax savings: | £7,360* |

| Annual after-tax cost: | £8,300* |

| Overall cost to investor | |

| Annual payment to lender: | £10,000 |

| Annual after-tax cost of retirement contribution: | £8,300 |

| Average annual after-tax rental income: | (£12,000) |

| Average annual after-tax cost: | £6,300 |

*I have used the Irish retirement allowances here; you will need to get an idea of the tax allowances in your jurisdiction so as to accurately re-create this example for yourself.

Tax rates vary dependent upon the extent of your income and the manner in which that income is earned. As with all examples used in this book, you will need to check the benefits you can enjoy based on your personal tax liabilities.

When compared to the capital and interest structure, this method is estimated to save you almost £80,000 over the 15 years. This improves your yield (once again assuming the property is valued at £582,100 at the end of the loan term) from 10.17% per annum to 14.3% per annum.

Thus, simply by paying attention to the way you repay your loans, you can vastly increase the profits you make. Obviously, this repayment structure is more costly over the 15 years than the interest-only alternative. However, the big advantage of this method is that, because the retirement plan pays off the loan, the property will continue to create income and capital gains long after the loan is repaid, whereas with the interest-only method, the property has to be sold to get your profit.

What I hope I have shown you in Golden Rule No. 1 is one of the key tricks of the rich. They know that debt is a tool, a device that can bolt a ‘turbo charger’ onto your investment returns. I have also shown you that it is the type of loan, and the tax treatment of interest and capital repayments, that will dictate the true costs of your finance. Lenders are not usually quick to offer these types of loan, as frankly they do not deliver more profit to them. You know now that the banks and other lenders have no interest in your profitability, so it should not surprise you that lenders typically structure loans to reduce their own risk and raise their profits. You need to question them at every turn, ask for the loans that best suit you and your financial ambitions and stop thinking that all loans are the same. You have seen that it is simply not true. Lenders are just purveyors of money, nothing more or less, although many people seem to think of them as demi-gods. In truth, if one bank will lend you money, most banks will lend you money; there is no such thing as loyalty or favours in the banking business (other than the loyalty we show our banks). By insisting that you speak with a number of lenders, you will create competition for your business and this will drive down the costs and/or improve the terms and conditions you are offered.

At times, let me warn you, lenders may try to argue that the retirement-backed structure increases your risk and will attempt to convince you to stick with the ordinary capital and interest structure. They will point out that, for the retirement plan to actually repay your loan, it needs to create a certain investment return. While it is true that the plan does need to earn a specific return (in Example 5 above, the return was assumed to be 6% per annum), it is not true that this increases your risk.

In order to judge accurately the risk being taken, we need to ask how the retirement plan would have to perform for you to pay the same price as the capital and interest structure. In fact, in Example 5, the retirement plan could produce a return as low as 0.49% per annum (less than half of one per cent – about the same as you get from a bank deposit account!), and the overall cost would be the same. If the retirement plan delivers more than 0.49% per annum, you get wealthier.

Remember: when a lender talks of risk, they generally are not referring to your risk but to their own.

Golden Rule No. 2: Invest your money before you pay tax

If I asked you what you think your greatest financial liability is, you might say one of the following:

Is your answer here? If not, I have left spaces for you to fill in your own greatest liability. Do that now before reading on.

Whatever you answered, unless you answered ‘tax’, it’s incorrect. Tax is the greatest liability in your life, in my life and, indeed, in nearly everyone’s life. The rich have recognised this, yet the rest of us have failed to see it.

Think about it for a moment. Every time you earn money you pay tax – and every time you spend money you pay tax. In the UK, income tax is charged at a top rate of 50%, in addition to which a National Insurance contribution is payable. What this means is that, at the top rate, we only get to keep less than half of what we earn. Then, when we spend this money, up to a further 17.5% tax is charged as VAT (due to be increased to 20% from January 2011). In the UK, as throughout the western world, at every turn, you are faced with a tax liability. Tax is the greatest liability in your life – and, therefore, it is the greatest obstacle to you achieving financial freedom. The rich know this and you have to learn it too!

What the rich have realised is that becoming financially free has little to do with how much you earn and everything to do with how much you keep! If you can make investments before you pay tax, then you will be keeping much more, even before you make a single penny on the investment. If you can achieve this, then you will have more money invested, for a longer time, and your wealth will grow considerably faster.

Pensions before tax? And why not?

łt is relatively easy to invest at least some of your income before paying tax, via your pension. The tax allowances to which you are entitled are dependent on your income and you will need to check with your new financial adviser the tax benefits you can enjoy.

However, despite what is an extremely attractive tax break, most people do not use their full allowances in this area. Why are such substantial tax benefits being summarily dismissed by most people? Are you one of them? There are many reasons, which range from complete lack of knowledge on the part of the investing public to the inappropriate manner in which such products are sold. However, the most important explanations are these:

- As various pieces of retirement legislation have been passed into law, they have been hijacked by the financial institutions, which created ‘pension plans’. You may have noticed that I have, until now, avoided the use of the word ‘pension’. This is quite deliberate. A pension is an insurance policy, a vehicle laden with charges (some hidden, others more obvious) and delivered to the public by commission-remunerated salespeople. I believe that the general public has long been dissatisfied with the returns being delivered by the insurance companies and this has led, unfortunately, to throwing out the baby with the bath water. By refusing to pay the often exorbitant charges levied by insurers, you also close the door to the huge tax concessions. While the rich certainly do not purchase off-the-shelf pensions, they do use the tax concessions that retirement legislation provides.

- Many of us, whether experienced investors or not, are most comfortable when we can make our investment choices ourselves. Off-the-shelf pensions available offer little flexibility, with investment options typically limited to a range of ‘own funds’ offered by the insurer. Funds labelled ‘Managed’ or ‘Equity’ or ‘Gilt’ offer little in the way of choice and, to be truthful, most people I meet have no real idea of what they actually invest in. This lack of flexibility, coupled with the investor’s lack of knowledge, has stopped many people from enjoying the tax concessions available.

If you are one of the many people who have never invested in a pension, or have dabbled but not used your entire allowances, then do not concern yourself too much. I happen to agree with your decision; the lack of transparency in such products (where charges are concerned), along with the ‘one size fits all’ attitude to investment that these plans take, makes them poor value for money. However, I do think that you should be taking advantage of the tax breaks and, like the rich, it is most likely that you can do so without having to buy a standard pension.

Legitimate retirement allowances are certainly the easiest tax break you will ever access and there is no question as to their effectiveness, or their authenticity. But retirement allowances are dictated directly by legislation and, as long as you do not invest beyond your personal allowance, you are guaranteed the tax break. Depending on which type of retirement fund you use, the allowance you will receive will depend on three things: your employment status, your age, and, on occasion, your gender (as women tend to live longer than men, their retirement allowances may be higher).

If you are self-employed or in non-pensionable employment, then the private pension fund accessible to you is sometimes known as a self-directed personal pension (SDPP). The maximum allowance to which you will be entitled, i.e. the amount of pre-tax income you can invest, is dictated by legislation and by the use you have made of the allowances in the past. Tax relief is limited to contributions up to the higher of the following:

- 100% of your UK taxable earnings

- £3,600.

So, taking the lower figure as an example, you should be able to pay at least £3,600 per annum from personal income into a retirement plan.

Of course, such an investment does not cost £3,600 out of your take-home pay as you save considerable tax. By way of an example, let us look at how much it will cost out-of-pocket.

| Gross annual contribution | £3,600 |

| Tax savings @ 50% | £1,800 |

| Net annual cost | £1,800 |

You can immediately see the second Golden Rule at work here: for a cost of £1,800 this investor has an investment fund of £3,600, which can now be placed in a range of investment assets including property, stocks and shares, deposit funds, land, etc.

If you are a proprietary director or a senior executive working for someone else, then the private pension fund available to you is known as a self-administered pension fund (SAPF). The allowances available to an individual who falls into this category can be substantially greater than the SDPP (and it is here that the allowances for women can be higher than for men), a reason for many self-employed people to switch to limited company trading.

No matter which private retirement fund is available, such vehicles will not levy a multitude of charges on you. Instead, you pay a fee to establish the vehicle and an annual fee to administer and monitor the scheme. The annual fee should also cover auditing and compliance services for the year. Do not – and this is one of the attitude changes I referred to in earlier chapters – let a fee scare you off. Remember that, for every £1,000 you pay in a fee, a contribution of £2,000 to the scheme will save you £1,000 tax (assuming the 50% rate; other tax rates will increase or decrease this figure) in the next year. After the break-even point, every additional penny you save in tax is taking you that bit closer to your financial freedom goal.

There is one more benefit to using your retirement allowances in the manner I have suggested. Inside the retirement fund, your investments will be exempt from income tax (a retirement fund pays no income tax on its investments, whether income comes from dividends on shares, rental income on properties or deposit interest from financial institutions) and capital gains tax. Yes, you read that correctly – a retirement fund is exempt from income tax on any income your investments create and, if you make a capital gain, this too will be tax-free.

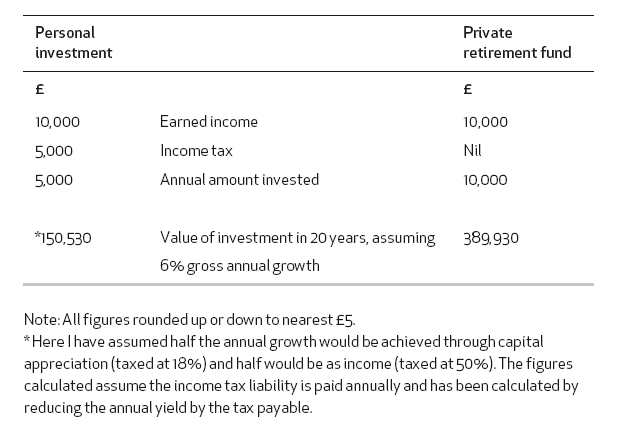

The rich use all available tax concessions; they keep more of their money for themselves and thus they can save more towards the future. The private retirement fund not only allows you to keep more of your regular income, but it also allows you to keep more of your investment income and investment gains too. Some tax will be payable later on and, while proper planning can reduce future tax liabilities too, in Table 2 opposite I have assumed the maximum amount of tax would be levied at the end.

Table 2 illustrates the power that tax-free investment has to make you wealthier. It is based on an annual income of £10,000, which is then invested. In the left-hand column, I assume that you pay tax on this income at 50% and invest the balance, while in the right-hand column, I assume you pay the full £10,000 directly into a private retirement fund. Obviously, if you invest in your own name you will pay tax on your annual profits, whereas the retirement fund pays no tax, so I have included tax within the personally-held investment. Tax will be levied once income is taken from the retirement fund, however, what we are interested in is the amount of cash that is being accumulated within the retirement fund when compared to the normal investment route. Note that you may receive 25% of your withdrawal tax-free, so tax is levied on 75% of the fund only.

Finally, I have assumed a 20-year investment term and a 6% per annum gross yield (yield before tax) in both situations.

Table 2 Personal investment vs private retirement fund

So you can see that making investments the way the rich do can have a huge effect on your future wealth. Remember, both the left-hand and right-hand columns represent the same money, earned in the same way, invested in the same assets, producing the same annual rate of return. Simply by copying how the rich invest you have accumulated for yourself 159%+ more money!

Remember, once you reach financial freedom, you will not need a pension in the same way as others need a pension – it will simply be one of your assets that provides the complete financial security that financial freedom brings.

Act now!

Now that you know the Golden Rules, resolve today to do something with your new-found knowledge. You must take action – immediate action, in my view – for the longer you delay, the less likely you are to do something positive.

One thing the rich know is that they must always act sooner rather than later. This is another change you have to make if you truly wish to achieve financial freedom and live like the rich. Earlier, I suggested that you would have to change the way you think about money; you will have to change the way you act about money too. The simple truth is that most of us do not act at all; rather we react to financial issues and usually only when they have started to cause us some problem. Now it is time for positive action and, while I have no doubt that some readers will have the ability to act for themselves, most of you should seek out a truly impartial financial adviser. Remember the lessons of an earlier chapter, look for someone who will charge you a fee and who will listen to your wishes. ‘Free advice’ is an oxymoron (it cannot exist); if it is free then it is not advice, it is product-selling!

Armed with the relatively basic knowledge that these first four chapters have given you, you now know more about money than most of the financial advisers I have ever met. Stick to your own agenda and find an adviser who will charge you a fee. (Remember to get references, preferably from existing clients – just because someone charges a fee does not mean they are good at the job.) That way, you know he works for you and has your best interests at heart. The rich will only deal with advisers that avoid the conflicts of interest caused by advisers’ need to sell something to make money, and so should you.

1 Source: Central Statistics Office, Census 2002.

2 Source: Irish Department of the Environment, Heritage & Local Government, 2005.

3 Although we saw earlier that Irish residential property had risen by 9.08% per annum from 1985 to 2005, it always pays to be conservative with your future estimates.