Money Management Before Trading

It’s never too early to start.

Success in Trading Depends on Money Management

So far, we have been laying the foundations for share trading. So, this is the final section to get you ready for trading. Please bear with me as this section is extremely important and must be taken seriously before you become a trader. Understand that savings and a savings plan is a long term commitment and a necessary one for you to prosper as a trader. The main difficulty with long-term saving is that inflation is an unknown variable.

If we could be sure that prices are going to rise at an average rate of 4 percent a year over the next 20 years, this difficulty would not exist: you could, for instance, put all your money into well-chosen bonds or index stocks, giving a profit of 8 percent a year. All you need is 7.5 percent annual return to double your money, but with an inflation rate of 4 percent it would effectively take you 20 years to double your funds.

In effect, the actual buying power of your money would only increase by 50 percent in just over 10 years, and would more than double in 20 years.

And if inflation averaged 10 percent a year, you would be able to buy only about 66 percent as much with your money after 20 years as you could have done when you saved it up, which isn’t a very appealing prospect.

For long-term saving, you need something that will stand a chance of keeping up and being higher than inflation, whatever heights it may reach—and this basically means something which is directly linked to the value of money.

There are three kinds of investment which, in the past, have met this need: ordinary shares of companies, which you buy on the stock exchange; houses and land; and valuable things such as certain paintings, antiques, and so on.

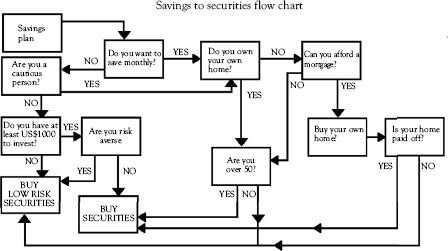

These volumes concentrate on the acquisition of shares. What this means is that, if you are saving for the long term, you have to spread your risk as widely as possible, so that, if one of the shares you have chosen does very badly, you don’t lose everything.

There are two stock exchange maxims, which have more than a grain of truth in it, which says: The small investor is always wrong and how did I make a small fortune in the market? I started out with a large fortune.

When you are saving for the long term, you have to choose something which stands a chance of coping with inflation—however bad inflation may become. This basically means that you have to be prepared to take risks, since the only things which are flexible enough to cope with inflation have no fixed value themselves: you have to rely on their value going up to give you the profit you need.

The stock exchange is one answer though buying stocks. If you want to put money on the stock exchange, you have three main choices: higher risk securities (shares and derivatives) and lower risk unit trusts, which can also fluctuate, but which are more stable.

If you want to invest direct in equities, you should aim to spend at least $200 to $300 on the shares of each company you choose a month: any less than that, and dealing charges start to become unduly expensive. If you also want to stand a reasonable chance of keeping your money safe, you will have to have a spread of shares; at least 10, carefully selected and spread among a number of different industries.

Buying shares in unit trusts will not need so much money, as your risk is already spread among a range of shares. Buying units in a unit trust needs less money, since the dealing charges are built into the buying and selling price of each unit and so are not prohibitively expensive on small amounts. Unit trusts are also safer, and have the advantage that you can save up regularly. But, on average, profits are not as good as those of securities.

Successful Investors Start with Savings

What do you do if you’re a trader who has not been able to trade for the entire month; whatever the reason may be? Novice traders tend to believe that once they understand some technical triggers and have opened up an online trading account, their careers start. Few novice traders are really prepared for difficult time. Some have told me that they can simply sell shares to pay expenses. Doing that means that you are reducing your trading capital. It also means that the next month you will have less capital to achieve the same goals. So, you will have to employ a higher risk strategy as you have less cash. Imagine that the following month is December and now you have fewer days to trade, face liquidity problems as professional; dealers take the Christmas break. Panic sets in and you take greater and riskier chances.

The end of that trader’s career is transparent.

There is only one way to attain financial security, as a trader and as a self-employed worker. Take heed before you face the reality that no work means no pay. To succeed therefore means that you have both a savings and a trading account. Ensure that you have your at least 6 months’ “salary” saved before you begin to trade.

Repeatedly, I have met the ultrawealthy traders, but also people who live modestly. They have funds that they trade and savings to meet their monthly expenses. They also go on holiday and their modest living gives them comfort that they are doing what they love for a living, which they do without panic.

You need to assess and develop a strategy for the following:

• Develop a financial plan with budgets.

• Establish a payment plan for high-interest debt.

• Set out timeframes for saving and investing.

Develop a Financial Plan with Budgets

There are literally thousands of books on budgets and how to easily accomplish financial goals. It is sufficient to state that you need to make a comprehensive list of expenses. Leave nothing out and then add a buffer for miscellaneous and unforeseen expenses.

Include in your list, among other, cost of mortgage, vehicle leasing, education, medical, and other insurance and holidays.

Once your list has been completed, prioritize the items and then set a timeframe to fulfill each goal. You need to do this as the first step in your trading will be to meet these goals with the appropriate trading risk profile.

Savings and High Interest Debt

There is an economic principle that states that you shouldn’t pay off your high interest bearing debt before you commence to trade. The reason is that, under an inflationary environment, the debt is effectively reduced as cost of money becomes less. Under such conditions you would have to calculate the real effect of your debt on your savings or trading or both.

As follows:

• Debt = 6 percent interest

• Savings = 4 percent interest

• Inflation = 2 percent

If you had $1,000 in debt and the same amount in savings, should you use the savings to pay off the debt? Remember that savings form part of your long-term trading plan. So, if inflation diminishes real debt, but also real returns, then look at the following using simplistic interest over 12 months.

• Debt = $1,000 × 0.06 = Total debt of $1,060;

• Savings = $1,000 × 0.04 = Total savings of $1,040;

• Interest on debt is higher than savings, therefore—while inflation affects both—it has more of an impact on the higher debt.

The issue isn’t an economic one, but one of practical efficiencies. For instance, you don’t really know whether inflation will rise or not. So, you must calculate whether your potential return in the market will enable you to meet these expenses or not.

Let’s end the chapter by saying that trading is obviously higher risk than a bank savings account. While you can lose your capital, you can certainly gain a greater percentage return with trading than the safe haven of banking your funds.

Chapter 9 is an overview of how to start your investment and trading career.