Chapter 6

Management Discussion and Analysis

(i) Smaller Reporting Companies

(ii) MD&A Disclosures on Fair Value and Liquidity and Capital Resources

(b) Critical Accounting Estimates

(d) Effect of Newly Issued But Not Yet Effective Accounting Standards

6.3 Related Accounting Literature

(c) Use of Estimates in the Preparation of Financial Statements

(d) Certain Significant Estimates

(e) Current Vulnerability Due to Certain Concentrations

6.4 External Auditor Involvement

6.1 Overview

(a) Introduction

Management must include, as part of Form 10-K filings, a section entitled “Management Discussion and Analysis of Financial Condition and the Results of Operations” (commonly referred to as Management Discussion & Analysis [MD&A]). The governing regulation is Section 229.303 of Regulation S-K and is referred to as Item 303. As stated in Item 303, the objective of the MD&A is “to provide to investors and other users information relevant to an assessment of the financial condition and results of operations of the registrant as determined by evaluating the amounts and certainty of cash flows from operations and from outside sources.” The MD&A should permit shareholders and users to see and understand the specific decisions made through the eyes of management. The Securities and Exchange Commission (SEC) has stated:

The Commission has long recognized the need for a narrative explanation of the financial statements, because a numerical presentation and brief accompanying footnotes alone may be insufficient for an investor to judge the quality of earnings and the likelihood that past performance is indicative of future performance. MD&A is intended to give the investor an opportunity to look at the company through the eyes of management by providing both a short- and long-term analysis of the business of the company. The Item asks management to discuss the dynamics of the business and to analyze the financials. [Securities Act Release No. 6711, April 24, 1987, 52 Federal Register (FR) 13715]

The SEC has especially emphasized the need for prospective disclosures:

The MD&A requirements are intended to provide, in one section of a filing, material historical and prospective textual disclosure enabling investors and other users to assess the financial condition and results of operations of the registrant, with particular emphasis on the registrant's prospects for the future. [Release Nos. 33-6835; 34-26831, May 18, 1989]

This is notably similar to the statement given by the Financial Accounting Standards Board (FASB) on the purpose of financial reporting in general:

Financial reporting should include explanations and interpretations to help users understand financial information provided. For example, the usefulness of financial information as an aid to investors, creditors, and others in forming expectations about a business enterprise may be enhanced by management's explanations of the information. Management knows more about the enterprise and its affairs than investors, creditors, or other “outsiders” and can often increase the usefulness of financial information by identifying certain transactions, other events, and circumstances that affect the enterprise and explaining their financial impact on it. [par. 54, FASB Concepts Statement, Objectives of Financial Reporting by Business Enterprises]

Additionally, the Financial Analysts Federation has endorsed the MD&A:

We have supported the efforts of the SEC to make these disclosures meaningful. The MD&A, when properly prepared, can be extremely valuable in helping users understand the results of operations and, by extension, the factors which will affect future operating results. [Letter dated September 30, 1986, from Anthony Cope, Chairman, SEC Liaison Committee of the Financial Analysts Federation, to Jonathan Katz, Secretary, SEC]

In sum, both the SEC and the investment community strongly support the MD&A requirement. Furthermore, in light of SEC enforcement actions, particular care should be exercised in drafting the MD&A.

(b) Brief History

The requirement for a management discussion section originated in 1968 when the SEC adopted the Guides for Preparation and Filing of Registration Statements (Securities Act Release No. 33-4936). These guides required a summary of earnings, which was to address unusual conditions affecting net income. In 1974, this summary was mandated for filings under the Securities Exchange Act and was broadened to include a discussion of underlying trends in profitability. Although specific topics to be discussed were not specified, recommendations were made. The SEC wanted to keep the requirements flexible, allowing management to discuss those items peculiar to its business, in order to prevent a “boilerplate” presentation. However, corporations generally fulfilled the requirement by providing percentage changes of financial statement line items (which investors could calculate themselves) without providing substantive reasons for the changes.

In 1977, the SEC's Advisory Committee on Corporate Disclosure reiterated that corporate management, in fact, be given broad latitude in their discussions but that better direction be provided. To elicit more meaningful prospective analyses, the SEC granted protection under safe harbor rules in 1979.1 Then in 1980, the MD&A requirement was substantially expanded and rewritten. Although “soft” information was to be provided, the overriding belief was that the potential relevance surpassed problems of verifiability. The 1980 requirements changed the MD&A from a summary of earnings only to an analysis of liquidity, capital resources, and results of operations.

In May 1989, the SEC issued an Interpretive Release, Management's Discussion and Analysis of Financial Condition and Results of Operations; Certain Investment Company Disclosures, which provided guidance, particularly on prospective or “forward-looking” disclosures.2 This is significant in that the examples included in the release can serve as standards against which the SEC can measure the adequacy of registrant disclosures. The entire 1989 release is known as FR 36. (See www.sec.gov/rules/interp/33-6835.htm.)

With respect to currently known trends, the 1989 release points out that management must assess whether the trend, demand, commitment, event, or uncertainty is likely to happen. If a matter is not likely, no disclosure is required. However, management must be able to make a determination that a matter is not likely. If management cannot make such a determination, it must evaluate the consequences based on the assumption that the event will happen and then disclose the effects if the consequences are material. The release distinguishes currently known trends from anticipated trends.

Examples of known trends affecting future operations include reductions in the registrant's product prices, erosion in market share, changes in insurance coverage, likely nonrenewal of a material contract, discontinuation of a growth trend, and implementation of recently enacted legislation. With respect to future liquidity, the release indicates that the SEC expects registrants to discuss both short- and long-term liquidity, and to use the framework of the statement of cash flows as a basis of discussion (i.e., future operating, investing, and financing cash flows).3

To underscore the SEC's insistence on enhanced prospective disclosures, the SEC issued this warning in footnote 28 in its May 1989 Interpretative Release:

Where a material change in a registrant's financial condition (such as a material increase or decrease in cash flows) or results of operations appears in a reporting period and the likelihood of such change was not discussed in prior reports, the Commission staff as part of its review of the current filing will inquire as to the circumstances existing at the time of the earlier filings to determine whether the registrant failed to discuss a known trend, demand, commitment, event or uncertainty as required by Item 303. [Release Nos. 33-6835; 34-26831, May 18, 1989]

Prior to the passage of the Sarbanes-Oxley Act of 2002 (SOX), the SEC issued additional guidance for MD&A. After the passage of SOX, two of the three releases were formally codified and incorporated into Regulation S-K through SEC rule making.

In 2001, the SEC issued Cautionary Advice Regarding the Use of “Pro Forma” Financial Information in Earnings Releases (also referred to as FR 59). In response to Section 401(b) of SOX and to codify guidance in FR 59, the SEC amended Regulation S-K with the issuance of the final rule, Conditions for Use of Non-GAAP Financial Measures, on January 22, 2003 (also referred to as FR 65).

The SEC also issued, in 2001, Cautionary Advice Regarding Disclosure About Critical Accounting Policies (referred to as FR 60). On May 10, 2002, the SEC proposed a rule entitled Disclosure in Management's Discussion and Analysis about the Application of Critical Accounting Policies. This proposal remains outstanding.

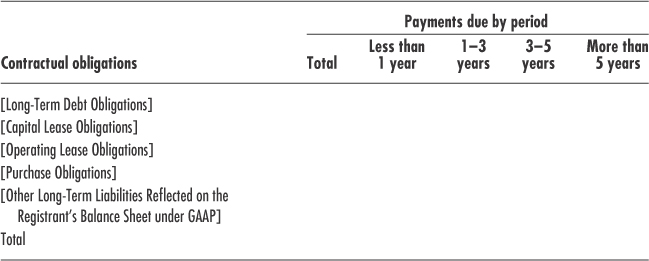

During 2001, the SEC also issued a statement entitled Commission Statement About Management's Discussion and Analysis of Financial Condition and Results of Operations (referred to as FR 61). This release primarily addressed liquidity and capital resources disclosures. In response to section 401(a) of SOX and to codify FR 61, the SEC amended Regulation S-K with the issuance of a final rule entitled Disclosure in Management's Discussion and Analysis About Off-Balance-Sheet Arrangements and Aggregate Contractual Obligations (also referred to as FR 67).

After the passage of SOX , the SEC continued issue MD&A guidance. During 2003, the SEC issued interpretative guidance entitled Commission Guidance Regarding Management's Discussion and Analysis of Financial Condition and Results of Operations (referred to as FR 72).

The SEC has continued to focus on MD&A disclosures on liquidity and capital resources. During 2010, the SEC issued an interpretative guidance entitled Commission Guidance on Presentation of Liquidity and Capital Resources Disclosures in Management's Discussion and Analysis (referred to as FR 83).

Exhibit 6.1 provides the full text of Section 229.303 (Item 303), “Management's Discussion and Analysis of Financial Condition and Results of Operations,” of Regulation S-K. Exhibit 6.2 lists, in chronological order, the major SEC releases related to the MD&A.

Exhibit 6.2 MD&A-Related SEC Releases

- Securities Act Release No. 4936 (December 9, 1968) (33 FR 18617), Guides for Preparation and Filing of Registration Statements under the Securities Act of 1933. This was the first requirement for a narrative discussion of the results of operations, which was incorporated in registration statements.

- Securities Act Release No. 5520 (September 3, 1974) (39 FR 31894), Commission's Guidelines for Registration and Reporting. This required a narrative discussion about the results of operations to accompany all periodic financial statements.

- Securities Act Release No. 5992 (November 7, 1978) (43 FR 53251), Guide for Reports or Memoranda Concerning Registrants. This release set forth a “safe harbor” for forward-looking information. As a result, the government or private plaintiffs are prevented from alleging fraud in suits where forward-looking projections fail to materialize, as long as they have a reasonable basis and are disclosed in good faith.

- Securities Act Release No. 6231 (September 2, 1980) (45 FR 63630), Amendments to Annual Report Form, Related Forms, Rules, Regulations, and Guides; Integration of Securities' Acts Disclosure System. This release expanded the required discussion to include liquidity, capital resources, as well as the results of operations. It also required discussion of certain prospective information. It remains in force.

- Securities Act Release No. 6349 (September 28, 1981), 23 SEC Docket 962 [not published in the Federal Register]. This release reported deficiencies in complying with the 1980 requirement and gave examples of disclosures to assist companies in drafting the MD&A.

- Securities Act Release No. 6711 (April 24, 1987) (52 FR 13715), (April 17, 1987), Concept Release on Management's Discussion and Analysis of Financial Condition and Results of Operations. This release was referred to as the Concept Release. Its main purpose was to seek comment from various parties to proposed changes in the MD&A requirements made by the accounting profession.

- Securities Act Release Nos. 33-6835; 34-26831; IC-16961; FR-36; (May 18, 1989) (54 FR 22427), Management's Discussion and Analysis of Financial Condition and Results of Operations; Certain Investment Company Disclosures; Certain Investment Company Disclosures. This release gave more examples of MD&A disclosures, particularly those pertaining to prospective information.

- Securities Act Release Nos. 33-8039, 34-45124, FR-59 (December 4, 2001) (Federal Register: December 10, 2001, Volume 66, Number 237), Cautionary Advice Regarding the Use of “Pro Forma” Financial Information in Earnings Releases. This release provides cautionary advice regarding the use of “pro forma” financial information in earnings releases.

- Securities Act Releases Nos. 33-8040, 34-45149, FR-60 (December 12, 2001) (Federal Register, December 17, 2001, Volume 66, Number 242), Cautionary Advice Regarding Disclosure About Critical Accounting Policies. This release provides cautionary advice regarding disclosure about critical accounting policies.

- Securities Act Release Nos. 33-8056; 34-45321; FR-61 (January 22, 2002) (Federal Register, January 25, 2002, Volume 67, Number 17), Commission Statement About Management's Discussion and Analysis of Financial Condition and Results of Operations. This release sets forth certain views of the Securities and Exchange Commission regarding disclosure in MD&A concerning liquidity and capital resources including off-balance-sheet arrangements; certain trading activities that include non-exchange-traded contracts accounted for at fair value; and effects of transactions with related and certain other parties.

- Securities Act Release Nos. 33-8098; 34-45907 (Federal Register, May 20, 2002, Volume 67, Number 97). Proposed rule, Disclosure in Management's Discussion and Analysis About the Application of Critical Accounting Policies. The SEC proposed disclosure requirements that would enhance investors' understanding of the application of companies' critical accounting policies. The proposals would encompass disclosure in two areas: accounting estimates a company makes in applying its accounting policies and the initial adoption by a company of an accounting policy that has a material impact on its financial presentation. This proposal remains outstanding at date of this publication.

- Release No. 33-8176; 34-47226; FR-65 (Federal Register, January 30, 2003, Volume 68, Number 20), Conditions for Use of Non-GAAP Financial Measures. This final rule addresses public companies' disclosure or release of certain financial information that is calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). The SEC also adopted a new disclosure regulation, Regulation G, which requires public companies that disclose or release such non-GAAP financial measures to include, in that disclosure or release, a presentation of the most directly comparable GAAP financial measure and a reconciliation of the disclosed non-GAAP financial measure to the most directly comparable GAAP financial measure. The SEC also adopted amendments to Item 10 of Regulation S-K to provide additional guidance to those registrants that include non-GAAP financial measures in SEC filings.

- Securities Act Release Nos. 33-8182, 34-47264, FR-67 (Federal Register, February 5, 2003, Volume 68, Number 24), Disclosure in Management's Discussion and Analysis about Off-Balance-Sheet Arrangements and Aggregate Contractual Obligations. This final rule requires a registrant to provide an explanation of its off-balance-sheet arrangements in a separately captioned subsection of the MD&A section of a registrant's disclosure documents. The amendments also require registrants (other than small business issuers) to provide an overview of certain known contractual obligations in a tabular format. Securities Act Release Nos. 33-8350, 34-48960, FR-72 (Federal Register, December 29, 2003, Volume 68, Number 248), Commission Guidance Regarding Management's Discussion and Analysis of Financial Condition and Results of Operations. This interpretation is intended to elicit more meaningful disclosure in MD&A in a number of areas, including the overall presentation and focus of MD&A, with general emphasis on the discussion and analysis of known trends, demands, commitments, events, and uncertainties, and specific guidance on disclosures about liquidity, capital resources, and critical accounting estimates.

- Securities Act Release Nos. 33-8876, 34-56994, 39-2451 (Federal Register: January 4, 2008, Volume 73, Number 3), Smaller Reporting Company Regulatory Relief and Simplification. This final rule amends the disclosure and reporting requirements under the Securities Act of 1933 and the Securities Exchange Act of 1934 to expand the number of companies that qualify for its scaled disclosure requirements for smaller reporting companies. Companies that have less than $75 million in public equity float will qualify for the scaled disclosure requirements under the amendments. Companies without a calculable public equity float will qualify if their revenues were below $50 million in the previous year. To streamline and simplify regulation, the amendments move the scaled disclosure requirements from Regulation S-B into Regulation S-K.

- Securities Act Release Nos. 33-9144, 34-62934, FR-83 (Federal Register, September 28, 2010, Volume 75, Number 187), Commission Guidance on Presentation of Liquidity and Capital Resources Disclosures in Management's Discussion and Analysis. This guidance that is intended to improve discussion of liquidity and capital resources in MD&A of financial condition and results of operations in order to facilitate understanding by investors of the liquidity and funding risks facing the registrant.

(c) General Guidance on MD&A

Companies are required, in the MD&A, to provide investors and other users with material information that is necessary to understand the company's financial condition and operating performance as well as its prospects for the future. On December 19, 2003, the SEC issued interpretative guidance entitled Commission Guidance Regarding Management's Discussion and Analysis of Financial Condition and Results of Operations (referred to as FR 72). This guidance is intended to elicit more meaningful disclosure in MD&A in a number of areas, including the overall presentation and focus of MD&A, with general emphasis on the discussion and analysis of known trends, demands, commitments, and events and uncertainties, and with specific guidance on disclosures about liquidity, capital resources, and critical accounting estimates. It provides guidance to assist companies in preparing MD&A disclosure that is easier to follow and understand and contains information that more completely satisfies the SEC's previously enunciated principal objectives of MD&A. The release captures the objective of the MD&A in this way:

The purpose of MD&A is not complicated. It is to provide readers information necessary to an understanding of [a company's] financial condition, changes in financial condition and results of operations. The MD&A requirements are intended to satisfy three principal objectives:

- To provide a narrative explanation of a company's financial statements that enables investors to see the company through the eyes of management;

- To enhance the overall financial disclosure and provide the context within which financial information should be analyzed; and

- To provide information about the quality of, and potential variability of, a company's earnings and cash flow, so that investors can ascertain the likelihood that past performance is indicative of future performance

MD&A should be a discussion and analysis of a company's business as seen through the eyes of those who manage that business. Management has a unique perspective on its business that only it can present. As such, MD&A should not be a recitation of financial statements in narrative form or an otherwise uninformative series of technical responses to MD&A requirements, neither of which provides this important management perspective. Through this release we encourage each company and its management to take a fresh look at MD&A with a view to enhancing its quality. We also encourage early top-level involvement by a company's management in identifying the key disclosure themes and items that should be included in a company's MD&A.

Based on our experience with many companies' current disclosures in MD&A, we believe there are a number of general ways for companies to enhance their MD&A consistent with its purpose. The recent review experiences of the staff of the Division of Corporation Finance, including its Fortune 500 review, have led us to conclude that additional guidance would be especially useful in the following areas:

- The overall presentation of MD&A;

- The focus and content of MD&A (including materiality, analysis, key performance measures and known material trends and uncertainties);

- Disclosure regarding liquidity and capital resources; and

- Disclosure regarding critical accounting estimates.

Therefore, in this release, we emphasize the following points regarding overall presentation:

- Within the universe of material information, companies should present their disclosure so that the most important information is most prominent;

- Companies should avoid unnecessary duplicative disclosure that can tend to overwhelm readers and act as an obstacle to identifying and understanding material matters; and

- Many companies would benefit from starting their MD&A with a section that provides an executive-level overview that provides context for the remainder of the discussion.

We also emphasize the following points regarding focus and content:

- In deciding on the content of MD&A, companies should focus on material information and eliminate immaterial information that does not promote understanding of companies' financial condition, liquidity and capital resources, changes in financial condition, and results of operations (both in the context of profit and loss and cash flows);

- Companies should identify and discuss key performance indicators, including non-financial performance indicators, that their management uses to manage the business and that would be material to investors;

- Companies must identify and disclose known trends, events, demands, commitments, and uncertainties that are reasonably likely to have a material effect on financial condition or operating performance; and

- Companies should provide not only disclosure of information responsive to MD&A's requirements, but also an analysis that is responsive to those requirements that explains management's view of the implications and significance of that information and that satisfies the objectives of MD&A.

For the full text of FR 72, see www.sec.gov/rules/interp/33-8350.htm.

As discussed in FR 72, the SEC provides several recommendations to assist registrants in improving their MD&A disclosures. The SEC believes that the presentation of the MD&A of too many companies may have become unnecessarily lengthy, difficult to understand, and confusing. It asserts that many companies can improve their MD&A by focusing on the most important information disclosed to investors. Disclosure should emphasize material information that is required or promotes understanding and deemphasize immaterial information that is not required and does not promote understanding. Companies should prepare MD&A with a strong focus on the most important information, provided in a manner intended to address the objectives of MD&A. The SEC recommends, in FR 72, consideration of these points:

- Companies should consider whether a tabular presentation of relevant financial or other information may help a reader's understanding of MD&A.

- Companies should consider whether the headings they use assist readers in following the flow of, or otherwise assist in understanding, MD&A, and whether additional headings would be helpful in this regard.

- Many companies' MD&A could benefit from adding an introductory section or overview that would facilitate a reader's understanding.

- While all required information must of course be disclosed, companies should consider using a “layered” approach. Such an approach would present information in a manner that emphasizes, within the universe of material information that is disclosed, the information and analysis that is most important.

(d) Recent Developments

(i) Smaller Reporting Companies

The SEC has adopted amendments to its disclosure and reporting requirements under the Securities Act of 1933 and the Securities Exchange Act of 1934 to expand the number of companies that qualify for its scaled disclosure requirements for smaller reporting companies. On December 19, 2007, the SEC issued a final rule, Smaller Reporting Company Regulatory Relief and Simplification (Releases Nos. 33-8876; 34-56994; 39-2451; File No. S7-15-07).

Companies that have less than $75 million in public equity float qualify for the scaled disclosure requirements under the amendments. Companies without a calculable public equity float will qualify if their revenues were below $50 million in the previous year. To streamline and simplify regulation, the amendments move the scaled disclosure requirements from Regulation S-B into Regulation S-K.

Specific to the MD&A requirements, the final rule allows smaller reporting companies to provide only two years of analysis if the company is presenting only two years of financial statements, instead of the three years of analysis required of larger companies that are required to provide three years of financial statements; also, smaller reporting companies are exempt from providing tabular disclosure of contractual obligations.

The final rule is available at: www.sec.gov/rules/final/2007/33-8876.pdf.

The SEC also issued additional guidance for smaller public companies:

- Smaller Reporting Company Compliance and Disclosure Interpretations, available at: www.sec.gov/info/smallbus/src-cdinterps.htm

- Small Entity Compliance Guide, available at: www.sec.gov/info/smallbus/secg/s3f3-secg.htm

(ii) MD&A Disclosures on Fair Value and Liquidity and Capital Resources

In December 2008, the staff of the SEC participated in the American Institute of Certified Public Accountants' (AICPA) National Conference on Current SEC and Public Company Accounting Oversight Board (PCAOB) Developments. During this conference, the SEC staff made several presentations including two that identified best practices for fair value MD&A disclosures and considerations for preparing the liquidity and capital resources section of the MD&A. The slides are available at: http://sec.gov/news/speech/2008/spch120908wc-slides.pdf/.

Fair Value Disclosures.

The SEC's top ten best practices for fair value MD&A disclosures, as noted on slides 34 to 60, include these areas:

These best practices were developed from two “Dear CFO” letters sent to 30 public companies in March 2008 and September 2008 by the SEC and posted to its Web site, given the much broader applicability of the guidance. The goal of these “Dear CFO” letters was to provide suggestions to improve transparency surrounding fair value measurements.

Subsequent to the issuance of the “Dear CFO” letters and the SEC staff speech, the FASB amended U.S. generally accepted accounting principles (GAAP) to improve financial statement disclosures about fair value. The primary changes for fair value disclosures were issued in 2010 and 2011 with the issuances of two Accounting Standards Updates (ASUs): ASU 2010-06, Fair Value Measurements and Disclosures (Topic 820): Improving Disclosures About Fair Value Measurements; and ASU 2011-04, Fair Value Measurement (Topic 820): Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.

Liquidity and Capital Resources Disclosures.

The SEC's top ten considerations for companies when preparing the liquidity and capital resources section of the MD&A were developed by the SEC staff not only to provide investors with a clear picture of the company's current financial condition but also to provide investors with the opportunity to evaluate the company's future prospects.

The SEC's top ten best practices for liquidity and capital resources MD&A disclosures, as noted on slides 76 to 87, include:

The SEC also issued, on September 17, 2010, an interpretative release entitled Commission Guidance on Presentation of Liquidity and Capital Resources Disclosures in Management's Discussion and Analysis (referred to as FR 83). The release was effective September 28, 2010, and was issued to improve discussion of liquidity and capital resources in MD&A in order to facilitate understanding by investors of the liquidity and funding risks facing the registrant. The three primary areas addressed in the release are liquidity disclosure, leverage ratio disclosures, and contractual obligation table disclosures.

The release is available at: www.sec.gov/rules/interp/2010/33-9144.pdf.

6.2 Current Guidance

(a) Overall Requirements

For large-accelerated and accelerated filers, the MD&A must cover the three most recent fiscal years and the two interyear comparisons. For smaller reporting companies,4 the MD&A must cover the two most recent fiscal years.

Registrants need not discuss the earliest year in comparison to the preceding year unless the discussion is necessary for an understanding of a trend of the registrant's financial position or results of operations. The general requirements, as summarized from Item 303, are summarized next.

- Discuss the registrant's financial condition, changes in financial condition and results of operations.

- With respect to all of the categories just listed, registrants are required to identify any currently known trends, demands, commitments, events, or uncertainties that are reasonably expected to have material affects on the registrant's liquidity, capital resources, and results of operations, or that would cause reported financial information not to be necessarily indicative of future operating results or financial condition.

- Provide such other information that the registrant believes to be necessary to an understanding of its financial condition, changes in financial condition and results of operations.

- These issues must also be discussed by business segments to the extent necessary, in the registrant's judgment, for an understanding of the business as a whole.

- Address both positive and negative aspects of a company's financial condition and results of operations.

- Where the consolidated financial statements reveal material changes from year to year in one or more line items, describe the causes for the changes to the extent necessary to an understanding of the registrant's businesses as a whole.

The required disclosures are ultimately conditional on passing both a “materiality” and a “cost” threshold. Immaterial effects or events need not be (but may be) disclosed.5 As stated in Item 303: “The information provided pursuant to this Item need only include that which is available to the registrant without undue effort or expense and which does not clearly appear in the registrant's financial statements.”

The full requirements are contained in Exhibit 6.1. Regulation S-K requires disclosure in these areas:

(b) Critical Accounting Estimates

On December 12, 2001, the SEC issued an interpretative release entitled Cautionary Advice Regarding Disclosure About Critical Accounting Policies (referred to as FR 60). The SEC's rules governing MD&A have long required disclosure about trends, events, or uncertainties known to management that would materially affect reported financial information; the SEC observed, in FR 60, that disclosure responsive to these requirements could be enhanced. For example, environmental and operational trends, events, and uncertainties typically are identified in MD&A, but the implications of those uncertainties for the methods, assumptions, and estimates used for recurring and pervasive accounting measurements are not always addressed. Communication between investors and public companies could be improved if management explained in MD&A the interplay of specific uncertainties with accounting measurements in the financial statements.

The SEC encourages public companies to include in their MD&A full explanations, in plain English, of their critical accounting policies, the judgments and uncertainties affecting the application of those policies, and the likelihood that materially different amounts would be reported under different conditions or using different assumptions. The objective of this disclosure is consistent with the objective of MD&A.

The SEC pointed out that investors may lose confidence in a company's management and financial statements if sudden changes in its financial condition and results occur but were not preceded by disclosures about the susceptibility of reported amounts to change, including rapid change. In FR 60,7 the SEC alerted public companies to the importance of employing a disclosure regimen in these ways:

1. Each company's management and auditor should bring particular focus to the evaluation of the critical accounting policies used in the financial statements. As part of the normal audit process, auditors must obtain an understanding of management's judgments in selecting and applying accounting principles and methods. Special attention to the most critical accounting policies will enhance the effectiveness of this process. Management should be able to defend the quality and reasonableness of the most critical policies, and auditors should satisfy themselves thoroughly regarding their selection, application, and disclosure.

2. Management should ensure that disclosure in MD&A is balanced and fully responsive. To enhance investor understanding of the financial statements, companies are encouraged to explain in MD&A the effects of the critical accounting policies applied, the judgments made in their application, and the likelihood of materially different reported results if different assumptions or conditions were to prevail.

3. Prior to finalizing and filing annual reports, audit committees should review the selection, application, and disclosure of critical accounting policies. Consistent with auditing standards, audit committees should be apprised of the evaluative criteria used by management in their selection of the accounting principles and methods. Proactive discussions between the audit committee and the company's senior management and auditor about critical accounting policies are appropriate.

4. If companies, management, audit committees, or auditors are uncertain about the application of specific GAAP principles, they should consult with our accounting staff. We encourage all those whose responsibility it is to report fairly and accurately on a company's financial condition and results to seek out our staff's assistance. We are committed to providing that assistance in a timely fashion; our goal is to address problems before they happen.

On May 10, 2002, the SEC proposed a rule entitled Disclosure in Management's Discussion and Analysis About the Application of Critical Accounting Policies. The proposal encompassed disclosure in two areas:

- The methodology and assumptions underlying them

- The effect the accounting estimates have on the company's financial presentation

- The effect of changes in the estimates

- What gave rise to the initial adoption

- The impact of the adoption

- The accounting principle adopted and method of applying it

- The choices it had among accounting principles

This proposal remains outstanding.

Many estimates and assumptions involved in the application of GAAP have a material impact on reported financial condition and operating performance and on the comparability of such reported information over different reporting periods. As previously discussed, the SEC's December 2001 Release, FR 60, reminded companies that, under the existing MD&A disclosure requirements, a company should address material implications of uncertainties associated with the methods, assumptions, and estimates underlying the company's critical accounting measurements. In its follow-up statement, FR 72, the SEC states that:

- When preparing disclosure under the current requirements, companies should consider whether they have made accounting estimates or assumptions where: The nature of the estimates or assumptions is material due to the levels of subjectivity and judgment necessary to account for highly uncertain matters or the susceptibility of such matters to change; and

- The impact of the estimates and assumptions on financial condition or operating performance is material.

If so, companies should provide disclosure about those critical accounting estimates or assumptions in their MD&A.

(c) Non-GAAP Measures

On December 4, 2001, the SEC issued a release entitled Cautionary Advice Regarding the Use of “Pro Forma” Financial Information in Earnings Releases (referred to as FR 59). The SEC issued this release to registrants that present their earnings and results of operations on the basis of methodologies other than GAAP. This is often referred to as pro forma financial information. The SEC states that pro forma financial information can serve useful purposes for public companies that wish to focus investors' attention on critical components of financial results to provide a meaningful comparison to results for the same period of prior years or to emphasize the results of core operations. However, the SEC observed that to a large extent, this has been the intended function of disclosures in a company's MD&A section of its reports.

In response to Section 401(b) of SOX and to codify guidance in FR 59, the SEC amended Regulation S-K. The SEC subsequently adopted new rules and amendments to address public companies' disclosure or release of certain financial information that is calculated and presented on the basis of methodologies other than in accordance with GAAP. The final rule, Conditions for Use of Non-GAAP Financial Measures, was issued on January 22, 2003. The disclosure regulation, Regulation G, requires public companies that disclose or release such non-GAAP financial measures to include, in that disclosure or release, a presentation of the most directly comparable GAAP financial measure and a reconciliation of the disclosed non-GAAP financial measure to the most directly comparable GAAP financial measure. The final rule also adopted amendments to provide additional guidance to those registrants that include non-GAAP financial measures in SEC filings.

Here is a recap of the requirements:

Regulation G

- Application. This regulation applies whenever a registrant required to file reports under Section 13(a) or 15(d) of the Exchange Act (other than a registered investment company), or a person acting on the registrant's behalf, discloses or releases publicly any material information that includes a non-GAAP financial measure. Typically, this information is furnished under Item 2.02 of Form 8-K.

- Requirements. The registrant must present the most directly comparable GAAP measure and a reconciliation of the differences between the non-GAAP measure disclosed or released with the most directly comparable GAAP measure. With regard to forward-looking information, a quantitative reconciliation is required only to the extent available without unreasonable efforts. If all of the information necessary is not available without unreasonable efforts, the registrant must identify the information that is unavailable and disclose probable significance.

Item 10(e) of Regulation S-K

- Application. This regulation applies to a registrant's filings with the SEC (e.g., 10-K, 10-Q, 20-F, S-1, F-1).

- Requirements. The registrant must present:

- With equal or greater prominence, the most directly comparable GAAP measure

- A reconciliation of the differences between the non-GAAP measure and the most directly comparable GAAP measures

- A statement disclosing why management believes the presentation of the non-GAAP measure provides useful information to investors regarding the registrant's financial condition and results of operations

- To the extent material, a statement disclosing the additional purposes, if any, for which management uses the non-GAAP measure

Subsequent to the enactment of these rules and regulations and the release of the SEC staff interpretative guidance, the SEC staff noted questions and inconsistencies in a recent study of registrant filings. As a result, in January 2010, the SEC's Division of Corporate Finance issued new Compliance and Disclosure Interpretations (C&DIs) on the use of non-GAAP financial measures. The C&DIs replace the interpretative guidance in the SEC staff's “Frequently Asked Questions Regarding the Use of Non-GAAP Measures” (FAQs), which was issued in June 2003, but the rules on non-GAAP financial measures (Regulation G and Item 10(e) of Regulation S-K) were not amended.

The issuance of the C&DIs was a result of the SEC staff's review of its June 2003 interpretations in an effort to eliminate any actual or perceived restrictions in the FAQs on the disclosure of non-GAAP information that were not consistent with the actual rules. In addition, they were issued to ensure that non-GAAP guidance is being read in a manner that provides clarity and flexibility to companies with respect to reporting information in their filings that they believe provides the most meaningful indicators of how they are doing and is consistent with other communications (e.g., through communications such as earnings calls and press releases).

(d) Effect of Newly Issued But Not Yet Effective Accounting Standards

Public companies must discuss the effect of newly issued, but not yet effective, accounting standards. SEC Staff Accounting Bulletin (SAB) Disclosure of the Impact That Recently Issued Accounting Standards Will Have on the Financial Statements of the Registrant When Adopted in a Future Period (SAB No. 74) requires disclosure of the expected impacts on financial information to be reported in the future and is required in the financial statements if the change to the new accounting standard will be accounted for in future periods by restatement of the current financials. Additionally, disclosure in the financials is to be considered when the change will be accounted for prospectively or as a change in accounting principle.

6.3 Related Accounting Literature

(a) Risks and Uncertainties

The financial statements disclosures under GAAP have similar objectives as the MD&A disclosures. In 1994, the AICPA's Accounting Standards Executive Committee (AcSEC) issued Statement of Position (SOP) 94-6, Disclosure of Certain Significant Risks and Uncertainties. This SOP, subsequently codified in FASB's Accounting Standards Codification (ASC) 275, Risks and Uncertainties, requires an entity to disclose, in the notes to the financial statements, forward-looking information about certain significant estimates and concentrations. This is a GAAP requirement rather than a MD&A requirement and is applicable to both public and private entities. As discussed in ASC 275-10-05-2:

The central feature of this Subtopic's disclosure requirements is selectivity: specified criteria serve to screen the host of risks and uncertainties that affect every entity so that required disclosures are limited to matters significant to a particular entity.

The disclosures focus primarily on risks and uncertainties that could significantly affect the amounts reported in the financial statements in the near term or the near-term functioning of the reporting entity. The risks and uncertainties this Subtopic addresses can stem from any of the following:

a. The nature of the entity's operations

b. The use of estimates in the preparation of the entity's financial statements

c. Significant concentrations in certain aspects of the entity's operations.

Namely, an entity must disclose:

The first two disclosures are always required. Disclosures about risks (related to concentrations) and uncertainties (concerning estimates) are required if specified criteria are met. The statement became effective for fiscal years ending after December 15, 1995. A summary of the required disclosures is presented next. For a complete understanding, readers should refer to the full text of ASC 275. (see: https://asc.fasb.org/subtopic&trid=2134480—a subscription service)

(b) Nature of Operations

The financial statements should include a description of the major products or services the entity sells or provides and its principal markets, including the locations of those markets. If the entity operates in more than one business, the disclosure should also indicate the relative importance of its operations in each business and the basis for the determination—for example, assets, revenues, or earnings. Disclosures about the nature of operations do not need to be quantified. The relative importance could be conveyed by use of terms such as “predominately,” “about equally,” or “major.”

(c) Use of Estimates in the Preparation of Financial Statements

Financial statements should include an explanation that the preparation of financial statements in conformity with GAAP requires the use of management's estimates.

(d) Certain Significant Estimates

Uncertainties concerning estimates that affect financial statement amounts (such as a valuation allowance for deferred tax assets or the carrying amount of inventory or a long-term contract) if it is at least reasonably possible the estimates will change in the near term and the effect of the change could be material to the financial statements must be disclosed.

As stated in ASC 275-10-50-8:

Disclosure regarding an estimate shall be made when known information available before the financial statements are issued or are available to be issued indicates that both of the following criteria are met:

a. It is at least reasonably possible that the estimate of the effect on the financial statements of a condition, situation, or set of circumstances that existed at the date of the financial statements will change in the near term due to one or more future confirming events. (The term reasonably possible as used in this Subtopic is consistent with its use in Subtopic 450-20 to mean that the chance of a future transaction or event occurring is more than remote but less than likely.)

b. The effect of the change would be material to the financial statements.

(e) Current Vulnerability Due to Certain Concentrations

Financial statements should include risks related to concentrations in volume of business, sources of supply, revenue, or market or geographic area if it is at least reasonably possible that the concentrations could have a severe impact on operations within the near term. As stated in ASC 275-10-50-16:

Vulnerability from concentrations arises because an entity is exposed to risk of loss greater than it would have had it mitigated its risk through diversification. Such risks of loss manifest themselves differently, depending on the nature of the concentration, and vary in significance. Financial statements shall disclose the concentrations described in paragraph 275-10-50-18 if, based on information known to management before the financial statements are issued or are available to be issued (as discussed in Section 855-10-25), all of the following criteria are met:

a. The concentration exists at the date of the financial statements.

b. The concentration makes the entity vulnerable to the risk of a near-term severe impact.

c. It is at least reasonably possible that the events that could cause the severe impact will occur in the near term.

Concentrations, including known group concentrations, are required to be disclosed if they meet the criteria of paragraph 275-10-50-16. Group concentrations exist if a number of counterparties or items that have similar economic characteristics collectively expose the reporting entity to a particular kind of risk. Some concentrations may fall into more than one of these categories:

- Volume of business with a particular customer, supplier, lender, grantor, or contributor

- Revenue from particular products, services, or fundraising events

- Source of supply of materials, labor, services, or licenses or other rights

- Market or geographic area in which operations are conducted

6.4 External Auditor Involvement

The external auditor is required follow Statement of Auditing Standards (SAS) No. 8, Other Information in Documents Containing Audited Financial Statements, when other information, such as the MD&A, is presented with the audited financial statements and the independent auditor's report. SAS 88 was issued by the AICPA in December 1975 and in the codification, the reference is AU Section 550, Other Information in Documents Containing Audited Financial Statements. As excerpted from par. 4 of SAS 8, the auditor has the responsibility to read the other information, such as the MD&A:

Other information in a document may be relevant to an audit performed by an independent auditor or to the continuing propriety of his report. The auditor's responsibility with respect to information in a document does not extend beyond the financial information identified in his report, and the auditor has no obligation to perform any procedures to corroborate other information contained in a document. However, he should read the other information and consider whether such information, or the manner of its presentation, is materially inconsistent with information, or the manner of its presentation, appearing in the financial statements.

For a complete understanding, readers should refer to the full text of the standard. The full text of SAS 8 is available on the PCAOB Web site at: http://pcaobus.org/Standards/Auditing/Pages/AU550.aspx

Management may wish to engage the external auditor to perform additional procedures related to the MD&A. To accommodate such an engagement, the AICPA issued, in 2001, Statement on Standards for Attestation Engagements No. 10, Attestation Standards: Revision and Recodification, which is relevant to the external auditor's association with MD&A. In the codification, the reference is attestation standards (AT) Section 701, Management's Discussion and Analysis. This statement provides performance and reporting guidance and applies to engagements where management has opted to engage the external auditor to examine and to review the MD&A included in audited financial statements or in other documents. The full text of AT Section 701 can be accessed on the PCAOB's Web site at: http://pcaobus.org/Standards/Attestation/Pages/AT701.aspx.

1 The safe harbor rule protects issuers from liability for forward-looking information, if such information has a reasonable basis and is disclosed in good faith. Otherwise, fraud actions under Rule 10b-5 may be brought against the firm.

2 Although the 1989 release emphasizes prospective analysis, the historical analysis of the 1980 release is also required. The 1989 release interprets, but does not supersede, the 1980 release. Therefore, by continuing to require a discussion of historical changes as well as prospective events, the SEC underscores its belief that a better understanding of the causes of past performance is necessary for investors to assess the likelihood that the past is indicative of the future.

3 As a matter of interest, the 1989 release mentions one known, future, material event that need not be disclosed. Merger negotiations do not have to be discussed in the MD&A unless the registrant has otherwise disclosed them. The SEC acknowledges that the risk of disclosure may jeopardize the transaction. There are other disclosure items that are required under different SEC releases and that may be disclosed in the MD&A. For instance, the SEC's Financial Reporting Release No. 6 (1982) mentions the MD&A as an appropriate place to discuss the degree of exposure to exchange rate risks, the functional currencies used to measure significant foreign operations, and the nature of the translation component of equity. Also, in its Staff Accounting Bulletin (SAB) No. 74 (1987), the SEC states that the MD&A may be used to discuss the impact (if known or reasonably estimable) of a future adoption of a recently issued accounting standard.

4 The SEC defines a “smaller reporting company” as one with public float of less than $75 million. Public float is computed at the end of the second quarter, using one year's information. If there is no public float, then a revenue test is used. The revenue test for a “smaller reporting company” is whether the company has revenue of under $50 million.

5 The SEC discussed materiality in SAB No. 99, Materiality, August 12, 1999. Further, the SEC relies on the decisions rendered by the Supreme Court in two separate cases. In TSC Industries Inc. v. Northway (1980), the Court stated that “an omitted fact is material if there is a substantial likelihood that reasonable shareholders would consider it important.” The Court further explained: “To fulfill the materiality requirement, there must be a substantial likelihood that the disclosure of the omitted fact would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.” In Basic, Inc. v. Levinson (1988), the Court addressed materiality as it relates to possible future events: “Materiality will depend at any given time upon a balancing of both the indicated probability that the event will occur and the anticipated magnitude of the event in light of the totality of the company activity.” Finally, and most important, for both past events and possible future events, the Court stated: “Materiality depends on the facts and is to be determined on a case by case basis.” Therefore, materiality is a relative concept.

6 Smaller public companies (as defined) are not required to provide tabular disclosure of contractual obligations.

7 www.sec.gov/rules/other/33-8040.htm

8 In April 2003, the PCAOB adopted certain preexisting standards as its interim standards. Pursuant to Rule 3200T, Interim Auditing Standards consist of generally accepted auditing standards, as described in the AICPA's Auditing Standards Board's Statement of Auditing Standards No. 95, in existence on April 16, 2003, to the extent not superseded or amended by the Board.