Chapter 8

Hedging Foreign Currency Liabilities

The global nature of the capital markets allows many entities to fund in the lowest cost market available to them. Frequently, entities capture lower costs of funds and greater market liquidity by raising capital in currencies other than their functional currency. Because a foreign currency liability is a monetary item, IAS 21 requires the liability to be translated into the entity's functional currency using the exchange rate prevailing at the reporting date, as covered in Chapter 6. The translation gains or losses on the debt are recorded in profit or loss. Thus, absence of an FX hedging strategy may result in significant volatility in profit or loss. This chapter deals with the hedge accounting treatment of foreign currency borrowings swapped back into the issuer's functional currency.

The most common technique to hedge foreign debt is through cross-currency swaps (CCS) that convert the debt's foreign cash flows back into the entity's functional currency. Assuming the EUR as the issuer's functional currency and a USD-denominated debt, there are four potential hedging situations (which are covered in the four case studies in this chapter):

| USD liability | CCS characteristics | Resulting EUR liability | Type of hedge |

| Floating | Receive USD floating – pay EUR floating | Floating | Fair value |

| Fixed | Receive USD fixed – pay EUR floating | Floating | Fair value |

| Floating | Receive USD floating – pay EUR fixed | Fixed | Cash flow |

| Fixed | Receive USD fixed – pay EUR fixed | Fixed | Cash flow |

8.1 CASE STUDY: HEDGING A FLOATING RATE FOREIGN CURRENCY LIABILITY WITH A RECEIVE-FLOATING PAY-FLOATING CROSS-CURRENCY SWAP

This case study illustrates the accounting treatment of a hedge of a floating rate foreign currency liability with a pay-floating receive-floating CCS. Because this case is very complex, it is necessary to discuss in detail some of the challenging aspects of the case, especially the selection of the most suitable hedging instrument, the interaction between the translation of the foreign currency liability and the hedge item fair value adjustments, and the calculation of accruals.

8.1.1 Background Information

On 15 July 20X0, ABC issued a USD-denominated floating rate bond. ABC's functional currency was the EUR. The bond had the following main terms:

| Bond terms | |

| Issue date | 15 July 20X0 |

| Maturity | 3 years (15 July 20X3) |

| Notional | USD 100 million |

| Coupon | USD Libor 12M + 0.50% annually, actual/360 basis |

| USD Libor fixing | Libor is fixed 2 days prior to the beginning of each annual interest period |

Since ABC's objective was to raise EUR floating funding, on the issue date ABC entered into a CCS. Through the CCS, the entity agreed to receive a floating rate equal to the bond coupon and pay a Euribor floating rate plus a spread. The CCS had the following terms:

| Cross-currency swap terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | Euribor 12M + 49 bps annually, actual/360 basis, on the EUR nominal Euribor is fixed two business days prior to the beginning of each annual interest period |

| ABC receives | USD Libor 12M + 0.50 bps annually, actual/360 basis. Libor is fixed 2 days prior to the beginning of each annual interest period |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The mechanics of the CCS are described next. It can be seen that through the combination of the USD bond and the CCS, ABC synthetically obtained a EUR floating liability.

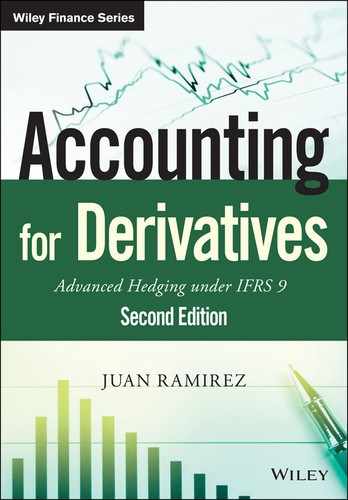

On the issue date at the start of the CCS, there was an initial exchange of nominal amounts through the CCS: ABC delivered the USD 100 million debt issuance proceeds and received EUR 80 million. The resulting EUR–USD exchange rate was 1.2500. The combination of the bond and CCS had the same effect as if ABC had issued a EUR-denominated bond, as shown in Figure 8.1.

Figure 8.1 Bond and CCS combination – initial cash flows.

An exchange of interest payments took place annually. ABC received USD Libor-linked interest on the USD nominal and paid Euribor-linked interest on the EUR nominal. ABC used the USD Libor cash flows it received under the CCS to pay the bond interest. Figure 8.2 shows the strategy's intermediate cash flows.

Figure 8.2 Bond and CCS combination – intermediate cash flows.

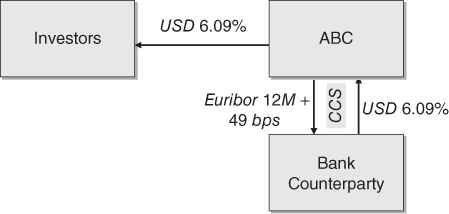

At maturity of the CCS and the debt, ABC re-exchanged the CCS nominals, using the USD 100 million it received through the CCS to redeem the bond issue, and delivering EUR 80 million to the CCS counterparty. Note that this final exchange was made at exactly the same rate used in the initial exchange (1.2500). Figure 8.3 shows the strategy's cash flows at maturity.

Figure 8.3 Bond and CCS combination – final cash flows.

8.1.2 Determining Risk Components to Include in the Hedging Relationship

The aim of the CCS was to hedge the changes in fair value of the bond. There were three risks affecting the bond's fair value:

- Exchange rate risk. An appreciation of the USD relative to the EUR would increase the EUR value of the bond's USD cash outflows, increasing the bond's fair value. Conversely, a depreciation of the USD relative to the EUR would decrease the EUR value of the bond's USD flows to be paid by ABC, decreasing the bond's fair value.

- Interest rate risk. The bond coupons were linked to the USD Libor 12-month rate. An increase in USD Libor rates would decrease the present value of the future USD cash flows, decreasing the bond's fair value. Conversely, a decline in USD Libor rates would increase the present value of the future USD cash flows, increasing the bond's fair value.

- Credit risk. The bond was issued with a credit margin of 50 basis points. During the life of the bond, a narrowing of ABC's credit margin would increase the bond's fair value. Conversely, a widening of the credit margin would decrease the bond's fair value.

The CCS hedged the exposure of the bond's fair value to the first two risks (exchange risk and interest rate risk). However, to hedge the third element (credit risk) would have implied ABC buying protection on its own credit risk, which no counterparty would provide unless a proxy credit name was used. Therefore, the bond's credit risk was excluded from the hedging relationship. Fair valuations of the hedged item would assume that the initial 50 bps credit margin remained unchanged during the term of the hedge.

When assessing effectiveness and calculating effective and ineffective amounts, the helpful simplification of a hypothetical derivative could not be used for fair value hedges. Therefore ABC needed to fair value the hedged item.

8.1.3 Hedging Relationship Documentation

ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to reduce the variability of the fair value of a foreign currency denominated floating rate bond issued by the entity. This hedging objective is consistent with the group's overall interest rate risk management strategy of transforming all new issued foreign-denominated debt into floating rate, and thereafter managing the exposure to interest rate risk through the proportion of fixed and floating rate net debt in its total debt portfolio. Exchange rate and interest rate risk. The designated risk being hedged is the risk of changes in the EUR fair value of the hedged item attributable to changes in the EUR–USD exchange rate and USD Libor interest rate. Fair value changes attributable to credit or other risks are not hedged in this relationship. Accordingly, the 50 bps credit spread is excluded from the hedging relationship |

| Type of hedge | Fair value hedge |

| Hedged item | The coupons and principal of the 3-year USD floating rate bond with reference number 678902. The main terms of the bond are a USD 100 million principal, an annual coupon of USD Libor plus 0.50% calculated on the principal |

| Hedging instrument | The cross-currency swap with reference number 014569. The main terms of the CCS are a USD 100 million nominal, a EUR 80 million nominal, a 3-year maturity, a USD annual interest of USD Libor 12-month rate plus 0.50% on the USD nominal to be received by the entity and a EUR annual interest of Euribor 12-month rate plus 0.49% on the EUR nominal to be paid by the entity. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

8.1.4 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument to changes in the fair value of the hedged item. Changes in the fair value of the hedging instrument (i.e., the CCS) will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in profit or loss, adjusting interest income/expense.

- The ineffective part of the gain or loss on the hedging instrument will be recognised in profit or loss, as other financial income/expenses.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is an already recognised liability that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative that does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a quantitative basis using the scenario analysis method for two scenarios:

- In a first scenario, USD Libor interest rates will be shifted upwards by 2%, the EUR–USD exchange rate increased by 10%, and the changes in fair value of the hedged item and the hedging instrument compared.

- In a second scenario, USD Libor interest rates will be shifted downwards by 2%, the EUR–USD exchange rate reduced by 10%, and the changes in fair value of the hedged item and the hedging instrument compared.

8.1.5 Hedge Effectiveness Assessment Performed at the Start of the Hedging Relationship

On 15 July 20X0 ABC performed a hedge effectiveness assessment which was documented as described next.

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the quantitative assessment performed, the entity concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

A quantitative assessment was performed to support the conclusion that the hedging instrument and the hedged item had values that would generally move in opposite directions. The quantitative assessment consisted of two scenario analyses as follows:

A parallel shift of +2% in the USD Libor interest rate and +10% in the EUR–USD spot rate, occurring simultaneously on the assessment date, was simulated. The fair values of the hedging instrument and the hedged item were calculated and compared to their initial fair values. As shown in the table below, the assessment resulted in a high degree of offset, corroborating that both elements had values that would generally move in opposite directions.

| Scenario 1 analysis assessment | ||

| Hedging instrument | Hedged item | |

| Initial fair value | -0- | <81,094,000> |

| Final fair value | <7,353,000> | <73,692,000> |

| Cumulative fair value change | <7,353,000> | 7,402,000 |

| Degree of offset | 99.3% | |

Similarly, a parallel shift of –2% in the USD Libor interest rate and –10% in the EUR–USD spot rate, occurring simultaneously on the assessment date was simulated. As shown in the table below, the assessment resulted in a high degree of offset, corroborating that both elements had values that would generally move in opposite directions.

| Scenario 2 analysis assessment | ||

| Hedging instrument | Hedged item | |

| Initial fair value | -0- | <81,094,000> |

| Final fair value | 9,023,000 | <90,157,000> |

| Cumulative fair value change | 9,023,000 | <9,063,000> |

| Degree of offset | 99.6% | |

The following potential sources of ineffectiveness were identified:

- a substantial deterioration in credit risk of either the entity or the counterparty to the hedging instrument; and

- a change in the timing or amounts of the hedged highly expected cash flows.

The hedge ratio was set at 1:1.

ABC also performed assessments at each reporting date, yielding similar conclusions. These assessments have been omitted to avoid unnecessary repetition.

8.1.6 Fair Valuations, Effective/Ineffective Amounts and Cash Flow Calculations

Fair Valuations of the Hedged Item

When calculating the fair value of the hedged item it is important to remember that credit risk was excluded from the hedging relationship. As a result, the expected cash flows were discounted using the USD Libor curve flat (i.e., without any credit spread). Otherwise, large inefficiencies may arise. The fair value of the hedged item on 15 July 20X0 was calculated as follows:

| Hedged item fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied USD Libor (1) | Discount factor (2) | Spread (3) | Expected cash flow (4) | Present value (5) |

| 15-Jul-X1 | 5.40% | 0.9481 | 0.50% | <5,982,000> | <5,672,000> |

| 15-Jul-X2 | 5.60% | 0.8972 | 0.50% | <6,185,000> | <5,549,000> |

| 15-Jul-X3 | 5.78% | 0.8475 | 0.50% | <106,367,000> | <90,146,000> |

| USD fair value | <101,367,000> | ||||

| EUR–USD spot | 1.2500 (6) | ||||

| EUR fair value | <81,094,000> | ||||

Notes:

(1) The implied USD Libor rate. For example, 5.40% was the USD Libor 12M rate set on 13-Jul-X0, and 5.60% and 5.78% were the USD Libor 12M rates expected to be set on 13-Jul-X1 and 13-Jul-X2 respectively

(2) The discount factor from the cash flow date to the valuation date. For example, 0.9481 was calculated as 1/(5.40% × 365/360), 365 being the number of calendar days from the valuation date to 15-Jul-X1

(3) The bond's credit margin over USD Libor 12M

(4) The expected cash flow to be paid on such date. For example, <5,982,000> was calculated as: <100 mn> × (5.40% + 0.50%) × 365/360, 365 being the number of calendar days in the interest period

(5) Expected cash flow × Discount factor

(6) EUR–USD spot rate on valuation date

Just to clarify, the fair value calculated differed from the initial carrying amount of the bond, which was EUR 80 million (USD 100 million proceeds divided by the 1.2500 spot rate). Had the discount factors been based on the USD Libor curve plus 0.50% (i.e., credit risk included), the valuation would have been EUR 80 million, as detailed in the following table:

| Bond fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Spread | Expected cash flow | Present value |

| 15-Jul-X1 | 5.40% | 0.9436 (*) | 0.50% | <5,982,000> | <5,645,000> |

| 15-Jul-X2 | 5.60% | 0.8886 | 0.50% | <6,185,000> | <5,496,000> |

| 15-Jul-X3 | 5.78% | 0.8354 | 0.50% | <106,367,000> | <88,859,000> |

| USD fair value | <100,000,000> | ||||

| EUR–USD spot | 1.2500 | ||||

| EUR fair value | <80,000,000> | ||||

(*) 1/[(5.40%+0.50%) × 365/360], 365 being the number of calendar days from the valuation date to 15-Jul-X1

Therefore, the carrying amount of the USD bond did not represent its full fair value but a mix between amortised cost and an element corresponding to the fair valuation due to interest rate movements since the start of the hedging relationship.

The fair value of the hedged item on 31 December 20X0 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Spread | Expected cash flow | Present value |

| 15-Jul-X1 | 5.50% (1) | 0.9709 (2) | 0.50% | <3,212,000> (3) | <3,119,000> |

| 15-Jul-X2 | 5.75% | 0.9174 | 0.50% | <6,337,000> | <5,814,000> |

| 15-Jul-X3 | 5.85% | 0.8660 | 0.50% | <106,438,000> | <92,175,000> |

| USD fair value | <101,108,000> | ||||

| EUR–USD spot | 1.2800 | ||||

| EUR fair value | <78,991,000> | ||||

Notes:

(1) The implied USD Libor rate from 31-Dec-X0 to 15-Jul-X1

(2) 1/(5.50% × 196/360), 196 being the number of calendar days from the valuation date (31-Dec-X0) to 15-Jul-X1

(3) <100 mn> × (5.40% + 0.50%) × 196/360, where 5.40% was the USD Libor 12M rate fixed on 13-Jul-X0 and 196 is the number of calendar days from the valuation date (31-Dec-X0) to 15-Jul-X1

The fair value of the hedged item on 31 December 20X1 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Spread | Expected cash flow | Present value |

| 15-Jul-X2 | 5.65% | 0.9702 | 0.50% | <3,294,000> | <3,196,000> |

| 15-Jul-X3 | 5.90% | 0.9154 | 0.50% | <106,489,000> | <97,480,000> |

| USD fair value | <100,676,000> | ||||

| EUR–USD spot | 1.2200 | ||||

| EUR fair value | <82,521,000> | ||||

The fair value of the hedged item on 31 December 20X2 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Spread | Expected cash flow | Present value |

| 15-Jul-X3 | 5.90% | 0.9689 | 0.50% | <103,348,000> | <100,134,000> |

| USD fair value | <100,134,000> | ||||

| EUR–USD spot | 1.1500 | ||||

| EUR fair value | <87,073,000> | ||||

The fair value of the hedged item on 15 July 20X3 was calculated as follows:

| Hedged item fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Spread | Expected cash flow | Present value |

| 15-Jul-X3 | — | 1.0000 | — | <100,000,000> | <100,000,000> |

| USD fair value | <100,000,000> | ||||

| EUR–USD spot | 1.1100 | ||||

| EUR fair value | <90,909,000> | ||||

Fair Valuations of the Hedging Instrument

The fair value of the hedging instrument on 15 July 20X0 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 0.50% | 5,982,000 | 5,672,000 |

| 31-Jul-X2 | 5.60% | 0.8972 | 0.50% | 6,185,000 | 5,549,000 |

| 31-Jul-X3 | 5.78% | 0.8475 | 0.50% | 106,367,000 | 90,146,000 |

| Total USD | 101,367,000 | ||||

| Total EUR (1.2500) | 81,094,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 0.49% | <4,047,000> | <3,871,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 0.49% | <4,218,000> | <3,850,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 0.49% | <84,364,000> | <73,371,000> |

| Total EUR | <81,092,000> | ||||

| Fair value (before adjustments) | 2,000 | ||||

| Adjustments (CVA/DVA and basis) | <2,000> | ||||

| Fair value (including adjustments) | -0- | ||||

It can be observed that the valuations of the USD leg of the CCS and of the hedged item were of opposite sign. The expected cash flow of the EUR leg was calculated as EUR 80 mn × (Euribor 12M + 0.49%) × Days/360, where Days was the number of days in the interest period.

The fair value of the hedging instrument on 31 December 20X0 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 0.50% | 3,212,000 | 3,119,000 |

| 31-Jul-X2 | 5.75% | 0.9174 | 0.50% | 6,337,000 | 5,814,000 |

| 31-Jul-X3 | 5.85% | 0.8660 | 0.50% | 106,438,000 | 92,175,000 |

| Total USD | 101,108,000 | ||||

| Total EUR (1.2800) | 78,991,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 0.49% | <2,173,000> | <2,120,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 0.49% | <4,291,000> | <3,992,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 0.49% | <84,412,000> | <74,772,000> |

| Total EUR | <80,884,000> | ||||

| Fair value (before adjustments) | <1,893,000> | ||||

| Adjustments (CVA/DVA and basis) | 57,000> | ||||

| Fair value (including adjustments) | <1,836,000> | ||||

The fair value of the hedging instrument on 31 December 20X1 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 0.50% | 3,294,000 | 3,196,000 |

| 31-Jul-X3 | 5.90% | 0.9154 | 0.50% | 106,489,000 | 97,480,000 |

| Total USD | 100,676,000 | ||||

| Total EUR (1.2200) | 82,521,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 0.49% | <2,282,000> | <2,224,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 0.49% | <84,412,000> | <78,326,000> |

| Total EUR | <80,550,000> | ||||

| Fair value (before adjustments) | 1,971,000 | ||||

| Adjustments (CVA/DVA and basis) | <49,000> | ||||

| Fair value (including adjustments) | 1,922,000 | ||||

The fair value of the hedging instrument on 31 December 20X2 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 0.50% | 103,348,000 | 100,134,000 |

| Total USD | 100,134,000 | ||||

| Total EUR (1.1500) | 87,073,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 0.49% | <82,369,000> | <80,211,000> |

| Total EUR | <80,211,000> | ||||

| Fair value (before adjustments) | 6,862,000 | ||||

| Adjustments (CVA/DVA and basis) | <69,000> | ||||

| Fair value (including adjustments) | 6,793,000 | ||||

The fair value of the hedging instrument on 15 July 20X3 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | 100,000,000 | 100,000,000 |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | <80,000,000> | <80,000,000> |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Effective and Ineffective Amounts

The following table summarises the period changes in the fair value of the hedged item and the hedging instrument:

| Hedging instrument | Hedged item | |||

| Fair value | Period change | Fair value | Period change | |

| 15-Jul-X0 | -0- | — | <81,094,000> | — |

| 31-Dec-X0 | <1,836,000> | <1,836,000> | <78,991,000> | 2,103,000 |

| 31-Dec-X1 | 1,922,000 | 3,758,000 | <82,521,000> | <3,530,000> |

| 31-Dec-X2 | 6,793,000 | 4,871,000 | <87,073,000> | <4,552,000> |

| 15-Jul-X3 | 10,909,000 | 4,116,000 | <90,909,000> | <3,836,000> |

On each valuation date, the effective part was the lower of the two period fair value changes (taking into account their opposing signs) and the ineffective part was any remainder:

| Hedging instrument | Hedged item | |||||

| Period change | Effective part | Ineffective part | Period change | Effective part | Ineffective part | |

| 31-Dec-X0 | <1,836,000> | <1,836,000> | -0- | 2,103,000 | 1,836,000 | 267,000 |

| 31-Dec-X1 | 3,758,000 | 3,530,000 | 228,000 | <3,530,000> | <3,530,000> | -0- |

| 31-Dec-X2 | 4,871,000 | 4,552,000 | 319,000 | <4,552,000> | <4,552,000> | -0- |

| 15-Jul-X3 | 4,116,000 | 3,836,000 | 280,000 | <3,836,000> | <3,836,000> | -0- |

Accruals and Payable/Receivable Amounts

The following table summarises the accruals and payables related to the bond:

| Bond accruals and payables | ||||||

| USD Libor 12M | Average EUR–USD | Spot EUR–USD | EUR coupon accrual (1) | EUR payable amount (2) | Retranslation payable (3) | |

| 31-Dec-X0 | 5.40% | 1.2630 | 1.2800 | <2,193,000> | <2,164,000> | |

| 15-Jul-X1 | 5.40% | 1.2680 | 1.2400 | <2,533,000> | <2,590,000> | <70,000> |

| 31-Dec-X1 | 5.55% | 1.2320 | 1.2200 | <2,305,000> | <2,328,000> | |

| 15-Jul-X2 | 5.55% | 1.2170 | 1.2100 | <2,707,000> | <2,722,000> | <19,000> |

| 31-Dec-X2 | 5.65% | 1.1680 | 1.1500 | <2,472,000> | <2,510,000> | |

| 15-Jul-X3 | 5.65% | 1.1240 | 1.1000 | <2,979,000> | <3,044,000> | <114,000> |

Notes:

(1) USD 100 mn × (USD Libor 12M + 0.50%) × (Days/360)/Average EUR–USD, where Days was the number of calendar days in the accrual period (i.e., 169 for accrual periods ending on 31 December and 196 for accrual periods ending on 15 July)

(2) USD 100 mn × (USD Libor 12M + 0.50%) × (Days/360)/Spot EUR–USD

(3) USD payable amount × (1/previous Spot EUR–USD – 1/current Spot EUR–USD), where USD payable amount was the USD 100 mn × (USD Libor 12M + 0.50%) × Days/360 corresponding to the previous accrual period

There was no need to retranslate into EUR the USD carrying amount of the bond, as it was already included in the fair valuation of the hedged item. Otherwise a double counting will occur.

The accruals and payables related to the USD leg of the CCS were identical to those of the bond, but of opposite sign. The following table summarises the accruals and payables related to the EUR leg of the CCS:

| CCS EUR leg accruals and payables | ||||

| Euribor 12M | Days | EUR leg accrual (*) | Payable amount | |

| 31-Dec-X0 | 4.50% | 169 | 1,874,000 | 1,874,000 |

| 15-Jul-X1 | 4.50% | 196 | 2,173,000 | 2,173,000 |

| 31-Dec-X1 | 4.75% | 169 | 1,968,000 | 1,968,000 |

| 15-Jul-X2 | 4.75% | 196 | 2,282,000 | 2,282,000 |

| 31-Dec-X2 | 4.95% | 169 | 2,043,000 | 2,043,000 |

| 15-Jul-X3 | 4.95% | 196 | 2,369,000 | 2,369,000 |

(*) 100 mn × (Euribor 12M + 0.49%) × Days/360, where Days was the number of calendar days in the accruing period

Note on Fair Value Adjustments and Translation

The USD bond was recognised at amortised cost. Without the hedge, being a floating rate bond and being issued at par, the effective interest rate in each interest period was the USD Libor 12-month plus 50 bps corresponding to such period. Also, the carrying amount of the bond was a constant USD 100 million. The translation of the carrying amount into EUR was relatively straightforward, calculated by dividing USD 100 million by the EUR–USD spot rate prevailing on the reporting date.

When fair value hedge accounting is applied to a hedge of a debt instrument, the carrying value of the debt is adjusted for movements in the hedged risk. IFRS 9 requires the fair value adjustment to be amortised to profit or loss as early as when the adjustment is made and no later than when the hedged item ceases to be fair value adjusted. This amortisation is included as part of the revised effective interest rate. Therefore:

- If ABC chose to amortise the fair value adjustment as soon as the adjustment was made, then because the fair value adjustment changed for each reporting period during the hedging relationship term, a revised effective interest rate needed to be determined at the start of each reporting period. Accordingly, the bond's effective interest rate had to take into account the fair value adjustments to the carrying amount of the USD bond, being different from the USD Libor 12M plus 50 bps corresponding to such period.

- Alternatively, if ABC chose to start amortising the adjustment when hedge accounting ceased it only needed to recalculate the effective interest rate at that point. Accordingly, the bond's effective interest rate was the USD Libor 12M plus 50 bps corresponding to the prevailing interest period, during the hedging relationship term. ABC adopted this alternative due to its much lower operational burden.

Regarding the translation of the fair value adjustments, the fair valuations of the hedged item for the risk being hedged were performed in EUR. Therefore, these fair valuations already included the translation into EUR of the fair value adjustments.

8.1.7 Accounting Entries

The required journal entries were as follows.

- Journal entries on 15 July 20X0

The bond was issued.

- No entries were required to record the CCS as its initial fair value was zero.

- Journal entries on 31 December 20X0

The accrued interest of the bond was EUR <2,193,000>. The payable related to this accrued interest was EUR <2,164,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 2,103,000 gain, of which EUR 1,836,000 was deemed to be effective and EUR 267,000 ineffective.

- The accrual of the USD leg of the CCS was EUR 2,193,000. The receivable related to this accrued interest was EUR 2,164,000.

- The accrual of the EUR leg of the CCS was EUR <1,874,000>.

- The change in fair value of the CCS produced a EUR 1,836,000 loss, fully deemed to be effective.

- Journal entries on 15 July 20X1

The accrued interest of the bond was EUR <2,533,000>. The payable related to this accrued interest was EUR <2,590,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 70,000 loss.

- The bond coupon was paid using the amount received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,533,000. The receivable related to this accrued interest was EUR 2,590,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 70,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,173,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X1

The accrued interest of the bond was EUR <2,305,000>. The payable related to this accrued interest was EUR <2,328,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 3,530,000 loss, fully deemed to be effective.

- The accrual of the USD leg of the CCS was EUR 2,305,000. The receivable related to this accrued interest was EUR 2,328,000.

- The accrual of the EUR leg was EUR <1,968,000>.

- The change in fair value of the CCS produced a EUR 3,758,000 gain, of which EUR 3,530,000 was deemed to be effective and EUR 228,000 ineffective.

- Journal entries on 15 July 20X2

The accrued interest of the bond was EUR <2,707,000>. The payable related to this accrued interest was EUR <2,722,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 19,000 loss.

- The bond coupon was paid using the USD amounts received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,707,000. The receivable related to this accrued interest was EUR 2,722,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 19,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,282,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X2

The accrued interest of the bond was EUR <2,472,000>. The payable related to this accrued interest was EUR <2,510,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 4,552,000 loss, fully deemed to be effective.

- The accrual of the USD leg of the CCS was EUR 2,472,000. The receivable related to this accrued interest was EUR 2,510,000.

- The accrual of the EUR leg was EUR <2,043,000>.

- The change in fair value of the CCS produced a EUR 4,871,000 gain, of which EUR 4,552,000 was deemed to be effective and EUR 319,000 ineffective.

- Journal entries on 15 July 20X3

The accrued interest of the bond was EUR <2,979,000>. The payable related to this accrued interest was EUR <3,044,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 114,000 loss.

- The bond coupon and principal were paid/repaid by using the amounts received under the USD leg of the CCS. The bond principal represented EUR 90,909,000 (= USD 100 mn/1.1000).

- The accrued interest of the USD leg was EUR 2,979,000. The receivable related to this accrued interest was EUR 3,044,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 114,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,369,000>.

- The interest payable corresponding to the EUR leg was paid.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 3,836,000 loss, fully deemed to be effective.

- The change in fair value of the CCS produced a EUR 4,116,000 gain, of which EUR 3,836,000 was deemed to be effective and EUR 280,000 ineffective.

- The CCS notionals were exchanged. ABC paid EUR 80 million and received USD 100 million (worth EUR 90,909,000). The difference was worth EUR 10,909,000 (=90,909,000 – 80,000,000).

- The remaining EUR 1,094,000 fair value adjustments related to the bond were amortised to profit or loss.

The following table gives a summary of the accounting entries:

| Cash | Interest receivable | Derivative contract | Financial debt | Interest payable | Profit or loss | |

| 15-Jul-X0 | ||||||

| Bond issuance | 80,000,000 | 80,000,000 | ||||

| 31-Dec-X0 | ||||||

| Bond accrued coupon | 2,164,000 | <2,164,000> | ||||

| Hedged item revaluation | <2,103,000> | 2,103,000 | ||||

| CCS accrual USD leg | 2,164,000 | 2,164,000 | ||||

| CCS accrual EUR leg | 1,874,000 | <1,874,000> | ||||

| CCS revaluation | <1,836,000> | <1,836,000> | ||||

| 15-Jul-X1 | ||||||

| Bond accrued coupon | 2,590,000 | <2,590,000> | ||||

| Bond accrual retranslation | 70,000 | <70,000> | ||||

| Bond coupon payment | <4,824,000> | <4,824,000> | ||||

| CCS accrual USD leg | 2,590,000 | 2,590,000 | ||||

| CCS interest receivable retranslation | 70,000 | 70,000 | ||||

| CCS USD leg receipt | 4,824,000 | <4,824,000> | ||||

| CCS accrual EUR leg | 2,173,000 | <2,173,000> | ||||

| CCS EUR leg payment | <4,047,000> | <4,047,000> | ||||

| 31-Dec-X1 | ||||||

| Bond accrued coupon | 2,328,000 | <2,328,000> | ||||

| Hedged item revaluation | 3,530,000 | <3,530,000> | ||||

| CCS accrual USD leg | 2,328,000 | 2,328,000 | ||||

| CCS accrual EUR leg | 1,968,000 | <1,968,000> | ||||

| CCS revaluation | 3,758,000 | 3,758,000 | ||||

| 15-Jul-X2 | ||||||

| Bond accrued coupon | 2,722,000 | <2,722,000> | ||||

| Bond accrual retranslation | 19,000 | <19,000> | ||||

| Bond coupon payment | <5,069,000> | <5,069,000> | ||||

| CCS accrual USD leg | 2,722,000 | 2,722,000 | ||||

| CCS interest receivable retranslation | 19,000 | 19,000 | ||||

| CCS USD leg receipt | 5,069,000 | <5,069,000> | ||||

| CCS accrual EUR leg | 2,282,000 | <2,282,000> | ||||

| CCS EUR leg payment | <4,250,000> | <4,250,000> | ||||

| 31-Dec-X2 | ||||||

| Bond accrued coupon | 2,510,000 | <2,510,000> | ||||

| Hedged item revaluation | 4,552,000 | <4,552,000> | ||||

| CCS accrual USD leg | 2,510,000 | 2,510,000 | ||||

| CCS accrual EUR leg | 2,043,000 | <2,043,000> | ||||

| CCS revaluation | 4,871,000 | 4,871,000 | ||||

| 15-Jul-X3 | ||||||

| Bond accrued coupon | 3,044,000 | <3,044,000> | ||||

| Bond accrual retranslation | 114,000 | <114,000> | ||||

| Bond coupon payment | <96,577,000> | <90,909,000> | <5,668,000> | |||

| CCS accrual USD leg | 3,044,000 | 3,044,000 | ||||

| CCS interest receivable retranslation | 114,000 | 114,000 | ||||

| CCS USD leg receipt | 5,668,000 | <5,668,000> | ||||

| CCS accrual EUR leg | 2,369,000 | <2,369,000> | ||||

| CCS EUR leg payment | <4,412,000> | <4,412,000> | ||||

| Hedged item revaluation | 3,836,000 | <3,836,000> | ||||

| CCS revaluation | 4,116,000 | 4,116,000 | ||||

| CCS exchange | 10,909,000 | <10,909,000> | ||||

| Fair value amortisation | 1,094,000 | <1,094,000> | ||||

| <12,709,000> | -0- | -0- | -0- | -0- | <12,709,000> |

8.1.8 Concluding Remarks

ABC's objective when entering into the combination of the bond and the CCS was to incur an expense representing Euribor 12-month plus 0.49%.

During the first year of the term of the bond (and of the hedging relationship) the overall impact of the strategy on profit or loss was a EUR 3,780,000 expense. The target expense during the first year was EUR 4,047,000 (=80 mn × (4.50% + 0.49%) × 365/360), corresponding to a 4.50% Euribor 12-month rate. The difference was due to the EUR 267,000 ineffective part of the change in fair value of the hedged item. Nonetheless, the net cash outflow was exactly EUR 4,047,000.

During the second year the overall impact of the strategy on profit or loss was a EUR 4,022,000 expense. The target expense during the second year was EUR 4,250,000 (=80 mn × (4.75% + 0.49%) × 365/360), corresponding to a 4.75% Euribor 12-month rate. The difference was due to the EUR 228,000 ineffective part of the change in fair value of the CCS. However, the net cash outflow was exactly EUR 4,250,000.

During the third year the overall impact of the strategy on profit or loss was a EUR 4,907,000 expense. The target expense during the third year was EUR 4,412,000 (=80 mn × (4.95% + 0.49%) × 365/360), corresponding to a 4.95% Euribor 12-month rate. The EUR 495,000 (=1,094,000 – 599,000) difference was due to the EUR 599,000 ineffective part of the change in fair value of the CCS and the EUR 1,094,000 amortisation of the fair value. Nonetheless, the net cash outflow was exactly EUR 4,412,000.

The sum of the interest expense over the three years equalled the sum of the three expense targets. Therefore over the three years, both from a cash and expense perspective, ABC achieved its objective of funding itself at Euribor 12-month plus 0.49%.

Finally, note that in our case the basis of the CCS was included in the hedging relationship. The full fair value movement of the CCS, including the basis component, was taken into account in the calculation of the effective part of the hedge. As a consequence, a volatile behaviour of the basis could have created substantial ineffectiveness. Similarly to the treatment of forward components of forward contracts, when the basis component of a CCS is excluded from a hedging relationship, IFRS 9 allows the choice between:

- recognising in profit or loss the change in the basis element fair value; and

- recognising changes in the basis element fair value in OCI to the extent that it relates to the hedged item, while amortising the initial basis element in profit or loss.

8.2 CASE STUDY: HEDGING A FIXED RATE FOREIGN CURRENCY LIABILITY WITH A RECEIVE-FIXED PAY-FLOATING CROSS-CURRENCY SWAP

This case study illustrates the accounting treatment of a fair value hedge of a fixed rate foreign currency financing with a pay-floating receive-fixed CCS.

8.2.1 Background Information

On 15 July 20X0, ABC issued a USD-denominated floating rate bond. ABC's functional currency was the EUR. The bond had the following main terms:

| Bond terms | |

| Issue date | 15 July 20X0 |

| Maturity | 3 years (15 July 20X3) |

| Notional | USD 100 million |

| Coupon | 6.09% annually, actual/360 basis |

Since ABC's objective was to raise EUR floating funding, on the issue date ABC entered into a CCS. Through the CCS, the entity agreed to receive a USD fixed rate equal to the bond coupon and pay a Euribor floating rate plus a spread. The CCS had the following terms:

| Cross-currency swap terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | Euribor 12M + 49 bps annually, actual/360 basis, on the EUR nominal. Euribor is fixed two business days prior to the beginning of each annual interest period |

| ABC receives | 6.09% annually, actual/360 basis |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The mechanics of the CCS are described next. It can be seen that through the combination of the USD bond and the CCS, ABC synthetically obtained a EUR floating liability.

On the issue date at the start of the CCS, there was an initial exchange of nominal amounts through the CCS: ABC delivered the USD 100 million debt issuance proceeds and received EUR 80 million. The resulting EUR–USD exchange rate was 1.2500. The combination of the bond and CCS had the same effect as if ABC had issued a EUR-denominated bond, as shown in Figure 8.4.

Figure 8.4 Bond and CCS combination – initial cash flows.

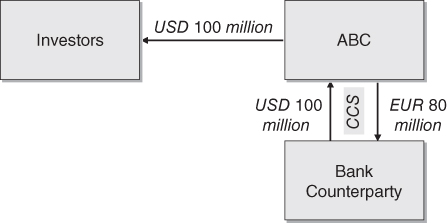

An exchange of interest payments took place annually. ABC received USD 6.09% interest on the USD nominal and paid Euribor-linked interest on the EUR nominal. ABC used the USD fixed cash flows it received under the CCS to pay the bond interest. Figure 8.5 shows the strategy's intermediate cash flows.

Figure 8.5 Bond and CCS combination – intermediate cash flows.

On maturity of the CCS and the debt, ABC re-exchanged the CCS nominals, using the USD 100 million it received through the CCS to redeem the bond issue, and delivering EUR 80 million to the CCS counterparty. Note that this final exchange was made at exactly the same rate used in the initial exchange (1.2500). Figure 8.6 shows the strategy's cash flows at maturity.

Figure 8.6 Bond and CCS combination – final cash flows.

ABC designated the CCS as the hedging instrument in a fair value hedge of the exchange rate and interest rate risks (see Section 8.1.2 for a discussion of the risk components of the bond). Credit risk was excluded from the hedging relationship. Therefore, fair valuations of the hedged item would assume that the initial credit margin of 50 basis points remained unchanged during the term of the hedge.

When assessing effectiveness and calculating effective and ineffective amounts, the helpful simplification of a hypothetical derivative could not be used for fair value hedges. Therefore ABC needed to fair value the hedged item.

8.2.2 Hedging Relationship Documentation

ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to reduce the variability of the fair value of a foreign currency denominated fixed rate bond issued by the entity. This hedging objective is consistent with the group's overall interest rate risk management strategy of transforming all new issued foreign-denominated debt into floating rate, and thereafter managing the exposure to interest rate risk through the proportion of fixed and floating rate net debt in its total debt portfolio. Exchange rate and interest rate risk. The designated risk being hedged is the risk of changes in the EUR fair value of the hedged item attributable to changes in the EUR–USD exchange rate and USD Libor interest rates. Fair value changes attributable to credit or other risks are not hedged in this relationship. Accordingly, the 50 bps credit spread is excluded from the hedging relationship |

| Type of hedge | Fair value hedge |

| Hedged item | The coupons and principal of the 3-year USD floating rate bond with reference number 678902. The main terms of the bond are a USD 100 million principal and an annual coupon of 6.09% calculated on the principal |

| Hedging instrument | The cross-currency swap with reference number 014569. The main terms of the CCS are a USD 100 million nominal, a EUR 80 million nominal, a 3-year maturity, a USD annual interest of 6.09% on the USD nominal to be received by the entity and a EUR annual interest of Euribor 12-month rate plus 0.49% on the EUR nominal to be paid by the entity. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

8.2.3 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument to changes in the fair value of the hedged item. Changes in the fair value of the hedging instrument (i.e., the CCS) will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in profit or loss, adjusting interest income/expense.

- The ineffective part of the gain or loss on the hedging instrument will be recognised in profit or loss, as other financial income/expenses.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is an already recognised liability that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative that does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a quantitative basis using the scenario analysis method for two scenarios:

- In a first scenario, USD Libor interest rates will be shifted upwards by 2%, the EUR–USD exchange rate increased by 10%, and the changes in fair value of the hedged item and the hedging instrument compared.

- In a second scenario, USD Libor interest rates will be shifted downwards by 2%, the EUR–USD exchange rate reduced by 10%, and the changes in fair value of the hedged item and the hedging instrument compared.

8.2.4 Hedge Effectiveness Assessment Performed at the Start of the Hedging Relationship

On 15 July 20X0 ABC performed a hedge effectiveness assessment which was documented as described next.

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the quantitative assessment performed, the entity concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

A quantitative assessment was performed to support the conclusion that the hedging instrument and the hedged item had values that would generally move in opposite directions. The quantitative assessment consisted of two scenario analyses performed as follows.

A parallel shift of +2% in the USD Libor interest rate and +10% in the EUR–USD spot rate, occurring simultaneously on the assessment date, was simulated. The fair values of the hedging instrument and the hedged item were calculated and compared to their initial fair values. As shown in the table below, the assessment resulted in a high degree of offset, corroborating that both elements had values that would generally move in opposite directions.

| Scenario 1 analysis assessment | ||

| Hedging instrument | Hedged item | |

| Initial fair value | -0- | <81,102,000> |

| Final fair value | <11,168,000> | <69,877,000> |

| Cumulative fair value change | <11,168,000> | 11,225,000 |

| Degree of offset | 99.5% | |

Similarly, a parallel shift of –2% the USD Libor interest rate and –10% in the EUR–USD spot rate, occurring simultaneously on the assessment date, was simulated. As shown in the table below, the assessment resulted in a high degree of offset, corroborating that both elements had values that would generally move in opposite directions.

| Scenario 2 analysis assessment | ||

| Hedging instrument | Hedged item | |

| Initial fair value | -0- | <81,102,000> |

| Final fair value | 14,070,000 | <95,104,000> |

| Cumulative fair value change | 14,070,000 | <14,102,000> |

| Degree of offset | 99.8% | |

The following potential sources of ineffectiveness were identified:

- a substantial deterioration in credit risk of either the entity or the counterparty to the hedging instrument; and

- a change in the timing or amounts of the hedged highly expected cash flows.

The hedge ratio was set at 1:1.

ABC also performed assessments at each reporting date, yielding similar conclusions. These assessments have been omitted to avoid unnecessary repetition.

8.2.5 Fair Valuations, Effective/Ineffective Amounts and Cash Flow Calculations

Fair Valuations of the Hedged Item

When calculating the fair value of the hedged item it is important to remember that credit risk was excluded from the hedging relationship. As a result, the expected cash flows were discounted using the USD Libor curve flat (i.e., without any credit spread). Otherwise, large inefficiencies may arise. The fair value of the hedged item on 15 July 20X0 was calculated as follows:

| Hedged item fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied USD Libor (1) | Discount factor (2) | Expected cash flow (3) | Present value (4) | |

| 15-Jul-X1 | 5.40% | 0.9481 | <6,175,000> | <5,855,000> | |

| 15-Jul-X2 | 5.60% | 0.8972 | <6,175,000> | <5,540,000> | |

| 15-Jul-X3 | 5.78% | 0.8475 | <106,175,000> | <89,983,000> | |

| USD fair value | <101,378,000> | ||||

| EUR–USD spot | 1.2500 (5) | ||||

| EUR fair value | <81,102,000> | ||||

Notes:

(1) The implied USD Libor rate. For example, 5.40% was the USD Libor 12M rate set on 13-Jul-X0, and 5.60% and 5.78% were the USD Libor 12M rate expected to be set on 13-Jul-X1 and 13-Jul-X2 respectively

(2) The discount factor from the cash flow date to the valuation date. For example, 0.9481 was calculated as 1/(5.40% × 365/360), 365 being the number of calendar days from the valuation date to 15-Jul-X1

(3) The expected cash flow to be paid on such date. For example, <6,175,000> was calculated as <100 mn> × 6.09% × 365/360, 365 being the number of calendar days in the interest period

(4) Expected cash flow × Discount factor

(5) EUR–USD spot rate on valuation date

The fair value of the hedged item on 31 December 20X0 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Expected cash flow | Present value | |

| 15-Jul-X1 | 5.50% (1) | 0.9709 (2) | <3,316,000> (3) | <3,220,000> | |

| 15-Jul-X2 | 5.75% | 0.9174 | <6,175,000> | <5,665,000> | |

| 15-Jul-X3 | 5.85% | 0.8660 | <106,175,000> | <91,948,000> | |

| USD fair value | <100,833,000> | ||||

| EUR–USD spot | 1.2800 | ||||

| EUR fair value | <78,776,000> | ||||

Notes:

(1) The implied USD Libor rate from 31-Dec-X0 to 15-Jul-X1

(2) 1/(5.50% × 196/360), 196 being the number of calendar days from the valuation date (31-Dec-X0) to 15-Jul-X1

(3) <100 mn> × 6.09% × 196/360, where 6.09% was bond's the fixed rate and 196 was the number of calendar days from the valuation date (31-Dec-X0) to 15-Jul-X1

The fair value of the hedged item on 31 December 20X1 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Expected cash flow | Present value | |

| 15-Jul-X2 | 5.65% | 0.9702 | <3,316,000> | <3,217,000> | |

| 15-Jul-X3 | 5.90% | 0.9154 | <106,175,000> | <97,193,000> | |

| USD fair value | <100,410,000> | ||||

| EUR–USD spot | 1.2200 | ||||

| EUR fair value | <82,303,000> | ||||

The fair value of the hedged item on 31 December 20X2 was calculated as follows:

| Hedged item fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Expected cash flow | Present value | |

| 15-Jul-X3 | 5.90% | 0.9689 | <103,316,000> | <100,103,000> | |

| USD fair value | <100,103,000> | ||||

| EUR–USD spot | 1.1500 | ||||

| EUR fair value | <87,046,000> | ||||

The fair value of the hedged item on 15 July 20X3 was calculated as follows:

| Hedged item fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied USD Libor | Discount factor | Expected cash flow | Present value | |

| 15-Jul-X3 | — | 1.0000 | <100,000,000> | <100,000,000> | |

| USD fair value | <100,000,000> | ||||

| EUR–USD spot | 1.1100 | ||||

| EUR fair value | <90,909,000> | ||||

Fair Valuations of the Hedging Instrument

The fair value of the hedging instrument on 15 July 20X0 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 6,175,000 | 5,855,000 | |

| 31-Jul-X2 | 5.60% | 0.8972 | 6,175,000 | 5,540,000 | |

| 31-Jul-X3 | 5.78% | 0.8475 | 106,175,000 | 89,983,000 | |

| Total USD | 101,378,000 | ||||

| Total EUR (1.2500) | 81,102,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 0.49% | <4,047,000> | <3,871,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 0.49% | <4,218,000> | <3,850,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 0.49% | <84,364,000> | <73,371,000> |

| Total EUR | <81,092,000> | ||||

| Fair value (before adjustments) | 10,000 | ||||

| Adjustments (CVA/DVA and basis) | <10,000> | ||||

| Fair value (including adjustments) | -0- | ||||

It can be observed that the valuations of the USD leg of the CCS and of the hedged item were of opposite sign. The expected cash flow of the EUR leg was calculated as EUR 80 mn × (Euribor 12M + 0.49%) × Days/360, where Days was the number of days in the interest period.

The fair value of the hedging instrument on 31 December 20X0 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 3,316,000 | 3,220,000 | |

| 31-Jul-X2 | 5.75% | 0.9174 | 6,175,000 | 5,665,000 | |

| 31-Jul-X3 | 5.85% | 0.8660 | 106,175,000 | 91,948,000 | |

| Total USD | 100,833,000 | ||||

| Total EUR (1.2800) | 78,776,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 0.49% | <2,173,000> | <2,120,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 0.49% | <4,291,000> | <3,992,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 0.49% | <84,412,000> | <74,772,000> |

| Total EUR | <80,884,000> | ||||

| Fair value (before adjustments) | <2,108,000> | ||||

| Adjustments (CVA/DVA and basis) | 63,000> | ||||

| Fair value (including adjustments) | <2,045,000> | ||||

The fair value of the hedging instrument on 31 December 20X1 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 3,316,000 | 3,217,000 | |

| 31-Jul-X3 | 5.90% | 0.9154 | 106,175,000 | 97,193,000 | |

| Total USD | 100,410,000 | ||||

| Total EUR (1.2200) | 82,303,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 0.49% | <2,282,000> | <2,224,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 0.49% | <84,412,000> | <78,326,000> |

| Total EUR | <80,550,000> | ||||

| Fair value (before adjustments) | 1,753,000 | ||||

| Adjustments (CVA/DVA and basis) | <44,000> | ||||

| Fair value (including adjustments) | 1,709,000 | ||||

The fair value of the hedging instrument on 31 December 20X2 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 103,316,000 | 100,103,000 | |

| Total USD | 100,103,000 | ||||

| Total EUR (1.1500) | 87,046,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 0.49% | <82,369,000> | <80,211,000> |

| Total EUR | <80,211,000> | ||||

| Fair value (before adjustments) | 6,835,000 | ||||

| Adjustments (CVA/DVA and basis) | <68,000> | ||||

| Fair value (including adjustments) | 6,767,000 | ||||

The fair value of the hedging instrument on 15 July 20X3 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | 100,000,000 | 100,000,000 | |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | <80,000,000> | <80,000,000> | |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Effective and Ineffective Amounts

The following table summarises the period changes in the fair value of the hedged item and the hedging instrument:

| Hedging instrument | Hedged item | |||

| Fair value | Period change | Fair value | Period change | |

| 15-Jul-X0 | -0- | — | <81,102,000> | — |

| 31-Dec-X0 | <2,045,000> | <2,045,000> | <78,776,000> | 2,326,000 |

| 31-Dec-X1 | 1,709,000 | 3,754,000 | <82,303,000> | <3,527,000> |

| 31-Dec-X2 | 6,767,000 | 5,058,000 | <87,046 ,000> | <4,743,000> |

| 15-Jul-X3 | 10,909,000 | 4,142,000 | <90,909,000> | <3,863,000> |

On each valuation date, the effective part was the lower of the two period fair value changes (taking into account their opposing signs) and the ineffective part was any remainder.

| Hedging instrument | Hedged item | |||||

| Period change | Effective part | Ineffective part | Period change | Effective part | Ineffective part | |

| 31-Dec-X0 | <2,045,000> | <2,045,000> | -0- | 2,326,000 | 2,045,000 | 281,000 |

| 31-Dec-X1 | 3,754,000 | 3,527,000 | 227,000 | <3,527,000> | <3,527,000> | -0- |

| 31-Dec-X2 | 5,058,000 | 4,743,000 | 315,000 | <4,743,000> | <4,743,000> | -0- |

| 15-Jul-X3 | 4,142,000 | 3,863,000 | 279,000 | <3,863,000> | <3,863,000> | -0- |

Accruals and Payable/Receivable Amounts

The following table summarises the accruals and payables related to the bond:

| Average EUR–USD | Spot EUR–USD | EUR coupon accrual (1) | EUR payable amount (2) | Retranslation payable (3) | |

| 31-Dec-X0 | 1.2630 | 1.2800 | <2,264,000> | <2,234,000> | |

| 15-Jul-X1 | 1.2680 | 1.2400 | <2,615,000> | <2,674,000> | <72,000> |

| 31-Dec-X1 | 1.2320 | 1.2200 | <2,321,000> | <2,343,000> | |

| 15-Jul-X2 | 1.2170 | 1.2100 | <2,725,000> | <2,740,000> | <19,000> |

| 31-Dec-X2 | 1.1680 | 1.1500 | <2,448,000> | <2,486,000> | |

| 15-Jul-X3 | 1.1240 | 1.1000 | <2,950,000> | <3,015,000> | <113,000> |

Notes:

(1) USD 100 mn × 6.09% × (Days/360)/Average EUR–USD, where Days was the number of calendar days in the accrual period (i.e., 169 for accrual periods ending on 31 December and 196 for accrual periods ending on 15 July)

(2) USD 100 mn × 6.09% × (Days/360)/Spot EUR–USD

(3) USD payable amount × (1/previous Spot EUR–USD – 1/current Spot EUR–USD), where USD payable amount was the USD 100 mn × 6.09% × Days/360 corresponding to the previous accrual period

There was no need to retranslate into EUR the USD carrying amount of the bond, as it was already included in the fair valuation of the hedged item. Otherwise a double counting would occur.

The accruals and payables related to the USD leg of the CCS were identical to those of the bond, but with opposite sign. The following table summarises the accruals and payables related to the EUR leg of the CCS:

| CCS EUR leg accruals and payables | ||||

| Euribor 12M | Days | EUR leg accrual (*) | Payable amount | |

| 31-Dec-X0 | 4.50% | 169 | 1,874,000 | 1,874,000 |

| 15-Jul-X1 | 4.50% | 196 | 2,173,000 | 2,173,000 |

| 31-Dec-X1 | 4.75% | 169 | 1,968,000 | 1,968,000 |

| 15-Jul-X2 | 4.75% | 196 | 2,282,000 | 2,282,000 |

| 31-Dec-X2 | 4.95% | 169 | 2,043,000 | 2,043,000 |

| 15-Jul-X3 | 4.95% | 196 | 2,369,000 | 2,369,000 |

(*) 100 mn × (Euribor 12M + 0.49%) × Days/360, where Days was the number of calendar days in the accruing period

Note on Fair Value Adjustments and Translation

The bond was recognised at amortised cost. As the bond was issued at par, the initial effective interest rate was 6.09%. ABC chose to start amortising fair value adjustments when hedge accounting ceased, avoiding having to recalculate the effective interest rate each time a fair value adjustment was performed. Accordingly, the bond's effective interest rate remained 6.09% during the hedging relationship term. See comments in Section 8.1.6.

Regarding the translation of the carrying amount and the fair value adjustments, the fair valuations of the hedged item for the risk being hedged were performed in EUR. Therefore, these fair valuations already included the translation into EUR of both the amortised cost amount and the fair value adjustments.

8.2.6 Accounting Entries

The required journal entries were as follows.

- Journal entries on 15 July 20X0

The bond was issued.

- No entries were required to record the CCS as its initial fair value was zero.

- Journal entries on 31 December 20X0

The accrued interest of the bond was EUR <2,264,000>. The payable related to this accrued interest was EUR <2,234,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 2,326,000 gain, of which EUR 2,045,000 was deemed to be effective and EUR 281,000 ineffective.

- The accrual of the USD leg of the CCS was EUR 2,264,000. The receivable related to this accrued interest was EUR 2,234,000.

- The accrual of the EUR leg of the CCS was EUR <1,874,000>.

- The change in fair value of the CCS produced a EUR 2,045,000 loss, fully deemed to be effective.

- Journal entries on 15 July 20X1

The accrued interest of the bond was EUR <2,615,000>. The payable related to this accrued interest was EUR <2,674,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 72,000 loss.

- The bond coupon was paid using the amount received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,615,000. The receivable related to this accrued interest was EUR 2,674,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 72,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,173,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X1

The accrued interest of the bond was EUR <2,321,000>. The payable related to this accrued interest was EUR <2,343,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 3,527,000 loss, fully deemed to be effective.

- The accrual of the USD leg of the CCS was EUR 2,321,000. The receivable related to this accrued interest was EUR 2,343,000.

- The accrual of the EUR leg of the CCS was EUR <1,968,000>.

- The change in fair value of the CCS produced a EUR 3,754,000 gain, of which EUR 3,527,000 was deemed to be effective and EUR 227,000 ineffective.

- Journal entries on 15 July 20X2

The accrued interest of the bond was EUR <2,725,000>. The payable related to this accrued interest was EUR <2,740,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 19,000 loss.

- The bond coupon was paid using the USD amounts received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,725,000. The receivable related to this accrued interest was EUR 2,740,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 19,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,282,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X2

The accrued interest of the bond was EUR <2,448,000>. The payable related to this accrued interest was EUR <2,486,000>.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 4,743,000 loss, fully deemed to be effective.

- The accrual of the USD leg of the CCS was EUR 2,448,000. The receivable related to this accrued interest was EUR 2,486,000.

- The accrual of the EUR leg was EUR <2,043,000>.

- The change in fair value of the CCS produced a EUR 5,058,000 gain, of which EUR 4,743,000 was deemed to be effective and EUR 315,000 ineffective.

- Journal entries on 15 July 20X3

The accrued interest of the bond was EUR <2,950,000>. The payable related to this accrued interest was EUR <3,015,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 113,000 loss.

- The bond coupon and principal were paid/repaid using the amounts received under the USD leg of the CCS. The bond principal represented EUR 90,909,000 (= USD 100 mn/1.1000).

- The accrued interest of the USD leg was EUR 2,950,000. The receivable related to this accrued interest was EUR 3,015,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 113,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,369,000>.

- The interest payable corresponding to the EUR leg was paid.

- The change in fair value of the hedged item for the risk being hedged produced a EUR 3,863,000 loss, fully deemed to be effective.

- The change in fair value of the CCS produced a EUR 4,142,000 gain, of which EUR 3,863,000 was deemed to be effective and EUR 279,000 ineffective.

- The CCS notionals were exchanged. ABC paid EUR 80 million and received USD 100 million (worth EUR 90,909,000). The difference was worth EUR 10,909,000 (=90,909,000 – 80 mn).

- The remaining EUR 1,102,000 fair value adjustments related to the bond were amortised to profit or loss.

The following table gives a summary of the accounting entries:

| Cash | Interest receivable | Derivative contract | Financial debt | Interest payable | Profit or loss | |

| 15-Jul-X0 | ||||||

| Bond issuance | 80,000,000 | 80,000,000 | ||||

| 31-Dec-X0 | ||||||

| Bond accrued coupon | 2,234,000 | <2,234,000> | ||||

| Hedged item revaluation | <2,326,000> | 2,326,000 | ||||

| CCS accrual USD leg | 2,234,000 | 2,234,000 | ||||

| CCS accrual EUR leg | 1,874,000 | <1,874,000> | ||||

| CCS revaluation | <2,045,000> | <2,045,000> | ||||

| 15-Jul-X1 | ||||||

| Bond accrued coupon | 2,674,000 | <2,674,000> | ||||

| Bond accrual retranslation | 72,000 | <72,000> | ||||

| Bond coupon payment | <4,980,000> | <4,980,000> | ||||

| CCS accrual USD leg | 2,674,000 | 2,674,000 | ||||

| CCS interest receivable retranslation | 72,000 | 72,000 | ||||

| CCS USD leg receipt | 4,980,000 | <4,980,000> | ||||

| CCS accrual EUR leg | 2,173,000 | <2,173,000> | ||||

| CCS EUR leg payment | <4,047,000> | <4,047,000> | ||||

| 31-Dec-X1 | ||||||

| Bond accrued coupon | 2,343,000 | <2,343,000> | ||||

| Hedged item revaluation | 3,527,000 | <3,527,000> | ||||

| CCS accrual USD leg | 2,343,000 | 2,343,000 | ||||

| CCS accrual EUR leg | 1,968,000 | <1,968,000> | ||||

| CCS revaluation | 3,754,000 | 3,754,000 | ||||

| 15-Jul-X2 | ||||||

| Bond accrued coupon | 2,740,000 | <2,740,000> | ||||

| Bond accrual retranslation | 19,000 | <19,000> | ||||

| Bond coupon payment | <5,102,000> | <5,102,000> | ||||

| CCS accrual USD leg | 2,740,000 | 2,740,000 | ||||

| CCS interest receivable retranslation | 19,000 | 19,000 | ||||

| CCS USD leg receipt | 5,102,000 | <5,102,000> | ||||

| CCS accrual EUR leg | 2,282,000 | <2,282,000> | ||||

| CCS EUR leg payment | <4,250,000> | <4,250,000> | ||||

| 31-Dec-X2 | ||||||

| Bond accrued coupon | 2,486,000 | <2,486,000> | ||||

| Hedged item revaluation | 4,743,000 | <4,743,000> | ||||

| CCS accrual USD leg | 2,486,000 | 2,486,000 | ||||

| CCS accrual EUR leg | 2,043,000 | <2,043,000> | ||||

| CCS revaluation | 5,058,000 | 5,058,000 | ||||

| 15-Jul-X3 | ||||||

| Bond accrued coupon | 3,015,000 | <3,015,000> | ||||

| Bond accrual retranslation | 113,000 | <113,000> | ||||

| Bond coupon payment | <96,523,000> | <90,909,000> | <5,614,000> | |||

| CCS accrual USD leg | 3,015,000 | 3,015,000 | ||||

| CCS interest receivable retranslation | 113,000 | 113,000 | ||||

| CCS USD leg receipt | 5,614,000 | <5,614,000> | ||||

| CCS accrual EUR leg | 2,369,000 | <2,369,000> | ||||

| CCS EUR leg payment | <4,412,000> | <4,412,000> | ||||

| Hedged item revaluation | 3,863,000 | <3,863,000> | ||||

| CCS revaluation | 4,142,000 | 4,142,000 | ||||

| CCS exchange | 10,909,000 | <10,909,000> | ||||

| Fair value amortisation | 1,102,000 | <1,102,000> | ||||

| <12,709,000> | -0- | -0- | -0- | -0- | <12,709,000> |

8.2.7 Concluding Remarks

ABC's objective when entering into the combination of the bond and the CCS was to incur an expense representing Euribor 12-month plus 0.49%.

During the first year of the term of the bond (and of the hedging relationship) the overall impact of the strategy on profit or loss was a EUR 3,766,000 expense. The target expense during the first year was EUR 4,047,000 (=80 mn × (4.50% + 0.49%) × 365/360), corresponding to a 4.50% Euribor 12-month rate. The difference was due to the EUR 281,000 ineffective part of the change in fair value of the hedged item. Nonetheless, the net cash outflow was exactly EUR 4,047,000.

During the second year the overall impact of the strategy on profit or loss was a EUR 4,023,000 expense. The target expense during the second year was EUR 4,250,000 (=80 mn × (4.75% + 0.49%) × 365/360), corresponding to a 4.75% Euribor 12-month rate. The difference was due to the EUR 227,000 ineffective part of the change in fair value of the CCS. However, the net cash outflow was exactly EUR 4,250,000.

During the third year the overall impact of the strategy on profit or loss was a EUR 4,920,000 expense. The target expense during the third year was EUR 4,412,000 (=80 mn × (4.95% + 0.49%) × 365/360), corresponding to a 4.95% Euribor 12-month rate. The EUR 508,000 (=1,102,000 – 594,000) difference was due to the EUR 594,000 ineffective part of the change in fair value of the CCS and the EUR 1,102,000 amortisation of the fair value. Again, the net cash outflow was exactly EUR 4,412,000.

The sum of the interest expense over the three years equalled the sum of the three expense targets. Therefore over the three years, both from a cash and expense perspective, ABC achieved its objective of funding itself at Euribor 12-month plus 0.49%.

Finally, note that in our case the CCS basis was included in the hedging relationship. The full fair value movement of the CCS, including the basis component, was taken into account in the calculation of the effective part of the hedge. As a consequence, a volatile behaviour of the basis could have created substantial ineffectiveness. Similarly to the treatment of forward components of forward contracts, when the basis component of a CCS is excluded from a hedging relationship, IFRS 9 allows the choice between:

- recognising in profit or loss the change in the basis element fair value; and

- recognising changes in the basis element fair value in OCI to the extent that it relates to the hedged item, while amortising the initial basis element in profit or loss.