8.3 CASE STUDY: HEDGING A FLOATING RATE FOREIGN CURRENCY LIABILITY WITH A RECEIVE-FLOATING PAY-FIXED CROSS-CURRENCY SWAP

This case study illustrates the accounting treatment of a cash flow hedge of a floating rate foreign currency liability with a pay-fixed receive-floating CCS.

8.3.1 Background Information

On 15 July 20X0, ABC issued a USD-denominated floating rate bond. ABC's functional currency was the EUR. The bond had the following main terms:

| Bond terms | |

| Issue date | 15 July 20X0 |

| Maturity | 3 years (15 July 20X3) |

| Notional | USD 100 million |

| Coupon | USD Libor 12M + 0.50% annually, actual/360 basis |

| USD Libor fixing | Libor is fixed 2 days prior to the beginning of each annual interest period |

Since ABC's objective was to raise EUR fixed funding, on the issue date ABC entered into a CCS. Through the CCS, the entity agreed to receive a floating rate equal to the bond coupon and pay a EUR fixed amount. The CCS had the following terms:

| Cross-currency swap terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | 5.19% annually, actual/360 basis, on the EUR nominal |

| ABC receives | USD Libor 12M + 0.50 bps annually, actual/360 basis. Libor is fixed 2 days prior to the beginning of each annual interest period |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The mechanics of the CCS are described next. It can be seen that through the combination of the USD bond and the CCS, ABC synthetically obtained a EUR fixed liability.

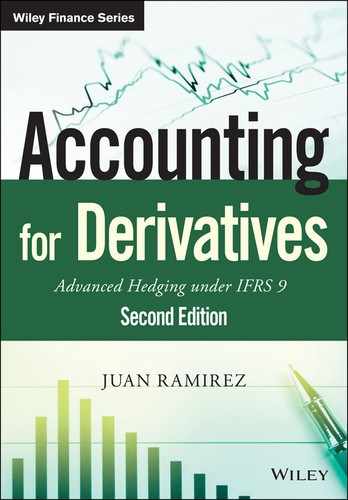

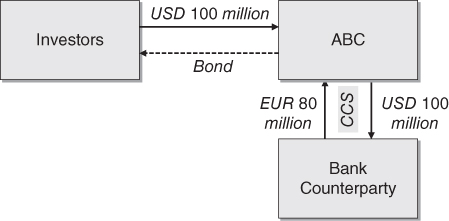

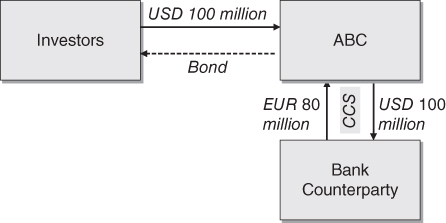

On the issue date at the start of the CCS, there was an initial exchange of nominal amounts through the CCS: ABC delivered the USD 100 million debt issuance proceeds and received EUR 80 million. The resulting EUR–USD exchange rate was 1.2500. The combination of the bond and CCS had the same effect as if ABC had issued a EUR-denominated bond, as shown in Figure 8.7.

Figure 8.7 Bond and CCS combination – initial cash flows.

An exchange of interest payments took place annually. ABC received USD Libor-linked interest on the USD nominal and paid 5.19% interest on the EUR nominal. ABC used the USD Libor cash flows it received under the CCS to pay the bond interest. Figure 8.8 shows the strategy's intermediate cash flows.

Figure 8.8 Bond and CCS combination – intermediate cash flows.

On maturity of the CCS and the debt, ABC re-exchanged the CCS nominals, using the USD 100 million it received through the CCS to redeem the bond issue, and delivering EUR 80 million to the CCS counterparty. Note that this final exchange was made at exactly the same rate used in the initial exchange (1.2500). Figure 8.9 shows the strategy's cash flows at maturity.

Figure 8.9 Bond and CCS combination – final cash flows.

Because the aim of the CCS was to eliminate the EUR variability of the cash flows stemming from the floating rate bond, ABC designated the CCS as the hedging instrument in a cash flow hedge. The exposures being hedged were the bond's interest rate and exchange rate risks. As explained in Section 8.1.2, the bond's credit risk was excluded from the hedging relationship.

ABC used a hypothetical derivative when assessing effectiveness and calculating effective and ineffective amounts, a tool that could be applied for cash flow hedges. Therefore, ABC did not need to fair value the hedged item, fair valuing instead a hypothetical derivative. In my view, in our case it was simpler to fair value the hedged item than to fair value the hypothetical derivative, but I have used the hypothetical derivative approach because it is the approach commonly used by the accounting community for cash flow hedges.

8.3.2 Hedging Relationship Documentation

ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to eliminate variability of the cash flows stemming from the floating rate coupon payments related to a USD-denominated debt instrument issued by the entity, against unfavourable movements in the USD Libor 12-month rate and the EUR–USD exchange rate. This hedging objective is consistent with the group's overall interest rate risk management strategy of transforming with cross-currency swaps all new issued foreign-denominated debt into EUR (either into floating or fixed rate), and thereafter managing the exposure to interest rate risk through the proportion of fixed and floating rate net debt in its total debt portfolio. Exchange rate and interest rate risk. The designated risk being hedged is the risk of changes in the EUR fair value of the hedged item attributable to changes in the EUR–USD exchange rate and USD Libor interest rates. Fair value changes attributable to credit or other risks are not hedged in this relationship |

| Type of hedge | Cash flow hedge |

| Hedged item | The coupons and principal of the 3-year USD floating rate bond with reference number 678902. The main terms of the bond are a USD 100 million principal, an annual coupon of USD Libor plus 0.50% calculated on the principal |

| Hedging instrument | The cross-currency swap with reference number 014577. The main terms of the CCS are a USD 100 million nominal, a EUR 80 million nominal, a 3-year maturity, a USD annual interest of USD Libor 12-month rate plus 0.50% on the USD nominal to be received by the entity and a EUR annual interest of 5.19% on the EUR nominal to be paid by the entity. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

8.3.3 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument to changes in the fair value of a hypothetical derivative. The terms of the hypothetical derivative are such that its fair value changes exactly offset the changes in fair value of the hedged item for the risk being hedged. The hypothetical derivative is a theoretical cross-currency swap with no counterparty credit risk and with zero initial fair value, whose main terms are as follows:

| Hypothetical derivative terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | 5.20% annually, actual/360 basis, on the EUR nominal |

| ABC receives | USD Libor 12M + 0.50 bps annually, actual/360 basis, on the USD nominal. Libor is fixed 2 days prior to the beginning of each annual interest period |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The EUR leg fixed rate of the hypothetical derivative is higher than that of the hedging instrument due to the absence of CVA in the former.

Changes in the fair value of the hedging instrument will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in the cash flow hedge reserve of OCI in equity, after taking into account the bond's retranslation gains/losses. The accumulated amount in equity will be reclassified to profit or loss in the same period during which the hedged expected future cash flow affects profit or loss, adjusting interest expense.

- The ineffective part of the gain or loss on the hedging instrument will be recognised immediately in profit or loss.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a group of highly expected forecast cash flows that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative that does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis by comparing the critical terms (notional, interest periods, underlying and fixed rates) of the hypothetical derivative and the hedging instrument. The assessment will be complemented by a quantitative assessment using the scenario analysis method for one scenario in which USD Libor and Euribor interest rates will be shifted upwards by 2%, the EUR–USD spot rate increased by 10%, and the changes in fair value of the hypothetical derivative and the hedging instrument compared.

8.3.4 Hedge Effectiveness Assessment Performed at the Start of the Hedging Relationship

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the qualitative assessment performed supported by a quantitative analysis, the entity concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

Due to the fact that the terms of the hedging instrument and those of the expected cash flow closely matched and the low credit risk exposure to the counterparty of the cross-currency swap contract, it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions. This conclusion was supported by a quantitative assessment, which consisted of one scenario analysis performed as follows. A parallel shift of +2% in the USD Libor and Euribor interest rates and +10% in the EUR–USD spot rate, occurring on the assessment date, was simulated. The fair values of the hedging instrument and the hypothetical derivatives were calculated and compared to their initial fair values. As shown in the table below, the high degree of offset implied that the change in fair value of the hedged item was expected to be largely offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

| Scenario analysis assessment | ||

| Hedging instrument | Hypothetical derivative | |

| Initial fair value | -0- | -0- |

| Final fair value | <2,999,000> | <3,097,000> |

| Cumulative fair value change | <2,999,000> | <3,097,000> |

| Degree of offset | 96.8% | |

The following potential sources of ineffectiveness were identified:

- a substantial deterioration in credit risk of either the entity or the counterparty to the hedging instrument; and

- a change in the timing or amounts of the hedged highly expected cash flows.

The hedge ratio was set at 1:1.

ABC also performed assessments on each reporting date, yielding the same conclusions. These assessments have been omitted to avoid unnecessary repetition.

8.3.5 Fair Valuations, Effective/Ineffective Amounts and Cash Flow Calculations

Fair Valuations of the Hedging Instrument

The fair value of the hedging instrument on 15 July 20X0 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 0.50% | 5,982,000 | 5,672,000 |

| 31-Jul-X2 | 5.60% | 0.8972 | 0.50% | 6,185,000 | 5,549,000 |

| 31-Jul-X3 | 5.78% | 0.8475 | 0.50% | 106,367,000 | 90,146,000 |

| Total USD | 101,367,000 | ||||

| Total EUR (1.2500) | 81,094,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 5.19% | <4,210,000> | <4,026,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 5.19% | <4,210,000> | <3,843,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 5.19% | <84,210,000> | <73,237,000> |

| Total EUR | <81,106,000> | ||||

| Fair value (before adjustments) | <12,000> | ||||

| Adjustments (CVA/DVA and basis) | 12,000 | ||||

| Fair value (including adjustments) | -0- | ||||

The expected cash flow of the EUR leg was calculated as EUR 80 mn × 5.19% × Days/360, where Days was the number of days in the interest period, and in respect of the 31 July 20X3 cash flow, the EUR 80 million nominal was also added.

The fair value of the hedging instrument on 31 December 20X0 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 0.50% | 3,212,000 | 3,119,000 |

| 31-Jul-X2 | 5.75% | 0.9174 | 0.50% | 6,337,000 | 5,814,000 |

| 31-Jul-X3 | 5.85% | 0.8660 | 0.50% | 106,438,000 | 92,175,000 |

| Total USD | 101,108,000 | ||||

| Total EUR (1.2800) | 78,991,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 5.19% | <2,261,000> | <2,206,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 5.19% | <4,210,000> | <3,917,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 5.19% | <84,210,000> | <74,593,000> |

| Total EUR | <80,716,000> | ||||

| Fair value (before adjustments) | <1,725,000> | ||||

| Adjustments (CVA/DVA and basis) | 52,000> | ||||

| Fair value (including adjustments) | <1,673,000> | ||||

The fair value of the hedging instrument on 31 December 20X1 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 0.50% | 3,294,000 | 3,196,000 |

| 31-Jul-X3 | 5.90% | 0.9154 | 0.50% | 106,489,000 | 97,480,000 |

| Total USD | 100,676,000 | ||||

| Total EUR (1.2200) | 82,521,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 5.19% | <2,261,000> | <2,203,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 5.19% | <84,210,000> | <78,138,000> |

| Total EUR | <80,341,000> | ||||

| Fair value (before adjustments) | 2,180,000 | ||||

| Adjustments (CVA/DVA and basis) | <55,000> | ||||

| Fair value (including adjustments) | 2,125,000 | ||||

The fair value of the hedging instrument on 31 December 20X2 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 0.50% | 103,348,000 | 100,134,000 |

| Total USD | 100,134,000 | ||||

| Total EUR (1.1500) | 87,073,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 5.19% | <82,261,000> | <80,106,000> |

| Total EUR | <80,106,000> | ||||

| Fair value (before adjustments) | 6,967,000 | ||||

| Adjustments (CVA/DVA and basis) | <70,000> | ||||

| Fair value (including adjustments) | 6,897,000 | ||||

The fair value of the hedging instrument on 15 July 20X3 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | 100,000,000 | 100,000,000 |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | <80,000,000> | <80,000,000> |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Fair Valuations of the Hypothetical Derivative

The fair value of the hypothetical derivative on 15 July 20X0 was calculated as follows:

| Hypothetical derivative fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 0.50% | 5,982,000 | 5,672,000 |

| 31-Jul-X2 | 5.60% | 0.8972 | 0.50% | 6,185,000 | 5,549,000 |

| 31-Jul-X3 | 5.78% | 0.8475 | 0.50% | 106,367,000 | 90,146,000 |

| Total USD | 101,367,000 | ||||

| Total EUR (1.2500) | 81,094,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 5.20% | <4,218,000> | <4,034,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 5.20% | <4,218,000> | <3,850,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 5.20% | <84,218,000> | <73,244,000> |

| Total EUR | <81,128,000> | ||||

| Fair value (before adjustments) | <34,000> | ||||

| Adjustments (CVA/DVA and basis) | 34,000 | ||||

| Fair value (including adjustments) | -0- | ||||

The expected cash flow of the EUR leg was calculated as EUR 80 mn × 5.20% × Days/360, where Days was the number of days in the interest period, and in respect of the 31 July 20X3 cash flow, the EUR 80 million nominal was also added.

The fair value of the hypothetical derivative on 31 December 20X0 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 0.50% | 3,212,000 | 3,119,000 |

| 31-Jul-X2 | 5.75% | 0.9174 | 0.50% | 6,337,000 | 5,814,000 |

| 31-Jul-X3 | 5.85% | 0.8660 | 0.50% | 106,438,000 | 92,175,000 |

| Total USD | 101,108,000 | ||||

| Total EUR (1.2800) | 78,991,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 5.20% | <2,265,000> | <2,210,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 5.20% | <4,218,000> | <3,924,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 5.20% | <84,218,000> | <74,600,000> |

| Total EUR | <80,734,000> | ||||

| Fair value (before adjustments) | <1,743,000> | ||||

| Adjustments (CVA/DVA and basis) | 17,000> | ||||

| Fair value (including adjustments) | <1,726,000> | ||||

The fair value of the hypothetical derivative on 31 December 20X1 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 0.50% | 3,294,000 | 3,196,000 |

| 31-Jul-X3 | 5.90% | 0.9154 | 0.50% | 106,489,000 | 97,480,000 |

| Total USD | 100,676,000 | ||||

| Total EUR (1.2200) | 82,521,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 5.20% | <2,265,000> | <2,207,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 5.20% | <84,218,000> | <78,146,000> |

| Total EUR | <80,353,000> | ||||

| Fair value (before adjustments) | 2,168,000 | ||||

| Adjustments (CVA/DVA and basis) | <11,000> | ||||

| Fair value (including adjustments) | 2,157,000 | ||||

The fair value of the hypothetical derivative on 31 December 20X2 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 0.50% | 103,348,000 | 100,134,000 |

| Total USD | 100,134,000 | ||||

| Total EUR (1.1500) | 87,073,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 5.20% | <82,265,000> | <80,110,000> |

| Total EUR | <80,110,000> | ||||

| Fair value (before adjustments) | 6,963,000 | ||||

| Adjustments (CVA/DVA and basis) | <21,000> | ||||

| Fair value (including adjustments) | 6,942,000 | ||||

The fair value of the hypothetical derivative on 15 July 20X3 was calculated as follows:

| Hypothetical derivative fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Spread/ fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | 100,000,000 | 100,000,000 |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | <80,000,000> | <80,000,000> |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Calculation of Effective and Ineffective Amounts

The ineffective part of the change in fair value of the hedging instrument was the excess of its cumulative change in fair value over that of the hypothetical derivative. The fair values of the hedging instrument and the hypothetical derivative at each relevant date were as follows:

| Date | Hedging instrument fair value | Period change | Cumulative change | Hypothetical derivative fair value | Cumulative change |

| 15-Jul-X0 | -0- | — | — | -0- | — |

| 31-Dec-X0 | <1,673,000> | <1,673,000> | <1,673,000> | <1,726,000> | <1,726,000> |

| 31-Dec-X1 | 2,125,000 | <3,798,000> | 2,125,000 | 2,157,000 | 2,157,000 |

| 31-Dec-X2 | 6,897,000 | <4,772,000> | 6,897,000 | 6,942,000 | 6,942,000 |

| 15-Jul-X3 | 10,909,000 | <4,012,000> | 10,909,000 | 10,909,000 | 10,909,000 |

The effective and ineffective parts of the change in fair value of the hedging instrument were the following (see Section 5.5.6 for an explanation of the calculations):

| Effective and ineffective amounts | ||||

| 31-Dec-X0 | 31-Dec-X1 | 31-Dec-X2 | 15-Jul-X3 | |

| Cumulative change in fair value of hedging instrument | <1,673,000> | 2,125,000 | 6,897,000 | 10,909,000 |

| Cumulative change in fair value of hypothetical derivative | <1,726,000> | 2,157,000 | 6,942,000 | 10,909,000 |

| Lower amount | <1,673,000> | 2,125,000 | 6,897,000 | 10,909,000 |

| Previous cumulative effective amount | -0- | <1,673,000> | 2,125,000 | 6,897,000 |

| Available amount | <1,673,000> | 3,798,000 | 4,772,000 | 4,012,000 |

| Period change in fair value of hedging instrument | <1,673,000> | 3,798,000 | 4,772,000 | 4,012,000 |

| Effective part | <1,673,000> | 3,798,000 | 4,772,000 | 4,012,000 |

| Ineffective part | -0- | -0- | -0- | -0- |

Fair value hedges of foreign currency debt were covered in the previous two case studies (see Sections 8.1 and 8.2). Fair value hedges require a fair valuation of the bond (i.e., the hedged item) for the risk(s) being hedged. There was no need to retranslate into EUR the USD carrying amount of the bond, as it was already included in the fair valuation of the hedged item. Otherwise a double counting would occur.

In a cash flow hedge, the recognition of the hedged item is not affected by the application of hedge accounting. Since the foreign currency bond is a monetary item, IAS 21 requires its carrying amount to be retranslated at each reporting date using the spot rate prevailing on such date. The adjustments to the cash flow hedge reserve of equity have to take into account the hedged item retranslation gains or losses. In other words, the effective parts of the hedge are recognised in the cash flow hedge reserve of equity after the hedged item's retranslation gains/losses. The following table summarises the amounts of retranslation gains/losses and the amounts recognised in the cash flow hedge reserve:

| Retranslation gains/losses and amounts in cash flow hedge reserve | ||||

| 31-Dec-X0 | 31-Dec-X1 | 31-Dec-X2 | 15-Jul-X3 | |

| Bond USD carrying amount | 100,000,000 | 100,000,000 | 100,000,000 | 100,000,000 |

| EUR–USD spot rate | 1.28 | 1.22 | 1.15 | 1.10 |

| EUR translated amount | 78,125,000 | 81,967,000 | 86,957,000 | 90.909.000 |

| Retranslation gain/loss | 1,875,000 | <3,842,000> | <4,990,000> | <3,952,000> |

| Effective part | <1,673,000> | 3,798,000 | 4,772,000 | 4,012,000 |

| Difference | 202,000 | <44,000> | <218,000> | 60,000 |

| Amount to be recognised in cash flow hedge reserve | 202,000 | <44,000> | <218,000> | 60,000 |

| Cumulative amounts in cash flow hedge reserve | 202,000 | 158,000 | <60,000> | -0- |

For the sake of clarity, let us look at the 31 December 20X0 figures. The effective part indicated that, in theory, EUR <1,673,000> would be added to the cash flow hedge reserve. However, EUR <1,875,000> was reclassified from this reserve to profit or loss to offset the bond's EUR 1,875,000 retranslation gain. As a result, EUR 202,000 was added to the cash flow hedge reserve on that date.

Accruals and Payable/Receivable Amounts

The following table summarises the accruals and payables related to the bond:

| Bond accruals and payables | ||||||

| USD Libor 12M | Average EUR–USD | Spot EUR–USD | EUR coupon accrual (1) | EUR payable amount (2) | Retranslation payable (3) | |

| 31-Dec-X0 | 5.40% | 1.2630 | 1.2800 | <2,193,000> | <2,164,000> | |

| 15-Jul-X1 | 5.40% | 1.2680 | 1.2400 | <2,533,000> | <2,590,000> | <70,000> |

| 31-Dec-X1 | 5.55% | 1.2320 | 1.2200 | <2,305,000> | <2,328,000> | |

| 15-Jul-X2 | 5.55% | 1.2170 | 1.2100 | <2,707,000> | <2,722,000> | <19,000> |

| 31-Dec-X2 | 5.65% | 1.1680 | 1.1500 | <2,472,000> | <2,510,000> | |

| 15-Jul-X3 | 5.65% | 1.1240 | 1.1000 | <2,979,000> | <3,044,000> | <114,000> |

Notes:

(1) USD 100 mn × (USD Libor 12M + 0.50%) × (Days/360)/Average EUR–USD, where Days was the number of calendar days in the accrual period (i.e., 169 for accrual periods ending on 31 December and 196 for accrual periods ending on 15 July)

(1) USD 100 mn × (USD Libor 12M + 0.50%) × (Days/360)/Spot EUR–USD

(1) USD payable amount × (1/previous Spot EUR–USD – 1/current Spot EUR–USD), where USD payable amount was the USD 100 mn × (USD Libor 12M + 0.50%) × Days/360 corresponding to the previous accrual period

The accruals and payables related to the USD leg of the CCS were identical to those of the bond, but with opposite sign. The following table summarises the accruals and payables related to the EUR leg of the CCS:

| CCS EUR leg accruals and payables | ||||

| Fixed rate | Days | EUR Leg accrual (*) | Payable amount | |

| 31-Dec-X0 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X1 | 5.19% | 196 | 2,261,000 | 2,261,000 |

| 31-Dec-X1 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X2 | 5.19% | 196 | 2,261,000 | 2,261,000 |

| 31-Dec-X2 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X3 | 5.19% | 196 | 2,261,000 | 2,261,000 |

(1) * 100 mn × 5.19% × Days/360, where Days was the number of calendar days in the accruing period

8.3.6 Accounting Entries

The required journal entries were as follows.

- Journal entries on 15 July 20X0

The bond was issued.

- No entries were required to record the CCS as its initial fair value was zero.

- Journal entries on 31 December 20X0

The accrued interest of the bond was EUR <2,193,000>. The payable related to this accrued interest was EUR <2,164,000>.

- The accrual of the USD leg of the CCS was EUR 2,193,000. The receivable related to this accrued interest was EUR 2,164,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 1,875,000 gain. The change in fair value of the CCS produced a EUR 1,673,000 loss, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X1

The accrued interest of the bond was EUR <2,533,000>. The payable related to this accrued interest was EUR <2,590,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 70,000 loss.

- The bond coupon was paid using the amount received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,533,000. The receivable related to this accrued interest was EUR 2,590,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 70,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X1

The accrued interest of the bond was EUR <2,305,000>. The payable related to this accrued interest was EUR <2,328,000>.

- The accrual of the USD leg of the CCS was EUR 2,305,000. The receivable related to this accrued interest was EUR 2,328,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 3,842,000 loss. The change in fair value of the CCS produced a EUR 3,798,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X2

The accrued interest of the bond was EUR <2,707,000>. The payable related to this accrued interest was EUR <2,722,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 19,000 loss.

- The bond coupon was paid using the USD amounts received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,707,000. The receivable related to this accrued interest was EUR 2,722,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 19,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X2

The accrued interest of the bond was EUR <2,472,000>. The payable related to this accrued interest was EUR <2,510,000>.

- The accrual of the USD leg of the CCS was EUR 2,472,000. The receivable related to this accrued interest was EUR 2,510,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 4,990,000 loss. The change in fair value of the CCS produced a EUR 4,772,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X3

The accrued interest of the bond was EUR <2,979,000>. The payable related to this accrued interest was EUR <3,044,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 114,000 loss.

- The bond coupon and principal were paid/repaid using the USD leg amounts. The bond principal represented EUR 90,909,000 (= USD 100 mn/1.1000).

- The accrued interest of the USD leg was EUR 2,979,000. The receivable related to this accrued interest was EUR 3,044,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 114,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 3,952,000 loss. The change in fair value of the CCS produced a EUR 4,012,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- The CCS notionals were exchanged. ABC paid EUR 80 million and received USD 100 million (worth EUR 90,909,000). The difference was worth EUR 10,909,000 (=90,909,000 – 80 mn).

The following table gives a summary of the accounting entries:

| Cash | Interest receivable | Derivative contract | Financial debt | Interest payable | Cash flow hedge reserve | Profit or loss | |

| 15-Jul-X0 | |||||||

| Bond issuance | 80,000,000 | 80,000,000 | |||||

| 31-Dec-X0 | |||||||

| Bond accrued coupon | 2,164,000 | <2,164,000> | |||||

| CCS accrual USD leg | 2,164,000 | 2,164,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | <1,875,000> | 1,875,000 | |||||

| CCS revaluation | <1,673,000> | 202,000 | <1,875,000> | ||||

| 15-Jul-X1 | |||||||

| Bond accrued coupon | 2,590,000 | <2,590,000> | |||||

| Bond accrual retranslation | 70,000 | <70,000> | |||||

| Bond coupon payment | <4,824,000> | <4,824,000> | |||||

| CCS accrual USD leg | 2,590,000 | 2,590,000 | |||||

| CCS interest receivable retranslation | 70,000 | 70,000 | |||||

| CCS USD leg receipt | 4,824,000 | <4,824,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| 31-Dec-X1 | |||||||

| Bond accrued coupon | 2,328,000 | <2,328,000> | |||||

| CCS accrual USD leg | 2,328,000 | 2,328,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | 3,842,000 | <3,842,000> | |||||

| CCS revaluation | 3,798,000 | <44,000> | 3,842,000 | ||||

| 15-Jul-X2 | |||||||

| Bond accrued coupon | 2,722,000 | <2,722,000> | |||||

| Bond accrual retranslation | 19,000 | <19,000> | |||||

| Bond coupon payment | <5,069,000> | <5,069,000> | |||||

| CCS accrual USD leg | 2,722,000 | 2,722,000 | |||||

| CCS interest receivable retranslation | 19,000 | 19,000 | |||||

| CCS USD leg receipt | 5,069,000 | <5,069,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| 31-Dec-X2 | |||||||

| Bond accrued coupon | 2,510,000 | <2,510,000> | |||||

| CCS accrual USD leg | 2,510,000 | 2,510,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | 4,990,000 | <4,990,000> | |||||

| CCS revaluation | 4,772,000 | <218,000> | 4,990,000 | ||||

| 15-Jul-X3 | |||||||

| Bond accrued coupon | 3,044,000 | <3,044,000> | |||||

| Bond accrual retranslation | 114,000 | <114,000> | |||||

| Bond coupon payment | <96,577,000> | <90,909,000> | <5,668,000> | ||||

| CCS accrual USD leg | 3,044,000 | 3,044,000 | |||||

| CCS interest receivable retranslation | 114,000 | 114,000 | |||||

| CCS USD leg receipt | 5,668,000 | <5,668,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| Bond retranslation | 3,952,000 | <3,952,000> | |||||

| CCS revaluation | 4,012,000 | 60,000 | 3,952,000 | ||||

| CCS exchange | 10,909,000 | <10,909,000> | |||||

| <12,630,000> | -0- | -0- | -0- | -0- | -0- | <12,630,000> |

8.3.7 Concluding Remarks

ABC's objective when entering into the combination of the bond and the CCS was to incur an annual expense representing 5.19%, or EUR 4,210,000 (=80 mn × 5.19% × 365/360).

During the first, second and third years of the term of the bond (and of the hedging relationship) the overall impact of the strategy on profit or loss was an annual expense of EUR 4,210,000. The annual net cash outflow was exactly EUR 4,210,000 as well. Therefore, ABC's objective was fully achieved.

This outcome occurred because there were no ineffective amounts. Otherwise, the target still would have been achieved from an annual net cash flow perspective, but not from an annual expense perspective. Even in the presence of inefficiencies, the overall 3-year expense would have been EUR 12,630,000 (=4,210,000 × 3).

As mentioned in the previous case studies, the basis component of the CCS was part of the hedging instrument. A notably volatile behaviour of the basis could have created significant inefficiencies. When the basis component of a CCS is excluded from the hedging instrument, IFRS 9 allows an entity to recognise changes in the fair value of this component either in profit or loss or temporarily in OCI to the extent that those changes relate to the hedged item.

8.4 CASE STUDY: HEDGING A FIXED RATE FOREIGN CURRENCY LIABILITY WITH A RECEIVE-FIXED PAY-FIXED CROSS-CURRENCY SWAP

This case study illustrates the accounting treatment of a cash flow hedge of a fixed rate foreign currency financing with a pay-fixed receive-fixed CCS.

8.4.1 Background Information

On 15 July 20X0, ABC issued a USD-denominated fixed rate bond. ABC's functional currency was the EUR. The bond had the following main terms:

| Bond terms | |

| Issue date | 15 July 20X0 |

| Maturity | 3 years (15 July 20X3) |

| Notional | USD 100 million |

| Coupon | 6.09% annually, actual/360 basis |

Since ABC's objective was to raise EUR fixed funding, on the issue date ABC entered into a CCS. Through the CCS, the entity agreed to receive a fixed rate equal to the bond coupon and pay a EUR fixed amount. The CCS had the following terms:

| Cross-currency swap terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | 5.19% annually, actual/360 basis, on the EUR nominal |

| ABC receives | 6.09% annually, actual/360 basis |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The mechanics of the CCS are described next. It can be seen that through the combination of the USD bond and the CCS, ABC synthetically obtained a EUR fixed liability.

On the issue date at the start of the CCS, there was an initial exchange of nominal amounts through the CCS: ABC delivered the USD 100 million debt issuance proceeds and received EUR 80 million. The resulting EUR–USD exchange rate was 1.2500. The combination of the bond and CCS had the same effect as if ABC had issued a EUR-denominated bond, as shown in Figure 8.10.

Figure 8.10 Bond and CCS combination – initial cash flows.

An exchange of interest payments took place annually. ABC received 6.09% interest on the USD nominal and paid 5.19% interest on the EUR nominal. ABC used the USD cash flows it received under the CCS to pay the bond interest. Figure 8.11 shows the strategy's intermediate cash flows.

Figure 8.11 Bond and CCS combination – intermediate cash flows.

On maturity of the CCS and the debt, ABC re-exchanged the CCS nominals, using the USD 100 million it received through the CCS to redeem the bond issue, and delivering EUR 80 million to the CCS counterparty. Note that this final exchange was made at exactly the same rate used in the initial exchange (1.2500). Figure 8.12 shows the strategy's cash flows at maturity.

Figure 8.12 Bond and CCS combination – final cash flows.

Because the aim of the CCS was to eliminate the EUR variability of the cash flows stemming from the foreign currency fixed rate bond, ABC designated the CCS as the hedging instrument in a cash flow hedge. The exposure being hedged was the bond's exchange rate risks. As explained in Section 8.1.2, the bond's credit risk was excluded from the hedging relationship. Also, because of its fixed rate coupons, the bond did not expose ABC to interest rate risk.

ABC used a hypothetical derivative when assessing effectiveness and calculating effective and ineffective amounts, a tool that could be applied for cash flow hedges. Therefore, ABC did not need to fair value the hedged item, fair valuing instead a hypothetical derivative.

8.4.2 Hedging Relationship Documentation

ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to eliminate variability of the cash flows stemming from the coupon payments related to a USD-denominated debt instrument issued by the entity, against unfavourable movements in the EUR–USD exchange rate. This hedging objective is consistent with the group's overall interest rate risk management strategy of transforming with cross-currency swaps all new issued foreign-denominated debt into EUR (either into fixed or floating rate), and thereafter managing the exposure to interest rate risk through the proportion of fixed and floating rate net debt in its total debt portfolio. Exchange rate risk. The designated risk being hedged is the risk of changes in the EUR value of the cash flows related to the hedged item attributable to changes in the EUR–USD exchange rate. Fair value changes attributable to credit or other risks are not hedged in this relationship |

| Type of hedge | Cash flow hedge |

| Hedged item | The coupons and principal of the 3-year USD floating rate bond with reference number 678902. The main terms of the bond are a USD 100 million principal, an annual coupon of 6.09% calculated on the principal |

| Hedging instrument | The cross-currency swap with reference number 014579. The main terms of the CCS are a USD 100 million nominal, a EUR 80 million nominal, a 3-year maturity, a USD annual interest of 6.09% on the USD nominal to be received by the entity and a EUR annual interest of 5.19% on the EUR nominal to be paid by the entity. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

8.4.3 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument to changes in the fair value of a hypothetical derivative. The terms of the hypothetical derivative are such that its fair value changes exactly offset the changes in fair value of the hedged item for the risk being hedged. The hypothetical derivative is a theoretical cross-currency swap with no counterparty credit risk and with zero initial fair value, whose main terms are as follows:

| Hypothetical derivative terms | |

| Trade date | 15 July 20X0 |

| Start date | 15 July 20X0 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 3 years (15 July 20X3) |

| USD nominal | USD 100 million |

| EUR nominal | EUR 80 million |

| Initial exchange | On start date, ABC receives the EUR nominal and pays the USD nominal |

| ABC pays | 5.20% annually, actual/360 basis, on the EUR nominal |

| ABC receives | 6.09% annually, actual/360 basis, on the USD nominal |

| Final exchange | On maturity date, ABC receives the USD nominal and pays the EUR nominal |

The EUR leg fixed rate of the hypothetical derivative is higher than that of the hedging instrument due to the absence of CVA in the former.

Changes in the fair value of the hedging instrument will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in the cash flow hedge reserve of OCI in equity, after taking into account the bond's retranslation gains/losses. The accumulated amount in equity will be reclassified to profit or loss in the same period during which the hedged expected future cash flow affects profit or loss, adjusting interest expense.

- The ineffective part of the gain or loss on the hedging instrument will be recognised immediately in profit or loss.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a group of highly expected forecast cash flows that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative that does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis by comparing the critical terms (notional, interest periods, underlying and fixed rates) of the hypothetical derivative and the hedging instrument. The assessment will be complemented by a quantitative assessment using the scenario analysis method for one scenario in which the EUR–USD spot rate will be increased by 10%, and the changes in fair value of the hypothetical derivative and the hedging instrument compared.

8.4.4 Hedge Effectiveness Assessment Performed at the Start of the Hedging Relationship

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the qualitative assessment performed supported by a quantitative analysis, the entity concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

Due to the fact that the terms of the hedging instrument and those of the expected cash flow closely matched and the low credit risk exposure to the counterparty of the cross-currency swap contract, it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions. This conclusion was supported by a quantitative assessment, which consisted of one scenario analysis performed as follows. A EUR–USD spot rate increase by 10% occurring on the assessment date was simulated. The fair values of the hedging instrument and the hypothetical derivatives were calculated and compared to their initial fair values. As shown in the table below, the high degree of offset implied that the change in fair value of the hedged item was expected to largely be offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

| Scenario analysis assessment | ||

| Hedging instrument | Hypothetical derivative | |

| Initial fair value | -0- | -0- |

| Final fair value | <7,156,000> | <7,362,000> |

| Cumulative fair value change | <7,156,000> | <7,362,000> |

| Degree of offset | 97.2% | |

The following potential sources of ineffectiveness were identified:

- a substantial deterioration in credit risk of either the entity or the counterparty to the hedging instrument; and

- a change in the timing or amounts of the hedged highly expected cash flows.

The hedge ratio was set at 1:1.

ABC also performed assessments on each reporting date, yielding the same conclusions. These assessments have been omitted to avoid unnecessary repetition.

8.4.5 Fair Valuations, Effective/Ineffective Amounts and Cash Flow Calculations

Fair Valuations of the Hedging Instrument

The fair value of the hedging instrument on 15 July 20X0 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 6.09% | 6,175,000 | 5,855,000 |

| 31-Jul-X2 | 5.60% | 0.8972 | 6.09% | 6,175,000 | 5,540,000 |

| 31-Jul-X3 | 5.78% | 0.8475 | 6.09% | 106,175,000 | 89,983,000 |

| Total USD | 101,378,000 | ||||

| Total EUR (1.2500) | 81,102,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 5.19% | <4,210,000> | <4,026,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 5.19% | <4,210,000> | <3,843,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 5.19% | <84,210,000> | <73,237,000> |

| Total EUR | <81,106,000> | ||||

| Fair value (before adjustments) | <4,000> | ||||

| Adjustments (CVA/DVA and basis) | 4,000 | ||||

| Fair value (including adjustments) | -0- | ||||

The expected cash flow of the USD leg was calculated as USD 100 mn × 6.09% × Days/360, where Days was the number of days in the interest period, and in respect of the 31 July 20X3 cash flow, the USD 100 million nominal was also added.

The expected cash flow of the EUR leg was calculated as EUR 80 mn × 5.19% × Days/360, where Days was the number of days in the interest period, and in respect of the 31 July 20X3 cash flow, the EUR 80 million nominal was also added.

The fair value of the hedging instrument on 31 December 20X0 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 6.09% | 3,316,000 | 3,220,000 |

| 31-Jul-X2 | 5.75% | 0.9174 | 6.09% | 6,175,000 | 5,665,000 |

| 31-Jul-X3 | 5.85% | 0.8660 | 6.09% | 106,175,000 | 91,948,000 |

| Total USD | 100,833,000 | ||||

| Total EUR (1.2800) | 78,776,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 5.19% | <2,261,000> | <2,206,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 5.19% | <4,210,000> | <3,917,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 5.19% | <84,210,000> | <74,593,000> |

| Total EUR | <80,716,000> | ||||

| Fair value (before adjustments) | <1,940,000> | ||||

| Adjustments (CVA/DVA and basis) | 58,000> | ||||

| Fair value (including adjustments) | <1,882,000> | ||||

The fair value of the hedging instrument on 31 December 20X1 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 6.09% | 3,316,000 | 3,217,000 |

| 31-Jul-X3 | 5.90% | 0.9154 | 6.09% | 106,175,000 | 97,193,000 |

| Total USD | 100,410,000 | ||||

| Total EUR (1.2200) | 82,303,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 5.19% | <2,261,000> | <2,203,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 5.19% | <84,210,000> | <78,138,000> |

| Total EUR | <80,341,000> | ||||

| Fair value (before adjustments) | 1,962,000 | ||||

| Adjustments (CVA/DVA and basis) | <49,000> | ||||

| Fair value (including adjustments) | 1,913,000 | ||||

The fair value of the hedging instrument on 31 December 20X2 was calculated as follows:

| Hedging instrument fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 6.09% | 103,316,000 | 100,103,000 |

| Total USD | 100,103,000 | ||||

| Total EUR (1.1500) | 87,046,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 5.19% | <82,261,000> | <80,106,000> |

| Total EUR | <80,106,000> | ||||

| Fair value (before adjustments) | 6,940,000 | ||||

| Adjustments (CVA/DVA and basis) | <69,000> | ||||

| Fair value (including adjustments) | 6,871,000 | ||||

The fair value of the hedging instrument on 15 July 20X3 was calculated as follows:

| Hedging instrument fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | 100,000,000 | 100,000,000 |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | <80,000,000> | <80,000,000> |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Fair Valuations of the Hypothetical Derivative

The fair value of the hypothetical derivative on 15 July 20X0 was calculated as follows:

| Hypothetical derivative fair valuation on 15-Jul-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.40% | 0.9481 | 6.09% | 6,175,000 | 5,855,000 |

| 31-Jul-X2 | 5.60% | 0.8972 | 6.09% | 6,175,000 | 5,540,000 |

| 31-Jul-X3 | 5.78% | 0.8475 | 6.09% | 106,175,000 | 89,983,000 |

| Total USD | 101,378,000 | ||||

| Total EUR (1.2500) | 81,102,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.50% | 0.9564 | 5.20% | <4,218,000> | <4,034,000> |

| 31-Jul-X2 | 4.71% | 0.9128 | 5.20% | <4,218,000> | <3,850,000> |

| 31-Jul-X3 | 4.89% | 0.8697 | 5.20% | <84,218,000> | <73,244,000> |

| Total EUR | <81,128,000> | ||||

| Fair value (before adjustments) | <26,000> | ||||

| Adjustments (CVA/DVA and basis) | 26,000 | ||||

| Fair value (including adjustments) | -0- | ||||

The expected cash flow of the EUR leg was calculated as EUR 80 mn × 5.20% × Days/360, where Days was the number of days in the interest period, and in respect of the 31 July 20X3 cash flow, the EUR 80 million nominal was also added.

The fair value of the hypothetical derivative on 31 December 20X0 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X0 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X1 | 5.50% | 0.9709 | 6.09% | 3,316,000 | 3,220,000 |

| 31-Jul-X2 | 5.75% | 0.9174 | 6.09% | 6,175,000 | 5,665,000 |

| 31-Jul-X3 | 5.85% | 0.8660 | 6.09% | 106,175,000 | 91,948,000 |

| Total USD | 100,833,000 | ||||

| Total EUR (1.2800) | 78,776,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X1 | 4.60% | 0.9756 | 5.20% | <2,265,000> | <2,210,000> |

| 31-Jul-X2 | 4.80% | 0.9303 | 5.20% | <4,218,000> | <3,924,000> |

| 31-Jul-X3 | 4.95% | 0.8858 | 5.20% | <84,218,000> | <74,600,000> |

| Total EUR | <80,734,000> | ||||

| Fair value (before adjustments) | <1,958,000> | ||||

| Adjustments (CVA/DVA and basis) | 20,000> | ||||

| Fair value (including adjustments) | <1,938,000> | ||||

The fair value of the hypothetical derivative on 31 December 20X1 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X1 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X2 | 5.65% | 0.9702 | 6.09% | 3,316,000 | 3,217,000 |

| 31-Jul-X3 | 5.90% | 0.9154 | 6.09% | 106,175,000 | 97,193,000 |

| Total USD | 100,410,000 | ||||

| Total EUR (1.2200) | 82,303,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X2 | 4.80% | 0.9745 | 5.20% | <2,265,000> | <2,207,000> |

| 31-Jul-X3 | 4.95% | 0.9279 | 5.20% | <84,218,000> | <78,146,000> |

| Total EUR | <80,353,000> | ||||

| Fair value (before adjustments) | 1,950,000 | ||||

| Adjustments (CVA/DVA and basis) | <10,000> | ||||

| Fair value (including adjustments) | 1,940,000 | ||||

The fair value of the hypothetical derivative on 31 December 20X2 was calculated as follows:

| Hypothetical derivative fair valuation on 31-Dec-X2 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | 5.90% | 0.9689 | 6.09% | 103,316,000 | 100,103,000 |

| Total USD | 100,103,000 | ||||

| Total EUR (1.1500) | 87,046,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | 4.95% | 0.9738 | 5.20% | <82,265,000> | <80,110,000> |

| Total EUR | <80,110,000> | ||||

| Fair value (before adjustments) | 6,936,000 | ||||

| Adjustments (CVA/DVA and basis) | <21,000> | ||||

| Fair value (including adjustments) | 6,915,000 | ||||

The fair value of the hypothetical derivative on 15 July 20X3 was calculated as follows:

| Hypothetical derivative fair valuation on 15-Jul-X3 | |||||

| Cash flow date | Implied interest rate | Discount factor | Fixed rate | Expected cash flow | Present value |

| Cash flows of USD leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | 100,000,000 | 100,000,000 |

| Total USD | 100,000,000 | ||||

| Total EUR (1.1100) | 90,909,000 | ||||

| Cash flows of EUR leg: | |||||

| 31-Jul-X3 | — | 1.0000 | — | <80,000,000> | <80,000,000> |

| Total EUR | <80,000,000> | ||||

| Fair value (before adjustments) | 10,909,000 | ||||

| Adjustments (CVA/DVA and basis) | -0- | ||||

| Fair value (including adjustments) | 10,909,000 | ||||

Calculation of Effective and Ineffective Amounts

The ineffective part of the change in fair value of the hedging instrument was the excess of its cumulative change in fair value over that of the hypothetical derivative. The fair values of the hedging instrument and the hypothetical derivative at each relevant date were as follows:

| Date | Hedging instrument fair value | Period change | Cumulative change | Hypothetical derivative fair value | Cumulative change |

| 15-Jul-X0 | -0- | — | — | -0- | — |

| 31-Dec-X0 | <1,882,000> | <1,882,000> | <1,882,000> | <1,938,000> | <1,938,000> |

| 31-Dec-X1 | 1,913,000 | 3,795,000 | 1,913,000 | 1,940,000 | 1,940,000 |

| 31-Dec-X2 | 6,871,000 | 4,958,000 | 6,871,000 | 6,915,000 | 6,915,000 |

| 15-Jul-X3 | 10,909,000 | 4,038,000 | 10,909,000 | 10,909,000 | 10,909,000 |

The effective and ineffective parts of the change in fair value of the hedging instrument were the following (see Section 5.5.6 for an explanation of the calculations):

| Effective and ineffective amounts | ||||

| 31-Dec-X0 | 31-Dec-X1 | 31-Dec-X2 | 15-Jul-X3 | |

| Cumulative change in fair value of hedging instrument | <1,882,000> | 1,913,000 | 6,871,000 | 10,909,000 |

| Cumulative change in fair value of hypothetical derivative | <1,938,000> | 1,940,000 | 6,915,000 | 10,909,000 |

| Lower amount | <1,882,000> | 1,913,000 | 6,871,000 | 10,909,000 |

| Previous cumulative effective amount | -0- | <1,882,000> | 1,913,000 | 6,871,000 |

| Available amount | <1,882,000> | 3,795,000 | 4,958,000 | 4,038,000 |

| Period change in fair value of hedging instrument | <1,882,000> | 3,795,000 | 4,958,000 | 4,038,000 |

| Effective part | <1,882,000> | 3,795,000 | 4,958,000 | 4,038,000 |

| Ineffective part | -0- | -0- | -0- | -0- |

Fair value hedges of foreign currency debt were covered in Sections 8.1 and 8.2. Fair value hedges require a fair valuation of the bond (i.e., the hedged item) for the risk(s) being hedged. There was no need to retranslate into EUR the USD carrying amount of the bond, as it was already included in the fair valuation of the hedged item. Otherwise a double counting would occur.

In a cash flow hedge, the recognition of the hedged item is not affected by the application of hedge accounting. Since the foreign currency bond is a monetary item, IAS 21 requires its carrying amount to be retranslated at each reporting date using the spot rate prevailing on such date. The adjustments to the cash flow hedge reserve of equity have to take into account the hedged item retranslation gains or losses. In other words, the effective parts of the hedge are recognised in the cash flow hedge reserve of equity after the hedged item's retranslation gains/losses. The following table summarises the amounts of retranslation gains/losses and the amounts recognised in the cash flow hedge reserve:

| Retranslation gains/losses and amounts in cash flow hedge reserve | ||||

| 31-Dec-X0 | 31-Dec-X1 | 31-Dec-X2 | 15-Jul-X3 | |

| Bond USD carrying amount | 100,000,000 | 100,000,000 | 100,000,000 | 100,000,000 |

| EUR–USD spot rate | 1.28 | 1.22 | 1.15 | 1.10 |

| EUR translated amount | 78,125,000 | 81,967,000 | 86,957,000 | 90.909.000 |

| Retranslation gain/loss | 1,875,000 | <3,842,000> | <4,990,000> | <3,952,000> |

| Effective part | <1,882,000> | 3,795,000 | 4,958,000 | 4,038,000 |

| Difference | <7,000> | <47,000> | <32,000> | 86,000 |

| Amount to be recognised in cash flow hedge reserve | <7,000> | <47,000> | <32,000> | 86,000 |

| Cumulative amounts in cash flow hedge reserve | <7,000> | <54,000> | <86,000> | -0- |

For the sake of clarity, let us look at the 31 December 20X0 figures. The effective part indicated that, in theory, EUR <1,882,000> would be added to the cash flow hedge reserve. However, EUR <1,875,000> was reclassified from this reserve to profit or loss to offset the bond's EUR 1,875,000 retranslation gain. As a result, EUR 7,000 was subtracted from the cash flow hedge reserve on that date.

Accruals and Payable/Receivable Amounts

The following table summarises the accruals and payables related to the bond:

| Average EUR–USD | Spot EUR–USD | EUR coupon accrual (1) | EUR payable amount (2) | Retranslation payable (3) | |

| 31-Dec-X0 | 1.2630 | 1.2800 | <2,264,000> | <2,234,000> | |

| 15-Jul-X1 | 1.2680 | 1.2400 | <2,615,000> | <2,674,000> | <72,000> |

| 31-Dec-X1 | 1.2320 | 1.2200 | <2,321,000> | <2,343,000> | |

| 15-Jul-X2 | 1.2170 | 1.2100 | <2,725,000> | <2,740,000> | <19,000> |

| 31-Dec-X2 | 1.1680 | 1.1500 | <2,448,000> | <2,486,000> | |

| 15-Jul-X3 | 1.1240 | 1.1000 | <2,950,000> | <3,015,000> | <113,000> |

Notes:

(1) USD 100 mn × 6.09% × (Days/360)/Average EUR–USD, where Days was the number of calendar days in the accrual period (i.e., 169 for accrual periods ending on 31 December and 196 for accrual periods ending on 15 July)

(1) USD 100 mn × 6.09% × (Days/360)/Spot EUR–USD

(1) USD payable amount × (1/previous Spot EUR–USD – 1/current Spot EUR–USD), where USD payable amount was the USD 100 mn × 6.09% × Days/360 corresponding to the previous accrual period

The accruals and payables related to the USD leg of the CCS were identical to those of the bond, but with opposite sign. The following table summarises the accruals and payables related to the EUR leg of the CCS:

| CCS EUR leg accruals and payables | ||||

| Fixed rate | Days | EUR leg accrual (*) | Payable amount | |

| 31-Dec-X0 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X1 | 5.19% | 196 | 2,261,000 | 2,261,000 |

| 31-Dec-X1 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X2 | 5.19% | 196 | 2,261,000 | 2,261,000 |

| 31-Dec-X2 | 5.19% | 169 | 1,949,000 | 1,949,000 |

| 15-Jul-X3 | 5.19% | 196 | 2,261,000 | 2,261,000 |

(1) * 100 mn × 5.19% × Days/360, where Days was the number of calendar days in the accruing period

8.4.6 Accounting Entries

The required journal entries were as follows.

- Journal entries on 15 July 20X0.

The bond was issued.

- No entries were required to record the CCS as its initial fair value was zero.

- Journal entries on 31 December 20X0

The accrued interest of the bond was EUR <2,264,000>. The payable related to this accrued interest was EUR <2,234,000>.

- The accrual of the USD leg of the CCS was EUR 2,264,000. The receivable related to this accrued interest was EUR 2,234,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 1,875,000 gain. The change in fair value of the CCS produced a EUR 1,882,000 loss, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X1

The accrued interest of the bond was EUR <2,615,000>. The payable related to this accrued interest was EUR <2,674,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 72,000 loss.

- The bond coupon was paid using the amount received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,615,000. The receivable related to this accrued interest was EUR 2,674,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 72,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X1

The accrued interest of the bond was EUR <2,321,000>. The payable related to this accrued interest was EUR <2,343,000>.

- The accrual of the USD leg of the CCS was EUR 2,321,000. The receivable related to this accrued interest was EUR 2,343,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 3,842,000 loss. The change in fair value of the CCS produced a EUR 3,795,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X2

The accrued interest of the bond was EUR <2,725,000>. The payable related to this accrued interest was EUR <2,740,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 19,000 loss.

- The bond coupon was paid using the USD amounts received under the USD leg of the CCS.

- The accrued interest of the USD leg was EUR 2,725,000. The receivable related to this accrued interest was EUR 2,740,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 19,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- Journal entries on 31 December 20X2

The accrued interest of the bond was EUR <2,448,000>. The payable related to this accrued interest was EUR <2,486,000>.

- The accrual of the USD leg of the CCS was EUR 2,448,000. The receivable related to this accrued interest was EUR 2,486,000.

- The accrual of the EUR leg was EUR <1,949,000>.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 4,990,000 loss. The change in fair value of the CCS produced a EUR 4,958,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- Journal entries on 15 July 20X3

The accrued interest of the bond was EUR <2,950,000>. The payable related to this accrued interest was EUR <3,015,000>.

- The interest payable corresponding to the bond's previous accrued interest was retranslated, producing a EUR 113,000 loss.

- The bond coupon and principal were paid/repaid using the amounts received under the USD leg of the CCS. The bond principal represented EUR 90,909,000 (= USD 100 mn/1.1000).

- The accrued interest of the USD leg was EUR 2,950,000. The receivable related to this accrued interest was EUR 3,015,000.

- The interest receivable corresponding to the USD leg's previous accrued interest was retranslated, producing a EUR 113,000 gain.

- The interest receivable corresponding to the USD leg was received.

- The accrual of the EUR leg was EUR <2,261,000>.

- The interest payable corresponding to the EUR leg was paid.

- The retranslation of the bond's carrying amount into EUR resulted in a EUR 3,952,000 loss. The change in fair value of the CCS produced a EUR 4,038,000 gain, fully deemed to be effective. The difference between these two amounts was recognised in the cash flow hedge reserve of equity.

- The CCS notionals were exchanged. ABC paid EUR 80 million and received USD 100 million (worth EUR 90,909,000). The difference was worth EUR 10,909,000 (=90,909,000 – 80 mn).

The following table gives a summary of the accounting entries:

| Cash | Interest receivable | Derivative contract | Financial debt | Interest payable | Cash flow hedge reserve | Profit or loss | |

| 15-Jul-X0 | |||||||

| Bond issuance | 80,000,000 | 80,000,000 | |||||

| 31-Dec-X0 | |||||||

| Bond accrued coupon | 2,234,000 | <2,234,000> | |||||

| CCS accrual USD leg | 2,234,000 | 2,234,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | <1,875,000> | 1,875,000 | |||||

| CCS revaluation | <1,882,000> | <7,000> | <1,875,000> | ||||

| 15-Jul-X1 | |||||||

| Bond accrued coupon | 2,674,000 | <2,674,000> | |||||

| Bond accrual retranslation | 72,000 | <72,000> | |||||

| Bond coupon payment | <4,980,000> | <4,980,000> | |||||

| CCS accrual USD leg | 2,674,000 | 2,674,000 | |||||

| CCS interest receivable retranslation | 72,000 | 72,000 | |||||

| CCS USD leg receipt | 4,980,000 | <4,980,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| 31-Dec-X1 | |||||||

| Bond accrued coupon | 2,343,000 | <2,343,000> | |||||

| CCS accrual USD leg | 2,343,000 | 2,343,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | 3,842,000 | <3,842,000> | |||||

| CCS revaluation | 3,795,000 | <47,000> | 3,842,000 | ||||

| 15-Jul-X2 | |||||||

| Bond accrued coupon | 2,740,000 | <2,740,000> | |||||

| Bond accrual retranslation | 19,000 | <19,000> | |||||

| Bond coupon payment | <5,102,000> | <5,102,000> | |||||

| CCS accrual USD leg | 2,740,000 | 2,740,000 | |||||

| CCS interest receivable retranslation | 19,000 | 19,000 | |||||

| CCS USD leg receipt | 5,102,000 | <5,102,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| 31-Dec-X2 | |||||||

| Bond accrued coupon | 2,486,000 | <2,486,000> | |||||

| CCS accrual USD leg | 2,486,000 | 2,486,000 | |||||

| CCS accrual EUR leg | 1,949,000 | <1,949,000> | |||||

| Bond retranslation | 4,990,000 | <4,990,000> | |||||

| CCS revaluation | 4,958,000 | <32,000> | 4,990,000 | ||||

| 15-Jul-X3 | |||||||

| Bond accrued coupon | 3,015,000 | <3,015,000> | |||||

| Bond accrual retranslation | 113,000 | <113,000> | |||||

| Bond coupon payment | <96,523,000> | <90,909,000> | <5,614,000> | ||||

| CCS accrual USD leg | 3,015,000 | 3,015,000 | |||||

| CCS interest receivable retranslation | 113,000 | 113,000 | |||||

| CCS USD leg receipt | 5,614,000 | <5,614,000> | |||||

| CCS accrual EUR leg | 2,261,000 | <2,261,000> | |||||

| CCS EUR leg payment | <4,210,000> | <4,210,000> | |||||

| Bond retranslation | 3,952,000 | <3,952,000> | |||||

| CCS revaluation | 4,038,000 | 86,000 | 3,952,000 | ||||

| CCS exchange | 10,909,000 | <10,909,000> | |||||

| <12,630,000> | -0- | -0- | -0- | -0- | -0- | <12,630,000> |

8.4.7 Concluding Remarks

ABC's objective when entering into the combination of the bond and the CCS was to incur an annual expense representing 5.19%, or EUR 4,210,000 (=80 mn × 5.19% × 365/360).

During the first, second and third years of the term of the bond (and of the hedging relationship) the overall impact of the strategy on profit or loss was an annual expense of EUR 4,210,000. The annual net cash outflow was exactly EUR 4,210,000 as well. Therefore, ABC's objective was fully achieved.

This outcome occurred because there were no ineffective amounts. Otherwise, the target still would have been achieved from an annual net cash flow perspective, but not from an annual expense perspective. Even in the presence of inefficiencies, the overall 3-year expense would have been EUR 12,630,000 (=4,210,000 × 3).

As mentioned in the previous case studies, the basis component of the CCS was part of the hedging instrument. A notably volatile behaviour of the basis could have created significant inefficiencies. When the basis component of a CCS is excluded from the hedging instrument, IFRS 9 allows an entity to recognise changes in the fair value of this component either in profit or loss or temporarily in OCI to the extent that those changes relate to the hedged item.