Introduction

If you are reading this book, you are almost certainly a trustee or board member. Or perhaps you are considering becoming one. Maybe you are an adviser looking for tips on how trustees think about the complex issues you advise on, or you are a board member of a pension fund, endowment or foundation. Irrespective of your level of expertise and profession in the industry, why should you read this book, and which problems are we attempting to solve here? More importantly, how should you use this book and apply it to your own practice for the benefit of your fund and its long-term performance?

The basic premise of this book is that trustees have a crucial role to play in the long-term success of pension funds and other long-horizon asset owner organizations: sovereign wealth funds, endowments and foundations. Trustees are able to make to a real and meaningful difference when it comes to sustainable pensions for millions of pensioners in the coming decades. For a trustee this may be a powerful, but at the same time scary, idea. In the past decade, the very low interest rates have dramatically increased the cost of meeting future pension payouts, beyond all expectations. The time that you allocate and the level of knowledge that you need to demonstrate have probably increased disproportionately over the years as a consequence of the increased regulation. The stakes for your personal reputation are higher than ever. You understand the importance of doing this job well. You are aware that you matter for the thousands and millions of future pensioners who depend on your choices for their future retirement. As a trustee you have both a large responsibility and a large opportunity regarding the investments you oversee. Given that you are at the beginning of the investment chain it is imperative to understand what contributes to investment success and what detracts from it. This matters all the more because the margin of error is steadily narrowing. Consider, for instance, that in the year 2000, trustees would have expected equities to earn 10% per year, whereas today, they would be more than happy to expect half as much.

It is easy to get lost in the complex landscape of investing. Understanding and overseeing what really matters is key. This book benefits anyone who is seeking to ask the right questions in the boardroom, and is looking for a guide that will help them in setting the agenda in ways that allow for effective and relevant decision-making. This book is also intended as a potent counterbalance to the highly skilled management of the investment organizations that trustees face. Above all, this book contributes in a very pragmatic way, as we review and consolidate years of academic research and case studies on day-to-day implementation, translating these into inspiring examples and actionable alternatives that are of practical use to trustees worldwide. We systematically integrate the important perspectives into the five parts of this book. In Chapter 14, all perspectives are brought together in a way that assists trustees in determining where they stand right now, and what is needed to move to the next level in the pursuit of investment excellence. Reading this chapter first will help you to read the book in a more goal-oriented manner.

As a trustee, having oversight and pushing the right buttons is difficult. We have come to this conclusion based on years of extensive practical and academic experience, in combination with our own research and the ample available evidence. We are fairly confident in saying that there is a lot to be gained from learning how to do this correctly. We feel that trustees should take an active role in this process on behalf of the beneficiaries they represent.

Trustees are often highly competent individuals who are relatively new to the situation in which they have to govern a pension organization. It can take quite some time before they grasp the task in its entirety, appreciate its complexity and fully understand what really matters and what does not. Trustees are more often than not in the process of “learning on the job,” which creates a risk of them only having a partial understanding of the issues at hand. Such a risk is manageable and may even be tolerable when financial markets are calm and the political environment is stable. Unfortunately, at this time, the opposite is true. We are witnessing abrupt and profound shifts in the political and technological landscape; and given generally low solvency, the margin of error is small. This book aims to bring the reader up to speed fast. Moreover, we hope it will stimulate a structured conversation within the fund, where views can be shared and exchanged in order to assess the current state of the fund, and possibilities to improve it can be determined.

We argue that there is a substantial governance “bonus” to be harvested. We believe that by transforming any weak pension organization into to an excellent one, additional annual long-term return gains of 1%–2% can be achieved.1 Of course, the potential gain depends to a large extent on the starting situation of the plan. Exhibit I.1 below specifies a number of sources of higher returns, splitting them in two parts: avoiding negative contributions to returns and intensifying the use of positive contributions.

EXHIBIT I.1 Bonus to be harvested when moving up from mediocre to excellent on the scale of excellence.

The potential gains of moving up on the scale of excellence depicted in the table above are crude and will differ from fund to fund. This table zooms in only on the financial side of things, but there also are other issues at hand that may drive success: How do you cope with environmental, social and governance (ESG) matters? What is your policy on climate change? We are witnessing a shift in the expectations of beneficiaries and other stakeholders. Not having a sound answer to these questions or hiding behind a narrow definition of fiduciary duty may come at a high cost in terms of the license to operate the fund.

Quite a few of the sources of improvement are accessible to almost all funds, regardless of their size. They all require well-applied knowledge and understanding from the board of trustees and investment committee. Essentially, the message here is to plug any leaks and avoid avoidable mistakes. Some of the sources are scale-dependent and depend on the availability of a “proprietary” investment organization that can, for example, harvest the risk premia available in illiquid assets in a cost-effective way. To a large extent, in both cases the board and the board investment committee play crucial roles in driving the fund into the direction of excellence—or vice versa. Therefore, the quality, knowledge and, most of all, drive of boards matter—a lot.

Doing 1–2% better is a considerable amount in a world in which expected returns for well-diversified portfolios are somewhere in the range of 3–6% in nominal terms. We estimate that harvesting 80% of this bonus requires only a limited amount of work once you understand the drivers and put in place the right groundwork. For example, it involves getting your beliefs right and making sure that they are consistently translated into the investment process. It involves designing an investment process that helps to achieve your fund's goals and tackling the main known governance issues. We believe that there are five activities that together can create “excellent investing;” we discuss them at a later point in time. We feel these are the roughly the same for every fund, even though pension funds come in all shapes and sizes. Our experience is that the same issues pop up around the globe. As the answers to these common issues may vary slightly due to cultural or regulatory circumstances, we will address such differences in size and structures (and their consequences) wherever necessary and appropriate.

The central message throughout this book is that the board is key in achieving long-term investment excellence. The board, however, is not the party managing the investments, but the party that is meant to be in charge of the design, strategy, monitoring, and improvement of the “machine” that delivers the output. This requires a specific set of perspectives, which we summarize as the right altitude, the right distance, and the right horizon. Altitude: Does the board look at the total fund setup and its outcomes from a helicopter view? Can it achieve a critical distance towards itself? Horizon: Has the board organized itself in such a way that it can look forward and backward at least over a 5–10 year perspective? Can it do so even if that time span is longer than the individual's timespan as a member of the board? And distance: Is the board able to maintain the right distance from the execution of the investment management—is it close enough to be able to fully carry out its responsibility, yet not so close that it is taking operational decisions that should be taken by the executive?

Excellent pension funds strike the right balance between altitude, distance and horizon. They do not get caught up in the vast forest of investment strategies, nor do they get drowned by oceans of financial data. They are not distracted by mathematics and investment industry jargon. Often, too much attention is paid to the (sometimes highly technical) detailed investment side (i.e. doing things right), while important issues remain unanswered (i.e. doing the right things). Excellent pension funds and especially their trustees, therefore, know when and how to take the fiduciary perspective in managing the investment organization, while at the same time making sure that they are a partner in the investment process, where all stakeholders depend on each other for sustainable results. In other words, transforming from good to great requires a board that is not only keen on staying the course but is, perhaps more importantly, very much attuned to learning, adapting and reflecting on its own behavior.

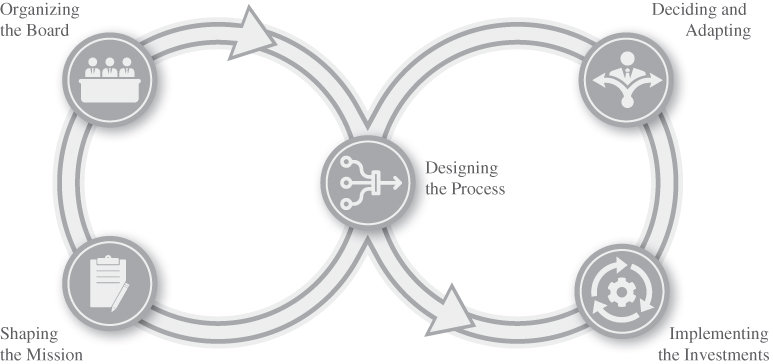

In order to balance the attention of the board between doing the right things and doing things right, we introduce the “excellence loop” presented in Exhibit I.2: the left part is the strategic, design, “doing the right things” loop; whereas the right part is the much faster implementation and the “doing the things right” feedback loop. The connection between the loops deserves a lot of attention: often this is the point where serious challenges can arise in terms of delegation and principal–agent issues.

EXHIBIT I.2 The excellence loop.

In this respect, our aim is to help trustees in identifying activities that need to be carried out in order to develop a good pension fund and, if their ambition reaches higher (which in our opinion it should), what is needed to develop an excellent pension fund. While drawing on our own experiences and research as well as that of generations of trustees and investment professionals, we offer trustees a practical “how to” guide in grasping the fundamentals of creating and operating a pension organization successfully.

Our goal is to provide insight into the key activities for building long-term excellence in investing. We combine “hard” investment thinking, for example about the design and implementation of the investment process, with “softer” elements, such as the organization of the investment committee or the self-reflection of the board. In doing so, we maintain an unbiased attitude towards the practical and academic evidence on what does and does not work in investment management. While overwhelming evidence already exists about the various ways we make decisions and about the sense and lack of sense of investment strategies, we also observe a growing body of evidence and literature that shows us how we can actually organize this in a good way. Unfortunately, trustees often enough ignore such evidence or are simply not aware that it exists. We trust that this book offers them powerful and compelling tools and knowledge.

We believe that pension funds and their beneficiaries may expect trustees and boards who are intrinsically motivated to move towards excellence. Therefore, we will almost never look at regulatory requirements or at the role of the regulator, which we see as a setter of minimum standards, not as a motivator to move towards excellence.

To summarize, this book will support the trustee at three levels. First, we outline the five key dimensions that drive long-term investment success. As a trustee, you know how the investment process is organized. But do you also know why the investment process is organized the way it is? Is it indeed the best way to achieve the pension fund's goals, and does it reflect the (right) risks in the pension plan? These are all obvious, but nevertheless crucial, questions that we will help you pose and formulate. You will see which assumptions matter, so that next time you don't simply go through the motions in a board or investment committee, but instead can immediately get to the questions that matter. Secondly, the book offers sound and practical advice that is built on both academic work and broad real-world experience. What might work in practice does not always have a sound theoretical basis, and vice versa. Consider, for instance, that the integration of sustainability in the investment process started long before academic evidence even supported such a move. Conversely, academic research has in turn produced many studies on new types of portfolio construction, such as factor investing for example, which may not (yet) have been (fully) embraced by the industry. The wise and successful trustee therefore would do well to be pragmatic in determining what exactly strengthens the investment process, rather than upending it. Finally, this book provides the trustee with the necessary insights to become a better decision maker while putting the ideas and concepts into practice. Boardroom dynamics are complex, as is making investment decisions today that will have an impact in decades to come. The challenge is to incorporate the insights whilst acknowledging that people and their interactions are crucial to the very success of their mandates. Here too, we choose a hands-on and evidence-based approach, recognizing that as a trustee, you are thrown in at the deep end, confronted with the acute challenges and complexities of an existing situation.

LEVELS OF EXCELLENCE: ASSESSING AND IMPROVING YOUR PRACTICE

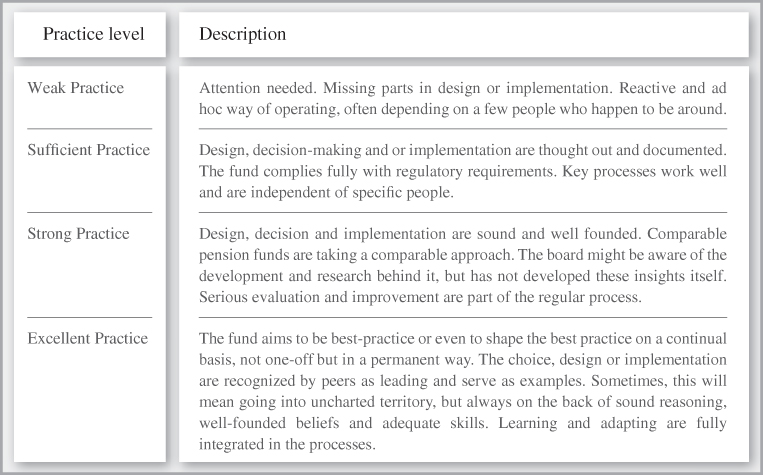

Every chapter in the book ends with a short list of self-reflection questions. You can use these to position yourself and the fund and help identify any points for improvement. In each chapter, you can assess your fund on the four levels explained below: “weak,” “sufficient,” “strong,” or “excellent.” In addition, you can build a list of issues to reflect on and issues to act on. This allows trustees to develop and test their own individual views on the main concepts treated in the book. The underlying logic of the four levels has a strong analogy with typical “maturity level” thinking. Think of weak as reactive, ad hoc, coincidental, individual, local, dogmatic and rigid. And think of excellent as proactive, planned, systematic, collective, holistic, learning and adaptive. A more detailed description of the different practices is given in Exhibit I.3. Looking at the cases we have studied, we also feel that being open and transparent in general correlates with higher levels of excellence.

EXHIBIT I.3 Levels of practice.

Becoming excellent is difficult but armed with examples and logic we feel it is achievable. However, it asks a lot. It also requires at least a certain scale; we would argue $5 billion or more: this is a size which makes it possible to have a serious governance budget, invest in the proprietary knowledge, and thereby enormously reduce the dependence on external advice and asset management. In practice, if a fund has a smaller size than this, by realizing strong practice it does a good job, and will probably be a lot better than the average peer, because there will be spillage going on. It takes strength to be disciplined.

Strong practice is known territory: you can get there by studying theory and evidence and learning from relevant peers. Excellence requires something more: the guts, trust, vision, and quality to move beyond charted territory. Strong practice takes time to develop and be embedded within regulation, the standard courses for trustees and other bodies of knowledge.

Sufficient practice is: keeping up with the existing design, decision and/or implementation to fit within the regulatory framework of the pension fund. This model suits pension funds that have a highly standardized and easy to implement pension—and investment framework—just fine.

Certainly, all levels of practice do develop over time. Even to simply stay in the same place, you must learn, change and adapt: the body of knowledge develops, the regulator develops, the available product and “investment ecosystem” develop, the external environment develops.

We previously mentioned that there are five activities towards excellence. These are: (i) Understanding the Role of Pension Funds, Shaping the Mission; (ii) Designing the Process; (iii) Implementing the Investments; (iv) Organizing the Board; (v) Learning, Adapting and Improving.

Correspondingly, this book consists of five parts, each covering one of the five key activities:

- Part I, “Pension Funds: Understanding the Role, Shaping the Mission,” has an introductory character, it provides a crash course into what trustees need to know in order to play their role well. This activity lays the foundations for the pension fund, defines purpose and translates purpose into strategy. What is the role of the fund, what are the roles and responsibilities of the board? Who are you and what do you want to achieve for your participants? This consists of having clarity about your purpose—why you exist for your participants, what the added value is that trustees want to highlight. Purpose, mission and strategy translate into achievable goals, such as the pension deal that you are you offering.

- Part II, “Designing the Process,” takes a strategic approach to the design of the investment function and investment organization that is needed for the strategy to be implemented. This part starts with creating a common language for trustees when investment is concerned. We review the key investment concepts that trustees need and will be used throughout the book. Next, we focus on investment beliefs or principles that drive the differentiating choices in the investment process. Then, we delve into the investment management process, the process by which the fund intends to achieve its returns. A number of “investment models” have emerged in recent decades, taking different approaches to the investment function and role of pension funds. We identify the main models and discuss what trustees need to consider when consciously choosing one of these models and making it their own.

- Part III, “Implementing the Investments,” focuses on the effective execution and implementation, from the perspective of a trustee. This part of the process is fully delegated. Execution builds on portfolio construction, implementation and feedback, monitoring and evaluation. The execution translates the objectives into investment outcomes. There will always be leakage between implementation and plan, but this should be minimized. For boards and investment committees, execution predominantly translates into: how do you organize the investment process in such a way that the different steps build on each other's insights; and how do you make sure that the results are continuously evaluated, where the art is to separate random short-term noise from results that affect the fund's long-term goals? The questions of the right distance, altitude and horizon are crucial here: if the board is short sighted and obsessed with detail, it will choke the investment organization. If the distance is too large, the tail—the investors—will wag the dog—the fund. Based on our research, we highlight the choices that trustees spend most of their time on in their role.

- Part IV, “Organizing the Board.” This part focuses on the oversight and governance of the investment process, designing, steering, and overseeing the realization of the mission of the pension fund. In the earlier activities, the emphasis was on relatively hard and objective matters: strategy, process, and implementation. The present activity is performed by boards and committees consisting of individuals with different backgrounds, skill sets, and mental makeups. To turn these into a well-performing orchestra, both in peacetime and in wartime, is an enormous task. So, in this activity the harder to pinpoint human factor plays the main role. How will the board organize itself to realize purpose and mission? What are the board's key tasks; what does it delegate to whom? What should the board be aware of, and organize beforehand when setting up investment committees and executive offices to support their tasks? And what are valuable insights in dealing with the investment management organization?

- Part V, “Learning, Adapting and Improving,” revisits the role of trustees and delves into learning and adapting. This activity focuses its attention on boardroom dynamics. What does it take to make a good decision? What special challenges does a board have when it is supported with complex decision tools such as Asset Liability Management (ALM)? Is the board aware of the special role advisors have, and how they can influence decision-making? Finally, it requires a down-to-earth board to take all the necessary steps in implementing the elements required to achieve investment excellence. It asks for an exceptional board that holds on to its strategy and beliefs and when financial markets come under stress, while at the same time keeping an open mind to adapt insights as new research and developments in the industry come to light that require the board to adjust its principles.

HOW TO USE THE BOOK

The book is mainly aimed at trustees of pension funds, endowments and foundations. Accordingly, it often directly addresses trustees. However, its contents are also very suitable for upper level undergraduate and MBA audiences that have an interest in institutional investments and investment governance. Let us have a look at how this book can be relevant to such a diverse audience of readers.

- Trustee. As a trustee, you can utilize this book to acquire knowledge on the drivers of investment excellence. You will gain valuable insights into methods of assessing and improving the quality of your fund's investments.

- Fiduciary manager, outsourced chief investment officer (OCIO). As a fiduciary manager or OCIO, you are in a unique position to be able to help boards to go on a conscious path of improvement. At the same time, you will reap the benefits in the form of an improved conversation with the board that may have positive consequences for quality and the outcomes of the fund at hand.

- Asset manager. As an asset manager, you will develop an improved insight into what really matters to trustees. Such enhanced understanding of the asset owner's perspective subsequently allows you to effectively design and continuously improve your (tailor-made) services to this group of clients.

- Regulator. As a regulator or government official, you will be able to accumulate the knowledge and theory needed to advance your understanding and judgment of the key issues that are relevant to pension funds within a political and regulatory context. You will be able to better grasp and comprehend the effects and impact of regulation on pension funds, recognize its potential barriers, and identify ways in which it can facilitate the industry.

- Student in finance and investment. As a student, you will be looking for additional reading material that complements your traditional textbooks by providing a rich and practical context to them. Our book offers such enrichment of the theoretical perspectives as we present real-life examples, as well as actionable models and concepts that can be implemented in practice.

In the book, special features have been integrated with the purpose of encouraging readers' interaction with, and application of, the text, and to assist them in effectively absorbing the material. For instance, self-reflection questions that allow readers to share and extend the main concepts presented within their own organization, thereby encouraging effective debate. We have concentrated the self-reflection questions in the last chapter of the book in order to allow trustees to collectively create a map of where the fund is and how it can go to the next level.

CHAPTERS OF THE BOOK

PART I: PENSION FUNDS: UNDERSTANDING THE ROLE, SHAPING THE MISSION

Part I provides a crash course into what trustees need to know in order to play their role well. It lays out the role, purpose and resulting strategy of a pension fund. It can be read selectively, either as a refresher or in order to build an understanding of the role of pension funds, or the fiduciary duty of trustees, for instance.

Chapter 1: The Role of Pension Funds, and the Role of Boards

The core of this introductory chapter is to understand the role of pension funds and the board of trustees. Why do large collective organizations (still) exist in a world where the global financial order and system are transforming at such a breakneck pace and with such profound impact on the structure and configuration of institutions? What part do they play within this context, and what is their actual function? Furthermore, we also investigate the role of trustees. As a trustee, you are a board member as well as a fiduciary. You have a specific role and an important task to fulfil that brings about several unique and serious responsibilities. We take a broad perspective on how trustees effectively define the goals of the pension fund, set policy, organize the investment process, and monitor and adjust choices in order to adapt to any changing circumstances.

Chapter 2: Developing Purpose, Mission, Vision and Goals

One of the key responsibilities of the board is to develop, implement and foster mission, goals and strategy. Investment organizations (should) have a purpose, made explicit in their missions and their goals. The design of the investment organization and process is rooted in beliefs, principles and theories on the basis of which organizations formulate their strategic course in order to stay ahead of important developments and capitalize on opportunities that may present themselves. Without such comprehensive frameworks, pension organizations will soon find it difficult to navigate through a world that is characterized by rapid and profound changes in demographics and socioeconomic trends, where disruptive innovations pose a threat to the overall continuity, and where increasingly volatile returns put the entire industry under heavy public scrutiny.

In this chapter, trustees will learn how to develop an effective mission and set of goals, partly by learning from other pension funds. We offer guidance on how to translate vision and mission into practical but powerful goals. In turn, these are translated into concrete return objectives and a risk appetite, formulated as a risk appetite statement. Combined, all of these aspects will help govern and steer the investment function and organization.

PART II: DESIGNING THE PROCESS

Part II takes a strategic approach to the design of the investment function and investment organization that is needed for the strategy. This part starts with creating a common language for trustees where investments and risk management are concerned. We review the key concepts that will be used throughout the book and identify common pitfalls. Next, we focus on how the investment function is organized, and identify the organizational values and beliefs that drive the differentiating choices in the investment process. A number of “investment models” have emerged in recent decades, taking different approaches to the investment function and role of pension funds. We identify the main models and discuss what trustees need to consider when consciously choosing one of these models and making it their own.

Chapter 3: Grasping the Investment Essentials

The day-to-day implementation of investments may seem bewildering and complex. However, the key concepts of investment theory are actually not as obscure as one may think. For a trustee to become relatively fluent in investment terminology, it requires them to get comfortable with roughly 10 building blocks. From the perspective of the trustee, we will discuss concepts such as efficient markets, expected return, risk, diversification, the use of benchmarks, and so forth.

We cover those topics and questions that we know will come up frequently in board meetings. By distinguishing between “big picture” and “detail” concepts we rank their importance. So, after having read this chapter you will be able to have meaningful conversations about investing with, for example, the people who represent the investment organizations that you and your fund deal with.

Chapter 4: Investment Beliefs as Guiding Tools

Observed from a distance, most pension funds and their investment processes look alike. What sets them apart from each other, however, are their underlying choices and decisions. These can differ quite fundamentally and completely change the entire structure and fabric of the pension organization. It is imperative that such underlying choices are identified and articulated for the purpose and benefit of the design and implementation of the investment management process. We delve further into the “beliefs” behind many of such fundamental choices and discuss how these should be viewed and put to use.

Beliefs can and will differ widely among the various funds and investment organizations. They are part of the fund's DNA and say something about the nature and character of the board and its stakeholders. Beliefs are not rigid or cast in stone, rather they tend to evolve and grow over time. Some beliefs have proven to be crucial for those choices that determine success or failure. Some beliefs are more important than others, and some are backed by more evidence than others. We identify those investments beliefs that are likely to have a strong effect on the fund's results. In our analysis, we ask ourselves whether a belief is practically applicable, and whether it makes sense in light of the state of today's finance and investments. Subsequently, we present practical examples and case studies, and demonstrate how trustees and institutions can use these investment beliefs and strategies to enhance their competitive edge.

Chapter 5: Designing the Investment Management Process

We take a detailed look at the investment process, translating the mission, vision, goals, and beliefs into actual investment choices and investments. The portfolio management process is an integrated combination of steps that need to be taken in a consistent and coherent manner in order to create and maintain an appropriate portfolio (i.e. a combination of assets) that meets the clients' stated goals.

The portfolio management process consists of three consecutive steps: planning, execution, and feedback. In the planning step, investment objectives and policies are formulated, capital market expectations are defined, and strategic asset allocations are established. In the implementation and execution phase, the portfolio manager constructs the portfolio. In the feedback step, the manager subsequently monitors and evaluates the portfolio and compares this with the initial plan. Any changes that the feedback may suggest must be examined carefully to ensure that they represent long-term motives and considerations. For each such step, we identify the role of the trustee in setting the policy, monitoring or accountability. The next chapters then elaborate on the main components of the investment management process.

Chapter 6: Organizing the Investment Function

Chapter 6 takes a strategic perspective to the investment management process and identifies five investment approaches models that currently dominate the pension fund industry worldwide. Boards may not necessarily be aware of this, but usually they have been given the advice to incorporate one of these main investment approaches. Its adoption includes a predefined set of assumptions, means of implementation, and requirements for governance. This chapter therefore integrates the insights of the previous chapters and illustrates the five dominant models by looking at their fundamentally different choices in: (i) mission, goals and beliefs; (ii) the investment process; and (iii) the investment organization. We identify the prerequisites, criteria and challenges that trustees would have to address when adopting one of those models.

PART III: IMPLEMENTING THE INVESTMENTS

Part III focuses on the execution, from the perspective of a trustee. Based on our research, we highlight the choices that trustees spend most of their time on in their role. One chapter focuses on the main choices and assumptions leading to the strategic asset strategy and allocation. In a chapter that discusses implementation, we focus on what really matters and is known. Finally, we expand on the monitoring and feedback: an important but not so well understood part of the investment cycle.

Chapter 7: Implementing the Investment Strategy

Implementation is the process that puts the pension fund's plans and strategies into action in order to achieve its goals and objectives. This chapter takes a closer look at how the fund's strategic plan should address the essential aspects of implementation that will ultimately determine the success (or failure) of an investment strategy. For example, we discuss how resources need to be assessed effectively and how objectives need to be quantified on a more granular level, in order to combine these into a flexible plan.

Moreover, the plan should also explain how the fund intends to diversify across opportunities and how it aims to manage the risk of failure in meeting minimum required returns (determined by way of scenario analysis in relation to the fund's defined risk appetite). As risk management forms such an integral and essential part of the entire implementation of the investment process, this chapter considers the most important factors affecting implementation. These include, for instance, the way the investment value chain is designed (are investment choices integrated or disaggregated), the way selection of mandates is organized, and the decision whether to manage all, or only parts, internally or externally (a decision which has enormous consequences for cost and flexibility).

Chapter 8: Building the Investment Portfolio

In portfolio construction, the actual synthesis of fund objectives and capital market expectations of relevant asset classes (i.e. equities, bonds, etc.) takes place, ultimately resulting in the fund's asset allocation. The chapter considers the fact that trustees have a wide range of choices to make at this stage of the design process, including asset allocation and diversification. Although this may sound like a rather mechanical process, in fact it is not. In addition to matters of diversification, the chapter continues with a discussion on supplemental considerations for trustees, which are relevant in constructing portfolios. For instance, we discuss active versus passive portfolio construction and demonstrate that the decision on which to choose should follow from the beliefs that are adopted. We further identify and elaborate on the grey zones that exist, so that trustees can really acquire a broad understanding that will help them rely on their own judgment when confronted with complex issues that require informed decision-making.

Chapter 9: Monitoring and Evaluation

Suboptimal (inefficient) governance of pension funds comes at a significant cost and is thus one of the biggest concerns for board members and those involved in the actual execution of the investments. In this respect, the monitoring function is one of the least thought-out components in the investment management process. This chapter discusses different monitoring “models” that will assist in determining how to effectively organize all of this, and enabling the trustee to differentiate between short- and long-term feedback, as well as distinguish skill from luck. As feedback loops tend to be long in financial markets, a poorly designed investment process may very well lead to good outcomes in a short-term horizon (i.e. by “luck”), whereas a well-thought-out process can lead to lousy outcomes. Clearly, the monitoring and feedback process should be carefully designed in a way that not only includes the outcomes of the process but, more importantly, also considers the quality of the process itself, so that (collective) learning is valid and can lead to improvement.

PART IV: ORGANIZING THE BOARD

Part IV looks at the organization of the pension fund. The board is supported by staff, committees, and in a number of cases is also the owner of the investment management organization. We look at the roles and responsibilities of these actors, as well as how they interact.

Chapter 10: Becoming an Effective Board

The primary role of the board is defining the goals, organizing the investment process, and monitoring and (re)adjusting choices in order to adapt to any changing circumstances. This may seem straightforward, but in reality it seldom is. This chapter reviews why this is the case and revisits the fiduciary responsibilities of the board. We then translate these findings into the strategic design of the investment management organization and its decision-making process.

Subsequently, we analyze the board's function and role in more detail, by looking at its composition, its focus, and the key roles that individual board members need to fulfil in order to encourage balanced board discussions. Finally, we discuss the role of the chairperson in further detail. How can the chairperson give shape to discussions and debate; what sort of agenda should they set; and what tools do they have at their disposal to create informed discussions and reach clear decisions that are executable and can be monitored effectively?

Chapter 11: Establishing the Investment Committee

The board is highly dependent on the investment committee and the executive office. It is therefore imperative that the board has articulated how they (should) work together. We highlight the position of the investment committee in more detail. In some cases, the committee fulfils a highly proactive role on basis of the executive mandate that is entrusted to the committee in making investment decisions on behalf of the fund. In other instances, the duties and responsibilities of the committee may be restricted to a purely advisory role, requiring its members only to meet a few times per year. We discuss in which cases each of these types of investment committees serves the specific goals and investment process of a particular fund best. Correspondingly, we examine the composition of the investment committee and discuss how its members and the committee's external advisors can operate and collaborate in an effective way. To this end, we also identify the potential pitfalls for external advisors. The chapter concludes with a review of the investment committee's agenda, the role of its chairperson, and the interplay between the committee and the board.

Chapter 12: Managing the Investment Management Organization

In this chapter, we turn our attention to the investment management organization. We begin with a discussion on the different types of investment management organizations, ranging from fully outsourced to fully insourced. We discuss implementation issues regarding the investment organization that currently dominate an industry-wide debate among trustees. “Alignment of interests” is such an example of a highly debated issue, because the interaction between the investment committee (representing the interest of the fund) and the investment management organization is regarded as probably the most important factor in creating investment success. It pertains to the very core of their relationship, involving multiple complex dimensions that need to be well understood and properly managed. We argue that any solution will, to a certain degree, bring alignment of interest problems as the difference between the asset owner and the asset manager is simply too large in terms of size, responsibilities, and potential earnings.

PART V: LEARNING, ADAPTING AND IMPROVING

Part V revisits the role of trustees. How can trustees improve decision-making, handle complex choices, and actually diagnose and improve the investment quality of the fund in cooperation with the other people and stakeholders that matter in the context of the fund? The reader will be provided with a set of concrete tools, instruments and real-life examples.

Chapter 13: Learning to Decide and to Take Advice

This chapter covers what is required from a board to make decisions. The profession of a trustee is hard work that involves the development of an appropriate strategic agenda fitting the fund's mission, goals and objectives. It requires careful and thorough preparation, while maintaining ongoing dialogue within the board in order to facilitate successful decision-making. In this chapter, we analyze what exactly is required for a board to actually make a good investment decision. Indeed, trustees have to make decisions all the time, ranging from trivial investment decisions (e.g. changes in investment restrictions) to decisions that have a substantial impact on the entire organization (e.g. asset allocation strategy, de-risking during crises, firing the fiduciary manager). Some boards may delay and hold off decisions by endlessly searching for more information, while others may invite external advisors to offer their recommendations. Whatever the procedure of decision-making, trustees are expected to solicit and pursue “proper advice” because failure to comply often means that a trustee will be directly (and personally) accountable to the relevant regulator. Pension funds may therefore choose to turn to an independent financial advisor, an investment consultant or the fund's own actuary for proper financial advice. In this respect, Chapter 13 also elaborates on how trustees can make sure that the internal or external advisor indeed will act in the interest of the board and will continue to provide the trustee with support, instead of taking over his or her role.

Chapter 14: Achieving Investment Excellence

Whereas in previous chapters the book confronted managers and trustees with thought-provoking questions, this chapter provides the trustees a practical instrument with which they are able to assess their fund's status in terms of achieving sustainable investment excellence. Chapter 14 equips the trustee with the necessary intelligence and practical tools that will allow the board to transform into a perpetual “learning board.”

SELF-REFLECTION QUESTIONS

This chapter provides the reader with self-reflections questions that can be used to perform a self-assessment. What is the level of practice of your fund? How well are you doing? Did you think of all the steps in a process? The chapter presents useful questions to conduct a self-assessment and serves as a reminder of important questions that nobody has asked you, nor have you asked yourself. Trustees often implicitly take processes or steps for granted; it is helpful to make these steps or processes explicit. Furthermore, this chapter serves as guiding tool for those who want to read specific sections of the book; the questions help to find the relevant sections for those readers who wish to read this book in a specific order.