Self-Reflection Questions

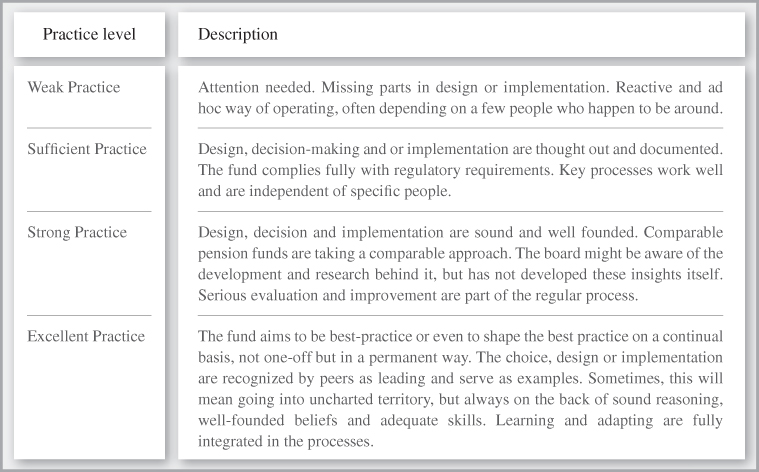

Trustees often implicitly take processes or steps for granted; it is helpful to make these steps or processes explicit. This chapter therefore presents practical self-reflection questions that boards can use for self-reflection. It links the material presented in the previous chapters by asking question designed to help you understand where you are at the moment, or it reminds you of important questions that nobody has asked you, nor have you asked yourself. Furthermore, this chapter will help you to scale your practice level which were discussed in Chapter 14. The exhibit presents the levels of excellence. We strongly encourage you to keep these levels in mind when reading the questions. Try to assess yourself depending on the answer you give to the questions. But do not stop there. Try to answer the questions as if you are at the different levels. We feel that this helps you to think of the steps that can help to increase your level of excellence.

CHAPTER 1: THE ROLE OF PENSION FUNDS, AND THE ROLE OF BOARDS

The primary role of the board is to define the goals, set policy, organize the investment process, and monitor and adjust choices in order to adapt to any changing circumstances.

- Are there clear and up-to-date documents defining the main duties of the board, focusing on key decisions and functions such as the choice of investment policy, the selection and monitoring of the fund's key executive staff and external service providers, and the monitoring of the fund's performance?

- Are these documents regularly and explicitly reviewed and brought to the attention of the board?

- Do board activities comprise everything they should do according to those documents? Do all activities get a balanced amount of attention?

- Do you have a mechanism ensuring that you pay attention to all tasks?

- Do you, either as an individual or as the board, collectively have the skills and experience to fulfill all these tasks well?

- Is the governance design fit for purpose? Are subcommittees (such as an investment committee) well defined and staffed to ensure that key topics receive the required level of consideration?

- Does the board evaluate its role on a regular basis? Does it use external help to do so?

- What is your overall opinion of the board?

CHAPTER 2: DEVELOPING PURPOSE, MISSION, VISION, AND GOALS

A key responsibility of the board is to develop, implement and foster mission, goals and strategy. Investment organizations should have a purpose, made explicit in their statement of mission and goals. Based on beliefs, principles and theories, the investment organization and process is then designed to enable pension funds to formulate their strategic course.

- Does the fund have a clearly defined purpose, mission, vision, and strategic goals?

- Does the fund have an explicit and shared idea of where it is now (Strengths, Weaknesses) and the relevant changes in the context over the next 5–10 years (Opportunities, Threats)?

- Are the values of the fund clear to everyone involved and do they have significant meaning in practice?

- Is there an explicit strategic plan to keep it fit for purpose in the light of the changing context? Does the strategic plan provide direction and focus?

- Does the board regularly spend time on strategy formulation, i.e. does it have a fresh look at the purpose and the mission, define the strategic objectives, define the competitive strategy, implement strategies, and evaluate progress?

- Are the employees and stakeholders aware of the fund's objectives, mission, and purpose? Do they understand and share them?

- Is the board able to effectively implement its strategic plan in order to achieve success? Are there clear action steps for meeting the strategies objectives?

CHAPTER 3: GRASPING THE INVESTMENT ESSENTIALS

For a trustee to become comfortable in the day-to-day implementation of the investment strategy, he or she needs to be relatively fluent in investment terminology, grasping its essence, limitations and application.

- Is there a shared understanding within the board of the meaning of the most important investment concepts? Is the board trained in this? Is there a manual defining the key concepts?

- When discussing and reporting on strategic investment issues, are you looking at the right level of the concepts?

- Is the board aware of and trained in recognizing behavioral traps? Is decision-making organized in a “thinking slow” way?

- Are you able to describe the investment approach of your fund on a single sheet of paper using the key concepts that we have talked about in this book?

- Are you honest and brave enough to declare yourself not capable of contributing to the decision-making in a certain area because you lack the relevant knowledge or skill?

- Do you regularly train and retrain existing and new board members in the key investment concepts and behavioral traps?

CHAPTER 4: INVESTMENT BELIEFS AS GUIDING TOOLS

Investment beliefs can and will differ widely among the various funds and investment organizations. They are part of the fund's DNA and tell you something about the nature and character of the board and its stakeholders. Beliefs are not rigid or cast in stone, rather, they tend to evolve and grow over time. And while some beliefs are obvious, others have proven to be crucial for those choices that determine success or failure.

- Does your fund have an actively and consciously developed set of investment beliefs? Are they spanning purely the investments, or also the organization of the investment process (e.g. delegation or agency issues)?

- Are these beliefs coherent and consistent? Do they have tangible impact on the investment process?

- Is the investment policy based on these investment beliefs? The translation of investment beliefs into investment policy should be straightforward, otherwise the investment beliefs need to be reformulated.

- Is the setup of your organization consistent with your investment beliefs?

- Are the beliefs shared broadly internally and externally?

- Are you able to attach tangible results to the beliefs that are reflected in the organization?

- Is there a regular process in which the beliefs are reviewed and improved every 5–10 years?

CHAPTER 5: DESIGNING THE INVESTMENT MANAGEMENT PROCESS

The investment process translates the mission, vision, goals and beliefs into actual investment choices and investments. The portfolio management process is an integrated combination of steps that need to be taken in a consistent and coherent manner in order to create and maintain an appropriate portfolio (i.e. a combination of assets) that meets the pension fund's stated goals. The portfolio management process moves from planning, through execution, and then to feedback.

- Is the investment process in your fund organized in a clear and consistent way? Are the components clear, and is it clear which role the board or the investment committee has in the decision-making during the process?

- Are the different parts of the process brought to the board (or investment committee) in an understandable way? Is there a clear and logical link between the inputs and the outputs of the components of the process?

- Is it clear why this process was chosen and not a different one? What would be the viable alternatives?

- Do you consider the board or investment committee fit for purpose to decide based on the provided information?

- Is there an Investment Policy Statement (IPS)? When was the last time it was updated?

- Have all the stakeholders been informed about the IPS?

- Is it clearly defined which service providers are serving in a fiduciary capacity versus which are not? How are conflicts of interest being resolved in the portfolio's favor?

CHAPTER 6: ORGANIZING THE INVESTMENT FUNCTION

Boards implicitly or explicitly adopt an investment approach model which includes predefined set of assumptions, means of implementation, and requirements for governance.

- After reading this chapter, do you consider your investment approach fully fit for purpose given your beliefs, DNA, and governance budget?

- Is there a clear reasoning why this approach has been chosen? Do you subscribe to the pros and cons of it?

- Are your competitive advantages fully used in the approach? Or, the other way around, does the approach need skills/intellectual property that are currently not available?

- Do you feel significant improvements could be made to the current approach?

- Are there exchanges of thoughts with boards or investment committees of funds that have chosen to take a different approach?

- Is the board or investment committee well equipped to govern the investment approach?

- Would you like to have a closer look at one of the alternatives for organizing the investment function?

CHAPTER 7: IMPLEMENTING THE INVESTMENT STRATEGY

Implementation is the process that puts the pension fund's plans and strategies into action in order to achieve its goals and objectives. A fund's strategy should address the essential aspects of implementation that will ultimately determine the success (or failure) of an investment strategy. Moreover, the plan should also explain how the fund intends to diversify across opportunities and how it aims to manage the risk of failure in meeting minimum required returns.

- Is it clear how the roles and decision rights in the investment process are delegated and why delegation is done this way? Is the delegation map complete? Is it Mutually Exclusive and Collectively Exhaustive?

- Is there a clear policy on total investment cost? Are internal costs (explicit and visible) and external cost (often more implicit) looked at from the same perspective?

- Is there a clear reasoning which underpins the logic of spending additional marginal cost?

- The governance budget is the combination of time, expertise, intellectual property, and organizational effectiveness of the decision makers, including the staff. Is the government budget in line with the tasks required of the fund given the set up? Would increasing the budget lead to better outcomes? Are there significant bottlenecks?

- Is there a well-defined manager selection process? Does it explicitly address the behavioral traps surrounding manager selection and evaluation?

- Is there sound reasoning behind the choice for passive or active management? Is the implementation fully aligned with the relevant beliefs?

- Is there clear and strategic reasoning behind the choice for internalizing or externalizing parts of the investment process?

- Do you have a clear policy on the relationship with external suppliers? Is this a pure and simple client-supplier relationship or do you strive for partnership, in which the supply of a service to the fund is an important part of the relationship?

CHAPTER 8: BUILDING THE INVESTMENT PORTFOLIO

In portfolio construction, trustees have a wide range of choices to make at this stage of the design process, including asset allocation and diversification.

- Is the resulting portfolio clearly based on and consistent with purpose, mission and strategy, risk appetite, and beliefs? Do you see a gap?

- Are the nine component steps clearly represented in the portfolio? Is each of them supported and documented by clear reasoning?

- Is the role of the board/investment committee in the different component steps clearly defined?

- Do you consider your portfolio to be a good portfolio based on the criteria in Exhibit 8.2? Has the board established criteria to judge the quality of the portfolio?

- Is the process of the building of the investment portfolio spread out well in the board-year?

- Are the different component parts reviewed/evaluated regularly by the board/investment committee? Do you use the outside opinions of peers or others to do this?

- Can the board or investment committee understand and look through the sensitivity of the assumptions or predictions portfolio and its potential outcomes?

CHAPTER 9: MONITORING AND EVALUATION

Ineffective governance of pension funds comes at a significant cost and is thus one of the biggest concerns for board members and those who are involved in the actual execution of the investments. The monitoring and feedback process should be carefully designed in a way that not only includes the outcomes of the process but, more importantly, also considers the quality of the process itself, so that (collective) learning is valid and can lead to improvement.

- How much of the time of the board or investment committee is spent on monitoring the investment outcomes? Is there a sound and positive relationship between the importance (the contribution to the fund objectives) and the time spent monitoring?

- How often do you monitor the investment outcomes?

- When you make a strategic decision, for which horizon do you do that?

- When you make a strategic decision, do you specify the ex-ante flags (both performance and machine) that will lead to look deeper into the strategy?

- Do you monitor on the basis of pre-specified criteria?

- Are the reports you base the monitoring on fit for their purpose? Have they been aligned to match your fund's strategy?

- Do you monitor both strategy (i.e. are we doing the right things) and implementation (i.e. are we doing things right)?

- Does the monitoring process lead to action? On which basis? How often? Do you think that you sometimes act on the basis of false negatives?

- Do you feel this action is based on the right reasons? Could it be that you suffer from action bias?

CHAPTER 10: BECOMING AN EFFECTIVE BOARD

The primary role of the board is defining the goals, organizing the investment process, and monitoring and (re)adjusting choices in order to adapt to any changing circumstances. This may seem straightforward, while actually it seldom is.

- Do the individual board members have a good working knowledge of all the topics that are handled in this book? Is there a board education program?

- Does the chairman take their role seriously? Do they make sure that the meeting runs smoothly, everybody gets a voice, decisions are made in an orderly fashion, and the decisions are well formulated?

- Within the board, are all relevant competencies represented, i.e. internal/external and strategic/operational mindset? Are there board members who have a good understanding of each of the key stakeholders' groups?

- Are the people in the board working well together? Are they listening, understanding, etc.? Are there dominant individuals or subgroups? Is there explicit attention for the cooperation in the board? Are a few people dominating the conversation?

- Is there explicit attention in the succession planning of the board to hire the best possible quality and personality when taking on board new board members?

- Is there a clear annual board agenda covering the formal responsibilities and strategic choices? For every meeting, is there a clear, balanced agenda? Are important topics in equilibrium with urgent topics? Are preparatory documents available in a timely manner, are they clear and well written? Do they have an acceptable length?

- Is the board challenged by an outside-in perspective? E.g. do you get feedback of peers, stakeholders or participants?

- Is the board and are the board members acting and fully feeling their responsibility? Do board members hide behind “experts” or arguments such as “apparently, this is the way they do things over here?”

- Does the board have the countervailing power and knowledge necessary to direct and manage the specialist parties and experts to whom tasks are delegated?

- Is the board aware of the big behavioral pitfalls that often lead to poor investment decision-making? Is there explicit attention to these pitfalls?

CHAPTER 11: ESTABLISHING THE INVESTMENT COMMITTEE

The Board is highly dependent on the investment committee and the executive office. It is therefore imperative that the board has articulated how they (should) work together. In some cases the committee fulfills a highly proactive role on the basis of the executive mandate that is entrusted to the committee in making investment decisions on behalf of the fund. In other instances, the duties and responsibilities of the committee may be restricted to a purely advisory role, requiring its members to only meet a few times per year.

- Do you feel the committee has the right altitude? Can you look at the total fund set up and its outcomes from a helicopter perspective?

- Has the committee organized itself in a way that you can look, analyze, and decide forward and backward at least in a 5–10-year perspective?

- Does the board keep the right distance from the execution of the investment management operation? Are you close enough to be able to fully bear your responsibility, yet not so close that you are taking operational decisions you really should not be making as a board?

- Are the committee and members fully feeling and acting on their responsibility?

- Is the balance between the investment committee and the executive organization right?

The investment committee also shares a number of self-reflection questions discussed with the board in Chapter 10:

- For every meeting, is there a clear, balanced agenda? Are important topics in equilibrium with urgent topics? Is the structure of the meeting clearly demarcated? How are decisions being made? Are they well documented? Is information on the historical decision-making accessible?

- Are preparatory documents available timely, are they clear and well written? Do they have an acceptable length?

- Is the committee challenged by an outside in perspective? Do you get feedback from peers, stakeholders or participants? Does the committee challenge the board's perspectives and assumptions?

- Do members hide behind “experts” or arguments like “apparently, this is the way they do things over here?”

- Does the board have the countervailing power and knowledge necessary to direct and manage the specialist parties and experts to whom tasks are delegated?

CHAPTER 12: MANAGING THE INVESTMENT MANAGEMENT ORGANIZATION

The interaction between board, investment committee and investment management organization is regarded as probably the most important factor in creating investment success.

- How clear and standardized is the mandate that the board has awarded the investment management organization? Is it well defined so that agency issues are adequately managed or minimized?

- Is the investment management organization aligned with the chosen investment model? How much “governance budget” do you have available?

- Is the board hands-on or hands-off? How much will it delegate to the investment management organization in practice?

- Is the compensation aligned with the objectives of the fund? Does the compensation system contribute to agency issues, rigidity in the organization, and selfish or uncooperative behavior? Does the compensation align with the investment management organization's urge to expand?

- How does the investment management organization monitor and manage the cost effectiveness?

- How does the investment management organization assess the quality of the building blocks? If building blocks have a lower than acceptable quality, what is done? Improve? Fire? Move from external to internal or vice versa?

- Are protocols in place when the investment management organization is not functioning properly? Do you know how to deal with this? Is it easy to change? Or is the barrier to change too large for cost-effective change?

- Do the people in the investment management organization know and align with the objectives and the principles of the fund? In the conversations with people from the investment management organization, do you observe and feel many of the success factors? Which ones are missing?

CHAPTER 13: LEARNING TO DECIDE AND TO TAKE ADVICE

Trustees have to make decisions all the time, ranging from trivial investment decisions to decisions that have a substantial impact on the entire organization. Whatever the procedure of decision-making, trustees are expected to solicit and pursue “proper advice” because failure to comply often means that a trustee might be directly (and personally) accountable to the relevant regulator.

- Do you feel your fund adapts fast enough to changing circumstances and context?

- Do you feel that your fund learns from its history and has a process for continuous improvement?

- Would you consider your board to be a learning board?

- Is the learning collective between board and investment management organization?

- What would be needed to become a learning board and organization?

- How much of the governance budget of the board (time and money) do you spend on learning?

- Is there a formal board learning process in place?

- Are new board members put through a formal learning process?

CHAPTER 14: ACHIEVING INVESTMENT EXCELLENCE

To attain excellence, a board has to learn and be able to assess their fund's status in terms of achieving sustainable investment excellence. A board should be able to, with the necessary intelligence and practical tools, to transform into a perpetual “learning board.”

- Does your fund have a process in play to promote learning and achieve higher forms of quality?

- Achieving excellence requires resources; does the board allocate enough governance budget of time and skill to move the fund towards it?

- Are new people in the organization introduced and schooled in the learnings of the fund? Do they get the proper guidance to achieve the fund's vision of excellence?

- Are documents regarding strategy, mission, vision, and beliefs regularly reviewed and updated when deemed needed? Does the board make sure this happens in a timely manner?

- Does the board view excellence as a continuous state of improving? If not, is this for the right reasons?

- Is there a shared understanding of all concepts used in the fund? Is there a system in place that ensures a collective reasoning?

- Is effort taken to minimize the effect of behavioral biases and focus on the goals that match the maturity of the fund? Are these effective now, and will they be in the future?

- Is enough time allocated to learning? How much time is spent on this, and how does this compare to other organizations?