Chapter 16

Starting a New Financial Year

In This Chapter

![]() Finishing the old year in style

Finishing the old year in style

![]() Getting data to your accountant if you don’t work in the cloud

Getting data to your accountant if you don’t work in the cloud

![]() Playing spot the difference

Playing spot the difference

![]() Communing with the company accountant

Communing with the company accountant

![]() Starting a new year (if you have to) and archiving data

Starting a new year (if you have to) and archiving data

The end of one financial year and the beginning of another can be a big deal for bookkeepers. Not only do you have to get a whole year’s books in order, ready for the company accountant to do their stuff, but in some situations, you also need to make journal entries so you can match your accounts with those from the accountant.

In this chapter, I talk about what’s required to get the old year’s accounts in order, including important details such as whether you can record transactions in the new year before the old has been finished, and what you need to get ready at the end of each financial year. I also dwell on that most delicate of relationships — the one between a bookkeeper and an accountant — and provide a few tips for a long and happy marriage.

Finally, I describe what happens at the end of the accounting cycle. I delve into the topic of final year-end adjustments (exciting stuff indeed) and — if required by your software — how to close one year for good before bringing in the new.

If you’re working in the cloud, you may well find that starting a new financial year is a relatively straightforward process, requiring little more than setting a lock date on the accounts and providing your accountant with a login. Nonetheless, you still need some understanding of the year-end process, and what things to stay alert for.

If you’re working in the cloud, you may well find that starting a new financial year is a relatively straightforward process, requiring little more than setting a lock date on the accounts and providing your accountant with a login. Nonetheless, you still need some understanding of the year-end process, and what things to stay alert for.

Finalising the Old Year

Here’s my failsafe prescription for seeing out the year: Start about three hours before midnight with an ample supply of single malt whisky and a bunch of convivial friends. Head off to see the fireworks — you can usually find some, somewhere or other — and afterwards lie on the grass looking up at the stars. As midnight strikes, break into song with ‘Auld Lang Syne’ and declare your love for everybody in that drunken, slightly maudlin way.

Whoops, I went off on a bit of a tangent there. Unfortunately, seeing out the financial year isn’t nearly as fun as seeing out the calendar year. Even worse, a fair bit of preparation is vital before you can do any wild carousing.

Out with the old year … in with the new

When you finish off the books for the year and you’re ready to tell the company accountant that they can get on and do their stuff, you want to be confident that you’ve done the best job possible, right? Then follow my step-by-step guide and don’t miss a beat:

Complete every transaction up to the last day of the financial year (usually 30 June in Australia, 31 March in New Zealand).

You can record transactions in the new year without having to finish recording transactions in the old. You’re fine to keep recording sales, customer payments and other everyday stuff in the new year, and take a few weeks to make sure that all transactions are spot on in the old year.

You can record transactions in the new year without having to finish recording transactions in the old. You’re fine to keep recording sales, customer payments and other everyday stuff in the new year, and take a few weeks to make sure that all transactions are spot on in the old year.Check your work for the previous 12 months.

Not sure where to begin? Chapter 14 provides the 12-step health check from hell.

Check that your Profit & Loss and Balance Sheet reports for the last 12 months make sense.

Generate all end-of-year reports that you require for your own records.

For more about end-of-year reports, see the following section.

If you’re working in a desktop-based accounting system (as opposed to working in the cloud), make a backup.

Don’t know how? Refer to Chapter 5.

Supply the company accountant with all the information they need.

Different accountants want different stuff, so ask for a list of what’s required (see also the following section). If you’re using desktop-based accounting software, the accountant will definitely need a copy of your company file. Alternatively, if you’re working with browser-based software, simply provide your accountant with a logon ID and password so they can work directly in your file.

Protect last year’s data so that you can’t inadvertently make any changes to the year just gone.

For this exercise in prudence, make your way to ‘Protecting against accidents’, later in this chapter. (Fear not, no contraceptive devices are involved.)

Wait a few weeks … la di da. When your accountant sends completed financial reports, figure out what adjustments you need to make, if any, to your current data.

Skip to ‘Matching the Accountant’s Figures Against Your Own’ for details. (Note: If you’re working in the cloud and your accountant does his or her adjustments directly in your company file, you can skip this step.)

Do a final backup and label it Final End of Year.

The only difference between end-of-year backups and regular backups is that you store end-of-year backups separately, never to be used again. For more about backups, see ‘Archiving data — just one more time’, later in this chapter. Again, if you’re working in the cloud, you don’t need to worry about this step.

If your accounting software requires it, initiate the new year process.

Some software, such as the non-cloud-based versions of MYOB, requires that you execute a command closing one year and starting another. Other software, such as QuickBooks Online, Reckon Accounts and Xero, doesn’t require you to lift a finger — you can keep as many years ‘open’ as you like.

Pop the champagne bottle — you’re done!

Generating end-of-year reports

Theoretically, if you keep organised backups of your company file or you’re working in the cloud, you don’t need to print any reports at all when preparing for year end. However, unless I’m working in the cloud, I like to save reports in PDF format as a final reference and supply these to the company accountant as part of the year-end process. (Not all accountants are familiar with all accounting software packages, so you may save the accountant time by providing them with all the reports they need, ready to go.)

When you work with browser-based software (such as MYOB Essentials, QuickBooks Online or Xero), you can’t take a point-in-time backup. A point-in-time backup is a copy of your data at a specific time, and can be useful if you want to compare what your data is now against what your data was before your accountant made his or her end-of-year adjustments. For this reason, I strongly recommend you generate a set of end-of-year reports before asking your accountant to review your accounts.

Here’s a list of end-of-year reports that provide a fairly complete reference of your financial position:

- A Profit & Loss report for the financial year.

- A Balance Sheet for the last month of your financial year.

- A summary GST report, either for the whole year or for each GST reporting period.

- An Aged Receivables and Aged Payables report for the last day of the financial year. (Note: In MYOB, this report is called a Receivables or Payables Reconciliation Summary; in QuickBooks Online and Reckon Accounts, this report is called an A/R or A/P Ageing Summary; in Xero, this report is simply an Aged Receivables or Payables report.)

- All end-of-year payroll reports, including year-end payroll reconciliations and, in Australia, copies of employee payment summaries.

- A report showing the cost value of inventory as at the last day of the financial year, along with any stocktake reports for that date.

- Bank reconciliation reports for each bank account for the last day of the financial year.

- A transaction report listing every single transaction for the year, sorted by account. (This is definitely a report you’ll want to save as a PDF, rather than printing out on paper.)

Xero has a neat feature that allows you to ‘publish’ reports, saving a PDF of any report within Xero itself. This means that your accountant (or anyone else for that matter) can simply go to the Published tab within the Reports menu to view all key reports.

Protecting against accidents

At Step 6 in the section ‘Out with the old year … in with the new’ earlier in this chapter, I mention protecting your data for the year that you have just completed. Exactly how you do this depends on what software you’re using: If you use a spreadsheet, simply write-protect the data; if you’re working in MYOB or Xero, you lock the periods; in QuickBooks Online and Reckon Accounts, you set a closing date.

When you protect data in this way, what you’re doing is preventing anyone from accidentally creating or editing transactions in the period that you’ve just completed. Here’s why:

Imagine if you tell the accountant that the books are ready for them to prepare your tax return. Your accountant starts finalising everything, but in the meantime you come across a credit card for that year that you’ve missed and you start adding transactions. Chances are that this moving feast of information will only serve to confuse your poor accountant, a scenario which will probably end up costing time and money.

Imagine if you tell the accountant that the books are ready for them to prepare your tax return. Your accountant starts finalising everything, but in the meantime you come across a credit card for that year that you’ve missed and you start adding transactions. Chances are that this moving feast of information will only serve to confuse your poor accountant, a scenario which will probably end up costing time and money.- In another scenario, imagine that your tax is already finalised for one year, but you inadvertently date a transaction with the wrong date, maybe dating an expense January 2015 rather than January 2016. Unless your accountant is completely on the ball checking opening balances, you’re likely to miss out on this tax deduction completely.

Note that protecting data at the end of a financial year is different from executing a command that formally ‘starts a new year’ — a process that some accounting software packages require (see ‘Starting a New Year’, later in this chapter, for more details). Protecting data simply prevents anyone from changing data from a prior year, whereas starting a new year often involves purging data from a prior year.

Incidentally I don’t reserve these data protection features for financial year-ends only. I often suggest clients protect data each time they lodge their Business Activity Statement or GST return so that they can’t inadvertently make changes to an accounting period that has already been finalised.

Sending Data to Your Accountant

If you’re sending data to the company accountant on a flash drive, CD, via email or via a service such as Dropbox (as opposed to providing your accountant with a login to your cloud-based company file), bear the following in mind:

Add passwords to your data: Before sending confidential company information off into the ether, add password protection. (Just don’t forget to let the accountant know the password.)

Add passwords to your data: Before sending confidential company information off into the ether, add password protection. (Just don’t forget to let the accountant know the password.)- Ask your accountant about file formats: If you use an Apple Macintosh (lucky you), do check that your accountant can read your file. You may need to contact the software company for assistance in transferring data from one platform to another, as most accountants work only with PCs.

- Beware of file size if emailing data: Most mail servers bounce back emails if attachments exceed 10 MB or so. If your data is larger than this limit, don’t even try to send it by email, but instead burn your data onto a CD or use a file mail service such as Dropbox or YouSendIt (see www.dropbox.com or www.yousendit.com for details).

- Create an accountant’s copy of your data if your accounting software has this feature: For example, Reckon Accounts has a clever feature that enables you to create a special accountant’s copy of your company file. Your accountant can use this copy at the same time as you keep working on your original company file. When the accountant sends their copy back to you, complete with adjustments, you then merge their file with yours.

Let the accountant know what you’ve done: I like to send a simple covering email or letter where I explain in bullet point form everything that I’ve completed (bank reconciliations, debtor reconciliations and so on). I also list everything that I know needs completing, such as depreciation journals, hire purchase journals or intercompany transactions.

Let the accountant know what you’ve done: I like to send a simple covering email or letter where I explain in bullet point form everything that I’ve completed (bank reconciliations, debtor reconciliations and so on). I also list everything that I know needs completing, such as depreciation journals, hire purchase journals or intercompany transactions.- Make a copy of your data first: When you make a copy of your file for your accountant, make an additional copy for yourself. This copy can be a useful reference if you’re trying to understand later on what the accountant has done in their adjustments, or if you end up in the tricky situation that someone else in the business inadvertently makes changes to the data for the period that you’ve already submitted to the accountant. (Refer to ‘Protecting against accidents’ earlier in this chapter for more info.)

- Send a copy of the data, rather than a backup: Most accounting software compresses data in some way as part of a backup routine, and decompressing data can be confusing for the accountant if they don’t use exactly the same version of software. You’re best to go to My Computer (on a PC) or the Finder (on a Mac) and simply make a copy of your company file.

Of course, if you’re using browser-based software, you don’t need to send any data to your accountant. All you have to do is set up your accountant as a financial advisor, and provide them with a login and password. Easy as pie.

If you’re a contract bookkeeper, you require specific permission from your client before making information available to their accountant. (The Professional Code of Conduct, a topic I cover in detail in Chapter 18, requires that you always get permission to release client information to a third party and, in this scenario, the external accountant counts as a third party.)

Matching the Accountant’s Figures Against Your Own

So, the months are ticking by and the company accountant finally finishes the accounts for the previous financial year, and delivers a shiny set of accounts complete with tax returns. What happens next?

If you’re working in the cloud and your accountant has made adjustments direct into your company file, you probably don’t need to do a thing. Simply double-check that the Balance Sheet in the printed set of accounts from your accountant matches with the Balance Sheet for the same date in your cloud-based accounts. (I still occasionally come across accountants who diligently log in to their clients’ cloud-based accounts, print out key reports, then rekey this information into their own practice software, and then make adjusting journals there. Sad, but true.)

If you work with desktop-based accounting and you’ve been working on your accounts at the same time as your accountant has been working in a copy of your company file, then the first thing to remember is that the accountant will have made adjustments to the set of books that you provided. In order for you to bring your accounts into line, matching up your records with those of the accountant, you need to make adjustments that mirror those of your accountant’s.

In the ideal world, the accountant sends you a sweet note with a list of the journal entries that they would like you to make in order to bring your accounts in line with theirs. I explain how to record these journal entries in the following section.

In the real world, many accountants don’t bother to keep track of the journal entries they make, leaving the bookkeeper to figure out these adjustments themselves. (Many accountants feel that their clients don’t really need to be able to generate their own Balance Sheets. For some simple businesses, this may be the case, but for most businesses, maintaining an accurate Balance Sheet is critical.) I explain how to get around this tricky situation later in this chapter in the section ‘Getting creative when the accountant gives you nothing’.

Recording year-end journals

Providing the accountant provides you with a halfway decent list of journals, recording year-end journals is as easy as pie:

Record your journal entries one by one.

Be careful to select exactly the same accounts as the accountant does on their journals and, unless the accountant specifically instructs otherwise, make sure that GST is zero on all of the transactions. Date these journals to be the last day of the financial year.

After recording these journal entries, reprint your Profit & Loss and Balance Sheet reports for the year, and check that your reports match with the accountant’s final reports.

So long as the net profit figure is the same, don’t worry too much if the Profit & Loss report shows slight differences in the way the accountant categorises transactions. However, do make sure that your Balance Sheet matches the accountant’s Balance Sheet, line for line.

Dealing with adjustments that only make things worse

In Chapter 14, I explain how to reconcile control accounts, such as Accounts Receivable, Accounts Payable and Stock on Hand, and I mention that allocating journals or general transactions to control accounts is a no-no. So what’s the solution when the company accountant makes year-end adjustments that record control accounts willy-nilly?

The answer is to give the accountant some of their own medicine. If an end-of-year adjustment affects either a control account such as Trade Debtors, Trade Creditors or Inventory, or a bank account that’s already reconciled and you know is perfectly balanced, then create a new equity account called ‘Accountant’s Adjustments That I Don’t Understand’. Allocate all mysterious adjustments to this account and leave them for the accountant to sort out.

Getting creative when the accountant gives you nothing

One of the trickier scenarios that a bookkeeper faces is when the accountant finalises the books at year’s end, but doesn’t provide the bookkeeper with a list of adjustments. You can tell that some adjustments are required, because your accountant’s closing Balance Sheet is clearly different from your closing Balance Sheet, but you’re not sure what these adjustments are.

The simplest approach is to ask the accountant for a list of journal entries. However, if your accountant proves recalcitrant in this regard — and, sadly, this often proves to be the case — there’s nothing for it but to do the job yourself. Here goes:

Print your own Balance Sheet for the last day of the year that the accountant has just completed.

Place this Balance Sheet alongside your accountant’s final Balance Sheet and play spot the difference.

Highlight all account balances where the accountant has a figure different from your own. Also, if your accountant has an account listed that you don’t have in your Accounts List, create it now.

Record a journal entry in your accounts, and for every account with a difference, record a journal that sets the balance to zero.

For example, if your Motor Vehicles asset account shows a value of $30,000 but your accountant’s shows a value of $12,500, credit this account by $30,000 to set the balance to zero.

Use a single journal entry to debit and credit all the accounts with a difference and, on the last line, allocate the difference between your debits and credits to Retained Earnings.

If you’re not sure whether you should enter the difference in the debit or the credit column, just make your best guess at this point.

- Redisplay your Balance Sheet report, and check that all accounts where there was a difference between your figures and the accountant’s figures now have a zero balance.

If not, return to Step 3 and figure out where you went wrong.

Record a second journal entry in your accounts and, for every account where there was a difference, record a journal entry that makes the balance match whatever the accountant had.

For example, if your accountant showed a value of $12,500 in your Motor Vehicles asset account, debit this account by $12,500. Like Step 3, use a single journal entry to debit and credit all the accounts with a difference and, on the last line, allocate the difference between your debits and credits to Retained Earnings.

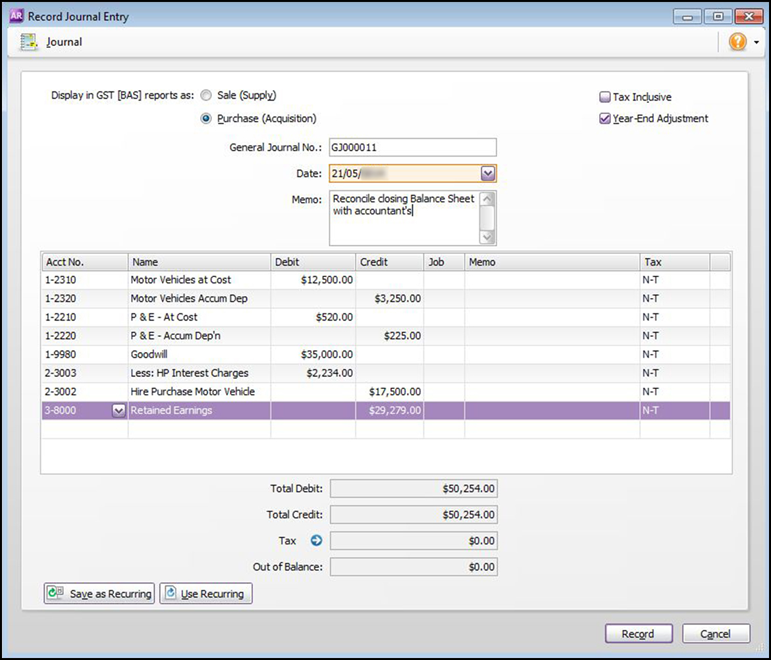

You can see how a typical journal looks in Figure 16-1.

Redisplay your Balance Sheet report, and check that your Balance Sheet now matches with the accountant’s.

If not, return to Step 5 and figure out where you went wrong. With patience and logic, you should be able to get the two reports to match perfectly.

Figure 16-1: Recording a journal entry to align your Balance Sheet with your accountant’s.

By the way, if an accountant doesn’t supply journal entries, I usually only focus on bringing the Balance Sheet into line, and I don’t try to match up the Profit & Loss report. My justification for this approach? I don’t put as much weight on reconciling Profit & Loss accounts because the balances all return to zero at the end of a financial year, whereas the balances of your Balance Sheet accounts all carry forward into the following year.

Bridging the Communication Gap

The biggest key to any relationship, whether it’s with your accountant, your lover or your cat, is communication.

When working with your accountant, keep the following in mind:

- Ask for advice instead of bookkeeping: Have you ever heard of an accountant who lowered annual fees? No, me neither. So, if the accountant used to provide bookkeeping services but now you’re doing 90 per cent of the work, harbour no illusions that these labours will save the business money. Instead, be realistic and get your pound of flesh by asking for business advice, in place of the bookkeeping services the accountant used to provide.

- Ask for criticism: Don’t be too laissez-faire about your accounts, relying on your accountant to fix up all your mistakes every time your tax falls due. It’s a waste to pay good money for your accountant to fix the same mistakes, year in, year out! A much healthier scenario is the one where you ask your accountant to explain what you’re doing wrong and get them to teach you something new every time they work with your file.

- Become more informed: With most accounting software, you can produce your own Profit & Loss and Balance Sheet reports whenever you want, at the click of a button. Ask your accountant to look through these statements with you, explain what they mean and analyse what the business could be doing better.

- Plan ahead: Don’t wait until the financial year end has come and gone before worrying about tax. Get your accountant to give your company file the once-over a couple of months beforehand and ask whether you should do anything before the financial year comes to a close.

Starting a New Year

Even after you finish the last year’s books as best you can and you send this information to the accountant, and even after you get the stuff back from the accountant and journal all those pesky year-end adjustments, your work is still not done.

Depending on what software you use, you may need to complete the year-end process by instructing the software to start a new year, clearing one year’s balances ready for the next. You also need to mark this auspicious occasion by backing up and archiving your data. (Note: The only mainstream software that requires you to start a new year is the non-cloud-based versions of MYOB. QuickBooks Online, Reckon Accounts and Xero don’t require this procedure.)

Understanding what happens when you start a new year

Are you trying to get a handle on why starting a new year is such a hullabaloo? The reason is this: When you start a new financial year, all the balances in your Profit & Loss accounts return to zero, but the balances in your Balance Sheet accounts stay constant, carrying forward from one year to the next. (Note: Profit & Loss accounts include all income, cost of sales and expense accounts; Balance Sheet accounts include all asset, liability and equity accounts.)

For example, when you start a new year in MYOB software, three things occur:

- You replace last year’s historical totals with the totals of the year just completed.

- Depending on your selections during the process, you either end up purging all transactions dated the previous year, or you end up locking these transactions so that they can never be changed, they can only be viewed.

- You move the balance of current year earnings into retained earnings and set all income, cost of sales and expense accounts to zero.

Archiving data — just one more time

Unless you have the happy security of working in the cloud, you probably already understand the importance of backing up, not only for the safety of your financial records, but also for the continuation of all life as we know it. But for how long do you need to keep these backups?

The exact length of time depends on whether you live in Australia or New Zealand, your business structure and whether you have employees or not, but in order to play it safe, a good general rule is to store backups in a safe place for at least seven years.

Hopefully, you already create a special backup at the end of each year and you store these backups separately in a safe place. (If not, it’s time to start, now!). However, if you change your password from time to time, can you guarantee that you’ll be able to remember what your password was five, six or even seven years earlier? Probably not.

Save yourself from such dramas by writing your password or a password clue on the front of your end-of-year backups (if you have physical backups) or by adding a password clue to the filename (if you store your backups online).

Even if you don’t work in the cloud on an everyday basis, storing your end-of-year data in a secure cloud location makes good sense. Storing backups off-site is the only way to protect valuable business data from fire and theft, and the cloud provides the perfect safe location.