32.3 HOW MANY MANAGERS SHOULD ONE CHOOSE?

The question lends itself to an interesting analysis of what an investor is trying to accomplish. For example, an investor may want to create a portfolio that tracks a diversified CTA index (e.g., Barclay CTA Index or Newedge CTA Index). This is a plausible goal, because these indices are widely used benchmarks. Further, in some cases the CTAs whose returns make up these indices are among the largest in the business and, in the case of the Newedge CTA Index, are open for business and provide daily returns. In examining the construction processes for CTA portfolios, Burghardt and Walls (2011) use the returns reported by CTAs that are part of the Newedge CTA Index in order to see how quickly the return on a portfolio of CTAs converges to the return on the index.

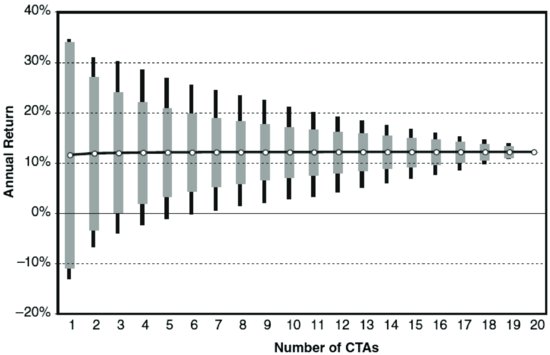

Exhibit 32.1 demonstrates the range of returns realized on randomly formed and equally weighted portfolios that include anywhere from one to 20 CTAs. The gray bars indicate the two middle quartiles while the black lines are related to the bottom and top quartiles. The index return in 2008 was about 12%. This exhibit shows that the main effect of increasing the number of CTAs in the portfolio is a decrease in the amount by which an investment might outperform or underperform the index. With a single-CTA portfolio, an investor might outperform the index by as much as 22%; however, the investor could also lose money on the investment, even if the industry is, on average, making money. From there, the main question is how much tolerance the investor has for slippage. In this example, it would take 10 CTAs to bring the range of outperformance or underperformance down to 5%. Further, with five or six CTAs, the chance of losing money when the industry is making money is reduced nearly to zero.

EXHIBIT 32.1 Annual Return on Randomly Formed Portfolios of CTAs

Source: Barclay Hedge, Newedge Prime Brokerage Research, 2008.

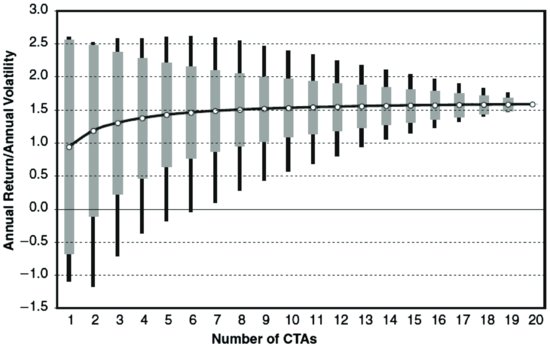

Another consideration is the risk-adjusted return. The effects of diversification will, as shown in Exhibit 32.2, tend to bring up the ratio of expected return to the volatility of returns. For the index, the ratio of return to standard deviation of returns was about 1.6. With a single adviser, the expected risk-adjusted return would have been less than 1.0. It is apparent from the curve that most of the expected gains from diversification are realized by the time the portfolio contains five or six CTAs. After this, diversification still helps, but less so.

EXHIBIT 32.2 Information Ratios of Randomly Selected Portfolios of CTAs

Source: Barclay Hedge, Newedge Prime Brokerage Research, 2008.

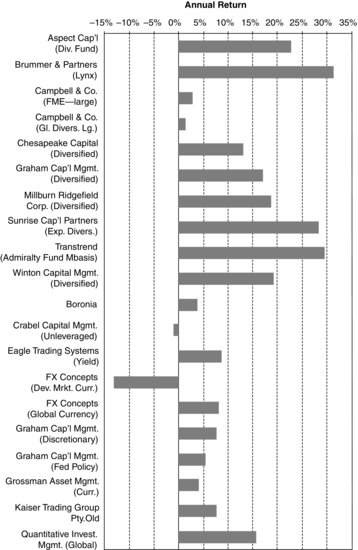

Still another issue is the outright expected return, irrespective of risk. The reason for bringing this into the discussion is shown in Exhibit 32.3, which illustrates the returns for each of the 20 managers in the Newedge CTA Index. For the purposes of this exhibit, trend-following CTAs are organized alphabetically first, with non-trend-following CTAs listed alphabetically second. Thus, Aspect through Winton are found in the first group, with Boronia through QIM in the second group.

EXHIBIT 32.3 Returns on CTAs in the Newedge CTA Index (2008)

Source: Barclay Hedge, Newedge Prime Brokerage Research.

In examining the two groups, it becomes apparent that trend-following CTAs tend to target a higher return volatility than non-trend-following CTAs, who strive for more diversity. In this example, the only way to earn more than 10% would be to focus the portfolio on trend-following CTAs. Even then, given the variability of this group's returns, four or five CTAs would be needed to gain confidence in the portfolio's outcome.

In short, five to six is about the minimum number of CTAs an investor would want in a portfolio of CTAs. This number affords the investor some protection from tracking error, provides some diversification, and would likely produce a risk-adjusted return similar to the index. From six on up, the investor makes smaller, but possibly important, improvements in how the portfolio performs.