Looking Forward

Throughout this text there has been a repeated focus on the rate of change of the elements in the commercialization cycle. These changes altered the enabling parts and helped us do things more effectively and faster. New means of funding early stage projects, new forms of incubation, more effective teaching, and better modeling tools are just some of the items to be noted. With these dramatic changes there is an increased risk of forecasting. But to codify them as they exist today becomes an interesting task.

A Changing World

To look forward certainly carries its own caveats about uncertainty. One aspect that we can easily agree on is that there is a tremendous rate of change surrounding the commercialization, entrepreneurship, and innovation cycles. We can at least see directional change by looking at the several categories that surround change. They include:

- Early stage investments

- Incubation trends

- Global competition

- Technology and IP changes

- Entrepreneurship training

- The Internet and customer demand

- Economic demands

In 1946 Georges Doriot (former Dean of the Harvard Business School and sometimes referred to as the “father of venture capitalism”) started the first recognized venture capital firm called American Research and Development Corporation (ARD). Its landmark early investment was $70,000 in Digital Equipment Corporation. With that investment a new investment industry was born that is estimated at $25 billion each year. The relevance of investments like these is not that they enable hundreds of early stage ventures to start but also that they allow underperforming portfolios such as pension funds to place a limited amount of their assets in high-risk/high-reward, professionally managed projects. They are the folks who become the limited partners of the venture firms. The early venture capital model carried the assumption that there would be a robust market for exiting their investments in initial public offerings (IPO) and the allure of high stock price multiples.

That speculative model carried industry growth until the year 2000, when the infamous “dot com” bubble of Internet-based stock prices collapsed. An abrupt collapse of perceived value created significant loses, including those involved in venture capital investments. The industry response was to retreat to more established (less risky) investments. This left a significant gap in early stage investments and in startup companies.

In 1978 Professor Bill Wetzel (faculty member of the University of New Hampshire and founder of its Center for Venture Research) observed the behavior of individuals placing private investments in early stage ventures. Most of them were located in New Hampshire. These individuals had cashed out from successful technology-based companies and invested in early stage projects. He coined them “angels” from the model of Broadway show investors who take investment risks before shows are launched.

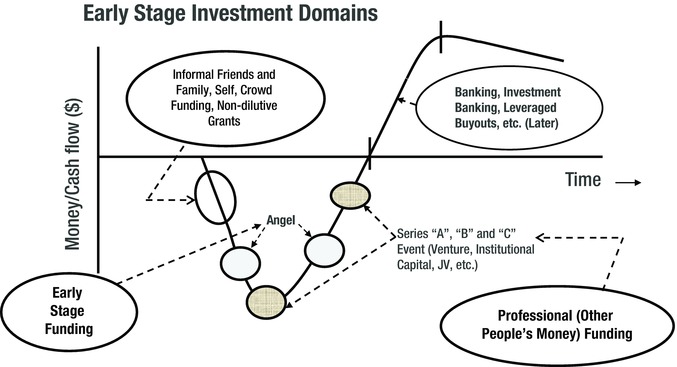

Today the annual level of angel investing equals that of venture capital efforts. Angels place less money per deal but participate in more deals. They also participate in earlier stage deals and those in the “gap” left behind in the movement of venture investors to later stage deals. Their comparative relationships are shown in Figure 12-1.

Figure 12-1. Early stage investment cycle

Both venture and angel deals have a common issue of who is capable of making those investments. The Securities Exchange Commission (SEC), in an attempt to protect those unable to absorb risk because of limited means, defined the “accredited investor.” Both angel and venture capital investors must meet the test of the accredited investor—they must have a Net worth of $1 million and an annual income of $200,000. Primary residences are not included in this tabulation. Later, the Dodd-Frank Act extended this definition. This means that only individuals with significant worth can invest.

On April 5, 2012 President Obama signed a bill entitled “Jumpstart Our Business Startups Act” or the JOBS Act for short. The act enables new sources of capital to be made available to early stage companies. It does so by allowing equity issues to be traded on the Internet and reduces the qualifying level of net worth of individuals. It also allows for an increased number of shareholders that could be brought into an organization before they had to be reported to the SEC. The JOBS Act democratized early stage investment, provided for a new distribution of wealth, and opened social media pathways for a new type of funding called “crowdfunding.” Almost anyone could invest in a company from anywhere in the world.

It also spawned a new crowdfunding industry characterized by the emergence of a company called Kickstarter. Started on April 28, 2009 by Parry Chen and others, Kickstarter became a portal where outsiders could invest in their portfolio companies. According to the web site in 2012, Kickstarter has raised $1.5 billion for 207,135 projects and touts a 40% success rate. Its model is further defined as an assurance contract whereby it will not release the funds for a given project unless all of the money has been raised. Kickstarter requires a 5% fee for its effort. It has certain restrictions to its projects that include:

- Banning the use of photorealistic renderings or simulations

- Banning genetically modified organisms

- Limiting items to “sensible sets”

- Requiring a physical prototype

- Requiring a manufacturing plan

Kickstarter is not alone. There is an array of companies like GoFundMe, Indiegogo, Teespring, Patreon, Crowdrise, and others that are already sharing the space. It is still unknown how effective they will be and how this new form of capital acquisition will survive, but what is clear is that the landscape is rapidly changing.

One more dimension of this new trend is the addition of non-equity based crowdfunding. In this scenario, goods (or a future promise for them) are exchanged for cash. An interesting example appeared in the April 29, 2012 issue of The New York Times. The article describes the journey of a 26-year-old engineer named Eric Migicovsky. Eric had developed a line of wristwatches called Pebble Watches that conveyed text messages from iPhones. First he tried the traditional venture capital routes to raise startup capital but was flatly turned down. He then turned to Kickstarter. He offered a Pebble Watch for anyone who would contribute $99. No equity was exchanged. In less than a week, he raised $7 million from nearly 50,000 people. Later company reports indicated that a total of $10 million was raised by the company in less than the two-week window offered by Kickstarter.

Pundits of this process say that without appropriate vetting, committee review, proper due diligence, and strict term sheets, the upside investment quality would falter. The same was stated about angel capital when it first started almost 40 years ago. Today, the angel investing industry has its own national best practices organization (ACA) and is reported to have placed an estimated $24 billion in 2014. This amount is equal to the funds placed by the venture capital industry in the same year.

Incubation

There is a moment in the early lifecycle of an organization in which the project is quite fragile. Teams aren’t complete, technology has not matured, or funding itself might not be totally secured. All of this is independent of the perceived value of the enterprise. Successful companies certainly prevail. Some need more time and the resources to achieve success.

In 1959, the first recognized incubator to meet these needs was created in Batavia, New York. The idea of a public entity to achieve this help took years to develop. In 1980, there were only 12 recognized “business incubators” in the country. As more industrial plants closed in the Northeast and the economy seemed to change in the 1980s, more incubators grew under the rubric of economic development. In 1982, the Ben Franklin Partnership Program was created as a first statewide organization. It became a model for many others. In 1985, an organization called the National Business Incubation Association was formed to serve as a clearing house of information and best practices. It was comprised of 40 members. Today there are 1,600 members.

In more recent history, the energy to create incubators reached beyond economic development terms that promised the creation of jobs through the creation of new companies. Internet companies that no longer require large capital investments in laboratories and physical resources have emerged at a breathtaking rate. A simple working space, administrative help and a broadband Internet capacity seem all that was needed. The Federal government did not stay on the sidelines. The U.S. Small Business Administration (SBA) created Small Business Development Centers (SBDC) to assist early stage companies. There are about 900 centers in the country. Other government programs such as the National Science Foundation (NSF), I–Corp, and the Small Business Innovation Research (SBIR) are further examples.

The incubation process is indeed global. In Switzerland, for example, there are government/industry cooperatives like the Technopark in Zurich and the Blue Factory in Fribourg. In Israel a state-run system of incubators was launched by the country’s Office of Chief Scientist in 1991. Its goal was to enable a “startup nation” in the country. In their model, the government contributes 85% of the early startup costs. It is not without its challenges. In the May 19, 2015 issue of the Israeli daily newspaper called Haartez, there was a lead article that asked, “Technology Incubators: Has Their Time Passed?” Although, the director of the organization, Yossi Smoler, commented that the model is changing to one of more inclusion of corporate and financial support, the article pointed out that open source software and cloud computing has changed the way many new companies are formed. Rather than join in this dialogue, I wonder if newer models need to be created.

There are already new models in operation. In Boston, for example, an accelerator program called Mass Challenge was created about five years ago. With international representation around the world, it claims to be the “world’s largest startup accelerator.” It offers a large itinerary of coaching, mentorship combinations, and access to investors and other resources.

In the February/March 2013 issue of the NBIA Review, published by the National Business Incubator Association (NBIA), the new director of the organization, Jasper Welch, is interviewed about his thoughts of the future of incubation. What is clear, he states, is that incubation must reach beyond the bricks and mortar model to operate in the “next practices.” Others have referred to this space as the virtual incubator. What is again clear is that this area of incubation will have to change with the changing needs of early stage companies.

Global Competition

If there is one theme that captures the essence of global competition, it is that of change. The United States and Europe have long dominated the expenditures of R&D investments. Yet, in a 2014 Global R&D funding forecast published by Battelle and R&D Magazine (rdmag.com), December, 2013, they stated that Asian countries have grown their share of global spending on R&D from 33% to 40% in the past five years and that “Southeast Asia has become the world’s largest region for new research investments-a trend expected to continue through the decade.” The shift in knowledge production is significant. China’s investment in education has borne fruit. The “country has overtaken the United States in the number of doctorates awarded in science and engineering. They have 1.6 million researches and academic and 30 million students enrolled in higher education institutions.” Once a bastion of low labor costs, China has been motivated by these trends to outsource labor costs to Africa, South America, and the Middle East. One byproduct of their educational and research activity is that since 2011, China has accounted for the greatest number of patent applications globally.

This shift in technology development has an interesting byproduct. In China, India, and Brazil, the number of the world largest corporations in residence has grown 6.7%. In the same time period, the United States, United Kingdom, and Germany have reported significant declines.1 One further indicator is the number of Total Early Stage Entrepreneurial Activity (TEA) index. TEA measures the percentage of individuals in an economy who are in the process of starting or running new ventures.

In the five countries reported, the United States and European Union reported the lowest TEA numbers, while Latin America and Africa reported the highest (Global Entrepreneurship Monitor (GEM) 2013 Annual Report, Jose Enesto Amardo, Amanda and Niels Bosma; Babson College et al., 2014). Innovative entrepreneurship is defined as creating a product or service that represents significant commercial opportunities. The presence of supportive environments in the emerging countries includes increased access to funding for early stage entities (venture capital), changes in culture, supportive regulatory initiative (such as eliminating capital gains taxes), relaxation of rules restricting foreign investments, and educational systems integrated with these trends.

Technology and the Changing Landscape of Intellectual Property

Intellectual property protection manifests itself in the form of patents, copyrights, trade secrets, and licensing innovative ideas. In common they provide a barrier to infringement and thus make it more attractive for financial investment and talent acquisition in those same ideas. The common law beginnings of intellectual property protection envisioned just this. What they didn’t see was the explosion of technology, the Internet, and the global competition that would surround it.

We have moved a long way from the lone inventor hunched over his or her worktable and shouting “eureka” as the proverbial light bulb of invention went on. Today we are involved in more collaborative complex technologies that vary across business sectors. Certainly, genomic models and their discovery, which are at the basis of modern medical science and the rapid advance of software and Internet-based solutions, were not envisioned by those who crafted patent laws around the world.

In 1970 a group of United Nation member nations created the World Intellectual Property Organization (WIPO) to “promote and harmonize intellectual property law internationally.” Among its early initiatives was the promotion of IP from industrial to developing countries. Creating a global context for IP is a daunting role. Cultures, trade agreements, and local judicial systems all complicate the drive to broaden encompassing laws. Yet, the needs for these agreements is greater than ever due to the global nature of technological competition. A newer initiative entitled the “Trade Related Aspects of Intellectual Property Rights” (TRIPS) within the WIPO is attempting to find flexible, yet encompassing directions of new legal development. A “one size fits all” direction seems an elusive goal.

At least one other consideration that affects the “flexible” approach that the TRIPS effort is trying to accomplish is that of shorter terms for the IP protection. In earlier years a 20-year term of patents seemed reasonable as a protective envelope to commercially recognize its value. Rapid technological advancements, improved enabling tools, and shorter lifecycles have challenged the 20-year boundary to the point where the term actually is perceived as a barrier to innovation and change. The value proposition simply becomes outdated before the patent or copyright expires.

Sometimes IP thwarts both social and societal need. An example is in the field of pharmaceuticals. Patents give their owners the right not to commercialize a given technology. It would be hopeful if societal, social, or even sustainability issues could be brought to bear as mitigating issues. At this point there seems little effort being exerted to find such solutions. In a telling article written by Richard Spinello, who is on the faculty of Boston College (entitled “The Future of Intellectual Property”—Ethics and Information Technology, Euwer Academic Publishers, Netherlands, 2003), he argues that the same issue applies to Internet-based IPs. In the absence of succinic rules of protection and privacy around the IP, the very basis of the innovation that created the application is in jeopardy. The World Economic Forum’s 2014 meeting in Davos wrote a member’s position paper entitled “Rethinking Intellectual Property in the Digital Age.” It proposed a series of “guidelines” that encourage collaboration—open dialogue, consumer engagement, and development of “shared goals.” Although not as specific as the incentive to modify laws and regulatory mandates, it may set the stage of additional cooperation.

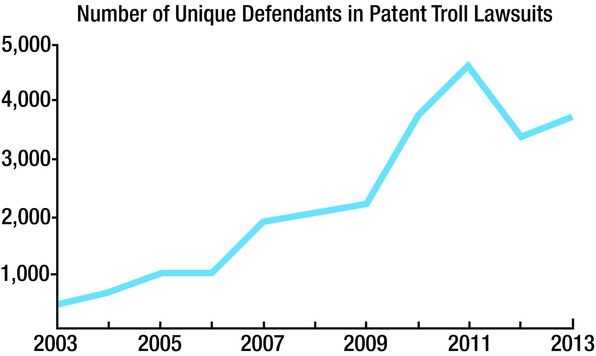

One last but disquieting theme impacting the future of IP is the emergence of patent “trolls.” They are firms that acquire rights to patents but do not manufacture any products or services. An example is a troll firm buying up the patent rights of a bankrupt company for the purposes of suing a more innovative and successful company and gaining instant fines derived from the suit. In the United States, there is the concept of share legal expenses, so the risk of the challenge is minimal (or shared). In the November, 2014 issue of the Harvard Business Review, James Bessen, an economist at the Boston University School of Law, notes what he deems is an alarming rise in the number of patent litigation cases created by these trolls. This trend is illustrated in Figure 12-2.

Figure 12-2. The rise of patent litigation cases created by Internet trolls2

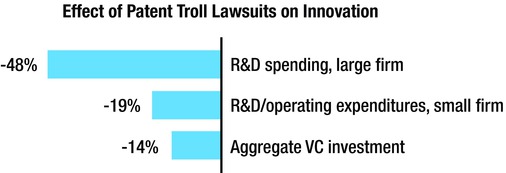

Further in the same article Bessen refers to a study conducted by Roger Smeets of Rutgers University and Catherine Tucker of MIT, where Smeets observes that smaller companies’ R&D spending diminished significantly when sued by the trolls. Tucker reports a 14% decline in venture capital firms in those same companies, while Smeets cites a 19% decrease in R&D spending by those same companies. Both trends are shown in Figure 12-3.

Figure 12-3. Effect of patent troll lawsuits on innovation3

Whatever the short-term impact of troll’s litigation prowess is on the innovative expenditure, it is only the federal government’s ability to legislate those changes in the laws that will mitigate the negative effect of their disruptive activity. Those changes and the ability of global entities to collaborate on their regulatory efforts will become markers for future changes in IP. Clearly the new forces of technological global innovation and the emergence of the Internet on music, film, and social media will be driving forces for these changes.

Entrepreneurship Training

One of the major historical bastions of the American economy has been the emergence of the entrepreneur. In many cases, he or she altered the landscape of our sense of business. Examples are many.

FedEx was started as a term paper in 1965 at Yale by Fredrick Smith. The paper was perceived by Smith’s professor as non-revolutionary. Today, FedEx is a firmly established fact of life. Michael Dell started the now famous Dell Computer company in his dormitory room at the University of Texas in 1984. Bill Gates was at Harvard when he and Paul Allen conceived the Microsoft operating system as a business.

In an essay entitled “The Chronology and Intellectual Trajectory of American Entrepreneurship Education,”4 Jerry Katz, a professor at Saint Louis University, cited the first economics/business courses references as early as 1876. The first published business text was cited at Gordon Baty’s “Playing to Win.”5 From there, an accelerating pace of symposia, journals, and case studies appeared. Business schools appeared but cantered their offerings in management. Entrepreneurship seemed to be a minor offering.

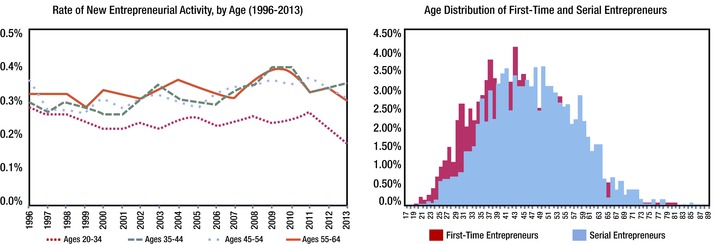

Looking ahead, the Kauffman Foundation published an article in February, 2015 written by Jason Weins and Emily Fetsch entitled “Demographic Trends Will Shape the Future of Entrepreneurship.” It cited the growth of millennials and baby boomers as the primary driving force. Education has responded by offering in 250 courses in entrepreneurship in 1985 to 5,000 in 2008. These demographics are in Figure 12-4.

Figure 12-4. Entrepreneurship demographics6

This means that new high-tech startups will be twice as likely to be started by individuals over 50 than those younger than 25. That shift may not be enough for the United States to maintain its leadership in entrepreneurship. Jim Clifton, Chairman and CEO of Gallup, wrote in the January 13, 2015 issue of the Gallup Business Journal that for the first time, the United States has projected that the number of business closures will exceed the number of startups. The United States will be twelfth in the global lineup of rates of startups. To reverse this trend, he argues that to “get back on track we have to quit pinning everything on innovation; we need to start focusing on the almighty entrepreneurs and business builders.”

Academia is responding to these changes in multiple and notable ways. It was only 40 years ago that the first master’s in business administration (MBA) with an entrepreneurship concentration was offered by the University of Southern California. Today there are many programs in place in cache universities such as Harvard, MIT, Stanford, Babson, and Kellogg. They are making significant inroads to teaching students and developing sufficient staff to teach them. Novel experiments in case writing have spawned new teaching tools of simulations and online courses. For a variety of reasons including outreach, student enrollment, and spiraling costs, new means of delivering information are now in place. Blended learning, for example, is where students can continue their education remotely but still maintain presence on campus several times a semester. Online courses are proliferating and collaboration with industry, including courses taught in remote plants, are currently in place.

Supporting these trends are an endless list of business plan competitions, entrepreneurship clubs, incubators, and practice labs on campuses. Courses integrated as minor offerings in alternative fields such as engineering and science are also prevalent.

The Internet and Customer Demand

To forecast the future of the Internet is a bit like asking the Wright Brothers what they thought of intercontinental flying at altitudes 40,000 feet and almost 600 mph. The rate of change and the acceptance as working tools in applications as diverse as medical information, marketing, finance, and entertainment are simply awesome.

The Internet as we know it today was not a single invention. Its first enablement was the concept of packet switching developed for the Department of Defense. When groups of data could be sent, the application of Internet Protocol allowed those packets to be sent between users. Tim Berners-Lee added the concept of a the World Wide Web to the process, which allowed e-mail, instant messaging, and finally voice over capability between users. All this occurred in just 30 years. Today we just accept its capacity in a verity of devices like handheld smart phones, financial interaction, and text and photo sharing, to name a few. Best of all this capacity is being recognized throughout the planet.

There are some early clues as to what the future holds. Let’s look at three. First, offerings of the “cloud” promise better access to data through multiple devices such as pads, computers, smart phones, and watches. It allows better allocation of resources because individual users do not have to invest in mainframes and memory that becomes easily obsolete. It is global so worldwide timing issues and interfaces become invisible to the users. The cost of the services can be allocated on a pay-as-you-go basis. This aspect alone is having enormous impact on the costs absorbed by the users.

There is a least one more consideration that affects the use of the Internet going forward. It is the speed that the technology can transport information. Today, the average home broadband speed is 10 megabytes per second (Mbps). Throughout the United States, this number varies wildly. In the populated centers like New York and Washington, speeds start to approach 100 Mbps. It is projected that by 2020, the number could reach 200 Mbps. Today, the infrastructure of fiber optic cable and transmission equipment is expensive and improvements are hard to justify financially. One possible solution is to rely on government legislation and funding to normalize this. Whether that happens is interesting to conjecture. Currently the United States is far behind countries like South Korea and Sweden in their ability to provide fast service to broad markets and applications. With increased capacity, more elaborate and complex information can join in the use of the Internet.

So here we see a technology that promises significant increases in its ability to transmit information, an exploding world of applications, apps, and devices, wireless connections, and the almighty cloud as alternatives for bringing all that information to us—wow.

All of this is not without its issues. Clearly at the top of the list are the domains of privacy and security. Hardly a day goes by without hearing that some system has been hacked or has been infected with malware, a Trojan, or some other virus. Some of this is a footrace between protection software and the worlds of individuals determined to thwart the use of the Internet. When domains of medical records, financial data, security, and other sensitive materials are considered, this issue becomes more important than ever. Firewalls and encryption schemes to protect the data are certainly defenses against security intrusion, but absolute integrity seems an elusive goal. I don’t doubt that as a society we will also adjust to a greater degree of intrusion. Just look at the current offerings of Google and Facebook to see how much “private” information is now in the public domain. Tracking software “cookies” can follow most transactions we do on the Internet. The fields of cybersecurity will grow as we find new forms of data protection.

No matter which way we view the future of the Internet, its overall potential is simply awesome and will impact how we commercialize new technology and its applications.

A View from the Trenches

A book like this one would be incomplete if it did not offer a perspective from the entrepreneur’s view. Every element of an entrepreneur’s environment is subject to change. It is not cool to remain a startup! To cite a few change elements:

- The renewed emphasis on innovation and entrepreneurship at all levels of the government and social frameworks. Endless federal and local programs and funding are available at a rate never imagined.

- Educational systems including new courses, seminars, workshops, and student-run clubs and laboratories are increasingly prevalent. Most academic environments encourage this activity.

- Available sources of capital in the form of new structures like crowdfunding to continued investments by venture and angel sources.

- Increased attention to environmental, sustainability, and social issues that require new venture to support them.

- Availability of incubation facilities created under the rubric of economic development.

- A culture of startups in cluster environments like the Innovation Center in Boston. Existing real estate that has been scoped to allow and encourage this behavior.

- Enabling technology that allows faster and more cost-effective creation of prototypes and products.

- And of course, the Internet, which allows global outreach, almost instant marketing outreach, and instantaneous feedback.

- A need to create new forms of employment for early stage careers.

- The “rest of the world” is embracing innovation and entrepreneurship at breathtaking levels.

On this list of positive forces, there is the view of the entrepreneur. Some argue that the lure of high-performing and somewhat unrealistic expectations of the Facebook, Google, Amazon, and Apple are within the reach of many of the new projects. Traditionally, the public offering that results in a 10 times multiple was within expectation. It is possible that some projects will do exceptionally well, but they are the exception. Early stage investors are content when 1 in 10 investments yields higher results.

Although the expectations of upside liquidation results (the motivational “carrot”) need to be in focus, the reality of early stage environment also needs clarification. There are clearly a cohort of individuals who deal with the uncertainties of the early stage companies. Those same people may not be the group to later build the enterprise. Many times inexperienced entrepreneurs express surprise at the difficulty of managing the early stage ventures because of the lack of supporting capital or people.

Some of the reality attributes include:

- Lack of recognition of either the brand or the product. This translates into longer and more expensive selling cycles. It also requires a different form of selling that relies on a term called “missionary” sales techniques where the context and need for the product (or service) needs to be identified before the sale can be considered. It’s an educational process that not all sales people can bridge.

- Startup skepticism in the form of questioning the viability of the enterprise. Would General Motors (or any established organization) buy products or services from an early stage company whose very viability is questioned? Like so many specific early stage issues, this one can be countered by offering a preemptive license to the potential customer whereby they have the exclusive rights to manufacture product themselves if the startup can’t. Although this option is a bit complicated, it requires a mindset that is different from an established enterprise. This, in turn, requires the early stage team to adapt in ways a more mature enterprise would not be required to embrace.

- Limited or immature organizational depth in early stage companies leads to an informal management style. Many entrepreneurs that I have spoken with have reported to be some of the best moments in their company’s evolution. In my company there was a period of time when we did not have a conference table because the mill in which we were located required an odd shaped table. That forced us to have a modest but custom size table. Those of us who were there all remember the informal “standup” meetings as memorable and efficient. This was probably romanticized over time, and the frustrations due to the lack of resources was real and stood in the way of accomplishing preset goals.

- A startup was once likened to the barnstorming years of flight. Although this evokes images of the freedom of open cockpit flight, those planes cannot go very far and are considered quite unreliable. A modern Boeing 777 is capable of flying great distances and with accompanying records of significant reliability. What type of journey do you want to achieve?

A Finale

As the world’s commercial, political, and economic forces change at an ever accelerating rate, so the pressures to compete in more innovative and entrepreneurial ways increase. Central governments and local municipalities have responded to these changes with a myriad of tax incentives, regulatory and legal modifications, sweeping programs such as NSF funding, and the creation of local incubation and support activities. Academia has certainly responded with its endless litany of courses, research, publications, student-run competitions, and aggressive technology transfer operations.

Enabling these efforts has been dramatic influences of enabling technology in the form of Internet-based information exchange that could only have been dreamed about a few years ago. Actual models of new ideas can be generated in real time due to computer-driven 3D modeling and the low-cost rapid prototyping. New materials allow these ideas to move to reality almost instantaneously.

Moore’s Law, coined by Intel co-founder Gordon Moore in 1965, predicts that the number of transistors on an electronic chip would double each year. That trend has continued, but now the forecast is for doubling every eighteen months. That predicted dynamic has invigorated the design and implementation of electronic hardware and application software to be developed at an increasing pace anywhere in the world. Medical advances have led nearly to the ability to create genomic-based designer drugs and procedures to implement them. Robotics and automation have moved the use of these ideas to new levels of productivity.

This book looked at the process of commercial reality from the newfound wealth of new, innovative, and entrepreneurial ideas that derive from technology-based products and services. It presented a model that represents probable pathways to commercial realization of the ideas and examined the multiple forces that impact the probability of success in achieving these goals. It is certain that in order for us to successfully compete in the ever-changing world, new models and practitioners who can successfully implement them must be developed.

___________________

1The Super-Cycle Lives: Emerging Markets Growth Is Key," November 6, 2013, https://www.sc.com/en/news-and-media/news/global/2013-11-06-super-cycle-EM-growth-is-key.html.

2Source: HBR.org.

3Source: HBR.org; Research by Catherine Tucker, Roger Smeets, Lauren Cohen, Umit Rurun, and Scott Kominers; Analysis by James Bessen

4Journal of Business Venturing 18, no. 2. (2003): 283–300.

5Reston Publishing, 1974.

6Sources: Robert W. Fairlie, Kaufman Index of Entrepreneurial Activity (2014), using data from Current Population Survey, US Census Bureau; Kauffman Firm survey.