We Don’t Need a New Business Model: “It Ain’t Broke and It Don’t Need Fixin”

Clark W. Gellings Clark Gellings and Associates, LLC, Morgan Hill, CA, United States

Abstract

Enhanced collaboration between regulators, utilities, and consumers would enable a participative framework wherein the existing regulatory model could be used to expand product and service offerings of utilities. The consumers win by having easier access to new technology, greatly increased choice, increased customer service, enhanced reliability, and improved power quality without suffering the complexities of a new business model. A new business model is not needed. Many, if not all, of the attributes of tomorrow’s power system can be met by the existing regulatory model. However, what remains unclear is what the cost and benefits of each model will be and how difficult the transitions may become.

Keywords

regulation

new regulatory model

transactive energy

demand-side management

demand response

energy efficiency

distribution utilities

distributed energy resources (DER)

1. Introduction

As described in several of the chapters in this volume, a popular subject these days has become the idea that “we” need a new business model for distributional utilities. Usually this is offered during discussion about the future of investor-owned distribution utilities, but the argument is meant to apply to public power and rural electric cooperatives as well. This dialogue is prompted by the dramatic changes in the cost and performance of distributed energy resources (DERs), including solar photovoltaic (PV) power, energy storage, and hyperefficiency appliances, as well as consumer interest in having control over energy costs and general support for sustainability. Indeed, there is a rapid pace of technological innovation taking place in the DER space.

The natural conclusion by the critics of the existing regulatory paradigm is to say that regulation, as currently practiced, has outlived its usefulness; hence the need for a new regulatory regime, new business models, new tariffs, etc. Others have offered that transactional energy is the ultimate solution and that utilities’ usefulness has passed us by. The purpose of this chapter is to argue that there is nothing conceptually wrong with the existing regulatory model based essentially on the rate of return regulation and suggests that, if properly applied, can continue largely as it was conceived. In fact, it will lead to a preferred basis for the distribution utility of the future.

This chapter is organized in seven sections, followed by the chapter’s conclusions. Section 2 revisits the driving force behind the discussions about today’s distribution utility business model; Section 3 offers an opinion for more changes; Section 4 describes the focus of a new regulation using the existing model; Section 5 discusses the rate of return regulation; Section 6 discusses as to why we do not need to reinvent the wheel; Section 7 discusses how we can move forward; and Section 8 compares the existing regulatory model to transactive energy (TE).

2. A reprise: what has prompted the discussions about new business models?

Electricity demand is driven by a complex combination of the desire for the comfort, convenience, and productivity that energy provides, but is tempered by the price, availability, and functionality of competing energy forms (e.g., natural gas) and the technology that converts electricity into services. Fundamental to this demand is the presence of income (in households) and/or economic activity (in business and industry). In each energy application, the technology that converts electricity or other energy forms into lighting, heating, cooling, motive power, or other energy services plays a key role in the effectiveness of the desired energy service, its economy, and the resultant environmental footprint.

Until recently, the relationship of electricity demand to these factors was straightforward. Now with the advent of cost-effective PV power generation, the expanding use of combined heat and power (CHP), and dramatic changes in the end use of electricity, the equation changes. Consumer demand for electricity is now potentially supplied by a combination of grid-supplied energy services and power generated on-site.

Beyond distributed generation, the advent of a myriad of other new and improved technologies also has a substantial impact on the technology landscape and then the overall demand for energy. Recent adoption of plug-in electric vehicles (PEVs) is a prime example of new technologies that can significantly increase the use of electricity. Other new technologies, such as tablets, PCs, home entertainment systems, and heat pumps, are additional examples. Finally, there are a myriad of new entrants into the industry offering everything from purchase power agreements to funding and revenue and cost sharing for innovative distributed power generation, storage, and efficient end-use technology and programs. These changes have led to a consideration of the evolution to a modern power-delivery infrastructure referred to as the Smart Grid. It is defined by the Energy Independence and Security Act of 2007 (EISA, 2007) as a modernization of the electricity-delivery system. Thus it monitors, protects, and automatically optimizes the operation of its interconnected elements, from the central and distributed generator, through the high-voltage network and distribution system, to industrial users and building automation systems, energy storage installations, and end-use consumers, including their thermostats, electric vehicles, appliances, and other household devices.

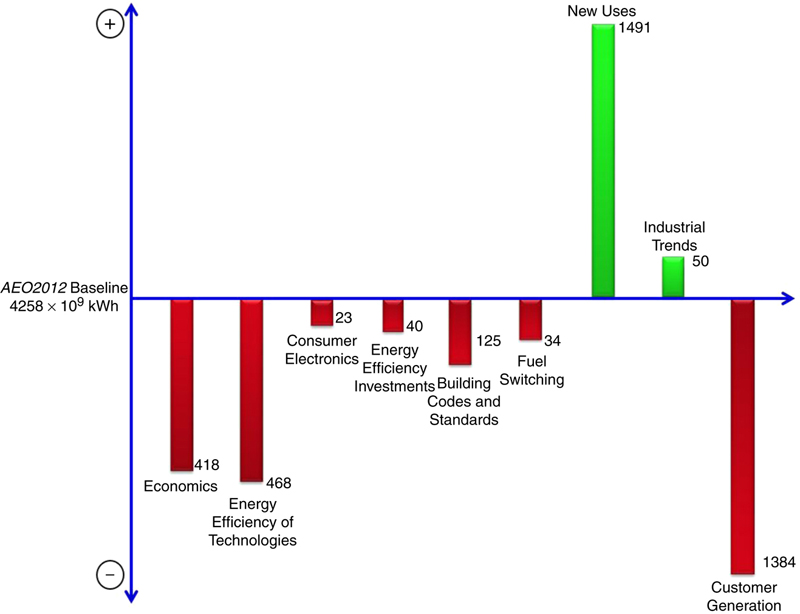

Fig. 11.1 illustrates the dilemma these changes will cause for the regulated distribution utility. The study it illustrates was based on the 2012 Annual Energy Outlook (AEO, 2012); it highlights how these changes may impact the demand for electricity leading up to 2035 and was responsible for igniting some of the most active debate among utility executives (Electric Power Research Institute, 2013). In this study the net electricity demand from grid-related services is projected to decrease substantially from energy efficiency and customer generation. This despite projected offsets by new uses of electricity, primarily electric vehicles. Most startling is that since the study was published: (1) energy efficiency has accelerated, (2) new uses have only grown modestly, and (3) customer generation has increased well beyond expectations. The bottom line is a further decline in electricity sales from grid-related services.

Figure 11.1Factors affecting growth and decline in the demand for electricity-related services by 2035 based on 2012 estimates.(Source: AEO (2012).)

These changes, further described in accompanying chapters, in technology and the introduction of new entrants offer the possibility that the grid will be characterized by a two-way flow of electricity and information to create an automated, widely distributed energy-delivery network. The grid will enjoy the benefits of distributed computing and communications to deliver real-time information and to enable the near-instantaneous balance of supply and demand at the device level.

3. Will there be more changes?

As a result of these factors among others, there are likely to be more changes in today’s power system in the next 10 years than there have been in the last 100. At no time since the first power systems were invented and deployed has there been such a variety of new energy technology available or waiting in the wings. These have the potential to fundamentally and profoundly change the generation, delivery, and utilization of electricity and related electric energy services.

It should be carefully noted that the author does NOT disagree that rapid change is coming with significant implications for the incumbents. What this chapter wishes to explore is whether we need a new business model to deal with these changes.

4. What should the new regulatory focus be?

The author agrees that we are not yet positioned to leverage the full value of all the innovation that new technologies have brought us. However, we do not need a new business model to do so. We can make the necessary changes within the current regulatory framework to enable them. These changes are as follows:

1. Increase focus on the consumer by building, maintaining, and operating the distribution system to maintain the highest practical reliability and power quality.

2. Support the adoption of DERs by adopting sufficient flexible resources so as not to constrain their proliferation, moving toward an integrated grid, installing and maintaining DER on the customer’s premises as part of rate-based assets, developing DER leasing or loan programs, and offering purchase power agreements.

3. Adopting innovative and dynamic rate design options, which align prices to reflect both fixed and variable costs, stimulate the adoption of innovative technology, fully recover capacity costs, and recognize that costs vary by time and season, as described in several chapters in this volume.

4. Facilitate the development and adoption of new uses of electricity, which displace fossil fuels, so as to recognize that electrification is the optimal path toward a low-carbon future. Facilitation must include enhancing R&D on electric end uses, incentive programs, and special tariffs.

5. Develop a full-service strategy to provide installation, operation, and maintenance of all electric technologies, including DERs, efficiency appliances, and other electrical devices. This includes enabling utility investment on customers’ premises for generation and storage assets.

Utilities should position themselves as the broker for all things electric in the customer’s eyes, “the great rebalancing” described in chapter by MacGill & Smith. The changes now underway will make the marketplace increasingly complex for energy consumers. Without the utility’s intervention, consumers will not be able to successfully deal with a number of actors in the marketplace (Gellings and Gudger, 1997). Collectively these service offerings would satisfy the needs originally identified by The Modern Grid Initiative (2007) (MGI). These also include:

• enabling active participation by consumers,

• facilitating participation in alternative service offerings and demand response programs,

• accommodating all generation and storage options,

• enabling new products and services,

• providing power quality for the digital economy, and

• optimizing asset utilization.

Theoretically these services could continue to be provided by the myriad of firms now in the marketplace, as well as others. However, for society to rely solely on some arbitrary organic growth will not insure that potential benefits of this revolution in technology will be fully realized. These needs are ones that could be provided by enabling electric utilities, in partnership with their regulators, to use existing arrangements to supply new and expanded desirable characteristics using the electric power system in its entirety from consumers to central and distributed resources. As alternative business models are considered, it is important to consider how these needs will be met in those arrangements and compare those potential arrangements to that which leverages today’s regulated business model.1

5. Rate of return regulation

Rate of return regulation has traditionally been used most often used by regulators to determine fair and reasonable prices for electricity. For the utility, fair and reasonable is intended to reflect the utility company’s ability to earn a reasonable return on costs incurred in providing electricity service and to avoid monopoly profits. For the customer, it is to restrict the profits the company can make, therefore protecting them from paying more than necessary. In the rate of return regulation, the regulator determines the appropriate amount for the company’s rate base, cost of capital, operating expenses, and depreciation (Jamison, 2005).

It uses these determinations to calculate how much revenue the utility needs to recover expenses. The rate of return regulation became popular during the development of the basic utility infrastructure we have today. It allowed for investors to comfortably provide capital to utilities to build power plants and power-delivery systems in exchange for guarantees against certain competition. For example, during the formation of the industry, this became evident in an arrangement, called the “regulatory compact” in which distribution utilities were franchised or allotted a geographic area in which they became the exclusive provider, provided they agreed to serve all consumers, referred to as an obligation to serve, in return for which they were guaranteed a “fair” rate of return.

There are several inherent advantages to the rate of return regulation. The first is that it is easily sustainable if there is limited competition because prices can easily be adjusted. Second, it provides more comfort to potential investors, as it constrains regulators from enabling too much volatility in price and therefore lowers risk and the cost of capital. In the rate of return regulation, investors can be confident that they have a fair opportunity to receive profit from their investments.

There are, however, four primary disadvantages of the rate of return regulation:

• It provides meager incentives for companies to operate optimally.

• The utility can easily succumb to encouragement to make unnecessary investments so as to inflate its allowed return.

• It requires frequent rate cases during times of high inflation.

• Without careful regulatory oversight, it provides and easy mechanism for companies to shift costs from competitive markets to noncompetitive markets. In short, the rate of return regulation continues to be useful in offsetting the power of natural monopoly. It is mostly applied to Investor-Owned Utilities (IOUs), where there is a divergence of basic interests between the customer wanting to pay little for electricity and investors wanting to earn a handsome return on the utility stocks and bonds it invests in.

Regulation as applied to public infrastructure in the United States first appeared in the case of railroads. During the 1800s railroads expanded, financed by investors eager to earn a premium return. Understandably their investments were targeted at the most profitable new routes, and prospective customers would be charged sometimes usurious rates. At first, railroads expanded in a rather haphazard fashion with inconsistent prices being charged for the same relative service. Both investors and politicians developed the realization that to best serve the public’s interest, regulation would be needed. Railroad regulation came forward in the 1880s, leading to formation of the National Association of Regulatory Utility Commissioners (NARUC), still active today, and well known for an association that supports regulators, which oversee electric utility regulation. Following the initial regulation of railroads, consumers and utilities themselves began to clamor for regulation of electric utilities.

The rate of return regulation of electric utilities resulted in oversight of prices for electricity and, in turn their capital expenditures, cost of capital, and operating expenditures. In that regard, they must justify and prioritize investments in the infrastructure for electric power generation, transmission, and distribution. To effectively judge the needs of consumers and to best measure utility performance, regulators measure reliability, customer service, power quality, environmental performance, and benchmark expenses as compared to others.

Admittedly, the rate of return regulation is an imperfect scheme, but it works and can easily be molded to accomplish what is needed for an evolving near-perfect power system.

6. Why we do not need to reinvent the wheel?

In considering the costs necessary to accommodate the needs of tomorrow’s power system, there will be expenditures, such as communications, information technology, controls, energy storage, and sensors, which may not be viewed purely as electricity related. However, over the history of the industry, allowed expenditures have often included those only remotely related to the provision of reliable and affordable electric service. Utilities have installed poles for community ball fields, constructed community parking lots, supplied free electricity to county fairs, repaired the electrical service entrance in the city hall building, strung Christmas lights on downtown streets, and performed many other gratuitous tasks, which were built into their expenses and paid for by average ratepayers.

The most substantial nontraditional expenditures are those related to Demand-Side Management (DSM). The most prevalent programs and activities considered to be DSM are: load control; thermal energy storage and dual-fuel heating; innovative rates; energy efficiency; demand response; and electrification (Demand-Side Management, 1984). In these programs and activities, distribution utilities often paid the majority share of expenses, with consumers paying little, if any. In considering future business models, it is not out of the question that this practice could be expanded to investments of communications, information technology, sensors, and the establishment of more complex energy-management systems.

The best DSM examples are energy efficiency and Demand Response. It is now common practice for most utilities to include energy efficiency–type DSM in their portfolios. These are often funded by ratepayer-based programs or other mechanisms to reduce energy consumption, over what it would have been without DSM. Upward trends in energy efficiency program expenditures signal downward pressure on electricity demand. The energy intensity of end uses will reduce further as a result of increased spending by electric utilities on DSM programs and activities. For example, utility spending in the United States and Canada on energy efficiency programs has risen to $9.9 billion in 2014 (Consortium for Energy Efficiency, 2016).

The US Energy Independence and Security Act of 2007 popularized the term Demand Response and generally defined it as including programs and activities that reduce peak demand by the use of dynamic pricing, advanced metering, and enabling technologies. The US Energy Information Administration estimates that over 9 million customers are enrolled in Demand Response Programs ( in 2014), yielding an actual peak demand savings of 12,700 MW. The US Federal Energy Regulatory Commission (FERC) has estimated that the potential for Demand Response is such, so as to reduce peak demand in 2019 by as much as 150 GW (NADRP, 2009).

The concepts of using the utility to fund programs that all utility customers my benefit from, albeit the benefits participants, nonparticipants, and ratepayers at large receive may differ, are very important in considering new business models. We managed to do this very effectively with DSM: why can’t we do it with DER and other service offerings?

As these changes evolve, the best societal option will increasingly be a truly dynamic power system. This approach enables resources and technologies to be deployed operationally to realize all potential benefits. It requires a robust and modern grid characterized by connectivity, rules enabling interconnection, and innovative rate structures that enhance the value of the power system to all consumers. DER, Demand Response, and DSM will be increasingly important in enabling a marriage between these various technologies and systems, so as to enhance the utilization of the power system and enable increased reliability and enhanced consumer choice, while maximizing the penetration of DERs, including PVs, energy storage and efficient buildings, appliances, and devices (Demand-Side Management, 1984).

The Solar Energy Industries Association (SEIA) recently reported that the United States solar market remains what they refer to as “on track” for a record-breaking year, with 1361 MW installed during the third quarter of 2015 and 4.1 GW installed during the first three quarters of 2015. Much of this is new solar power generation installed on residential buildings (www.seia.org). These installations are often funded by third parties and contracted for by consumers through a variety of purchase power agreements. The lowest cost and most effective power system can no longer be configured solely by combinations of central station power generation knitted to customers by power-delivery systems. Today and increasingly into the future, society’s needs for reliable, affordable, and sustainable electricity can best be met by an optimal combination of distributed generation, distributed energy storage, energy efficiency, and new uses of electricity integrated with central generation and bulk system storage.

A more recent report by GTM Research in collaboration with the SEIA reports that a new record was set with the installation of 4.1 GW at an average of 2 MW of solar PV installed per hour through the third quarter of 2016 (GTM Research and SEIA, 2016).

As these distributed solar installations proliferate, the value of DSM will evolve, as will the DSM market participants. DSM incentives targeted toward consumers to influence the pattern and amount of electricity usage will still be valuable, but will change in how they are offered.

7. How can we move forward?

One example, can be gleaned from Salt River Project (SRP), an electric utility in the Phoenix, Arizona area, faced with substantial increases in PV system adoption by its consumers, has modified how it compensates customers who produce excess energy. SRP’s current tariffs allow consumers with excess PV power generation to sell those kilowatt-hours to SRP at a flat rate, which does not vary by time of day. Rather than pay a flat rate, SRP’s plan encourages the use of emerging storage and control technologies so as to reduce the demand on its system during critical periods (www.srpnet.com).

Another example is the City of Austin, Texas. In the so called Pecan Street project, Pecan Street Inc., a research and development organization (www.pecanstreet.org) learned through experimentation that the kilowatt-hours generated from homes with west-facing solar panels were more valuable than those generated from homes with south-facing roofs. The energy generated from west-facing panels occurred later in the day when the sun’s arc was westward leaning generating energy that could displace more expensive central generation alternatives. In this example, as DSM evolves, incentives like those for solar energy will need to be tied to the time-varying benefit of load shape changes. If the displaced central generation is more expensive later in the day, then utilities can pay more for the replacement.

Likewise, if the displaced generation is less costly, then the utilities will pay less. As power systems evolve, so will the focus of DSM, but with the same overall objective of maximizing the benefits of electricity to consumers and society. Albeit neither of these examples is of IOUs, they each have their own forms of regulation; SRP has an oversight board and the City of Austin has the city council to deal with.

Any change that derives itself form expansion of distributed technologies can be resolved using the existing regulatory model. The key to enabling necessary changes is for regulators to allow utilities to make investments in DERs, including generation, storage, hyperefficiency tend uses, and the necessary controls and infrastructure to enable their integration with the grid. Fortunately, these concepts are under discussion. For example, in April 2016, Mike Florio, one of the commissioners at the California Public Utilities Commission (CPUC) floated the idea that—perhaps—utilities should be compensated for buying DERs from their customers (California Current, 2016). In its April 8, 2016 issue, California Current reported that: California’s IOUs could get a 3.5% return on power they buy from distributed resources if a proposal by Commission Florio goes forward (EEnergy Informer, 2016).

While many of the details of this proposed approach remain to be resolved, finding a regulatory fix to make DERs an attractive option to IOUs, just as investing in poles and wires currently are, would make sense in this context. A similar regulatory “fix” was conceived and implemented in California to make energy efficiency profitable for IOUs. Why not try the same for DERs?

Admittedly, it is a difficult concept to implement, requiring more regulatory intervention. However, as noted by Baak in his chapter, all indications are that California, at least, is de facto moving in this direction with complicated regulatory proceedings to encourage certain investments for certain cases to achieve the state’s broader desired goals and objectives. So one could argue that this is already happening.

New York, by contrast, appears to want to walk away from micromanaging DERs by drawing lines in who can do what and to whom, while letting the various stakeholders figure out the details further described in the book’s Introduction.

Here are a few examples of how this can be implemented:

• The installation of PV systems and energy storage on individual customer premises, commercial buildings, or as community solar projects can be handled as capacity expansion. Particularly when the externalities of environment and economic growth are considered. Schemes, such as net energy metering (NEM), would be adjudicated based on the value of the energy contributed. However, the capacity contribution would be considered as in the rate base and maintenance as an allowed operating expense.

• Subsidizing or funding the installation of hyperefficient and use technologies can be financed by electric utilities and considered as an investment to defer the need for generation or distribution capacity expansion.

• Funding the installation of electric vehicle–charging stations can be justified based on the societal benefits to all citizens.

• Funding research, development, and demonstration of DERs, demand-side management, and related technologies would be considered as allowed operating expenses and considered in the rate recovery process.

The danger may be that the IOUs may abuse their monopoly power if they are allowed to get into the DER business without adequate regulatory oversight. Moreover, the IOUs may also be tempted “gold plate” and “exaggerate” DER investments if proposals, such as those by Mike Florio previously mentioned, are in place. These problems are well known to regulators. The bottom line is that nothing is perfect and some form of regulatory oversight will most likely be required, regardless of which approach is implemented.

8. Is transactive energy the new model?

TE is a relatively new concept, increasingly popular in utility media stories, roughly described as a market of multiple dimensions wherein consumers, utilities, and providers of all types can transact with anyone in the energy marketplace. It is hard to separate discussions about TE from those about the Smart Grid, the Internet of Things-Electric (IOT-E). One popular definition is provided by the GridWise Architecture Council as: “A set of economic and control mechanisms that allows the dynamic balance of supply and demand across the entire electrical infrastructure using value as a key operational parameter” (GridWise Architecture Council, 2014). Advocates of TE have effectively pointed out that in order for TE to work Distribution System Operators (DSOs) will be needed. As observed by Masiello and Aguero: “The complexity, fun and necessity for a distribution system operator (DSO) arise from the need to coordinate DER operations to preserve and improve, not jeopardize, grid reliability” (Masiello and Romero Aguero, 2016). However, creating effective DSOs is likely more difficult than simply assuring that communications and control are overlaid on the power-delivery infrastructure. TE by itself does not mean a new business model, but will require a great deal of evolving regulatory oversight.2

Some of the more critical questions regarding TE have been raised by the CA PUC’s Policy and Planning Division, a few of which are listed below(paraphrased) here (Atamturk and Zafar, 2014):

• Is TE empowering consumers or complicating their lives?

• What pricing and services will TE develop?

• What is the cost and benefit of TE to consumers?

• Who should oversee the service providers?

• Can the TE systems and technologies be trusted?

In the spirit of an American folk wisdom saying: “If it ain’t broke, don’t fix it.”, the author examined some of the needs that the power system of the future will provide, as well as its opportunities, and compared them to the tentative promises of TE. Table 11.1 summarizes this comparison.

Table 11.1

Paticipation in the market will promote efficiency

Tomorrow’s needs

Rate of return regulation

TE

Enable active participation by consumers

It is unclear that the technology needed to truly allow customers to actively participate in the buying and selling of electricity exist now or will evolve without research funding encouraged by IOU investment in R&D. Once systems mature, the regulated entities will be able to implement the new systems more effectively

IT firms are anxious to move into this space, but their focus on profit may leave some important options aside, such as hyperefficient appliances and devices

Facilitate participation in alternative service offerings and demand response programs

Regulators will need to encourage utilities to offer more options; they are often reluctant to do so when left to their own devices

ISOs have successfully offered Demand Response programs in active wholesale markets. Mechanisms must be developed to allow more consumers to participate in a variety of offerings

Accommodate all generation and storage options

Rate of return regulation is the most effective means to force utilities to make these accommodations and to provide the needed cost recovery

In TE, these resources must compete with conventional sources, and without laws or regulations will receive limited penetration

Enable new products and services

Regulators must remove all barriers and become more tolerant of investments that may potentially fail and not penalize utilities for taking risks in trying new products and services

New product and service offerings are subject to the whims of investors. Fewer innovations may succeed in TE, but those that make it to the demonstration phase are more likely to be sustainable

Provide power quality for the digital economy

Price-differentiated offerings of varying levels of reliability can be easily supported in the Rate of Return Business model. Regulators need to encourage this kind of innovation

The open market will come forward with Power Quality solutions, as they do now. In TE, not as many consumers may be able to afford these options

Optimize asset utilization and operate efficiently

In a regulatory model, regulators can set up ways to measure the efficiency of utilities and reward them financially

The incentives to be efficient are successful participation in the market itself. This is highly dependent on what part of the power system(s) the market participant is focused on. With <3000 distribution utilities in the United States, the opportunities are limited as to where vendors can apply new products and services

Improve system reliability

This is the holy grail of power systems and is the subject of extensive oversight in the regulated model

Both purchase power and transmission services arrangements will need to be crafted to offer incentives and penalties for TE to assure that reliability targets are met. Also it is not clear who sets those targets

Reduce system losses

Requires active regulatory intervention, as the price of energy is sufficiently low, so as to mask losses

Difficult to see how TE can assure losses are reduced unless the opportunities are substantial

Operate resiliently against attack and natural disaster

Requires regulation at the Federal and State levels

Requires regulation at Federal and State level.

Implement DSM

An ongoing part of the regulatory process now that can easily be part of tomorrow’s power system

Will be left to the development of products and services and included as cost effectiveness is clear

Assure sustainability of the electricity system

Regulation at the State and Federal levels will be required to assure this is done most effectively

Regulation at the State and Federal levels will be required to assure this is done most effectively

Facilitate consumer access to information

Easily part of a regulatory model

Will be accommodated as part of open market promotional programs. May not be as effective in TE

Maintain high levels of safety

The hallmark of electrical workers. Likely to be continually reinforced in a regulatory model

Applies to all levels of electrical work by state and federal law. Likely not to be compromised in TE

Understandably many of the attributes of tomorrow’s power system can be met by the existing regulatory model. However, what remains unclear is what the cost and benefits of each model will be and how difficult the transitions may become.

9. Conclusions

Debating concepts like these will help develop viable options in determining the landscape for tomorrow’s power system. However, without orchestrating a careful transition from the existing financial arrangements that utilities enjoy, unleashing TE can place a great deal of risk on the ability to continue to support the existing power-delivery infrastructure.

Many of the proposed changes, some of which are described here and in number of other chapters in this volume, could conceivably be adopted and accomplished with the existing regulatory framework, enabling the existing electric distribution utility to become an “Uber Utility” of the future.

An Uber Utility would act as a one-stop shop for consumers, delivering a host of electric energy services they need. It would provide electric energy service along with service and installation of all related electric generation, storage, and energy-efficient devices. Such a utility would be allowed to include all of the assets that could provide overall support to the grid in their rate base. In return, it would retain an exclusive service territory in exchange for providing universal access to all at tariffs, which assure full cost recovery. As noted by Sioshansi in his chapter, the existing grid is a valuable asset already paid for by all. It will most likely remain indispensible to most consumers and most likely even more valuable to prosumers and prosumagers, who will continue to rely on it for reliability, voltage and frequency support, balancing, storage, and backup. For all these reasons, it is incumbent on the regulators to ensure that the integrated grid of the future is adequately funded and maintained by the widest population of possible consumers, prosumeers, and prosumagers, all of whom will continue to benefit from its many valuable services.