Access Rights and Consumer Protections in a Distributed Energy System

Abstract

Within Australia’s National Electricity Market (NEM), distributed technologies are delivering energy in ways that were not contemplated when regulations governing consumer rights and protections were developed. The adoption of technologies, such as rooftop solar, battery storage, electric vehicles, and virtual power plants will give rise to an increasingly heterogeneous mix of electricity customers who will expect their utilities to cater for their individual preferences. Over time, the types of grid services that are considered to be “essential” may evolve, leading to redefined and technology-neutral access rights for electricity infrastructure. Consumer protection frameworks will need to balance innovation and consumer choice with universal access to electricity supply.

Keywords

1. Introduction

2. Consumer market developments in the NEM

3. Outlook for distributed technologies in the NEM

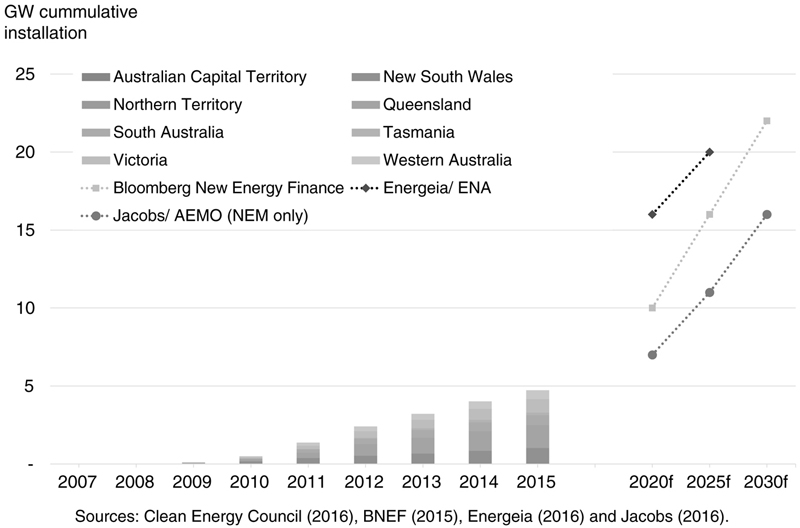

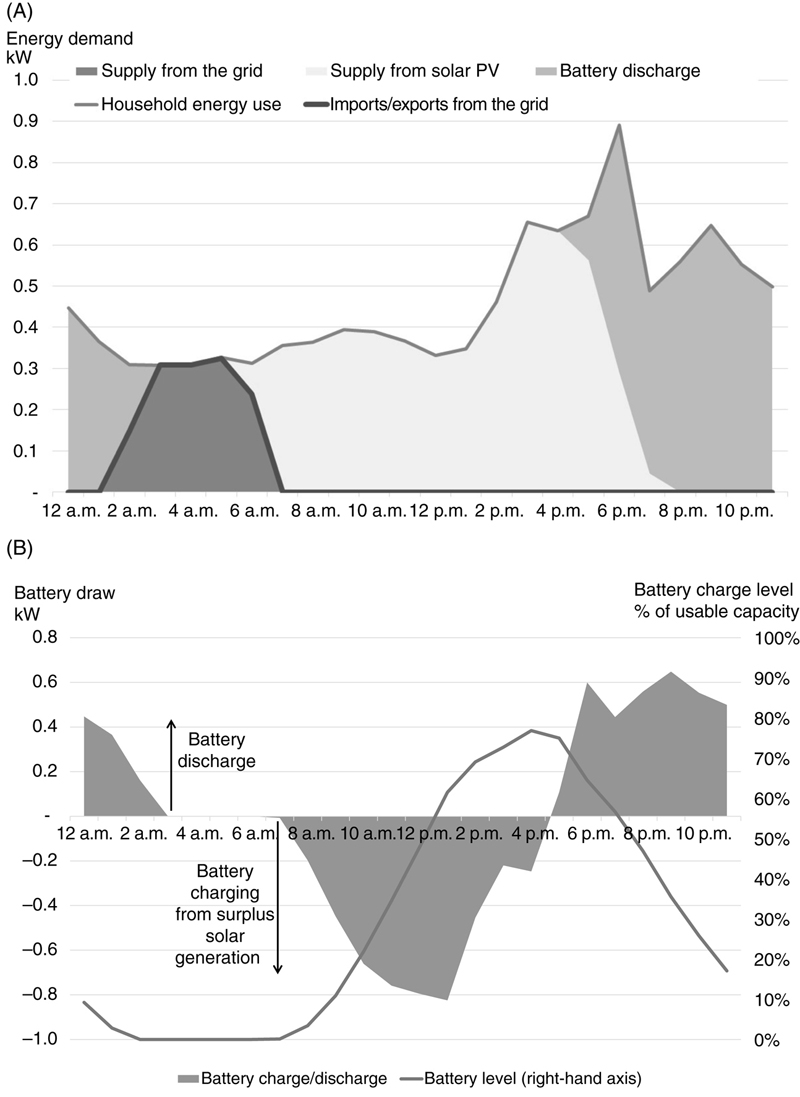

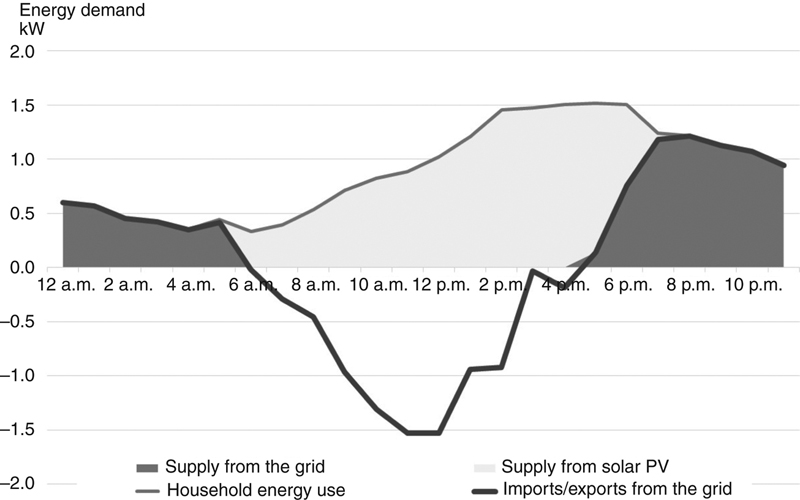

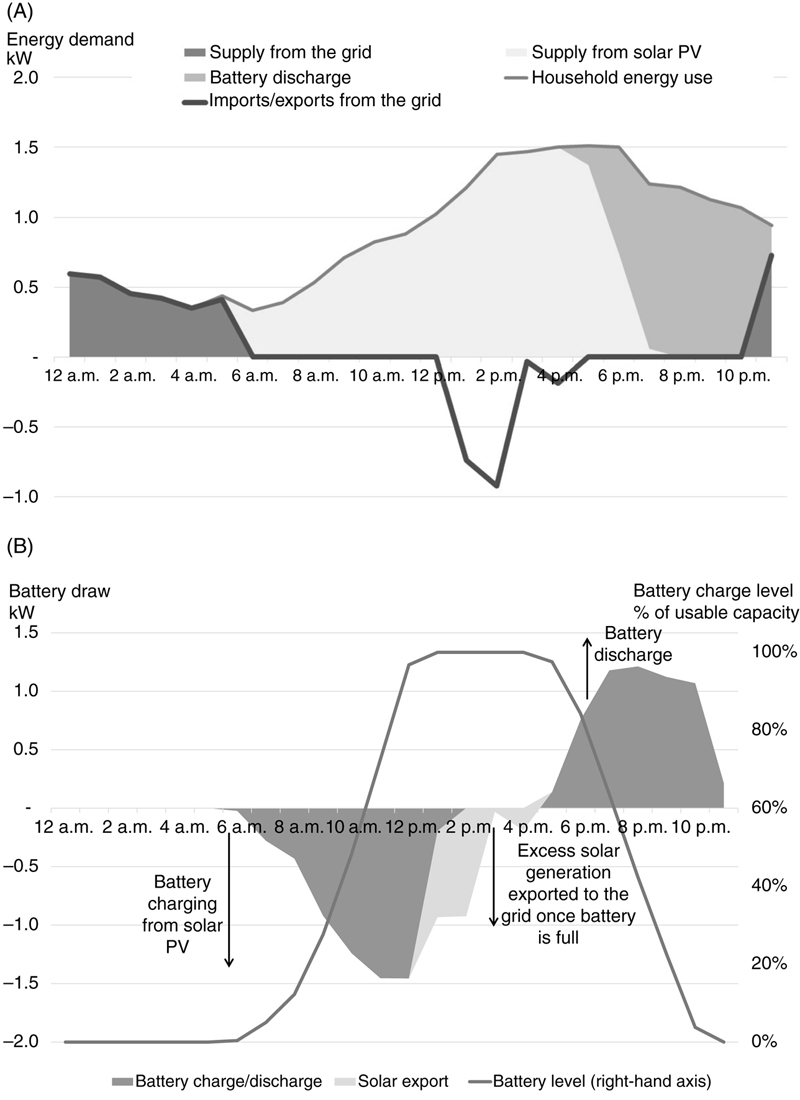

3.1. Solar PV

AEMO, Australian Energy Market Operator; ENA, Energy Networks Australia; NEM, National Electricity Market.

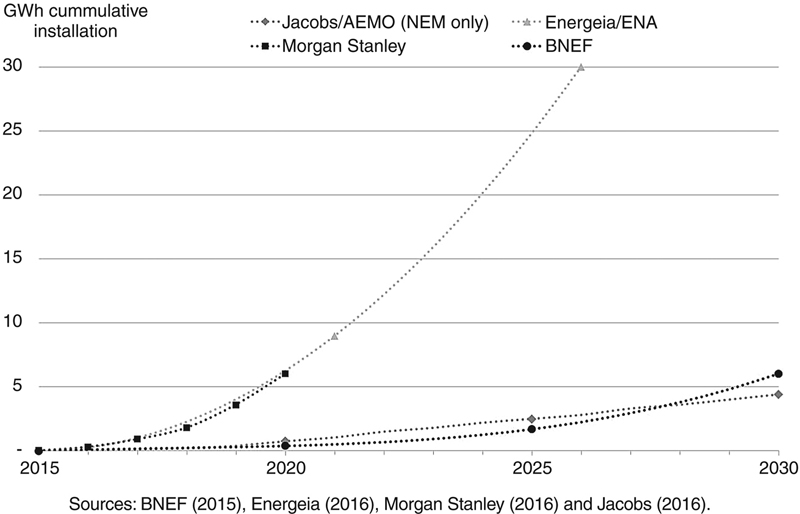

3.2. Energy Storage

Table 14.1

Cost-Reflective Network Tariffs From 2017

| Network business | Proposed tariff |

| Ergon | Opt-in Seasonal Time-of-Use Energy and Seasonal Time-of-Use Demand tariffs |

| Energex | Opt-in Demand tariff includes Hot Water Tariff for Demand customers |

| Ausgrid | Opt-in Time-of-Use tariffs. From July 1, 2018, all new customers assigned to Time-of-Use tariffs with opportunity to opt-out to a transitional tariff. All existing customers with digital metering to be assigned to this transitional tariff on July 1, 2018 |

| Essential | Time-of-Use tariff default for new customers, new solar PV installations and metering upgrades. Opt-in Demand-based tariffs also available |

| Endeavour | Opt-in Time-of-Use tariffs. All new customers with interval meters assigned to Time-of-Use tariffs from July 1, 2018 on an opt-out basis |

| ActewAGL | Time-of-Use tariff default for all new residential and small business customers. Small business customers can opt-in to Demand tariffs. Possible gradual introduction from December 1, 2017 of residential demand tariff |

| Citipower. Powercor, United Energy, Jemena, AusNet | Opt-in residential Demand Tariffs (not available in AusNet service area until 2018). Opt-in Demand tariffs for all small business customers consuming <60 MWh per annum. United and Jemena: Demand tariffs mandatory for small businesses consuming >60 MWh per annum. Powercor, CitiPower, and AusNet: transitional Demand tariff mandatory for small business consuming >60 MWh per annum. Cost reflectivity of the transitional tariff will increase between 2017 and 2022 |

| South Australia Power Networks | Opt-in cost-reflective residential Demand tariff. Opt-in “fully” cost-reflective demand tariff for small business customers. Mandatory assignment to transitional Demand tariff (50% cost reflective Demand) for new three-phase customers and progressive increases in cost-reflectivity until 2022 |

Source: Distribution network businesses tariff statements.

3.3. Electric Vehicles

3.4. Virtual Power Plants

4. Growing customer heterogeneity: impacts of technology adoption on household demand

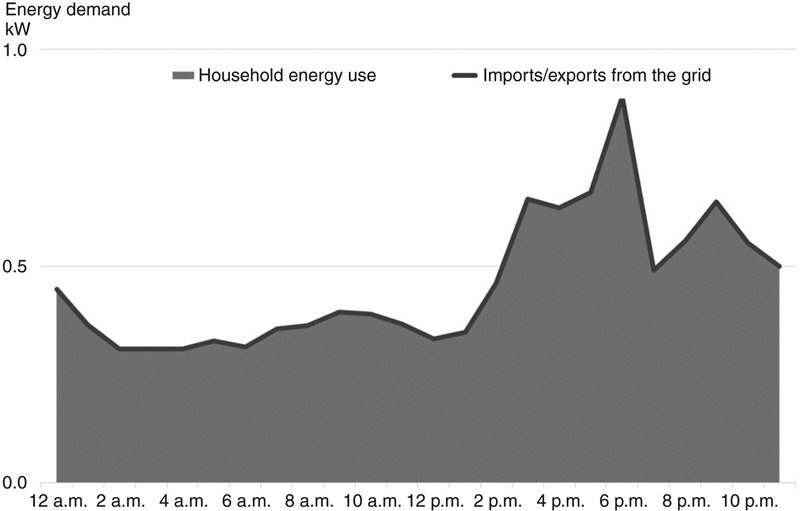

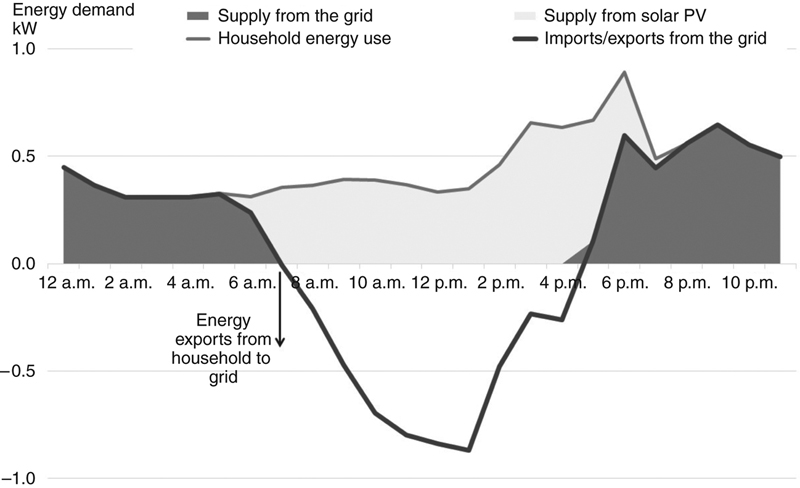

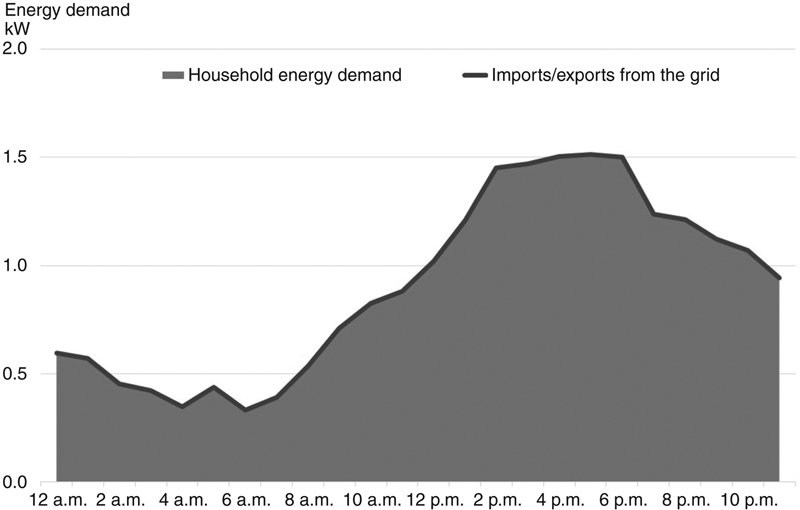

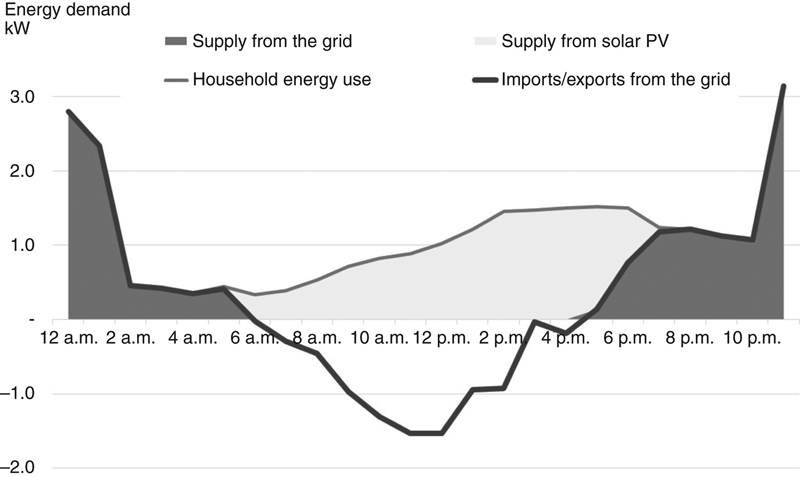

4.1. Typical Demand Days

4.2. Peak Demand Days

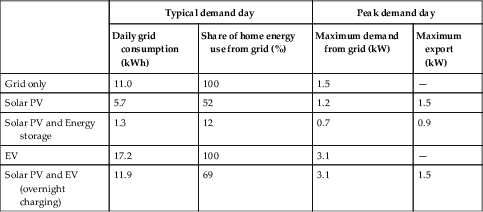

4.3. Divergent Customer Requirements

Table 14.2

Customer Requirements From the Grid Depend on Technology Choices

| Typical demand day | Peak demand day | |||

| Daily grid consumption (kWh) | Share of home energy use from grid (%) | Maximum demand from grid (kW) | Maximum export (kW) | |

| Grid only | 11.0 | 100 | 1.5 | — |

| Solar PV | 5.7 | 52 | 1.2 | 1.5 |

| Solar PV and Energy storage | 1.3 | 12 | 0.7 | 0.9 |

| EV | 17.2 | 100 | 3.1 | — |

| Solar PV and EV (overnight charging) | 11.9 | 69 | 3.1 | 1.5 |

EV, Electric vehicle.

5. Evolution of consumer rights and protections

5.1. Consumer Protections in a Distributed Energy Marketplace

Table 14.3

Consumer Protections for the Use of Solar Energy

| Product type | Description | Protection frameworka |

| Solar PV | Consumer-owned system, purchased outright | ACL |

| Solar PV financing plan | Consumer-owned system, purchased with or without an upfront deposit, and with monthly repayment obligations | ACL |

| Solar PPA | Third party–owned system installed at customer premises. Under the PPA, the customer buys solar power from the system provider for an agreed period of time, for example, 10 years | ACL and retail license exemptions framework |

| Solar leasing | Third party–owned system installed at customer premises. The customer pays a monthly fee to lease the system for an agreed period of time, for example, 10 years | ACL |

| GreenPower | Purchase of remotely generated renewable energy from a licensed energy retailer via the energy grid | ACL and NECF or equivalent jurisdictional framework |

ACL, Australian Consumer Law; NECF, National Energy Consumer Framework; PPA, power purchase agreements.

a If products involve loans or product leasing, the National Consumer Credit Protection Act also applies.

5.2. Technology Connections and Access Rights

6. Conclusions

The challenge Australia’s energy market now faces is that effective competition, innovation and market efficiency require informed customer participation, but evidence shows that consumers don’t trust, and are not engaged in the energy market. Moreover, people don’t make the decisions expected of them, almost always preferring the status quo and feeling that choices in the energy market are too confusing, too much ‘hassle’ or not genuine as the products are all the same.