The Great Rebalancing: Rattling the Electricity Value Chain from Behind the Meter

Abstract

This chapter aims to redress traditional conceptions of the electricity value chain which have focused heavily on costs on the grid side of the meter. DER is now driving a great rebalancing, rattling the value chain and refocusing the sector on costs and benefits behind the meter. Most assets are behind the meter and the consumer surplus from energy services is almost certainly the largest segment of the value chain. This raises questions about the relevance of the meter as the key dividing line in the industry value chain. The chapter then considers the implications of this great rebalancing for cost reflective pricing and regulation.

Keywords

1. Introduction

2. Greater comfort and convenience

The position of utilities as regulated monopolies is assuredly more of an advantage than a disadvantage for the conservative investor. Under law they are entitled to charge rates sufficiently remunerative to attract the capital they need for their continuous expansion, and this implies adequate offsets for inflated costs. While the process of regulation has often been cumbersome and perhaps dilatory, it has not prevented utilities from earning a fair return on their rising invested capital over many decades.7

Our confidence is justified both by our past experience and by the knowledge that society will forever need huge investments in both transportation and energy. It is in the self-interest of governments to treat capital providers in a manner that will ensure the continued flow of funds to essential projects. It is concomitantly in our self-interest to conduct our operations in a way that earns the approval of our regulators and the people they represent.

In its electric utility business, our Berkshire Hathaway Energy (“BHE”) operates within a changing economic model. Historically, the survival of a local electric company did not depend on its efficiency. In fact, a “sloppy” operation could do just fine financially. That’s because utilities were usually the sole supplier of a needed product and were allowed to price at a level that gave them a prescribed return upon the capital they employed. The joke in the industry was that a utility was the only business that would automatically earn more money by redecorating the boss’s office. And some CEOs ran things accordingly. That’s all changing……. tax credits, or other government-mandated help for renewables, may eventually erode the economics of the incumbent utility, particularly if it is a high-cost operator. BHE’s long-established emphasis on efficiency—even when the company didn’t need it to attain authorized earnings—leaves us particularly competitive in today’s market (and, more important, in tomorrow’s as well).8

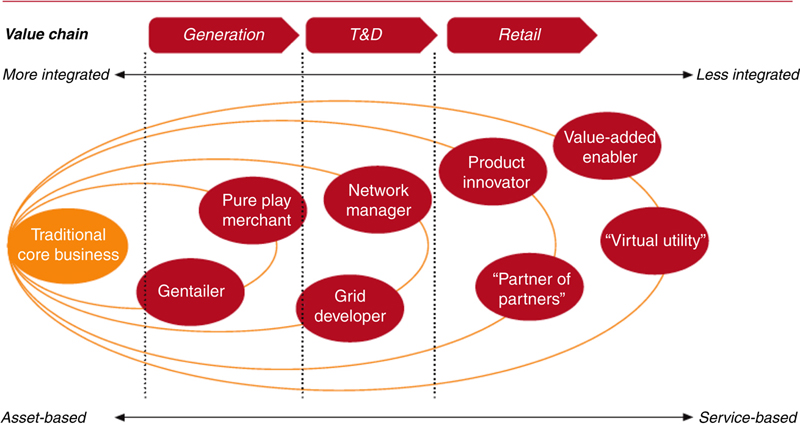

3. New visions of the value chain: rhetoric, reality, regulation, and the REV

the traditional provider’s role has evolved to a platform service that enables a multi-sided market in which buyers and sellers interact. The platform collects a fee for this critical market-making service, while the bulk of the capital risk is undertaken by third parties.15

3.1. Complicated or Complex?

4. The tariff cost stack, the mystery beyond the meter and the full electricity value chain

Table 3.1

The Electricity Tariff Cost Stack, Australian Grid Asset Values 2015

| $ Billion | |

| Powerlink | 6.6 |

| TransGrid | 5.8 |

| AusNet | 2.5 |

| ElectraNet | 2.0 |

| TasNetworks | 1.2 |

| NEM Transmission | 18.2 |

| Energex | 10.9 |

| Ergon Energy | 9.0 |

| Ausgrid | 14.6 |

| Endeavour | 5.7 |

| Essential | 6.9 |

| ActewAGL | 0.8 |

| Powercor | 3.1 |

| AusNet Services | 3.2 |

| United Energy | 1.9 |

| CitiPower | 1.7 |

| Jemena | 1.1 |

| SA Power Networks | 3.6 |

| TasNetworks | 1.5 |

| NEM Distribution | 64.1 |

| Western Power | 10.0 |

| Total | 74.1 |

Source: www.aer.gov.au

4.1. Customer Assets Beyond the Meter

Table 3.2

Australian Household Expenditures (Australian Bureau of Statistics, 2011)

| Household expenditure on goods and services $ per week 2009-10 | ||||||

| Lowest | Second | Third | Fourth | Highest | All households | |

| Electricity (selected dwelling) | 16.83 | 21.00 | 23.28 | 27.45 | 32.60 | 24.23 |

| Whitegoods and other electrical appliances (excluding stoves and related) | 5.47 | 10.14 | 9.53 | 10.47 | 15.64 | 10.25 |

| Cooking stoves, ovens, microwaves, hot plates and ranges | 0.98 | *1.68 | 1.69 | *3.45 | 5.17 | 2.60 |

| Audio-visual equipment and parts | 7.28 | 10.74 | 12.29 | 18.08 | 23.46 | 14.37 |

| Home computer equipment (including pre-packaged software) | 1.58 | 5.15 | 7.87 | 9.21 | 13.16 | 7.39 |

| Blank and pre-recorded media (excluding pre-packaged computer software) | 2.31 | 4.33 | 6.09 | 9.54 | 13.42 | 7.14 |

| Appliances (selected & media) | 17.62 | 32.04 | 37.47 | 50.75 | 70.85 | 41.75 |

| Appliance spendi as a % of Electricity spend | 105% | 153% | 161% | 185% | 217% | 172% |

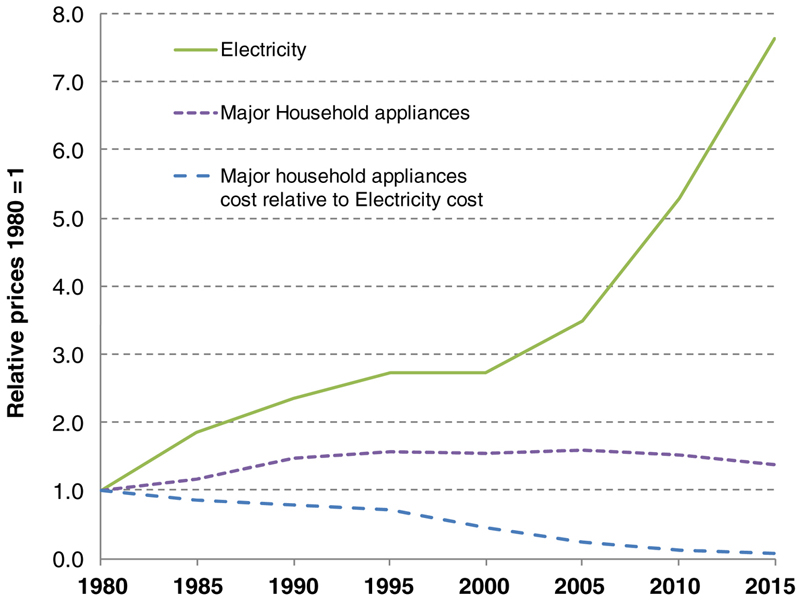

The latest 2015–16 survey is completed but unpublished however air conditioning, smartphone, and mobile computing usage has increased along with rooftop PV. Simultaneously there had been a bubble in distribution and transmission asset spending in Australia, as well as renewable generation and closures of fossil fuel plants.

(Australian Bureau of Statistics, 2016).

Prices are shown at 5-year intervals. Customer anger over electricity price rises has flowed from both historic expectation of real price deflation and “just price” concepts, which date back to St. Thomas Aquinas.

Table 3.3

IBIS World Revenue Estimates, 2016–17 ($ Billion)

| Selected Wholesaling | $B |

| Telecommunications and Other Electrical Goods | 30 |

| Computer and Computer Peripheral | 18 |

| Household Appliance | 8 |

| Electrical Wholesale | 56 |

| Selected Retail and services | |

| Electrical Services | 19 |

| Domestic Appliance Retailing | 14 |

| Air Conditioning and Heating Services | 7 |

| Computer and Software Retailing | 6 |

| Electrical and Lighting Stores | 2 |

| Insulation Services | 1 |

| Elevator Installation and Maintenance | 1 |

| Domestic Appliance Repair and Maintenance | 1 |

| 51 | |

| Electricity Grid | |

| Fossil Fuel Electricity Generation | 14 |

| Hydro generation | 2 |

| Wind and Other Electricity Generation | 2 |

| Electricity Transmission | 3 |

| Electricity Distribution | 17 |

| Generation transmission and distribution | 38 |

| Electricity Retailing | 46 |

Source: https://www.ibisworld.com.au/

Table 3.4

Australian System of National Accounts Information Technology Net Capital Stock, Selected Items by Industry

| $ Billions | ||||

| Computers and peripherals | Electrical and electronic equipment | Computer software | Total | |

| Electricity, gas, water and waste services | 1.4 | 15.1 | 2.6 | 19.1 |

| Information media and telecommunications | 0.7 | 9.7 | 4.0 | 14.5 |

| Financial and insurance services | 3.0 | 1.6 | 9.2 | 13.8 |

| Public administration and safety | 2.8 | 1.8 | 5.4 | 10.0 |

| Transport, postal and warehousing | 0.8 | 3.3 | 4.6 | 8.7 |

| Professional, scientific and technical services | 1.6 | 0.9 | 5.4 | 7.9 |

| Rental, hiring and real estate services | 2.3 | 4.0 | 1.1 | 7.4 |

| Retail trade | 1.3 | 2.6 | 2.7 | 6.7 |

| Wholesale trade | 1.1 | 2.6 | 2.7 | 6.4 |

| Manufacturing | 1.0 | 1.9 | 3.3 | 6.2 |

| Health care and social assistance | 1.0 | 2.1 | 2.3 | 5.4 |

| Construction | 1.1 | 2.8 | 1.2 | 5.1 |

| Education and training | 1.0 | 1.0 | 3.0 | 5.0 |

| Arts and recreation services | 0.4 | 2.2 | 1.0 | 3.6 |

| Mining | 0.2 | 1.6 | 1.7 | 3.5 |

| Accommodation and food services | 0.3 | 2.4 | 0.3 | 3.0 |

| Other services | 0.3 | 2.1 | 0.5 | 2.9 |

| Administrative and support services | 0.6 | 0.3 | 1.6 | 2.5 |

| Agriculture, forestry and fishing | 0.2 | 1.5 | 0.4 | 2.0 |

| Total | 21.0 | 59.6 | 52.9 | 133.4 |

| Total nonutility | 19.6 | 44.4 | 50.3 | 114.3 |

5. The DER dilemma for the true electricity value chain